Are financial leases subjected to TDS?

Yutika Lohia

yutika@vinodkothari.com

Introduction

In today’s time, leasing has become an indispensable element of businesses – Any and every asset movable or immovable, equipment or software can be taken on lease. Colloquially, lease refers to an arrangement where a property owned by one is given for use by another, against regular rentals. In India, there are two types of lease transactions-financial lease and operating lease. Typically, a financial lease is a disguised financial transaction whereas operating lease is akin to rental contracts.

While leasing has gained much importance and relevance over the years, its feasibility and viability depends a major deal on its tax implications – they could easily make or break the deal. The technical aspects with respect to taxation on implementation makes it all the more significant. Issues like depreciation, lease rentals, tax deduction at source and exposure to GST are key concerns. Further, though leases are classified as finance or operating, it is important to note that such distinction is essentially from an accounting perspective – the Income Tax Act, 1961, however, does not distinguish between the two.

A rather significant but overlooked aspect of leasing is the ‘tax deduction at source’ (‘TDS’). As is known TDS is a key element of the Indian taxation framework which aims to collect tax at the source of generation of income. In case of a lease transaction, the lessee is required to deduct tax under 194-I of the Income Tax Act at the time of payment of lease rentals to the lessor.

While there are several judicial precedents dealing with TDS vis-à-vis lease transactions, the Hon’ble High Court of Karnataka in a recent order, in the case of Commissioner of Income Tax vs. Texas Instruments India Pvt Ltd (2021),[1] concluded that in case of a financial lease, the lease financing company did not provide any particular service as a driver or otherwise for the purpose of usage of the car. The only transaction entered between the assessee and the lease financing company was to make payments of the amount due to the company. To say there was a mere financing arrangement and therefore section 194-I of the IT Act shall not be applicable in case of a financial lease transaction.

In this article we shall discuss the above stated ruling in detail.

The case of Texas Instruments India Pvt Ltd

The Assessee, Texas Instruments India Pvt Ltd being in the business of manufacture and export of computer software had taken motor vehicle on finance lease for its employees. It considered the lease rentals as business expenditure and claimed deduction of the same under the head income from business and profession. TDS was not deducted on the finance lease rentals as the assessee contested that the same did not fall under the provision of section 194-I or 194-C of the IT Act.

However, the Assessing Officer disallowed the claimed expenditure on the grounds that the lease rentals were being paid to the vendor under the contract and therefore the payment/ expenses would be attracting the provisions of section 194-C.

Aggrieved by the order of the A.O., the Assessee preferred an appeal before to the CIT(A). Upon such appeal, the CIT(A) overturned the A.O’s order and held that the payments made by assessee were not in the nature of service rendered by the leasing company for the carriage of goods or passengers. The CIT(A) also held that the assets were in the disposition of the Assessee.

Following such order, the matter was appealed before the Income tax Appellate Tribunal (ITAT) where it was held that provisions of Section 194-C will not be applicable on lease rentals.

Once again, the matter was taken for appeal before the Hon’ble Karnataka High Court where it was held that the leasing financing company did not provide any particular service as a driver or otherwise for the purpose of usage of car. The maintenance was carried by the employees of the assessee. The only transaction entered between the assessee and the leasing company was to make payments of the amount due to the company. Since no services were being provided by the leasing company and is a mere financing agreement, provisions of section 194-C and 194-I shall not be applicable.

Understanding the Provisions of Law

Section 194-I of the Income Tax Act, 1961: TDS on Rent

Section 194-I of the IT Act 1961 governs tax deduction at source in case of lease rentals. As already mentioned, Income Tax Act does not draw any line of distinction between financial lease and operating lease, let us understand whether TDS needs to deducted on lease rentals in case of both financial lease and operating lease.

Section 194-I of the IT Act explains rent as follows:

“rent” means any payment, by whatever name called, under any lease, sub-lease, tenancy or any other agreement or arrangement for the use of (either separately or together) any

(a) land; or

(b) building (including factory building); or

(c) land appurtenant to a building (including factory building); or

(d) machinery; or

(e) plant; or

(f) equipment; or

(g) furniture; or

(h) fittings,

whether or not any or all of the above are owned by the payee;

Rent has been broadly defined under section 194-I and shall be applicable when asset is given for use for any payment under lease, sub lease, tenancy, or any other arrangement or agreement.

