Levying of penal charges or late payment charges are claimed as ‘just’, owing to the underlying breach of contract under the Contract Act, 1972. A breach or a non-performance by one party entitles the other party to receive compensation for any loss or damage suffered due to such breach. Penalties may not only be compensatory; they also have a deterrent element.

In order to ensure compliant behaviour, lenders charge penalties to their borrowers for various ‘events of default’; the predominant ones being penalty for delayed payments (in the form of charges or interest) and prepayment penalties. However, such charges stopped being ‘just’ and ‘reasonable’ when lenders started maneuvering such penalties as revenue enhancement tools, rather than as a deterrent measure and compensation for a breach. Such unreasonable penalties coupled with non-disclosures, compounding of penal interest, etc. were highly prejudicial to consumer interest and accordingly, caught the eye of the regulator.

The RBI introduced guidelines to the lenders to ensure reasonableness and transparency in the disclosure of penal interest vide its Circular on ‘Fair Lending Practice – Penal Charges in Loan Accounts’(RBI Guidelines on penal charges’) dated August 18, 2023. Our article and FAQs[1]on the same may be read here[2].Our YouTube video discussing the guidelines may be viewed here.

However, charging penal interest also raises several practical questions for lenders, mainly indirect taxation and accounting of penal charges, which will be discussed in detail in this article.

The Finance Bill, 2023[1], has quite nearly caused the demise of the so-called “Market-Linked Debentures” (MLDs)[2]. The changes made pursuant to the Finance Bill, 2023, took away what seemed to be a strong reason for popularity of MLDs, i.e., the tax arbitrage.

Prior to the change, listed MLDs had the advantage of being exempt from the withholding tax under section 193 of the Income Tax Act, 1961, as well as being taxed at 10% as Long Term Capital Gains (LTCG) tax, if held for at least 12 months.

Finance Bill, 2023 inserts a new section 50AA to the Income Tax Act, 1961, which makes MLDs to be taxed at slab rates as a short term capital asset in all cases at the time of transfer or redemption on maturity, irrespective of the period of holding, therefore losing out on the earlier lower LTCG rate of 10%.

In addition, the earlier exemption from withholding tax on listed debentures has now been removed pursuant to an amendment in section 193, which means that interest paid on listed debentures would now be subject to withholding tax with effect from April 01, 2023[3].

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2023-05-17 12:59:382023-05-17 12:59:39Shorn of tax benefit, MLDs now face tax deduction on payouts

“The Supreme Court’s only armour is the cloak of public trust; its sole ammunition, the collective hopes of our society.” – Irving R. Kaufman

Background

The Supreme Court has ruled that service tax will not be levied on corporate guarantees by a parent company to its subsidiaries where there is no consideration involved.

This article discusses the impact of this ruling on companies which issue corporate guarantees without consideration.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2023-04-12 12:32:572023-04-12 20:05:34A Critical Analysis on Corporate Guarantees under Service Tax and GST

Secondment of employees have become increasingly popular amongst corporate entities which enter into secondment arrangements to leverage the expert knowledge and specific skill sets. The seconded employees work on a deputation basis in the seconded companies they are seconded to which require their technical expertise on certain matters. Since the seconded employee works for the seconded company during the secondment period, a pertinent question arises on whether the seconded employee becomes an employee of the seconded company. If yes, then what are the likely implications in the context of service tax.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Neha Sinhahttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngNeha Sinha2022-11-21 12:05:222022-11-22 12:13:06Secondment contract as ‘services’: Supreme Court held under Indian taxation regime

Rating agency Standard and Poor’s recently noted that at least 60 percent of the world’s economies are either into recession already or heading towards the same. The same report notes that 29 of the 33 countries covered by the study have disorderly inflation above the targets set by the respective central banks[1]. OECD’s interim report of September, 2022 says that despite a boost in activity as COVID-19 infections drop worldwide, global growth is projected to remain subdued in the second half of 2022, before slowing further in 2023 to an annual growth of just 2.2%. This is accompanied by inflationary pressures in most countries[2]. India is one of the two countries projected to have a growth rate of more than 6%.

