FAQs on mandatory demat of securities by private companies

You may refer to our other FAQs on dematerialization of shares here and you may also refer to our Snippet, detailed article and YouTube Video

You may refer to our other FAQs on dematerialization of shares here and you may also refer to our Snippet, detailed article and YouTube Video

– Team Vinod Kothari and Company | corplaw@vinodkothari.com

Our Resource Centre on Related Party Transactions can be viewed here

Changes proposed in manner of RP identification, threshold for significant RPTs

– Avinash Shetty, Manager and Sourish Kundu, Executive | corplaw@vinodkothari.com

Related Party Transactions (“RPTs”) have been one such evergreen and ever-evolving aspect of corporate governance that has been put to guardrails on a frequent basis. SEBI, in its Consultation Paper dated 7th February, 2025 has again rolled out a new set of proposals, this time primarily centered around RPTs undertaken by subsidiaries of a listed entity, but nevertheless leaving listed entities pondering on what their actionables might be. In this article, we have analysed the proposals in brief.

Proposal: Following SEBI’s Informal Guidance on the manner of identification of Related Parties (“RPs”), which opined that the subsidiaries of LEs should maintain a list of their RPs in accordance with the Listing Regulations, instead of maintaining the same as per their respective applicable/local laws, SEBI now proposed to effectuate the same by way of appending an explanation to Reg. 2(1)(zc) that RP of subsidiary to be identified as per Reg. 2(1)(zb) of the Listing Regulations.

Although the proposed insertion does not differentiate between a listed and an unlisted subsidiary, it is clearly understood that a listed subsidiary shall, by default, be following the holistically covered definition of RP given under Reg. 2(1)(zb). On the other hand, an unlisted subsidiary which may so far been following the definition of RP as given under the Companies Act, 2013 (“the Act”) might be expected to buckle up to bring in a lot more persons under the purview of the RPT regime as per the LODR definition – for the purpose of facilitating the parent’s RPT compliances.

Possible concerns: While the SEBI’s approach of applying an entity-agnostic definition may seem to bring consistency and ease of collation of information across the group, but may raise several issues:

The issues in putting the said proposal in action have been discussed in detail in our write up on SEBI’s IG on RP identification by unlisted subsidiaries.

Actionables: If the proposals take the shape of law, the following actionables might arise:

Proposal: Moving on to thresholds for significant RPTs – an RPT of the subsidiary to which the holding LE is not a party requires prior approval of the AC of the holding LE before it can be entered into, if the value of such RPT exceeds 10% of annual standalone turnover, as per the latest audited financial statements of the subsidiary, taken together with all transactions during a FY. [Pursuant to Regulation 23(2)(c) of the Listing Regulations] (hereafter referred to as “significant RPTs”)

However, as discussed in the CP, there may be cases where a transaction by a subsidiary of a LE exceeds the material RPT threshold, requiring shareholder approval, but does not exceed 10% of the subsidiary’s standalone turnover, thus bypassing the AC approval. For example, if a subsidiary has a standalone turnover of ₹12,000 crore, a transaction of ₹1,100 crore would cross the material RPT threshold of ₹1,000 crore . This would require shareholder approval. However, since ₹1,100 crore is below 10% of the subsidiary’s standalone turnover (₹1,200 crore), AC’s approval would not be needed.

The proposal seeks to include the absolute threshold of Rs. 1,000 crores as well in determining significant RPTs. Significance would be determined on the basis of value of transaction being Rs. 1,000 crores or 10% of annual standalone turnover of the subsidiary, whichever is lower. In our view, however, this proposal is more clarificatory in nature as it is difficult to envisage that any RPT proposal going to shareholders of an LE can go directly without coming before the AC of the LE. We have covered this scenario in our FAQs on RPT as well.

A specific carve out from the above requirement has been set down in respect of listed subsidiaries on which corporate governance norms and RPT framework norms are applicable.

Further, in order to impose RPT controls on SME listed entities, SEBI in its Board Meeting held on 18th December, 2024 approved, among other items, the materiality threshold of Rs. 50 crores or 10% of annual consolidated turnover, whichever is lower. Accordingly, for the purpose of determining significant RPTs of an unlisted subsidiary of SME LE, the threshold is Rs. 50 crores or 10% of annual consolidated turnover, whichever is lower. Note that the provision is applicable to a subsidiary of an SME LE – this is clear from para 5.3.1 of the CP.

The proposal as to thresholds is as tabulated below:

| Limits for Significant RPTs (whichever is lower) | Having financial track record* | Not having financial track record* |

| Subsidiaries of Main Board LEs | Rs. 1,000 crores or 10% of annual standalone turnover | Rs. 1,000 crores or 10% of standalone net worth |

| Subsidiaries of SME LEs | Rs. 50 crores or 10% of annual standalone turnover | Rs. 50 crores or 10% of standalone net worth |

*Note:

Actionables: Unlisted subsidiaries of listed entities will have to reassess their transactions falling under significant RPTs to be taken to the listed parent’s AC.

Although the change is merely clarificatory in nature, it is pertinent to note that there has been some ambiguity for RPT approvals, when RPTs are being entered into between a holding company and its wholly owned subsidiary (WoS). Given that applicability of the Listing Regulations encompasses only listed entities, it was implied that the holding company referred is a listed holding company whose accounts are consolidated and presented to shareholders at the general meeting, and not an unlisted one.

This interpretive addition of the word “listed” aims to remove any ambiguity in respect of the exemptions granted for certain RPTs involving WoS.

The impact of the changes, if and when notified, may be expected to be as far fetched and require a revised understanding of the RPT regime to some extent, even if not entirely, similar to the rippling effect of the SEBI (LODR) (3rd Amendment) Regulations, 2024 dated 12th December, 2024. Further, there are certain aspects such as revision in definition of RPs for subsidiaries, which would require an introspection not just on the part of the subsidiaries of LEs, but at the group level as well. Needless to say, RPT – regime and controls, has always been a trending topic and changes w.r.t the same, although the first of this year, can definitely not be expected to be the last.

The RPT framework under the Listing Regulations has already been amended 7 times, and every time, it becomes tougher, all in the name of “Ease of Doing Business”. A document collating the evolution of RPT framework over the years is here: https://lnkd.in/gZ3Ca5yQ

Read more on Related Party Transactions here.

– Sourish Kundu, Executive | corplaw@vinodkothari.com

Read More:

Subsidiaries to refer LODR definition of “related party” – going too far with relationships?

– Resolution Team, Vinod Kothari and Company | resolution@vinodkothari.com

Read More:

Group Insolvency: Relevance of Substantive Consolidation in Indian Context

Interim Finance becomes effective and attractive

Discussion on IBBI Discussion Paper dated 4th February, 2025

-Abhirup Ghosh (abhirup@vinodkothari.com)

Partial Credit Enhancement (PCE) is a risk-mitigating financial tool where a third party provides limited financial backing to improve the creditworthiness of a debt instrument. It ensures that investors are partially protected against default risk, making it easier for issuers to raise funds at better terms.

The key features of a PCE are as follows:

The concept of PCE has been in India for quite some time now, and is commonly used in securitisation transactions. However, the Finance Minister’s announcement during Union Budget 2025 about setting up of a PCE facility under the National Bank for Financing Infrastructure Development (NaBFID) has brought this into the limelight.

Infrastructure development is the backbone of economic growth, but funding large-scale projects such as highways, railways, power plants, and airports requires substantial capital. Infrastructure projects often face challenges in raising funds due to their long gestation periods, high risks, and lower credit ratings. PCE serves as an effective financial tool to improve the creditworthiness of infrastructure bonds, making them more attractive to investors. By providing a partial guarantee or security, PCE helps reduce the cost of borrowing and widens investor participation, ultimately facilitating infrastructure financing.

Infrastructure bond issuances face several obstacles that make fundraising difficult. One of the primary challenges is low credit ratings. Infrastructure projects, especially those in their early stages, often receive sub-investment-grade ratings (such as BBB or lower), making them unattractive to investors. Additionally, these projects are subject to high perceived risks, including revenue uncertainty, regulatory hurdles, construction delays, and cost overruns. Since many infrastructure projects rely on user charges, such as tolls or metro fares, their cash flow projections can be unpredictable.

Another major issue is the long maturity period of infrastructure bonds. Most investors prefer short- to medium-term investments, whereas infrastructure bonds typically have tenures of 10 to 30 years. This mismatch reduces the appetite for such bonds in the market. Lastly, lack of institutional investor participation further limits the success of infrastructure bond issuances, as pension funds, insurance companies, and mutual funds prefer highly rated bonds with stable returns.

One of the most significant ways PCE helps infrastructure bond issuances is by improving their credit ratings. When a bank or financial institution provides partial credit enhancement in the form of a guarantee or reserve fund, it reduces the default risk associated with the bond. This leads to a higher credit rating, making the bond more attractive to investors. For example, an infrastructure company with a BBB-rated bond issuance may improve its rating to A with a 20% PCE support, or AA with a 50% PCE support thereby increasing demand from investors. A higher rating not only boosts investor confidence but also expands the pool of potential buyers, including institutional investors such as pension funds and insurance companies.

By improving the credit rating of infrastructure bonds, PCE directly leads to a reduction in interest costs. Bonds with higher ratings attract lower interest rates, which helps infrastructure companies secure financing at more affordable terms. For instance, without PCE, a BBB-rated bond may require 12%, whereas a bond upgraded to an AA rating with PCE support may only require 9%. This reduction in interest rates can result in significant savings over the life of the bond. Lower borrowing costs also make infrastructure projects more financially viable, ensuring their timely execution and long-term sustainability.

Institutional investors, such as mutual funds, pension funds, and insurance companies, typically have strict investment guidelines that restrict them from investing in low-rated securities. Since many of these investors require bonds to be rated AA or higher, infrastructure bonds often struggle to meet these requirements. PCE helps bridge this gap by enhancing the credit rating, making infrastructure bonds eligible for investment by these large institutional players. This leads to greater liquidity and stability in the corporate bond market, ensuring a steady flow of capital to infrastructure projects.

PCE contributes to the overall development of the corporate bond market by encouraging more issuers to raise funds through bonds rather than relying solely on bank loans. Traditionally, infrastructure financing in India has been dependent on banks, which exposes them to high asset-liability mismatches due to the long tenure of infrastructure projects. By facilitating infrastructure bond issuances, PCE helps shift the burden away from banks and towards a broader investor base. This not only diversifies funding sources but also enhances financial stability in the banking sector.

As per a CII report (2022), the infrastructure financing gap is estimated at over 5% of GDP. Approx. 80% of the investment in infrastructure space is by government agencies (80%), and the remaining 20% comes from private developers.

As per the National Infrastructure Pipelines, the total investment target was set at INR 111 trillion (USD 1.34 trillion) for the period between FY 20 and FY 25; and only 6-8% (INR 6.66-8.88) of the such targets were expected to be met by bond issuances. Reliance on bond markets is planned to the extent of 6% to 8% (INR 6.66 – 8.88 trillion). As per the said estimates, the average annual issuances should have been INR 1.480 trillion. However, between FY18 and FY22, the issuance of infrastructure bonds has been at INR 5.37 trillion, that is, an average of INR 1.07 trillion per annum, that is a shortfall of ~30% compared to the target.

Furthermore, the issuances have been highly concentrated in the top 5 PSUs. The charts below show the annual bond issuances between FY 18 – FY 22, and share of issuance by top 5 PSUs and others:

Source: CRISIL

The market is dominated by highly rated issuers. In general approx. 75% of bond issuers are rated AAA, and more than 90% of the issuances are by AA and above rated entities. The reason for this dominance by highly rated issuers is the fact that for practical purposes, the most acceptable rating in the infra bonds space is AA, as long term investors like insurance companies, pension funds etc. are by regulation required to invest in AA or above rated papers.

PCE support from a credible source will help a lot of infrastructure operators, who are stopped at the gate, with ratings in the range of A, with easy access to the market.

The existing scheme for PCE was notified by the RBI in 2015. In a nutshell, the scheme provides for the following:

Form of PCE: To be structured as a non-funded, irrevocable contingent line of credit. This facility can be drawn upon in the event of cash flow shortfalls affecting bond servicing.

Limitations: The total PCE extended by a single bank cannot exceed 20% of the bond’s total size; however, overall, the PCE provided by all banks, in aggregate, cannot exceed 50% of the bond’s total size.

Further, PCE can be provided only to bonds which have a pre-enhanced rating of BBB- or above.

Capital Requirements: The bank providing PCE does not hold capital based only on its PCE amount. Instead, it calculates the capital based on the difference between:

The objective is to ensure that the PCE provider should absorb the risks that it covers in the entire transaction. Illustrating with an example:

Assume that the total bond size is Rs. 100 crores for which PCE to the extent of Rs. 20 crore is provided by a bank. The pre-enhanced rating of the bond is BBB which gets enhanced to AA with the PCE. In this scenario:

As can be seen, the capital has to be maintained on the total bond issuance, and not just the exposure. Ironically, this capital has to be maintained until the outstanding principal of bonds falls below the extent of PCE provided. Usually, the bonds are amortising in nature – that is, the actual exposure of the guarantor continues to come down. Given, however, that default in bonds may be back-ended, the capital has still to be maintained till the redemption of the bonds. This requires the PCE provider to maintain huge regulatory capital for a significantly long period of time; which also gets reflected in the ultimate cost to the beneficiary, therefore, making it unviable.

The FM’s announcement though comes with a lot of promise, as it shows a positive intent. But to make things work, there are quite a few things that should be put into place:

Read more on RPTs here.

Harshita Malik and Anshika Agarwal (finserv@vinodkothari.com)

-Subhojit Shome (subhojit@vinodkothari.com)

The tokenisation of real-world assets (RWA) using cryptographic technology is rapidly emerging as a transformative innovation in the financial ecosystem. Note here that the term RWA refers to all traditional assets including both real assets as well as traditional financial assets that exist in the physical world. By leveraging blockchain technology, tokenisation enables the representation of tangible assets, such as real estate, commodities, and artwork, or intangible assets like intellectual property, as digital tokens on a distributed ledger. This development is reshaping the way assets are managed, traded, and accessed, creating new opportunities and challenges.

RWA tokenisation has garnered attention due to several converging factors. Blockchain technology offers a streamlined alternative to traditional systems by reducing intermediaries, lowering transaction costs, and ensuring faster settlement times. Fractional ownership of high-value assets makes them accessible to a broader range of investors, enhancing market liquidity. Blockchain’s immutable nature provides a transparent record of transactions and ownership, reducing fraud and enhancing trust. Additionally, tokenised assets are borderless, enabling seamless cross-border trading and investment opportunities.

According to market reports, the capital locked in tokenised RWA is expected to touch $50 billion by the end of 2025 surpassing all previous records. In 2024, the ecosystem had achieved a 32% annual growth rate.

In this article, we look at the impetus behind this technology, its status of adoption in India and critical issues that act as roadblocks in its development.

The tokenisation market has witnessed significant advancements in a number of areas. Real estate tokenisation has enabled properties to be tokenised for fractional ownership, reducing entry barriers for smaller investors. Similarly, commodities like gold and other precious metals have been tokenised, providing an efficient means of trading and ownership. High-value artworks and collectibles are being tokenised to allow multiple investors to own shares in masterpieces. Tokenisation has also extended into private equity and debt markets, enabling innovative funding mechanisms and the development of secondary market opportunities. Moreover, the emergence of regulated tokenisation platforms in certain developed economies (e.g. the UK) underscores the growing maturity of this market.

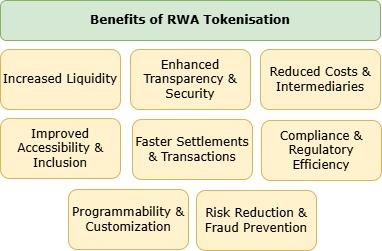

Figure 1: Benefits of Tokenisation of Real-World Assets using Blockchain

Fractional ownership creates liquidity in traditionally illiquid assets. It also democratises investment by enabling wider participation through reduced minimum investment thresholds. Here the emphasis is not on reduction of any regulatory investment threshold but rather, being represented in the digital world, RWA tokenisation allows infinitesimally fractional parts of an asset to be bought and sold. Cost efficiency is achieved by reducing reliance on intermediaries, which lowers transaction and administrative costs. Blockchain’s transparency increases trust and reduces fraud risks. Furthermore, smart contracts enable automation of compliance, dividend distribution, and other processes.

The process of RWA tokenisation broadly involves the following steps –

Figure 2: Process of RWA tokenisation

In the tokenisation process one may note that the custody of the underlying asset is separated from the ownership of the asset. While the ownership is represented by use of tokens, the underlying asset may need to be held with a custodian ‘off-chain’ (i.e. in the physical world).

However, tokenisation is not without challenges. Regulatory uncertainty remains a significant hurdle due to inconsistent global regulatory frameworks. Technology risks, such as cybersecurity concerns and vulnerabilities in smart contracts, could undermine trust. Market volatility is another concern, as tokens may experience higher price fluctuations compared to their underlying assets. Some tokenised assets may face illiquidity risks if the secondary markets lack sufficient depth. Additionally, legal ambiguity regarding ownership rights and the enforceability of tokenised claims persists in many jurisdictions.

Several key regulatory considerations must be addressed. Asset classification is crucial for defining whether tokenised assets are securities, commodities, payment instruments or another category altogether.

In India, regulatory uncertainty remains the key issue in the implementation of RWA tokenisation. Say, for instance, there is tokenisation of real estate in which the management of the property is overseen by the issuer or by a manager appointed by such issuer and fractional ownership units are offered for sale to retail investors. Such a transaction starts to take on the colour of a collective investment scheme and SEBI may intervene and mandate the issuer to register as such with the regulator. In the case of real estate these schemes can also be viewed as having a structure akin to a REIT especially SM REIT.

The SEBI is yet to notify any regulatory prescription specifically for the purposes of regulating crypto-assets and or token offerings to the retail public and it has been reported in the press1 that the securities market regulator has informed the Parliamentary Standing Committee on Finance that regulation of crypto-assets would be difficult given the nature of technology that sustains them. In the matter of, An RTI enquiry, as referenced in the matter of Appeal No. 4532 of 2021 filed by Rohith Methayil Rajagopal, was raised with the SEBI’s CPIO as to the stand of Regulator with regard to “digital trading and possession of Cryptocurrencies by the Indian Citizens” and if SEBI had any “legal document and its date that permits digital trading of Bitcoin / Cryptocurrencies in India”. The response of the CPIO, as affirmed by the appellate authority, was that it did not have the knowledge of either matter. Based on this one can conclude that the Regulator has not, yet, formalised its stance over dealings in crypto assets. Recently, however, the Regulator has expressed an openness to a multi-regulator based oversight framework for crypto-assets.2

There have been interest shown by mutual fund houses to invest in ETFs or indices on blockchain-based projects and crypto-assets and draft scheme information documents were filed with the Regulator. SEBI, however, has expressed its reservations3 on approving such funds/ fund of funds. Highlighting high degree of regulatory uncertainty when it comes to crypto-assets which is not an ideal situation either for business houses looking to raise funds using crypto-assets or for investors who have invested in such assets.

Another major inhibitor is the tax treatment of such tokenised assets. This is because given the construct of such token it will get classified as virtual digital asset under section 2(47A)4 of the Income Tax Act, 1961. The implication of this is that income on sale of such assets will get taxed at a flat rate of 30%. Other than the cost of acquisition, any other expenses incurred with respect to such assets are not allowed to be deducted while computing the income. Further, any loss from the transfer of such assets are also not allowed to be set-off against such income or under income computed under any provision of the act. Accordingly, such losses are also not allowed to be carried forward to any succeeding assessment years.

Recently, however, there has been some headway in asset tokenisation in Gujarat International Finance Tec-City (GIFT City) which may be poised to host India’s inaugural regulated platform for the tokenization of real estate and infrastructure assets. This initiative aims to democratize investment opportunities by enabling fractional ownership through digital tokens, leveraging blockchain technology to enhance liquidity and transparency in the sector. To this extent the IFSCA has constituted an ‘Expert Committee on Asset Tokenization’; the terms of reference of this committee are as follows –

Tokenisation is a transformative technology that has the capability to change the very nature of real world assets in the way they are managed and traded. The flow of capital into this sector is an indication of the potential of this sector in contributing to the economic growth of a country. In the formation of the working group on crypto-assets to reform US digit asset regulations, the US has taken stock of this development in the market and the need to make such technologies mainstream. It is encouraging to see India’s intention to move ahead with such innovation in the GIFT City. It is now time to wait and watch whether tokenisation will find acceptance in the economic mainstream and for this to happen a clear regulatory architecture has to emerge in India.