NFRA Circular on effective communication between auditors and TCWG – Frequently Asked Questions

Team Corplaw | corplaw@vinodkothari.com

Other resources:

NFRA’s Call for a Two-Way Communication: A New Requirement or a Gentle Reminder?

Team Corplaw | corplaw@vinodkothari.com

Other resources:

NFRA’s Call for a Two-Way Communication: A New Requirement or a Gentle Reminder?

– Heta Mehta, Senior Executive | corplaw@vinodkothari.com

Watch our video here: https://youtu.be/XaS6Eh3Ekd4

See our other resources:

– Team Corplaw | corplaw@vinodkothari.com

– Abhishek Namdev, Assistant Manager | corplaw@vinodkothari.com

– Team Corplaw | corplaw@vinodkothari.com

In line with an overhaul of changes proposed in the Companies Act, 2013, the Corporate Laws (Amendment) Bill proposes some changes in the Limited Liability Partnership (LLP) Act, 2008. Aimed at greater ease of doing business for corporates, the proposals are dominated by provisions to recognise LLPs operating in International Financial Services Centres by allowing them to issue and maintain share capital in foreign currency as permitted by the International Financial Services Centres Authority . Further, decriminalisation of various procedural defaults under the LLP Act have been provided for by replacing criminal provisions with civil penalties, , and easing compliances for Alternative Investment Funds which are formed asLLPs.

Read our coverage on the amendments proposed in the Companies Act, 2013 here.

– Saloni Khant, Executive | corplaw@vinodkothari.com

It is common for companies to enter into multi-year contracts in its usual business operations, to secure supply of goods or services, access to premises for operations, or for other commercial reasons etc. In the maze of RPT compliances, however, given that the transactions are usually approved by the Audit Committee and/ or shareholders on an omnibus basis, challenges arise on the ideal way of dealing with and taking approval for multi-year contracts.

The relevance of multi-year contracts in the context of RPTs arises for two reasons:

Several questions arise:

The crucial point in considering whether a contract requires yearly approval or one single approval valid for the whole contract is based on the “divisibility” of the contract – that is to say, its ability to be divided into smaller units instead of considering the contract as a whole. If it is a single contract for a fixed term, the approval of the contract is approval of the entire exchange of resources/services that takes place over such term.

The divisibility of a contract may be judged against various factors, for instance:

We discuss each of these in detail below.

Several contracts may have a fixed tenure, but does the fixity of tenure itself implies that such a contract shall be required to be approved through a single approval – valid for the whole tenure of the transaction?

There may be several contracts having a fixed term, but the fixity of term in itself may not be the essential feature in all such contracts. For example, a contract might have been entered into 3 years for supply of certain goods or services. While the tenure of the contract is 3 years, each instance of supply of goods or services constitutes an independent divisible supply in itself. Hence, in such cases, merely based on the tenure of the contract, the indivisibility of such arrangement cannot be argued.

In a multi-year contract, there are usually payment milestones based on performance of the contract. For example, a contract for development of software may contain milestones, such as, (i) development of UAT model, (ii) development of final software interface, and (iii) activation of the software etc. While the contract value may be divided based on the three different stages or milestones specified in the contract – it is important to note that the performance of the contract becomes complete only upon activation of the software, and hence, the divisions based on the performance milestones do not have an independent existence. Hence, dividing the contract would not be feasible here.

The most important factor in considering the divisibility of a contract is the actual performance of the contract. Whether the contract is of such nature that the delivery happens “over a period of time”, or is it such that while the exchange of resources/ services take place over the tenure of the term, the performance may be said to be complete only “at a point of time”.

Period of time v. point of time: drawing reference from Ind AS 115

In order to understand the divisibility of a contract based on ‘period of time’ v/s ‘point of time’- reference may be drawn from its closest equivalent under Ind AS 115 read with its guidance note for the purpose of revenue recognition.

Ind AS 115 specifies conditions based on which it may be said that the performance obligation is satisfied and revenue is required to be recognised over a period of time: [Para 35]

Where none of these conditions are satisfied, the performance obligation in the contract is considered to be satisfied at a point in time.

(a) the customer simultaneously receives and consumes the benefits provided by the entity’s performance as the entity performs;

The key question here is if the performance of the contract is stopped midway, would the customer still be considered to have benefitted from the performance already done?

For e.g., in a rental agreement, the tenant takes the benefit of the premises simultaneously. Even if the tenancy is terminated midway, it does not take away the benefits already enjoyed by such tenant during the period of the contract, he would remain benefitted for the fulfilled period of tenancy.

This may be compared with a construction agreement, where, in the event of an early termination of the contract, the performance obligations would remain incomplete, with no benefits to the customer for the period of time during which the service has been performed prior to its termination. Even where the work is rerouted to another supplier, it would require substantial rework.

(b) the entity’s performance creates or enhances an asset (for example, work in progress) that the customer controls as the asset is created or enhanced;

The renovation of an office building owned by the customer would amount to a contract over a period of time. The service may be terminated midway and can be completed by another service provider since the control of the asset remains with the owner at all times.

(c) the entity’s performance does not create an asset with an alternative use to the entity and the entity has an enforceable right to payment for performance completed to date.

The term ‘an alternative use’ must be considered from the perspective of practical limitations and contractual restrictions. Where the nature of the asset is such that it cannot be redirected to another contract, for example – machinery with unusual specifications cannot be sold to another customer, it is said to not have an alternative use. Even where the resources are portable, but the contractual terms restrict such redirection, there is no alternative use.

