An August 2025 Informal Guidance by SEBI for Welspun Corp Limited sought to clarify the applicability of contra trade on release of pledge. However, it goes on to say that: “…in case of creation of pledge/ revocation, the beneficial ownership does not change till pledge is invoked”. While the IG was specific to revocation of pledge, this seems to be creating a confusion on the contra trade restrictions on creation of pledge. In this article, we discuss the nature of pledge as a trade, and applicability of trading related restrictions on various stages of pledge. Also see a detailed article on treatment of various stages of pledge as trading under PIT Regulations.

Is pledge a trade?

Answer is yes

Trading means dealing in securities in any form [Reg 2(1)(l) of PIT Regulations]

Explanation to the definition expressly includes “pledging”

Creation of pledge may be considered equivalent to disposal/ intent to dispose the shares

Is release of pledge a trade?

Technically, a release (or so-called revocation) of a pledge is also a trade. However, given there is no change in beneficial ownership, there is no concern, at least from a contra trade perspective

There is no actual acquisition or intent to acquire shares, it is mere restoring back the position as it was prior to the creation of pledge

The shares are coming back to the person who was the beneficial owner of such shares previously.

Is invocation of pledge a trade?

No, since invocation of pledge is not at the discretion of the holder of shares

Invocation results in actual disposal of shares, however, related compliances w.r.t. such shares are undertaken at the stage of creation of pledge itself

Examples to understand contra-trade on pledge

Any opposite trade within 6 months of a prior trade attracts violation of contra-trade, except in case of specific waiver for a bona fide purpose. We discuss various combinations of trades within a span of 6 months to understand whether such trades attract contra-trade restrictions.

Transaction 1

Transaction 2

Is it contra-trade?

Can a waiver be granted by CO?

Purchase of shares (Buy)

Creation of pledge (Sell)

Yes, opposite trades within 6 months

Yes, if the DP is able to demonstrate the urgency and bona fide nature of such transaction

Creation of pledge (Sell)

Purchase of shares (Buy)

Yes, opposite trades within 6 months

In such a case, it is very difficult to prove bona fide of the subsequent trades of purchase of shares after creation of pledge.

Creation of pledge (Sell)

Release of pledge

No, since the release of pledge does not result in an opposite trade per se, it is incidental to the primary trade of pledge creation and only restores back the position as it was prior to creation of pledge.

NA

Release of pledge

Creation of pledge with another person (Sell)

No

Yes, if the DP is able to demonstrate the urgency and bona fide nature of the underlying transaction for which the pledge is to be created

Purchase of shares (Buy)

Invocation of pledge (Sell)

No, since the invocation of pledge is not at the discretion of the shareholder. The relevant act of disposal of shares is taken into account as a “trade” upon creation of pledge itself, and hence, not considered as “trade” again, upon such invocation.

NA

Invocation of pledge (Sell)

Purchase of shares (Buy)

NA

What is a bonafide purpose in the case of a pledge?

How does the Compliance officer verify/ensure that the purpose of the pledge is bonafide?

There cannot be any sure or one-size-fits-all response to this. Pledge is not for its own sake; pledge for an underlying transaction, which may be margin trading facility, borrowing, etc. The Compliance Officer should see whether that underlying transaction is within the regular business or activity of the pledgor. Whether the pledge is limited to the shares of the listed entity or has other securities? Whether the pledgee is an entity which is engaged in providing similar facilities to several unrelated entities? Whether the timing of the pledge is not indicating the advantage of a price spurt, etc.

Compliances applicable to various stages of pledge

The applicability of contra trade restrictions on the various stages of pledge are tabulated hereunder:

Stage of pledge

Nature of trade (Acquisition/ Disposal)

Pre-clearance required?

TWC applicable?

Contra-trade restrictions applicable?

Remarks

Creation of pledge

Disposal

Yes

No, if the trade is bona fide

Yes

While creation of pledge amounts to trade, exemptions from TWC and contra trade may be availed if the trade is for bona fide purpose.