The RBI’s monetary policy, September, 2022, as expected, has announced an interest rate hike of 50 bps in the policy rates.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2022-09-30 15:52:312022-09-30 15:57:33Stressed for reform: RBI proposes stressed assets securitisation and loss provisioning

The Energy Conservation (Amendment) Bill, 2022 (“Bill”) seeks to provide a regulatory framework for carbon markets in India. The Bill was passed in the Lok Sabha on 8th August, 2022, and has been passed in the Rajya Sabha on 12th December, 2022. The President’s asset is all that is required to bring the carbon markets within the statutory framework of India. However, there is still a long way to go before carbon markets are implemented in India, which will require notification of the procedures and rules governing the same. Further, the carbon markets in other countries are still developing in a phased manner, identifying the gaps in the existing system and modifying accordingly. India cannot be an exception to the same. However, the concept of “carbon credits” is not unknown to India since there are several entities in the country which are already generating tons of carbon credits. This article seeks to delve upon the legal aspects of carbon credits markets around the world, the consequences of not exporting the same, and the tax implications upon sale of the generated credits. As we study the existing carbon markets around the world, some learnings from these markets may be taken into consideration for the developing carbon market in India.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Payal Agarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngPayal Agarwal2022-08-31 18:06:512023-01-13 15:08:44Emission law amendments: Laying the framework for Carbon trading market in India

By Devika Agrawal, Executive, Vinod Kothari and Company

devika@vinokothari.com

Background

The preamble to the Insolvency and Bankruptcy Code, 2016 (‘Code’) enlists value maximisation as one of its key objectives. In line with the said objective, the Code included ‘Going Concern Sale’ (‘GCS’) of the corporate debtor or the business of the corporate debtor in liquidation, vide the Amendment dated 22nd October, 2018[1] in the Liquidation Process Regulations, as one of the modes of sale. The underlying intent of introducing GCS in liquidation was to maximise value. It was expected that introduction of GCS in liquidation would give a breather and will be looked forward to by Corporate Debtors undergoing liquidation process, however, the statistics presented by the Quarterly Newsletter of the IBBI, for the quarter ended 30th September, 2021[2] give a different view as only six out of the 1419 orders for commencement of liquidation, were closed by a sale as a going concern under liquidation process. For an enhanced understanding of a GCS, our Articles on the topic can be referred to.[3]

One probable reason for lesser use of GCS may be tax considerations attached to such sale, (for example, questions concerning write back of liabilities, continuation of tax benefits, carry forward of losses and unabsorbed depreciation). Besides, given how different GCS in liquidation is from a conventional GCS and a GCS in CIRP, acquirers often face issues in accounting for assets acquired under a GCS in liquidation. Further, there remains uncertainty with respect to the accounting for and recording of transactions. In this article the author attempts to discuss accounting and tax issues in GCS in liquidation.

GCS in liquidation vs. conventional GCS vs. GCS in CIRP

As stated above, it is important to note that a GCS in liquidation is different from a conventional GCS and a GCS in CIRP by way of a resolution plan. The difference lies not just in the circumstances under which a GCS takes place in each of the said three modes but also the manner of treatment of assets, liabilities, profits, losses and share capital. The accounting and tax considerations depend on the same. When one talks about accounting and taxation, it becomes important to see what happens to each component when a transaction takes place.

A snapshot of the treatment of these components under different modes of sale specified above has been tabulated below.

Sl. No

Basis

GCS in liquidation

Conventional GCS

GCS by way of a Resolution Plan in CIRP

1.

Transfer of liabilities

All liabilities are settled from the sale proceeds, in accordance with Section 53. Thereafter, pending liabilities, if any stand extinguished.

Liabilities associated with the assets are transferred to the acquirer.

Liabilities are in the form of claims on the CD. They are paid off in a manner provided for in the Resolution Plan as approved by CoC.

2.

Valuation of Assets

The successful auction bidder pays a lump sum, without assigning values to individual assets. In a GCS in liquidation, the value of assets may be comparatively lower because it bears the burden of a failed resolution process.

The buyer pays a lump sum, without assigning values to individual assets.

The buyer pays a lump sum, without assigning values to individual assets.

3.

Carry forward of losses

The benefit of carry forward of losses has not been provided for the purpose of a GCS in liquidation. However, in certain rulings[4], the Hon’ble NCLT has allowed carry forward of losses, but again, subject to approval of IT Authorities. See discussion below.

The Income Tax Act, 1961, does not allow carry forward and set off of losses when a business is sold as a going concern.

