FAQs on mandatory demat of securities by private companies

You may refer to our other FAQs on dematerialization of shares here and you may also refer to our Snippet, detailed article and YouTube Video

You may refer to our other FAQs on dematerialization of shares here and you may also refer to our Snippet, detailed article and YouTube Video

Loading…

Loading…

Read our other resources:

| Register here |

Loading…

Other resources on the amendment:

Archisman Bhattacharjee and Manisha Ghosh I finserv@vinodkothari.com

On April 16, 2024, the Reserve Bank of India (RBI) issued Draft Directions on the Regulation of Payment Aggregators (PAs) (‘Draft PA Directions’) serving two primary purposes:

– Avinash Shetty, Asst. Manager & Hari Dwivedi, Executive (corplaw@vinodkothari.com)

The Ministry of Corporate Affairs (‘MCA’) in the year 2018, introduced the provision for declaration by individuals identified as Significant Beneficial Owners (‘SBOs’) for companies under section 90 of the Companies Act, 2013 (‘Act’). Subsequently, MCA extended the ambit of the said provisions to Limited Liability Partnerships (LLPs) through notification dated February 11, 2022. However, the notification prompted concerns and queries regarding the implementation of SBO provisions on LLPs. These concerns have been addressed by the recent notification dated November 9, 2023 (‘LLP SBO Rules’). The rationale behind this extension is to align the framework for identification of SBO’s of LLPs with that of companies.

While the provisions are on similar lines as that brought for companies under the Act, however, the difference is mostly in terms of the manner of determining the SBOs in case of LLPs. In case of LLPs it is calculated based on holding of capital contribution (shares in case of companies), voting rights in respect of management or policy decisions of LLP (shares in case of companies) and right to receive or participate in distributable profits (dividend in case of companies) or any other distribution besides, the right to exercise control or significantly influence in any manner other than direct holdings.

The article explains the requirements of the LLP SBO Rules, obligations of the LLPs, and the actionables to be taken in order to comply with the requirements.

Read more →

Loading…

You may also refer to our detailed article and youtube video.

Loading…

You may also refer to our detailed article and YouTube video on the same.

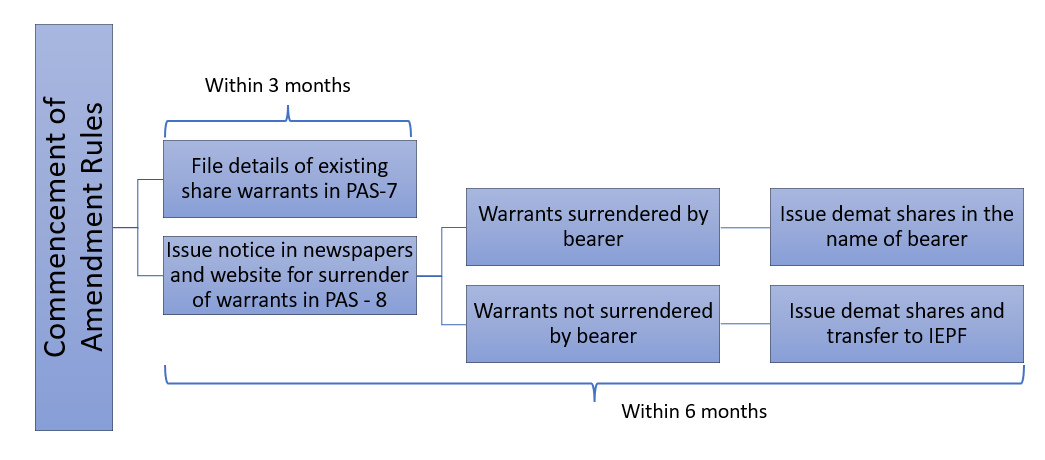

Share warrants are one of the widely used means to raise funds, particularly, in case of start-ups. MCA has recently notified the Companies (Prospectus and Allotment of Securities) Second Amendment Rules, 2023 (“Amendment Rules”) vide which Rule 9 has been amended to require mandatory conversion of the existing share warrants issued by public companies under the erstwhile Companies Act, 1956 (“Erstwhile Act”) into dematerialised form of securities.

Following this amendment, a significant question comes up to be addressed is whether public companies will not be allowed to issue share warrants altogether? We attempt to decode the implications of the present amendment in this write up.

The newly inserted sub-rule (2) and (3) to Rule 9 of the PAS Rules requires every unlisted company to –

The company shall be required to issue notice for the bearers of share warrants in form PAS-8 on its website as well as two newspapers – in vernacular language, having wide circulation in the district and in English language having wide circulation in the state in which the registered office of the company is situated.

