Presentation on Value Chain Partners for Financial Institutions

Watch our YouTube video here.

See our Resource Centre on BRSR here.

Watch our YouTube video here.

See our Resource Centre on BRSR here.

Palak Jaiswani, Manager & Simrat Singh, Executive | corplaw@vinodkothari.com

Refer consultation paper here.

Loading…

Loading…

Our resources on the topic:

-An emerging and promising financing substitute

Surabhi Chura | corplaw@vinodkothari.com

There has been a growing emphasis on sustainability across various sectors including finance, especially, with a growing mandatory requirement of disclosure of sustainability practices by companies around the world. Various sustainability-linked finance products are designed to promote the ESG objectives of the borrower while providing financial solutions.

Traditionally, loans have remained the most common way of raising finance, and sustainable finance is no exception to the same. These loans may be labelled as green loans, social loans, sustainable loans etc. Various organisations have issued voluntary guiding principles around the same[1]. A commonality in these loans is the restriction on the “use of proceeds” – that are directed towards the green, social or sustainable objectives of the borrower. Another form of sustainable finance through loans is Sustainability-linked Loans (SLLs), where the loan contains certain sustainability-linked terms. Contrary to typical green finance products, which allocate funds for designated green projects or assets, SLLs align the loan conditions with the sustainability performance of the borrower.

Other instruments of raising sustainable finance can be through the issuance of labelled bonds or GSS+ bonds. Read more about the same in our article – Sustainable finance and GSS+ bonds. One of the more recent innovative ways of financing sustainability objects of the borrower can be through Sustainability-linked derivatives.

Read more →– Payal Agarwal, Manager (payal@vinodkothari.com)

The consequences of climate change and the need for a positive climate action need no introduction in the present world. What once remained a matter of concern for the so-called “environmental activists”, gradually traveled their way to the government as countries committed towards achieving “net zero”. Climate action requires involvement of the masses, and therefore, the government is coming up with new regulatory devices towards developing climate action on a large scale.

India is no exception to the same, and following the footsteps of other countries, has proposed to develop a compliance mechanism and domestic market for carbon credits in India. Regulatory inclusion is provided to carbon credits in India by way of an amendment to the Energy Conservation Act, 2001 (“ECA”). Carbon credits are a form of emission trading schemes (ETS), that incentivize the reduction in emissions, against the offsetting of higher emissions by other market participants. A brief comparison of the domestic ETS in other parts of the world, and the existing emissions trading markets in India can be referred to at Emission law amendments: Laying the framework for Carbon trading market in India.

Read more →– Alignment with international standards and avoidance of greenwashing

– Payal Agarwal and Shreya Salampuria | corplaw@vinodkothari.com

Sustainability labeled bonds, more popularly known as GSS+ bonds, are looked upon as one of the primary means of raising funds towards sustainable development. The same has been discussed in Sustainable finance and GSS+ bonds: State of the Market and Developments. India is also not oblivious to the concept of GSS+ bonds, and companies in India have also been issuing such bonds, in one or more forms.

The issuance of green debt securities (“GDS”) in India was initially formalized through a circular issued by SEBI in 2017 in this regard, later absorbed under the SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021 (“ILNCS Regulations”) read with Chapter IX of the Operational Circular on the same. The regulatory framework for GDS in India has since been reviewed, and following a Consultation Paper on Green and Blue Bonds as a mode of Sustainable Finance (“Consultation Paper”) dated 4th August, 2022, SEBI, in its meeting dated 20th December, 2022 (“Board Meeting”) has approved amendments to the existing regulatory framework for GDS issuance. The press release of the Board Meeting reads as “in the backdrop of increasing interest in sustainable finance in India as well as around the globe, and with a view to align the extant framework for green debt securities with the updated Green Bond Principles (GBP) recognised by IOSCO, SEBI undertook a review of the regulatory framework for green debt securities.”

Pursuant to the review of the regulatory framework for GDS, the following has been notified –

In this write-up, we intend to discuss the revised regulatory framework for GDS issuance in India.

Read more →– Vinod Kothari and Payal Agarwal | corplaw@vinodkothari.com

Readers of financial statements get to know the performance of the company in terms of its financial accomplishments, asset values, etc. However, in a world where sustainability of business models in not very long run will be impacted by environment, climate change, social factors, etc., readers of financial statements also need to be informed about the sustainability aspects of a company’s business model.

Over time, sustainability reporting, either on voluntary basis or as a part of listed company reporting, has become a widely accepted practice, at least by large companies. A KMPG Survey of 2022 states that “rates of sustainability reporting among the world’s leading 250 companies are at an impressive 96 percent”.

While there have been various voluntary sustainability reporting standards such as GRI Standards, SASB Standards, CDP Standards, IIRF, GHG protocol etc, the most recent development in the field of sustainability reporting standards is the IFRS Sustainability Standards, prepared as a consolidation of various major sustainability reporting standards around the world. Further, various countries, mostly through the stock exchanges, have formulated their own mandatory sustainability reporting requirements in full or partial adoption of such voluntary standards.

Currently, the sheer multiplicity of standards is baffling. In mid-2019, the NYSCPA ran an article titled As Sustainability Frameworks Multiply, Navigating Them Becomes a Concern. It quoted the-then chair of IASB saying: “There are simply too many standards and initiatives in the space of sustainability reporting”. The situation is seemingly leading to some consolidation, as the various standards bodies are collaborating. However, even as of now, there is no clear sense of direction, as the requirements of mandated sustainability reporting quite often differ from those of voluntary standards such as GRI.

Read more →– Payal Agarwal and Neha Sinha | corplaw@vinodkothari.com

The importance of ESG aspects in the corporate world does not need an introduction in the current scenario. As the concept travels from the global conferences to the corporate boardrooms, so do the risks and opportunities of the same. Climate change has evolved from an “ethical, environmental” issue to one that presents foreseeable financial and systemic risks (and opportunities) over mainstream investment horizons, as discussed in detail in the Fiduciary Duties and Climate Change in the United States published by Commonwealth Climate and Law Initiative (CCLI). The corporate laws provide a general duty of the directors towards the protection of the environment, and therefore, directors cannot deny their responsibilities towards the same. The same has been dealt with at length in our writeup “Directors’ Liability towards Climate Change: Why Boards should be bothered”.