Section 79(2)(c) of the Income Tax Act, provides an incentive to resolution applicants and has allowed the benefit of carry forward losses where a change in shareholding takes place pursuant to a resolution plan.

4.

Profits

Profits during liquidation, if any, get subsumed in the liquidation estate, and distributed in accordance with section 53.

Assets and liabilities are transferred on a particular date.

At this juncture, having discussed the difference between the above mentioned modes of sale, it becomes important to discuss the accounting and taxation concerns which may have become the probable reasons for lesser use of GCS in Liquidation.

Accounting Concerns

Preparation of books of accounts in liquidation – Obligation of the Liquidator or Auction purchaser?

Section 35 of the Code enlists the duties and powers of the liquidator appointed under the Code, which has to be read with the provisions of the Liquidation Regulations.

Liquidation is a terminal process and as such, it is a settled principle that during the liquidation process, the liquidator does not prepare any balance sheet or profit and loss account. Instead, reg. 15(3) requires the liquidator to prepare a receipt and payments account on a cash-basis. Hence, the question of any preparation of profit and loss account or balance sheet does not arise.

However, after a GCS is completed, sale consideration is received and a sale certificate is issued by the liquidator in favour of the auction purchaser, the corporate debtor is transferred to the auction purchaser. At this juncture, an important question that raises its head is, who would be responsible to prepare the books of accounts of the corporate debtor post the completion of a GCS – Liquidator or an Auction purchaser.

Once the sale is completed, it becomes the responsibility of the acquirer to take all the necessary steps viz-a-viz the corporate debtor. It was held in the case of Gaurav Jain Vs. Sanjay Gupta (Liquidator of Topworth Pipes & Tubes Pvt Ltd)[5]:

“The Corporate Debtor survives, only the ownership is transferred by the Liquidator to the purchaser. All the rights, titles and interest in the Corporate Debtor including the legal entity is transferred to the purchaser. After the sale as a ‘going concern’, the purchaser will be carrying on the business of the corporate debtor.”

Thus, it may be concluded that once the corporate debtor is transferred to the acquirer, it should become the responsibility of the acquirer to prepare the books of accounts and annual financial statements of the Company. The Liquidator remains responsible only for the preparation of the receipts and payments account until the liquidation process is over.

However, the situation can get tricky when GCS takes place in the middle of a financial year. In such a situation, the following questions need to be answered for a smooth completion of GCS of the CD in liquidation.

What date should be considered as the date of sale?

Who prepares the financial statements for the entire financial year in which the sale takes place?

On the first question, one may note Schedule I of the Liquidation Regulations which states:

“On payment of the full amount, the sale shall stand completed, the liquidator shall execute a Certificate of sale or sale deed to transfer such assets and the assets shall be delivered to him in the manner specified in the terms of sale.”

Hence, ideally, the date on which sale certificate is issued should be taken as the date of sale.

On the second question, say, the sale takes place on 15th January, 2022. Should the acquirer prepare the financial statements for the entire FY 2021-22? Or, should the liquidator provide completed financial statements to the acquirer as on 31st March, 2022?

As indicated earlier, after sale, the responsibility to prepare financial statements, is that of the acquirer. Before sale, the liquidator does not prepare any balance sheet/profit and loss statement. Hence, the acquirer shall prepare financial statements from the period 15th January to 31st March, 2022 to close the accounts of the financial year.

Given how liabilities and assets are dealt with in a GCS in liquidation, the accounting shall be done as follows:

Asset Side:

In a GCS, the buyer pays a lump sum amount as sale consideration, without assigning values to individual assets. Therefore, the valuation of individual assets of the corporate debtor after completion of sale as a going concern shall be the responsibility of the acquirer. The acquirer puts a value on the assets of the corporate debtor, which is his bid price – it may, therefore, spread the purchase consideration paid by him to various assets of the corporate debtor as is commonly done in case of a slump sale.

Liabilities side:

All liabilities of the corporate debtor, including the share capital becomes a claim on the liquidation estate. As such the same are settled in terms of sec. 53 of the Code. Therefore, the question of carryover of any liabilities of the corporate debtor onto the books of the entity, acquired under GCS, does not arise.

In the matter of Gaurav Jain v. Sanjay Gupta (Supra), it was held by the Hon’ble NCLT, Mumbai bench that,

“The Applicant shall not be responsible for any other claims / liabilities / obligations etc. payable by the corporate debtor as on this date to the Creditors or any other stakeholders including Government dues. All liabilities of the Corporate Debtor as on the date stands extinguished, as far as the Applicant is concerned.”

