Wadia Ghandy Award for Structured Finance Research – Shortlisted articles

A compendium of shortlisted articles submitted for the 4th edition of Wadia Ghandy Award for Structured Finance Research

A compendium of shortlisted articles submitted for the 4th edition of Wadia Ghandy Award for Structured Finance Research

Move from Narrative Disclosures to Structured Transparency

– Payal Agarwal, Partner | payal@vinodkothari.com

The draft Capital Adequacy Amendment Directions of RBI propose changes to the existing Directions in relation to the Pillar 3 disclosure requirements (Market Discipline). The amendments are proposed to be made towards better alignment of the regulatory disclosure framework with the Basel norms. In addition to the new disclosure requirements with respect to Liquidity Risks and Macro-prudential Supervisory measures, the Draft proposes a move from narrative disclosures to a more structured, comprehensive transparency.

Proposed to be effective from: quarter ended 30th September, 2026

The proposed format, amongst others, incorporates a new field for liquidity related disclosures. This includes, qualitative and quantitative disclosures on liquidity risk management aspects, alongside disclosure of Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR):

| Qualitative disclosures: LRM governance Funding strategy including policies on diversification and tenor Liquidity risk mitigation techniquesExplanation of stress testingOutline of contingency funding plans | Quantitative disclosures: Measurement tools for structural liquidity and cash flow projections Concentration limits on collateral pools and sources of fundingLiquidity exposures and funding needs and entity and branch level including limitations on transferability of liquidityBalance sheet and off-balance sheet items broken down into maturity buckets and the resultant liquidity gaps |

|

Proposed Format |

Existing Format |

New Disclosures |

Frequency of Disclosure |

|---|---|---|---|

|

1. Overview of risk management, key prudential metrics, and RWA |

|||

|

Template KM1: Key metrics (at consolidated group level) |

New addition in the form of summary table, cross-linked to respective detailed tables |

|

Quarterly |

|

Table OVA: Bank risk management approach |

General qualitative disclosure requirement under Risk Exposure and Assessment |

More granular information such as risk governance structure, qualitative information on stress testing etc. |

Annual |

|

Template OV1: Overview of RWA |

No specific equivalent |

RWAs and minimum capital requirements broken down for various risk categories: credit, CCR, market, operational etc. |

Quarterly |

|

2. Linkages between financial statements and regulatory exposures |

|||

|

Table LIA: Explanations of differences between accounting and regulatory exposure amounts |

New table, some information overlap with Table DF-1: Scope of application |

Qualitative explanations on the differences observed between accounting carrying value and amounts considered for regulatory purposes |

Annual |

|

Table LIB: Outline of the differences in the scope of consolidation (entity by entity) |

Corresponds to Table DF-1: Scope of application |

– |

Annual |

|

Template LI1: Differences between accounting and regulatory scopes of consolidation and mapping of financial statement categories with regulatory risk categories |

No specific table; however, overlaps with Table DF-12: Composition of capital – reconciliation requirements |

Breakdown of each component of balance sheet by risk framework — credit risk, CCR, securitisation, market risk, or not subject to capital requirements/ capital deduction |

Annual |

|

Template LI2: Main sources of differences between regulatory exposure amounts and carrying values in financial statements |

No specific table; source of material differences between its total balance sheet assets (net of on-balance sheet derivative and SFT assets) as reported in its financial statements and its on-balance sheet exposures to be disclosed and detailed in line 1 of the common disclosure template. |

Detailed template covers sources of differences, viz., valuation differences, netting differences, provisions, and prudential filters — by risk category column. |

Annual |

|

Template PV1 – Prudent valuation adjustments (PVAs) |

– Only a single line-item within regulatory capital composition table |

Break down PVAs by type (CVA loss, closeout cost, early termination, model risk, operational risk, funding costs, administrative costs, other) and by instrument category (equity, rates, FX, credit) and book (trading / banking). |

Annual |

|

3 Composition of Capital |

|||

|

Table CCA – Main features of regulatory capital instruments |

Table DF-13: Main features of regulatory capital instruments |

– |

Ongoing, at least on a semi-annual basis |

|

Template CC1 – Composition of regulatory capital |

Table DF-11: Composition of capital |

– |

Semi-annual |

|

Template CC2: Reconciliation of regulatory capital to balance sheet |

Table DF-12: Composition of capital – reconciliation requirements |

Higher granularity provided under each line-item |

Semi-annual |

|

4 Remuneration |

|||

|

Table REMA – Remuneration policy |

Qualitative disclosures under Table DF-15: Disclosure requirements for remuneration |

