Trust, but verify: AIFs cannot be used as regulatory arbitrage

SEBI mandates ongoing due diligence for investors and investments made by AIFs

-Vinita Nair, Senior Partner and Lavanya Tandon, Executive | corplaw@vinodkothari.com

May 03, 2024 (updated on October 9, 2024)

Background

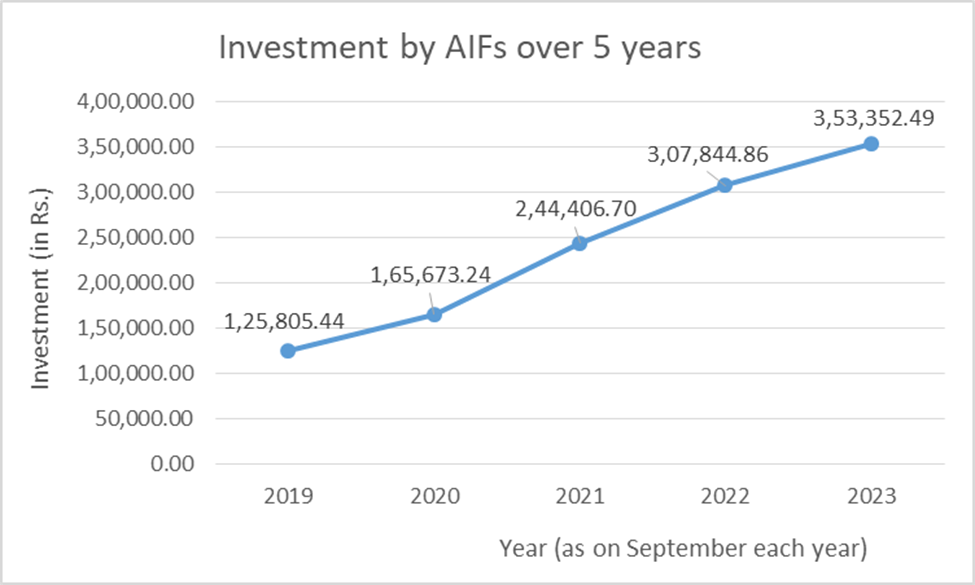

SEBI had raised concerns relating to evergreening of loans, circumvention of FEMA norms, QIB regulations and other concerns on regulatory arbitrage by Alternative Investment Funds (‘AIFs’) in its Consultation Paper issued in January, 2024. SEBI also recorded 40+ cases wherein the structure of AIF had been abused and used to circumvent extant financial sector regulations. Read our analysis in the article ‘AIFs ail SEBI: Cannot be used for regulatory breach’ dated January 31, 2024. Further, RBI had also barred all regulated entities (REs) with respect to their investments in AIFs, discussed in our article.

Subsequent to receipt of public comments, the proposal to mandate due-diligence (‘DD’) of investors and each of the investments made by the AIF was approved in the SEBI Board meeting held on March 15, 2024. SEBI notified SEBI (Alternative Investment Funds) (Second Amendment) Regulations, 2024 effective from April 25, 2024 amending Reg. 20 of the SEBI (Alternative Investment Funds) Regulations, 2012 (‘AIF Regulations’) dealing with general obligations thereby requiring every a. AIF, b. investment manager of the AIF, c. KMP of the AIF, and d. KMP of the investment manager, to exercise specific DD with respect to their investors and investments in order to prevent facilitation of circumvention of such laws as may be specified by SEBI from time to time.

The list of laws, thresholds and conditions for DD, reporting requirements etc. has been provided in SEBI circular dated Oct 8, 2024 (‘SEBI Circular’). DD is required to be carried out prior to making of investments as per implementation standards formulated by Standard Setting Forum for AIFs (‘SFA’) and published on websites of the industry associations which are part of the SFA, i.e., Indian Venture and Alternate Capital Association (‘IVCA’), PE VC CFO Association and Trustee Association of India.