Release of pledge

Acquisition

No

No

No

No change in beneficial ownership, and no actual acquisition/ disposal – mere restoration of the position prior to creation of pledge

Notice of invocation of pledge

NA

NA

NA

NA

No dealing in securities, mere notice specifying intent

Invocation of pledge

Disposal, however, continuation of the prior action of creation of pledge

No

NA

No

Invocation of pledge is done by the pledgee upon default. Once a pledge is created, the pledgor has no control over the invocation of such pledge upon default. Further, since creation of pledge is itself considered as ‘disposal’, the same shares cannot be considered to have been ‘disposed’ again, upon invocation.

Sale of pledged securities

Disposal, however, continuation of the prior action of creation of pledge

No (however, intimation to CO post sale, if not covered by System Driven Disclosure)

NA

No

Sale of pledged securities is done by the pledgee, and is not under the control of the pledgor. Further, since creation of pledge is itself considered as ‘disposal’, the same shares cannot be considered to have been ‘disposed’ again, upon sale.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-09 18:32:312026-03-12 09:49:20Span of Welspun: Is pledge/unpledge a trade under PIT?

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-02-10 19:27:072026-02-10 19:30:12NFRA’s reminder to fill gaps under two-way communication with Statutory Auditors

SEBI has issued a Consultation Paper on 05.02.2026 proposing amendments to the InvIT Regulations related to end-use of borrowings, status of SPVs and investment in under-construction projects. Further, it has also proposed to enhance the investible options for both REITs and InvITs w.r.t liquid mutual funds.

InvITs and REITs have continued on a strong upward growth trajectory. As of November 2025, the aggregate AUM of 27 InvITs stood at approximately ₹7,00,000 Crores after growing at a CAGR of approx 18% per annum since FY 21. The assets spann nine infrastructure sectors including roads, telecom, and power, as well as emerging asset classes such as warehouses and educational infrastructure. Reflecting their expanding scale and leverage capacity, aggregate borrowings of InvITs have crossed ₹2,03,000 Crores1. In contrast, REITs continue to trail InvITs in terms of scale, with the combined AUM of the five listed REITs amounting to approximately ₹2,35,000 Crores during the same period.2 May refer to our article “Roads to Riches: A Snapshot of InvITs in India”.

SEBI has consistently sought to create a more enabling regulatory environment for these vehicles. A notable example is the classification of REIT units as equity for mutual funds (as discussed below), which sought to enhance institutional participation and liquidity. Complementing these regulatory efforts, the Union Budget 2026 introduced several targeted measures to deepen infrastructure financing, including the proposed Partial Credit Enhancement (PCE) framework and the creation of a dedicated infrastructure fund (see our write-up on the Budget 2026 here). Lastly, RBI in its Statement on Developmental and Regulatory Policies also allowed Banks to lend to REITs, putting them on same footing as InvITs (see our write-up on RBI’s Statement here). Taken together, these developments indicate that the growth trajectory of InvITs and REITs is expected to remain firmly positive.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-02-10 11:45:132026-02-12 19:45:47InvITs and REITs: Regulatory actions for more enabling environment

NFRA moved the needle, and it is to be seen if the ocean starts boiling.! A 7th Jan 2026 circular from NFRA, addressed to listed entities and their auditors, seemed like an attention-drawer to standards of auditing which are already there, and yet, the auditing fraternity is holding meetings with boards and senior management of listed entities, to comply with what was always a compliance requirement. Does the 7th Jan circular bring up any new boxes to be ticked, any new procedures to be laid or responsibilities to be reiterated? As we detail out in this article, there may be need for action on several fronts on the part of listed entities – identification of nodal persons, listing developments that need to be communicated, constituting team for responding to the findings of the auditors in course of their audit other than those that sit in the audit report, formation of sub-groups of TCWG, etc.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-02-07 13:09:102026-04-23 18:49:25NFRA’s Call for a Two-Way Communication: A New Requirement or a Gentle Reminder?

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-02-07 11:53:112026-02-07 12:48:57Representation to SEBI for RPT provisions of LODR

Finance Bill, 2026 brings tax relief to investors for share buybacks, by partially restoring the position that existed before the Finance Bill 2024 amendment. The 2024 Finance Bill changed the taxability of buybacks to impose tax on buyback consideration, taxing the entire “receipt” as “dividend”, implying tax at applicable regular tax rates rather than as capital gains.[See our article on the 2024 amendments here.]

