SEBI removes redundancy to ease compliance

– Team Corplaw | corplaw@vinodkothari.com

See our other resources:

– Team Corplaw | corplaw@vinodkothari.com

See our other resources:

– Payal Agarwal, Partner | Vinod Kothari & Company | corplaw@vinodkothari.com

Year 2025 will go down in the history of independent India as the year of the most brisk legislative activity – mostly by way of consolidation of some of the major laws. Income Tax Act, labour laws, securities markets, IBC, RBI Regulations etc – everywhere, we find the lawmakers have been quite busy themselves, of course making the subjects and companies even busier. The Securities Market Code (SMC) has been introduced in the Lok Sabha, pursuant to the announcement in the Union Budget 21-22. Divided into a total of 18 chapters, the SMC seeks to consolidate and repeal the following:

The Code reflects a structural consolidation exercise, however, also with an underpinning attempt to make rule making more practical and principled, providing for investor protection by reintroducing ombudsman, providing legal sanctity to inter-regulatory coordination, covering complex securities transactions, etc. Further, the gazette notifications issued in relation to the aforesaid Acts are also proposed to be made a part of the Code.

– Vinita Nair and Saloni Khant | corplaw@vinodkothari.com

– Updated on May 3, 2025

Being the 10th largest[1] in the world, the Indian Insurance market grows at 10-15% annually but insurance penetration is only at 3.7% of the GDP[2] as against the global average of 7.3%. With a view to boost growth in the sector and implement the vision of ‘”Insurance for All by 2047’, amendments in the existing insurance laws were placed before the public for consultation in November, 2024. Following the due process of legislation, the draft bill underwent several changes, was passed by both the houses of the parliament, assented to by the president and finally notified in the Official Gazette as the Sabka Bima Sabki Raksha (Amendment Of Insurance Laws) Act, 2025 (“Amendment Act”) on December 21, 2025. The Amendment Act, that amends the Insurance Act, 1938, Life Insurance Corporation Act, 1956 and Insurance Regulatory and Development Authority Act, 1999, introduces fundamental reforms by liberalising foreign investments and reducing capital requirements but at the same time, strengthens regulatory oversight on the market participants with additional measures to protect the interest of the policyholders.

The Amendment Act became effective from February 5, 2026. The amendment relating to prohibition on common MD and officers among insurance companies, banking companies and investment companies (Section 32A of the Insurance Act), has not been made effective, in view of industry representation made to IRDA, refer the discussion below.

Read more →– Sikha Bansal and Nitu Poddar | corplaw@vinodkothari.com

– Published in Moneylife on December 16, 2025

The Indian Stamp Act, 1899 (“Stamp Act”) was amended in 2019 by the Finance Act, 2019 (“Amendment”), broadly – to introduce a unified mechanism for levy and collection stamp duty on issuance and transfer of securities, by insertion of sections 4(3), 9A, 9B, 62A, 73A, Article 56A among others. That Amendment introduced a unified, nationally applicable stamp duty framework that prescribes 0.005% as the duty on the issue of shares, to be collected centrally through depositories. This is how the era of dematerialised issuance of capital market instruments was ushered and furthered.

After more than 5 years of the Amendment, Delhi-based companies have begun receiving notices from the Delhi Revenue Department questioning the stamp duty paid on the issue of shares. The Department has, in fact, issued Letters to the depositories [NSDL, CDSL] asserting that stamp duty ought to have been paid at the rate of 0.1% on the value of shares issued, based on Article 19 of the State stamp law, disregarding the 2019 Amendment, and prohibiting the depositories from collecting stamp duties on their behalf.

The State move has triggered uncertainty regarding share issuances effected after 1 July 2020, when the amended Stamp Act came into force. The communications issued by the Revenue Department of Delhi , with an ask of duty which is 20 times more than the rate approved by the Parliament, disregard and challenge this uniform regime, leaving the companies grappling with compliance ambiguity and the risk of retrospective financial exposure, despite having followed the statutory mechanism approved by the Parliament.

If other States start asking for duties as per their respective laws, the intended harmonisation of stamp laws will soon turn into a cacophony!

This article touches upon the objective of the Amendments and looks for potential answers on the way forward.

Pursuant to the Amendment, sections 9A and 9B were introduced in the Stamp Act. Section 9A is a non-obstante provision, which mandates that the depositories shall collect the duty on behalf of the State Government (“SG”) from the issuer, on the total market value of the securities. Similar provisions are there to deal with sale or transfer of securities. Section 9A(2) provides for levy of stamp duty as per the applicable rates given in Schedule I. Currently, as per Article 19 read with Article 56A of Schedule I, the stamp duty on the issue of shares is fixed at 0.005%.

Notably, section 9A(3) expressly prohibits SGs from levying or collecting stamp duty on instruments covered under Section 9A(1), including the issue/sale/transfer of shares. Therefore, it is clear from a reading of bare provisions of the Stamp Act, that it was a conscious call to unify the mechanism for levy and collection of stamp duties, albeit, the right of the SGs to receive the duty remains protected – as the depositories will collect the stamp duty, only on behalf of the SGs.

The rationale and intent behind the Amendments was given in the Statement of Objects and Reasons in the Finance Bill, 2019 as follows:

“13. Clauses 11 to 21 of the Bill seek to amend the Indian Stamp Act, 1899 for levy and administration of stamp duty on securities market instruments by the States at one place through one agency, viz., through Stock Exchanges or its Clearing Corporation or Depositories on one instrument, and for appropriately sharing the same with respective State Governments based on State of domicile of the ultimate buying client.”

The Press Release by the Ministry of Finance dated Feb 21, 2019 states that, “In order to facilitate ease of doing business and to bring in uniformity and affordability of the stamp duty on securities across States and thereby build a pan-India securities market, the Central Government, after due deliberations, in exercise of powers under Entry 91 of the List I and Entry 44 of List III of the 7th Schedule of Indian Constitution, has decided to amend the Indian Stamp Act, 1899 to create the legal and institutional mechanism to enable states to collect stamp duty on securities market instruments at one place by one agency (through Stock Exchanges or Clearing Corporations authorized by it or by the Depositories) on one Instrument and develop a mechanism for appropriately sharing the stamp duty with relevant State Governments.”

Further clarification on implementation of the Amendments was given vide Press Release dated June 30, 2020 which also reiterated the above and indicated that the Amendments were done after due consultation with State Governments.

See also, RBI Press Release dated July 1, 2020.