In this article, the authors try to look at the kinds of litigation in the field of climate change where corporations have been held accountable and identify the potential of litigation risks and the extent to which the directors of a company can be held liable for the climate change actions.

Read more →– Payal Agarwal, Vinod Kothari & Company (payal@vinodkothari.com)

This version: 23rd December, 2022

The Energy Conservation (Amendment) Bill, 2022 (“Bill”) seeks to provide a regulatory framework for carbon markets in India. The Bill was passed in the Lok Sabha on 8th August, 2022, and has been passed in the Rajya Sabha on 12th December, 2022. The President’s asset is all that is required to bring the carbon markets within the statutory framework of India. However, there is still a long way to go before carbon markets are implemented in India, which will require notification of the procedures and rules governing the same. Further, the carbon markets in other countries are still developing in a phased manner, identifying the gaps in the existing system and modifying accordingly. India cannot be an exception to the same. However, the concept of “carbon credits” is not unknown to India since there are several entities in the country which are already generating tons of carbon credits. This article seeks to delve upon the legal aspects of carbon credits markets around the world, the consequences of not exporting the same, and the tax implications upon sale of the generated credits. As we study the existing carbon markets around the world, some learnings from these markets may be taken into consideration for the developing carbon market in India.

Read more →Having dealt with the detailed actionable required under each of the NGRBC principles, in our article Getting ready to implement BRSR from FY 2022-23 (Part-I), in this article, we aim at guiding the management at “how” the reporting entity needs to prepare itself for the successful BRSR implementation.

While a company prepares itself for principle-wise disclosures, the general, management and process disclosures are also very significant in terms of providing an overview of the entity’s take on ESG and sustainability.

This part deals with the basic details of the reporting entity, the products and services it provides, locations and markets it operates in, types of customers it serves, details of employees, board and KMP and the group structure. Part VII of this Section is of much relevance and attracts some preparatory actions on part of the reporting company.

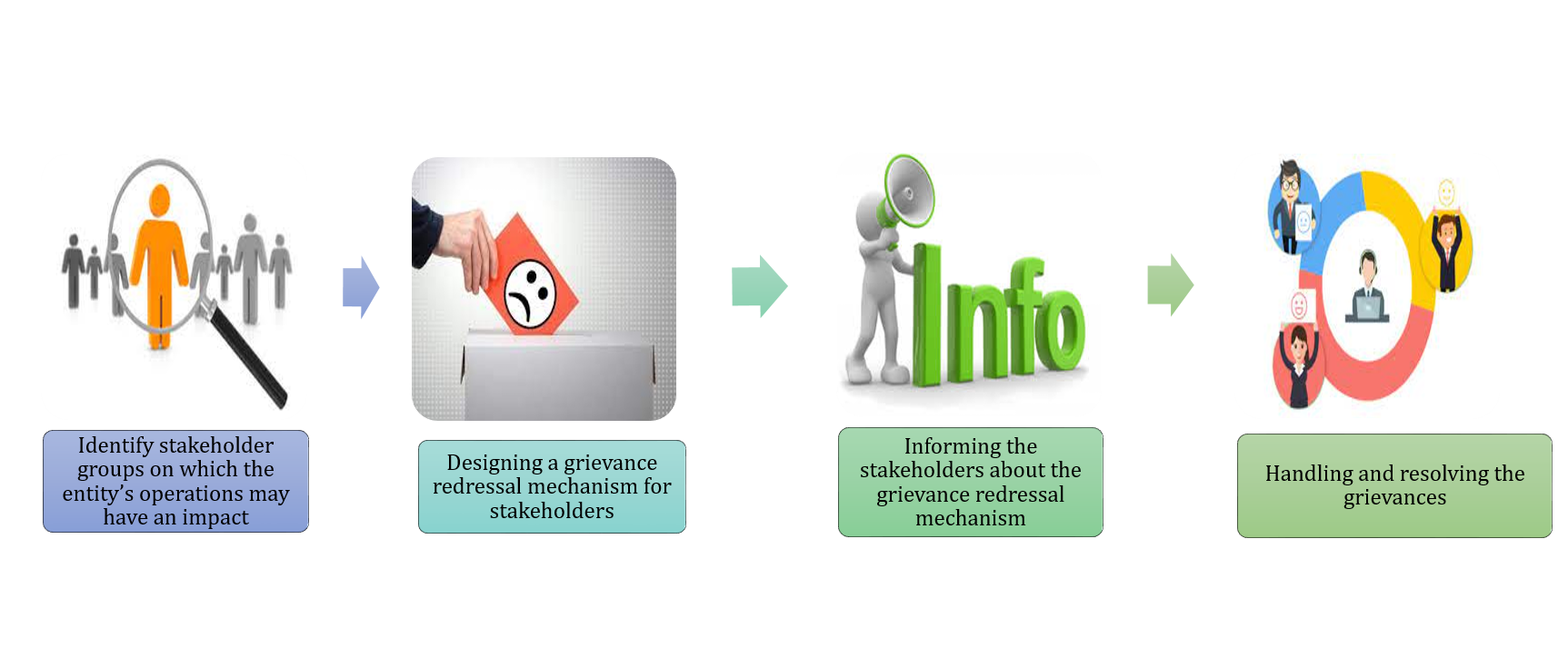

Clause 23 of Part VII of Section A requires disclosure on the complaints/ grievances received on any of the nine principles on which the BRSR is based. It requires a company to –

BRSR requires identification of the stakeholder group since the company is required to report on the complaints received by them. While the format lists out some stakeholder groups such as community, investors (other than shareholders), shareholders, employees and workers, customers and value chain partners, it is an inclusive list and retains scope for identification and inclusion of other stakeholder groups. The term “stakeholder” has been defined in the Guidance Note as –

Stakeholders are individuals or groups concerned or interested with or impacted by the activities of the businesses and vice-versa, now or in the future. Typically, stakeholders of a business include, but are not limited to, its investors, shareholders, employees and workers (and their families), customers, communities, value chain members and other business partners, regulators, civil society actors, and media.

| Therefore, any individual or group impacted or having the potential to be impacted by the operations of the entity at any point in time may be identified as the stakeholder group for the company. This includes government, regulators, media, NGOs, public trusts and charitable societies, apart from the direct stakeholders listed in the format itself. | ‘impact’ refers to the effect an organization has on the economy, the environment, and/or society, which in turn can indicate its contribution (positive or negative) to sustainable development.[1] |

Identification of stakeholders is particularly relevant for P4 which requires business to respect the interests of and be responsive to all stakeholders.