The 2026 Bill proposes omission of Section 2(40) (f), [dealing with deemed dividend] and amendments to Section 69, [specifically dealing with tax on buybacks]. The net result of this:

Buyback consideration not to be treated as deemed dividend;

Shareholder pays tax on the difference between buyback consideration received and cost of acquisition taxable as capital gains – depending on whether the gain in short term (20%) and long-term (12.5%)

In case of promoter shareholders, an additional tax, so as to bring the effective tax rate to 22% in case of corporate shareholders, and 30% in case of non corporate shareholders. No difference between short-term and long-term capital gains.

Applicability of the amendments: The amended provisions apply for buybacks done on or after 1st April, 2026. The existing provisions were introduced effective 1st Oct., 2024 and therefore, they would have had a life of only 15 months.

Why buyback?

Buyback is not merely a means of distribution of profits to the shareholders. There may be various reasons or motivations for which buyback may be done by a company, for example:

Distribution or upstreaming of profits – Buyback is used as a means of distribution of accumulated profits (free reserves as well as securities premium) to the shareholders.

Scaling down of operations – It is a mode of scaling down the operations of the company, without going through the tedious process of capital reduction through NCLT.

Selective exit to certain shareholders – Buyback may also be used as a means of providing selective exit to certain shareholders, based on pre-determined arrangements. This may include, for instance, exit to some strategic investor, or a particular promoter, or shareholders not willing to dematerialise their securities etc.

Put options to strategic or private equity investors – In case of strategic/ private equity investors, the shareholder agreements may include clauses on exit through put options. One of the ways of giving exit to the shareholders exercising the put option may be through buyback of their shares.

Encashment of stock options granted to employees – It is quite common primarily in case of start-ups, to go for buyback of ESOPs granted to employees, instead of issuing shares upon exercise of options. This helps in providing liquidity to the employees, while also avoiding dilution in the shareholding structure of the company.