As it appears from the aforesaid Press Release, and also the Budget Speech for 2018-19 by the then Finance Minister, Shri Arun Jaitely, necessary consultation has been done with the States before amending the Central Act. Section 9A(4) specifically mandates that the 2019 Rules governing collection of stamp duty through depositories be framed in consultation with SGs

The issue, as it appears, involves a question of constitutionality. The Centre has enacted the Amendments citing “Entry 91 of List I: rates of stamp duty on instruments including transfer of shares and debentures” and “Entry 44 of List III: stamp duties other than judicial stamps, excluding “rates of stamp duty”.

However, the Delhi Revenue Department appears to be disregarding the Amendments possibly on the following grounds:

Now, the question of constitutionality is itself a complicated matter, and is subject to judicial examination and interpretation. However, until the question of constitutionality is settled, any act/omission to act should ideally be judged on the basis of these two very important principles: One, Central law prevails over State laws, and two, presumption of validity of laws, as discussed below.

First, that in case of inconsistency, if at all, between the law prescribed by the Centre and law prescribed by the State, the Central law prevails. Once Parliament legislates within its competence, and particularly when the legislation is later in time and designed to create a comprehensive framework, the Central law prevails in case of conflict. This is also referred to as doctrine of repugnancy. The Supreme Court has consistently affirmed the primacy of Parliamentary legislation in cases of overlap or conflict.

See an exhaustive discussion on the doctrine of repugnancy in Forum for People’s Collective Efforts (FPCE) & Anr. v. the State of West Bengal and Others (2021). See also, I.T.C. Ltd. Etc v. State Of Karnataka (1985), in which the Supreme Court also observed that, “There may also be cases where despite an entry being in List II, the Parliament may under the provisions of Art. 246(3) take over that particular field and legislate on that subject which will debar the late legislative from adding or passing any such legislation which has been taken over under Act. 246(3).” See also, Baijnath Kedia v. State Of Bihar(1969).

Applied to the present context, the intent behind the 2019 amendment was unambiguous – to harmonise stamp duty on securities across India and eliminate State-level divergences that impede market efficiency.

Secondly, it is a well-established principle that there is a presumption always in favour of constitutionality of law, until a competent court declares it unconstitutional. The onus to prove otherwise is on the person challenging it. In Chiranjit Lal Chowdhuri v. Union of India and Others, the Supreme Court observed, “ . . .the presumption is always in favour of the constitutionality of an enactment, and the burden is upon him who attacks it to show that there has been a clear transgression of the constitutional principles.” See also, Nand Kishore v. State of Punjab, Dharmendra Kirthal v. State of Uttar Pradesh and Another.

Therefore, in so far the question of constitutionality of the Stamp Amendments is concerned, the said Amendments have not been struck down by any court of law. Hence, there shall be a presumption that the Amendments are constitutionally valid and the stakeholders remain bound by the central framework.

The contention that depositories require authorisation from individual State Governments is misplaced. Depositories collect stamp duty not as agents appointed by States but as statutory collecting authorities designated by Parliament under the Act read with Rules. Once Parliament has prescribed the mode of collection, State consent is not required.

Operationally, no. Companies issuing shares in dematerialised form have no option but to pay stamp duty at the rate of 0.005 percent. Depositories auto-calculate and collect duty at 0.005% based on the consideration value, leaving no discretion to issuers. The stamp duty calculator on the website of the depository also calculates the duty at the rate of 0.005% of the issue size. Further, CDSL’s SOP states, “the issuers have to remit applicable stamp duty to CDSL in the designated bank account before executing the corporate action in the system. If sufficient stamp duty amount is not present against the issuer, then the corporate action setup/ file uploaded by RTA remains under ‘Pending for Stamp Duty’ Status in CDSL system. In case of issuance stamp duty is applicable @0.005% of the consideration value. A stamp duty calculator has also been provided on the website for the purpose of applicable stamp duty. “

From the discussion above, it is clear that:

As such, all concerned are bound by such law. No fault can lie with the issuer companies which simply complied by the Centre-enacted law, and paid duty as per directions of authorities.

Given the situation, the companies which receive any similar notice can take the following steps (to be evaluated on a case-by-case basis):

The unified stamp duty framework introduced in 2020 is a considered step calling for centralisation of duty collection on securities. As the communications by the Delhi Revenue Department attempt to enforce a pre-2020 State rate, it is quite possible that the issue goes for judicial determination, mainly on the grounds of constitutionality. In any case, until the question of constitutionality is determined, the presumption of validity exists in favour of the Amendments.

Our other resources:

– Payal Agarwal | payal@vinodkothari.com

– Aligns intra group exposure norms with Large Exposure Framework; junks a 2016 framework for “large borrowers”

On 4th December, 2025, less than a week after the massive consolidation exercise of RBI regulations, the RBI carried out amendments vide Reserve Bank of India (Commercial Banks – Concentration Risk Management) Amendment Directions, 2025, thus amending the recently consolidated Reserve Bank of India (Commercial Banks – Concentration Risk Management) Directions, 2025.

A track change version of the Reserve Bank of India (Commercial Banks – Concentration Risk Management) Directions, 2025, as amended vide the present Amendment Directions can be accessed here.

Refer to our other resources here:

– Kunal Gupta | corplaw@vinodkothari.com

– Team Corplaw | corplaw@vinodkothari.com

When it comes to insider trading regulation breaches, it is the adverse headline value which is far more punitive than the amount of penalties.

Bhagavad Gita says:

अकीर्तिं चापि भूतानि

कथयिष्यन्ति तेऽव्ययाम् |

सम्भावितस्य चाकीर्ति

र्मरणादतिरिच्यते 2/34

Reputation damage (अकीर्तिं ) for reputed people (सम्भावित ) is worse than death. That is to say, the more reputed one is, the more is the risk to reputational capital.

Therefore, every precedent teaches a lesson to all insiders and compliance officers to take calculated and conservative views, when it comes to timely disclosure of price sensitive information.

A recent order of the Supreme Court (dated December 2, 2025) dismissed an appeal against SAT on a matter involving selective dissemination of an unpublished price sensitive information, thereby, affirming the penalty of Rs. 30 lakh levied by SAT. The issue revolved around whether or not a media report, resulting into a selective, inadvertent dissemination of unpublished price sensitive information, requires prompt public disclosure by the listed entity.

