NFRA’s Call for a Two-Way Communication: A New Requirement or a Gentle Reminder?

Tagging auditors and TCWG to make amends

– Team Corplaw | corplaw@vinodkothari.com

Introduction

NFRA moved the needle, and it is to be seen if the ocean starts boiling.! A 7th Jan 2026 circular from NFRA, addressed to listed entities and their auditors, seemed like an attention-drawer to standards of auditing which are already there, and yet, the auditing fraternity is holding meetings with boards and senior management of listed entities, to comply with what was always a compliance requirement. Does the 7th Jan circular bring up any new boxes to be ticked, any new procedures to be laid or responsibilities to be reiterated? As we detail out in this article, there may be need for action on several fronts on the part of listed entities – identification of nodal persons, listing developments that need to be communicated, constituting team for responding to the findings of the auditors in course of their audit other than those that sit in the audit report, formation of sub-groups of TCWG, etc.

Read more →Representation to SEBI for RPT provisions of LODR

– Team Corplaw | corplaw@vinodkothari.com

The NBFC that doesn’t have to be: CICs and Principal Business paradox

– Dayita Kanodia, Assistant Manager | finserv@vinodkothari.com

Holding Companies whose primary intent is to invest in their group companies have lately faced a paradox with respect to the requirement of registration as a Core Investment Company (CIC).

CICs are entities whose principal activity is the acquisition and holding of investments in group companies, rather than engaging in external investments or lending exposure outside the group. Para 3 of the Reserve Bank of India (Core Investment Companies) Directions, 2025 (‘CIC Directions’) prescribes the quantitative thresholds for classification of an NBFC as a CIC. In terms thereof, an NBFC that holds not less than 90% of its net assets in the form of investments in group companies, of which at least 60% is in equity instruments, is classified as a CIC and is required to obtain registration from the RBI, unless exempted.

Conceptually, a CIC is a sub-category of a Non-Banking Financial Company (NBFC) (para 3 of the CIC Directions), just like Housing Finance Companies, Micro Finance Institutions, etc. The threshold criteria that NBFCs are required to satisfy is the principal business criteria (PBC), pursuant to which at least 50% of the total assets of the entity must consist of financial assets and at least 50% of its total income must be derived from such financial assets.

The PBC has historically served as the foundational threshold for determining whether an entity is an NBFC. Once the entity satisfies this principal requirement of carrying out financial activity, the sub-category is to be determined based on its line of business, which, lately, has seen quite a varietty – fron tradtional variants such as investment and lending activities (ICC), to housing finance (HFC), to financing of receivables (Factoring companies), the more recent inclusions are account aggregators (AA), mortgage guarantee companies (MGCs), infrastructure finance compaies (IFC), etc. Each of these NBFCs first, and then they fall in their respective class. For instance, HFCs are a type of NBFCs that primarily focus on extending housing loans and hence, must have a minimum housing loan portfolio of 60% and an individual housing loan of 50%.

Accordingly, all categories of NBFCs must first be ascertained to be carrying out financial activities as their primary business, and thereafter, the specific product helps to determine the category. Consequently, holding companies or CICs should ideally also adhere to the 50-50 criteria first and thereafter meet the 90-60 criteria for CIC classification.

However, there is a common perception among the market participants that CICs, irrespective of meeting such PBC, in case they reach the 90-60 criteria, will be required to obtain registration as a CIC. Several news reports also note this perception.

This perception among the market participants that CICs are not required to adhere to the PBC criteria stems from para 17(3) of the CIC Directions, which explicitly provides that:

“CICs need not meet the principal business criteria for NBFCs as specified under paragraph 38 of the Reserve Bank of India (Non-Banking Financial Companies – Registration, Exemptions and Framework for Scale Based Regulation) Directions.”

It may be noted that the above-quoted provision, which has recently been made a part of the CIC Directions pursuant to the November 28 consolidation exercise, was earlier included in the FAQs released by RBI on CICs. FAQs are RBI staff views; whereas Directions or Regulations are a part of subordinate law; however, in the consolidation exercise, a whole lot of FAQs and circulars became a part of the Directions.

Going by the intent of the NBFC classification and categorisation, the above-quoted provisions seem more relevant for registered CICs, implying that CICs once registered need not meet the PBC on an ongoing basis. CICs predominantly hold investments in group companies and therefore satisfy the 90–60 thresholds, but often do not derive any financial income from such investments. Group investments, being strategic in nature, are rarely disposed of, and the dividend income from such investments depends on the dividend/payout ratio, which may be quite low. In several cases, such entities continue to earn income, say, by way of royalty for a group brand name. Even the slightest of non-financial income will seem to breach the PBC criteria, which may challenge the continuation of registration of the CIC as an NBFC. In order to redress this, the provision under para 17(3) of the CIC Directions provides that CICs need not meet the PBC criteria on an ongoing basis.

What is the basis of this argument? The definition of a CIC comes from para 3, which says as follows: “These directions shall be applicable to every Core Investment Company (hereinafter collectively referred to as ‘CICs’ and individually as a ‘CIC’), that is to say, a non-banking financial company carrying on the business of acquisition of shares and securities, and which satisfies the following conditions.” Para 17 (3) is a note to Para 17, which apparently deals with conditions of continued registration.

Given that CIC is a category of NBFC, it would be counter-intuitive to say that the regulatory requirement requires holding companies to go for registration as a CIC even if they do not meet the PBC for an NBFC. In fact, if an entity is not an NBFC because it fails the principality of its business, it would not even come under the statutory ambit of the RBI by virtue of section 45-IC.

Accordingly, without going by just the text of the regulations, in our view, considering the regulatory intent, the following could be inferred:

- If there are group holding companies which have intra group investments, but also have operating income from one or more sources, such that the operating income is more than finanical income, these companies are not NBFCs at all. If they are not NBFCs, they cannot be CICs irrespctive of the extent of investment/loans as a part of their asset base. As we say this, we emphaise that the operating income shoudl be substantive and should be indicating a strategic business intent, rather than a pure one-off or passive income.

- CICs are a type of NBFC.

- Holding companies will be classified as a CIC in case they first meet the 50-50 criteria for NBFC and thereafter the 90-60 criteria as well. The registration requirement may then be ascertained based on the asset size and access to public funds by the CIC.

- A CIC (registered or unregistered) need not meet the PBC criteria on an ongoing basis.

Other Resources:

Unified Investment Limits and Enhanced Exit Flexibility for FPIs

Manisha Ghosh, Senior Executive | finserv@vinodkothari.com

Investment limits under Voluntary retention route (Rs. 2,50,000 crore) for investment in corporate bonds and G-secs have been merged and made a part of the limit assigned for regular investments by FPIs under General Route (15%, 2% and 6% of outstanding stock of Corporate debt securities, State Government securities and Central Government respectively); as a result, FPIs that commit to keep funds for at least 3 years may escape the restrictions applicable in case of corporate bonds relating to minimum residual maturity requirement and issue-wise limits on single FPI (not exceeding 50% of any issue). This introduces significant scope for those FPIs that are sure of staying invested in India for a long term, avoiding opportunism while granting them significant operational flexibility.

The Indian market has witnessed a sharp and sustained decline in FPI investments over the past few years, reflecting a clear shift toward net outflows. The data reflects a structural decline in FPI investments over the period, transitioning from strong inflows in 2020 to persistent net withdrawals from 2022 onwards. The brief stabilization in 2024 appears temporary rather than a trend reversal, suggesting continued caution or reallocation by FPIs in recent financial years.

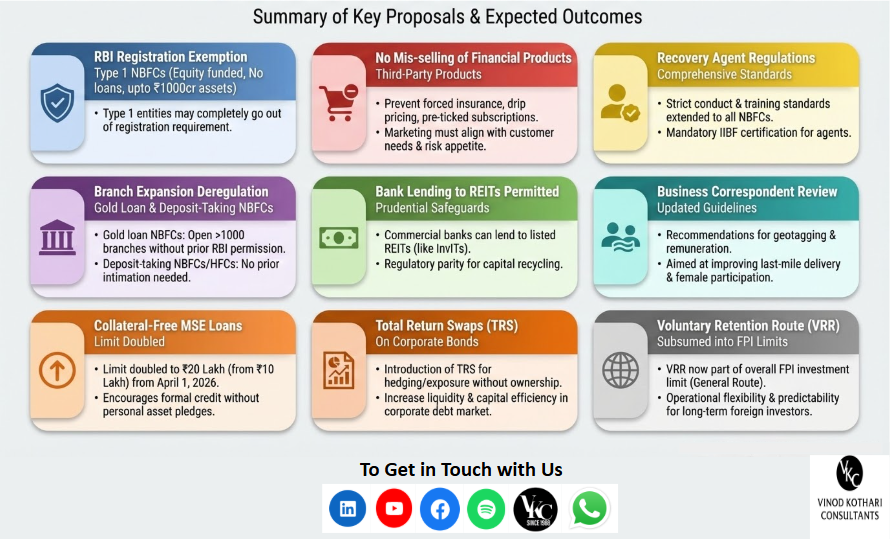

Regulator’s February Bonanza: RBI’s Sweet Surprises for NBFCs

Team Finserv | finserv@vinodkothari.com

The Budget 2026 may not have brought any significant regulatory amendments or reliefs for the financial sector entities, however, the regulator has proposed a box full of surprises for the regulated entities. The Statement on Developmental and Regulatory Policies dated February 6, 2026 has proposed various significant changes. The measures span a wide spectrum, from exempting Type 1 NBFCs (with no public funds and no customer interface) from registration, to stricter norms on sale of third-party products, a harmonised recovery agent framework, permission for bank lending to REITs and an increase of collateral-free loan limits for MSMEs, among others. While the detailed guidelines for each of the proposals are yet to be issued, we provide a quick snapshot and implications of these proposals.

1. Exemption from RBI registration for Type 1 NBFCs upto Rs 1000 crores in assets

After several years of regulatory supervision over investment companies and small size NBFCs, the RBI has proposed to exempt NBFCs having no public funds and customer interface, with asset size not exceeding ₹1000 crore, from the requirement of registration. This will bring such NBFCs, which are commonly referred to as Type 1 NBFCs, outside the purview of RBI supervision, compliance and reporting requirements.

Earlier, access to public funds and customer interface were factors for applicability of several regulations, but not for complete exemption.

What is Customer Interface[1]

Para 6(4) of under the RBI (NBFCs – Registration, Exemptions and Framework for Scale Based Regulation) Directions, 2025 (“RBI Master Directions”) defines customer interface as “interaction between the NBFC and its customers while carrying on its business”

In essence, customer interface exists where an NBFC directly deals with customers in the course of its business, such as sourcing borrowers, communicating loan terms, collecting repayments, or addressing grievances. The concept focuses on direct dealing/direct public engagement between the NBFC and its customers in the conduct of its business.

Entities engaged in capital market transactions such as trading in shares, investments etc are not seen as having customer interface.

As to whether lending intragroup results in customer interface, the question is contentious – see our article here. .

Currently, NBFCs that do not have any customer interface are exempt from the fair lending practice norms, KYC norms, CIC reporting requirements are such other customer centric compliances.

What is “Public Funds”

Public funds is defined under RBI Master Directions as “includes funds raised either directly or indirectly through public deposits, inter-corporate deposits, bank finance and all funds received from outside sources such as funds raised by issue of Commercial Papers, debentures etc. but excludes funds raised by issue of instruments compulsorily convertible into equity shares within a period not exceeding five years from the date of issue.”

The expression public funds is much wider than public deposits; public deposits are only one part of it. Public funds broadly mean all funds raised by an NBFC from sources other than its own or self-funds. The definition is inclusive and covers multiple forms of debt funding, while also leaving room for other similar sources. Importantly, public funds are to be understood in contrast with self-funds, such as equity capital, which represent ownership and not fundraising. Funds raised from group entities are generally not regarded as public funds; however, if a group entity merely acts as a conduit for funds raised from the outside sources, such funds will still carry the character of public funds due to the direct and clear nexus with the public source.

The use of public funds is a key trigger for prudential regulation, as the RBI seeks to ensure safety and stability where public money is involved. In the absence of access to public funds, NBFCs are exempted from complying with prudential regulations, liquidity risk management framework and LCR norms.

Why Customer Interface and Public Funds Are Important

The RBI uses customer interface and public funds as risk filters to determine the extent of regulatory oversight required for an NBFC. Entities that neither deal with external customers nor raise public funds are considered to pose minimal consumer and systemic risk.

In line with this risk-based approach, the RBI has proposed to exempt NBFCs with no customer interface and no public funds, and with asset size not exceeding ₹1,000 crore, from the requirement of registration.

2. No mis-selling of third party Financial Products

Banks and NBFCs routinely distribute third-party products alongside extending their core financial services. Such distribution is undertaken both through physical branches and through digital lending applications and platforms. It has, however, been frequently observed that certain banks and NBFCs take undue advantage of borrowers by using deceptive practices and dark patterns to sell third party products.

Dark patterns are tricky user interfaces “that benefit an online service by leading users into making decisions they might not otherwise make. Some dark patterns deceive users while others covertly manipulate or coerce them into choices that are not in their best interests[2]. Hence, there comes a need to regulate the same. The Central Consumer Protection Authority (“CCPA”), issued the Guidelines for Prevention and Regulation of Dark Patterns, 2023 to regulate such practices.

Digital lenders themselves may quite often be employing practices such as:

- Drip pricing: elements of pricing which are not disclosed.

- BNPL offerings: Please make it clear that after the so-called free credit period, if you choose to convert the purchase into financing, the same will start incurring interest. Give the offer to pay and avoid interest.

- Adding subscriptions, donations or other discretionary items with EMIs or borrower payouts, if they are pre-ticked

- Repeated and persistent messages or calls to avail credit facility Reduced ROI for a limited period to create false demand

- Not opting for insurance in case of asset finance is shown as shaming the borrower of agreeing to keep the asset unsecured

- Pressuring the borrower to share personal information like Aadhaar or credit card details, even when the information is not mandatory

- Hiding the cancellation option to opt out of the loan/ close the loan during the cooling off period

Accordingly, there is a felt need to ensure that third party products and services that are being sold at the bank counters or lending platforms are suitable to customer needs and are commensurate with the risk appetite of individual clients. It has therefore been decided to issue comprehensive instructions to REs on advertising, marketing and sales of financial products and services. The draft instructions in this regard shall be issued shortly for public consultation.

3. Proposed comprehensive regulation for Recovery Agents

RBI has, from time to time, reminded lenders that they shall remain fully responsible for activities outsourced by them and, accordingly, are accountable for the conduct of their service providers, including recovery agents. In particular, the regulator has emphasised that lenders must ensure that neither they nor their agents engage in any form of intimidation or harassment, whether verbal or physical, during debt recovery.