In such cases, where a contract is terminated midway, the service provider must have the right to receive payment on quantum meruit basis i.e. the work is sufficiently divisible to assess the payment due to the supplier.

When a contract fulfills any of the three conditions, it satisfies one principle criteria:

Any exit from the contract may require the contractual parties to replace the party, and may have penal consequences, but it is not as if the contract was not performed at all.

Where the transaction is a single indivisible contract i.e. takes place over a period of time, the IND AS recognises revenue over time by measuring the progress in the performance of the contract[1]. Accordingly, the transaction must be placed in its entirety with its full value for approval before the audit committee, the board of directors and the shareholders (if the materiality threshold is crossed). The transactions placed before all the three bodies must be aligned. Once approved, the actual implementation of the transaction shall come merely for review before the audit committee on a yearly basis in terms of section III.B.5 of the SEBI Master Circular dated January 30, 2026.

An interesting question arises here. Once approved, shall this amount be aggregated with new proposed transactions in the next year? Let us consider an illustration here. The materiality threshold for A Ltd. (listed entity) is Rs. 2000cr. In FY 25-26, A enters into a construction contract (single indivisible multiyear contract) and in FY 26-27, a contract for purchase of goods (one off transaction) with B Ltd for various amounts as tabulated below:

| S. No. | FY 25-26 | FY 26-27 | |||||

| Construction Contract Amt (Rs.) (I) | Whether I is material and approved by shareholders? | Purchase Contract Amt (Rs.) (II) | Whether II is material and needs shareholders’ approval? | Whether (I) and (II) shall be aggregated for materiality threshold? | Does the aggregate of (I) and (II) cross the materiality threshold? | Whether (I) shall be placed for noting before shareholders? | |

| 1 | 1000cr | No | 500cr | No | Yes | No | No |

| 2 | 1000cr | No | 1500cr | No | Yes | Yes | Yes |

| 3 | 1000cr | No | 2300cr | Yes | Yes | Yes | Yes |

| 4 | 3000cr | Yes | 1 | No | No | No | Already approved by the shareholders |

| 5 | 3000cr | Yes | 2500cr | Yes | Not required | Yes | |

For the first 3 cases, the transactions are aggregated for testing the material threshold since transaction (I), even though ongoing in FY 26-27, has never been placed before the shareholders. In effect, in case 2, the actual transactions ongoing with B in FY26-27 are crossing the materiality threshold and thus, must be placed for approval before the shareholders.

In case 3, while Transaction (II) crosses the threshold independently, it is only logical for the shareholders to be apprised of the other ongoing transactions (Transaction I) with the same RP to understand the true position of the transactions between the RP and the listed entity. The Industry Standard Note on RPTs (ISN), anyways, requires this disclosure. [Part A(3)] Read our latest article on the ISN: Repetitive Overhaul: RPT regime to get softer

In case 4, Transaction (I) has already been placed before the shareholders for approval. If its value is aggregated with Transaction (II), even a Rs. 1 transaction will require the approval of the shareholders. The essence of the materiality thresholds is seeking approval for material contracts. Such aggregation would defeat the very intent of the law.

In case 5, Transaction (I) is already approved by the shareholders and Transaction (II) crosses the materiality threshold independently. There arises no question of aggregation.

Thus, the decision of aggregating the value of a single indivisible contract in the previous FY for materiality thresholds in the current FY depends upon

On the other hand, where the transaction is a divisible contract over a term, the estimated value to be utilised in that particular year may be placed for approval before the audit committee, board of directors and shareholders, as the case may be. In case a material transaction was approved by the audit committee on an omnibus basis, it shall continue to be placed before the shareholders. [Section III.B.5 of the Master Circular]. Since the yearly value of the transaction is being approved and utilised, there arises no question of aggregation of previously approved value with proposed transactions in a new FY.

The law enables securing transparent approvals for indivisible contracts. The ISN requires an estimated break-up financial year-wise in case of a transaction spanning over multiple years to be placed before the audit committee as well as shareholders, as the case may be [Para A5(5)]. (See our FAQs on the Industry Standard Note)

Further, while disclosing RPTs on a half yearly basis as a part of quarterly integrated filing (governance) to the stock exchange, the Master Circular requires disclosure of the aggregate value of the RPT as approved by the Audit Committee as well as the value of transaction during the reporting period.

With SEBI settling RPT approval related non-compliances for settlement fees running into crores[2], compliance officers need to tread more carefully than ever. Deciding whether a multi year contract should be approved as a whole or in parts remains a crucial decision, particularly in the absence of detailed guidance under Companies Act and SEBI LODR. While accounting standards primarily address revenue recognition and may not directly apply to all RPTs, the principles outlined therein can still offer useful guidance in navigating such situations.

[1] Para 39 of the IND AS 115

[2]https://www.sebi.gov.in/enforcement/orders/feb-2026/settlement-order-in-the-matter-of-kalyani-steels-limited_99922.html

Refer to our other resources:

Register here: https://forms.gle/1iR2xaFKGBU1kRJ3A

Read our brief analysis of the proposals here:

Corporate Laws Amendment Bill: Easing, Streamlining and Updating the Regulatory Framework

– Team Corplaw | corplaw@vinodkothari.com

The Statement of Objects and Reasons refers to the Govt’s constant “endeavour to facilitate greater ease of doing business for corporates”; after reading through the provisions of the Bill, that indeed seems to be the intent, though, as happens often, the intent may get miscarried. The provisions are admittedly inspired by the recommendation of the 2025 High Level Committee on Non-financial Regulatory Reforms.

Broadly, the Bill focuses on decriminalisation, streamlining of provisions, bringing more audit quality oversight with powers to NFRA, regulation of the profession of valuations, etc. While doing so, it also makes the provisions of the State more aligned to present day realities, permitting greater digitisation, recognising concepts such as stock-appreciation rights or similar share-related benefits, etc. Note that the Bill has been referred to the Joint Parliamentary Committee.

Presently, the Companies Act does not include specific provisions to enable companies to prepare accounts or financial statements in foreign currencies. Taking into account the nature of companies set up in IFSC jurisdiction, this is a welcome change. It also seeks to clarify that such companies shall pay fees, fines and penalties under the Companies Act and the rules made thereunder in Indian rupees.

IBBI to be Valuation Authority; valuers get significant powers and responsibilities

Striking off names of defunct companies – [Sec 248]

| Section | Action | Existing Penalty | Proposed Penalty |

| 4(5)(ii) | Name applied by furnishing wrong or incorrect information | Upto 1 Lakh | 50, 000 |

| 42(10) | Makes offer or accepts money in contravention of sec. 42 | Upto money raised through private placement or 2 crore, whichever is lower | Money raised through private placement or 2 crore, whichever is lower |

| 128(6) | MD, WTD, CEO fails to comply with Section 129 | 50,000 – 5,00,00 | 5,00,000 – listed company and 50,000 -any other company |

| 166(8) | Director violated the provisions of sec. 166 except sub-section (5) | 1 lakh – 5 lakh | Listed company – 5 lakhOther company – 2 lakh |

| 189 | Fails to comply with provisions w.r.t Register of contracts or arrangements in which directors are interested | NA | 2 lakh |

| 446B | Lesser Penalty for certain companies | In case of Company- upto 50% of penalty specified in provisions upto 2 lakh In case of officer in default or any other person- upto 50% of penalty specified in provisions upto 1 lakh | In case of Company- 50% or such per cent not exceeding the 50% penalty prescribed in such provision upto 2 lakh In case of officer in default or any other person-50% or such per cent not exceeding the 50% penalty prescribed in such provision upto 1 lakh |

| Section | Action | Existing FIne | Proposed Penalty |

| 128(6) | MD, WTD, CEO fails to comply with Section 128 | 50,000 – 5,00,000 | 5,00,000 – listed company and 50,000 -any other company |

| 147(1) | Punishment for contravention of provisions of sections 139 to 146 | Company- Fine – 25,000 – 5,00,000 OID – Fine – 10,000 – 1,00,000 | Company – Penalty – 1,00,000 – 5,00,000 OID – Penalty – 25,000 – 1,00,000 |

| 166(7) | Default in complying with Section 166 except sub-section (5) | Director – 1,00,000 – 5,00,000 | Listed company – 5,00,000Any other Company – 2,00,000 |

| 167(2) | In case a Director continues as a director even when he knows that the office of director held by him has become vacant on account of any of the disqualifications | Director – 1,00,000 – 5,00,000 | Listed company – 5,00,000Any other Company – 2,00,000 |

Compounding of certain offences [Sec 441]

Miscellaneous [Sec 447- 470]

Read our coverage on the amendments proposed in the LLP Act, 2008 here.