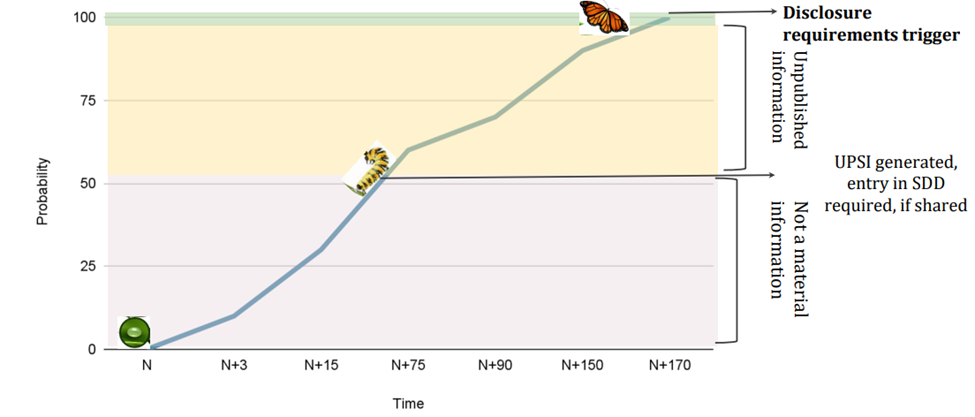

The whole idea of fair disclosure of inside information is that there is no information asymmetry, as the same kills meaningful price discovery in the market. If there is a leakage of information, before any information is released by the company, that creates an asymmetry and non-democratic spreading of unconfirmed information or so-called rumour. In such a situation, the listed entity has to act and either confirm what is being rumoured, or deny, and it cannot remain silent. There, a stance that the information is not ripe for disclosure, does not work, as the information is already spreading. See our presentation on Verification of Market Rumour by listed entities & other related amendments and FAQs on Verification of Market rumour by Listed Entities.

With the recent amendments in the PIT Regulations clarifying that unverified events or information reported in print or electronic media cannot be considered as “generally available information”, this is no longer a question as to whether such information can escape the ambit of UPSI. In fact, regulations along with the stock exchange guidance have gone a long way in quantifying the market impact.

Reg 8(1) of PIT Regulations requires companies to put in place a Code for Fair Disclosure of Information, in accordance with the model Code provided under Schedule A. Para 1 of Schedule A requires prompt public disclosure of UPSI as soon as credible and concrete information comes into being in order to make such information generally available.This coincides with the requirement of disclosure of material events and information to the stock exchanges under Reg 30 of LODR.

Also, Para 4 of the Schedule 1 requires: Prompt dissemination of unpublished price sensitive information that gets disclosed selectively, inadvertently or otherwise to make such information generally available.

While Principle 1 pertains to a general principle of making material information available to the public, Principle 4 seeks to fill the information asymmetry in case of an inadvertent leak of UPSI.

In a May 2025 order, SAT has discussed the distinction between the application of disclosure requirements in the aforesaid principles:

“Principle-1 requires it to ipso facto make prompt disclosure, as and when a credible and concrete information comes into being in order to make it ‘generally available’. Thus, if the UPSI is concrete and credible, the company would have already made its disclosure to make it generally available. But before such a stage is reached, and the UPSI gets disclosed selectively, then in such a scenario, even though the company was not required to make disclosure in accordance with Principle-1, Principle-4 makes it obligatory to make prompt disclosure to make information generally available to ensure compliance with general Principle–2.”

In the said ruling, one of the contentions of the Appellants was that the material information, on account of being published in media sources, becomes generally available. However, SAT observed that, “Till the information is disclosed by the company, it remains unauthenticated.”. In the absence of a clarity on the matter by the company to the investors and public at large, speculative information will keep floating around. As such, “selective leakage of the information, howsoever accurate or otherwise or complete or in bits and pieces, does not discharge the company from its responsibility of making prompt disclosure to make it generally available, moreso when such information has been classified by company as UPSI.”

Thus, while Reg 30(11) of LODR provides discretion to the listed entities (except top 250 listed entities based on market capitalisation) w.r.t. responding to market rumours, such discretion cannot override the requirements of the PIT Regulations. Also see our FAQs on Verification of Market rumour by Listed Entities.

The metamorphosis of an internal development into UPSI and ultimately a disclosable event is based on its probability of occurrence, over that of non-occurrence. Generally speaking, once the probability of occurrence of an event is more than the probability of its non-occurence, UPSI may be said to have been germinated, thus, requiring preservation of such information and all related controls.

See our presentation on verification of market rumour by listed entities & other related amendments.

While the SEBI Listing Regulations appear to grant leeway to listed entities to remain silent on rumours floating in the market, such leeway is not absolute and the PIT Regulations still require the listed entities to ensure public dissemination of information, where a leak of UPSI has occurred. While the Supreme Court dismissed the appeal, citing that the same has been comprehensively dealt with by SEBI and SAT on the basis of the factual matrix, the proceedings signal the SC’s stand that the principles underlying the PIT Regulations have to be upheld at all times, and if going by the principles, it is essential for the listed entity to speak, it cannot remain silent.

In view of the significance of the subject, we are conducting a 12 hours Certificate Course on Insider Trading for Compliance Officers, see details here – https://vinodkothari.com/2025/11/12-hours-certificate-course-on-insider-trading-for-compliance-officers/

Our other resources:

Updated as on 7th January, 2025

Simrat Singh | Finserv@vinodkothari.com

Private credit is becoming a new force in India’s lending ecosystem. As traditional banks and NBFCs operate under the strict regulations on capital, exposure and asset quality norms, they are often unable, or unwilling to cater to certain borrowers. In addition, for banks in particular, what kind of lending opportunities can be tapped is often a matter of having typecast lending products, policies and procedures. This leaves occasional, however, lucrative gaps in funding needs which are not serviced by regulated lenders. Into these gaps step in Private Credit AIFs (in India), Business Development Companies (BDCs) and Private Collateralized Loan Obligations (CLOs) (in the USA and Australia), these funds can structure deals creatively, customise financing to borrower needs and capture higher-yield opportunities that conventional lenders must pass over. What is emerging is a parallel channel of credit, one that is nimble, agile and focused.

Globally, this shift hasn’t gone unnoticed. Policymakers and institutions like the IMF have flagged the risks tied to private credit markets, especially around opacity, leverage and borrower quality (see below). Yet in India, the momentum continues to build. Tight constraints on banks, the rise of alternative asset managers and the unmet capital needs of businesses beyond the traditional credit universe are all fuelling rapid expansion.

This article examines what private credit is, why it is growing in India, the risks associated with this market and whether their growth creates regulatory arbitrage relative to banks and NBFCs.

As per an IMF paper1, private credit is defined as “non-bank corporate credit provided through bilateral agreements or small “club deals” outside the realm of public securities or commercial banks. This definition excludes bank loans, broadly syndicated loans, and funding provided through publicly traded assets such as corporate bonds.