Section 194-C of the Income Tax Act, 1961: Payment to contractors

(1) Any person responsible for paying any sum to any resident (hereafter in this section referred to as the contractor) for carrying out any work (including supply of labour for carrying out any work) in pursuance of a contract between the contractor and a specified person shall, at the time of credit of such sum to the account of the contractor or at the time of payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct an amount equal to—

(i) one per cent where the payment is being made or credit is being given to an individual or a Hindu undivided family;

(ii) two per cent where the payment is being made or credit is being given to a person other than an individual or a Hindu undivided family,

of such sum as income-tax on income comprised therein.

XX

Conclusion

The judgement highlights that by virtue of the fact that no services were provided by the leasing company and that it was a mere financing agreement, section 194-C and 194-I would not be applicable in the given case.

Therefore, it seeks attention on the fact whether TDS has to be deducted on financial lease rentals.

Also, one must contemplate whether TDS should have been deducted under section 194-A of the IT Act as the lease transaction was considered as a mere finance agreement. This remains unanswered.

De-novo Master Directions on PPIs

I. Introduction

The Reserve Bank of India (RBI) on August 27, 2021, issued the Master Directions on Prepaid Payment Instruments[1] (‘Master Directions’) repealing the Master Directions on Issuance and Operation of Prepaid Payment Instruments[2] (‘Erstwhile Master Directions’) with immediate effect. These Master Directions have been issued keeping in mind the recent updates to the Erstwhile Master Directions.

In this write-up we aim to cover the major regulatory changes brought about by the Master Directions.

II. Overview of key changes

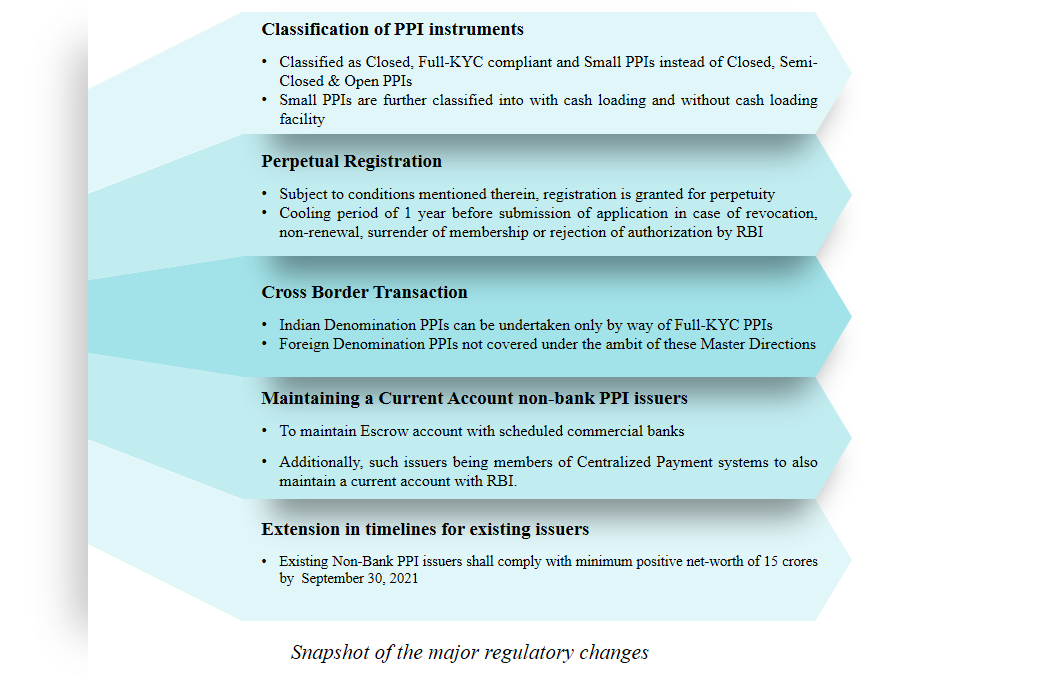

1. Classification of PPIs instruments

The Erstwhile Master Directions classified PPIs into three categories namely closed ended PPIs which could be issued by anyone and required no RBI approval, semi-closed PPIs and open ended PPIs which could be issued only by Banks. The new Master Directions have also classified PPIs in three categories i.e. Closed-ended PPI, Small PPIs and Full-KYC PPIs. However, since closed-ended PPIs are not a part of the payment and settlement system, they are not regulated by the RBI. A brief snapshot of the nature of the other two types of PPIs is presented below:

| Basis | Small PPI | Full KYC PPIs | |

| With cash loading facility | Without cash loading facility | ||

| Issuer | Banks and non-banks after obtaining minimum details of PPI holder (mobile number verified with OTP; self-declaration of name and unique identity/identification number of any OVD) | Banks and non-banks after completing KYC of holder | |

| Identification Process | Verification of mobile number through an OTP

Self-declaration of name and unique identify number of any OVD as recognized in KYC Master Directions |

Video-based Customer Identification Process | |

| Nature of PPI | Reloadable and can be issued in electronic form.

Electronic payment transactions have been divided into two categories- transactions that do not require physical PPIs and those which require. Hence, even cards could be issued. |

Reloadable and can be issued in card or electronic form.

Loading/Reloading shall be from a bank account / credit card / full-KYC PPI.

|

Reloadable and can be issued in electronic form.

Electronic payment transactions have been divided into two categories- transactions that do not require physical PPIs and those which require. Hence, even cards could be issued. |

| Maximum amount that can be loaded | In a month: INR 10,000

In a year: INR 120,000 |

No maximum limits | |

| Maximum outstanding amount at any point of time | INR 10,000 | INR 200,000 | |

| Limit on debit during a month | INR 10,000 per month | No limit | No limit |

| Usage of funds | For purchase of goods and services only.

Cash withdrawal or fund transfer not permitted

|

Transfer to source or bank account of PPI holder, other PPIs, debit or credit card permitted subject to:

Pre-registered benefit – maximum INR 200,000 per month per beneficiary

Other cases – maximum INR 10,000 |

|

| Cash Withdrawal | Not permitted | Permitted subject to limits:

INR 2000 per transaction and INR 10,000 per month |

|

| Conversion | To be converted into full-KYC PPIs within a period of 24 months from the date of issue of the PPI. | Small PPI with cash loading can be converted into Small PPI without cash loading, if desired by the PPI holder. | Not applicable |

| Restriction on issuance to a single person | Cannot be issued to same person using the same mobile number and same minimum details more than once. | No such restriction | No such restriction |

| Closure | Funds transferred back to source or Holders bank account after complying with KYC norms

|

Funds transferred to pre-designated bank account or

PPIs of the same issuer |

|

The concept of ‘Small PPI’ and ‘Full-KYC PPI’ cannot be said to be a new introduction, rather, it is more of a merger of the existing variety of semi closed PPIs in Small PPI and the open ended PPI to Full KYC PPI. However, an important change that has been inserted is the recognition of non-bank PPI issuers to issue Full KYC PPI, who were earlier not allowed to issue open ended PPIs.

2. Validity of Registration

Earlier, the Certificate of Authorisation was valid for five years unless otherwise specified and was subject to review including cancellation of the same. However, under the Master Directions, the authorisation is granted for perpetuity (even for existing authorisation which becomes due for renewal) subject to compliance with the following conditions:

- Full compliance with the terms and conditions subject to which authorisation was granted;

- Fulfilment of entry norms such as capital, net worth requirements, etc.;

- No major regulatory or supervisory concerns related to operations, as observed during onsite and / or offsite monitoring;

- Efficacy of customer grievance redressal mechanism;

- No adverse reports from other departments of RBI / regulators / statutory bodies, etc.

Also, the concept of ‘cooling period’ was introduced in December 2020[3], for effective utilisation of regulatory resources. PPI issuer whose CoA is revoked or not-renewed for any reason; or CoA is voluntarily surrendered for any reason; or application for authorisation has been rejected by RBI; or new entities that are set-up by promoters involved in any of the above categories; will have a one year cooling period. During the said cooling period, entities shall be prohibited from submission of applications for operating any payment system under the PSS Act.

3. Cross border transactions in Indian denomination

The Erstwhile Master Directions provided that Cross Border Transactions in INR denominated PPIS was allowed only by way of KYC compliant semi-closed and open PPIs which met the conditions specified therein. However, under the Master Directions, such issuances have been permitted only in the form of Full-KYC PPI and other conditions as prescribed earlier have not been altered.

4. Maintenance of Current Account

Apart from maintaining an escrow account with a scheduled commercial bank, non-bank PPI issuer that is a member of the Centralised Payment Systems operated by RBI i.e. non-bank issuers as covered under Master Directions on Access Criteria for Payment Systems[4] which have been allowed to access Real Time Gross Settlement (RTGS) System and National Electronic Fund Transfer (NEFT) Systems and any other such systems as provided by RBI, shall also be required to maintain a current account with the RBI.

Transfer from and to such current account is permitted to be credited or debited from the escrow account maintained by the PPIs.

5. Ensuring additional safety norms

- To ensure safety and security, PPIs issuers are now required to put in place a Two Factor Authentication (2FA) in place for all wallet transactions involving debit to wallet transactions including cash withdrawals. However, it is not mandatory in case of PPI-MTS and gift PPIs.

- The Erstwhile Master Directions required PPI issuers to put in place a mechanism to send alerts to the PPI holder regarding debit/credit transactions, balance available /remaining in the PPI. In addition to the same, the Master Directions now require issuers to send alerts to the holder even in case of offline transactions. The issuer may send a common alert for all transactions as soon as the issuer receives such information. Separate alerts for each transaction shall not be required.

6. Miscellaneous

- In case of co-branding, additionally it has been specified that the co-branding partner can also be a Government department / ministry.

- The Erstwhile Master Directions provided banks and non-banks a period of 45 days to apply to the Department of Payment and Settlement Systems (DPSS) after obtaining the clearance under the Payment and Settlement Systems Act, 2007. The same has now been reduced to 30 days from obtaining such clearance.

- In addition to the satisfactory system audit report and net worth certificate, RBI also requires issuers to submit a due diligence report for granting final Certificate of Authorisation (CoA).

- Transfer of funds back to source account in case of Gift PPIs has been allowed after receiving the consent of the PPI holder.

- To improve customer protection and grievance redressal, the Master Directions have provided customers of non-bank PPI issuers to have recourse to the Ombudsman Scheme for Digital Transactions.

7. Effect on existing issuers

The timeline for complying with the minimum positive net-worth of 15 crores by non-bank PPI issuers has been extended and shall now be met with by September 30, 2021 instead of March 31, 2020. Non-bank issuers shall submit the provisional balance sheet indicating the positive net-worth and CA certificate to the RBI on or before October 30, 2021, failing which they may not be permitted to carry on their business.

III. Conclusion

In this write-up we have aimed to cover the gist of changes introduced in the Master Directions as compared to the Erstwhile Master Directions. The changes made in the regulatory framework for the PPIs have created a level playing field for banks and non-banks, especially, with respect to issuance of full KYC PPIs. Comparatively, the new directions are way more liberal than the earlier one, which only indicates how bullish the regulator must be with respect to PPIs.

[1] https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=12156#MD

[2] https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=11142

[3] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=12001&Mode=0

[4] MD51170116C65788DE8A564165B74D5FECE0626A73.PDF (rbi.org.in)

Credit Default Swaps (Global and Indian Scenario)

Credit default swaps (what is happening in global markets and the recommendations of the working group)

Other ‘I am the best’ presentations can be viewed here

Our other resources on related topics –

-

-

- https://vinodkothari.com/wp-content/uploads/RBIa%CC%82%C2%80%C2%99s-Guidelines-on-Credit-Default-Swaps-for-Corporate-Bonds.pdf

- https://vinodkothari.com/2021/02/rbi-issues-draft-directions-on-credit-derivatives/

- https://vinodkothari.com/isda_new_definition_credit-derivs_impact/

- https://vinodkothari.com/2013/12/secnews-110810/

- https://vinodkothari.com/rbi-new-cds-guidelines-feeble-effort-start-non-starting-product/

-

Workshop on KYC : Concepts and Operations

We have gone housefull for our workshop to be held on 16th and 17th September and not accepting further registrations. In view of the overwhelming interests shown, a repeat workshop will be announced in due course. You can register your interest in the form below –

You may register your interest for the repeat workshop here:

https://forms.gle/HHCVp6XKhAB567cc9

Our Resources on KYC:

- Article on RBI Governor’s Statement on KYC – https://vinodkothari.com/2021/05/rationalisation-of-kyc/

- Article on introduction to Digital KYC – https://vinodkothari.com/2019/08/introduction-of-digital-kyc/

- Video on KYC basics – https://www.youtube.com/watch?v=oU69z7M2ngg

- Guide to KYC through CKYCR – https://vinodkothari.com/2020/02/guide-to-identity-verification-through-ckycr/

- Articles on CKYCR:

- Article on Supreme Court Verdict on Aadhaar – https://vinodkothari.com/2018/10/the-supreme-court-aadhaar-verdict-major-blow-to-fintech-companies/

- Article on Aadhaar Ordinance – https://vinodkothari.com/2019/03/aadhaar-ordinance-paving-way-for-use-of-voluntary-aadhaar-by-private-companies/

- Articles on amendments to KYC Directions and PMLA:

- https://vinodkothari.com/2020/01/kyc-goes-live-rbi-promotes-seamless-real-time-secured-audiovisual-interaction-with-customers/

- https://vinodkothari.com/2019/05/rbi-amends-the-kyc-master-directions/

- https://vinodkothari.com/2018/04/analysis-of-amendments-to-kyc-master-directions-2016/

- https://vinodkothari.com/2016/05/rbis-kyc-directions-additional-compliances-to-be-mindful-of/

- https://vinodkothari.com/2015/01/rbi-simplifies-kyc-norms-for-nbfcs/

- https://vinodkothari.com/2017/10/mandatory-linking-of-aadhaar-and-pan-under-pmla/

Registration under Money-Lending laws

Aanchal Kaur Nagpal and Parth Ved (corplaw@vinodkothari.com)

Introduction

More often than not, the term ‘lending activities’ instantaneously brings the ‘Reserve Bank of India’ (‘RBI’) to mind. However, lending business is not the domain of RBI alone. Amidst multiple RBI guidelines governing numerous financial institutions, the state legislations on money-lending have become long forgotten.

Money-lending laws were introduced with an intention to curb non-regulated indigenous lenders from charging exorbitant interest rates to borrowers. These laws typically require licensing of money lenders, impose a ceiling on rate of interest that money lenders can charge, and generally provide that a court shall not take cognizance of a matter filed by an unlicensed money lender.

While financial entities such as non-banking financial companies (‘NBFCs’), banks, insurance companies etc. have been exempted from obtaining money-lending licence as these are regulated by other laws, the question arises whether non-regulated entities undertaking the ‘business’ of lending would require to register under the money-lending laws.

Who are money lenders?

Although there is a strong network of financial institutions, recourse to such institutions, at most times, is not accessible to the rural parts of the country. Further, it is difficult for banks to extend loans to small farmers due to their rigid requirements for KYC and collateral. Money lenders perform a gap-filling function as they majorly cater to a class of borrowers whom other financial institutions, including banks, cannot reach.

Since they have been such an important link between the formal lending sector and the informal borrowing sector, there was a need for a strong framework to regulate their working. According to Entry 30 of List II (i.e. State List) of the Seventh Schedule to the Constitution of India, the State Legislature has exclusive power to make laws on activities relating to money-lending. To regulate the transactions of money-lending in the State of Maharashtra, the state legislature has enacted Maharashtra Money-Lending (Regulation) Act, 2014 (‘Money Lending Act’). However, other states too, have their respective money-lending laws. Our article deals with provisions under the Maharashtra Money Lending Law.

Applicability for registration and exemption

The Money Lending Act states that no money lender shall carry on the business of money-lending except in the area for which he has been granted a licence. The term used here is “business of money-lending”. Business of money-lending is defined as the business of advancing loans whether in cash or kind and whether or not in connection with, or in addition to any other business.

The above definition provides clarity on the following aspects –

- Money-lending transactions should constitute a business for the lender.

- It may or may not be the primary business of the lender.

- It may or may not be in cash.

This raises an important question as to what constitutes ‘business of money-lending’. Are there any lending transactions which are excluded from its purview? The money lending laws exclude certain kinds of loans and lenders. Accordingly, below we discuss various transactions which may not be classified as business of money-lending:

Exclusions from business of money-lending

1. Secluded or isolated lending transactions

Including secluded or isolated lending transactions in the definition of money-lending business could result in classification of any loan of any amount given by anyone as a business of money-lending. Surely this could not have been the intention of the legislature. Recognising this, the Hon’ble Bombay High Court in Mandubai Vitthoba Pawar v. The State of Maharashtra & Ors. observed:

“11. …for constituting a business of money lending there has to be a continuous and systematic activity by application of labour or skill with a view of earning income and then it could be called “business”. In order to do business of money lending, it would be necessary for the State to point out multiple activities of money lending done by the petitioner. Merely referring to one isolated transaction claimed to be a loan transaction or money lending would not be enough to attract the provisions of the Act and to brand the petitioner to be a person involved in business of money lending without having any license.”

