Ombudsman Scheme for PPI issuers

By Simran Jalan (simran@vinodkothari.com)

Introduction

The payment technology has evolved and the number of digital transactions is increasing enormously. With this rapid adoption of digital mode of transactions, there was an emerging need for an expeditious grievance redressal mechanism for strengthening the consumer confidence in this channel. Consequently, the Reserve Bank of India (RBI) has issued an Ombudsman Scheme for Digital Transactions, 2019[1] (Ombudsman Scheme) to provide a mechanism for redressal of complaints against deficiency in services related to digital transactions.

In this article we shall discuss the important provisions of the scheme and their impact on Prepaid Payment Instrument (PPI) issuers.

Applicability

As per the Scheme, only “System Participants” will be covered. The term “System Participants” has been defined in the following manner:

‘System Participant’ means any person other than a bank participating in a payment system as defined under Section 2 of the Payment and Settlement Systems Act, 2007 excluding a ‘System Provider’.

The definition of system provider is derived from section 2 of the Payment and Settlement Systems Act, 2007 which defines “System Provider” as a person who operates an authorised payment system.

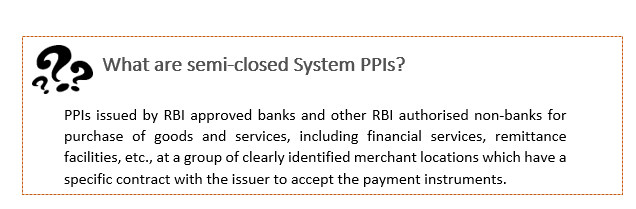

The Ombudsman Scheme does not apply to the PPIs issued by banks, this is because banks are otherwise covered by a separate scheme issued specifically for them. Further, this Scheme only applies to the semi-closed System PPIs.

Meaning of Ombudsman

The Ombudsman for digital transactions shall mean the senior official appointed by the RBI, for a period not exceeding 3 years at a time, to redress the customer complaints and to carry out the functions entrusted to them by or under the Scheme.

Grounds of Complaint

As per Clause 8 of the Ombudsman Scheme, the Ombudsman for digital transactions shall receive and consider complaints on deficiency in services against the PPI issuers on any of the following grounds:

- Failure in crediting merchant’s account within reasonable time;

- Failure to load funds within reasonable time in wallets/cards;

- Unauthorized electronic fund transfer;

- Non-Transfer/Refusal/failure to transfer within reasonable time, the balance in the PPIs to the holder’s own bank account or back to source at the time of closure, expiry of validity period etc., of the PPI.

- Failure to refund within reasonable time/ refusal to refund in case of unsuccessful/returned/rejected/cancelled/transactions;

- Non-credit/ delay in crediting the account of the PPI holder as per the terms and conditions of the promotion officer(s) from time to time, if any;

- Non-adherence to any other instruction of the RBI on PPIs.

While the Scheme does specify, at length, the grounds for filing of compliant, it also specifies the following conditions which must be satisfied before filing of a complaint.

- Before approaching the Ombudsman, the complainant must have approached the PPI Issuer by way of a written representation. Only where the PPI issuer has either rejected the complaint; or has not replied within one month or has not given a satisfying reply, the complainant may approach the Ombudsman.

- The complaint must be made within one year from the date of receiving reply of the PPI issuer or in case no reply is received then within one year and one month after the date of submitting the written representation to the PPI issuer.

- The complaint must not pertain to the same cause of action for which any proceeding is ongoing in any court or, an order has been passed by the court, tribunal or arbitrator or any other forum.

- The complaint shall not be vexatious in nature.

- The complaint must not pertain to disputes arising from a transaction between customers.

Quick actionable by PPI issuers pursuant to the scheme

The following is the set of actionable required on the part of the PPI issuers:

Display salient features of the scheme for Public Knowledge

- The internal customer grievance redressal framework, including contact details of the designated nodal officer to handle the customer complaints along with escalation matrix to be displayed prominently in all offices and branches of the PPI issuer.

- The purpose of the scheme and the contact details of the Ombudsman to whom the complaints are to be made by the aggrieved party to be displayed prominently in all the offices and branches.

- The PPI issuers shall ensure that a copy of the Scheme is available with the designated officer of the company for perusal in the office premises, if anyone desires to do so, and notice about the availability of the Scheme with such designated officer shall be displayed. Further, the PPI issuers shall place a copy of the Scheme on their websites.

Appointment of nodal officers

- The PPI issuers must appoint nodal officers at their Regional/Zonal offices who shall be responsible for representing the company and furnishing information to the Ombudsman in respect of complaints filed against the PPI issuer.

Information to all offices of Ombudsman

- The PPI issuers shall inform all the offices of the Ombudsman about the appointment of nodal officers. Wherever more than one zone/ region of a PPI issuer is falling within the jurisdiction of an Ombudsman, one of the Nodal Officers shall be designated as the ‘Principal Nodal Officer’ for such zones or regions.

Obligations of the PPI issuers

Providing Information to the Ombudsman

- Provide information to the Ombudsman when the Ombudsman calls for it to decide upon any complaint filed, and furnish all certified copies and documents as required from time to time.

Specific Performance

- On admission of a complaint, the Ombudsman may pass an award and it may contain the directions to do specific performance of its obligations in addition to or otherwise, the amount, if any to be paid by it to the complainant by way of compensation for any loss suffered by the complainant arising directly out of the act or the omission of the PPI issuer.

Compliance of the Award

- Within one month from the date of receipt of the letter of acceptance in writing of the Award by the complainant, the PPI issuer shall ensure compliance with the Award and intimate the same to the Ombudsman.

Implementation of the Award

- It is the obligation of the PPI issuer to implement the settlement arrived with the complainant or the Award passed by the Ombudsman when it becomes final.

Reporting to the RBI

- The PPI issuer after implementing the Award, shall send a report in this regard to the RBI within 15 days of the Award becoming final.

Grievance redressal framework under the Master Direction

RBI had issued the Master Direction on Issuance and Operation of Prepaid Payment Instruments on October, 2017[2] wherein it provided the grievance redressal framework to be adopted by the PPI issuers. It instructed the PPI issuers to establish a formal, publicly disclosed customer grievance redressal framework and to designate a nodal officer to handle the customer complaints, the escalation matrix and turnaround time for complaint resolution.

Further, the non-bank PPI issuers were required to provide a quarterly report in the prescribed format regarding the receipt of complaints and action taken status thereon by the 10th of the following month to the respective Regional Office of DPSS.

Conclusion

In the wake of rising discrepancies, the Ombudsman Scheme is expected to increase the responsibility of the non-bank PPI issuers and other system participants as covered under the Scheme. RBI’s overall aim through this is to reduce instances of fraud and ensure that confidence in the payment systems goes up.

[1] https://rbidocs.rbi.org.in/rdocs/Content/PDFs/OSDT31012019.pdf

[2]https://rbidocs.rbi.org.in/rdocs/notification/PDFs/58PPIS11102017A79E58CAEA28472A94596CFA79A1FA3F.PDF

Leave a Reply

Want to join the discussion?Feel free to contribute!