Simply, private credit is the lending by non-bank and non-NBFCs. The sector predominantly involves alternative asset managers2 who raise capital from institutional investors using closed-end funds and lend directly to predominantly middle-market firms3.

Unlike traditional credit, private credit is typically tailored to the specific needs of each borrower. Repayment terms can, for instance, be aligned with the timing of a funding round or disbursements can be structured to match capital expenditure plans. Interest rates may also be designed on a step-up basis, linked to the borrower’s turnover. Many elements that are otherwise rigid under RBI-regulated lending can be flexibly structured in private credit (see table 2 below). This flexibility is especially valuable for start-ups and small businesses, which often require customised financing solutions that traditional lenders may be unable to provide.

| Parameter | Private Credit | Traditional Credit |

| Source of Capita | Private debt funds (Category II AIFs), investors like HNIs, family offices, institutional investors | Banks, NBFCs and mutual funds |

| Target Borrowers | Companies lacking access to banks; SMEs, mid-market firms, high-growth businesses | Higher-rated, established borrowers. |

| Deal Structure | Bespoke, customised, structured financing | Standardised loan products |

| Flexibility | High flexibility in terms, covenants, and structuring | Restricted by regulatory norms and rigid approval processes |

| Returns | Higher yields (approx. 10–25%) | Lower yields (traditional fixed-income) |

| Risk Level | Higher risk due to borrower profile and limited diversification | Lower risk due to stronger credit profiles and diversified portfolios |

| Regulation | Light SEBI AIF regulations; fewer lending restrictions | Heavily regulated by RBI and sector-specific norms |

| Liquidity | Closed-ended funds; limited exit options | More liquid; established repayment structures; some products have secondary markets |

| Diversification | Limited number of deals; concentrated portfolios | Broad, diversified loan books |

| Role in Market | Fills credit gaps not served by traditional lenders | Core credit providers in the financial system |

Table 1: Differences between private credit and traditional credit

Global private credit assets under management have quadrupled over the past decade to US$2.1 trillion in 20234. Compared with the rest of the world, the private credit market in India is very small, with estimated assets under management of $25 billion to $30 billion as of March 31, 2025, representing about 0.6% of India’s GDP and 30-35% of the total investments made by AIFs in India.5

Figure 1: Private credit share (1%) as a part of overall corporate lending. Source: RBI, AMFI

Figure 2: Size of Private Credit Market. Source: RBI

Private credit is expanding rapidly because it steps in where traditional banks hesitate. It provides capital for last-mile project completion, cost overruns and promoter equity infusion; areas that fall outside the comfort zone of regulated lending. The asset class has also delivered consistently higher risk-adjusted returns, a compelling draw for global and domestic investors, especially through long phases of low interest rates.6

A key advantage lies in its flexibility. Private lenders can tailor covenants7, link returns to cash flows and restructure repayment terms during stress, offering a level of customisation that conventional bank credit cannot match. For investors, this translates into both diversification and access to high-growth segments that remain beyond the scope of mainstream credit markets.

Sector specific regulatory gaps: There is a concern that tighter bank regulation will continue to encourage the migration of credit from banks to private credit lenders8. Certain regulatory restrictions on banks directly push borrowers toward private credit:

Apart from the above, The IBC significantly strengthened creditor rights and recovery prospects, boosting confidence among lenders and supporting the growth of private credit. At the same time, many borrowers, particularly smaller firms, those with weak earnings, high leverage or insufficient collateral, struggle to access bank loans making private credit a natural alternative11. This shift was further accelerated by an extended period of low global interest rates, which pushed investors to seek higher-yielding opportunities and increased capital flows into private credit strategies.

The most common structure for channelising private credit is an AIF – more specifically, a Category II AIF. A ‘Private Credit AIF’ is essentially an AIF whose primary investment strategy is direct debt financing (by investing in debt instruments) to borrowers outside the conventional banking/syndicated loan market. Since AIFs are not subject to the same regulatory framework as traditional lenders (for example, no deposit-taking, no CRR/SLR requirements etc.), they can offer tailor-made structures such as step‐up interest rates, bullet repayments, equity warrants, convertible features, etc.

A private credit fund requires long-term, stable capital, and frequent redemption demands can disrupt lending strategy. A closed-ended Category II AIF structure suits this model well, as it locks in investor capital for the fund’s life and prevents premature withdrawals. Private credit deals are idiosyncratic and difficult for outside parties to value or trade, lenders typically rely on long-term pools of locked-up capital for financing. One advantage AIFs have over mutual funds is that mutual funds are restricted to investing only up to 10% of their debt portfolio in unlisted plain vanilla NCDs.

Compared to private equity or venture capital, where performance depends heavily on market conditions and timing exits, private credit offers returns that are largely predetermined by contract. The trade-off, however, is that like most AIFs, these investments typically come with multi-year lock-ins and fewer exit opportunities, underscoring their inherently illiquid nature. Typically, investors which can commit long term capital are well-suited to invest in such AIFs – such as pension funds and sovereign wealth funds etc.

A Business Development Company (BDC) is a U.S. investment vehicle designed to channel capital to small and mid-sized businesses that lack easy access to traditional bank financing or public capital markets. BDCs were created by the U.S. in 1980, through amendments to the Investment Company Act of 1940 (see sections 2(48), 54 and 55), with a clear policy objective: to allow retail investors to participate in private credit and growth capital, an area previously accessible only to institutional investors.

As per a Federal Reserve Paper: BDCs are a way for retail investors to invest money in small and medium-sized private companies and, to a lesser extent, other investments, including public companies. BDCs are structured in different ways. Public BDCs refer to those with shares traded on national securities exchanges, and those whose shares are not traded on national securities exchanges but placed through SEC-registered or private placement offerings are non-publicly traded BDCs. BDCs typically finance middle-market firms—companies with EBITDA between $5 to $100 million, which historically have had limited access to funding from commercial banks and public debt markets. They also provide finance to development-stage companies in sectors such as technology, life science, healthcare information and services and sustainability industries, and private-equity owned or sponsored companies.

Structure and regulatory framework: Legally, a BDC is an unregistered closed-end investment company (fund). To qualify as BDC, a company must invest at least 70% of its assets in ‘eligible portfolio companies’ i.e. firms with market values below $250 million and provide ‘significant managerial assistance’ to its portfolio companies [see section 2(48) of the Investment Company Act, 1940]. These companies are often private, thinly traded public firms, or businesses undergoing financial stress. To avoid corporate-level taxation, they must distribute at least 90% of their taxable income to shareholders each year (like REITs and InvITs in India). BDCs are also permitted to use leverage (up to 2x the amount of assets).

BDCs raise capital through IPOs, follow-on equity issuance, corporate bonds or hybrid securities. While many BDCs are publicly traded on stock exchanges (50 in number), offering daily liquidity to investors, some exist as non-traded BDCs with limited liquidity (47 in number) and yet some as private BDCs (50 in number).12

Investment mix: Although BDCs are permitted to invest in both equity and debt, their portfolios are majorly debt-focused. In practice, 60–85% of a typical BDC portfolio is invested in debt instruments, such as senior secured loans, second-lien loans, or mezzanine debt. Equity investments usually comprise 15–30% of assets.13 Because of this allocation, interest income from loans is the primary driver of BDC earnings. This income tends to be steady and predictable, which aligns well with the BDC structure. For example, Ares Capital, one of the largest BDCs, allocates roughly 78–83% of its portfolio to debt (primarily first-lien loans) and about 17% to equity.

How BDCs generate returns: BDCs generate returns through multiple channels:

Many BDC loans are floating-rate, which provides partial protection in rising interest rate environments. However, most BDC investments are below investment-grade or unrated and equity positions are often in privately held or financially stressed companies, introducing credit and valuation risk.

Comparison with venture capital, private equity AIFs and Mutual Funds: BDCs are often compared with venture capital and private equity funds because all three invest in private, illiquid companies and may provide strategic or managerial support. The key distinction lies in investor access and structure. Venture capital and private equity funds are privately placed vehicles, restricted to institutions and wealthy investors, with long lock-ups and limited transparency. BDCs, by contrast, are designed to be accessible to retail investors and trade on public exchanges.

This distinction becomes especially relevant when comparing BDCs with AIFs in India, particularly private credit AIFs. Economically, BDCs resemble private credit AIFs; both lend to mid-market companies and rely heavily on interest income. The crucial difference lies in retail participation. In India, AIFs exclude retail participation by making the minimum investment amount of Rs. 1 Crore and prohibiting public issuances. In the U.S., BDCs were created to enable retail participation therefore there are no minimum investment norms and public issuances are allowed for BDCs. In this sense, BDCs can be thought of as private credit AIF-like strategies wrapped in a publicly traded structure, placing them between mutual funds (fully liquid public-market vehicles) and AIFs (illiquid private-market vehicles) on the investment spectrum.

From an Indian regulatory perspective, mutual funds offer the closest structural comparison to BDCs, albeit with important distinctions. Indian mutual funds are not permitted to employ leverage as part of their investment strategy and may borrow only to meet temporary liquidity requirements, capped at 20% of net assets (see Regulation 44 of the SEBI Mutual Fund Regulations). In addition, mutual funds face strict asset-side constraints, including a limit of 10% of the debt portfolio in unlisted plain-vanilla non-convertible debentures (see paragraph 12.1.1 of the SEBI Master Circular on Mutual Funds). These restrictions constrain exposure to illiquid private credit, making a BDC-like structure regulatorily infeasible in India under the mutual fund framework.

Global context: No other major market has created a true equivalent of the BDC. While regions such as Europe, Canada, and Australia have listed private credit funds, specialty finance vehicles, or credit income trusts, these structures typically limit or discourage retail participation.

Risk considerations: While BDCs may have stable and regular income, they carry elevated risks. Their portfolios consist largely of non-investment-grade debt and equity in small or distressed companies, often with limited public information. Credit losses, economic downturns or excessive leverage can materially impact returns.

IMF in its 2024 Global Financial Stability Report highlighted risks w.r.t rise in private credit since its growth comes with several structural weaknesses that make the market vulnerable, especially in a downturn. Its rapid expansion is happening largely outside traditional regulatory oversight and because the market has not been stress-tested, the true scale of risk remains unclear. Borrowers tend to be smaller and more leveraged and with most loans being floating-rate, repayment stress can escalate quickly when interest rates rise. Although private credit funds’ leverage appears low compared with other lenders, end borrowers tend to be more highly leveraged than those in public markets, increasing the risks to financial stability.14

The increased complexity and the interconnections with leveraged financial entities create more channels through which unexpected losses in private credit could spread to the broader financial system15

Instruments such as PIK interest16 only defer the problem, increasing loss severity if performance deteriorates. Liquidity is another pressure point since private credit funds are inherently illiquid. Risk is further amplified by layers of hidden leverage, at the borrower, SPV, investor and fund level making contagion hard to track. Layers of leverage are created by the AIF lending against equity to a holding entity, which infuses the equity into an operating company, and the operating company borrowing against such equity.

Because loans are private, unrated and rarely traded, valuation is opaque and losses may remain masked until too late. Growing competition also risks weakening underwriting standards and covenant discipline, particularly as larger banks participate in private deals.

Practical challenges add to this vulnerability. Collateral enforcement may not always hold up legally, say due to restrictions on transferability of collateral (say, shares of a private company). Equity-linked security is volatile as well, and during distress, equity tends to lose its value almost completely. In essence, private credit offers flexibility and returns, but its opacity, leverage, illiquidity and weaker borrower profiles create risks that could surface sharply in stress conditions. Private credit certainly warrants closer attention. Nonbank lenders, especially private credit funds, have grown rapidly in recent years, adding to financial stability risks because they are less transparent and not as firmly regulated.

What you cannot do directly, you cannot do indirectly – the age-old maxim might apply in case a RE which is otherwise barred by RBI for an object, uses the AIF route to achieve that object. Below we examine some of the distinctions in the regulatory oversight:

| Function | Private Credit AIFs | RE |

|---|---|---|

| Credit & Investment rules | ||

| Credit underwriting standards | No regulatory prescription | No such specific rating-linked limits. However, improper underwriting will increase NPAs in the future. |

| Lending decision | Manager-led Investment Committee under Reg. 20(7) may decide lending Manager controls composition of IC; IC may include internal/external members; IC responsibilities may be waived if investor commitment ≥₹70 Cr w/ undertaking Primarily i.e. the main thrust should be in: – Unlisted securities; and/or – Listed debt rated ‘A’ or below | Lending decisions guided by Board-approved credit policy |

| Exposure norms | Max 25% of investible funds in one investee company. | Exposure is limited to 25% of Tier 1 Capital per borrower and 40% per borrower group for NBFC ML; No such limit for NBFC BL. Banks can lend maximum upto 15% of their Tier 1 + Tier 2 capital to a single borrower. Large exposure norms may apply in case of banks and Upper Layer NBFCs |