– Saloni Khant, Executive | corplaw@vinodkothari.com

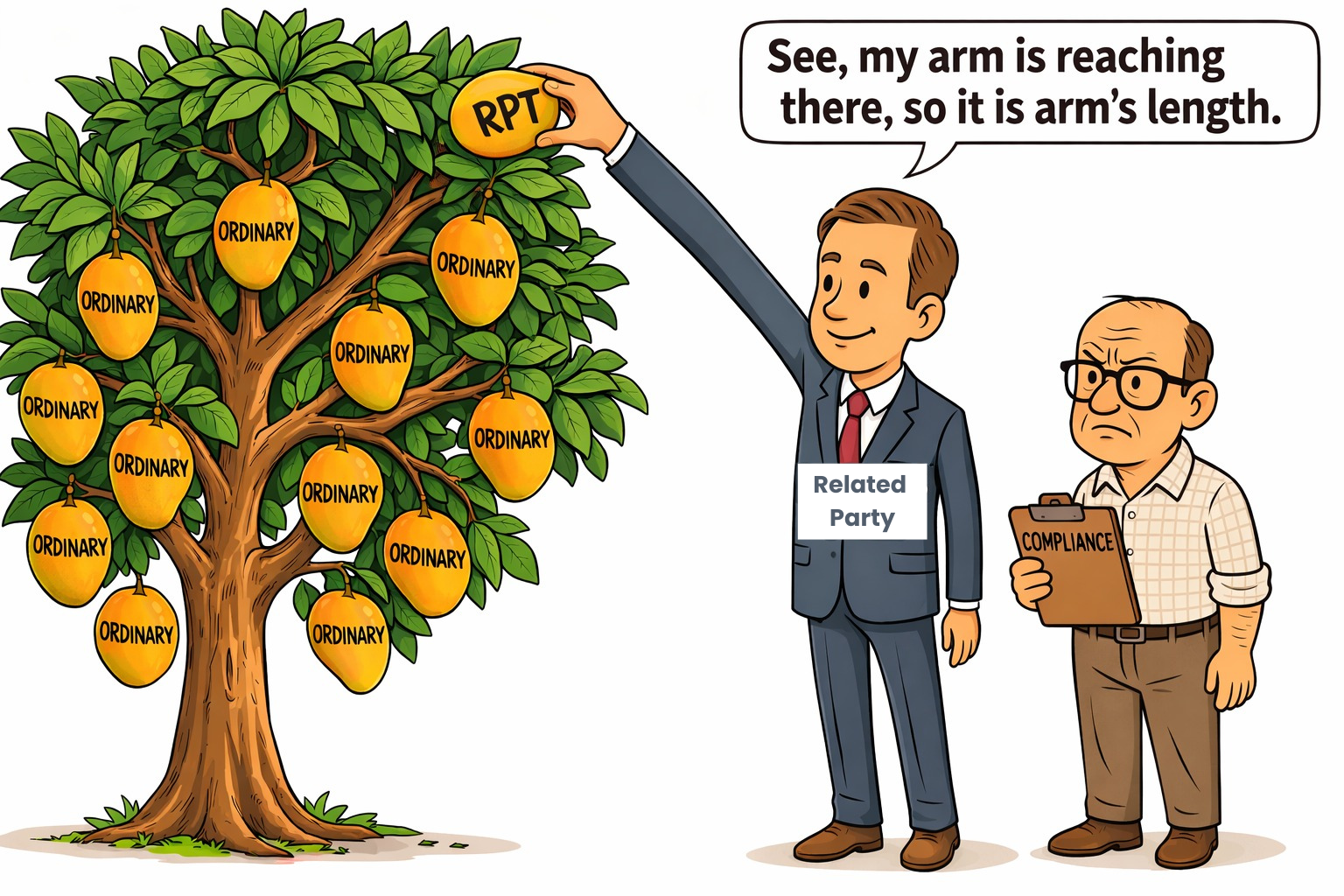

The relevance of “arm’s length assessment” in any related party transaction is non-negotiable. Arm’s length is a consideration that runs across all corporate transactions, including those with unrelated parties. However, where the party itself is at arm’s length, that is, unrelated, the question of the transaction terms being other than arm’s length does not surface. In case of related parties, going by the very nature, the party is not at arm’s length, which is precisely why the need to establish arm’s length arises.

Typically, companies will have hundreds of transactions with unrelated parties. Obviously enough, these hundreds cannot be having a uniform price. It does not require elaboration to say that in business reality, prices have a range, and not a single price. When companies try to justify their impugned transactions with a related party, the practice quite often is to pull one value out of the range of values with unrelated parties, juxtapose that with the proposed RPT, and thus find a justification for the arm’s length.

Is one value out of the range of values sufficient to establish arm’s length? Or does AL have to be the central tendency (that is, a median or modal value) out of the range? This is the point that this article tries to deal with.

Additionally, the article also deals with the meaning of arm’s length beyond pricing, ways of establishing arm’s length where comparables are not available to the company, compliances and consequences pursuant to non arm’s length transactions.

This brings us to the more basic question of what exactly is the “arm’s length terms”, and can it be established based on terms comparable at any specific point of the arm or is it the length of the arm that matters – based on which the middle point of the distribution becomes the ideal indicator of arm’s length.

There is no explicit mention of arm’s length under SEBI LODR. An explanation under section 188 of CA, 2013 refers to the term as follows:

‘The expression “arm’s length transaction” means a transaction between two related parties that is conducted as if they were unrelated, so that there is no conflict of interest.’

The standards on auditing (SA 550 pertaining to Related Parties) also defines the term as:

A transaction conducted on such terms and conditions as between a willing buyer and a willing seller who are unrelated and are acting independently of each other and pursuing their own best interests.

Therefore, in order to consider a transaction to be at an arm’s length, two elements are important:

While considering comparables to establish arm’s length, companies often cherry pick a few transactions at similar terms with non RPs. But how difficult is it to engineer a near favourable transaction with a non RP? These transactions may be termed very differently from the majority of the transactions and yet appear to be comparables.

Illustrating the problem with Outliers

Let us consider this illustration where a company sells a product to its non RP customers at varying prices and its RP at Rs. 651. The management presents 4 transactions of series A (Rs. 650) to C (Rs. 652), done with unrelated parties, as comparable transactions, which establish the RPT to be at arm’s length. The audit committee is obviously not doing a full fledged factual examination, and therefore, may not even get into transactions of series D (Rs. 655) to F (Rs. 657) where most (25) of the transactions are placed.

Given the above diversity, can a transaction at Rs. 651, a value at an extreme left of the above frequency distribution, still be an arm’s length value? The key question is – does arm’s length justification come from just one from a range of values, or from the central tendency in the range?

Arm’s length is a question that is not limited to CA or LODR. Arm’s length considerations span over Income-tax law, GST law, audit framework, etc. In fact, corporate governance is all about transacting with arm’s length valuations. We will not even expect corporate laws to provide detailed guidance on whether the arm of the arm’s length can be long enough to pick an extreme value, or does it have to be the elbow of the arm, that is, the hump in the middle.

The Income Tax Laws provides some guidance

The Income Tax Act provides several methods to determine arm’s length pricing for a transaction, of which, one shall pick the most appropriate:

Where the most appropriate method is any method from (a) to (c) or (e) that leads to several values being possible ALPs, a dataset shall be constructed of such values. This is the guidance we get from Income Tax Rules:

This would easily eliminate the outliers. Cherrypicking of transactions would not work here since the majority of the transactions must be placed as comparables before the audit committee.