The term community has not been defined in the Guidance Note as well as NGRBC principles. The GRI Standards Glossary defines local community to mean “persons or groups of persons living and/or working in any areas that are economically, socially or environmentally impacted (positively or negatively) by an organization’s operations.” In the context of a listed entity, people from all around the country, as well as other parts of the world where the entity operates, or receives investments from, will be included in the meaning of community and construed likewise.

[1] GRI Standards Glossary – (Page 12)

As specified in the Guidance Note –

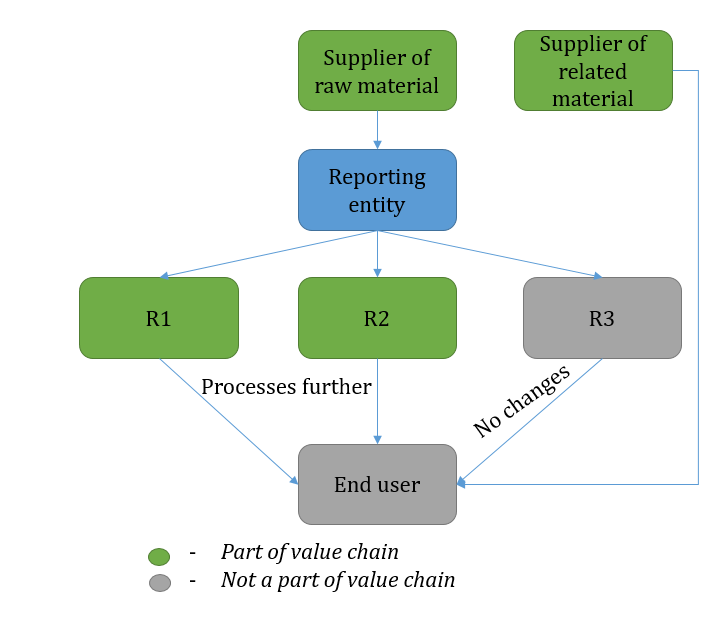

An organization’s value chain encompasses the full range of an organization’s upstream and downstream activities that convert input into output by adding value. It includes entities with which the organization has a direct or indirect business relationship and which either –

(a) supply products or services that contribute to the organization’s own products or services, or

(b)receive products or services from the organization.

Therefore, addition of value is important for identifying an entity as a value chain partner. For example, in the case of a car manufacturing entity, the suppliers of raw materials such as steel, aluminium etc are value chain partners. Similarly, the supplier of related material such as fuel for cars, may also be identified as a VCP, considering they have a role in adding value for the ultimate user. Products manufactured by the reporting entity may further be re-processed (R1 and R2) by the recipients or be sold as such. In case no further value is added before selling it to the end user, such downstream recipient (R3) cannot be identified as a VCP.

The reference to VCP can be found under P1 (ethics, integrity and transparency), P3 (employee well-being) and P5 (human rights).

The NGRBC defines grievance redressal mechanism to mean, “Mechanism for any stakeholder individually or collectively to raise and resolve reasonable concerns affecting them without impeding access to other judicial or administrative remedies.”

BRSR requires reporting of grievance redressal mechanisms in respect of employees (P3), human rights concerns (P5) and community (P8).

The objective of providing a grievance redressal mechanism serves various purpose:

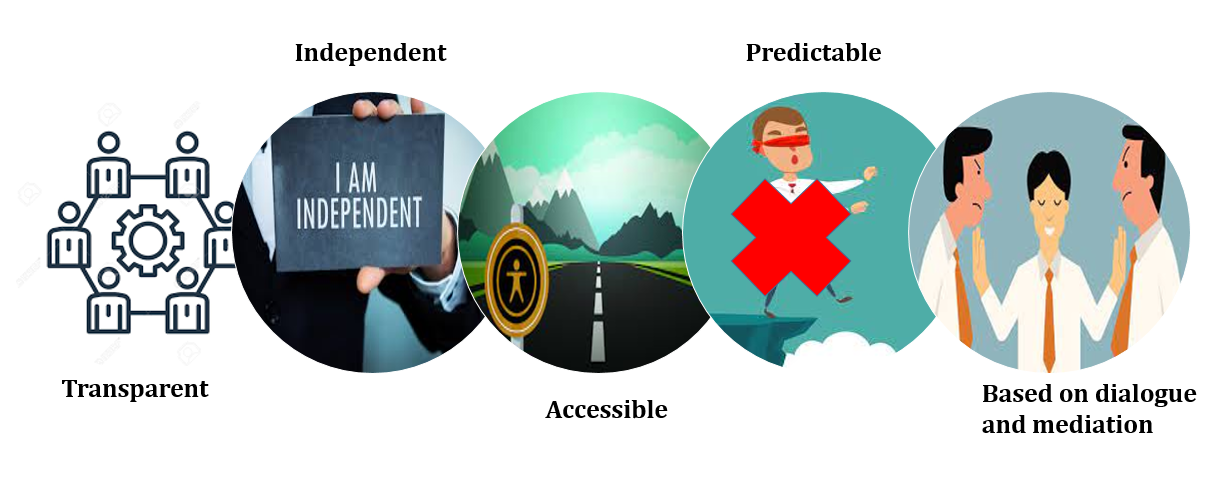

Features of effective grievance redressal mechanism –

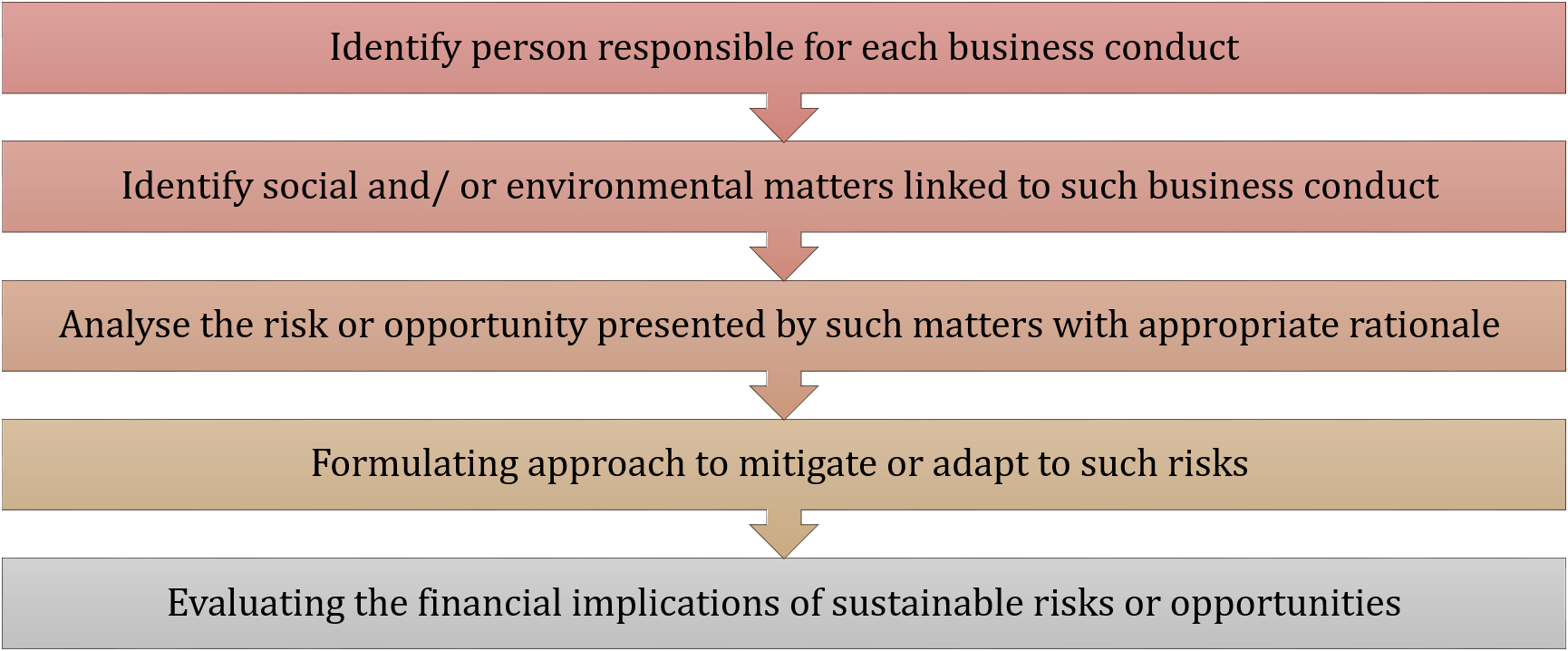

This is yet another significant clause of reporting. The reporting entity is required to indicate the material responsible business conduct of the entity, and sustainability issues pertaining to the social and environmental matters that present a risk or an opportunity to the business of the entity. In order to report on this clause, the reporting entity needs to have a well-defined system in place. It involves the following –

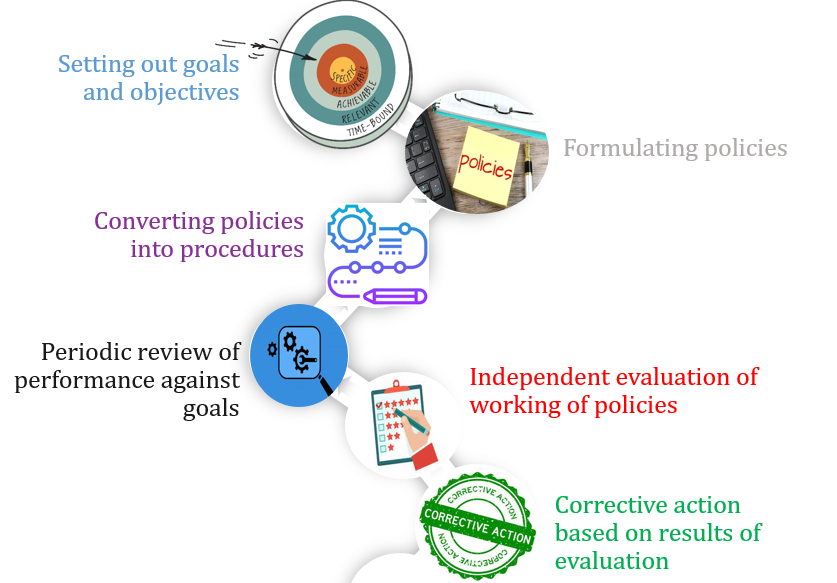

For the purpose of proper implementation of BRSR, one needs to know what is to be done, how the same has to be done and who is the ultimate authority to be reported to. Therefore, this Section aims at setting out goals and objectives, formulating policies on how the same should be achieved and converting the same into procedures, performance on stated goals and review by relevant responsible authorities. Furthermore, the performance against goals needs to be evaluated independently, and based on the “maker-checker” concept, it is always advisable to get the same evaluated by an external agency.

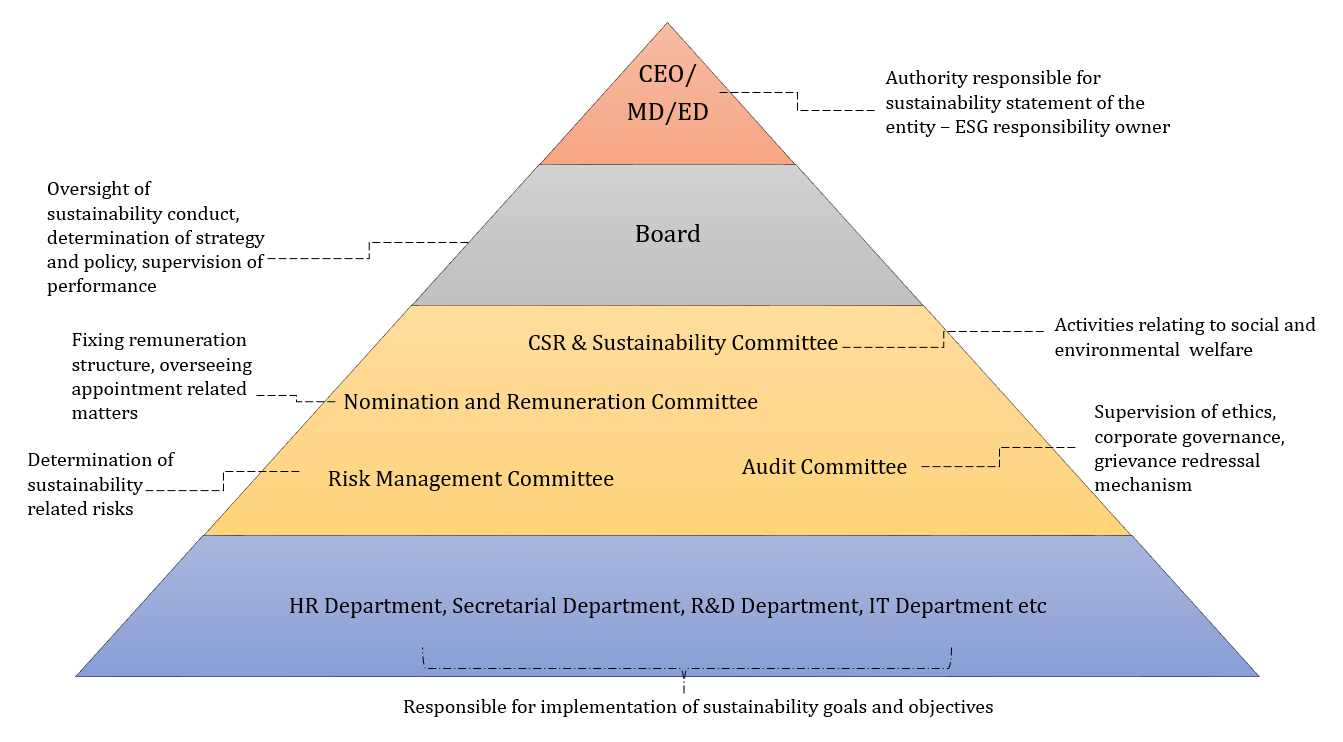

Implementing BRSR requires a comprehensive approach starting from setting up of goals and ending with review of corrective actions taken based on the assessment. While it is the call of the reporting entity to decide the governance outlook of BRSR, given below is an indicative governance structure for BRSR –

Please note that the above is, but only an indicative structure towards the BRSR governance. Companies may, on the basis of their size and nature, adopt different governance structures towards BRSR implementation and supervision.

Section C deals with the principle-wise disclosures, dealing with each of the nine principles of NGRBCs. Below, we provide the indicative contents of the policies that a reporting entity may be required to frame and the laws relating to the theme of each of the principles. Please note that the laws are not generic and their applicability may vary on the basis of the nature of operations of the reporting entity.

| Principle 1 – Businesses should conduct and govern themselves with integrity, and in a manner that is ethical, transparent, and accountable | |

| Policy to be framed | Broad contents of the policy |

| Code of Conduct and Ethics | ● Specify the values and ethics of the company ● of the employees, workers, board and management of the company ● Define responsibilities of board ● Designate authority responsible for governance of ethical conduct and receiving complaints on same ● Ethical conduct includes respect for stakeholders, equitable treatment, fair dealings, transparency of information, exercise independent judgement ● Identification and managing potential of conflicts of interests |

| Suppliers’ Code of Conduct | |

| Anti-Corruption and Anti-Bribery Policy | ● Incidents that amount to corruption ● Zero retaliation against bribery ● Legitimate vs prohibited gifts and hospitality ● Means for reporting instances of corruption and bribery ● Actions taken against the alleged or accused |

| Code of Conduct under Insider Trading | The same is a statutory requirement under SEBI (Prohibition of Insider Trading) Regulations, 2011 |

| Whistle blower Policy | Statutory requirement in terms of Section 177 of the Companies Act, 2013 read with Regulation 18 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 |

| Laws relevant to the Principles | Compliances required to be ensured |

| The Prevention of Corruption Act, 1988 | ● Prohibition on payment of gratification to public servant ● Prohibition on taking gratification for exercise of personal influence with public servant |

| Prevention of Money Laundering Act, 2002 (‘PMLA’) | ● Identifying principal officer having access to top management for ensuring compliance with PMLA provisions ● Maintain record of potentially suspicious transactions as specified in relevant rules ● Evolving internal mechanism for proper maintenance and preservation of records and quick retrieval of data ● Formulate and review at regular intervals, policies and procedures on prevention of money-laundering and terrorist financing |

| The Companies Act, 2013 | ● Obtaining requisite approvals before entering into Related Party Transactions ● Obtaining requisite approvals before entering into contracts/ arrangements in which the director is interested ● Establishment of vigil mechanism to enable people to report genuine concerns before audit committee |

| SEBI (Prohibition of Insider Trading) Regulations, 2011 | ● Prohibition of trading on the basis of unpublished price sensitive information ● Fair disclosure of information by Designated Persons and insiders |

| Principle 2- Business should provide goods and services in a manner that is sustainable and safe. | |

| Policy to be framed | Broad contents of the policy |

| Responsible Sourcing Policy | ● Ensuring sustainable utilization of natural resources ● Complying with all applicable regulatory requirements pertaining to the products and/ or services ● Identify, assess and incorporate environmental and social considerations in product/ service development ● Encourage minimum/ no use of non renewable natural resources ● Encourage minimum/ no use of hazardous or toxic substances ● Implementation of Extended Producer Responsibility, wherever possible for buyback of non-degradable components of products |

| Laws relevant to the Principles | Compliances required to be ensured |

| Environment(Protection) Act, 1986 | ● Monitoring pollution discharge in excess of prescribed limits ● Comply with procedural safeguards in handling of hazardous substance |

| Hazardous and Other Wastes (Management and Transboundary Movement) Rules, 2016 | ● Ensuring proper treatment and disposal of the hazardous waste generated in the establishment ● Holding valid authorisation (application/renewal) for handling such hazardous and other wastes ● Maintenance of proper records for hazardous and other wastes stored |

| E-waste (Management and Handling) Rules, 2016[2] | ● Plan for management of the equipment after its end of life ● Designing an appropriate collection or product take back system such that it facilitates channelization of EWaste for environmentally sound management ● Creating awareness about the product offered in the market ● Publicize and periodically update the contact details of the authorized collection centers and collection points or their collection mechanism |

| Principle 3 – Businesses should respect and promote the well-being of all employees, including those in their value chains. | |

| Policy to be framed | Broad contents of the policy |

| Employee Rights Policy | ● Respect and recognition for employee rights ● Provision for parental leave ● Periodic training and skill development ● Consideration of occupational health and safety of workers and employees ● Criteria for payment of remuneration Observing practice of non-discrimination and harrasment |

| Equal Opportunity Policy | Statutory requirement under Section 21 of the Rights of Persons with Disabilities Act, 2016[3]. It broadly covers the manner of appointment, provision of assistance and facilities provided to persons with disability |

| Prevention of Sexual Harrassment at Workplace Policy | Statutory requirement in terms of the Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013 |

| Laws relevant to the Principles | Compliances required to be ensured |

| Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013 | ● Constitution of Internal Complaints Committee ● Rendering assistance to the aggrieved making the complaint ● Filing a report with the findings of the inquiry and taking necessary action ● Abiding by the minimum duties of employer as prescribed therein |

| Public Liability Insurance Act, 1991 | ● Obtaining insurance policies of specified value before handling any hazardous substances ● Ensuring timely renewal of the insurance policies taken ● Make timely payment of the insurance premium |

| Workmen’s Compensation Act, 1923 | ● Payment of compensation in case of work related injuries ● Maintenance of records for settlement of compensation in periodic payments by way of an agreement |

| Children (Pledging of Labour) Act, 1933 | ● Prohibition on employment of a child by way of pledge of labour |

| Industrial Employment (Standing Orders) Act, 1946 | ● Submission of draft standing orders (related to working conditions) ● Publication of certified standing order in the industrial establishment in languages known to workmen ● Maintenance of register of certified standing orders ● Payment of subsistence allowance in case of suspension of a workman pending investigation or inquiry |

| Payment of Wages Act, 1936 | ● Designate a person responsible for payment of wages ● Periodic payment wages within stipulated time ● Monitor that only authorised deductions are made from the wages ● Maintenance of registers and records of persons employed, the work performed by them, the wages paid to them, the deductions made from their wages, the receipts given by them and such other particulars |

| Minimum Wages Act, 1948 | ● Payment of wages to every employee engaged in a scheduled employment under him wages at a rate not less than the minimum rate of wages as prescribed ● Maintenance of registers and records giving such particulars of employees employed by him, the work performed by them, the wages paid to them, the receipts given by them and such other particulars |

| Employees Provident Fund and Miscellaneous Provisions Act, 1952 | ● Contribution of the prescribed amount to the provident fund established ● Contribution to the Deposit-linked Insurance Fund in pursuance of the Insurance Scheme as applicable |

| Maternity Benefits Act, 1961 | ● Payment of maternity benefit at the prescribed rate of average daily wages ● Prohibition of employment of a woman during the six weeks immediately following the day of her delivery or her miscarriage ● Prohibition of imposing any work which is of an arduous nature or which involves long hours of standing or which in any way is likely to interfere with the pregnancy or the normal development of the foetus, or is likely to cause miscarriage or otherwise to adversely affect the health of a woman who has made a request in this regard |

| Payment of Bonus Act, 1965 | ● Payment of minimum bonus at the prescribed rate of salary or wage earned by the employee |

| Contract Labour (Regulation & Abolition) Act, 1970 | ● Registration of establishment employing contract labour ● Appointment of representative to be present at the time of disbursement of wages by the contractor ● Display of notices in the prescribed form containing particulars about the hours of work, nature of duty and such other information |

| Payment of Gratuity Act,1972 | ● Payment of gratuity at the prescribed rate of wages based on the wages last drawn by the employee ● Obtaining insurance in the manner prescribed, for his liability for payment towards the gratuity under the Act |

| Bonded Labour System (Abolition) Act, 1976 | ● Prohibition on acceptance of any bonded debt from bonded labourer |

| Inter-State Migrant Workmen (Regulation of Employment and Conditions of Service) Act,1979 | ● Prohibition on employment of an inter-State migrant workmen unless registration certificate has been established ● Appointment of representative to be present at the time of disbursement of wages by the contractor |

| Child Labour (Prohibition & Regulation) Act, 1986 | ● Prohibition on employment of child except for some specified purposes ● Prohibition on employment of adolescents to hazardous processes ● Designing working hours and days in compliance with the requirements under the Act ● Compliance with rules relating to health and safety in workplace |

| Building and Other Construction Workers (Regulation of Employment and Conditions of Service) Act,1996 | ● Fixation of working hours in compliance with the provisions ● Provision for overtime wages ● Exhibit notice containing particulars of working hours and overtime wages in working areas ● Prohibition on employment of persons with disabilities in places that involve risk of accident for him/ her ● Maintenance of register of workers employed, hours worked, wages paid etc |

| Rights of Persons with Disabilities Act, 2016 | ● Prohibition on discrimination on grounds of disability, unless legitimate cause shown ● Maintenance of records of persons with disabilities employed in the entity ● Observance of accessibility norms in the infrastructure of the premises |

| Principle 4- Businesses should respect the interests of and be responsive to all its stakeholders. | |

| Policy to be framed | Broad contents of the policy |

| Stakeholder Engagement Policy | ● Means of identifying stakeholder relevant to the operations and structure of the entity ● Understanding and addressing genuine concerns of the stakeholders ● Engaging with the stakeholders in a responsible manner |

| Laws relevant to the Principles | Compliances required to be ensured |

| Public Liability Insurance Act, 1961 | Refer under Principle 3 |

| Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitation and Resettlement Act, 2013 | ● Preparation of Social Impact Assessment study in consultation with appropriate government ● Obtaining approvals from Government for proposed land acquisition ● Providing public notice to enable them to raise objections and/ or register claims ● Prohibition on acquisition of multi-crop irrigated land except under exceptional circumstances ● Compliance of conditions specified in the Rehabilitation and Resettlement Award |

| The Scheduled Castes And The Scheduled Tribes (Prevention Of Atrocities) Act, 1989 | ● Prohibition on discrimination and harrassment to any person who is a member of Scheduled Caste or Scheduled Tribe |

| Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013 | Refer under Principle 3 |

| Principle 5- Businesses should respect and promote human rights | |

| Policy to be framed | Broad contents of the policy |

| Human Rights Policy | ● Human rights recognised by the entity[1] ● Grievance mechanisms for addressing concerns on human rights ● Consequences of breach of human rights policy |

| Laws relevant to the Principles | Compliances required to be ensured |

| All laws relating to Principle 3 (Employee well-being) and Principle 4 (Stakeholder Engagement) |

| Principle 6- Businesses should respect and make efforts to protect and restore the environment | |

| Policy to be framed | Broad contents of the policy |

| Environmental Policy | ● Adopting best practices in its operations in an environmentally conducive manner ● Conduct environmental impact assessment study periodically ● Maintenance of proper compliance with applicable environmental laws ● Monitoring use of carbon in operations ● Minimisation of use of carbon-intensive technology ● Setting of objectives and goals towards climate change |

| Laws relevant to the Principles | Compliances required to be ensured |

| Environment(Protection) Act, 1986 | Refer under Principle 2 |

| Hazardous and Other Wastes (Management and Transboundary Movement) Rules, 2016 | |

| E-waste (Management), Rules, 2016 | |

| Public Liability Insurance Act, 1991 | Refer under Principle 3 |

| Biological Diversity Act 2002 | ● Prohibition on obtaining biological resource for research or commercial utilisation etc without approval of National Biodiversity Authority (‘Authority’) ● Restriction on application for Intellectual Property Rights without requisite approvals from Authority Prior intimation to Authority for use/ research etc on biological resource where prior approval is not required |

| Wildlife Protection Act, 1972 | ● Prohibition on hunting of specified wild animals ● Holding valid permit for hunting of wild animals ● Prohibition on dealing in specified plants in any manner ● Holding valid permit for dealing in such plants for purposes such as education, scientific research etc ● Prohibition on cultivation of specified plants |

| Water (Prevention and Control of Pollution) Act, 1974 | ● Restriction on new establishments resulting in new discharge of sewage ● Access to government officer for periodic assessment of existing sewage and discharge of effluents |

| Water (Prevention and Control of Pollution) Cess Act, 1977 | ● Payment of cess for use of water in the operations and industries |

| Air (Prevention and Control of Pollution) Act, 1981 | ● Identifying whether any industrial plant is/ proposed to be set up in air pollution control area ● Obtaining permission before establishment of industrial plant in air pollution control area ● Prohibition on emission of air pollutant in air pollution control area |

| National Environment Tribunal Act, 1995 | ● Liability to pay compensation in case of death of, or injury to, any person (other than a workman) or damage to any property or environment has resulted from an accident as specified in the Schedule thereto |

| Energy Conservation Act, 2001 | ● Ensuring that the equipment or appliances that consume, generates, transmits or supply energy is in line with the energy consumption standards ● Ensure display of specified particulars on the label on such equipment or appliance ● Get energy audit conducted by the accredited energy auditor ● Appoint energy manager with such qualification as prescribed ● Arrange and organise training of personnel and specialists in the techniques for efficient use of energy and its conservation |

| Principle 7 – Businesses, when engaging in influencing public and regulatory policy, should do so in a manner that is responsible and transparent | |

| Policy to be framed | Broad contents of the policy |

| Policy on Responsible Advocacy | ● Recognise the values and principles advocated by the entity ● Identify the means of advocacy ● Adopting a collaborative approach in influencing public ● Designate authorities responsible to oversee implementation of the Policy |

| Fair Competition Policy | ● Define fair competition vs anti-competition Pledge not to indulge in anti-competitive practices ● Define fair competition vs anti-competition ● Pledge not to indulge in anti-competitive practices ● Consequences upon persons found to be indulged in anti-competitive practices ● Incidents that amount to abuse of dominant position |

| Laws relevant to the Principles | Compliances required to be ensured |

| Competition Act, 2002 | ● Identify whether any contract/ arrangement entered into by the company involves an appreciable adverse impact on the fair competition ● Obtain appropriate approvals before entering into any combination arrangements ● Do not indulge in activities that amount to abuse of dominant position or anti-competitive practices |

| All laws relating to Principle 3 (Employee well-being) and Principle 4 (Stakeholder Engagement) |

| Principle 8 – Business should promote inclusive growth and equitable development | |

| Policy to be framed | Broad contents of the policy |

| Inclusion & Diversity Policy | ● Recognition of diversity in workplace ● Meaning of inclusion and diversity in the context of the reporting entity ● Approach of the entity towards ensuring diversity ● Ways adopted to promote inclusion of diversity in workforce ● Extent of inclusion and diversity – does it extends to value chain etc ● Providing accessibility to all in absence of any valid reasons behind restricting the same |

| Preferential Procurement Policy | ● Give preference to small producers, farmers, MSME etc ● Allocating a percentage of raw materials to be sources from such suppliers ● Manner and responsibility of persons reviewing actual procurement against budgeted allocation |

| Corporate Social Responsibility Policy | Statutory requirement under Section 135 of the Companies Act, 2013 |

| Laws relevant to the Principles | Compliances required to be ensured |

| Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitation and Resettlement Act, 2013 | Refer under Principle 4 |

| The Scheduled Castes And The Scheduled Tribes (Prevention Of Atrocities) Act, 1989 | |

| Public Liability Insurance Act, 1991 | Refer under Principle 3 |

| Biological Diversity Act 2002 | Refer under Principle 6 |

| Essential Commodities Act, 1955 | ● Dealing with essential commodities only with a valid permit from Government ● Dealing with essential commodities at prices fixed by Government ● Abstain from withholding supply of essential commodities |

| The Companies Act, 2013 | Spending on projects and activities in line with Schedule VII for the benefit of one or more classes of the society |

| Principle 9 – Businesses should engage with and provide value to their consumers in a responsible manner | |

| Policy to be framed | Broad contents of the policy |

| Cyber Security and Data Privacy Policy | ● Define legitimate use vs misuse of information ● Ensure proper access and usage of information ● Prevent misuse of information ● Maintain confidentiality of personal information of clients, suppliers, consumers and employees ● Undertaking that any information shared can be done only with prior consent of the concerned ● Policy for non-retention of personal information beyond specified use |

| Laws relevant to the Principles | Compliances required to be ensured |

| Consumer Protection Act | ● Prohibition of unfair trade practice and/or restrictive trade practice ● Removal of defect/ replacement of defective goods ● Abstain/ discontinue offering hazardous goods for sale ● Payment of adequate compensation against the damage caused due to the products/ services of the entity |

| Competition Act, 2002 | Refer under Principle 7 |

| Consumer Protection (E-Commerce) Rules, 2020 | ● Appointment of nodal officer to ensure compliance with applicable laws and regulations ● Abstain from adoption of any unfair trade practice ● Establish and maintain grievance redressal mechanism ● Abstain from any sort of price manipulation, discrimination among consumers ● Display of necessary information prominently such as contact details, location, payment modes etc ● Ensure that all advertisements are consistent with the actual characteristics of the products/ services |

| Food Safety and Standards (Packaging and labelling) Regulations, 2011 | ● Minimum information required to be specified in the label of pre-packaged products ● Use of specified types of containers for various pre-packaged products |

| Recycled Plastics Manufacture and Usage Rules, 1999 | ● Recycling of plastic products in line with the prescribed standards ● Abstain from using single-use plastics ● Appropriate marking/ codification of the plastic products used |

It is apparent that the reporting entities need to ensure that a lot of policies, processes and systems are in place in order to demonstrate a positive ESG position. While it seems to be a very rigorous exercise, companies making to the top in the country in respect of their ESG conduct should already be having much of it in place. For them, BRSR will give a way to demonstrate their commitment towards ESG and their responsible business practices. Considering the growing importance given to the adoption of NGRBC principles across the group entities and value chain partners, the impact of implementing BRSR will not fall only on the top 1000 listed entities on which the same is applicable, but extends far beyond the legal scope.

[1] GRI Standards Glossary – (Page 12)

[2] These rules shall apply to every producer, consumer or bulk consumer, collection centre, dismantler and recycler of e-waste involved in the manufacture, sale, purchase and processing of electrical and electronic equipment or components

[3] Rule 6(3) of the Rights of Persons with Disabilities Rules, 2017 specifies the following information to be made part of the Policy –

(3) The equal opportunity policy of a private establishment having twenty or more employees and the Government establishments shall inter alia, contain the following, namely:-

(a) facility and amenity to be provided to the persons with disabilities to enable them to effectively discharge

their duties in the establishment;

(b) list of posts identified suitable for persons with disabilities in the establishment;

(c) the manner of selection of persons with disabilities for various posts, post-recruitment and pre-promotion

training, preference in transfer and posting, special leave, preference in allotment of residential accommodation if any, and other facilities;

(d) provisions for assistive devices, barrier-free accessibility and other provisions for persons with disabilities;

(e) appointment of liaison officer by the establishment to look after the recruitment of persons with disabilities and provisions of facilities and amenities for such employees.

(4) The equal opportunity policy of the private establishment having less than twenty employees shall contain facilities and amenities to be provided to the persons with disabilities to enable them to effectively discharge their duties in the establishment.

[4] Minimum components of human rights should include rights as specified under the Constitution of India, International Bill on Human Rights, United Nations Guiding Principles for Business and Human Rights

Our resource center on Business Responsibility and Sustainable Reporting can be accessed here –

Abhishek Saraf, Manager and Payal Agarwal, Executive (corplaw@vinodkothari.com)

The Business Responsibility and Sustainability Reporting (“BRSR”), originating from the MCA report on Business Responsibility Reporting, has found its way into the regulatory provisions by way of an amendment to the Regulation 34(2)(f) of the Listing Regulations[1], notified on 5th May, 2021. Further, SEBI vide circular dated 10th May, 2021 introduced the format of BRSR and the guidance note to enable the companies to interpret the scope of disclosures.

The BRSR will replace the existing BRR format w.e.f. FY 2022-23. For the FY 2021-22, the top 1000 listed entities may voluntarily submit the BRSR and from FY 2022-23 onwards, the same has to be submitted mandatorily. It is notable that the BRSR, though replacing BRR, is actually an extension of the existing BRR reporting While the BRSR has been made effective from FY 2022-23, it has to be understood that reporting is secondary, and needs to be backed by the company taking appropriate actions to ensure a positive report. Where the BRSR reporting of a company is negative, the same, though not a non-compliance of the regulatory provisions, will result in a negative impact on the minds of the stakeholders.