In the context of the newly inserted sub-rule (2) of Rule 9, the term share warrants is to be interpreted in a much restricted sense. The provision refers to “share warrants prior to commencement of the Companies Act, 2013 and not converted into shares”, which implies share warrants issued under the Erstwhile Act only. In this regard, one may refer to section 114 of the Erstwhile Act that allowed public companies to issue “bearer warrants” entitling the bearer of such warrants to the shares specified therein. The same was referred to as “share warrants” under the said Act, and the shares contained therein can be transferred through mere delivery of the warrant.

The present amendment requires mandatory surrender of such “share warrants” in the form of “bearer warrants” against issuance of shares in dematerialised form.

As mentioned above, the “share warrants” referred to under the Amendment Rules are limited to the bearer warrants issued in accordance with the Erstwhile Act, and do not extend to all share warrants which companies issue under the various provisions of law.

In general context, share warrants are actually written options to subscribe to the shares of a company on pre-agreed terms at a future date. Such warrants are fairly common in the corporate world on account of the benefits associated with the same, and the present amendment cannot be said to rule out the possibility of issuance of such share warrants. Share warrants are directly or indirectly recognised under various provisions of law, for instance:

While the Act does not mention at several places under it about share warrants, however, at few places, like the provisions under section 68 dealing with buy back of securities as well as reference to employee “stock options”, which, by nature are equivalent to share warrants are given the Act.

Therefore, there are no explicit provisions that prohibit the issuance of share warrants by unlisted companies, and the same, being a “security” can very well be issued by a company, whether listed or unlisted, in compliance with the applicable provisions of law to meet the required funding as well as investment objectives.

The Amendment Rules aim at the wiping out of the bearer share warrants, since the legal and beneficial ownership of the shares are non-traceable in such a case. However, that does not eliminate the concept of share warrants as a whole, that are issued to an identified set of persons, and follows a due procedure laid down in the law for transfer of such warrants. Although not expressly defined under the Act, the concept of share warrants is legally recognised under various laws and are being widely issued by Indian companies, whether listed or unlisted, including private companies. The current set of amendments will have no impact on the permissibility of issuing share warrants issued under the Act and other laws as mentioned hereinabove.

MCA notifies mandatory dematerialisation for securities of private companies

Two major amendments have been notified by MCA on 27th October, 2023 impacting all companies, and majorly the private companies. These include the Companies (Management and Administration) (Second Amendment) Rules, 2023 introducing the concept of “designated person” with respect to beneficial interest in shares of a company[1] and the Companies (Prospectus and Allotment of Securities) Second Amendment Rules, 2023 (“PAS Amendment Rules”). The PAS Amendment Rules encompass two major amendments: (i) with respect to the bearer share warrants under the erstwhile Companies Act, 1956, and (ii) mandatory dematerialisation for all private companies excluding small companies. In this write-up, we briefly discuss the amendments with respect to mandatory dematerialisation of securities for the private companies and the implications thereto.

Sub-section (1A) was inserted under Section 29 of the Companies Act 2013 (“the Act”) facilitating the Central Government to prescribe such class or classes of unlisted companies for which the securities shall be held and/ or transferred in dematerialised form only. In exercise of the powers conferred under the said section, Rule 9B has been inserted vide the PAS Amendment Rules specifying the requirement of mandatory dematerialisation of securities issued by private companies.

The mandatory dematerialisation requirement is applicable on all securities of every private company, excluding small companies[2] and government companies. The provisions are applicable with immediate effect, and a timeline of 18 months is provided from the closure of the financial year in which a private company is not a small company for the compliance with the mandatory dematerialisation requirements.

For example, a private company (other than a company that is a small company as on 31st March, 2023) is required to comply with mandatory dematerialisation of securities within a period of 18 months from the end of FY 22-23, i.e., on or before 30th September 2024.

In case a company ceases to be a small company after 31st March, 2023, the timeline of 18 months triggers from the close of the financial year in which it ceases to be a small company. Therefore, if a company ceases to be a small company at any time during FY 23-24, the timeline of 18 months will trigger from 31st March, 2024 and therefore, shall be complied with by 30th September 2025.

Rule 9B of the PAS Rules, enforcing mandatory dematerialisation of the securities of private companies, is applicable on all private companies other than the following:

In case of unlisted public companies, sub-rule (11) of Rule 9A extends a similar exemption from dematerialisation requirements. The said sub-rule covers the following public companies –

It is important to note that a wholly owned subsidiary, though exempt from the dematerialisation requirements under Rule 9A, similar exemption does not extend to a private company under Rule 9B. Therefore, currently it seems that a wholly-owned subsidiary, incorporated in the form of a private company, is not exempt from dematerialisation requirements.

Further, for a private company that is a wholly-owned subsidiary of a public company, and therefore, a deemed public company, it remains an open question as to whether it will be exempt under sub-rule (11) of Rule 9A or the provisions of Rule 9B will apply.

The position may be summarised as below –

| Nature of wholly-owned subsidiary | Nature of holding company | Applicability of dematerialisation provisions |

| Public company | Public company | Exempt under Rule 9A(11) |

| Public company | Private company | Exempt under Rule 9A(11) |

| Private company | Private company | Covered under Rule 9B as of now |

| Private company | Public company | The same being a deemed public company, there is no clarity on whether Rule 9A applies or Rule 9B. If considered to be a private company – covered under Rule 9B If considered to be a public company – exempt in terms of Rule 9A(11) |

A private company, covered under the provisions of mandatory dematerialisation shall –

Apart from the aforesaid, the compliances applicable to an unlisted public company under sub-rule (4) to (10) of Rule 9A are also applicable to private companies. These include –

As for persons holding securities of a private company, while the mandatory dematerialisation cannot be enforced by the private company, the same is expected to be taken care of by way of sub-rule (4) of Rule 9B that requires –

Therefore, the mandatory dematerialisation of securities of a private company is ensured through placing restrictions on both a private company and the holders of securities issued by the same.

There are no specific penal provisions governing the non-compliance with the provisions of section 29 of the Act read with Rule 9B of the PAS Rules, and therefore, general penal provisions under section 450 of the Act should apply.

Section 450 specifies the following:

“If a company or any officer of a company or any other person contravenes any of the provisions of this Act or the rules made thereunder, or any condition, limitation or restriction subject to which any approval, sanction, consent, confirmation, recognition, direction or exemption in relation to any matter has been accorded, given or granted, and for which no penalty or punishment is provided elsewhere in this Act, the company and every officer of the company who is in default or such other person shall be liable to a penalty of ten thousand rupees, and in case of continuing contravention, with a further penalty of one thousand rupees for each day after the first during which the contravention continues, subject to a maximum of two lakh rupees in case of a company and fifty thousand rupees in case of an officer who is in default or any other person.”

The existence of shell companies and personification of shareholders is not a rare scenario, and such a situation is likely to be more common in case of a private company, unlike a public company. Historically, dematerialisation of shares is looked upon by the government as a means to curb black money[3]. As for listed companies and unlisted public companies[4], the dematerialisation of securities is already a mandatory requirement. With the present amendments being notified, the private companies have also been covered by the mandatory dematerialisation requirements.

As on 31st January, 2023, more than 14 lac companies registered with MCA comprising 95% of the total active companies are private companies, out of which approximately 50,000 companies are small companies[5]. Thus, with the mandatory dematerialisation for private companies coming into existence, a large number of companies will be forced to move towards dematerialisation of shares. Further, while the company can be held accountable for the mandatory dematerialisation of securities held by promoters, directors and KMPs, given the closely held nature of private companies, barely any securityholder (particularly shareholders) will remain outside the purview of the same.

Further, it is clarified that, in no way such a mandatory dematerialisation for private companies can be taken to mean that the restriction on transfer of shares of such a company is relaxed, and adequate systems can be implemented at the depository’s level to ensure compliance with the basic distinguishing characteristic of a private company and thereby have filters before executing any transfer of securities.

You may also refer to our Snippet, FAQs and YouTube Video

[1] Read our article on the same here – https://vinodkothari.com/2023/10/companies-to-disclose-designated-person-with-respect-to-beneficial-interest-in-shares/

[2] As per the definition under the Act read with the rules made thereunder, a small company means a company, other than a public company, having paid up share capital not exceeding Rs. 4 crores and turnover not exceeding Rs. 40 crores. Further, the following cannot be a small company –

(A) a holding company or a subsidiary company;

(B) a company registered under section 8; or

(C) a company or body corporate governed by any special Act.

[3] https://www.moneycontrol.com/news/trends/legal-trends/government-looking-to-dematerialise-shares-of-unlisted-cos-to-curb-black-money-2382347.html

[4] https://vinodkothari.com/wp-content/uploads/2018/09/Physical-to-demat-a-move-from-opacity-to-transparency.pdf

Loading…