This was again reiterated in Uttam Bhikaji Belkar vs The State of Maharashtra. This makes it clear that there has to be a continuous lending activity with profit motive to constitute a business of money-lending. If this condition is satisfied, the money lender has to obtain a valid license to carry on such business. Therefore, providing one-time loans with no intention to carry on the business of lending money, will not trigger the requirement of adhering to the money lending laws.

2. Inter-corporate deposits

The intention of a company giving an Inter-corporate Deposit (ICD) is not to engage in a money-lending transaction but to earn a surplus on the idle funds available with them. In Pennwali India Ltd. and others vs Registrar of Companies it was observed that there exists a relationship of a debtor and a creditor in both cases – loans and deposits. But ICDs could also be for safe-keeping or as a security for the performance of an obligation undertaken by the depositor. Further, in the case of ICD, which is payable on demand, the deposit would become payable when a demand is made. In Housing and Urban Development Corporation Ltd. v. Joint Commissioner of Income Tax, the Hon’ble Income Tax Appellate Tribunal, Delhi Bench held:

“22. …the two expressions loans and deposits are to be taken different and the distinction can be summed up by stating that in the case of loan, the needy person approaches the lender for obtaining the loan therefrom. The loan is clearly lent at the terms stated by the lender. In the case of deposit, however, the depositor goes to the depositee for investing his money primarily with the intention of earning interest.”

Therefore, the money-lending transactions shall not include ICD and companies shall not be required to obtain a license for undertaking such transactions.

3. Loans to group companies (subsidiary, associate etc.)

In lending transactions between companies within the same group, the intention is not to earn interest on such loan but to facilitate availability of funds to the group company for furtherance of business. Further, loans by companies are governed by Section 186 of the Companies Act, 2013. Section 2(13)(i) of the Money Lending Act states that “a loan does not include a loan to, or by, or deposit with any corporation (being a body not falling under any of the other provisions of this clause), established by or under any law for the time being in force which grants any loan or advance in pursuance of that Act”. Including such transactions under the scope of money-lending business would not be in line with the objects of the Money Lending Act which is to prevent the harassment to the farmers-debtors at the hands of the money lenders or to curb charging exorbitant interest rates.

4. Parking of money

Parking of or investing idle funds in fixed deposits with Banks is in the nature of investments to earn a surplus on idle funds. Further, since regulation of banking and financial corporations is a matter of List I (i.e. Union List) of the Seventh Schedule to the Constitution of India, Section 2(13)(h) of the Money Lending Act explicitly states that “a loan shall not include a loan to, or by, a bank”, thereby excluding Banks from its purview.

5. Loans by Non-banking Financial Companies

The term money lender, as defined in the Money Lending Act, includes individuals, HUF, companies, unincorporated bodies of individuals who carry on the business of money-lending or have a principal business place in Maharashtra.

However, it has excluded from its purview, non-banking financial companies (NBFC) since they are regulated by RBI under Chapter IIIB of the Reserve Bank of India Act, 1934.

Further, other regulated entities such as insurance companies, banks etc. from its purview.

Our write-up giving a detailed analysis of the definition of NBFC can be accessed here.

Accordingly, NBFCs shall not be required to obtain a license to carry out money-lending business in the State of Maharashtra.

Lending in multiple states

In case a company lends in multiple states, it will have to adhere to provisions under the money lending laws of each such State.

Consequences of non-registration

Section 39 of the Money Lending Act states that whoever carries on the business of money-lending without obtaining a valid licence, shall be punished with –

- imprisonment for a term which may extend to 5 years; or

- with fine which may extend to Rs.50,000; or

- with both.

Conclusion

Even though getting a valid license under the Money Lending Act helps money lenders to carry on business lawfully and have legal recourse against the defaulters, one of the major reasons for non-registration is the ceiling on interest rate. Many lenders are not even aware about the requirement of such registration. Considering the serious nature of punishment for lending money without a valid license, it’s imperative for entities to identify if they are undertaking business of money-lending and whether they have a valid license to do so.

Minority shareholders under IBC

-Sikha Bansal

Below we provide a quick snapshot of the extant provisions of the insolvency framework in India vis-a-vis Minority Shareholders, in light of related laws and judicial developments so as to assess their rights and standing in the current insolvency ecosystem –