Concept of Buyback and Compliances Involved

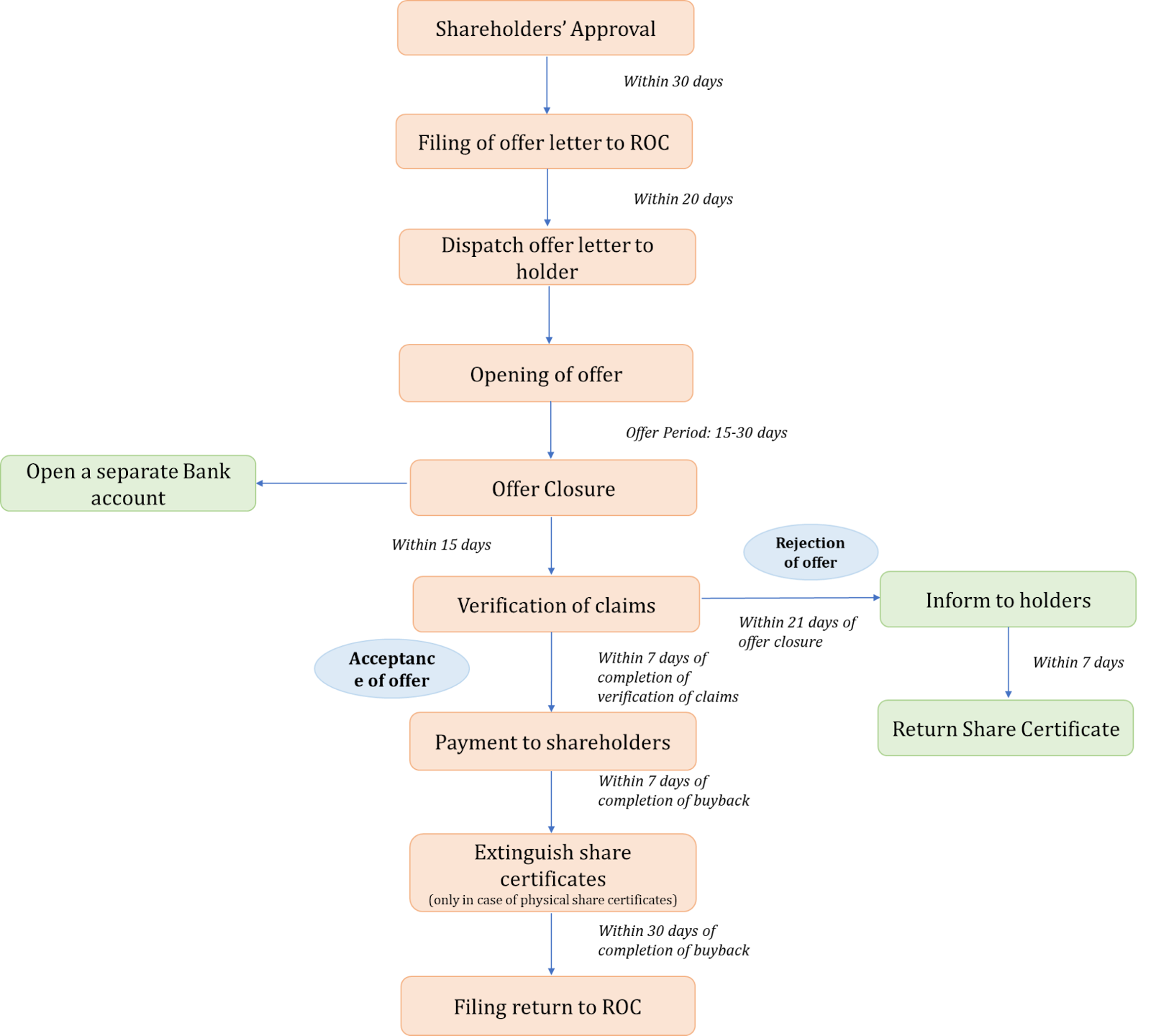

Governed by section 68 of the Companies Act read with the rules made thereunder (also see figure 1)

Out of free reserves, securities premium or proceeds of issue of shares

Only upto 25% of paid up share capital and free reserves, with shareholders’ special resolution

Maximum no. of equity shares cannot exceed 25% of total paid-up equity share capital for that financial year

For detailed guidance on the procedure and compliances involved, refer to our FAQs on buyback here.

Figure 1: Buyback process and timelines under Companies Act

Reduction of share capital as an alternative to buyback

For buyback of capital beyond the statutory limits, the provisions of capital reduction u/s 66 apply. With the buyback consideration being taxed as deemed dividends, capital reduction through NCLT route was also being seen as an alternate route for scaling down capital in a relatively tax-efficient manner. There are rulings favouring capital reduction as an alternative to buyback, for instance, the ruling of NCLAT in the matter of Brillio Technologies Pvt. Ltd v. ROC, subsequently also referred to by NCLT Mumbai in the matter of Reliance Retail Ltd. Some of these rulings even permitted selective reduction of capital. See our article on reduction of capital here.

One of the primary deterrents in capital reduction u/s 66 of the Companies Act is the approval requirements – of the shareholders, creditors and even the NCLT.

Buyback of shares vis-a-vis dividend on shares

The scope of dividend distribution is quite narrower as compared to share buybacks. The primary difference between the two is in the source of payment. Dividend distribution can be made only out of surplus; where free reserves are proposed to be utilised for dividend payment, additional conditions are applicable. In no case, can such declaration be made out of securities premium, or proceeds of fresh issuance – which are permissible sources for buyback. Buyback, on the other hand, requires mere liquidity, availability of profits is not mandatory. Therefore, dividends are merely a way to upstream the earned profits; buyback can even be the way to scale down, for example, by releasing the share premium, or using one class of shares to buy back the other.

Once dividend is approved by shareholders with requisite majority, there is no provision for a shareholder to waive off his right to the dividend [see our article on the same here], and unclaimed dividend, if any, are kept in a separate account to be transferred to IEPF. In case of buyback, while the same is also offered to all shareholders, the buyback consideration is paid only to such shareholders who tender their shares for buyback; the question of waiver of rights or unclaimed amounts does not arise.