“Creditors of the corporate debtor which include creditors in any form or category including government departments shall stand extinguished qua the Applicant”

[Emphasis Supplied]

As it has been discussed, there is no case of remission or cessation of liability, as it becomes a claim on the liquidation estate and not the corporate debtor. Thus, the question of writing off liabilities does not arise, let alone the taxability of the same under section 41(1) (a) of the Income Tax Act, 1961.

Note that, in certain cases, by agreement, buyers may take over certain liabilities. In that case, the acquired liabilities too, will appear on the new balance sheet.

Share Capital:

As for the share capital of the Corporate Debtor, the existing shares shall stand cancelled without there being any payment to the shareholders, since such shareholders assume the nature of claimholders upon commencement of liquidation, who shall be paid in terms of sec. 53 of the Code, only if proceeds from liquidation estate are that sufficient.

As regards recording of capital by the auction purchaser, the corporate debtor issues new shares to the extent of the share capital. It is understood that the consideration received from the acquirer will be split into share capital and liabilities, based on the capital structure that the acquirer decides.

Reference may be drawn from the IBBI Discussion paper dated 27th April, 2019,[6] which discusses the modalities of a GCS and says as follows;

“The consideration received from the sale will be split into share capital and liabilities, based on a capital structure that the acquirer decides. There will be an issuance of shares by the corporate debtor being sold to the extent of the share capital. The existing shares of the corporate debtor will not be transferred and shall be extinguished. The existing shareholders will become claimants front he liquidation proceeds under section 53 of the Code”

[Emphasis Supplied]

Tax Considerations

Tax issues under GCS would arise as a result of confusion surrounding the following:

Carry forward and set off of losses and unabsorbed depreciation – Section 115JB and Section 79(2)(c) of Income Tax Act, 1961.

Writing off Liabilities

Carry forward and set off of losses and unabsorbed depreciation – Section 115JB and Section 79(2)(c) of Income Tax Act, 1961

Carry Forward and set off of losses and unabsorbed depreciation – Section 115JB

Section 115JB of the Income Tax Act, 1961,[7] provides for levy of a minimum alternate tax (MAT) on the “book profits” of a company. For the purpose of computation of book profits, the said section allows a deduction in respect of the amount of loss brought forward or unabsorbed depreciation, whichever is less as per the books of accounts.

However, for companies whose application for CIRP under the Code has been admitted by the AA, a carve out has been provided. Accordingly, an aggregate of unabsorbed depreciation and loss brought forward shall be allowed to be reduced from the book profits, if any.

The Act provides that;

“(iih) the aggregate amount of unabsorbed depreciation and loss brought forward in case of a—

(A) company, and its subsidiary and the subsidiary of such subsidiary, where, the Tribunal, on an application moved by the Central Government under section 241 of the Companies Act, 2013 (18 of 2013) has suspended the Board of Directors of such company and has appointed new directors who are nominated by the Central Government under section 242 of the said Act;

(B) company against whom an application for corporate insolvency resolution process has been admitted by the Adjudicating Authority under section 7 or section 9 or section 10 of the Insolvency and Bankruptcy Code, 2016 (31 of 2016).”

[Emphasis supplied]

It can be clearly deduced from the provisions of the said section that the above mentioned carve out has been provided specifically for the purpose of a Resolution Plan during CIRP and not for a GCS in liquidation.

Carry forward of losses – Section 79(2)(c)

Additionally, Section 79(2)(c) of the Income Tax Act, 1961 (‘Act’)[8], provides that the benefit carry forward of loss cannot be taken where there has been a change in shareholding. However, to provide an incentive to resolution applicants, the Income Tax Act has allowed the benefit of carry forward losses where such change in shareholding takes place pursuant to a resolution plan.

However, no such exemption has been provided for the purpose of a GCS in liquidation. Hence, there exists uncertainty w.r.t the same. At this juncture, reliance may be drawn to certain NCLT rulings[9], wherein such benefit has been allowed by the Adjudicating Authority, subject to the approval by the concerned Income Tax Authorities under the relevant provisions of the Act.