Scope of laws covered under the ambit of due diligence

The list of laws provided in the SEBI Circular comprises of the following:

- Provisions of SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (‘ICDR Regulations’), and other regulations of SEBI wherein benefits or relaxations have been provided to entities designated as Qualified Institutional Buyers (‘QIBs’).

- Provisions of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (‘SARFAESI Act’) wherein benefits are provided to entities designated as Qualified Buyers (‘QBs’).

- Prudential norms specified by RBI for regulated lenders with respect to Income Recognition, Asset Classification, Provisioning and restructuring of stressed assets;

- Rule 6 of FEMA (Non-Debt Instruments) Rules, 2019 (NDI Rules) for investment from countries sharing land border with India ( read with Press Note 3 dated April 17, 2020 of FDI Policy 2020)

Timing, thresholds for DD, reporting requirements

Pursuant to the SEBI Circular, the due diligence for various investors and investments is required to be carried out by a. AIF, b. investment manager of the AIF, c. KMP of the AIF, and d. KMP of the investment manager in accordance with the Implementation Standards. The table below indicates in brief the criteria, checkpoints and timelines for conducting due diligence along with the consequences of the outcome.

| Sr. No | Objective intended to be achieved by investors through investments in AIF scheme | Regulations/ Directions/ Norms applicable | Applicability of requirement of DD for every scheme of AIF (refer Note 1) | Checkpoints for manager for specific DD | Timing of DD | Consequence of outcome of DD & reporting requirements, if any |

|---|---|---|---|---|---|---|

| 1 | Benefits designated for QIBs | ICDR and other SEBI Regulations | If an investor, or investors belonging to the same group, contribute(s)50% or more to the corpus of the scheme. | Manager to check if such if investor/ investors of the same group is/are:(i) QIBs themselves or,(ii) Entities established, owned or controlled by the Central Government or a State Government or the Government of a foreign country, including central banks and sovereign wealth funds.Note: Where such investor is an AIF or fund set up in IFSC or outside India, above check to be carried out on a look through basis. | Prior to availing benefits available to QIBs | Refer Note 2 below for existing investments & Note 3 for proposed investments.Manager to provide confirmation to SE or lead manager or merchant banker on this. |

| 2 | Benefits designated for QBs | Under SARFAESI Act | If an investor, or investors belonging to the same group, contribute(s)50% or more to the corpus of the scheme. | Same as above | Prior to making any investments or availing benefits | Refer Note 2 below for existing investments & Note 3 for proposed investments. |

| 3 | RBI regulated lenders/ entities ever-greening their stressed loans/ assets & circumventing RBI norms | RBI norms on Income Recognition, Asset Classification, Provisioning and Restructuring of stressed loans/ assets | (a)whose manager or sponsor is an entity regulated by RBI; or,(b)that has investor(s)regulated by RBI who:(i)individually or along with investors of the same group contribute(s) 25% or more to the corpus of the scheme; or(ii) is an associate of the manager/ sponsor of the AIF;(iii) has majority or veto power [by itself, or through its representatives/ nominees] in voting over decisions of the investment committee set up by the manager to approve investment decisions of the scheme.Note: where investor is an AIF or fund set up in IFSC or outside India, criteria check to be carried out on a look through basis. | Refer Note 4. | Prior to making any investments, to avoid indirect investment by RBI regulated lender/ entity. | Refer Note 2 below for existing investments & Note 3 for proposed investments. |