What if the transaction is priced at the other extreme of the range, in our example above, say, at a price of Rs. 661. Because the transaction is that of a sale, selling at more than moderate prices is in the interest of the entity. . Yet, the RPT would not be at arm’s length. The Report of the Expert Group on Transfer Pricing Guidelines provides the rationale:

‘It must be emphasised that even a transfer price more favourable to the company than an arm’s length price is problematic. This is so because

(a) valuation is impacted by the possibility that the related party may demand an arm’s length price in the future and

(b) the threat to charge an arm’s length price in future could become a form of poison-pill/blackmail.’

Typically, once a price is determined to be arm’s length, it is arm’s length for either party to the bargain. Arm’s length is all about equilibrium, and equilibrium perfectly balances the interests of either party. The other way of saying this is that what is not arm’s length from the counterparty’s perspective should not usually be arm’s length from the perspective of the other party.

The Indian Judiciary on selection of comparables

The Indian Courts scrutinise comparables used to determine the ALP with a fine tooth comb. In the case of CIT v. Mentor Graphics (Noida) Pvt. Ltd., the ITAT noted how selecting comparables with wide differences in operating margins is faulty. On appeal, the Delhi High Court held that where the profit level indicator of just one comparable out of a set is lower than the tax assessee, the transaction cannot be at arm’s length.

The Global View

The OECD Transfer Pricing Guidelines [Para A.7.3] discourage considering extreme comparables and require the rationale for picking such transactions to be examined. The reason might be a defect in comparability or exceptional conditions being met by an otherwise comparable third party; not dissimilar to engineering favourable transactions with non RP.

The USA’s Electronic Code of Federal Regulations provides that to increase the reliability of comparables, an interquartile range from 25th to 75th percentile of a set of comparables must be used[4]. See Ukraine as well. The Code further provides that arbitrary selection of a comparable that corresponds to an extreme point in the range is unlikely to be at arm’s length.

From the judicial perspective, Courts scrutinize the methodology of determining comparables and disregard those which provide absurd [3] results.[The Coca-Cola Company & Subsidiaries v. Commissioner Of Internal Revenue]

Several other countries consider a range of comparables to determine ALP instead of a single comparable which may fall on the extreme end of a range of comparables. See Norway, Switzerland, Bulgaria.

Price is, but only, an element in the determination of arm’s length criteria for a transaction. The arm’s length assessment, in fact, is based on all the applicable terms of a transaction, as is customarily offered to an unrelated party, vis-a-vis its comparison with a related party.

An illustrative list of checkpoints for assessing arm’s length for various categories of transactions follow:

| Nature of transaction | Relevant factors for assessment | Examples for discussion |

| Granting of loans | Credit profile of the borrower, Interest rate/basis of arriving at interest rate, Tenure, Security and security cover, Penal charges, Other covenants, Cost of funds to the lender company, End use of loan,Outstanding exposures, | Power Bank Ltd. gives loan to A Pvt. Ltd. a company in which its director holds control without any prepayment charges and to other borrowers with similar profiles with heavy prepayment charges. This failure to levy prepayment charges indicates that the transaction may not be at arm’s length. |

| Providing guarantee in favour of RP | Credit worthiness, Past defaults by the debtor,Obligations undertaken pursuant to guarantee agreement,Margin involved | Nofin Ltd. (a NBFC) has a policy of not providing guarantee on behalf of persons with any default in repayment in the past 3 years. However, it provides a guarantee on behalf of its related party which has defaulted twice in the past 3 years. This indicates that the transaction may not be at arm’s length. |

| Availing borrowings | Cost of borrowing Security covenantsPre payment charges | A Ltd. (RP) lends to B Ltd. on the condition of a security cover of 50% as against requirement of 1.25 X for other borrowers. The security cover is grossly lacking; hence, even if the lending/ borrowing rate is arm’s length, the terms of security are not. |

| Sale of goods | Pricing, Credit terms including advance receipts, Other covenants, Alternative options available | A Ltd. provides a credit period of 4 months to all its customers, except its RPs, where the period extends to over a year. Not only this, past records show that the RP has not paid for earlier sales, and new sales are made without interruption. his unusual credit period indicates that the transaction is not at arms’ length, even though at the same price.. |

| Purchase of goods | Pricing, Credit terms including advance payments, Other covenants, Alternative options available | A Ltd. does not pay in advance for purchase of any goods other than those purchased from its RP. This unusual advance payment indicates that the transaction is not at arms’ length even though at the same price. |

| Lease/ sub-lease of premises | Rent charged (including terms for period increment), Security deposit, Tenure; lock-in period, exit rightsApportionment of common maintenance charges | Y Ltd. has provided a part of its premises on rent to X Ltd. (a subsidiary) without security deposit as against the market practice of 3 months’ deposit. While the rental may be in line with the market, the absence of security deposit indicates that the transaction may not be at arm’s length. |

Companies usually pick transactions with non RPs to establish arm’s length of RPTs. But as it so often occurs in group structures, how can arm’s length be established where the transaction is carried out exclusively with the RP? Sharing of premises, software, payment of brand usage fees are all transactions that do not have market comparables; the sole reason for carrying out such transactions is the counterparty being a RP.