While detailed guidelines governing the conduct of recovery agents are prescribed for HFCs, similar comprehensive guidelines are currently not specifically extended to NBFCs. RBI has now proposed that it will harmonise all the extant conduct-related instructions on engagement of recovery agents and other aspects related to the recovery of loans for all regulated entities.

An important requirement for recovery agents was with respect to the training of recovery agents. The recovery agents engaged by HFCs are required to undergo the training as prescribed by Indian Institute of Banking and Finance (IIBF) and obtain the certificate from the institute. If such training and certification requirements for recovery agents are extended to NBFCs, it will increase compliance and operational costs due to training expenses, certification fees, and time invested in upskilling agents. NBFCs may also need to strengthen their internal processes for onboarding, monitoring, and periodic re-certification of recovery agents. However, while this may raise short-term costs, it is likely to improve the quality of recoveries, reduce customer complaints and conduct risk, and strengthen long-term operational discipline.

4. Deregulated branch expansion

As per the RBI Branch Authorisation Directions, NBFC-ICCs engaged in the business of lending against gold collateral are required to obtain prior approval of the RBI to open branches exceeding 1,000. Further, deposit-taking NBFCs and HFCs are required to inform the RBI and NHB, respectively, before opening any branch.

RBI has proposed to dispense with the requirement of prior approval or intimation for opening branches by such NBFCs. The change is likely to reduce hurdles in opening new branches for gold loan NBFCs, allowing them to expand more quickly and grow their operations.

| Type of NBFC | Erstwhile Requirement | Proposed Requirement |

| Deposit Taking NBFCs | Prior Intimation for the opening of branches | No need for prior intimation |

| HFCs | Prior Intimation to NHB before opening any branch | No need for prior intimation |

| NBFC-ICC (involved in gold lending) | Prior approval is required for branches exceeding 1000 | No need for prior approval |

The draft amendment directions have been issued here.

5. Bank Lending to REITs permitted

Banks were originally not permitted to lend to either InvITs or REITs, as these vehicles were created to refinance banks’ exposures in completed projects using market-based investor funds. While bank lending to InvITs was later allowed, subject to a prudential framework prescribed by the RBI. Banks must have a Board-approved policy governing InvIT exposures, covering appraisal, sanctioning, internal limits, and monitoring.

Prior to lending, banks are required to assess critical parameters including sufficiency of cash flows at the InvIT level, ensure that the combined leverage of the InvIT and its underlying SPVs remains within approved limits, and continuously monitor SPV performance, as the InvIT’s repayment capacity depends on these SPVs; banks must also consider the legal aspects of lending to trust structures, particularly enforcement of security. Lending is permitted only where none of the underlying SPVs with existing bank loans is facing financial difficulty, and any bank finance used by InvITs to acquire equity in other entities must comply with existing RBI restrictions.Lending to REITs, however, continued to be prohibited.

Regulatory Cap on Bank Investment in REITs/InvITs:

- A bank shall not invest more than 10% of the unit capital of any single REIT or InvIT.

- Such investment shall be within the overall ceiling of 20% of the bank’s net worth applicable to all direct investments in shares, convertible bonds/debentures, units of equity-oriented mutual funds, and exposures to AIFs.

In view of the strong regulatory, disclosure, and governance framework applicable to listed REITs, it is now proposed to permit commercial banks to lend to REITs, subject to appropriate prudential safeguards. At the same time, the existing lending framework for InvITs will be harmonised with the safeguards proposed for REITs to ensure consistency and parity across both structures.

The proposal allows banks to lend to REITs within a well-defined risk framework, ensuring financial stability is not compromised. The proposal brings regulatory consistency between REITs and InvITs, creating a more uniform and predictable regime. At the same time, it enables efficient recycling of capital from completed real estate and infrastructure projects, supporting new lending without adding significant systemic risk.

- Review of the Business Correspondent Guidelines

A Business Correspondent (‘BC’) acts as an extension of a bank itself, to provide banking related services in areas which do not have access to such services. The intent of the BC model is financial inclusion, in order to connect everyone to the banking system. The scope includes among other things, creating awareness about savings and other products and education and advice on managing money and debt counselling, processing and submission of applications to banks, etc.

The activities to be undertaken by the BCs would be within the normal course of the bank’s banking business, but conducted through the BCs at places other than the bank premises/ATMs. Thus, the scope would not just be limited to marketing, sourcing and distribution of financial products, rather, it would be extended to provide banking services to the customers from the place of business of the BC.

Business Correspondents have been functioning as critical enablers of last mile access to financial services, particularly in respect of underserved, rural, and remote locations. Presently, BCs are regulated through RBI (Commercial Banks – Branch Authorisation) Directions, 2025. The Directions outline the eligibility criteria, due diligence requirements, oversight and monitoring, scope of activities, etc for engaging a Business Correspondent by banks.

RBI had set up a committee, consisting of officials from RBI , Department of Financial Service, Indian Banking Association and NABARD, to comprehensively examine their operations and make suitable recommendations for enhancing their efficiency. Discussions were held on action points of the previous meeting, Geotagging of BCs, Development of BC portal, Penalties imposed by banks on CBCs, Caution Money required from CBCs, BC Remuneration, participation of women in BC workforce etc.

Based on the Committee’s recommendations, the related regulatory guidelines are being reviewed, and the draft amendment directions will be issued shortly.

7. Collateral free loan limit for MSEs doubled to Rs 20 lacs

In 2010, following the RBI Working Group’s report (released March 6, 2010) on the Credit Guarantee Scheme (CGS) under CGTMSE, RBI mandated banks via circular in May 2010 to provide collateral-free business loans up to Rs. 10 lakh to Micro and Small Enterprises (MSEs).

A collateral-free business loan is an unsecured loan for business needs, requiring no pledge of assets like house, car, or property as mortgage until repayment backed by CGTMSE guarantee cover.

| MSEs are defined under the MSMED Act, 2006 and require mandatory Udyam Registration for eligibility, bank loans, priority sector benefits, and CGTMSE coverage—along with no blacklisting, viable project, and engagement in approved manufacturing/service/retail activities. Classifications: Micro enterprise (investment in plant/machinery ≤ Rs. 2.5 crore; turnover ≤ Rs. 10 crore); Small enterprise (investment ≤ Rs. 25 crore; turnover ≤ Rs. 100 crore); and Medium enterprise (investment ≤ Rs. 125 crore; turnover ≤ Rs. 500 crore). Banks must enforce this at branches, linking CGS/CGTMSE usage to staff evaluations for strict compliance. This remains the existing statutory requirement for MSE lending. |

RBI has decided to raise the collateral-free loan limit for MSEs from Rs. 10 lakh to Rs. 20 lakh, applicable to loans sanctioned or renewed on or after April 1, 2026, aiming to improve formal credit access, entrepreneurial activity, and last-mile delivery for collateral-scarce MSEs.

This policy shift represents a watershed moment for India’s grassroots economy, effectively doubling the financial runway for the nation’s most resilient entrepreneurs. By aligning with the PMMY ceiling, the policy ensures that a business’s potential rather than a proprietor’s personal property dictates its growth. This extra funding allows small businesses to move beyond daily expenses and finally invest in better machinery or technology to compete. Furthermore, it opens doors for women and young owners who may not own property to get formal bank support based purely on their performance. Ultimately, this change encourages more businesses to register officially, clearing the path for millions of small units to scale up and create more jobs without the fear of losing personal assets.

