RPTs: Do extreme comparables distort arm’s length?

– Saloni Khant, Executive | corplaw@vinodkothari.com

The relevance of “arm’s length assessment” in any related party transaction is non-negotiable. Arm’s length is a consideration that runs across all corporate transactions, including those with unrelated parties. However, where the party itself is at arm’s length, that is, unrelated, the question of the transaction terms being other than arm’s length does not surface. In case of related parties, going by the very nature, the party is not at arm’s length, which is precisely why the need to establish arm’s length arises.

Typically, companies will have hundreds of transactions with unrelated parties. Obviously enough, these hundreds cannot be having a uniform price. It does not require elaboration to say that in business reality, prices have a range, and not a single price. When companies try to justify their impugned transactions with a related party, the practice quite often is to pull one value out of the range of values with unrelated parties, juxtapose that with the proposed RPT, and thus find a justification for the arm’s length.

Is one value out of the range of values sufficient to establish arm’s length? Or does AL have to be the central tendency (that is, a median or modal value) out of the range? This is the point that this article tries to deal with.

Additionally, the article also deals with the meaning of arm’s length beyond pricing, ways of establishing arm’s length where comparables are not available to the company, compliances and consequences pursuant to non arm’s length transactions.

This brings us to the more basic question of what exactly is the “arm’s length terms”, and can it be established based on terms comparable at any specific point of the arm or is it the length of the arm that matters – based on which the middle point of the distribution becomes the ideal indicator of arm’s length.

Meaning of arm’s length: How the regulators define the term?

There is no explicit mention of arm’s length under SEBI LODR. An explanation under section 188 of CA, 2013 refers to the term as follows:

‘The expression “arm’s length transaction” means a transaction between two related parties that is conducted as if they were unrelated, so that there is no conflict of interest.’

The standards on auditing (SA 550 pertaining to Related Parties) also defines the term as:

A transaction conducted on such terms and conditions as between a willing buyer and a willing seller who are unrelated and are acting independently of each other and pursuing their own best interests.

Therefore, in order to consider a transaction to be at an arm’s length, two elements are important:

- The transaction is undertaken on terms similar to those between unrelated parties, and

- There is no conflict of interest, that is, the transaction is undertaken independently, in the best interest of the entities in question.

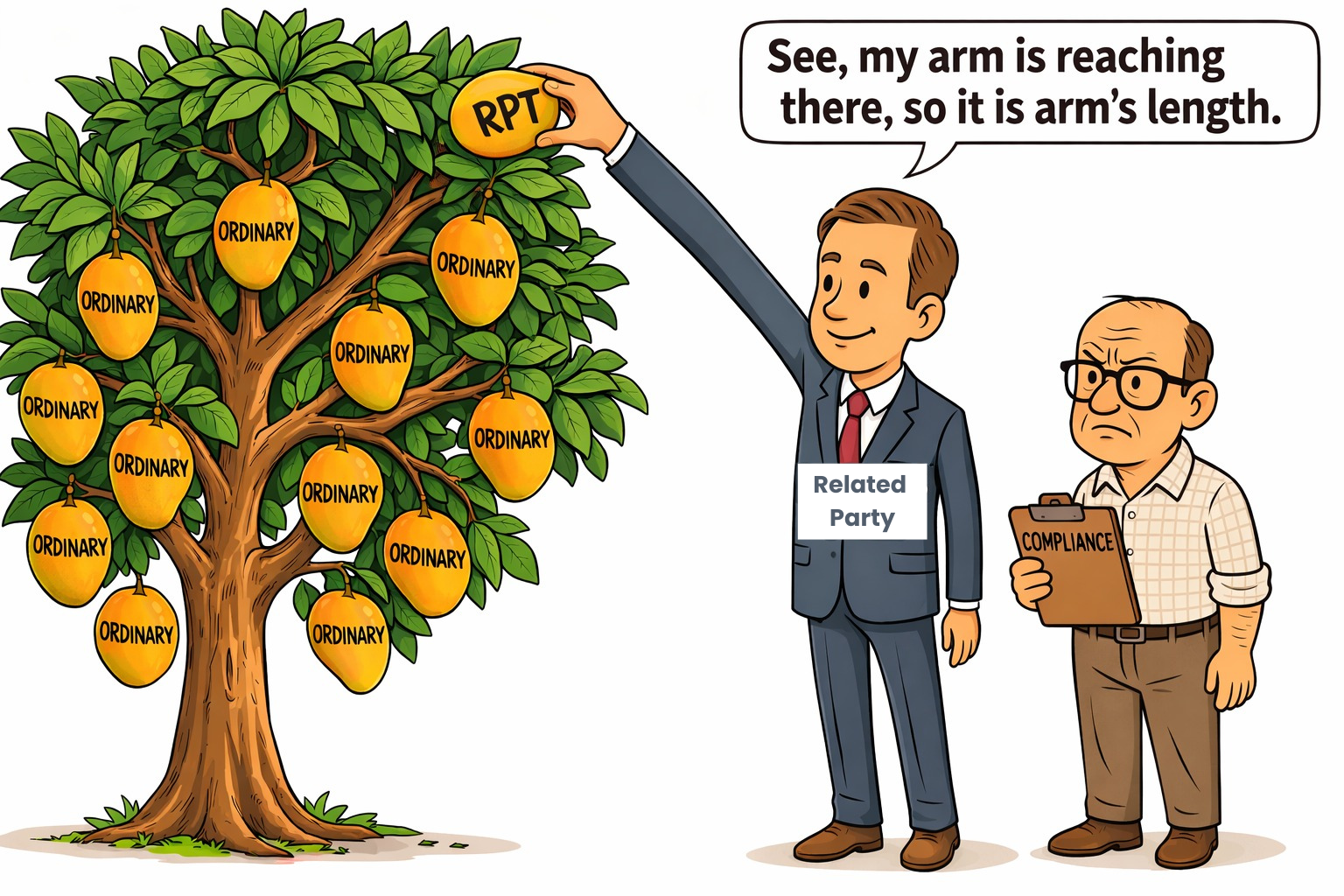

Similarity of terms with unrelated parties: are outliers good comparables?

While considering comparables to establish arm’s length, companies often cherry pick a few transactions at similar terms with non RPs. But how difficult is it to engineer a near favourable transaction with a non RP? These transactions may be termed very differently from the majority of the transactions and yet appear to be comparables.

Illustrating the problem with Outliers

Let us consider this illustration where a company sells a product to its non RP customers at varying prices and its RP at Rs. 651. The management presents 4 transactions of series A (Rs. 650) to C (Rs. 652), done with unrelated parties, as comparable transactions, which establish the RPT to be at arm’s length. The audit committee is obviously not doing a full fledged factual examination, and therefore, may not even get into transactions of series D (Rs. 655) to F (Rs. 657) where most (25) of the transactions are placed.

Given the above diversity, can a transaction at Rs. 651, a value at an extreme left of the above frequency distribution, still be an arm’s length value? The key question is – does arm’s length justification come from just one from a range of values, or from the central tendency in the range?

Arm’s length is a question that is not limited to CA or LODR. Arm’s length considerations span over Income-tax law, GST law, audit framework, etc. In fact, corporate governance is all about transacting with arm’s length valuations. We will not even expect corporate laws to provide detailed guidance on whether the arm of the arm’s length can be long enough to pick an extreme value, or does it have to be the elbow of the arm, that is, the hump in the middle.

The Income Tax Laws provides some guidance

The Income Tax Act provides several methods to determine arm’s length pricing for a transaction, of which, one shall pick the most appropriate:

- Comparable Uncontrolled Price Method: Price charged in a comparable uncontrolled transaction is identified and adjusted for differences, if any.

- Resale price method: price at which property/services obtained from an associated enterprise is resold to an unassociated enterprise – adjusted by a normal gross profit margin in a CU transaction, expenses, and differences, if any.

- Cost plus method: Direct/indirect costs are increased by an adjusted mark-up to such costs. Adjusted mark-up is normal gross profit mark-up arising in an uncontrolled comparable transaction adjusted for differences, if any.

- Profit split method: Combined net profit is split amongst enterprises in proportion to relative contributions. Relative contribution is evaluated on the basis of reliable external market data – unrelated enterprises performing comparable functions.

- Transactional net margin method: The net profit margin (computed in relation to costs incurred, sales effected, etc.) arising in a comparable uncontrolled transaction is adjusted for differences.[1]

Where the most appropriate method is any method from (a) to (c) or (e) that leads to several values being possible ALPs, a dataset shall be constructed of such values. This is the guidance we get from Income Tax Rules:

- If the dataset consists of at least 6 values, a range of ALPs shall be considered from the 35th to the 65th percentile of this range.[2]

- If the actual price of the transaction is outside this range, the median of the range shall be considered as the ALP for the purpose of tax assessment[3].

This would easily eliminate the outliers. Cherrypicking of transactions would not work here since the majority of the transactions must be placed as comparables before the audit committee.

What if the transaction is priced at the other extreme of the range, in our example above, say, at a price of Rs. 661. Because the transaction is that of a sale, selling at more than moderate prices is in the interest of the entity. . Yet, the RPT would not be at arm’s length. The Report of the Expert Group on Transfer Pricing Guidelines provides the rationale:

‘It must be emphasised that even a transfer price more favourable to the company than an arm’s length price is problematic. This is so because

(a) valuation is impacted by the possibility that the related party may demand an arm’s length price in the future and

(b) the threat to charge an arm’s length price in future could become a form of poison-pill/blackmail.’

Typically, once a price is determined to be arm’s length, it is arm’s length for either party to the bargain. Arm’s length is all about equilibrium, and equilibrium perfectly balances the interests of either party. The other way of saying this is that what is not arm’s length from the counterparty’s perspective should not usually be arm’s length from the perspective of the other party.

The Indian Judiciary on selection of comparables

The Indian Courts scrutinise comparables used to determine the ALP with a fine tooth comb. In the case of CIT v. Mentor Graphics (Noida) Pvt. Ltd., the ITAT noted how selecting comparables with wide differences in operating margins is faulty. On appeal, the Delhi High Court held that where the profit level indicator of just one comparable out of a set is lower than the tax assessee, the transaction cannot be at arm’s length.

The Global View

The OECD Transfer Pricing Guidelines [Para A.7.3] discourage considering extreme comparables and require the rationale for picking such transactions to be examined. The reason might be a defect in comparability or exceptional conditions being met by an otherwise comparable third party; not dissimilar to engineering favourable transactions with non RP.

The USA’s Electronic Code of Federal Regulations provides that to increase the reliability of comparables, an interquartile range from 25th to 75th percentile of a set of comparables must be used[4]. See Ukraine as well. The Code further provides that arbitrary selection of a comparable that corresponds to an extreme point in the range is unlikely to be at arm’s length.

From the judicial perspective, Courts scrutinize the methodology of determining comparables and disregard those which provide absurd [3] results.[The Coca-Cola Company & Subsidiaries v. Commissioner Of Internal Revenue]

Several other countries consider a range of comparables to determine ALP instead of a single comparable which may fall on the extreme end of a range of comparables. See Norway, Switzerland, Bulgaria.

Other aspects of arm’s length RPTs

Price is, but only, an element in the determination of arm’s length criteria for a transaction. The arm’s length assessment, in fact, is based on all the applicable terms of a transaction, as is customarily offered to an unrelated party, vis-a-vis its comparison with a related party.

An illustrative list of checkpoints for assessing arm’s length for various categories of transactions follow:

| Nature of transaction | Relevant factors for assessment | Examples for discussion |

| Granting of loans | Credit profile of the borrower, Interest rate/basis of arriving at interest rate, Tenure, Security and security cover, Penal charges, Other covenants, Cost of funds to the lender company, End use of loan,Outstanding exposures, | Power Bank Ltd. gives loan to A Pvt. Ltd. a company in which its director holds control without any prepayment charges and to other borrowers with similar profiles with heavy prepayment charges. This failure to levy prepayment charges indicates that the transaction may not be at arm’s length. |

| Providing guarantee in favour of RP | Credit worthiness, Past defaults by the debtor,Obligations undertaken pursuant to guarantee agreement,Margin involved | Nofin Ltd. (a NBFC) has a policy of not providing guarantee on behalf of persons with any default in repayment in the past 3 years. However, it provides a guarantee on behalf of its related party which has defaulted twice in the past 3 years. This indicates that the transaction may not be at arm’s length. |

| Availing borrowings | Cost of borrowing Security covenantsPre payment charges | A Ltd. (RP) lends to B Ltd. on the condition of a security cover of 50% as against requirement of 1.25 X for other borrowers. The security cover is grossly lacking; hence, even if the lending/ borrowing rate is arm’s length, the terms of security are not. |

| Sale of goods | Pricing, Credit terms including advance receipts, Other covenants, Alternative options available | A Ltd. provides a credit period of 4 months to all its customers, except its RPs, where the period extends to over a year. Not only this, past records show that the RP has not paid for earlier sales, and new sales are made without interruption. his unusual credit period indicates that the transaction is not at arms’ length, even though at the same price.. |

| Purchase of goods | Pricing, Credit terms including advance payments, Other covenants, Alternative options available | A Ltd. does not pay in advance for purchase of any goods other than those purchased from its RP. This unusual advance payment indicates that the transaction is not at arms’ length even though at the same price. |

| Lease/ sub-lease of premises | Rent charged (including terms for period increment), Security deposit, Tenure; lock-in period, exit rightsApportionment of common maintenance charges | Y Ltd. has provided a part of its premises on rent to X Ltd. (a subsidiary) without security deposit as against the market practice of 3 months’ deposit. While the rental may be in line with the market, the absence of security deposit indicates that the transaction may not be at arm’s length. |

How about unique transactions which do not have comparables?

Companies usually pick transactions with non RPs to establish arm’s length of RPTs. But as it so often occurs in group structures, how can arm’s length be established where the transaction is carried out exclusively with the RP? Sharing of premises, software, payment of brand usage fees are all transactions that do not have market comparables; the sole reason for carrying out such transactions is the counterparty being a RP.

Arm’s length terms in case of unique transactions is not a problem that does not have a solution. In fact, even in case of unrelated parties, there are often transactions which are tailored, specific or unique in nature. The assessment of fairness of pricing and terms of the transaction gets into several factors:

- Burden and benefit analysis: What is the sacrifice, burden or cost incurred by either party to the transaction, and what is the benefit obtained by either. The idea is to at least equate the benefit with the burden. Consider, for example, the use of brand name or flagship name. The basis for charging a licensing fee is that the user entity gets the advantage of the reputation, brand value or goodwill associated with the flagship name or brand. Instead of a complete greenfield start, it gets the backing of an established name. Hence, the analysis will be: what is the profitability, revenue potential, borrowing cost or other outgo of the entity using the name, as compared to other similar starters which do not have the benefit of the name.

- Cost split: In case of sharing of resources, the possible solution may be to split the costs on the basis of a relevant parameter. The relevant parameter will differ on the basis of the expense: for example, in case of using office space, it may be the headcount. In the case of IT resources, it may be transactional volume. Cost allocation techniques may be used here. Is it important to charge a mark-up on the costs? In our view, no, because neither party is doing resource sharing with a view to mark profits.

- Benchmarking studies: If there are instances of similar or nearly similar transactions, it may be useful to benchmark the transaction against industry similars. The availability of data may be a challenge; but sometimes, even an anecdotal evidence may be useful. This is precisely how one would have got an assurance of fair pricing: for example, if you are engaging a consultant for a complex, one-off project, you would get comfort that you are not being over-charged by asking a few peers.

The simple rule is: if the RPT is originated, negotiated, priced and finalised using the same rigour, discipline, independence of approach and process as would have been deployed in case of any other transaction, we are doing what the law/regulations expect. On the contrary, if it is the relationship which is playing on the transaction, we clearly have an issue.

Conclusion

RPT controls have become an all-time favourite subject of the regulators. The recent surge in actions against the use of abusive RPT structures makes it evident that the relevance of RPT controls is expected to only increase ahead. With arms’ length considerations forming an integral part of RPT controls, moving from cherrypicking comparables to presenting appropriate comparables at the median of the range has become all the more important.

[1] Sec. 92C of the Income Tax Act, 1961 read with rule 10B of the Income Tax Rules, 1962 corresponding to section 165

[2] Rule 10CA(4) of the Income Tax Rules, 1962

[3] Rule 10CA(6) of the Income Tax Rules, 1962

[4] 26 CFR § 1.482-1(2)(iii)(C)

See our other resources:

Leave a Reply

Want to join the discussion?Feel free to contribute!