Conclusion

While the process w.r.t. conduct of GCS has been explained by the Liquidation Regulations, the above discussed points have not been explicitly mentioned or ascribed in any guidance note or standards. Due to these uncertainties, these questions have often been subject to litigation, which leads to further delays. Hence, the need of the hour is a clear set of rules and standards, addressing the questions discussed above, as a result of which GCS is expected to gain further traction and deliver better results.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-02-23 11:00:092022-02-23 11:00:11Accounting and Tax considerations in Going Concern Sale in Liquidation

Entities are exposed to financial risks arising from many aspects of their business. The nature of the risks varies with the nature of the business activities carried on by the business entities, for example, some entities might be concerned about exchange rates or interest rates, while others might be concerned about commodity prices. Entities implement different risk management strategies to eliminate or reduce their risk exposures.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-02-22 13:00:572022-09-01 13:51:14Guide to Hedge Accounting under Ind AS 109/IFRS 9

On September 24, 2021, the RBI released Master Direction – Reserve Bank of India Securitisation of Standard Assets) Directions, 2021. The same has been released after almost 15 months of the comment period on the draft framework issued on June 08, 2020. This culminates the process that started with Dr. Harsh Vardhan committee report in 2019.

It is said that capital markets are fast changing, and regulations aim to capture a dynamic market which quite often leads the regulation than follow it. However, the just-repealed Guidelines continued to shape and support the securitisation market in the country for a good 15 years, with the 2012 supplements mainly incorporating the response to the Global Financial Crisis. Read more →

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2021-10-11 11:31:002022-09-01 14:02:06FAQs on Securitisation of Standard Assets

The financial statements of a company are not merely meant to show the profit or loss and/or assets and liabilities of the company. The notes to such financial statements also disclose various nuances that the shareholders of the company shall be aware of. Such disclosures may vary from material transactions with related parties to the purpose of inter-corporate loans, guarantee or security. The financial statements are meant to be prepared in accordance with Schedule III (‘Schedule’) to the Companies Act, 2013 (‘Act’). On March 24, 2021, MCA introduced more elaborative disclosure requirements regarding financial statements of companies which are effective from April 1, 2021 i.e. for financial statements prepared for FY 2021-22. One such requirement is disclosure of transactions with companies struck off by Registrar of Companies (‘RoC’) under section 248 of the Act, or under section 560 of the Companies Act, 1956. The following particulars are to be disclosed in such case:

Name of the struck off company

Nature of transactions with company

Balance outstanding and relationship with the struck off the company.

The transaction can be in the nature of investment in securities, receivables, payables, shareholding of the struck-off company in the company and any other outstanding balances.

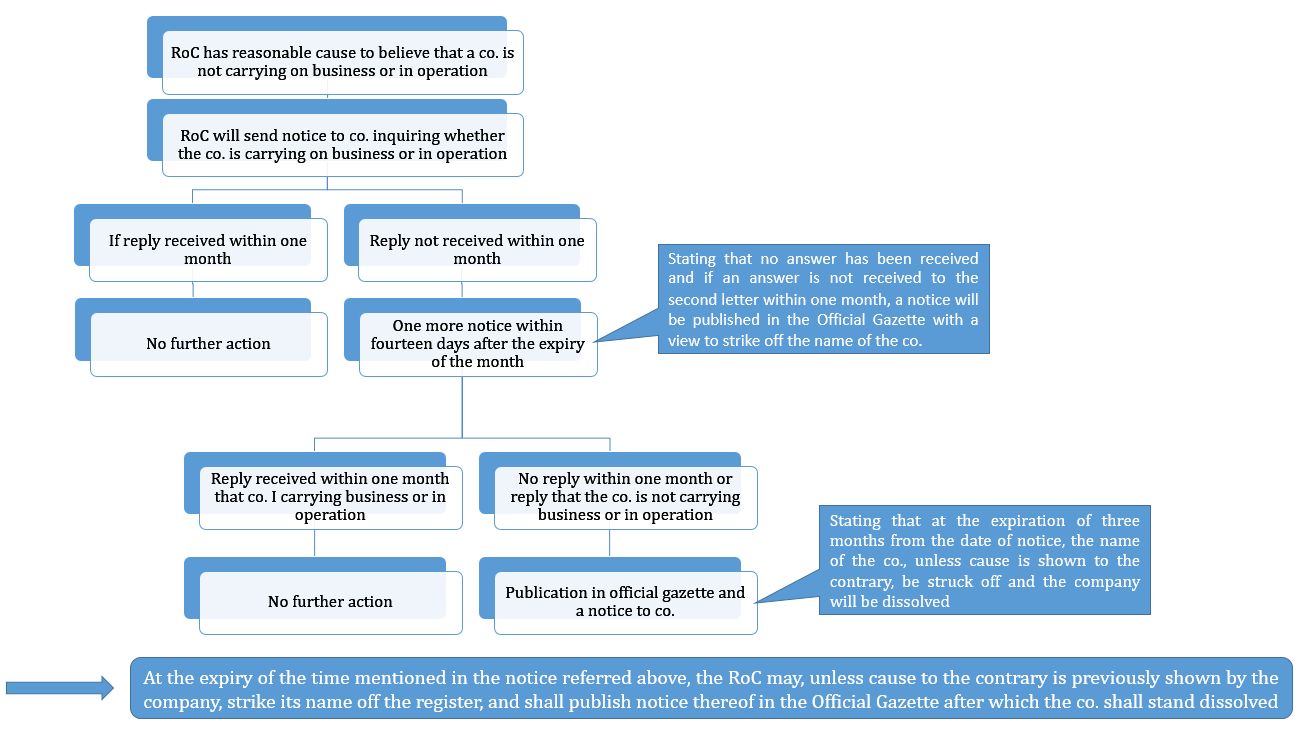

Before digging deep on the disclosure requirements, it is imperative to understand the provisions for striking off a company by RoC both under the Act as well as the Companies Act, 1956.

Under the Companies Act, 1956

Under the Act

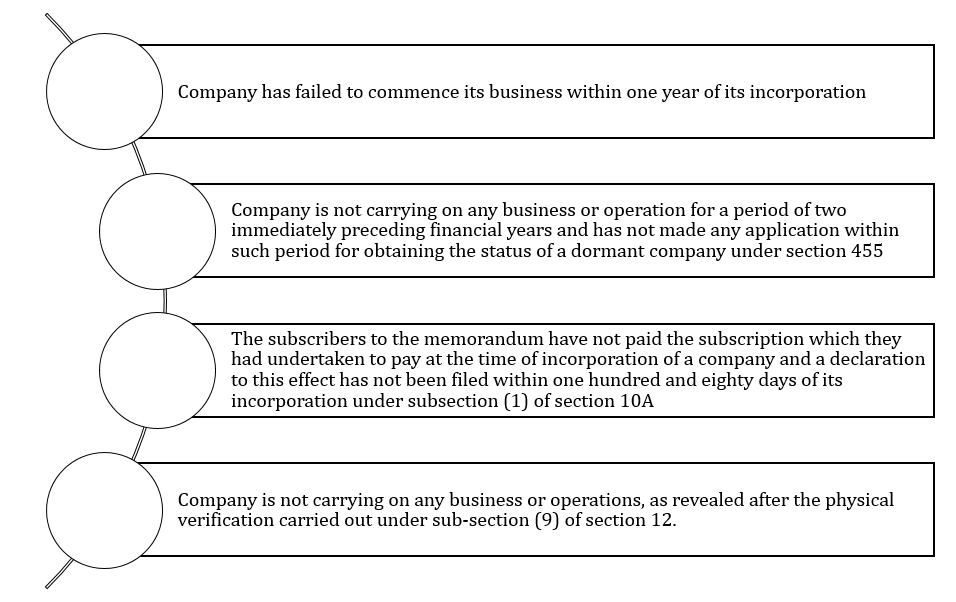

If the RoC has reasons to believe that:

A notice to the company and all the directors of the company, shall be sent by RoC articulating intention to strike off the name of the company and requesting them to send their representations within a period of thirty days from the date of the notice. At the expiry of the time, the RoC may, unless cause to the contrary is shown, strike off its name and shall publish notice thereof in the Official Gazette pursuant to which the company shall stand dissolved.

Further, a company may itself by passing a special resolution or consent of seventy-five per cent members after extinguishing all its liabilities, file an application to the RoC for removing its name on all or any of the grounds specified in the figure above.

Practical difficulties in disclosures

The disclosure requirements of transactions with companies the name of which has been struck off is too vigorous since it requires too much background work to be done on the end of companies. Further, MCA has been issuing circulars containing names of companies which have been struck off. The companies will literally have to struggle through such a cumbersome and tedious task to find out one name among the thousands as issued by MCA.