Buyback taxation: existing scenario vs new scenario

Particulars

Finance Bill, 2024

Finance Bill, 2026

Applicability for buybacks done

w.e.f. 1st October, 2024

w.e.f. 1st April, 2026

Taxable as

Deemed dividend. The holding cost of the bought back shares allowed as short term capital loss

Capital gains

Tax incidence on

Recipient shareholder

Recipient shareholder

Amount taxable

Entire buyback consideration

Gains on buyback, that is, Buyback consideration minus, cost of acquisition

Rate of tax

Applicable income tax slab rate

LTCG – 12.5%, subject to exemption upto Rs. 1.25 lacs STCG: 20% In case of promoters: 22%/ 30% (depending on whether domestic company/ otherwise)

Differential treatment for promoter shareholders

No

Yes, additional tax rates apply

Under the erstwhile regime, the entire buyback consideration was taxable as deemed dividend, with the cost of acquisition claimable as capital loss. In such a case, the higher the cost of acquisition on such shares, higher would have been disincentive in the form of taxing the cost component as dividends. The benefits of capital loss depend on the existence of capital gains, and hence, the effective tax rates on buyback could not be ascertained.

In the amended tax regime, buyback consideration, minus, cost of acquisition, is taxed at flat rates of capital gains – 12.5%/ 20%, depending on whether the capital gains are long-term or short-term in nature.

Disincentives under the extant regime and market reaction

The disincentives were two-fold:

Higher tax slabs: The treatment as “deemed dividend” resulted in higher tax rates for top bracket individuals, as compared to capital gains, chargeable @ 12.5%/ 20% – depending on long-term/ short-term capital gains.

Taxing entire consideration: The entire “receipt” was taxable, instead of the actual gains, that is, excess of the receipts over the cost of acquisition.

Cost of acquisition as capital loss: The cost of acquisition was to be treated as short term capital loss. As a result, there is an advantage to those shareholders who have short-term capital gains to offset the short term capital loss created as a result of the buyback. Note that the deemed dividend, in case of corporate shareholders, may be claimed as a deduction u/s 80M.

Resultant market reaction: a sharp decrease in buyback offers during FY 24-25 as compared to previous financial years. As per the publicly available data in case of listed companies, the total buyback size for 2024-25 was ₹7,897 Crores when compared to 2023-24 with a buyback offer size of Rs. 49,836 crores, indicating a decrease of 84.2 per cent.

The number of buyback offers sharply declined, with only 17 instances of buyback offer by listed entities between 1st October 2024 till date (3rd February, 2026) as compared to about 36-40 instances in each of FY 22-23 and FY 23-24.

How Finance Bill 2026 rationalises the tax treatment?

Pursuant to the Finance Bill, 2026, the buyback taxation appears to be rationalised in the following manner:

Buyback consideration not to be treated as deemed dividend [omission of clause (f) to Sec 2(40)]

Difference between consideration received and cost of acquisition taxable as capital gains [S. 69(1)]

In the hands of the recipient shareholder

In case of promoter shareholders, tax payable at higher rates depending on whether promoter is a domestic company or not

Effective rate of 22% in case of domestic company and 30% in case of persons other than domestic company

With this, while the tax incentive remains in the hands of the recipient shareholders, the tax treatment is rationalised in the form of value that is to be taxed and the manner in which tax is levied. However, the provision differentiates between a promoter and non-promoter shareholder.

Meaning of promoter: moving beyond the statutory definition

In case of listed company

Refers to the definition of promoter under Reg 2(1)(k) of SEBI Buyback Regulations

SEBI Buyback Regulations, in turn, refers to Reg 2(1)(s) of SAST Regulations

Under SAST Regulations, promoters include “promoter group”

Promoter

Promoter group

Person having control over the affairs of the company, or Named as promoter in annual return, prospectus etc.

Includes immediate relatives of promoters Entities in which >20% is held by promoters Entities that hold >20% in promoters etc. Persons identified as such under “shareholding of the promoter group” in relevant exchange filings

The scope of “promoter group” thus, is much broader than “promoter”.

In case of an unlisted company

Refers to the definition of promoter under Sec 2(69) of the Companies Act

Concept of promoter group is not there under Companies Act

To broaden the scope, a person holding > 10% shares in the company, either directly or indirectly, has also been covered.