Annual |

|

|

Template REM1 – Remuneration awarded during financial year |

Quantitative disclosures under Table DF-15: Disclosure requirements for remuneration |

More granular details sought |

Annual |

|

Template REM2: Special payments |

Annual |

||

|

Template REM3: Deferred remuneration |

Annual |

||

|

5. Credit Risk |

|||

|

Table CRA – General qualitative information about credit risk |

Table DF-3: Credit risk: general disclosures for all banks |

Specific disclosure w.r.t. credit risk function, viz.,

|

Annual |

|

Template CR1: Credit quality of assets |

Semi-annual |

||

|

Template CR2: Changes in stock of non-performing loans and debt securities |

Semi-annual |

||

|

Table CRB: Additional disclosure related to the credit quality of assets |

|

Annual |

|

|

Table CRC: Qualitative disclosure related to credit risk mitigation techniques |

Table DF-5: Credit risk mitigation: disclosures for standardised approaches |

– |

Annual |

|

Template CR3: Credit risk mitigation techniques – overview |

– |

Semi-annual |

|

|

Table CRD: Qualitative disclosures on bank’s use of external credit ratings under the standardised approach for credit risk |

Table DF-4 – Credit risk: disclosures for portfolios subject to the standardised approach (qualitative) |

Annual |

|

|

Template CR4: Standardised approach – credit risk exposure and Credit Risk Mitigation (CRM) effects |

– |

On-balance sheet and off-balance sheet exposures for each asset class:

|

Semi-annual |

|

Template CR5: Standardised approach – exposures by asset classes and risk weights |

Table DF-4 – Credit risk: disclosures for portfolios subject to the standardised approach (quantitative) |

Risk weight buckets increased; existing format divides into 3 major risk buckets |

Semi-annual |

|

6. Counterparty credit risk |

|||

|

Table CCRA – Qualitative disclosure related to counterparty credit risk |

Table DF-10: General disclosure for exposures related to counterparty credit risk |

– |

Annual |

|

Template CCR1 – Analysis of counterparty credit risk (CCR) exposure by approach |

Structured in a tabulated form with more granular data requirements |

Semi-annual |

|

|

Template CCR3 – CCR exposures by regulatory portfolio and risk weights |

Semi-annual |

||

|

Template CCR4 – Composition of collateral for CCR exposures |

Semi-annual |

||

|

Template CCR5 – Credit derivatives exposures |

|||

|

Template CCR6 – Exposures to central counterparties |

|||

|

7. Securitisation |

|||

|

Table SECA – Qualitative disclosure requirements related to securitisation exposures |

Table DF-6: Securitisation exposures: disclosure for standardised approach |

List of:

|

Annual |

|

Template SEC1 – Securitisation exposures in the banking book |

Bifurcation based on:

|

Semi-annual |

|

|

Template SEC2 – Securitisation exposures in the trading book |

Semi-annual |

||

|

Template SEC3 – Securitisation exposures in the banking book and associated regulatory capital requirements – bank acting as originator |

– |

Semi-annual |

|

|

Template SEC4 – Securitisation exposures in the banking book and associated capital requirements – bank acting as investor |

– |

Semi-annual |

|

|

8. Market Risk |

|||

|

Table MRA – Qualitative disclosure requirements related to market risk |

Table DF-7: Market risk in trading book |

Elaboration of qualitative disclosures, viz.,

|

Annual |

|

Template MR1 – Market risk under the standardised approach |

Classification of positions:

|

Semi-annual |

|

|

9. Operational Risk |

|||

|

Table ORA: Disclosure related to operational risk and operational resilience |

Table DF-8: Operational risk |

Elaboration of qualitative disclosures |

|

|

10. Interest rate Risk |

|||

|

Table IRRA: Disclosure related to Interest Rate Risk |

Table DF-9: Interest rate risk in the banking book (IRRBB) |

Elaborated qualitative disclosures |

Annual for qualitative disclosure and semiannual for quantitative disclosure |

|

11. Macroprudential supervisory measures |

|||

|

Template GSIB1 – Disclosure of G-SIB indicators |

– |

12 indicators used in the assessment methodology of the G-SIB framework |

Annual |

|

Template CCyB1 – Geographical distribution of credit exposures used in the countercyclical capital buffer |

– |

Geographical breakdown of private sector credit exposures (values and RWAs) and Countercyclical capital buffer rate for computation of the bank-specific countercyclical capital buffer rate and amount |

Semi-annual |

|

12. Leverage Ratio |

|||

|

Template LR1 – Summary comparison of accounting assets vs leverage ratio exposure measure |

Table DF 17- Summary comparison of accounting assets vs. leverage ratio exposure measure |

– |

Quarterly |

|

Template LR2 – Leverage ratio common disclosure template |

Table DF-18: Leverage ratio common disclosure template |

– |

Quarterly |

|

13. Liquidity |

|||

|

Table LIQA – Liquidity risk management |

– |

See above |

Annual |

|

Template LIQ1 – Liquidity coverage ratio (LCR) |

– |

Unweighted and weighted values of

|

Quarterly |

|

Template LIQ2 – Net stable funding ratio (NSFR) |

– |

Unweighted value by residual maturity and weighted value of

|

Semi-annual |

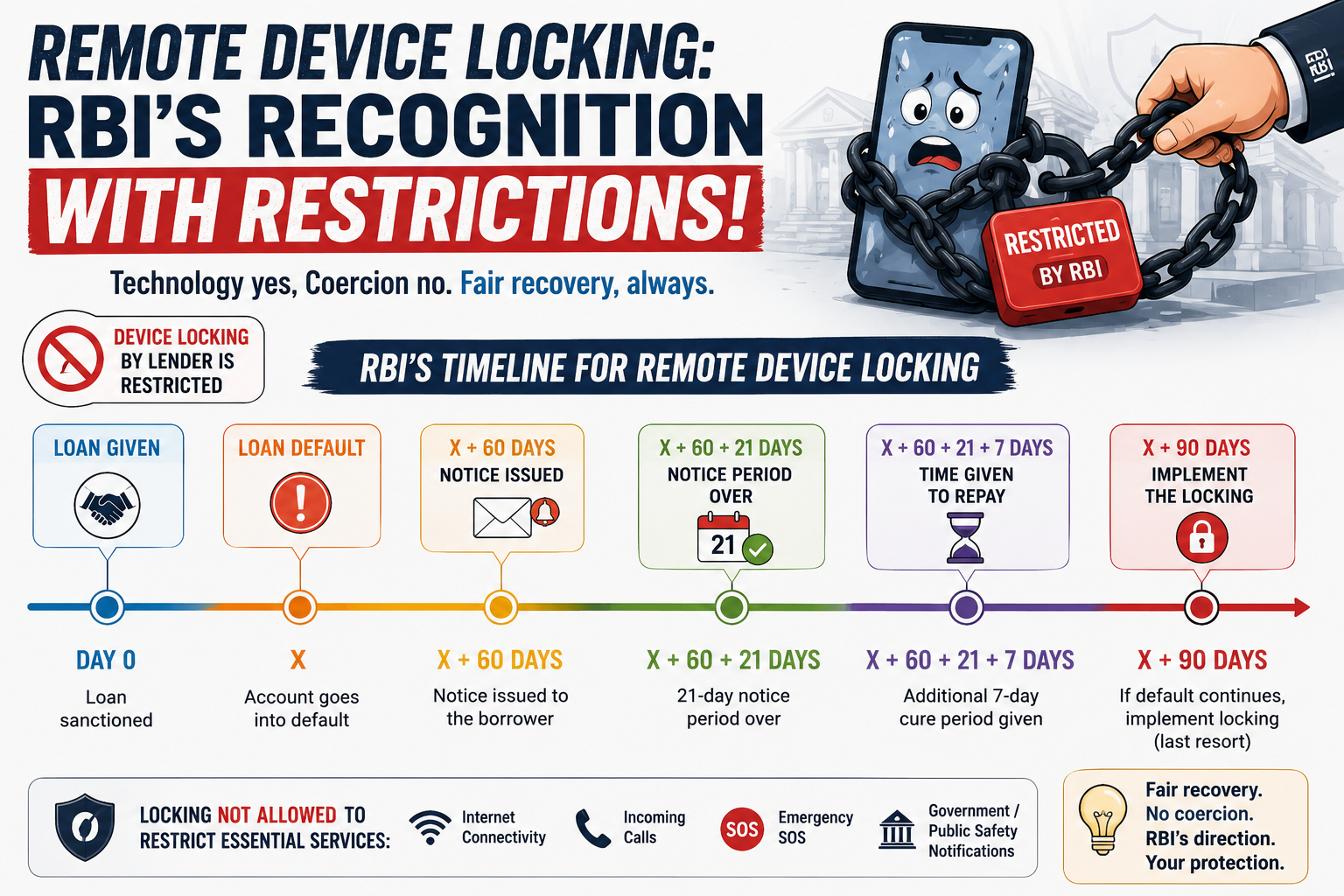

Some proposals may be impractical

– Jeel Ranavat, Assistant Manager| finserv@vinodkothari.com

On May 21,2026, RBI issued revised draft RBI (Non-Banking Financial Companies – Responsible Business Conduct) Amendment Directions, 2026 that contains several paragraphs, not being there in the earlier Draft RBI (Non-Banking Financial Companies – Responsible Business Conduct) Second Amendment Directions, 2026 version, which permit a financier of devices to be able to remotely lock its partial functionality, on continued non-payment of dues. Among other safeguards, such as preserving the basic functionality (access to internet, incoming calls, emergency SOS features, and receipt of emergency Government or public-safety notifications), the RBI also imposes a minimum 90 days default to trigger the locking. In our view, given the short tenure of funding, the 90-day default threshold, clearly a legacy of long-term lending practices, is quite impractical in the context. We present the highlights and our critical appraisal of the RBI’s proposals.

Remote device locking is fast becoming the new device in recovery practices. With the ability to remotely restrict access to a borrower’s device, lenders are increasingly viewing the technology as a powerful tool to control defaults and strengthen recoveries.

In the past supervisory observations, RBI raised concerns regarding “full device locking” mechanisms adopted by certain lenders/Lending Service Provider (LSPs), noting that such measures may be disproportionate, coercive, and restrict access to essential device functionalities. The concerns appear to stem from borrower protection and fair practices considerations, particularly where borrowers are denied access to basic device features unrelated to the financed asset or outstanding dues.

At the same time, the Digital Personal Data Protection Act, 2023 (DPDP Act) introduces an additional layer of regulatory scrutiny like device-level restrictions and monitoring inherently involve the processing and control of personal data, making borrower consent, lawful processing, proportionality, purpose limitation, and data minimisation central to any remote locking framework.

From a data protection perspective, excessive control over a borrower’s device may raise serious concerns around privacy, digital autonomy, and the broader obligation to safeguard the rights of data principals.

The RBI has issued Revised Draft – RBI (Non-Banking Financial Companies – Responsible Business Conduct) Amendment Directions, 2026 which provides deployment of technology-based mechanism for recovery of loan duesalso known as “Remote Device Locking”, and proposes to restrict the use of device-locking mechanisms as a recovery tool, except where the loan was specifically granted for financing the concerned mobile device.

The regulatory message is increasingly clear that technology-driven recovery mechanisms cannot come at the cost of privacy, fairness, or access to essential digital services.

Device-locking mechanisms as a recovery tool is not permitted. However, in case the loan was specifically granted for financing the concerned mobile device, such measures may be adopted by the lenders subject to certain conditions:

Most device financing loans are short-tenure products, typically ranging from 3 to 12 months. If lenders are required to wait until 60 DPD, followed by a 21-day notice period, an additional 7-day cure window, and eventual restriction only after 90 DPD, this may significantly reduce the commercial effectiveness of remote device locking as a recovery tool.

In short-tenure device financing loans, recovery measures are most effective during the early stages of delinquency, when the borrower continues to actively rely on the device.

In practice, several lenders have historically adopted much earlier-stage device restrictions upon payment default. However, RBI appears to be consciously moving away from such practices due to concerns around coercive recovery measures, borrower protection, proportionality, and access to essential digital services.

We are pleased to announce the launch of our e-book — Securitisation, Transfer and Distribution of Credit Risk- for Banks and NBFCs.

This book, spanning over 900+ pages, provides a comprehensive analysis of the evolving regulatory and transactional landscape relating to credit risk transfer in India, with detailed commentary on:

• RBI regulations on securitisation

• Transfer of Loan Exposures or so-called direct assignments

• Co-lending arrangements

• Loan syndication arrangements

• SEBI regulations governing the issue and listing of securitised debt instruments

Designed specifically for banks, NBFCs, market participants, legal professionals and compliance teams, the publication offers practical insights into the regulatory framework governing structured finance and credit distribution transactions.

The Commentary is based on RBI’s November, 2025 version of consolidated Directions.

The book was launched during the 14th Securitisation Summit, and the e-book is available exclusively through the Premium Section of our website.

Kindly note that access to the book will be for a period of one year from the date of purchase of the book.

Read an excerpt from the book here.

Click here to purchase now directly, or

Table of Contents

About the book ……………………………………………………………………………………………………………………………. 1

Preface to Second Edition …………………………………………………………………………………………………………… 22

Chapter 1: Understanding the Basics of Securitisation & Structured Finance ……………………………………. 24

Chapter 2: Securitisation in India: Tracing the developments in the market ………………………………………. 51

Chapter 3: Asset Classes and Structures in India ……………………………………………………………………………. 67

Chapter 4: Law of assignment and true sale of receivables ……………………………………………………………… 83

Chapter 5: Commentary on the Directions on Securitisation of Standard Assets ………………………………. 107

Chapter 6: Listing Regulations On Securitised Debt Instruments & Security Receipts ……………………… 458

Chapter 7: Commentary on the Directions on Transfer of Loan Exposures ……………………………………… 659

Chapter 8: Co-lending Arrangements …………………………………………………………………………………………. 844

Chapter 9: Loan syndication, Consortium Lending, Participation Certificates and Balance Transfers …. 917

Chapter 10: Taxation aspects of Securitisation, Transfer of Loan Exposures and Co-lending ……………. 939

ABOUT THE CONTRIBUTORS ……………………………………………………………………………………………… 960

– Anita Baid, Dayita Kanodia & Chirag Agarwal | finserv@vinodkothari.com

Loading…

Loading…

-Anita Baid & Dayita Kanodia | finserv@vinodkothari.com

RBI, on May 5, 2026, came out with the draft directions on Specified Non-financial Assets (SNFA). These directions have been introduced with the intent of specifying the treatment of non-financial and non-banking assets, particularly immovable property, acquired by the lender in satisfaction of their claims on the borrower.

It is relevant to note that a common framework has been introduced for banks and NBFC, which is in contradiction to the recent consolidation approach adopted by the Department of Regulations. This could possibly also create confusion as to the treatment of non-banking assets relevant for banks, being referred to under the common framework, to be also made applicable on NBFC. In case of banks, the Banking Regulations Act prohibits banks from holding such non-banking assets (NBAs) beyond a period of 7 years, except for property acquired for own use.

Our comments on the key proposals have been provided below:

VKC comment: This would mean that movable property, like vehicles, equipment, is not being covered under the purview of these regulations. Further, the restriction on banks as provided under the BR Act to acquire any immovable assets other than assets put to its own use should not apply to NBFCs.

VKC comment: This could be practically challenging since in certain adverse situations (like fraud classification) the RE may not want to wait for the asset to turn into an NPA before repossession is done. However, practically, evaluation and classification as fraud would easily take 90 days.

Further, the fact that all other means of recovery has been explored and deemed unviable would be very subjective to establish.

VKC comment: It is understood that any compromise settlement of the dues would be done as per the extant regulations for banks and NBFCs (as the case may be) and the amount outstanding post such settlement shall be considered to determine the remaining claims, if any.

At each subsequent reporting date, the SNFA shall be carried on the balance sheet at the lower of the last available distress sale value, or the revised NBV (value of extinguished exposure, net of the notional provisions applicable had the exposure continued on the books of the RE).

VKC Comment: The accounting treatment of the SNFA should have been governed as per the provisions of the accounting standards (para 3.2.23 of Ind AS 109). There could be a possible conflict since the accounting standards require the asset to be recognised on fair value.

VKC Comment: This is consistent with the IRAC provisions which requires the RE to shift from accrual accounting to cash basis accounting upon the asset turning into an NPA.

VKC Comment: SARFAESI is applicable to NBFCs having an asset size of more than 100 crore and where the outstanding amount is a minimum of ₹20 L. Accordingly, in some cases, SARFAESI may not be applicable at all. In such cases, following SARFAESI procedures should ideally not be made mandatory.

VKC Comments: Even under IBC, 29A bars the borrower and its connected persons from bidding on the repossessed assets (except for certain exemptions in case of MSME borrowers).

the asset shall be deemed to have been employed for its own use by the RE and will be recorded as a fixed asset.

VKC Comments: It seems unclear if the RE concerned can put the assets to its own use immediately on the acquisition of such assets.

Also, read our article,

– Team Finserv | finserv@vinodkothari.com

Existing companies may apply within 6 months of 1st July; new companies may avoid registration on satisfying Type 1 and asset size conditions

The RBI’s relief to exempt pure investment companies from exemption from regulation, is now in final shape. We have earlier commented on the draft Amendment Directions. The final amendments in Directions, notified on 29th April, 2026, accept some of the public feedback. However, the condition that the NBFC seeking exemption should not have any debt on the liability, nor any debt on the asset side, even if from/to group entities, remains.

The exemption window opens on 1st July, based on asset size, no customer interface, no public funds and some other conditions (discussed below). The window remains till 31st Dec., 2026; however, even in future, it will be open for NBFCs to opt to exit from registration.

Read more →See our article A[U]n Expected Injury: ECL is here, likely to hurt bank profits and retained earnings in FY28 for an in-depth analysis.