8. Total Return Swaps on Corporate Bonds

A Total Return Swap (TRS) is a derivative contract where a protection buyer exchanges the variable total return of an asset for a fixed return, shielding them from volatility. In this setup, the protection buyers swap the “total return” from the asset pool, with a return computed at a fixed spread on a base rate, say LIBOR. Protection sellers in a TRS guarantee a prefixed spread to protection buyers, who in turn, agree to pass on the actual collections and actual variations in prices on the credit asset to protection sellers. Essentially, the protection seller gains market exposure without a large upfront investment, while the protection buyer hedges their risk. Since protection sellers receive the total return from the asset, protection sellers also have the benefit of upside, if any, from the reference asset.

In India, the corporate bond market has historically lacked deep liquidity. To solve this, the Union Budget 2026 and the RBI have proposed introducing TRS specifically for corporate bonds and credit indices.

This development is a strategic shift toward “capital-efficient” investing. For business professionals, this means institutional investors can now gain exposure to corporate debt or hedge their existing bond portfolios without locking up massive amounts of capital on their balance sheets. By allowing the market to trade the “risk” and “returns” of bonds separately from the bonds themselves, the RBI aims to boost liquidity and make it easier for companies across various credit ratings to raise funds. Ultimately, this reform bridges a critical gap in India’s financial ecosystem, transforming the corporate bond market into a more active, transparent, and globally competitive space.

The draft amendment directions have been issued here.

- Voluntary Retention Route subsumed into FPI investment limits

Voluntary retention route for investment bonds and G-secs has been merged and made a part of the limit assigned for regular investments by FPIs; as a result, FPIs that commit to keep funds for at least 3 years may escape the minimum residual maturity requirement and the limits on investment in a bond issue by a single FPI. This introduces significant flexibility for those FPIs that are sure of staying invested in India for a long term, avoiding opportunism while granting them significant flexibility.

According to the Master Direction – Reserve Bank of India (Non-resident Investment in Debt Instruments) Directions, 2025, there are 5 channels of investments in debt instruments by non-resident investors. Under the VRR Route, FPIs are granted various operational exemptions, easing the investment process. VRR was introduced to encourage long term FPI investment in Indian debt markets by offering a dedicated investment channel with greater flexibility.

Given the strong utilisation of the VRR limits and to improve predictability and ease of doing business, the RBI has now decided to subsume VRR investments within the overall FPI investment limits under the General Route, while also providing additional operational flexibilities to FPIs investing through the VRR.

The detailed mechanism governing such limits has been notified here.

[1] Refer to our detailed write up on this topic- https://vinodkothari.com/2025/09/all-in-the-group-and-still-a a-customer/

IT Outsourcing Under the RBI’s 2025 Directions: What Has Changed?

By Archisman Bhattacharjee & Avikal Kothari | Finserv@vinodkothari.com

Introduction

On November 28, 2025, the Reserve Bank of India (“RBI”) issued the Reserve Bank of India (Non-Banking Financial Companies – Managing Risks in Outsourcing) Directions, 2025 (“Outsourcing Directions”), thereby repealing the erstwhile directions governing IT outsourcing and financial services outsourcing. For the purposes of this article, our discussion is confined to Chapter IV of the Outsourcing Directions, which specifically deals with outsourcing of information technology (“IT”) services. While the Outsourcing Directions largely represent a consolidation of the existing regulatory framework as also clarified by the RBI in its Consolidation of Regulations – Withdrawal of Circulars dated November 28, 2025, they also provide enhanced clarity and structure to the regulatory expectations applicable to IT outsourcing arrangements of NBFCs. This article seeks to examine whether, and to what extent, any additional or expanded obligations have been introduced by the RBI under the consolidated framework.

Applicability

Chapter IV of the Outsourcing Directions, dealing with IT services outsourcing is applicable on NBFC-ML and above, which was also the case for the Erstwhile IT Outsourcing Directions

Transitional Timeline for Compliance of Existing IT Outsourcing Arrangements

The erstwhile IT Outsourcing Directions had become applicable with effect from October 1, 2023. Under the Outsourcing Directions, the RBI has now prescribed a specific transition mechanism for existing IT outsourcing arrangements. In this regard, para 2 of the Outsourcing Directions provides that:

“These Directions shall come into force with immediate effect

Provided that for Non-Banking Financial Companies covered under the scope of these Directions, as mentioned in paragraph 3, their existing Information Technology (IT) outsourcing agreements, regardless of whether they are due for renewal on or after the effective date of these Directions, shall comply with the provisions of these Directions either at the time of renewal or by April 10, 2026, whichever is earlier.”

Given that the Outsourcing Directions are primarily in the nature of a consolidation exercise and do not introduce materially new obligations, the timeline up to April 10, 2026 appears to be intended to provide NBFCs with a reasonable window to align their existing IT outsourcing agreements with the consolidated framework. Accordingly, NBFCs should utilise this transition period to review, amend, and, where necessary, renegotiate their existing IT outsourcing contracts to ensure full compliance with the Outsourcing Directions within the prescribed timeline.

Against this backdrop, it becomes important to examine the substantive requirements laid down under Chapter IV of the Outsourcing Directions in relation to outsourcing of IT services to third-party vendors. The following section discusses the key regulatory expectations and compliance obligations applicable to NBFCs when engaging third-party service providers for IT outsourcing.

- Expanded scope of Service Provider Definition

The definition of “service provider” as defined under paragraph 58(3) of the Outsourcing Directions is expansive and extends beyond the primary contracting entity to include sub-contractors, third-party vendors, and entities forming part of the service delivery chain. Further the Outsourcing Directions under paragraph 58(4)have also now defined the term “sub-contractor” to mean:

“… those providing material / significant IT services to the service provider and is specific to the material / significant IT services arrangement that the NBFC has entered into with the service provider”

Accordingly, a sub-contractor that provides material or significant IT services to a service provider, where such services are critical to the delivery of the outsourced arrangement to the NBFC, would also fall within the ambit of the Outsourcing Directions. For instance, where an NBFC avails a SaaS solution from a third-party service provider, any entity that supplies core software or technology to such SaaS provider, without which the service cannot be effectively rendered, may be regarded as a material service provider for the purposes of the Outsourcing Directions.

While the erstwhile IT Outsourcing Directions did prescribe certain obligations in respect of sub-contractors (and the obligations of NBFCs vis-à-vis their primary service providers largely remain unchanged under the Outsourcing Directions), the current framework introduces greater clarity on who qualifies as a “sub-contractor.”

Actionables for NBFCs:

NBFCs should reassess their existing IT outsourcing landscape to identify all arrangements that fall within the expanded scope, including indirect or layered service delivery models. Vendor inventories should be updated to capture not only primary service providers but also material sub-contractors and supply-chain entities involved in the provision of IT services. Furthermore, NBFCs are advised suitably amend its existing policies to clearly specify the framework and criteria for identification of sub-contractors. This may, inter alia, include requiring service providers to furnish a list of their appointed sub-contractors along with details of the functions performed by each, and undertaking an assessment, in consultation with the relevant service provider, to determine whether such sub-contractors are material or non-material.

- Audit and Due Diligence

The Outsourcing Directions require NBFCs to conduct risk-based due diligence of IT service providers, this includes tracking system performance, uptime, service availability, Service Level Agreement, compliance and incident response on an ongoing basis. Regular risk-based audits of service providers, including sub-contractors, have been formalised, with an option to rely on pooled audits or recognised third-party certifications, though this does not dilute the NBFC’s responsibility for data security and system availability. NBFCs must also periodically review the financial and operational strength of service providers to identify any deterioration in performance, security or resilience. Access rights have been strengthened, requiring service providers to provide unrestricted access to relevant data and premises for NBFCs, auditors and regulators.