Question may arise on what does “indirect” shareholding mean? Does it include shareholding through relatives, or through other entities as well? The word “indirect” is not the same as “together with” or “persons acting in concert”. Indirect shareholding should usually mean shares held through controlled entities.

Why additional tax for promoters?

The amendments bring higher tax rates for promoters, in view of the distinct position and influence of promoters in corporate decision-making including in relation to buyback transactions. Promoters may want to influence buyback decisions for various reasons, for example:

Providing exit to an existing promoter/ strategic shareholder in accordance with any existing arrangement

Creation of capital losses (assuming buyback consideration is lower than the cost of acquisition) thus setting off the capital gains earned from other sources

Encashing securities premium or accumulated profits in the company etc.

In view of the promoter’s ability to influence buyback decisions to meet own objectives, additional tax is levied on buyback consideration received by the promoters, thus addressing any tax-arbitrage that could have been created through buybacks.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-02-03 17:01:012026-02-03 17:53:47From Bye Backs to Buy Backs: how new taxation rules impact equity extraction

The recent Finance Bill 2026 brings relief to investors in the form of changes in taxation for buyback consideration. With the omission of sub-clause (f) from Section 2(40) of the Income Tax Act, 2025 [dealing with deemed dividend], the position as it existed prior to 1st October, 2024, has been restored, except for additional tax rates in case of promoter shareholders.

Applicability of the amended provisions

For any buyback of shares on or after 1st April, 2026

Existing provisions on taxability of buyback

Included u/s 2(40)(f) of IT Act

The entire amount paid by the company taxable as “dividend”

Tax payable by shareholders

Entire buyback consideration taxable as dividend

TDS provisions as applicable to dividends apply

Taxable at slab rates as applicable to respective shareholders, with a flat surcharge @ 15%

Entire cost of acquisition in respect of shares bought back to be booked as “capital loss” [section 69 of IT Act]

Such capital loss may be set off against capital gains subsequently

As per section 111 of IT Act, the set-off is available for a period of 8 AYs immediately after the AY in which loss arises

Amended provisions on taxability of buyback

Buyback consideration not to be treated as deemed dividend [omission of clause (f) to Sec 2(40)]

Difference between consideration received and cost of acquisition taxable as capital gains [S. 69(1)]

In the hands of the recipient shareholder

In case of promoter shareholders, tax payable at higher rates depending on whether promoter is a domestic company or not

Effective rate of 22% in case of domestic company and 30% in case of persons other than domestic company

Meaning of promoter

In case of a listed company,

As per Reg 2(1)(k) of SEBI (Buy-Back of Securities) Regulations, 2018

Refers to the definition of promoter under SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018

In any other case

As per Section 2(69) of the Companies Act, 2013, or

A person who holds, directly or indirectly, more than 10% of the shareholding in the company

Example to understand taxability under old regime v/s new regime

Particulars

Price per share

No. of shares

Amount (Rs.)

Total cost of acquisition

Rs. 50

100

5,000

Shares tendered and accepted for buyback

Rs. 80

40

3,200

Tax under old regime (effective 1st Oct, 2024)

Rs. 80

40

3,200 as dividend @ applicable tax slabs

Tax under new regime (effective 1st Apr, 2026)

Rs. (80-50) = Rs. 30

40

1,200 as capital gains @ short-term/ long-term capital gain rates

Intent of the amendments

The extant tax regime on treating buyback consideration as deemed dividend resulted in taxing a “receipt” as income, without factoring the cost incurred in such receipts. See our article on the same here. The amended tax regime restores back the past position, by treating the difference between the buyback consideration and cost of acquisition as capital gains.

Additional tax rates have been proposed for promoters, in view of the distinct position

and influence of promoters in corporate decision-making, particularly in relation to buy-back transactions.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-02-01 15:08:392026-02-02 13:08:48Quick Bytes on Union Budget 2026

The relevance of climate finance in climate action cannot be undermined, since climate change mitigation and adaptation require large-scale mobilisation of financial resources. The Economic Survey 2025-26, tabled in Parliament by Union Finance Minister Nirmala Sitharaman on January 29, 2026, highlights that the current climate finance levels are inadequate for developing countries to achieve their climate goals. This climate funding gap is not a lack of ambition, rather, is imbibed in the structural weaknesses of the international financial system.