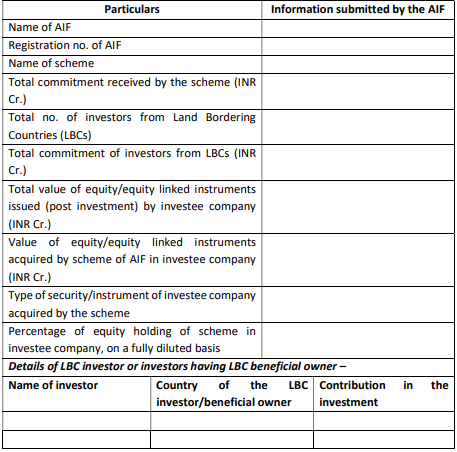

| 4 | Investment from countries sharing land border with India | FEMA (NDI) Rules, 2019 | Where 50% or more of the corpus of the scheme is contributed by investors (a)who are citizens of/are from/are situated in a country which shares land border with India; or(b)whose beneficial owners, as determined in terms of Rule 9 (3) of the PMLA (Maintenance of Records) Rules, 2005, are citizens of/are from/are situated in a country which shares a land border with India. | If the proposed investment would result in the scheme holding 10 % or more of equity/equity-linked securities issued by the company (on a fully-diluted basis), the manager to check details stated in the previous column, by collecting information on the country of investors and their beneficial owners. | Prior to making any investment | Refer Note 2 below for existing investments & Note 5 for proposed investments. |

Note 1: same group’ shall mean ‘related parties’ and ‘relatives’ as defined in SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

Note 2:

For Sr nos 1 to 3: DD requirement is applicable for existing investments too, held by AIF schemes as on October 8, 2024:

- If DD check not satisfactory – details of investment to be reported to AIF’s custodian on or before April 07, 2025, in the format as per Annexure 1 of the circular;

- If DD check satisfactory – AIF manager to submit an undertaking to AIF’s custodian on or before April 07, 2025.

For Sr no. 4: Reporting is required to be made for existing investments held by AIF schemes as on October 8, 2024 if the scheme holds 10% or more of equity/ equity-linked securities on a fully-diluted basis, to AIF’s custodian on or before April 07, 2025 in the format prescribed by SFA.

Note 3:

Consequence of not satisfying requirements of DD checks specified by SFA for proposed investments in case of Sr nos 1 to 3:

- Such investor or investor group to be excluded along with necessary disclosure in the private placement memorandum (PPM); or

- Investment cannot be made.

Note 4:

Note 5: Details of investment, which would result in the scheme holding 10% or more of equity/ equity-linked securities on a fully-diluted basis, to be reported to the custodian within 30 days of investment, in the below format specified by SFA.

DD requirement – one-time or ongoing?

As discussed in the SEBI BM Agenda, the purpose of the due-diligence check is to prevent facilitation of any circumvention of provisions of financial sector regulators, which cannot be a time specific check. An entity who intends to circumvent can design the structure in such a way that, at a later date post investment, it acquires the units of AIFs post investment, such as buying the units of an existing investor or by acquiring control over the existing investor entity, as per prior arrangement. Accordingly, it has been indicated that due diligence around investors and investments will be an ongoing one.

Applicability of DD – prospective or retrospective?

As per the SEBI circular this is applicable for existing and prospective investments. Refer Note 2 above.

Obligations of Custodian to the AIF

- Information received from AIFs under Note 2 to be furnished to SEBI on or before May 7, 2025.

- Information received from AIFs in terms of Note 4 above on a monthly basis to be compiled and reported to SEBI within 10 working days from month end.