Arm’s length terms in case of unique transactions is not a problem that does not have a solution. In fact, even in case of unrelated parties, there are often transactions which are tailored, specific or unique in nature. The assessment of fairness of pricing and terms of the transaction gets into several factors:

The simple rule is: if the RPT is originated, negotiated, priced and finalised using the same rigour, discipline, independence of approach and process as would have been deployed in case of any other transaction, we are doing what the law/regulations expect. On the contrary, if it is the relationship which is playing on the transaction, we clearly have an issue.

RPT controls have become an all-time favourite subject of the regulators. The recent surge in actions against the use of abusive RPT structures makes it evident that the relevance of RPT controls is expected to only increase ahead. With arms’ length considerations forming an integral part of RPT controls, moving from cherrypicking comparables to presenting appropriate comparables at the median of the range has become all the more important.

[1] Sec. 92C of the Income Tax Act, 1961 read with rule 10B of the Income Tax Rules, 1962 corresponding to section 165

[2] Rule 10CA(4) of the Income Tax Rules, 1962

[3] Rule 10CA(6) of the Income Tax Rules, 1962

[4] 26 CFR § 1.482-1(2)(iii)(C)

See our other resources:

Vinita Nair, Joint Managing Partner and Ankit Singh Mehar, Assistant Manager | corplaw@vinodkothari.com

Updated on May 4, 2026

A 15th March 2026 Press Note from Department for Promotion of Industry and Internal Trade (DPIIT) implements the cabinet decision to align investments from land-border countries (LBCs) with “beneficial owner” definition of PMLA. Accordingly, where investments come from a non-LBC, where beneficial ownership traces back to LBC, either to a citizen of LBC or an entity set up there, the investments will be allowed only in approval mode. In our view, even if there are multiple such citizens or entities, the amendment requires an aggregation of the investments of all LBC citizens or entities.

The 15th March DPIIT Press note 2 (‘PN2’) was preceded by a decision of Central Government, on March 10, 2026 (‘CG press release’) relaxing the restrictions placed in 2020 on FDI from countries sharing land-border with India (LBC) by (a) prescribing a strict approval timeline of 60 days in case of specified sectors/activities of manufacturing in capital goods, electronic capital goods, electronic components etc and (b) by allowing certain investments under automatic route where the investors have non-controlling LBC Beneficial Ownership of up to 10%. The objective is to facilitate ease of doing business and attract FDI inflows especially in critical sectors.

DPIIT issued Press Note 2 of 2026 dated March 15, 2026 (PN2) amending the Consolidated FDI Policy with respect to eligible investors (Para 3.1.1). PN2 shall take effect from the date of notification of amendment in NDI Rules. A corresponding amendment in Rule 6 of the FEMA (Non-Debt Instruments) Rules, 2019 (‘NDI Rules’) was notified and published in gazette on May 2, 2026. Accordingly, the amendment takes effect from May 2, 2026.

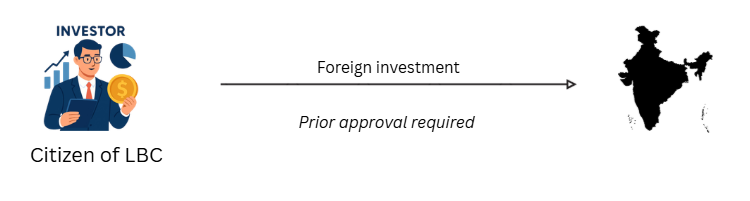

Since April 2020, in terms of rule 6 of NDI Rules and FDI Policy, prior approval of the government is required for any investment made by an entity from LBC or where the beneficial owner of an investment into India (a) – is situated in LBC; or (b) is a citizen of such LBC. Likewise, any transfer of ownership of existing or future FDI that results in the beneficial ownership of the investment shifting to a person who is a citizen of, or situated in, a LBC also requires prior government approval.

These requirements were notified pursuant to Press Note No 3 dated April 17, 2020 and subsequent notification of FEMA (Non Debt Instruments) Amendment Rules, 2020. Refer to our earlier write-up titled India seals its borders to corporate acquisitions dealing with the said press note. Our earlier you-tube video covering the overview of FDI can be accessed here.

In order to meet the objectives of Aatmanirbhar Bharat and increase FDI inflows, India has decided to revisit the restrictions placed during Covid pandemic to curb opportunistic takeovers/acquisitions by Chinese companies. In this article we discuss the changes approved and notified by way of PN2 and amendments made in NDI Rules effective May 2, 2026.

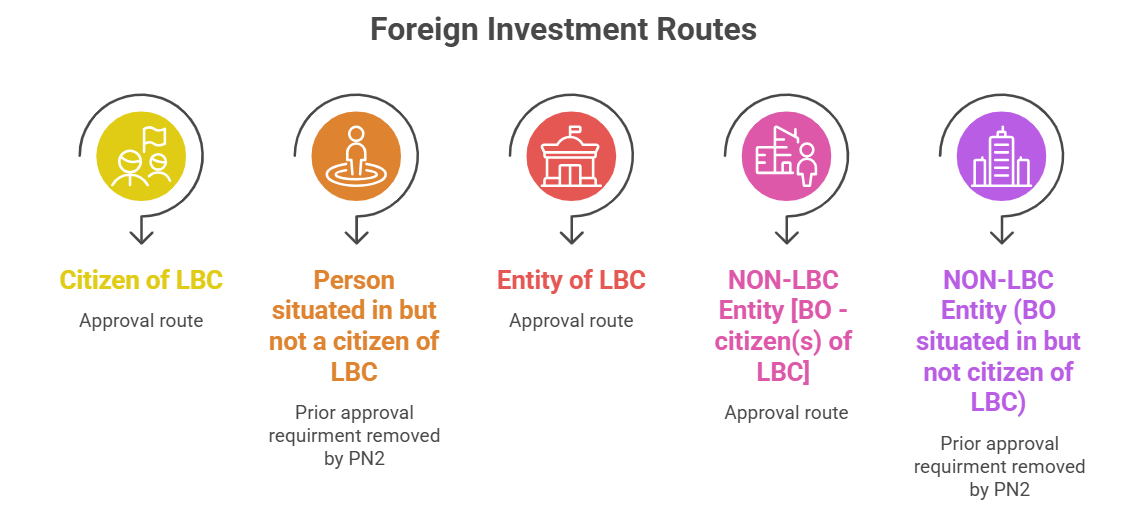

Prior approval of the government is now required for any investment made by an entity or citizen from LBC. The approval requirement also extends to investments made in India where the beneficial owner of an investment into India is a citizen of LBC.

The restriction arising on account of being ‘situated in LBC’ has been deleted. This relaxes the requirement for individuals of different nationalities situated in LBC investing in India or receiving ESOPs from Indian companies, as they will no longer require government approval.

Accordingly, the amended position is as under:

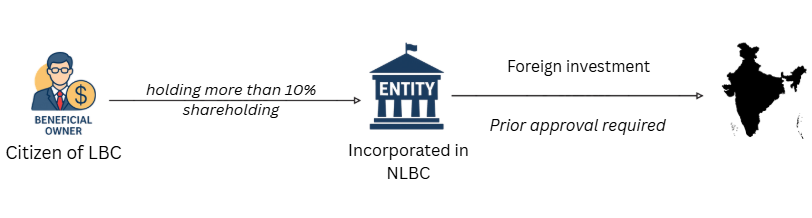

Prior approval of the government is now required for any investment by PROI from non-LBC, where the beneficial owner of an investment into India is a citizen/entity of LBC.

Meaning of ‘beneficial owner of an investment into India’:

Let us first understand the meaning of “investor entity”.

It means the beneficial owner(s) of the investor entity incorporated or registered in a country other than LBC. Manner of identifying the beneficial owner(s) of the investor entity will be as discussed below in Clause 4.

Prior approval is required for any direct or indirect transfer of ownership of existing or future FDI in an Indian entity that results in the beneficial ownership of the investment into India shifting to an entity or a citizen of LBC.

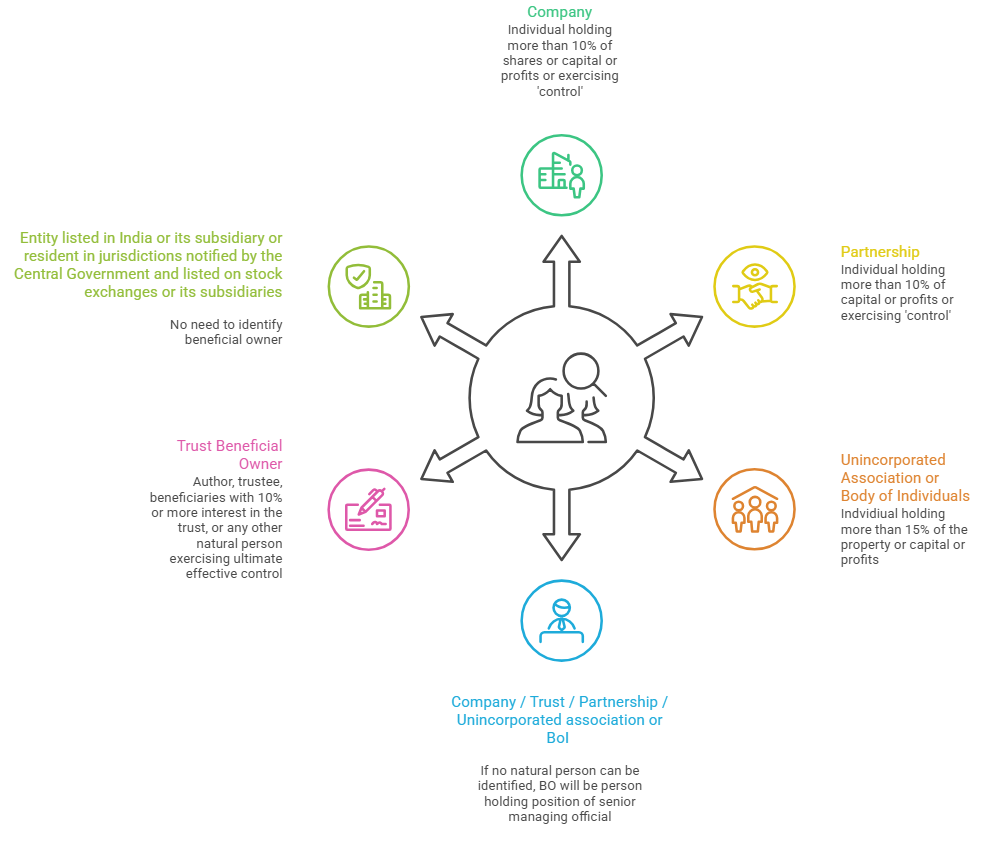

As per PN 2 and NDI Rules, the manner of identifying BO is aligned with Section 2(1)(fa) of the Prevention of Money-laundering Act, 2002 read with Rule 9 (3) of Prevention of Money Laundering (Maintenance of Records) Rules, 2005 (PML Rules). The reference to PML rules is mainly for the thresholds (refer below).