Climate Finance gap in India and other developing countries

By 2030, developing economies are estimated to need USD 5–6 trillion1 for effective climate action. With that in mind, the following may be noted:

Despite global efforts, developing countries continue to face a significant funding gap of around USD 4 trillion annually for sustainable development, as highlighted at the Fourth International Conference on Financing for Development (Compromiso de Sevilla)2.

Climate finance in India remains skewed towards only the mature sectors such as solar, wind energy and energy efficiency.

Critical areas, including adaptation, financing for micro, small, and medium enterprises (MSMEs), urban infrastructure, and hard-to-abate industries, remain underfunded.

1.1. Challenges in mobilising private capital for climate finance

In 2023, global financial assets under management totalled USD 1.9 trillion, with private capital accounting for nearly USD 1.3 trillion3. Most of this private capital went to advanced economies, with China receiving another 30%, whereas other developing countries, excluding China, received merely around 15%. The reasons for such a gap include:

Developing countries, being more vulnerable to climate change, face higher borrowing costs owing to currency volatility, lower sovereign credit ratings, and financial systems that lack depth.

Most of the abundant global capital flows to developed economies with stronger financial markets and economies that pose minimal risks.

Investors often hesitate to finance climate resilience projects in developing countries.

Policy Initiatives towards bridging the Finance Gap

While the overall progress of the country towards the climate goals remain insufficient4, India has, over years, through policy initiatives and regulatory reforms, have mobilised climate finance to the extent that has resulted in a 36% reduction in emissions intensity since 2005 and achieved 50% non-fossil power capacity ahead of schedule. The policy initiatives taken include the following:

Allowing 100% foreign direct investment in renewable energy projects.

Implementing SEBI’s Business Responsibility and Sustainability Reporting (BRSR) framework, green bond guidelines. [Refer to our BRSR resource centre]

Provision of credit lines and financing for climate-related investments by Development finance institutions in India, including IREDA, NABARD, SIDBI, PFC, and REC.

Issuance of Sovereign Green Bonds to fund low-carbon public infrastructure, providing policy signalling and market benchmarks. [Refer to our article on SGBs here]

Introduction of green deposit framework by RBI that optimises the flow of credit to green activities/projects by channelising institutional and household savings, with guardrails in place to overcome greenwashing challenges. [Refer to our article on green deposits here]

Incorporating risk mitigation, reconstruction, and recovery, as well as prevention, under the State Disaster Mitigation Fund (SDMF) and the National Disaster Mitigation Fund (NDMF), institutionalised as part of the Disaster Management Act 2005.

Implementation of Glacial Lake Outburst Flood Mitigation Programme approved under NDMF to monitor glaciers and glacial lakes in the Indian Himalayan region.

2.1. Bridging the gap domestically

Currently, around 83 per cent of India’s finance for mitigation and 98 per cent of finance for adaptation is sourced domestically, reflecting strong internal financing. While relying solely on domestic resources is insufficient to meet India’s overall climate investment needs, some steps towards strengthening the domestic financial system may include:

Issuing municipal green bonds can unlock USD 2.5–6.9 billion for local bodies driven climate action over the next 5–10 years.

Strengthening the financial ecosystem through the mobilisation of blended finance, de-risking of projects, and capacity building through technical assistance and training through specialised development finance institutions like IREDA, NABARD, SIDBI, PFC, and REC can play a critical role in advancing India’s climate finance landscape by supporting low-carbon and renewable energy projects.

Extending insurance coverage to safeguard people against economic losses associated with the physical risks of climate change, and improving the creditworthiness of climate-exposed borrowers such as farmers and MSMEs.

Conclusion

There is a wide disparity between the climate vulnerability and the funds available towards supporting the climate action. While policy incentives are being shaped towards mobilising domestic finance, an effective global response is required, particularly towards the developing countries. The global capital allocation needs to be mobilised towards areas where the investment needs for sustainable development are most pressing.

UNFCCC (2024, September 10). Second report on the determination of the needs of developing country Parties related to implementing the Convention and the Paris Agreement: https://unfccc.int/documents/64075↩︎