Actionables for NBFCs:

NBFCs should strengthen vendor due diligence processes and establish mechanisms for periodic review of service providers. Oversight frameworks should extend to subcontractors and material supply-chain entities, with clear accountability resting on the primary service provider. Overall, the changes make due diligence an ongoing obligation rather than a one-time exercise, requiring NBFCs to strengthen internal monitoring structures, audit planning and vendor risk management practices.

Further, considering that the RBI has mandated compliance of the agreements with the Outsourcing Directions by April 10, 2026, it is advisable for NBFCs to undertake a comprehensive review of the service level agreements and other contractual arrangements executed with all its material IT vendors to ensure alignment with the requirements set out under paragraphs 33, 34, 73 and 74 of the Outsourcing Directions.

Additionally, prior to April 10, 2026, NBFCs are suggested to conduct audits of its material service providers to verify:

- compliance with the contractual obligations agreed between the NBFC and the respective vendor; and

- adherence by such vendors to the applicable requirements prescribed under the IT outsourcing framework.

Alternatively, the Company may also rely on globally recognised third-party certifications made available by the service provider in lieu of conducting independent audits.

Where, based on such review or audit, the NBFC forms the view that a vendor is not in compliance with the contractual terms or applicable regulatory requirements, the NBFC should require the vendor to implement corrective action within defined timelines and, where necessary, amend or renegotiate the existing agreements to ensure alignment with the Outsourcing Directions.

Further, the NBFC should appropriately document such reviews, audits, and remediation measures and place the same before the senior management, in accordance with the requirements of paragraph 78 of the Outsourcing Directions, and/or before such a committee as may be identified under the NBFC’s IT Outsourcing Policy. Any material or adverse developments should also be escalated to the Board in alignment with the requirements of paragraph 78 of the Outsourcing Directions.

In cases where remediation or contractual modification is not feasible, the Company should maintain an exit plan/exit strategy, including identification of alternate service providers and/or arrangements for bringing the outsourced services in-house, so as to ensure continuity of critical operations and minimal disruption to customers.

Conclusion

The Outsourcing Directions mark a significant step by the RBI towards consolidating and strengthening the regulatory framework governing IT outsourcing by NBFCs. While the underlying obligations remain broadly consistent with the erstwhile regime, the transition period up to April 10, 2026 provides NBFCs with a critical opportunity to holistically reassess their IT outsourcing arrangements, rationalise vendor ecosystems, and embed robust contractual, operational, and governance safeguards. NBFCs that proactively undertake structured reviews, strengthen vendor risk management, and institutionalise ongoing monitoring mechanisms will be better positioned not only to achieve regulatory compliance but also to enhance operational resilience and customer trust.

Ultimately, IT outsourcing under the Outsourcing Directions is no longer a purely contractual or procurement function—it is a core governance and risk management responsibility. Treating it as such will be essential for NBFCs navigating an increasingly digital and interconnected financial services ecosystem.

See our other resources:

From Bye Backs to Buy Backs: how new taxation rules impact equity extraction

– Vinod Kothari and Payal Agarwal | corplaw@vinodkothari.com

Finance Bill, 2026 brings tax relief to investors for share buybacks, by partially restoring the position that existed before the Finance Bill 2024 amendment. The 2024 Finance Bill changed the taxability of buybacks to impose tax on buyback consideration, taxing the entire “receipt” as “dividend”, implying tax at applicable regular tax rates rather than as capital gains.[See our article on the 2024 amendments here.]

The 2026 Bill proposes omission of Section 2(40) (f), [dealing with deemed dividend] and amendments to Section 69, [specifically dealing with tax on buybacks]. The net result of this:

- Buyback consideration not to be treated as deemed dividend;

- Shareholder pays tax on the difference between buyback consideration received and cost of acquisition taxable as capital gains – depending on whether the gain in short term (20%) and long-term (12.5%)

- In case of promoter shareholders, an additional tax, so as to bring the effective tax rate to 22% in case of corporate shareholders, and 30% in case of non corporate shareholders. No difference between short-term and long-term capital gains.

Applicability of the amendments: The amended provisions apply for buybacks done on or after 1st April, 2026. The existing provisions were introduced effective 1st Oct., 2024 and therefore, they would have had a life of only 15 months.

Why buyback?

Buyback is not merely a means of distribution of profits to the shareholders. There may be various reasons or motivations for which buyback may be done by a company, for example:

- Distribution or upstreaming of profits – Buyback is used as a means of distribution of accumulated profits (free reserves as well as securities premium) to the shareholders.

- Scaling down of operations – It is a mode of scaling down the operations of the company, without going through the tedious process of capital reduction through NCLT.

- Selective exit to certain shareholders – Buyback may also be used as a means of providing selective exit to certain shareholders, based on pre-determined arrangements. This may include, for instance, exit to some strategic investor, or a particular promoter, or shareholders not willing to dematerialise their securities etc.

- Put options to strategic or private equity investors – In case of strategic/ private equity investors, the shareholder agreements may include clauses on exit through put options. One of the ways of giving exit to the shareholders exercising the put option may be through buyback of their shares.

- Encashment of stock options granted to employees – It is quite common primarily in case of start-ups, to go for buyback of ESOPs granted to employees, instead of issuing shares upon exercise of options. This helps in providing liquidity to the employees, while also avoiding dilution in the shareholding structure of the company.

