Continuing Disclosures by listed entities: Regulation 30 of SEBI LODR

– Vinod Kothari | corplaw@vinodkothari.com

Loading…

Loading…

Our article on Reg 30 of LODR Regulations can be viewed here

– Vinod Kothari | corplaw@vinodkothari.com

Loading…

Our article on Reg 30 of LODR Regulations can be viewed here

Policies seem to be working at cross-purposes

Vinita Nair, Senior Partner | corplaw@vinodkothari.com

The need to promote bond markets is almost cliched, and does not require elaboration. However, when one observes the regulatory and fiscal developments concerning bond markets in recent times, one wonders whether there is a clear and unified sense of direction. The role of policymaker may be supporting, reformative, protective, promotional, etc. Sometimes, protective regulation may also be intended to play a promotional role – for example, if investors’ interest is better protected, it may promote investor confidence and hence, appetite. However, it is hard to see a clear theme in the spate of changes concerning bond markets in the recent past.

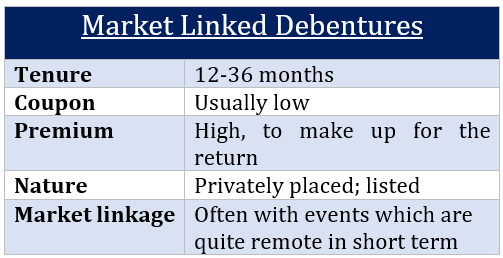

As regards fiscal measures, there are several changes in the Budget 2023 that may be directly or indirectly affecting the bond markets. The Budget saw market-linked debentures[1], a bit controversial development, as a case of fiscal arbitrage, and killed the same, resulting in the death of the instrument. The exemption from withholding tax exemption in case of listed bonds was taken away – which will be difficult to understand as the theoretical justification for withholding tax is the possibility of tax leakage in case of destination-based tax. The case for the leakage is difficult to make, as listed bonds are issued in demat format, and hence, all transactions take place through regular banking channels. If the intent of policymakers was to promote retail investment in bonds, this is certainly antithetical to that objective.

Another fiscal change, which may have a long-term negative impact, is the denial of long-term capital gain treatment to investment in debt mutual funds[2]. Debt mutual funds were also responsible for the demand-side of corporate bonds. Mutual fund’s share in the outstanding corporate bonds as at the end of FY 2022 stood at 15.85%[3]

Read more →Timothy Lopes, Manager

Crowdfunding as a concept has been in the limelight for quite some time now. Globally there are several crowdfunding platforms that exist. These crowdfunding platforms essentially allow almost anybody to raise funds for any cause, ideas or business ventures. Interestingly, the first online crowdfunding platform was launched back in 2001[1].

However, with the advent of online crowdfunding platforms also comes the inherent risks associated with it. Through this article, the author aims to highlight the inherent risks associated with crowdfunding along with the legal permissibility and restraints in India.

Read more →No grandfathering for MLDs, prospectively, tax benefit for debt mutual funds goes away

-Vinod Kothari and Aanchal Kaur Nagpal

As expected, the Finance Bill, 2023 was passed on March 24, 2023 by Lok Sabha within minutes. With a huge amount of changes including several newly inserted provisions, the so-called amendments were actually a Bill in itself, minus any “notes on clauses” or “memorandum of delegated legislation”, and given the amending document that refers to page numbers and line numbers of the Bill, it is a hard to read document, more so to realise the long term impact it has for the capital markets.

For capital markets, the amended Bill confirms that there will be no grandfathering for market-linked debentures (MLDs), as it specifically provides for a grandfathering only for debt mutual funds. Thus, the future of an approximately Rs. 20 lakh crore non-equity-oriented mutual funds in the country[1], going forward, will be questionable.

Read more →– Vinita Nair, Senior Parnter | corplaw@vinodkothari.com

Loading…

– Alignment with international standards and avoidance of greenwashing

– Payal Agarwal and Shreya Salampuria | corplaw@vinodkothari.com

Sustainability labeled bonds, more popularly known as GSS+ bonds, are looked upon as one of the primary means of raising funds towards sustainable development. The same has been discussed in Sustainable finance and GSS+ bonds: State of the Market and Developments. India is also not oblivious to the concept of GSS+ bonds, and companies in India have also been issuing such bonds, in one or more forms.

The issuance of green debt securities (“GDS”) in India was initially formalized through a circular issued by SEBI in 2017 in this regard, later absorbed under the SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021 (“ILNCS Regulations”) read with Chapter IX of the Operational Circular on the same. The regulatory framework for GDS in India has since been reviewed, and following a Consultation Paper on Green and Blue Bonds as a mode of Sustainable Finance (“Consultation Paper”) dated 4th August, 2022, SEBI, in its meeting dated 20th December, 2022 (“Board Meeting”) has approved amendments to the existing regulatory framework for GDS issuance. The press release of the Board Meeting reads as “in the backdrop of increasing interest in sustainable finance in India as well as around the globe, and with a view to align the extant framework for green debt securities with the updated Green Bond Principles (GBP) recognised by IOSCO, SEBI undertook a review of the regulatory framework for green debt securities.”

Pursuant to the review of the regulatory framework for GDS, the following has been notified –

In this write-up, we intend to discuss the revised regulatory framework for GDS issuance in India.

Read more →– Shreya Salampuria, Executive | corplaw@vinodkothari.com

Loading…

Read our comments to SEBI on the said consultation paper:

– Aanchal Kaur Nagpal, Manager | finserv@vinodkothari.com

Tax proposal to tax gains on MLDs as short-term capital gains

The Budget proposes that the capital gains on market linked debentures (MLDs) will be taxed as short term capital gain.

Presently, MLDs are mostly listed, and as listed securities they have 2 advantages:

Market linked debentures is a concept that prevails world-over, with different names such as equity-linked bonds, index-linked bonds, etc. However, in India, the issuance of MLDs was being exploited as a regulatory and tax arbitrage device.

– Vinod Kothari and Payal Agarwal | corplaw@vinodkothari.com

The topic of sustainable finance has become as critical as sustainable development, since finance is the prerequisite for sustainable development. “Finance can play a leading role in allocating investment to sustainable corporates and projects and thus accelerate the transition to a low carbon and more circular economy. Moreover, investors can exert influence on the corporates in which they invest. In this way, long-term investors can steer corporates towards sustainable business practices.”[1] Hence, there is momentum towards organising funds and resources to transition from low energy efficiency to high energy efficiency, or renewable energy devices.

The expression “sustainable finance” is broader, as it encompasses the use of ESG considerations in financing decisions.[2] However, sustainability bonds are capital market instruments issued with a stated end-use. The term GSS+ bonds, which has recently been much in vogue, has G, S, S and then augmented by the + sign. The components of “GSS+” are as follows:

G : Green

S: Social

S: Sustainability

+ : Other labeled bonds, particularly, transition bonds, and depending on the usage, may also include sustainability-linked bonds.

The other labeled bonds may also include blue bonds, gender bonds, climate bonds, yellow bonds etc., although the same may already be covered under one of the components of the GSS bonds. For instance, blue bonds are taken as a part of green bonds, and gender bonds are taken as a part of social bonds.

GSS+ bonds are also called “thematic” or “labeled” bonds, with the use of their proceeds linked with the respective theme represented by such bonds. These expressions may be somewhat overlapping[3].

Read more →– Vinod Kothari | vinod@vinodkothari.com

This version: 31st January, 2023

Following the Sovereign Green Bond framework issued by the Govt of India, and in accordance with the calendar of events issued by RBI, the first tranche of the sovereign green bonds has been successfully issued by the Govt of India. Remarkably, the bonds achieved a greenium of 6 basis points against the expected 2-3 basis points, with the issue selling at a 5-6 basis points lower yield than the sovereign yield of similar tenure. The issuance was more than four times oversubscribed. The five-year bond was priced at 7.10% and 10-year bond at 7.29%, as per the auction results released by RBI. Indian government bonds with the same maturity period were trading at a yield of 7.16% and 7.35%, respectively, during the relevant period.

After the launch of the Sovereign Green Bond framework in November 2022, India has made its fast move for debuting with a Rs 16,000 crore green bond issuance, in two tranches, in January and February 2023, according to an RBI announcement. The proceeds will be deployed in public sector projects which help in reducing the carbon intensity of the economy. The details of such projects are not immediately available; however, going by settled Green Bond Principles , which has also been adopted by India’s own sovereign framework, these projects will be identified and ascertainable disclosed by the issuer in the offer documents[1].

The GoI green bonds will qualify as SLR securities. They will also be available for investment by non-residents on automatic route. There are two maturities – 5 years, and 10 years, each with a value of Rs 8000 crores.

Green bonds are a part of a larger category of sustainability finance instruments, including social, sustainability, transition or other various thematic bond issuances. Green bonds constitute the largest components of the so-called GSS+ bonds.

Green bonds are issued by financial sector entities, direct users as also by sovereigns. The issuance by sovereigns, such as the Government of India in the present case, is fair recent – Poland is said to be the first country in 2016 to have issued a green bond.

Read more →