Indian Securitisation Market opens big in FY 20 – A performance review and a diagnosis of the inherent problems in the market

By Abhirup Ghosh , (abhirup@vinodkothari.com)(finserv@vinodkothari.com)

Ever since the liquidity crisis crept in the financial sector, securitisation and direct assignment transactions have become the main stay fund raising methods for the financial sector entities. This is mainly because of the growing reluctance of the banks in taking direct exposure on the NBFCs, especially after the episodes of IL&FS, DHFL etc.

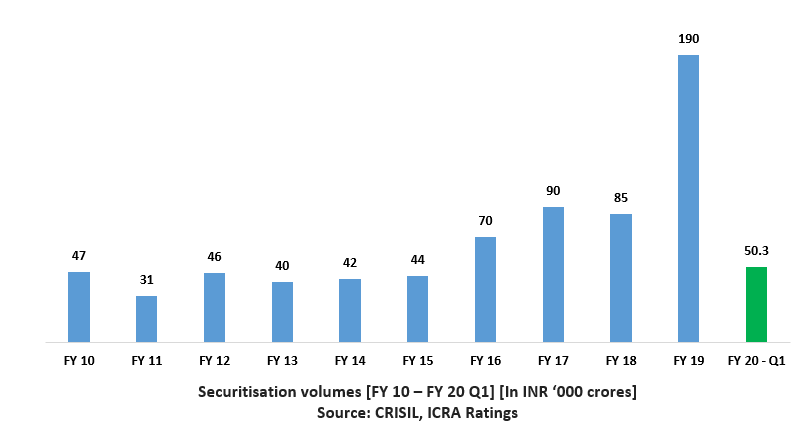

Resultantly, the transactions have witnessed unprecedented growth. For instance, the volume of transactions in the first quarter of the current financial year stood at a record ₹ 50,300 crores[1] which grew at 56% on y-o-y basis from ₹ 32,300 crores. Segment-wise, the securitisation transactions grew by whooping 95% to ₹ 22,000 crores as against ₹ 11,300 crores a year back. The volume of direct assignments also grew by 35% to ₹ 28,300 crores as against ₹ 21,000 crores a year back.

The chart below show the performance of the industry in the past few years:

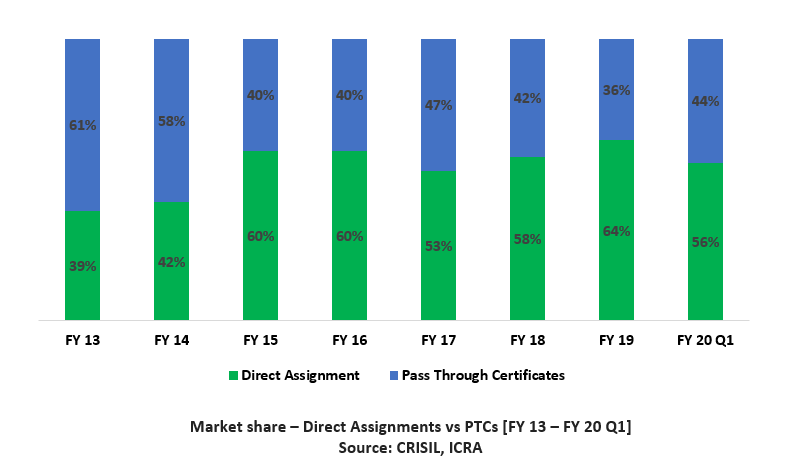

Direct Assignments have been dominating market with the majority share. During Q1 FY 20, DAs constituted roughly 56% of the total market and PTCs filled up the rest. The chart below shows historical statistics about the share of DA and PTCs:

In terms of asset classes, non-mortgage asset classes continue to dominate the market, especially vehicle loans. The table below shows the share of the different asset classes of PTCs:

|

Asset class |

Q1 FY 20 share | Q1 FY 19 share | FY 19 share |

| Vehicle (CV, CE, Car) | 51% | 57% | 49% |

| Mortgages (Home Loan & LAP) | 20% | 0% | 10% |

| Tractor | 6% | 0% | 10% |

| MSME | 5% | 1% | 4% |

| Micro Loans | 4% | 23% | 16% |

| Lease Rentals | 0% | 13% | 17% |

| Others | 14% | 6% | 1% |

Asset class wise share of PTCs

Source: ICRA

Shortcomings in the current securitisation structures

Having talked about the exemplary performance, let us now focus on the potential threats in the market. A securitisation transaction becomes fool proof only when the transaction achieves bankruptcy-remoteness, that is, when all the originator’s bankruptcy related risks are detached from the securitised assets. However, the way the current transactions are structured, the very bankruptcy-remoteness of the transactions has become questionable. Each of the problems have been discussed separately below:

Commingling risk

In most of the current structures, the servicing of the cash flows is carried out of the originator itself. The collections are made as per either of the following methods:

- Cash Collection – This is the most common method of repayment in case of micro finance and small ticket size loans, where the instalments are paid in cash. Either the collection agent of the lender goes to the borrower for collecting the cash repayments or the borrower deposits the cash directly into the bank account of the lender or at the registered office or branch of the lender.

- Encashment of post-dated cheques (PDCs) – The PDCs are taken from the borrower at the inception of the credit facility for the EMIs and as security.

- Transfer through RTGS/NEFT by the customer to the originator’s bank account.

- NACH debit mandate or standing instructions.

In all of the aforesaid cases, the payment flows into the current/ business account of the originator. The moment the cash flows fall in the originator’s current account, they get exposed to commingling risk. In such a case, if the originator goes into bankruptcy, there could be serious concerns regarding the recoverability of the cash flows collected by the originator but not paid to the investors. Also, because redirection of cash flows upon such an event will be extremely difficult to implement. Therefore, in case of exigencies like the bankruptcy of the originator, even an AAA-rated security can become trash overnight. This brings up a very important question on whether AAA-PTCs are truly AAA or not.

This issue can be addressed if, going forward, the originators originate only such transactions in which repayments are to happen through NACH mandates. NACH mandates are executed in favour of third party service providers which triggers direct debit from the bank account of the customers every month against the instalments due. Upon receipt of the money from the customer, the third party service providers then transfer the amount received to the originators. Since, the mandates are originally executed in the name of the third party service providers and not on the originators, the payments can easily be redirected in favour of the securitisation trusts in case the originator goes into bankruptcy. The ease of redirection of cash flows NACH mechanism provides is not available in any other ways of fund transfer, referred above.

Will the assets form part of the liquidation estate of the lessor, since under IndAS the assets continue to get reflected on Balance Sheet of the originator?

With the implementation of Ind AS in financial sector, most of the securitisation transactions are failing to fulfil the complex de-recognition criteria laid down in Ind AS 109. Resultantly, the receivables continue to stay on the books of the originator despite a legal true sale of the same. Due to this a new concern has surfaced in the industry that is, whether the assets, despite being on the books of the originator, be absolved from the liquidation estate of the originator in case the same goes into liquidation.

Under the current framework for bankruptcy of corporates in India, the confines of liquidation estate are laid in section 36 of the IBC. Section 36 (3) lays what all will be included therein. Primarily, section 36 (3) (a) is the relevant provision, saying “any assets over which the corporate debtor has ownership rights” will be included in the estate. There is a reference to the balance sheet, but the balance sheet is merely an evidence of the ownership rights. The ownership rights are a matter of contract and in case of receivables securitised, the ownership is transferred to the SPV.

The bounds of liquidation estate are fixed by the contractual rights over the asset. Contractually, the originator has transferred, by way of true sale, the receivables. The continuing balance sheet recognition has no bearing on the transfer of the receivables. Therefore, even if the originator goes into liquidation, the securitised assets will remain unaffected.

Conclusion

Despite the shortcomings in the current structures, the Indian market has opened big. After the market posted its highest volumes in the year before, several industry experts doubted whether the market will be able to out-do its previous record or for that matter even reach closer to what it has achieved. But after a brilliant start this year, it seems the dream run of the Indian securitisation industry has not ended yet.

[1] https://www.icra.in/Media/OpenMedia?Key=94261612-a1ce-467b-9e5d-4bc758367220

Good Presentation