| End-use restrictions | None prescribed under AIF Regulations, results in high investment flexibility | Banks cannot lend for land acquisition or for funding a M&A deal [refer ‘sector-specific regulatory gaps’ above] NBFCs do not have any such restrictions. They do have internal limits on sensitive sector exposures which includes capital market and commercial real estate [See Para 92 of SBR] |

| Related party transactions | Need 75% investors consent [reg 15(1)(e)] | Board approval mandatory for loans ≥₹5 Cr to directors/relatives/interested entities; Disclosure + abstention from decision-making;Loans to senior officers requires Board reporting [See para 93 of SBR] |

| Capital, Liquidity & Leverage Requirements | ||

| Capital requirements | No regulatory prescription as the entire capital of the fund is unit capital | Minimum net owned funds of ₹10 Cr, CRAR 15% for NBFC-ML and above [See para 133.1 of SBR]9% CRAR in case of banks, |

| Liquidity & ALM | Uninvested funds may be parked in liquid assets (MFs, T-Bills, CP/CDs, deposits etc.) [15(1)(f)] | NBFC asset size more than 100 Cr. have to do LRM [Para 26] |

| Leverage limits | No leverage permitted at AIF level for investment activities Only operational borrowing allowed | Leverage ratio of BL NBFC cannot be more than 7 No restriction on NBFC ML however, CRAR of 15% makes results into leverage limit of 5.6 times For Banks, in addition to CRAR, there is minimum leverage ratio is 4% |

| Monitoring, Restructuring and Settlements | ||

| Loan monitoring | No regulatory prescription | RBI-defined SMA classification, special monitoring, provisioning & reporting. |

| Compromise & settlements | No regulatory prescription | Governed by RBI’s Compromise & Settlement Framework |

| Governance, Oversight & Compliance | ||

| Governance & oversight | Operate in interest of investors Timely dissemination of info Effective risk management process and internal controls Have written policies for conflict of interest, AML. Prohibit any unethical means to sell/market/induce investors Annual audit of PPM termsAudit of accounts 15(1)(i) – investments shall be in demat form Valuation of investments every 6 months | A Risk Management Committee is required for all NBFCs. [See para 39 of SBR] AC [94.1], NRC [94], CRO [95] ID and internal guidelines on CG [100] required for NBFC-ML and above |

| Diversity of borrowers | Private credit AIFs usually have 15-20 borrowers. | Far more diversified as compared to AIFs |

| Pricing | Freely negotiated which allows for high structuring flexibility | Guided by internal risk model |

Table 2: Differences in regulatory oversight between AIFs and Regulated Entities (REs)

The core difference between private credit AIFs and RBI-regulated lenders lies in regulatory intent. SEBI is a disclosure-driven market regulator, it relies on transparency, governance and informed investor choice. RBI is a prudential regulator tasked with protecting systemic stability, and therefore imposes capital buffers, exposure limits and stricter supervision. Private credit AIFs operate within SEBI’s lighter, disclosure-based approach, while banks and NBFCs function under RBI’s risk-averse framework. This does not always create arbitrage, but it does allow credit activity to grow outside the prudential perimeter. As private credit scales, a coordinated SEBI-RBI framework may be necessary to preserve flexibility without compromising financial stability.

It is important to recognise that Category I and Category II AIFs are prohibited from taking long-term leverage. As a result, any loss arising from their lending or investment exposures does not cascade into the wider financial system. Therefore, concerns around applying capital adequacy requirements to these AIF categories are largely unwarranted.

Though still a small fragment of India’s wider corporate lending landscape, private credit AIFs are steadily gaining ground reaching those nooks and crannies of credit demand that banks and NBFCs often cannot, or would not, serve. Their ability to operate beyond the traditional comfort zone of regulated lenders is what makes this segment structurally relevant and increasingly attractive to borrowers and investors alike.

At the same time, rapid expansion brings the potential for regulatory arbitrage. The RBI has already acknowledged this risk, most notably through its actions on evergreening via AIF structures, ultimately resulting in exposure caps of 10% for individual regulated entities and 20% collectively, along with mandatory full provisioning where exposure exceeds 5% in an AIF lending to the same borrower. These measures serve as guardrails to prevent private credit vehicles from functioning as an indirect tool for evergreening of loans.

See our other resources of Alternative Investment Funds here

Saket Kejriwal, Assistant Manager | corplaw@vinodkothari.com, finserv@vinodkothari.com

The structure of a trust inherently creates a separation of roles, typically involving three distinct parties viz. the author/settlor, trustee, and beneficiaries. While the control/operations rests with the trustee, economic benefit lies with the beneficiaries, and the settlor may continue to exert influence through the trust deed or reserved powers, thus making it difficult to clearly identify who actually “owns” or “controls” the trust. This intrinsic separation of legal control, economic interest and potential influence renders trusts far more opaque than other conventional structures like companies or partnerships. What makes the structure even more complicated is that trusts are mostly governed by 19th century laws. Trusts are not required to publicly file information about their beneficiaries; in many cases, trustees may even contend that they are not maintaining any such regular list.

Adding to this complexity is the fact that trusts may be structured in different forms. Based on the degree of control with the trustees, trusts may be discretionary, where the trustee has full discretion to identify the beneficiaries and/or their share, or non-discretionary, where the beneficiaries have identifiable and predetermined rights in the trust property.There are trusts where the determination of beneficiaries is either contingent or future – for example, children and grandchildren of the settlor. In discretionary trusts, beneficiaries may not have a defined share or enforceable claim at any given point, making it unclear whether they can be treated as beneficial owners at all. In non-discretionary trusts, although the beneficiaries are identifiable, the trustee continues to hold legal title, again blurring the line of who truly “owns” the trust.

For Reporting Entities1 (“REs”), including Banks and NBFCs, identification and onboarding becomes more complex when the customer is a non-individual entity. The extent of verification varies by entity type, and trusts in particular create added challenges because of the reasons cited above.

Before discussing how REs should identify a trust’s BO, it is important to understand why they must do so. Under para 9 and 10 of the RBI KYC Directions, 2016, every regulated entity is required to frame a Customer Acceptance Policy which, at a minimum, mandates that no account-based relationship or transaction may be undertaken unless full Customer Due Diligence (‘CDD’) is completed. The same is based on R.10 of The FATF Recommendations.