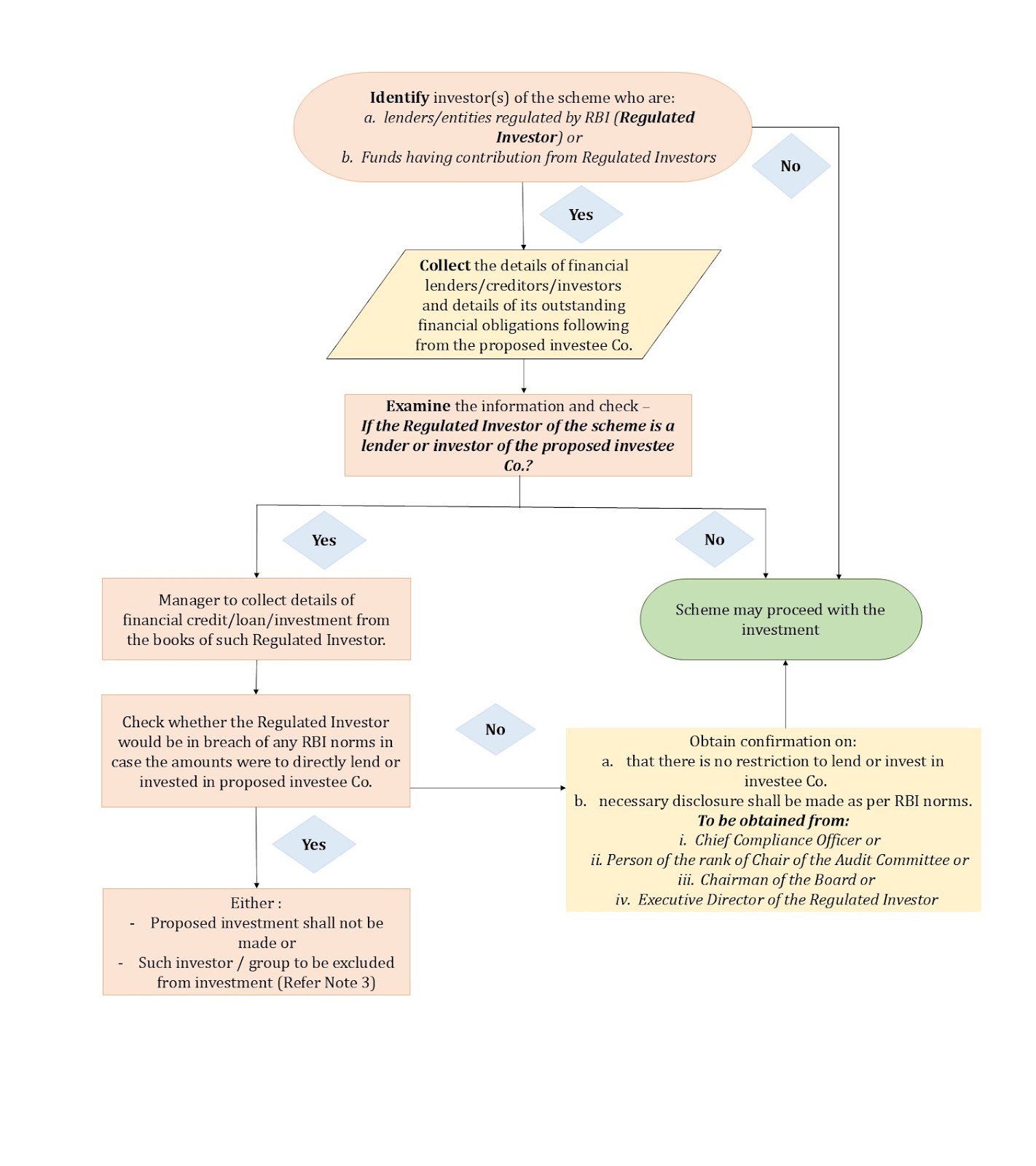

Power of AIF to exclude an investor

As per SEBI Circular, in cases where the outcome of DD is not satisfactory, in that case the AIF will either have to exclude the investor or investor group or abstain from making the proposed investment.