There are some more practical complications that needs to be highlighted where the name of the company, that has been struck off, as available in records of the company may not match with the one mentioned in MCA’s list:

Such company has merged with some other company

Such company has changed its name

Such company might have converted itself to some other kind of entity like LLP

Going further, even in terms of volumes, there are a bunch of companies with whom a company transacts in its course of business. Tracing each one of them and identifying those which has been struck off seems to be a next to impossible task for a lot of companies.

Recommendations for companies for complying with the requirements

The companies may opt for following systems and procedures depending upon the nature of transaction it has with a company the name of which has been struck off:

Nature of relationship

Practical way of dealing

Debtor

The company might look through debtors periodically, especially those the receivables from whom are due for too longer than the usual time.

Creditor

If the payment made by the company has bounced for more than once, they may check if the aforesaid has been struck off.

Investment in securities

Unless a co. is an investment company or NBFC, it will not have several investments. Therefore, it will be comparatively easy to track such companies.

Shares held by stuck off company

This one might seem like a demon. There are listed companies with lakhs of shareholders. One more point to be noted in this regard is there might be cases of restructuring where a company might have merged or demerged. In such cases, the resulting company will have to carry the baggage of the transferor company (old company) as well in this regard. We might also take into account that there are certain benami shareholders in many companies for which IEPF rules are already in place. Tracking the names of such companies which have been struck off from such a large number of shareholders and collating data is a next to impossible task.

Other outstanding balances (to be specified)

This is a residuary field which requires any outstanding balance with a struck off company to be disclosed. Needless to say, this is an open-ended heading and includes in its ambit any transaction that is not covered above. Through this, the reporting company is expected to get into an exercise of identifying all transaction(s) with a struck off company with which the company has outstanding balance as on the last day of reporting period.

Pursuant to the January 2022 edition of the ICAI Guidance Note on Division II – Ind AS Schedule III to the Companies Act, 2013 and Guidance Note on Division II – Non-Ind AS Schedule III to the Companies Act, 2013, the following guidance is provided with respect to disclosure of information regarding outstanding balances with struck off companies:

Identification of struck-off company

The names of the companies are required to be searched / authenticated from public notice (STK-7) during the reporting period or any previous year(s), if balances with such companies are outstanding as on the last day of the reporting period.

Further, there should not have been any order for restoration of the name of such companies before the approval of the financial statement. It may be noted that this again is an task to track if the name of the companies have been restored vide order of any NCLT any other adjudicating authority as the orders remain scattered and at times not timely uploaded on the website.

Amount of balance outstanding

(1) The gross carrying amount is required to be disclosed without netting any provision for doubtful debts or impairment loss allowance.

(2) Infact the Guidance Note states that even such transaction which might have happened during a financial year and settled/reversed/squared off, etc., during the same financial year such that the balance outstanding is NIL as at the end of the reporting period, even such transactions are required to be disclosed. This adds up to the anyway unending disclosure in this context. There may be a situation where a company is not a struck off company at the time of transaction but eventually becomes one and is a struck off company as on the last day of the reporting period. With the point (2) above, one is left to an endless thought whether the reporting company is required to review all the transactions it had during the previous year(s)? because only then it may be able to track if there is any entry which might come under point (2) above.

Relationship with the struck-off company, if any, to be disclosed

In this field, the company is required to disclose its relationship, if any, with the corresponding struck-off companies as per section 2(76) of the Act, as on the balance sheet date.

Details not to be included

Companies whose names were struck off during the financial year but the order had been passed by any adjudicating authority (for e.g., NCLT) name before approval of the financial statements.

Conclusion

In a nutshell, MCA is asking companies to search for the dead man but the dead man isn’t waking up. There might be cases where the name/identity of the dead man would have already been extinguished or changed during its lifetime. We understand that the intent of the Government is to read out all the struck off companies from the database of corporates. However, to effectively meet this purpose, MCA may opt to come out with a digital database of all companies which have been struck off either under the Act or the previous Act since it will facilitate companies to search data at one place. This might not be a complete way out but due to the practical hassles as discussed above in the article, MCA needs to review the requirement considering the practical issue being faced by the companies and introduce systems in place to enable compliance.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2021-10-09 19:09:072022-03-09 17:14:37Disclosure in financial statements: Relationship with struck off companies