As defined under para 3(b) Clause (v) of RBI KYC Directions, 2016, “Customer Due Diligence means identifying and verifying the customer and the beneficial owner using reliable and independent sources of identification”. Further, clause 3 under explanation to the above para extends this requirement to “Determining whether a customer is acting on behalf of a beneficial owner, and identifying the beneficial owner and taking all steps to verify the identity of the beneficial owner, using reliable and independent sources of identification.”. Similar to what is prescribed under Rule 9(1) of PML Rules, 2005.

As part of CDD, REs are required to identify customers and their BOs, which in turn places a corresponding obligation on customers to truthfully disclose their ownership structure and furnish relevant documents that establish the identity of a natural BO. This process obliges REs to verify the authenticity and completeness of the information and documents submitted, use these findings to determine whether to establish the business relationship and to appropriately assign a risk rating.

However, in practice, BOs may be reluctant to provide their KYC documents due to privacy concerns, fear of scrutiny, or because complex structures were intentionally designed to keep the BO’s identity concealed.

As per para 3(a)(iv) clause (d) of RBI KYC Directions, “Where the customer is a trust, the identification of beneficial owner(s) shall include identification of the author of the trust, the trustee, the beneficiaries with 10 percent or more interest in the trust and any other natural person exercising ultimate effective control over the trust through a chain of control or ownership”. A similar definition is provided under Rule 9(3) of PML Rules, 2005.

Aforesaid definitions originates from The FATF Recommendations which clearly defines that in context of legal arrangements i.e. Trust, beneficial owner includes: “(i) the settlor(s); (ii) the trustee(s); (iii) the protector(s) (if any); (iv) each beneficiary, or where applicable, the class of beneficiaries and objects of a power; and (v) any other natural person(s) exercising ultimate effective control over the arrangement. In the case of a legal arrangement similar to an express trust, beneficial owner refers to the natural person(s) holding an equivalent position to those referred above.”

In a discretionary trust, the trustee has full discretion, whereas in a non-discretionary trust, beneficiaries have fixed rights and the trustee has limited discretion. This influences who can practically be identified as exercising control.

Now, in the case of a discretionary trust, the above framework is usually manageable because the trustee, who exercises control, may not object to being identified as a BO. However, in a non-discretionary trust, the trustee does not exercise independent discretion. In such cases, the trustee may express reluctance to be classified as a BO because he does not “benefit” from the trust in an economic sense and may view BO identification as an unwarranted extension of responsibility. This confusion often results from equating BO with someone who derives economic benefit, whereas under AML laws the emphasis is on identifying at least one identifiable individual, ensuring that there is an accountable natural person whom authorities and REs can pursue in the event of ML/TF concerns, regardless of whether they receive monetary benefit.

It is important to understand that the terms “beneficiary” and “beneficial owner” serve different purposes. The objective of identifying the BO is not to treat the trustee or settler as recipients of trust benefits, but to ensure that the RE can clearly trace the natural persons involved in controlling, directing, and/or benefiting from the trust arrangement. BO identification is a regulatory requirement aimed at preventing misuse of trusts for ML/TF purposes, not a determination of who is entitled to trust assets. When viewed this way, trustee and settler identification becomes a matter of transparency and risk assessment, not a reclassification of their legal or economic rights under the trust.

REs typically encounter two scenarios that require them to look behind the trust structure, first, when the trust is the direct customer, second, when the trust is recognised as a BO of another entity.

When the trust itself is the customer, the BO identification framework is relatively straightforward. The PML Rules clearly prescribe that the following individuals must always be treated as BOs:

These natural persons fall squarely within the definition of beneficial owners and should be identified and verified without debate.

Where specific beneficiaries cannot be identified, for example, in a public charitable trust, or in a private trust where beneficiaries do not meet the 10% threshold, the obligation to identify BOs does not fall away. In such cases, the RE must still identify:

Thus, the absence of identifiable beneficiaries does not dilute the requirement.

Complexity increases when the customer is not the trust, but another legal entity, such as a company, LLP, or partnership, in which a trust holds a substantial stake. In such cases, identifying the natural person as BO requires a deeper “look-through” analysis.

The Interpretive Note to Recommendation 10 of The FATF Recommendations provides a structured cascading approach to determine BOs of legal persons. This approach should be applied sequentially2:

Determine whether any natural person ultimately owns or controls the entity through direct or indirect ownership (including ownership via the trust), if yes, identify the person(s) as BO.

If no natural person is identifiable through ownership, identify the natural persons exercising control of the entity through other means, such as through one or more juridical persons.

In such cases, the BO definition for trusts should not be imported from the definitions as discussed above i.e. all parties to the trust need not automatically be treated as BOs of the entity concerned.

Instead, the focus should be on identifying the natural person(s), whether trustee or settlor, who genuinely hold or exercise the relevant control over the underlying company, and evaluating them against the test of control.

If no natural person can be identified under Step 1 or Step 2, the reporting entity must identify and verify a Senior Managing Official of the customer entity itself.

Intent behind this clause, might be to cater to conditions where the legal person is held by another legal person which is, in turn, held by a trust or where the trust is a charitable trust with no identifiable beneficiaries and no effective control exercised by the trustee, the chain may not yield any natural person with a controlling ownership or control interest. In such situations, the responsibility reverts to the customer entity itself, and the senior managing official (SMO) of the customer is identified as the BO for CDD purposes.

However, even in such cases, the SMO is identified purely for the purposes of AML laws, as discussed above. (see para 31 of the FATF Guidance on Beneficial Ownership of Legal Persons).

While the concept of a BO and the concept of a Significant Beneficial Owner (SBO) under the Companies Act both aim to identify the natural persons behind an entity, the two frameworks differ significantly in scope and approach. The SBO definition focuses on identifying individuals who hold a prescribed level of ownership or control, and it does not provide a structured fallback if no individual meets that threshold.

In contrast, the BO identification under the Rule 9(3) PML Rules follows a cascading approach i.e. REs must first identify natural persons with ownership, then those who exercise control through other means. Further, only when neither approach detects a clear individual do the rules require identifying the senior managing official as the BO of last resort. This ensures that BO identification cannot be left blank, every entity must ultimately map to a natural person for AML purposes, even where no SBO exists, so that transactions are not carried out in benami or opaque structures.

It is important to clarify that being identified as a BO is primarily a regulatory formality for compliance. It does not alter a person’s rights, liabilities, or relationship with the trust or entity. The core objective is simply to ensure that there is a clearly identifiable natural person connected to the legal entity so that the RE can complete its due diligence and satisfy ALM requirements. Following are the limited obligations of being identified as a BO:

Highlights:

Following a 32-pager consultation paper proposing significant amendments to RPT provisions, towards ease of doing business, rolled out by SEBI on August 4, 2025, several amendments were approved by SEBI in its Board Meeting on 12th September, 2025. The SEBI (Listing Obligation and Disclosure Requirements) (Fifth Amendment) Regulations, 2025 have been notified on 19th November, 2025 amending the RPT framework for listed entities.