Concept of Buyback and Compliances Involved

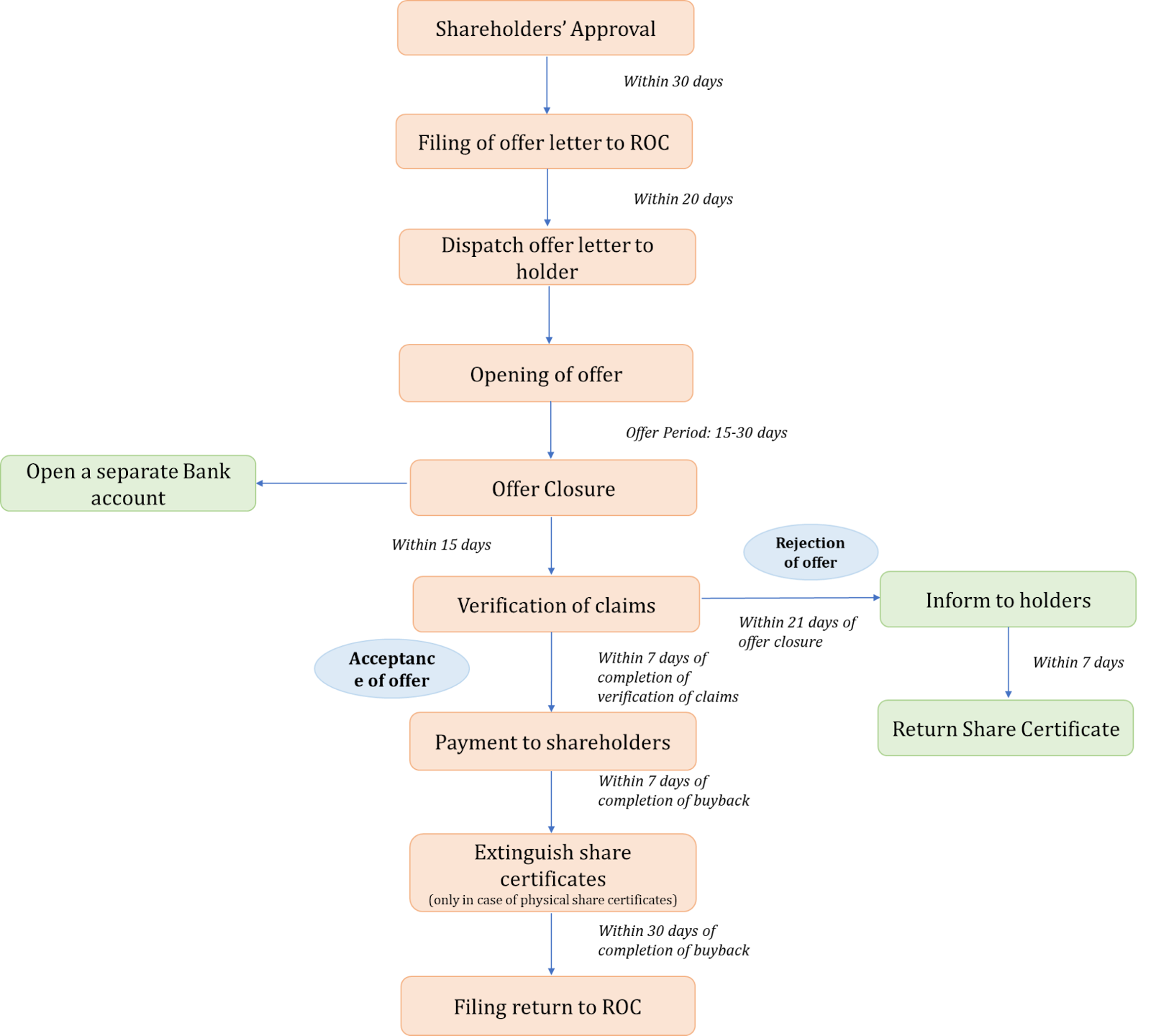

- Governed by section 68 of the Companies Act read with the rules made thereunder (also see figure 1)

- Out of free reserves, securities premium or proceeds of issue of shares

- Only upto 25% of paid up share capital and free reserves, with shareholders’ special resolution

- Maximum no. of equity shares cannot exceed 25% of total paid-up equity share capital for that financial year

For detailed guidance on the procedure and compliances involved, refer to our FAQs on buyback here.

Figure 1: Buyback process and timelines under Companies Act

Reduction of share capital as an alternative to buyback

For buyback of capital beyond the statutory limits, the provisions of capital reduction u/s 66 apply. With the buyback consideration being taxed as deemed dividends, capital reduction through NCLT route was also being seen as an alternate route for scaling down capital in a relatively tax-efficient manner. There are rulings favouring capital reduction as an alternative to buyback, for instance, the ruling of NCLAT in the matter of Brillio Technologies Pvt. Ltd v. ROC, subsequently also referred to by NCLT Mumbai in the matter of Reliance Retail Ltd. Some of these rulings even permitted selective reduction of capital. See our article on reduction of capital here.

One of the primary deterrents in capital reduction u/s 66 of the Companies Act is the approval requirements – of the shareholders, creditors and even the NCLT.

Buyback of shares vis-a-vis dividend on shares

The scope of dividend distribution is quite narrower as compared to share buybacks. The primary difference between the two is in the source of payment. Dividend distribution can be made only out of surplus; where free reserves are proposed to be utilised for dividend payment, additional conditions are applicable. In no case, can such declaration be made out of securities premium, or proceeds of fresh issuance – which are permissible sources for buyback. Buyback, on the other hand, requires mere liquidity, availability of profits is not mandatory. Therefore, dividends are merely a way to upstream the earned profits; buyback can even be the way to scale down, for example, by releasing the share premium, or using one class of shares to buy back the other.

Once dividend is approved by shareholders with requisite majority, there is no provision for a shareholder to waive off his right to the dividend [see our article on the same here], and unclaimed dividend, if any, are kept in a separate account to be transferred to IEPF. In case of buyback, while the same is also offered to all shareholders, the buyback consideration is paid only to such shareholders who tender their shares for buyback; the question of waiver of rights or unclaimed amounts does not arise.

Buyback taxation: existing scenario vs new scenario

| Particulars | Finance Bill, 2024 | Finance Bill, 2026 |

| Applicability for buybacks done | w.e.f. 1st October, 2024 | w.e.f. 1st April, 2026 |

| Taxable as | Deemed dividend. The holding cost of the bought back shares allowed as short term capital loss | Capital gains |

| Tax incidence on | Recipient shareholder | Recipient shareholder |

| Amount taxable | Entire buyback consideration | Gains on buyback, that is, Buyback consideration minus, cost of acquisition |

| Rate of tax | Applicable income tax slab rate | LTCG – 12.5%, subject to exemption upto Rs. 1.25 lacs STCG: 20% In case of promoters: 22%/ 30% (depending on whether domestic company/ otherwise) |

| Differential treatment for promoter shareholders | No | Yes, additional tax rates apply |

Under the erstwhile regime, the entire buyback consideration was taxable as deemed dividend, with the cost of acquisition claimable as capital loss. In such a case, the higher the cost of acquisition on such shares, higher would have been disincentive in the form of taxing the cost component as dividends. The benefits of capital loss depend on the existence of capital gains, and hence, the effective tax rates on buyback could not be ascertained.

In the amended tax regime, buyback consideration, minus, cost of acquisition, is taxed at flat rates of capital gains – 12.5%/ 20%, depending on whether the capital gains are long-term or short-term in nature.

Disincentives under the extant regime and market reaction

The disincentives were two-fold:

- Higher tax slabs: The treatment as “deemed dividend” resulted in higher tax rates for top bracket individuals, as compared to capital gains, chargeable @ 12.5%/ 20% – depending on long-term/ short-term capital gains.

- Taxing entire consideration: The entire “receipt” was taxable, instead of the actual gains, that is, excess of the receipts over the cost of acquisition.

- Cost of acquisition as capital loss: The cost of acquisition was to be treated as short term capital loss. As a result, there is an advantage to those shareholders who have short-term capital gains to offset the short term capital loss created as a result of the buyback. Note that the deemed dividend, in case of corporate shareholders, may be claimed as a deduction u/s 80M.

Resultant market reaction: a sharp decrease in buyback offers during FY 24-25 as compared to previous financial years. As per the publicly available data in case of listed companies, the total buyback size for 2024-25 was ₹7,897 Crores when compared to 2023-24 with a buyback offer size of Rs. 49,836 crores, indicating a decrease of 84.2 per cent.

The number of buyback offers sharply declined, with only 17 instances of buyback offer by listed entities between 1st October 2024 till date (3rd February, 2026) as compared to about 36-40 instances in each of FY 22-23 and FY 23-24.

How Finance Bill 2026 rationalises the tax treatment?

Pursuant to the Finance Bill, 2026, the buyback taxation appears to be rationalised in the following manner:

- Buyback consideration not to be treated as deemed dividend [omission of clause (f) to Sec 2(40)]

- Difference between consideration received and cost of acquisition taxable as capital gains [S. 69(1)]

- In the hands of the recipient shareholder

- In case of promoter shareholders, tax payable at higher rates depending on whether promoter is a domestic company or not

- Effective rate of 22% in case of domestic company and 30% in case of persons other than domestic company

With this, while the tax incentive remains in the hands of the recipient shareholders, the tax treatment is rationalised in the form of value that is to be taxed and the manner in which tax is levied. However, the provision differentiates between a promoter and non-promoter shareholder.

Meaning of promoter: moving beyond the statutory definition

In case of listed company

- Refers to the definition of promoter under Reg 2(1)(k) of SEBI Buyback Regulations

- SEBI Buyback Regulations, in turn, refers to Reg 2(1)(s) of SAST Regulations

- Under SAST Regulations, promoters include “promoter group”

| Promoter | Promoter group |

| Person having control over the affairs of the company, or Named as promoter in annual return, prospectus etc. | Includes immediate relatives of promoters Entities in which >20% is held by promoters Entities that hold >20% in promoters etc. Persons identified as such under “shareholding of the promoter group” in relevant exchange filings |

The scope of “promoter group” thus, is much broader than “promoter”.

In case of an unlisted company

- Refers to the definition of promoter under Sec 2(69) of the Companies Act

- Concept of promoter group is not there under Companies Act

- To broaden the scope, a person holding > 10% shares in the company, either directly or indirectly, has also been covered.

Question may arise on what does “indirect” shareholding mean? Does it include shareholding through relatives, or through other entities as well? The word “indirect” is not the same as “together with” or “persons acting in concert”. Indirect shareholding should usually mean shares held through controlled entities.

Why additional tax for promoters?

The amendments bring higher tax rates for promoters, in view of the distinct position and influence of promoters in corporate decision-making including in relation to buyback transactions. Promoters may want to influence buyback decisions for various reasons, for example:

- Providing exit to an existing promoter/ strategic shareholder in accordance with any existing arrangement

- Creation of capital losses (assuming buyback consideration is lower than the cost of acquisition) thus setting off the capital gains earned from other sources

- Encashing securities premium or accumulated profits in the company etc.

In view of the promoter’s ability to influence buyback decisions to meet own objectives, additional tax is levied on buyback consideration received by the promoters, thus addressing any tax-arbitrage that could have been created through buybacks.

See our Quick Bytes on Budget, 2026 at here

Our other resources on buyback at here

RBI Issues Draft Directions on Relief Measures in Areas Affected by Natural Calamities for Regulated Entities

Simrat Singh | finserv@vinodkothari.com

When nature unsettles the ordinary course of life, the regulatory hand should neither be withdrawn nor clenched; it should extend a humane touch, easing distress and guiding the return of order. In this spirit, the RBI has released draft directions on Relief Measures in Areas Affected by Natural Calamities, setting out a framework under which banks, NBFCs and other Regulated Entities (REs) may provide relief to borrowers impacted by natural calamities or similar external events. The framework enables REs to extend resolution plans to eligible borrowers, while permitting retention of standard asset classification and lower provisioning, benefits that would otherwise not be available if such restructuring were undertaken under the normal IRACP framework.

It may be noted that earlier RBI had issued guidelines for banks in connection with matters relating to relief measures to be provided in areas affected by natural calamities consolidated under ‘Master Direction – Reserve Bank of India (Relief Measures by Banks in Areas affected by Natural Calamities) Directions 2018 – SCBs’ dated October 17, 2018. In 2016, these guidelines were made applicable, mutatis mutandis, to all NBFCs as well, in areas affected by natural calamities as identified for implementation of suitable relief measures by the institutional framework viz., District Consultative Committee (DCCs)/ State Level Bankers’ Committee (SLBCs). However, given that the provisions were drafted considering the banking operations, the implementation by NBFCs was ambiguous and the provisions were often overlooked.

While the proposed framework applies to both banks (Commercial, RRB, Local area banks etc) and NBFCs, there are separate draft Directions issued for each RE. In case of banks the provisions carry additional system-level and public service responsibilities, reflecting their role within SLBCs and DCCs.

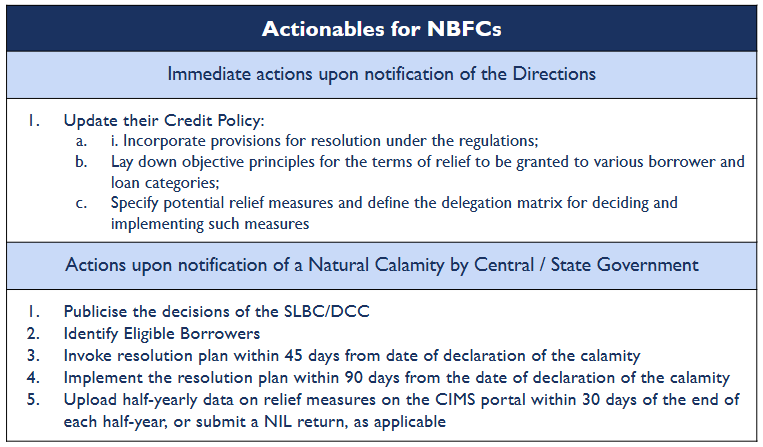

Fig 1: Actionables for NBFCs under the draft directions

Applicability and process flow

The draft directions are proposed to come into effect from 1 April 2026, after the final directions are notified. The framework is triggered upon formal notification of a natural calamity by the Central Government or the concerned State Government.

Where a calamity affects a substantial part of a State, it is proposed that a special meeting of the SLBC shall be convened within 15 days of such declaration. If the impact is confined to one or more districts, the corresponding DCC(s) are required to meet within the same timeframe. These committees assess the severity of the impact on economic activity, determine objective criteria for identifying impacted borrowers and indicate the nature and extent of relief such as moratoriums that may be extended by regulated entities operating in the affected areas. The decisions taken in these meetings are communicated to regulated entities and are required to be given adequate publicity, primarily by banks, through field outreach and public communication. The relief framework becomes operational in line with such Government notifications and the decisions of the SLBC or DCC, as applicable.

Amendments in the Credit Policy

The draft directions propose that the REs update their credit policies to incorporate a structured and pre-defined framework for dealing with borrower stress arising from natural calamities. The credit policy is expected to provide for resolution in line with the provisions and to set out objective principles governing the terms of relief across different borrower segments and loan categories.

While the precise parameters may vary depending on the nature and severity of the calamity, the decisions of the SLBC/DCC/Governments, the credit policy is expected to lay down a consistent framework to be applied by the REs when extending relief. This includes identifying potential relief measures, specifying verifiable parameters for determining eligibility of borrowers and extent of relief and defining the delegation matrix for approval and implementation. The emphasis is on ensuring timely decision-making, particularly in relation to restructuring of existing exposures and sanction of additional finance.

Eligible Borrowers and Coverage

Relief under the draft Directions is proposed to be available only to borrowers who meet the prescribed eligibility conditions as on the date of occurrence of the natural calamity. To qualify, the borrower’s account must be classified as ‘Standard’ and must not be in default for more than 30 days with the concerned RE in respect of any facility. Other additional conditions may be laid down in the credit policy.

Borrowers who do not meet these conditions fall outside the scope of the calamity relief framework and may instead be considered for resolution under the applicable Resolution of Stressed Assets Directions. In such cases, however, the RE does not receive the benefit of standard asset classification or lower provisioning (see discussion below). The framework extends its shelter only to those borrowers who, till the moment the calamity struck, had kept their financial obligations substantially intact. The protection is not meant to rescue infirm credit, but to steady sound accounts momentarily shaken by forces beyond human control.

Resolution Plan and Permissible Relief Measures

Where a RE decides to extend relief, the resolution plan is to be structured based on an assessment of the borrower’s post-calamity viability. The draft Directions propose a range of relief measures, including rescheduling of repayments, grant of moratorium, and conversion of accrued or future interest into another credit facility. Regulated entities may also consider sanctioning additional or fresh finance to address temporary financial stress, subject to appropriate assessment of viability and credit risk.

Notably, the framework is enabling rather than mandatory. It does not require automatic restructuring of all eligible accounts, thereby allowing REs to exercise credit judgement while operating within the prescribed regulatory parameters.

Timelines for Invocation and Implementation

It is proposed that resolution under the framework must be invoked within 45 days from the date of declaration of the natural calamity, unless an extension is granted by the Regional Director or Officer-in-Charge of the Reserve Bank. This would mean that the aggrieved borrower must approach the lender and the terms of restructuring must be agreed between both of them within the said timeframe. Once invoked, the resolution plan must be implemented within 90 days from the date of invocation.

In practice, this means that following the Government notification and the SLBC or DCC meeting, typically held within the first 15 days from the notification, REs have a limited 30-day window to complete borrower identification, viability assessment, documentation and approval. Failure to adhere to these timelines results in loss of the regulatory benefits available under the framework.

Asset classification treatment

The most significant regulatory benefit under the proposed framework relates to asset classification. Where a resolution plan is implemented in compliance with the Directions, borrower accounts classified as ‘Standard’ may be retained as such upon implementation instead of facing any downgrade. Further, accounts that may have slipped into NPA status between the date of occurrence of the calamity and the implementation of the resolution plan are permitted to be upgraded to ‘Standard’ upon implementation. However, as per the ECL Policy of the RE, generally any restructuring would automatically be treated as a SICR and therefore, the staging may change and a higher ECL would be required to be provided on such restructuring which may nullify the benefit.

After implementation, subsequent asset classification is governed by the applicable IRACP norms. The proposed framework also addresses cases of repeated restructuring. Where a borrower account is restructured again under these Directions before the reversal of additional provisions (see below), it may continue to be classified as ‘Standard’, subject to recognition of interest on a cash basis from the second restructuring onwards and maintenance of an additional specific provision of five per cent of the outstanding debt for each restructuring, subject to an overall ceiling of 100 per cent.

Income Recognition and Provisioning

For restructured accounts, it is proposed that interest income may be recognised on an accrual basis. At the same time, REs are required to maintain an additional specific provision of 5% of the outstanding debt, over and above the applicable provisioning under IRACP norms. Reversal of this additional provision can happen only where the borrower repays at least 20% of the outstanding debt, the account does not slip into NPA status after implementation of the restructuring and no further restructuring is undertaken during the relevant period. Specifically for banks, if the outstanding debt post-restructuring is only in the form of non-fund-based facilities or facilities in the nature of cash credit / overdraft, the additional provisions can be reversed after one year, post implementation of the restructuring, provided the borrower was not in default at any point of time during the period concerned.

Ancillary relief measures and government support

It is proposed that the REs be required to extend interest subvention or prompt repayment incentive benefits notified by the Government to all eligible borrowers. They must also ensure that any relief already provided, or being provided, by the Central or State Governments is duly factored into the resolution process.

For agricultural loans secured by land, the draft Directions propose acceptance of certificates issued by Revenue Department officials where original title documents have been lost due to the calamity. In areas governed by community ownership arrangements, certificates issued by competent community authorities may also be accepted. REs may also, at their discretion, provide additional relief such as waiver or reduction of fees and charges for borrowers in affected areas, for a period not exceeding one year. Expected proceeds from insurance policies may also be kept while deciding the relief. Additionally for banks it is proposed that they shall open small accounts for displaced borrowers and take immediate action to restore ATM services in the impacted areas. They may operate their natural calamity affected branches from temporary premises under advice to the RBI. For continuing the temporary premise beyond 30 days, banks may obtain specific approval from the concerned Regional Office of RBI. A bank shall also make arrangements to render banking services in the affected areas by setting up satellite offices, extension counters or mobile banking facilities etc. under intimation to the RBI.

Reporting Requirements

It is proposed that the REs shall upload data on relief measures extended under the framework in the prescribed format on a half-yearly basis. The data points include ‘Outstanding eligible for restructuring as on the date of notification of natural calamity’, ‘Credit facilities restructured/rescheduled during the half year’, ‘Additional/fresh loans provided to affected borrowers during the half year’ etc. The data must be submitted within 30 days from the end of each half-year, i.e., as of 30 September and 31 March, through the CIMS portal. Where no relief measures are extended during a reporting period, a NIL statement is required to be submitted.

See our other resources:

Buyback taxation rationalised with limited relief to promoter shareholders

– Finance Bill 2026 omits deemed dividend treatment on buyback consideration

– Payal Agarwal, Partner | corplaw@vinodkothari.com

Our quick bytes on Union Budget 2026 can be accessed here – https://vinodkothari.com/2026/02/quick-bytes-on-union-budget-2026/

The recent Finance Bill 2026 brings relief to investors in the form of changes in taxation for buyback consideration. With the omission of sub-clause (f) from Section 2(40) of the Income Tax Act, 2025 [dealing with deemed dividend], the position as it existed prior to 1st October, 2024, has been restored, except for additional tax rates in case of promoter shareholders.

- Applicability of the amended provisions

- For any buyback of shares on or after 1st April, 2026

- Existing provisions on taxability of buyback

- Included u/s 2(40)(f) of IT Act

- The entire amount paid by the company taxable as “dividend”

- Tax payable by shareholders

- Entire buyback consideration taxable as dividend

- TDS provisions as applicable to dividends apply

- Taxable at slab rates as applicable to respective shareholders, with a flat surcharge @ 15%

- Entire cost of acquisition in respect of shares bought back to be booked as “capital loss” [section 69 of IT Act]

- Such capital loss may be set off against capital gains subsequently

- As per section 111 of IT Act, the set-off is available for a period of 8 AYs immediately after the AY in which loss arises

- Amended provisions on taxability of buyback

- Buyback consideration not to be treated as deemed dividend [omission of clause (f) to Sec 2(40)]

- Difference between consideration received and cost of acquisition taxable as capital gains [S. 69(1)]

- In the hands of the recipient shareholder

- In case of promoter shareholders, tax payable at higher rates depending on whether promoter is a domestic company or not

- Effective rate of 22% in case of domestic company and 30% in case of persons other than domestic company

- Meaning of promoter

- In case of a listed company,

- As per Reg 2(1)(k) of SEBI (Buy-Back of Securities) Regulations, 2018

- Refers to the definition of promoter under SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018

- As per Reg 2(1)(k) of SEBI (Buy-Back of Securities) Regulations, 2018

- In any other case

- As per Section 2(69) of the Companies Act, 2013, or

- A person who holds, directly or indirectly, more than 10% of the shareholding in the company

- In case of a listed company,

- Example to understand taxability under old regime v/s new regime

| Particulars | Price per share | No. of shares | Amount (Rs.) |

| Total cost of acquisition | Rs. 50 | 100 | 5,000 |

| Shares tendered and accepted for buyback | Rs. 80 | 40 | 3,200 |

| Tax under old regime (effective 1st Oct, 2024) | Rs. 80 | 40 | 3,200 as dividend @ applicable tax slabs |

| Tax under new regime (effective 1st Apr, 2026) | Rs. (80-50) = Rs. 30 | 40 | 1,200 as capital gains @ short-term/ long-term capital gain rates |

- Intent of the amendments

- The extant tax regime on treating buyback consideration as deemed dividend resulted in taxing a “receipt” as income, without factoring the cost incurred in such receipts. See our article on the same here. The amended tax regime restores back the past position, by treating the difference between the buyback consideration and cost of acquisition as capital gains.

- Additional tax rates have been proposed for promoters, in view of the distinct position

- and influence of promoters in corporate decision-making, particularly in relation to buy-back transactions.

See our other resources on buyback – https://vinodkothari.com/2024/08/resource-centre-on-buyback/