BO will be construed as vested with the LBC if the citizen(s) of LBC or entity (ies) incorporated/ registered with LBC has/ have the ability to hold rights/ entitlements in excess of thresholds under PML rules or exercise control over the investor entity or ultimate control over the investee i.e the Indian entity in any manner:

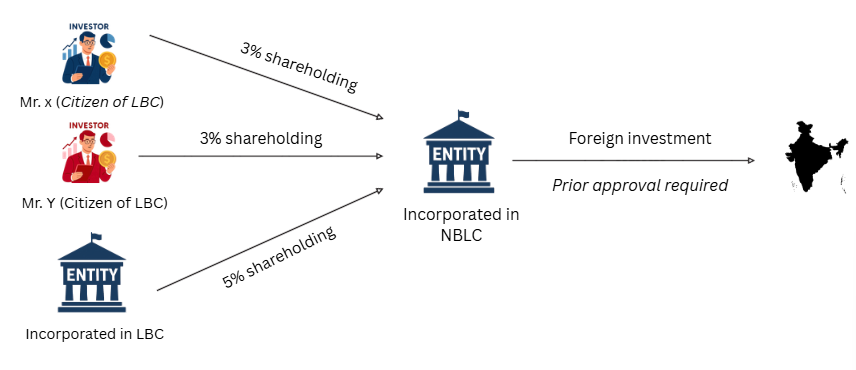

Whether holdings by different citizens or entities of LBC to be aggregated?

In our view, yes. The intent is to allow investments from entities where the investors from LBC hold a non-controlling interest. Therefore, one will have to consider all investments put together. The approval requirements have been further clarified by way of following illustrations:

Illustration 1

Illustration 2

Illustration 3

Illustration 4

One might argue that if neither of the persons referred above i.e. Mr. X or Mr. Y or Entity incorporated in LBC, are qualifying as ‘beneficial owners’ under PMLA Rules on a standalone basis, then why do we need to aggregate their shareholding?

Here, reference needs to be made to the language of the proviso to Para 3.1.1.(c) of the FDI Policy and Explanation 2 to NDI Rules, which requires considering the rights/entitlements held – directly or indirectly, individually or cumulatively, independently or collectively, whether acting together or otherwise. The language seems to indicate that aggregation needs to be done irrespective of whether the person in question is acting independently or collectively or whether they are acting together or otherwise. Hence, in our view, one has to consider if investors of the Non-LBC with BO from LBC cumulatively hold in excess of the prescribed thresholds.

As per Para 3.1.1(d) of the amended FDI Policy, investments from an investor entity having any direct or indirect ownership by a citizen or an entity of LBC not requiring prior government approval shall be subject to reporting requirements as per the SOP laid down by DPIIT and prescribed by RBI.

The amended proviso to Rule 6 (a) of the NDI Rules clarifies that any Multilateral Bank (like World Bank, Asian Development Bank, Asian Infrastructure Investment Bank, New Development Bank etc.) or Fund (like International Monetary Fund, International Fund for Agricultural Development etc) of which India is a member shall not be treated as an entity of a particular country, nor any country would be treated as beneficial owner of any investments made by such Bank/Fund in India. This was not provided in PN2 and clarified vide amendment in NDI Rules.

Presently, the timeline for obtaining government approval for FDI ranges between 12–14 weeks.

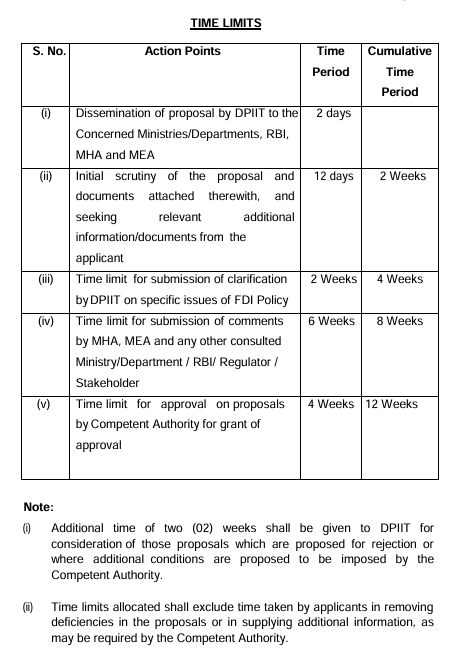

Source: Annexure V of SOP for Processing FDI Proposals

In cases where the investee entities are engaged in the specified sectors / activities concerning manufacturing of Capital goods, Electronic capital goods, Electronic components, Polysilicon and ingot-wafer etc. a timeline of 60 days shall be adhered to for government approval, in view of the criticality. The list will be provided by DPIIT. The majority shareholding and control of such Investee entities should be with the residents.

The Government will continue to assess the proposals on a case to case basis and accord approval. Recently, an electronics manufacturer company received MEITY approval for receiving investment of 26% in a joint venture from a Chinese investor.

As discussed in the CG press release, the existing restrictions to cases where LBC investors only have non-strategic, non-controlling interests were seen as adversely affecting investment flows from investors including global funds such as PE/ VC funds. By loosening the said restrictions cautiously, greater FDI inflows and speedier fundraising can be encouraged, particularly into startups and deep techs while protecting the nation’s security interests. The relaxed norms aim to increase access to technology, facilitate ease of doing business for Indian entities and strengthen India’s position as an attractive destination for investment and manufacturing.

Refer our other resources on FDI here