Some of our comments on the proposals, as recommended to SEBI, have also been accepted in the approved decisions. Our comments on the Consultation Paper may be read here.

While the Amendment Regulations have been notified, the amendments with respect to the RPT framework are effective from the 30th day of the notification of the Amendment Regulations, that is, with effect from 19th December, 2025.

A scale-based threshold mechanism has been approved, such that the RPT materiality threshold increases with the increase in the turnover of the company, though at a reduced rate, thus leading to an appropriate number of RPTs being categorized as material, thereby reducing the compliance burden of listed entities. The maximum upper ceiling of materiality has been kept at Rs. 5,000 crores, as against the existing absolute threshold of Rs. 1000 crores. The thresholds have been provided in Schedule XII, along with an illustration towards better understanding of the materiality thresholds.

Materiality thresholds as specified in Schedule XII:

| Annual Consolidated Turnover of listed entity (in Crores) | Approved threshold (as a % of consolidated turnover) | Maximum upper ceiling (in Crores) |

| < Rs.20,000 | 10% | 2,000 |

| 20,001 – 40,000 | 2,000 Crs + 5% above Rs. 20,000 Crs | 3,000 |

| > 40,000 | 3,000 Crs + 2.5% above Rs. 40,000 Crs | 5,000 (deemed material) |

Back-testing the proposal scale on RPTs undertaken by top 100 NSE companies show a 60% reduction in material RPT approvals for FY 2023-24 and 2024-25 with total no. of such resolutions reducing from 235 and 293, to around 95 to 119. The 60% reduction may itself be seen as a bold admission that the existing regulatory framework was causing too many proposals to go for shareholder approval.

With the amendments becoming effective, RPT regime is all set to be a lot relaxed, with the absolute threshold for taking shareholders’ approval to be doubled to Rs. 2000 crores. In addition, for larger companies, there will be a scalar increase in the threshold, rising to Rs. 5000 crores. A lot lesser number of RPTs will now have to go before shareholders for approval in general meetings.

In times to come, a multi-metric approach, depending on the nature of the transaction, may be adopted, drawing on a consonance-based criteria as seen in Regulation 30 of the LODR Regulations, thus offering a more balanced and effective approach. See detailed discussion in the article here.

Pursuant to the amendments in 2021, RPTs exceeding a threshold of 10% of the standalone turnover of the subsidiary are considered as Significant RPTs, thus, requiring approval of the Audit Committee of the listed entity. The following modifications have been approved with respect to the thresholds of Significant RPTs of Subsidiaries:

This is a mathematical impossibility, since materiality threshold is based on “consolidated turnover”, and hence, includes the turnover of the subsidiary. Further, unlike networth, turnover cannot be a negative number, and hence, even if one or more of the subsidiaries of the listed entity are loss-making entities, the same cannot reduce the consolidated turnover of the listed entity to a number below the standalone turnover of its subsidiaries, whose accounts are being consolidated with the entity.

The aggregate value of paid-up capital and securities premium, to be considered for the purpose of determination of Significant RPTs, should not be older than three months prior to the date of seeking AC approval. Since the value of paid-up capital and securities premium would be available with the company on a real-time basis, the same does not result in any additional compliance burden.

For newly incorporated subsidiaries, the Consultation Paper proposed linking the thresholds with net worth, and requiring a practising CA to certify such networth, thus leading to an additional compliance burden in the form of certification requirements. Following the approval in SEBI BM, the Amendment Regulations provide a threshold based on paid-up share capital and securities premium, and hence, certification requirement does not arise.

The existing provisions [Para (C)11 of Section III-B of LODR Master Circular] permit the validity of the omnibus approval by shareholders for material RPTs as:

Pursuant to the Amendment Regulations, the timelines have been incorporated as a proviso to Reg 23(4). Further, a clarification has been incorporated that the AGM to AGM approval will be valid till the date of next AGM held within the timelines prescribed as per section 96 of the Companies Act.

Proviso (e) to Regulation 2(1)(zc) of the extant SEBI LODR Regulations exempted transactions involving retail purchases by employees from being classified as Related Party Transactions (RPTs), even though employees are not technically classified as related parties. Conversely, it includes transactions involving the relatives of directors and Key Managerial Personnel (KMPs) within its ambit.

The CP proposed that the exemption related to retail transactions should be expressly limited to related parties (i.e., directors, KMPs, or their relatives) to grant the appropriate exemption.

Under the extant framework, retail purchases made on the same terms as applicable to all employees were excluded from the meaning of RPTs when undertaken by employees, but not when made by relatives of directors or KMPs. This led to an inconsistent treatment, where similarly situated individuals receive different regulatory treatment solely on the basis of their relationship with the company.

Pursuant to the Amendment Regulations, the exclusion for retail purchases has been extended to the relatives of the directors/ KMP, when undertaken on “terms which are uniformly applicable/offered to all employees, directors, key managerial personnel and relatives of directors or key managerial personnel ”. While the language refers to terms offered to “employees, directors, key managerial personnel and relatives of directors or key managerial personnel”, the same cannot be read to mean that preferential terms can be granted to “director”, “KMPs” or “relatives of such directors/ KMPs” as a separate class. The terms need to be uniform to what is otherwise offered to “employees” by such a listed entity/ its subsidiaries.

Regulation 23(5)(b) provides an exemption from audit committee and shareholder approvals for transactions between a holding company and its wholly owned subsidiary. However, the term “holding company” used in this context has remained undefined, leaving ambiguity as to whether it refers only to a listed holding company or includes unlisted ones as well.

A clarification has been inserted to provide the interpretational guidance that the term ‘holding company’ refers to the listed entity. The relevance of the aforesaid clarification would primarily be in cases where the unlisted subsidiary of the listed entity enters into a significant RPT with its wholly owned subsidiary (step-down subsidiary of the listed entity). Pursuant to the aforesaid proposal, as approved, no exemption will be available in such a case.

The amendments seem more or less welcoming, relaxing the RPT regime for listed entities. With the new leadership at SEBI meant to rationalise regulations, it was quite an appropriate occasion to do so. In sum, SEBI’s iterative approach to RPT governance demonstrates commendable responsiveness, contributing to the ease of compliances and in turn, of doing business by the companies.

Our resources: