Can CICs invest in AIFs? A Regulatory Paradox

-Anshika Agarwal (finserv@vinodkothari.com)

Core Investment Companies (CIC) and Alternative Investment Funds (AIF) are two very common modes to channelise investments in the Indian market. Both are regulated by different regulators; while CICs are regulated by the RBI, AIFs are regulated by the SEBI. Under their respective regulatory frameworks, both are technically permitted to invest in one another. However, this permissibility introduces an intriguing paradox, especially for a CIC, which is allowed to invest in group companies. It points out that this approach effectively creates two investment pools—one directly under the CICs and another through the AIFs. This dual-pool structure complicates what could otherwise be a straightforward process, introducing unnecessary layers of complexity, thus deviating from the primary purpose of CICs to hold and manage investments efficiently within group companies.

The following article examines the implications of Paragraph 26(a)1 of the Master Direction – Core Investment Companies (Reserve Bank) Directions, 2016 (“CIC Master Directions”), but before delving into the specifics, it may be worthwhile to discuss in brief the concepts of AIF and CIC.

What are AIFs (Alternative Investment Funds)?

AIFs have gained prominence as a pivotal part of the financial ecosystem, providing investors with access to diverse and innovative investment opportunities. The key features of an AIF are as follows:

- An AIF is a privately pooled investment vehicle, therefore, it cannot raise money from public at large through a public issue of units;

- The investors could be Indian or foreign – there is no bar on the nature of the investor who can invest.

- The investments made by the fund should be in accordance with the investment policy.

- There are three categories of AIFs, depending on the kind of investments they make, and each category is regulated differently:

- Category 1 which invests in start up or early stage ventures or social ventures or SMEs or infrastructure or other sectors or areas which the government or regulators consider as socially or economically desirable and shall include venture capital funds, SME Funds, social venture funds, infrastructure funds and such other Alternative Investment Funds as may be specified.

- Category 2 which does not fall in Category I and III and which does not undertake leverage or borrowing other than to meet day to day operational requirements and as permitted in these regulations. It includes private equity funds or debt funds for which no specific incentives or concessions are given by the government or any other regulator shall be included.

- Category 3 which employs diverse or complex trading strategies and may employ leverage including through investment in listed or unlisted derivatives.

What are Core Investment Companies (CICs)?

CICs are a specialized subset of Non-Banking Financial Companies (NBFCs) established with the primary purpose of holding and managing investments in group companies. CICs do not engage in traditional financial intermediation but play a vital role in maintaining financial stability within the ‘group companies’. CICs are governed under the CIC Master Directions to ensure that their activities align with regulatory standards.

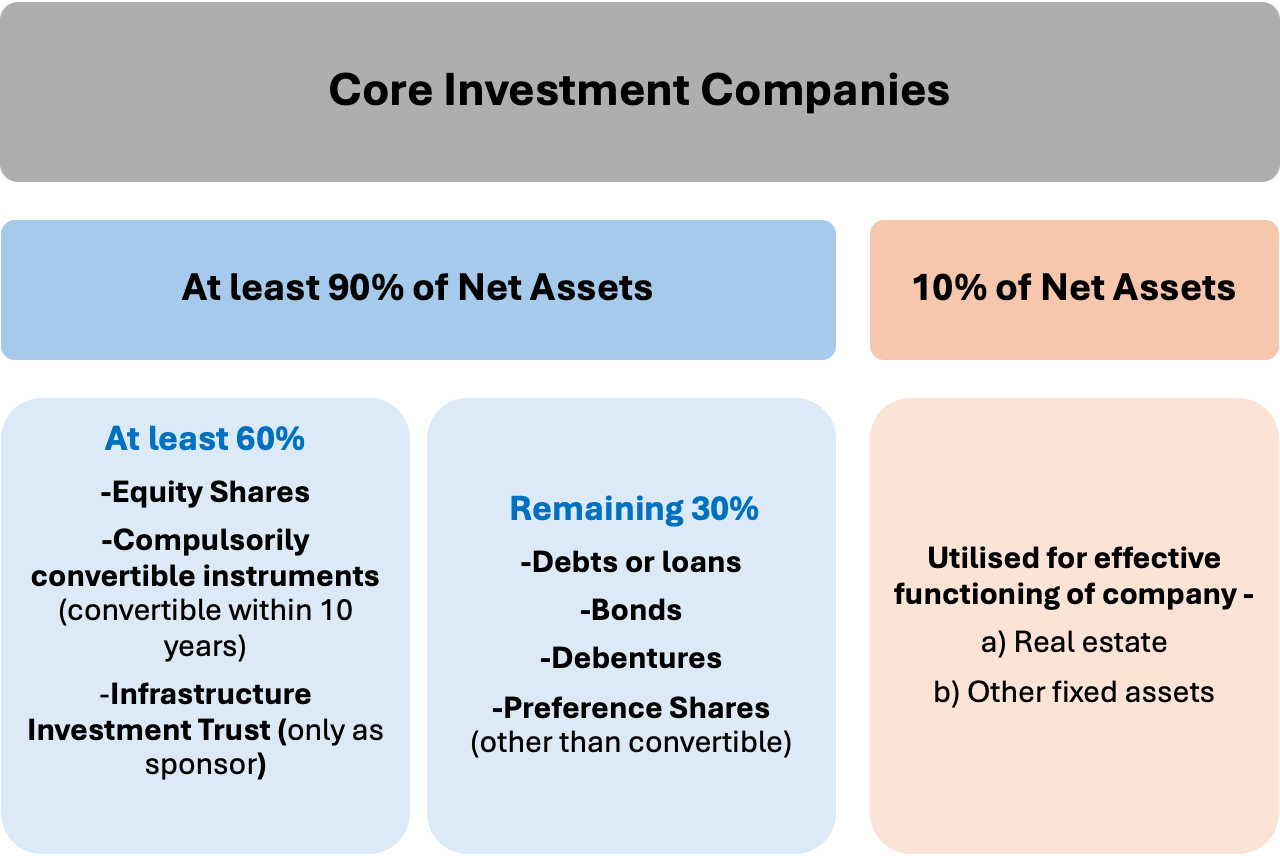

Below given graph explains the regulatory permissibility of the kind of investments a CIC can make:

In addition with the aforesaid, it may further be noted that CICs are permitted to carry out the following financial activities only:

- investment in-

- bank deposits,

- money market instruments, including money market mutual funds that make investments in debt/money market instruments with a maturity of up to 1 year.

- government securities, and

- bonds or debentures issued by group companies,

- granting of loans to group companies and

- issuing guarantees on behalf of group companies.

It may be noted that the RBI’s FAQs on Core Investment Companies, particularly Question 92 has clarified about the 10% of Net Asset –

“What items are included in the 10% of Net assets which CIC/CIC’s-ND-SI can hold outside the group?

Ans: These would include real estate or other fixed assets which are required for effective functioning of a company, but should not include other financial investments/loans in non group companies.”

Who are included in Group Companies?

The term “group companies” is defined under Para 3(1)(v) of the CIC Master Directions. It refers to an arrangement involving two or more entities that are related to each other through any of the following relationships:

| Subsidiary – Parent (as defined under AS 21), Joint Venture (as defined under AS 27), Associate (as defined under AS 23), Promoter-Promotee (as per the SEBI [Acquisition of Shares and Takeover] Regulations, 1997 for listed companies), Related Party (as defined under AS 18), Entities sharing a Common Brand Name, or Entities with an investment in equity shares of 20% or more |

The Issue with Paragraph 26(a): The paradox

Para 26A of the CIC Master Directions deals with Investments in AIFs. The language of the provisions suggest that CICs are permitted to invest in AIFs. However, this provision introduces a significant legal contradiction that undermines the regulatory framework governing CICs. According to the Doctrine of Colorable Legislation, a legal principle ensuring legislative consistency, what cannot be achieved directly cannot be permitted indirectly. By allowing CICs to invest in AIFs, Para 26(a) effectively circumvents the explicit restriction on investments outside group companies. This indirect allowance is inconsistent with the foundational objectives of the CIC Master Directions and creates substantial legal and operational confusion.

Can there be an AIF which in turn invests in the group only?

Under the SEBI (Alternative Investment Funds) Regulations, 2012, the primary objective of an Alternative Investment Fund (AIF) is to pool funds from investors and allocate them across diverse investment opportunities. However, structuring an AIF to invest predominantly or exclusively in entities within the same group raises concerns regarding compliance with SEBI’s regulatory framework, particularly its diversification. SEBI imposes strict investment concentration limits, as outlined in one of its Circular3.

For Category I and II AIFs, no more than 25% of their investable funds can be allocated to a single investee company, while Category III AIFs are restricted to 10%. These regulations inherently prevent AIFs from focusing solely on group entities unless the investment structure strictly adheres to these limits. For CICs intending to invest in AIFs, these restrictions pose significant limitations if the goal is to channel funds primarily into group companies.

Can AIFs be a Group Entity in a CIC’s Group Structure?

Technically, the answer is affirmative—AIFs can be part of a group entity within a group if it satisfies any of the conditions mentioned in the definition. However, if CICs invest in AIFs within the same group structure, it fails to resolve the underlying issue. AIFs often invest outside the group companies, exposing CICs indirectly to entities external to the group. This contradicts the core purpose of CICs, which is to focus investments within their own group companies. Such a structure not only undermines the original intent of CICs but also raises compliance concerns. The RBI adopts a pass-through approach in these cases and is likely to view such practices as non-compliant.

Conclusion

The regulatory paradox of allowing CICs to invest in AIFs under Para 26(a) of the CICs Master Direction raises important questions about the practicality and purpose of this provision. At its core, CICs are meant to simplify and streamline the management of investments within their group companies. However, the inclusion of AIFs creates an unnecessary layer of complexity, dividing investments into dual investment pools and making it harder to track, manage, and maintain transparency.

This arrangement doesn’t just complicate operations, it also moves CICs away from their original purpose. By routing investments through AIFs, CICs are exposed to entities outside their group, which can lead to compliance risks, regulatory confusion, and inefficiencies. Even from a taxation perspective, the setup offers no real benefits, adding financial burdens without meaningful gains. Paragraph 26(a) of the CICs Master Direction has been taken from the SBR Master Direction, which is applicable to NBFCs. However, including it in the CICs Master Direction, which provided regulation specifically for CICs NBFC does not appear to serve any purpose. Even if it were to be amended, its relevance of stating the same for CICs NBFC would still remain questionable.

- Reserve Bank of India, Master Direction – Core Investment Companies (Reserve Bank) Directions, 2016. Available at:https://www.lawrbit.com/wp-content/uploads/2021/05/Master-Direction-Core-Investment-Companies-Reserve-Bank-Directions-2016.pdf (Accessed: 19 January 2025). ↩︎

- FAQs on Core Investment Companies, available at: https://www.rbi.org.in/commonman/english/scripts/FAQs.aspx?Id=836 (Accessed: 19 January 2025). ↩︎

- SEBI (Alternative Investment Funds) Regulations, 2012 available at: https://www.sebi.gov.in/legal/regulations/apr-2017/sebi-alternative-investment-funds-regulations-2012-last-amended-on-march-6-2017-_34694.html ↩︎

FAQs on Specific Due Diligence of investors & investments of AIFs

Team Vinod Kothari & Company | corplaw@vinodkothari.com

Refer to our related resources below:

- Trust, but verify: AIFs cannot be used as regulatory arbitrage (updated as on October 9, 2024)

- AIFs ail SEBI: Cannot be used for regulatory breach

- Cat I & II AIFs can borrow to meet temporary shortfall in investment drawdown

- RBI bars lenders’ investments in AIFs investing in their borrowers

- Some relief in RBI stance on lenders’ round tripping investments in AIFs

Trust, but verify: AIFs cannot be used as regulatory arbitrage

SEBI mandates ongoing due diligence for investors and investments made by AIFs

-Vinita Nair, Senior Partner and Lavanya Tandon, Executive | corplaw@vinodkothari.com

May 03, 2024 (updated on October 9, 2024)

Background

SEBI had raised concerns relating to evergreening of loans, circumvention of FEMA norms, QIB regulations and other concerns on regulatory arbitrage by Alternative Investment Funds (‘AIFs’) in its Consultation Paper issued in January, 2024. SEBI also recorded 40+ cases wherein the structure of AIF had been abused and used to circumvent extant financial sector regulations. Read our analysis in the article ‘AIFs ail SEBI: Cannot be used for regulatory breach’ dated January 31, 2024. Further, RBI had also barred all regulated entities (REs) with respect to their investments in AIFs, discussed in our article.

Subsequent to receipt of public comments, the proposal to mandate due-diligence (‘DD’) of investors and each of the investments made by the AIF was approved in the SEBI Board meeting held on March 15, 2024. SEBI notified SEBI (Alternative Investment Funds) (Second Amendment) Regulations, 2024 effective from April 25, 2024 amending Reg. 20 of the SEBI (Alternative Investment Funds) Regulations, 2012 (‘AIF Regulations’) dealing with general obligations thereby requiring every a. AIF, b. investment manager of the AIF, c. KMP of the AIF, and d. KMP of the investment manager, to exercise specific DD with respect to their investors and investments in order to prevent facilitation of circumvention of such laws as may be specified by SEBI from time to time.

The list of laws, thresholds and conditions for DD, reporting requirements etc. has been provided in SEBI circular dated Oct 8, 2024 (‘SEBI Circular’). DD is required to be carried out prior to making of investments as per implementation standards formulated by Standard Setting Forum for AIFs (‘SFA’) and published on websites of the industry associations which are part of the SFA, i.e., Indian Venture and Alternate Capital Association (‘IVCA’), PE VC CFO Association and Trustee Association of India.

Scope of laws covered under the ambit of due diligence

The list of laws provided in the SEBI Circular comprises of the following:

- Provisions of SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (‘ICDR Regulations’), and other regulations of SEBI wherein benefits or relaxations have been provided to entities designated as Qualified Institutional Buyers (‘QIBs’).

- Provisions of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (‘SARFAESI Act’) wherein benefits are provided to entities designated as Qualified Buyers (‘QBs’).

- Prudential norms specified by RBI for regulated lenders with respect to Income Recognition, Asset Classification, Provisioning and restructuring of stressed assets;

- Rule 6 of FEMA (Non-Debt Instruments) Rules, 2019 (NDI Rules) for investment from countries sharing land border with India ( read with Press Note 3 dated April 17, 2020 of FDI Policy 2020)

Timing, thresholds for DD, reporting requirements

Pursuant to the SEBI Circular, the due diligence for various investors and investments is required to be carried out by a. AIF, b. investment manager of the AIF, c. KMP of the AIF, and d. KMP of the investment manager in accordance with the Implementation Standards. The table below indicates in brief the criteria, checkpoints and timelines for conducting due diligence along with the consequences of the outcome.

| Sr. No | Objective intended to be achieved by investors through investments in AIF scheme | Regulations/ Directions/ Norms applicable | Applicability of requirement of DD for every scheme of AIF (refer Note 1) | Checkpoints for manager for specific DD | Timing of DD | Consequence of outcome of DD & reporting requirements, if any |

|---|---|---|---|---|---|---|

| 1 | Benefits designated for QIBs | ICDR and other SEBI Regulations | If an investor, or investors belonging to the same group, contribute(s)50% or more to the corpus of the scheme. | Manager to check if such if investor/ investors of the same group is/are:(i) QIBs themselves or,(ii) Entities established, owned or controlled by the Central Government or a State Government or the Government of a foreign country, including central banks and sovereign wealth funds.Note: Where such investor is an AIF or fund set up in IFSC or outside India, above check to be carried out on a look through basis. | Prior to availing benefits available to QIBs | Refer Note 2 below for existing investments & Note 3 for proposed investments.Manager to provide confirmation to SE or lead manager or merchant banker on this. |

| 2 | Benefits designated for QBs | Under SARFAESI Act | If an investor, or investors belonging to the same group, contribute(s)50% or more to the corpus of the scheme. | Same as above | Prior to making any investments or availing benefits | Refer Note 2 below for existing investments & Note 3 for proposed investments. |

| 3 | RBI regulated lenders/ entities ever-greening their stressed loans/ assets & circumventing RBI norms | RBI norms on Income Recognition, Asset Classification, Provisioning and Restructuring of stressed loans/ assets | (a)whose manager or sponsor is an entity regulated by RBI; or,(b)that has investor(s)regulated by RBI who:(i)individually or along with investors of the same group contribute(s) 25% or more to the corpus of the scheme; or(ii) is an associate of the manager/ sponsor of the AIF;(iii) has majority or veto power [by itself, or through its representatives/ nominees] in voting over decisions of the investment committee set up by the manager to approve investment decisions of the scheme.Note: where investor is an AIF or fund set up in IFSC or outside India, criteria check to be carried out on a look through basis. | Refer Note 4. | Prior to making any investments, to avoid indirect investment by RBI regulated lender/ entity. | Refer Note 2 below for existing investments & Note 3 for proposed investments. |

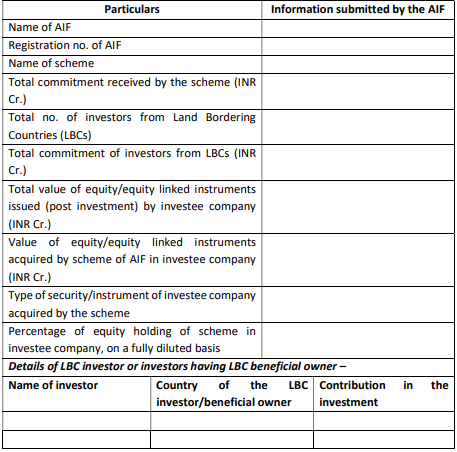

| 4 | Investment from countries sharing land border with India | FEMA (NDI) Rules, 2019 | Where 50% or more of the corpus of the scheme is contributed by investors (a)who are citizens of/are from/are situated in a country which shares land border with India; or(b)whose beneficial owners, as determined in terms of Rule 9 (3) of the PMLA (Maintenance of Records) Rules, 2005, are citizens of/are from/are situated in a country which shares a land border with India. | If the proposed investment would result in the scheme holding 10 % or more of equity/equity-linked securities issued by the company (on a fully-diluted basis), the manager to check details stated in the previous column, by collecting information on the country of investors and their beneficial owners. | Prior to making any investment | Refer Note 2 below for existing investments & Note 5 for proposed investments. |

Note 1: same group’ shall mean ‘related parties’ and ‘relatives’ as defined in SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

Note 2:

For Sr nos 1 to 3: DD requirement is applicable for existing investments too, held by AIF schemes as on October 8, 2024:

- If DD check not satisfactory – details of investment to be reported to AIF’s custodian on or before April 07, 2025, in the format as per Annexure 1 of the circular;

- If DD check satisfactory – AIF manager to submit an undertaking to AIF’s custodian on or before April 07, 2025.

For Sr no. 4: Reporting is required to be made for existing investments held by AIF schemes as on October 8, 2024 if the scheme holds 10% or more of equity/ equity-linked securities on a fully-diluted basis, to AIF’s custodian on or before April 07, 2025 in the format prescribed by SFA.

Note 3:

Consequence of not satisfying requirements of DD checks specified by SFA for proposed investments in case of Sr nos 1 to 3:

- Such investor or investor group to be excluded along with necessary disclosure in the private placement memorandum (PPM); or

- Investment cannot be made.

Note 4:

Note 5: Details of investment, which would result in the scheme holding 10% or more of equity/ equity-linked securities on a fully-diluted basis, to be reported to the custodian within 30 days of investment, in the below format specified by SFA.

DD requirement – one-time or ongoing?

As discussed in the SEBI BM Agenda, the purpose of the due-diligence check is to prevent facilitation of any circumvention of provisions of financial sector regulators, which cannot be a time specific check. An entity who intends to circumvent can design the structure in such a way that, at a later date post investment, it acquires the units of AIFs post investment, such as buying the units of an existing investor or by acquiring control over the existing investor entity, as per prior arrangement. Accordingly, it has been indicated that due diligence around investors and investments will be an ongoing one.

Applicability of DD – prospective or retrospective?

As per the SEBI circular this is applicable for existing and prospective investments. Refer Note 2 above.

Obligations of Custodian to the AIF

- Information received from AIFs under Note 2 to be furnished to SEBI on or before May 7, 2025.

- Information received from AIFs in terms of Note 4 above on a monthly basis to be compiled and reported to SEBI within 10 working days from month end.

Power of AIF to exclude an investor

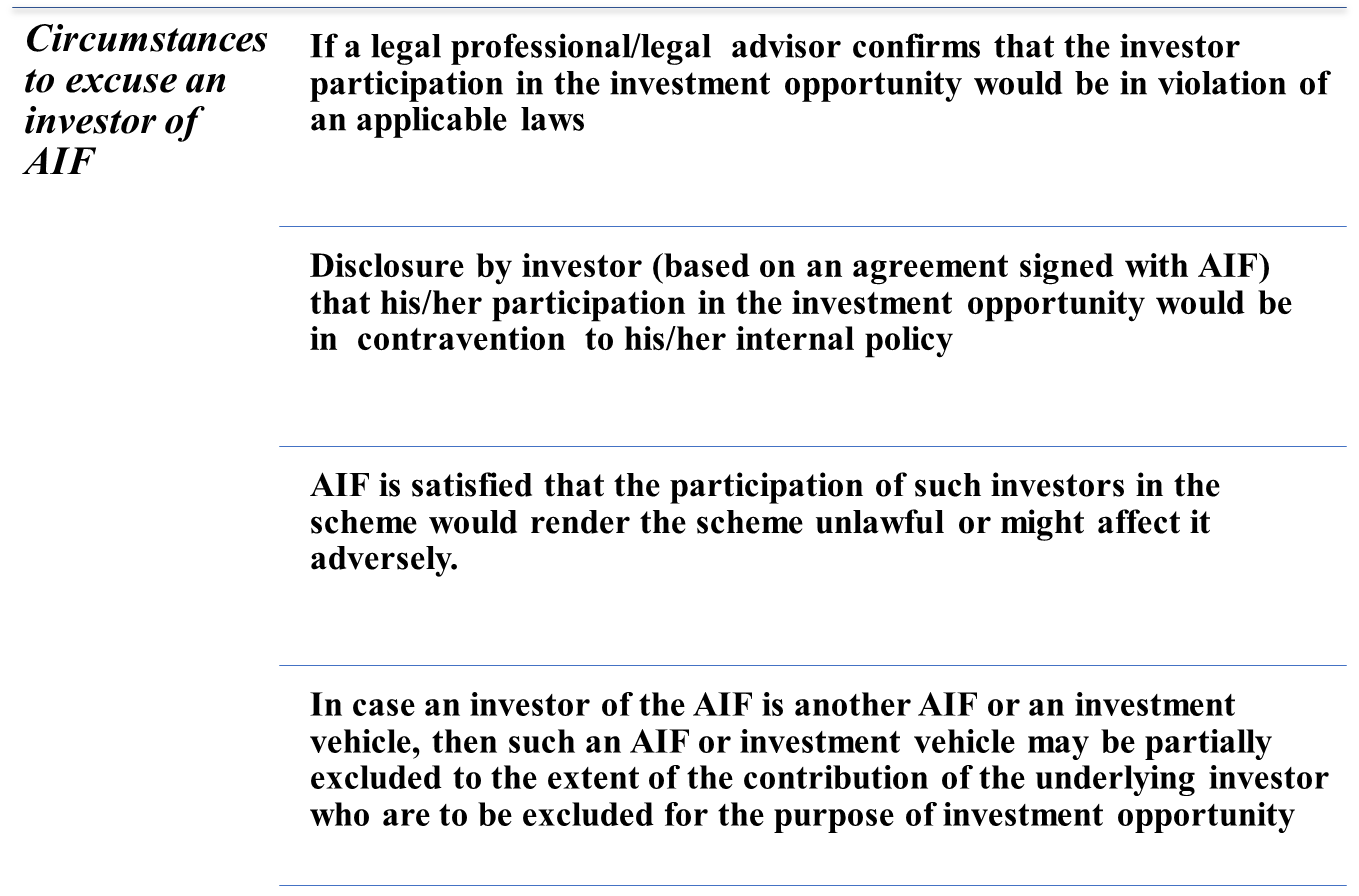

As per SEBI Circular, in cases where the outcome of DD is not satisfactory, in that case the AIF will either have to exclude the investor or investor group or abstain from making the proposed investment.

Dealing with power to exclude an investor, in April 2023 SEBI had issued ‘Guidelines with respect to excusing or excluding an investor from an investment of AIF that empowered an AIF to excuse its investor from participating in a particular investment in the following circumstances:

Figure 1: Circumstances to excuse an investor of AIF

Conclusion

The present amendment and SEBI Circular lays an onerous burden on the AIF, manager and KMP of the AIF and the manager. The DD requirement has become effective from October 8, 2024 and applies to existing investments as well. The AIFs have an actionable of evaluating the existing investments in the scheme in the light of the present amendment and ensure reporting in next 6 months. The obligation of on-going due diligence will result in a compliance burden, but is justified given the intent of law as “quando aliquid prohibetur ex directo, prohibetur et per obliquum” i.e. things that cannot be done directly should not be done indirectly either. AIFs will continue ‘trust, but verify’ using the DD standards for due diligence. The trustee/ sponsor of the AIF is required to ensure that compliance status of this amendment is reported to SEBI in the ‘Compliance Test Report’ prepared by the manager in terms of Chapter 15 of Master Circular for AIFs.

Our other resources:

REIT and InvIT unitholders with 10% aggregate holding get Board nomination rights

Avinash Shetty, Assistant Manager | corplaw@vinodkothari.com

Comparison between NBFC-ICC, CIC and AIF

Loading…

Loading…

Our resources on related topics – https://vinodkothari.com/category/financial-services/

AIF Second Amendment Regulations, 2021 – Regulated Steps towards Liberalised Investment

-Megha Mittal (mittal@vinodkothari.com)

Amidst the various concerns addressed in the Board Meeting dated 25th March, 2021,[1] the Securities and Exchange of Board of India (‘SEBI’) extensively dealt with several issues identified with respect to Alternative Investment Funds (‘AIFs’), inter-alia a green signal to AIFs for investing in units of other AIFs; ambiguity regarding the scope of the term ‘start-up’; and the need for a code of conduct laying down guiding principles on accountability of AIFs, their managers and personnel, towards the various stakeholders including investors, investee companies and regulators.

Thus, with a view to target the issues in consideration, the Board proposed that the following amendments be introduced in the SEBI (Alternative Investment Funds) Regulation, 2012 (‘AIF Regulations’/ ‘Principal Regulations’)[2] –

- provide a framework for Alternative Investment Funds (AIFs) to invest simultaneously in units of other AIFs and directly in securities of investee companies;

- provide a definition of ‘start-up’ as provided by Government of India and to clarify the criteria for investment by Angel Funds in start-ups

- prescribe a Code of Conduct for AIFs, key management personnel of AIFs, trustee, trustee company, directors of the trustee company, designated partners or directors of AIFs, as the case may be, Managers of AIFs and their key management personnel and members of Investment Committees and bring clarity in the responsibilities cast on members of Investment Committees; and

- remove the negative list from the definition of venture capital undertaking.

The aforesaid proposals, put to the fore in view of the suggestions and requests received from several stakeholder groups like the domestic AIFs, global investors, and the regulatory bodies, have now been notified vide notification dated 5th May, 2021, via the SEBI (Alternative Investment Funds) (Second Amendment) Regulations, 2021[3] (‘Amendment Regulations’). A key takeaway from the Amendment Regulations is the flexibility granted w.r.t. indirect investments by AIFs for investment in units of another AIF, however with some riders and possible gaps, as discussed below.

Below we summarise and discuss the amendments introduced vide the Amendment Regulations, and analyse its impact

Law relating to collective investment schemes on shared ownership of real assets

-Vinod Kothari (finserv@vinodkothari.com)

The law relating to collective investment schemes has always been, and perhaps will remain, enigmatic, because these provisions were designed to ensure that enthusiastic operators do not source investors’ money with tall promises of profits or returns, and start running what is loosely referred to as Ponzi schemes of various shades. De facto collective investment schemes or schemes for raising money from investors may be run in elusive forms as well – as multi-level marketing schemes, schemes for shared ownership of property or resources, or in form of cancellable contracts for purchase of goods or services on a future date.

While regulations will always need to chase clever financial fraudsters, who are always a day ahead of the regulator, this article is focused on schemes of shared ownership of properties. Shared economy is the cult of the day; from houses to cars to other indivisible resources, the internet economy is making it possible for users to focus on experience and use rather than ownership and pride of possession. Our colleagues have written on the schemes for shared property ownership[1]. Our colleagues have also written about the law of collective investment schemes in relation to real estate financing[2]. Also, this author, along with a colleague, has written how the confusion among regulators continues to put investors in such schemes to prejudice and allows operators to make a fast buck[3].

This article focuses on the shared property devices and the sweep of the law relating to collective investment schemes in relation thereto.

Basis of the law relating to collective investment schemes

The legislative basis for collective investment scheme regulations is sec. 11AA (2) of the SEBI Act. The said section provides:

Any scheme or arrangement made or offered by any company under which,

- the contributions, or payments made by the investors, by whatever name called, are pooled and utilized solely for the purposes of the scheme or arrangement;

- the contributions or payments are made to such scheme or arrangement by the investors with a view to receive profits, income, produce or property, whether movable or immovable from such scheme or arrangement;

- the property, contribution or investment forming part of scheme or arrangement, whether identifiable or not, is managed on behalf of the investors;

- the investors do not have day to day control over the management and operation of the scheme or arrangement.

The major features of a CIS may be visible from the definition. These are:

- A schematic for the operator to collect investors’ money: There must be a scheme or an arrangement. A scheme implies a well-structured arrangement whereby money is collected under the scheme. Usually, every such scheme provides for the entry as well as exit, and the scheme typically offers some rate of return or profit. Whether the profit is guaranteed or not, does not matter, at least looking at the definition. Since there is a scheme, there must be some operator of the scheme, and there must be some persons who put in their money into the scheme. These are called “investors”.

- Pooling of contributions: The next important part of a CIS is the pooling of contributions. Pooling implies the contributions losing their individuality and becoming part of a single fungible hotchpot. If each investor’s money, and the investments therefrom, are identifiable and severable, there is no pooling. The whole stance of CIS is collective investment. If the investment is severable, then the scheme is no more a collective scheme.

- Intent of receiving profits, produce, income or property: The intent of the investors contributing money is to receive results of the collective investment. The results may be in form of profits, produce, income or property. The usual feature of CIS is the operator tempting investors with guaranteed rate of return; however, that is not an essential feature of CISs.

- Separation of management and investment: The management of the money is in the hands of a person, say, investment manager. If the investors manage their own investments, there is no question of a CIS. Typically, investor is someone who becomes a passive investor and does not have first level control (see next bullet). It does not matter whether the so-called manager is an investor himself, or may be the operator of the scheme as well. However, the essential feature is there being multiple “investors”, and one or some “manager”.

- Investors not having regular control over the investments: As discussed above, the hiving off of the ownership and management of funds is the very genesis of the regulatory concern in a CIS, and therefore, that is a key feature.

The definition may be compared with section 235 of the UK Financial Services and Markets Act, which provides as follows:

- In this Part “collective investment scheme” means any arrangements with respect to property of any description, including money, the purpose or effect of which is to enable persons taking part in the arrangements (whether by becoming owners of the property or any part of it or otherwise) to participate in or receive profits or income arising from the acquisition, holding, management or disposal of the property or sums paid out of such profits or income.

- The arrangements must be such that the persons who are to participate (“participants”) do not have day-to-day control over the management of the property, whether or not they have the right to be consulted or to give directions.

- The arrangements must also have either or both of the following characteristics—

- the contributions of the participants and the profits or income out of which payments are to be made to them are pooled;

- the property is managed as a whole by or on behalf of the operator of the scheme.

- If arrangements provide for such pooling as is mentioned in subsection (3)(a) in relation to separate parts of the property, the arrangements are not to be regarded as constituting a single collective investment scheme unless the participants are entitled to exchange rights in one part for rights in another.

It is conspicuous that all the features of the definition in the Indian law are present in the UK law as well.

Hong Kong Securities and Futures Ordinance [Schedule 1] defines a collective investment scheme as follows:

collective investment scheme means—

- arrangements in respect of any property—

- under which the participating persons do not have day-to-day control over the management of the property, whether or not they have the right to be consulted or to give directions in respect of such management;

- under which—

- the property is managed as a whole by or on behalf of the person operating the arrangements;

- the contributions of the participating persons and the profits or income from which payments are made to them are pooled; or

- the property is managed as a whole by or on behalf of the person operating the arrangements, and the contributions of the participating persons and the profits or income from which payments are made to them are pooled; and

- the purpose or effect, or pretended purpose or effect, of which is to enable the participating persons, whether by acquiring any right, interest, title or benefit in the property or any part of the property or otherwise, to participate in or receive—

- profits, income or other returns represented to arise or to be likely to arise from the acquisition, holding, management or disposal of the property or any part of the property, or sums represented to be paid or to be likely to be paid out of any such profits, income or other returns; or

- a payment or other returns arising from the acquisition, holding or disposal of, the exercise of any right in, the redemption of, or the expiry of, any right, interest, title or benefit in the property or any part of the property; or

- arrangements which are arrangements, or are of a class or description of arrangements, prescribed by notice under section 393 of this Ordinance as being regarded as collective investment schemes in accordance with the terms of the notice.

One may notice that this definition as well has substantially the same features as the definition in the UK law.

Judicial analysis of the definition

Part (iii) of the definition in Indian law refers to management of the contribution, property or investment on behalf of the investors, and part (iv) lays down that the investors do not have day to day control over the operation or management. The same features, in UK law, are stated in sec. 235 (2) and (3), emphasizing on the management of the contributions as a whole, on behalf of the investors, and investors not doing individual management of their own money or property. The question has been discussed in multiple UK rulings. In Financial Conduct Authority vs Capital Alternatives and others, [2015] EWCA Civ 284, [2015] 2 BCLC 502[4], UK Court of Appeal, on the issue whether any extent of individual management by investors will take the scheme of the definition of CIS, held as follows: “The phrase “the property is managed as a whole” uses words of ordinary language. I do not regard it as appropriate to attach to the words some form of exclusionary test based on whether the elements of individual management were “substantial” – an adjective of some elasticity. The critical question is whether a characteristic feature of the arrangements under the scheme is that the property to which those arrangements relate is managed as a whole. Whether that condition is satisfied requires an overall assessment and evaluation of the relevant facts. For that purpose it is necessary to identify (i) what is “the property”, and (ii) what is the management thereof which is directed towards achieving the contemplated income or profit. It is not necessary that there should be no individual management activity – only that the nature of the scheme is that, in essence, the property is managed as a whole, to which question the amount of individual management of the property will plainly be relevant”.

UK Supreme Court considered a common collective land-related venture, viz., land bank structure, in Asset Land Investment Plc vs Financial Conduct Authority, [2016] UKSC 17[5]. Once again, on the issue of whether the property is collective managed, or managed by respective investors, the following paras from UK Financial Conduct Authority were cited with approval:

The purpose of the ‘day-to-day control’ test is to try to draw an important distinction about the nature of the investment that each investor is making. If the substance is that each investor is investing in a property whose management will be under his control, the arrangements should not be regarded as a collective investment scheme. On the other hand, if the substance is that each investor is getting rights under a scheme that provides for someone else to manage the property, the arrangements would be regarded as a collective investment scheme.

Day-to-day control is not defined and so must be given its ordinary meaning. In our view, this means you have the power, from day-to-day, to decide how the property is managed. You can delegate actual management so long as you still have day-to-day control over it.[6]’

The distancing of control over a real asset, even though owned by the investor, may put him in the position of a financial investor. This is a classic test used by US courts, in a test called Howey Test, coming from a 1946 ruling in SEC vs. Howey[7]. If an investment opportunity is open to many people, and if investors have little to no control or management of investment money or assets, then that investment is probably a security. If, on the other hand, an investment is made available only to a few close friends or associates, and if these investors have significant influence over how the investment is managed, then it is probably not a security.

The financial world and the real world

As is apparent, the definition in sec. 235 of the UK legislation has inspired the draft of the Indian law. It is intriguing to seek as to how the collective ownership or management of real properties has come within the sweep of the law. Evidently, CIS regulation is a part of regulation of financial services, whereas collective ownership or management of real assets is a part of the real world. There are myriad situations in real life where collective business pursuits, or collective ownership or management of properties is done. A condominium is one of the commonest examples of shared residential space and services. People join together to own land, or build houses. In the good old traditional world, one would have expected people to come together based on some sort of “relationship” – families, friends, communities, joint venturers, or so on. In the interweb world, these relationships may be between people who are invisibly connected by technology. So the issue, why would a collective ownership or management of real assets be regarded as a financial instrument, to attract what is admittedly a piece of financial law.

The origins of this lie in a 1984 Report[8] and a 1985 White Paper[9], by Prof LCB Gower, which eventually led to the enactment of the 1986 UK Financial Markets law. Gower has discussed the background as to why contracts for real assets may, in certain circumstances, be regarded as financial contracts. According to Gower, all forms of investment should be regulated “other than those in physical objects over which the investor will have exclusive control. That is to say, if there was investment in physical objects over which the investor had no exclusive control, it would be in the nature of an investment, and hence, ought to be regulated. However, the basis of regulating investment in real assets is the resemblance the same has with a financial instrument, as noted by UK Supreme Court in the Asset Land ruling: “..the draftsman resolved to deal with the regulation of collective investment schemes comprising physical assets as part of the broader system of statutory regulation governing unit trusts and open-ended investment companies, which they largely resembled.”

The wide sweep of the regulatory definition is obviously intended so as not to leave gaps open for hucksters to make the most. However, as the UK Supreme Court in Asset Land remarked: “The consequences of operating a collective investment scheme without authority are sufficiently grave to warrant a cautious approach to the construction of the extraordinarily vague concepts deployed in section 235.”

The intent of CIS regulation is to capture such real property ownership devices which are the functional equivalents of alternative investment funds or mutual funds. In essence, the scheme should be operating as a pooling of money, rather than pooling of physical assets. The following remarks in UK Asset Land ruling aptly capture the intent of CIS regulation: “The fundamental distinction which underlies the whole of section 235 is between (i) cases where the investor retains entire control of the property and simply employs the services of an investment professional (who may or may not be the person from whom he acquired it) to enhance value; and (ii) cases where he and other investors surrender control over their property to the operator of a scheme so that it can be either pooled or managed in common, in return for a share of the profits generated by the collective fund.”

Conclusion

While the intent and purport of CIS regulation world over is quite clear, but the provisions have been described as “extraordinarily vague”. In the shared economy, there are numerous examples of ownership of property being given up for the right of enjoyment. As long as the intent is to enjoy the usufructs of a real property, there is evidently a pooling of resources, but the pooling is not to generate financial returns, but real returns. If the intent is not to create a functional equivalent of an investment fund, normally lure of a financial rate of return, the transaction should not be construed as a collective investment scheme.

[1] Vishes Kothari: Property Share Business Models in India, https://vinodkothari.com/blog/property-share-business-models-in-india/

[2] Nidhi Jain, Collective Investment Schemes for Real Estate Investments in India, at https://vinodkothari.com/blog/collective-investment-schemes-for-real-estate-investment-by-nidhi-jain/

[3] Vinod Kothari and Nidhi Jain article at: https://www.moneylife.in/article/collective-investment-schemes-how-gullible-investors-continue-to-lose-money/18018.html

[4] http://www.bailii.org/ew/cases/EWCA/Civ/2015/284.html

[5] https://www.supremecourt.uk/cases/docs/uksc-2014-0150-judgment.pdf

[6] https://www.handbook.fca.org.uk/handbook/PERG/11/2.html

[7] 328 U.S. 293 (1946), at https://supreme.justia.com/cases/federal/us/328/293/

[8] Review of Investor Protection, Part I, Cmnd 9215 (1984)

[9] Financial Services in the United Kingdom: A New Framework for Investor Protection (Cmnd 9432) 1985

Our Other Related Articles

Property Share Business Models in India,< https://vinodkothari.com/blog/property-share-business-models-in-india/>

Collective Investments Schemes: How gullible investors continue to lose money < https://www.moneylife.in/article/collective-investment-schemes-how-gullible-investors-continue-to-lose-money/18018.html>

Collective Investment Schemes for Real Estate Investments in India, < https://vinodkothari.com/blog/collective-investment-schemes-for-real-estate-investment-by-nidhi-jain/>

2020 – Year of changes for AIFs

Timothy Lopes – Senior Executive CS Harshil Matalia – Assistant Manager

The year 2020 – ‘Year of pandemic’, rather we can say the year of astonishing events for everyone over the globe. Without any doubt, this year has also been a roller coaster ride for Alternative Investment Funds (‘AIFs’) with several changes in the regulatory framework governing AIFs in India.

Recent Regulatory Changes for AIFs

In continuation to the stream of changes, Securities Exchange Board of India (‘SEBI’), in its board meeting dated September 29, 2020, has approved certain amendments to the SEBI (Alternative Investment Funds) Regulations, 2012 (‘AIF Regulations’). The said amendments have been notified by the SEBI vide notification dated October 19, 2020. The following article throws some light on SEBI (AIFs) Amendment Regulations, 2020 (‘Amendment Regulations’) and tries to analyse its impact on AIFs.

Clarification on Eligibility Criteria

Regulation 4 of AIF Regulations prescribes eligibility criteria for obtaining registration as AIF with SEBI. Prior to the amendment, Regulation 4(g), provided as follows:

“4 (g) the key investment team of the Manager of Alternative Investment Fund has adequate experience, with at least one key personnel having not less than five years experience in advising or managing pools of capital or in fund or asset or wealth or portfolio management or in the business of buying, selling and dealing of securities or other financial assets and has relevant professional qualification;”

The amended provision to 4 (g) extends the meaning of relevant professional qualification, the effect of which seems to add more qualitative criteria to the management team of the AIF, to be evaluated at the time of grant of certification. The newly amended section 4(g) of the AIF Regulations reads as follow:

“(g) The key investment team of the Manager of Alternative Investment Fund has –

- adequate experience, with at least one key personnel having not less than five years of experience in advising or managing pools of capital or in fund or asset or wealth or portfolio management or in the business of buying, selling and dealing of securities or other financial assets; and

- at least one key personnel with professional qualification in finance, accountancy, business management, commerce, economics, capital market or banking from a university or an institution recognized by the Central Government or any State Government or a foreign university, or a CFA charter from the CFA institute or any other qualification as may be specified by the Board:

Provided that the requirements of experience and professional qualification as specified in regulation 4(g)(i) and 4(g)(ii) may also be fulfilled by the same key personnel.”

It is apparent from the prima facie comparison of language that the key investment team of the Manager may have one key person with five years of experience (quantitative) as well as a personnel holding professional qualification (qualitative) from institutions recognised under the regulation. Further, clarity has been appended in form of proviso to the section that quantitative and qualitative requirements could be met by either one person, or it could be achieved collectively by more than one person in the fund.

With this elaboration, SEBI has harmonized the qualification requirements as that with the requirement specified for other intermediaries such as Investment Advisers, Research Analysts etc. in their respective regulations. Detailed prescription on degrees and qualifications for AIF registration by SEBI is a conferring move and is expected to aid as a clear pre-requisite on expectations of SEBI from prospective applications for registration of the fund.

Formation of Investment Committee

Regulation 20 of AIF Regulations specifies general obligations of AIFs. Erstwhile, the responsibility of making investment decisions was upon the manager of AIFs. It has been noticed by the SEBI from the disclosures made in draft Private Placement Memorandums (‘PPMs’) filed by AIFs for launch of new schemes, that generally Managers prefer to constitute an Investment Committee to be involved in the process of taking investment decisions for the AIF. However, there was no corresponding obligation in the AIF Regulations explicitly recognizing the ‘Investment Committee’ to take investment decisions for AIFs. Such Investment Committees may comprise of internal or external members such as employees/directors/partners of the Manager, nominees of the Sponsor, employees of Group Companies of the Sponsor/ Manager, domain experts, investors or their nominees etc.

These amendments are based on the recommendations to SEBI to recognize the practice followed by AIFs to delegate decision making to the Investment Committee.[1] The rationale behind amendments to AIF Regulations is based on the following merits as proposed in the recommendations::

- Presence of investors or Sponsors or their nominees in an Investment Committee which may serve to improve the due diligence carried out by the Manager, as they are stakeholders in the AIF’s investments.

- Presence of functional resources from affiliate/group companies of the Manager (legal advisor, compliance advisor, financial advisor etc.) in the Investment Committee may be useful to ensure compliance with all applicable laws.

- Presence of domain experts in the committee may provide comfort to the investors regarding suitability of the investment decisions, as the investment team of the Manager may not have domain expertise in all industries/ sectors where the fund proposes to invest.

Thus, the insertion was made, giving the option to the Manager to constitute an investment committee subject to the following conditions laid down in the newly inserted sub-regulation, i.e. Regulation 20(6) of the AIF Regulations given below –

- The members of the Investment Committee shall be equally responsible as the Manager for investment decisions of the AIF.

- The Manager and members of the Investment Committee shall jointly and severally ensure that the investments of the AIF comply with the provisions of AIF Regulations, the terms of the placement memorandum, agreement made with the investor, any other fund documents and any other applicable law.

- External members whose names are not disclosed in the placement memorandum or agreement made with the investor or any other fund documents at the time of on-boarding investors shall be appointed to the Investment Committee only with the consent of at least seventy five percent of the investors by value of their investment in the Alternative Investment Fund or scheme.

- Any other conditions as specified by the SEBI from time to time.

The constitution of investment committee is a global standard practice followed by the Funds. However, funds structure in India might be altered with the new defining role of investment committee under the AIF Regulations. The investment committee generally comprises of nominees of large investors in the fund and at times other external independent professional bodies that act as a consenting body towards prospective deals of the fund. The amendment will alter the role of investors holding positions at investment committee as the new defining role might deter them from taking underlying obligations. From the funds perspective seeking external independent professionals might get costly as there is an obligation introduced by way of this amendment regulation. Further, it casts an onus on the investment committee to be involved in day to day functioning of the fund, which used to be otherwise (where members were usually involved in mere finalising the deals). Lateral entry of the members to investment committee post placement of memorandum with the consent of investors is aimed at greater transparency in funds functioning.

Test for indirect foreign investment by an AIF

As per Clause 4 of Schedule VIII of FEMA (Non-Debt Instrument) Rules, 2019 (‘NDI Rules’) any investment made by an Investment Vehicle into an Indian entity shall be reckoned as indirect foreign investment for the investee Indian entity if the Sponsor or the Manager or the Investment Manager –

(i) is not owned and not controlled by resident Indian citizens or;

(ii) is owned or controlled by persons resident outside India.

Therefore, in order to determine whether the investment made by AIFs in Indian entity is indirect foreign investment, it is essential to identify the nature of the Manager/Sponsor/investment manager, whether he is owned or controlled by a resident Indian citizen or person resident outside India.

RBI in its reply to SEBI’s query on downstream investment had clarified that since investment decisions of an AIF are taken by its Manager or Sponsor, the downstream investment guidelines for AIFs were focused on ownership and control of Manager or Sponsor. Thus, if the Manager or Sponsor is owned or controlled by a non-resident Indian citizen or by person resident outside India then investment made by such AIF shall be considered as indirect foreign investment.

Whether an investment decision made by the Investment Committee of AIF consisting of external members who are not Indian resident citizens would amount to indirect foreign investment?

In light of the above provisions of the NDI Rules and with the introduction of the concept of an “Investment Committee”, SEBI has sought clarification from the Government and RBI vide its letter dated September 07, 2020[2].

Conclusion

With the enhancement in eligibility criteria, SEBI has ensured that the investment management team of the AIF would have relevant expertise and required skill sets.

Further, giving recognition to the concept of an investment committee will cast an obligation on investment committee fiduciary like obligations towards all the investors in the fund. . However, there exists certain ambiguity under the NDI Rules, for applications wherein external members of investment committee who are not ‘resident Indian citizens’, which is currently on hold and pending receipt of clarification.

[1] https://www.sebi.gov.in/sebi_data/meetingfiles/oct-2020/1602830063415_1.pdf

[2] https://www.sebi.gov.in/sebiweb/about/AboutAction.do?doBoardMeeting=yes

SEBI introduces enhanced disclosure and standardized reporting for AIFs

Timothy Lopes, Executive, Vinod Kothari Consultants Pvt. Ltd.

SEBI has vide circular dated 5th February, 2020[1] introduced a standard Private Placement Memorandum (PPM) and mandatory performance bench-marking for Alternative Investment Funds (AIF). The move is part of SEBI’s initiative to streamline disclosure standards in the growing AIF space. The changes are made based on the recommendations of the SEBI Consultation Paper[2] on ‘Introduction of Performance Bench-marking’ and ‘Standardization of Private Placement Memorandum for AIFs’.

Template for Private Placement Memorandum (PPM)

The SEBI (AIF) Regulations, 2012 specified broad areas of disclosures required to be made in the PPM. This led to a significant variation in the manner in which various clauses, explanations and illustrations are incorporated in the PPMs. Hence, this led to concerns that the investors receive a PPM which provides information in a manner which is too complex to easily comprehend or with too little information on important aspects of the AIF, e.g. potential conflicts of interests, risk factors specific to AIF or its investment strategy, etc.

Thus, SEBI has mandated a template[3] for the PPM providing certain minimum level of information in a simple and comparable format. The template for PPM consists of two parts –

Part A – Section for minimum disclosures, which includes the following –

- Executive Summary –

This lays down the summary of the parties and terms of the transaction. In effect, it is a summary term sheet of the PPM, laying down essential features of the transaction.

- Market opportunity / Indian Economy / Industry Outlook;

The theme of this section includes a general economic background followed by investment outlook and sector/ industry outlook. This section may include any additional information as well which may be relevant. An illustrative list of additional items which may be included has been specified in the template.

- Investment Objective, Strategy and Process;

A tabular representation of the investment areas and strategy to be employed is laid down in under this head. Further, a flow chart depicting the investment decision making process and detailed description of the same is required to be specified. This will give investors a comprehensive idea of the ultimate investment objective and strategy.

- Fund/Scheme Structure;

A diagrammatic structure of the Fund/ Scheme which discloses all the key constituents and a brief description of the activities of the Fund/ Scheme.

The diagrammatic representation shall specify, for instance, the sponsor, trustee, manager, custodian, investment advisor, offshore feeder, etc.

- Governance Structure;

To enhance the governance disclosures to investors and ensure transparency this section mandates disclosures of all details of each person involved in the Fund/ Scheme structure, including details about the investment team, advisory committees, operating partners, etc.

- Track Record of the Manager;

The track record of the Fund Manager is of great significance since investors would like to know the skill, experience and competence of the Manager before making an investment.

The template mandates disclosures about the manager including explicit disclosure of whether he is a first time manager or experienced manager.

- Principal terms of the Fund/ Scheme;

Explicit disclosures about the principal terms such as minimum investment commitment, size of the scheme, target investors, expenses, fees and other charges, etc. are required to be disclosed as per the template.

Major terms and disclosures are covered under this section.

- Principles of Portfolio Valuation;

This section would broadly lay down the principles that will be used by the Manager for valuation of the portfolio company.

The investors would get a fair idea of the manner in which valuation of the portfolio would be undertaken, in this section.

- Conflicts of interest;

All present and potential conflicts of interests that the manager would envisage during the operation of the Fund/ Scheme at various levels are to be disclosed under this section.

This would enable investors to factor in the conflicts of interests existing or which may arise in the future of the fund and make an informed decision.

- Risk Factors;

All risk factors that investors should take into account such as specific risks of the portfolio investment or the fund structure are required to be disclosed in the PPM.

These risks would include operational risks, tax risks, regulatory risks, etc. among other risk factors.

- Legal, Regulatory, and Tax Consideration;

This section shall include standard language for legal, regulatory and tax considerations as applicable to the Fund/Scheme, including the SEBI (AIF) Regulations, 2012, Takeover Regulations, Insider Trading Regulations, Anti-Money Laundering, Companies Act, 2013. Taxation aspects of the fund are also to be disclosed.

- Illustration of fees, expenses and other charges;

A tabular representation of the fees and other charges along with the expenses of the Fund are required to be disclosed for transparency of investors and no hidden charges.

- Distribution Waterfall;

The payment waterfall to different classes of investors is required to be disclosed in detail.

- Disciplinary History.

Any prior disciplinary action taken against the sponsor, manager, etc. will be required to be disclosed for better informed decision making of investors.

Part B – Supplementary section to allow full flexibility to the Fund in order to provide any additional information, which it deems fit.

The template requires enhanced disclosures mandatorily required to be made by the AIF, such as risk factors, investment strategy, conflicts of interest and several other areas that may affect the interest of the investors of AIFs.

This will standardize disclosures across the AIF space and increase simplicity of information to investors in a standard reporting format. Enhancing disclosure requirements will increase investor understanding about AIF schemes.

Further there is a mandatory requirement to carry out an annual audit of the compliance of the PPM by either an internal or external auditor/ legal professional. The findings arising out of the audit are required to be communicated to the Trustee or Board or Designated Partners of the AI, Board of the Manager and SEBI.

Exemption has been provided from the above PPM and audit requirements to the following classes of funds:

- Angel Funds as defined in SEBI (Alternative Investment Funds), Regulations 2012.

- AIFs/Schemes in which each investor commits to a minimum capital contribution of Rs. 70 crores (USD 10 million or equivalent, in case of capital commitment in non-INR currency) and also provides a waiver to the fund from the requirement of PPM in the SEBI prescribed template and annual audit of terms of PPM, in the manner provided at Annexure 3 of the SEBI Circular.

These requirements are however applicable from 01st March, 2020.

Bench-marking for disclosure of performance

Considering that investments by AIFs have grown at a rate of 75% year on year in the past two years, a need was felt to introduce disclosures by AIFs indicating returns on their investments. Prior to the SEBI circular there was no disclosure requirement for AIFs on their investment performance.

There was no bench-marking of returns disclosed by AIFs to their prospective or existing investors. However, returns generated on investment is one of the most important factors taken into consideration by potential investors and is also important for existing investors in order to be informed about the performance of their investment in comparison to a benchmark.

Therefore, it is felt that there is a need to provide a framework to bench-marking the performance of AIFs to be available for the investors and to minimize potential misselling.

In this regard SEBI has introduced the following –

- Mandatory bench-marking of the performance of AIFs (including Venture Capital Funds) and the AIF industry.

- A framework for facilitating the use of data collected by Bench-marking Agencies to provide customized performance reports.

The new bench-marking framework prescribes that each AIF must enter into an agreement with a Bench-marking Agency (notified by an AIF association representing at least 51% of the number of AIFs) for carrying out the bench-marking process.

The agreement between the Bench-marking Agencies and AIFs shall cover the mode and manner of data reporting, specific data that needs to be reported, terms including confidentiality in the manner in which the data received by the Bench-marking Agencies may be used, etc.

Reporting to the Bench marking Agency –

AIFs are required to report all the necessary information including scheme-wise valuation and cash flow data to the Bench-marking Agencies in a timely manner for all schemes which have completed at least one year from the date of ‘First Close’. The form and format of reporting shall be mutually decided by the Association and the Benchmarking Agencies.

If an applicant claims a track-record on the basis of India performance of funds incorporated overseas, it shall also provide the data of the investments of the said funds in Indian companies to the Benchmarking Agencies, when they seek registration as AIF.

PPM and Marketing material –

In case past performance of the AIF is mentioned in the PPM or any marketing material the performance versus benchmark report provided by the benchmarking agencies for such AIF/Scheme is also required to be provided.

Operational Guidelines for the benchmarking criteria is placed in Annexure 4 to the SEBI Circular.

Further there is an exemption from the above requirements to Angel Funds registered under sub-category of Venture Capital Fund under Category-1 AIF.

Conclusion

These changes are likely to bring about higher disclosure and transparency in the AIF space, especially for existing as well as potential investors of AIFs. Standardization of PPM will eliminate any variance from the manner of disclosures made by various AIFs.

Links to related write ups –

https://vinodkothari.com/2018/03/can-aif-grant-loans/

https://vinodkothari.com/aifart/

[1] https://www.sebi.gov.in/legal/circulars/feb-2020/disclosure-standards-for-alternative-investment-funds-aifs-_45919.html

[2] https://www.sebi.gov.in/reports-and-statistics/reports/dec-2019/consultation-paper-on-introduction-of-performance-benchmarking-and-standardization-of-private-placement-memorandum-for-alternative-investment-funds_45215.html

[3] https://www.sebi.gov.in/sebi_data/commondocs/feb-2020/an_1_p.pdf