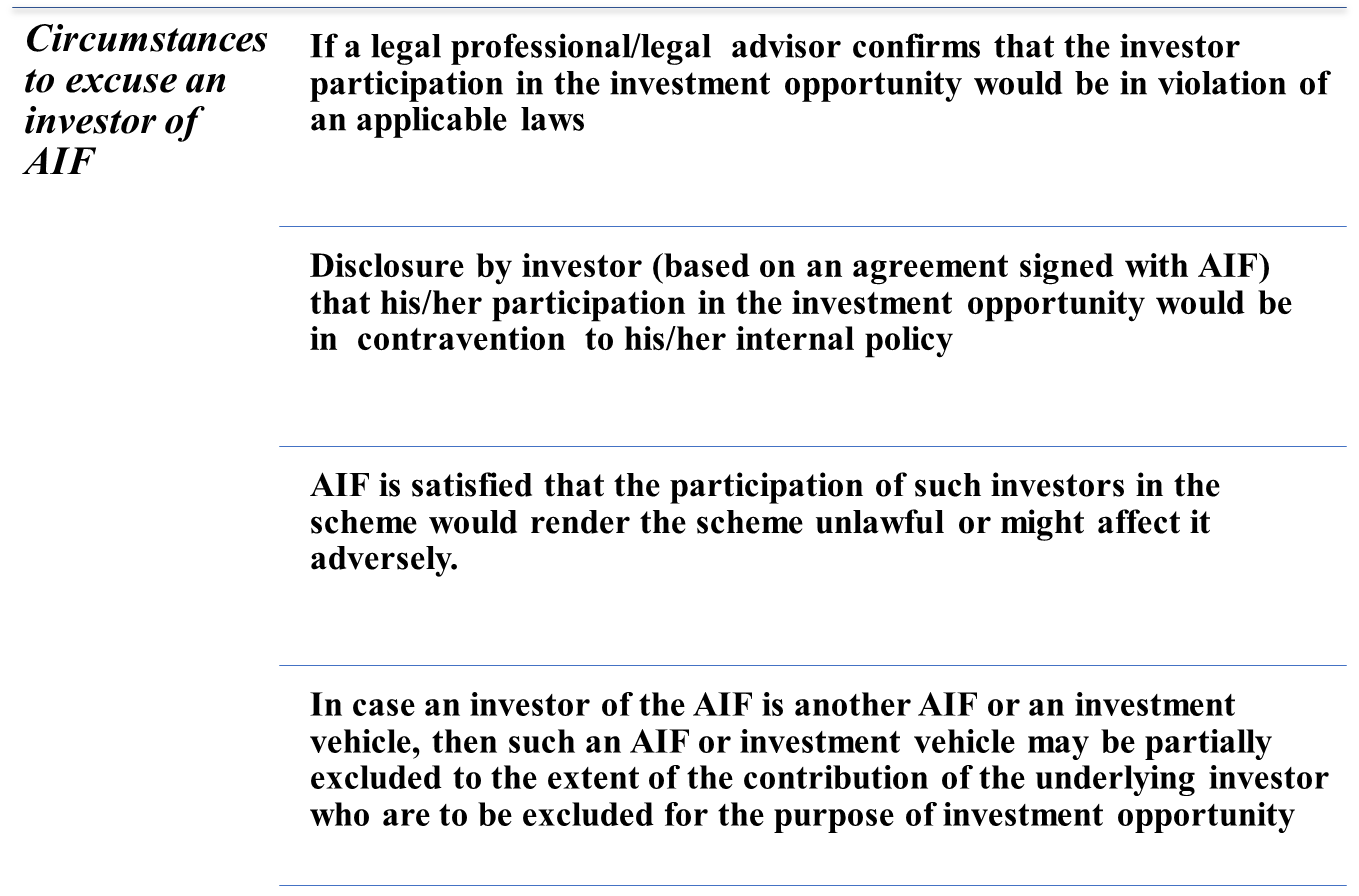

Dealing with power to exclude an investor, in April 2023 SEBI had issued ‘Guidelines with respect to excusing or excluding an investor from an investment of AIF that empowered an AIF to excuse its investor from participating in a particular investment in the following circumstances:

Figure 1: Circumstances to excuse an investor of AIF

Conclusion

The present amendment and SEBI Circular lays an onerous burden on the AIF, manager and KMP of the AIF and the manager. The DD requirement has become effective from October 8, 2024 and applies to existing investments as well. The AIFs have an actionable of evaluating the existing investments in the scheme in the light of the present amendment and ensure reporting in next 6 months. The obligation of on-going due diligence will result in a compliance burden, but is justified given the intent of law as “quando aliquid prohibetur ex directo, prohibetur et per obliquum” i.e. things that cannot be done directly should not be done indirectly either. AIFs will continue ‘trust, but verify’ using the DD standards for due diligence. The trustee/ sponsor of the AIF is required to ensure that compliance status of this amendment is reported to SEBI in the ‘Compliance Test Report’ prepared by the manager in terms of Chapter 15 of Master Circular for AIFs.

Our other resources: