A significant part of the RBI’s regulatory framework for Non-Banking Financial Companies (NBFCs) hinges on a fundamental distinction: whether or not an NBFC maintains a customer interface. This is not a mere definitional distinction; it is a classification that dictates the scale of regulatory oversight, the applicability of consumer protection norms, and the intensity of several conduct-of-business compliance obligations. NBFCs that directly engage with customers are naturally placed under a stricter regime, while those that operate without such interaction enjoy lighter requirements. These NBFCs which do not have a customer interface and do not also access public funds are called NBFC-Type I.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-09-18 18:42:242025-10-09 16:38:14All in the Group and still a Customer!

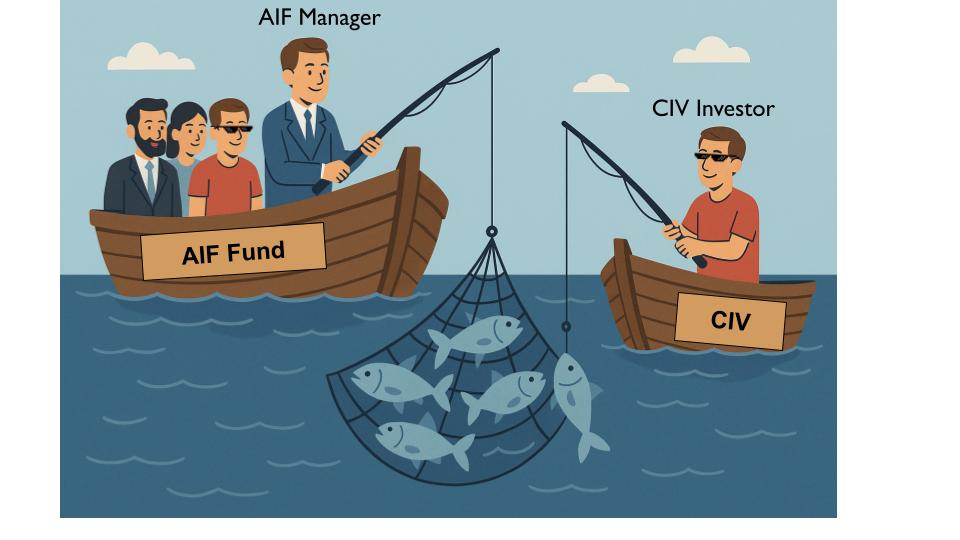

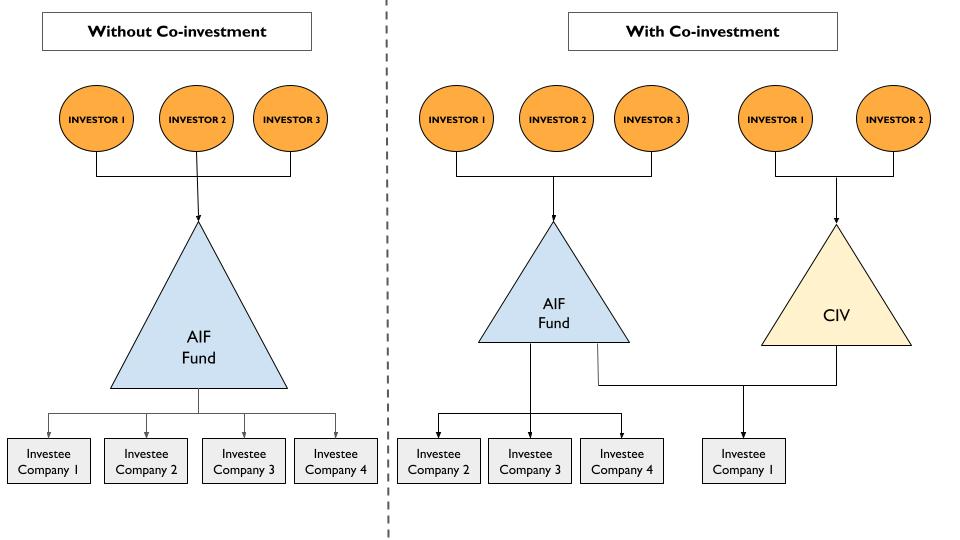

Within an AIF structure, funds are committed by the investors and the AIF in turn, through its Investment Manager, makes investments in investee entities in line with the fund’s strategy. Situations may arise where an investee company of the AIF may require additional capital, that the Investment Manager may not be willing to provide out of the fund’s corpus possibly due to multiple reasons such as over-exposure, non-alignment with funding strategy, capital constraints etc.

In such cases, the Manager may encourage investors to commit further funds directly into the investee. This gives rise to what is known as ‘co-investment’ –an investment by limited partners (LPs or investors) in a specific investee alongside, but distinct from, the flagship fund. Globally, these are also called ‘Sidecar’ funds or ‘parallel’ funds.1

Benefits of co-investments

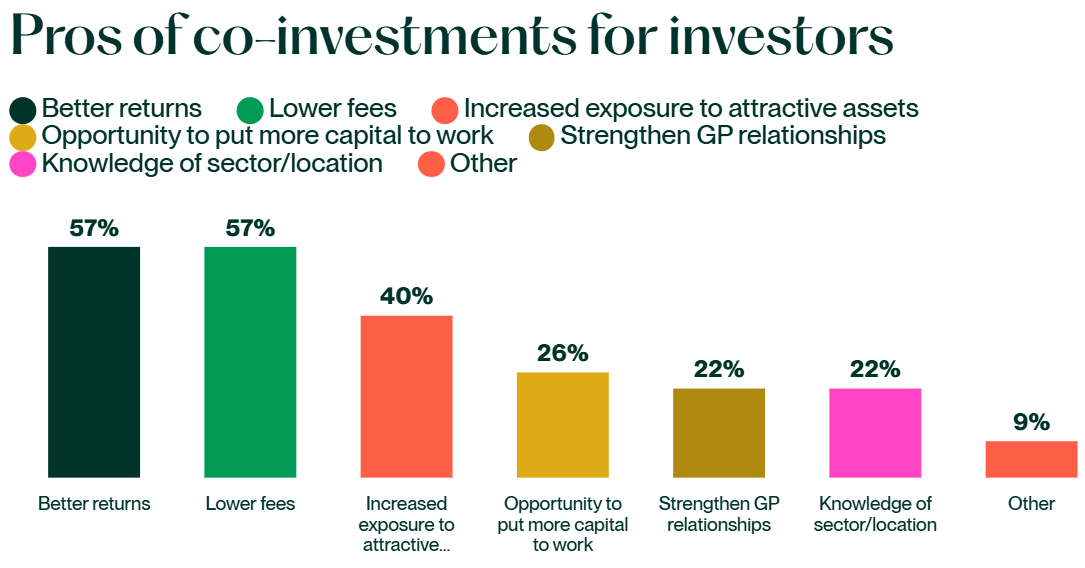

Investors benefit from co-investments primarily in terms of cost efficiency, in the following ways:

No or lower management fees and a reduced rate of carried interest.2

Reducing/ removing operational and administrative expenses such as in due diligence process & deal sourcing

Where management and incentive fees are directly charged on co-investments, they are usually capped and lower than when investing directly into the PE Fund.3

Not only are headline rates4 typically lower, but management fees are often charged on invested rather than committed capital, reducing fee drag and mitigating the J-Curve.5

For Managers co-investment offers the following advantages:

Provide access to expanded capital;

Enables it to pursue larger transactions without over extending the main fund

A Preqin study6 found that 80% of LPs reported better performance from equity co-investments than traditional fund structures.

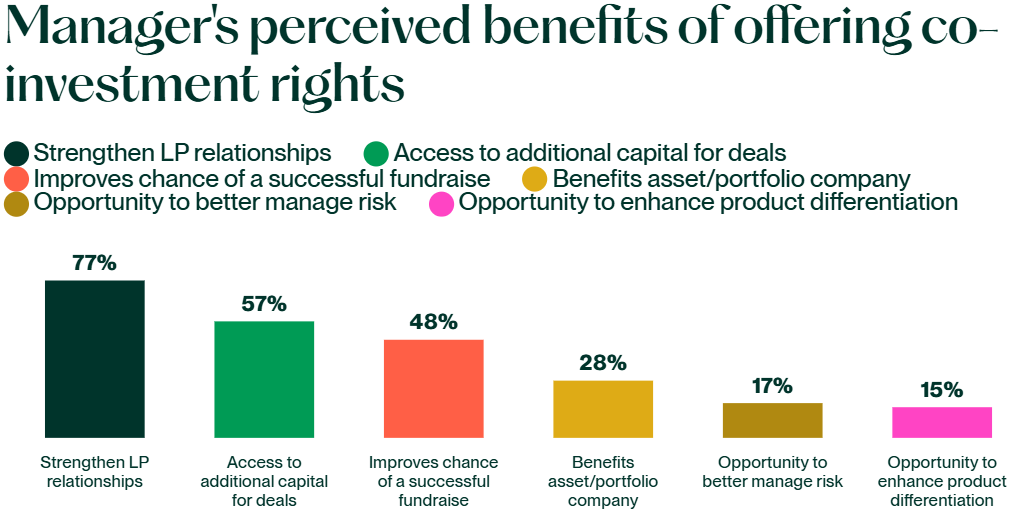

Fig 2: Investor’s perceived benefits of co-investment

Co-investments by AIF investors in the investees of AIF were primarily offered in accordance with the SEBI (Portfolio Managers) Regulations, 2020 (“PM Regulations”). In 2021, PM Regulations were amended to regulate AIF Managers offering co-investments by acting as a portfolio manager of the investors (see need for regulating the co-investment structure below). The AIF Regulations, in turn, required the investment manager to be registered under PM Regulations, for providing co-investment related services.

Keeping in view the rising demand for co-investments, SEBI, based on a recent Consultation Paper issued on 9th May 2025, has amended the AIF Regulations, vide notification dated 9th September, 2025 and issued a circular in September 2025 introducing a dedicated framework for co-investments within the AIF regime itself. Note that the recently introduced framework is in addition to and does not completely replace the co-investment framework through PM as provided in the PM Regulations.

The newly introduced framework refers to co-investments as an affiliate scheme within the main scheme of the fund, in the form of a Co-investment Vehicle Scheme (CIV) and does not require a separate registration by the Investment Manager in the form of Portfolio Manager under PM Regulations.

Interestingly, in May 2025, IFSCA also issued a Circular specifying operational aspects for co-investments by venture capital funds and restricted schemes operating in the IFSC. In this article, we discuss the new framework vis-a-vis the existing PMS route.

Need for regulating co-investments

Conflicts of interest

Especially around the timing of exit. Main fund vs. co-investors may have different preferences.

Voting rights alignment

Misalignment can fragment decision-making.

Risk concentration for investors

Exposure to a single company rather than a diversified portfolio.

Disclosure and transparency obligations for managers

Other fund investors need clarity on why the deal was structured as a co-investment.

Questions may arise on whether the main fund had sufficient capacity to invest.

Risk of concerns about preferential treatment of select investors.

Operational issues:

Warehousing: main fund may initially acquire the investment until co-investment vehicle is ready; requires proper compensation to the fund for interim costs.

Expense allocation: management costs must be fairly shared between the fund and the co-investment vehicle.

Co-investment through PMS Route – the existing framework

Under the PMS Route, the AIF Manager intending to offer co-investment opportunities to its investors shall first register itself as a ‘Co-investment Portfolio Manager’ (see reg. 2(1)(fa) of PM Regulations) post which it can invest the funds of investors subject to the following conditions:

100% of AUM shall be invested in unlisted securities [see reg. 24(4B)];

Only a manager of a Cat I & II AIF is allowed to offer co-investment;

The terms of co-investment in an investee company by a co-investor, shall not be more favourable than the terms of investment of the AIF [see proviso to reg. 22(2)]:

Terms relating to exit of co-investors shall be identical to that of exit of AIF [see proviso to reg. 22(2)];

Early termination/withdrawal of funds by co-investor shall not be allowed. [see reg. 24(2)(a)]

The AIF Manager, registered as a Co-investment Portfolio Manager, is subject to all the compliances as required under the PM Regulations, read with the circulars issued thereunder, except the following:

The minimum investment limit of Rs. 50 Lac per investor in case of PMS will not apply [see reg. 23(2)];

Min. net worth criteria of Rs. 5 Crore shall not apply to such a PM [see reg. 11(e)];

Appointment of a custodian is not required. (see reg. 26)

Roles and responsibilities of the compliance officer can be discharged by the principal officer of the Manager. [see reg. 34(1)]

Particulars

Discretionary

Non-discretionary

Co-investment

No. of clients

1,92,548

6,733

609

AUM (Rs. Crores)

33,05,958

3,18,685

4,674

Table 1: No. of co-investment clients and their total AUM as on 31.07.2025.

As per Table 1, it is evident that co-investment under the PMS Regulations has not taken off yet. One of the major reasons is the additional registration & compliance burden associated with this route.

Co-investment through CIV : the recently approved framework

“Co-investment” means investment made by a Manager or Sponsor or investor of a Category I or II Alternative Investment Fund in unlisted securities of investee companies where such a Category I or Category II Alternative Investment Fund makes investment;”

The framework is restricted to “unlisted securities” only, for the following reasons:

There is a greater information symmetry in case of unlisted securities;

In case of investment in listed securities, it is difficult to establish whether an investor’s decision to invest is driven by the fund manager’s advice or based on the investor’s own independent assessment;

Co-investments are typically undertaken in unlisted entities.

Reg 2(1)(fa) defines co-investment scheme as:

“Co-investment scheme” means a scheme of a Category I or Category II Alternative Investment Fund, which facilitates co-investment to investors of a particular scheme of an Alternative Investment Fund, in unlisted securities of an investee company where the scheme of the Alternative Investment Fund is making investment or has invested;”

The conditions for co-investment through the AIF route is prescribed through the newly inserted Reg 17A to the AIF Regulations read with the Circular dated September 09, 2025. Additionally, the Circular also refers to the implementation standards, if any, formulated by SFA with regard to offering of the co-investment schemes by the AIFs. Since the CIV operates as an affiliate AIF, in order to make it operationally feasible, a CIV has been granted the following exemptions under the AIF Regulations [See reg. 17A(10) of AIF Regulations]:

No minimum corpus of ₹20 Cr.

No continuing sponsor/manager interest (2.5%/₹5 Cr).

Exempt from Placement Memorandum contents, filing modalities, tenure requirement.

Exempt from 25% single-investee company concentration limit

Investment via PMS vs Investment via CIV of an AIF

Post the AIF Amendment, investors have a choice for investing either through the PMS Route or through the CIV route under AIF Regulations. A comparison between the 2 routes is listed below:

Aspects

Investing through CIV

Investing through PMS

Regulatory framework

SEBI (Alternative Investment Funds) Regulations, 2012

SEBI (Portfolio Managers) Regulations, 2020

Limit on investment by each investor

Upto 3 times of investment made by such investor in the investee company through AIF.

Directly in the securities of the investee company.

Co-terminus exit

Timing of exit of CIV = Timing of exit of AIF Scheme from such investee company.

Co-terminus exit

Eligibility of investor

Only Accredited Investors

Any investor

No regulatory bypass

CIV cannot: – Give indirect exposure to such investees where direct exposure is not permitted to the investors; – Create situations needing additional disclosures; – Channel funds where investors are otherwise restricted.

Considered as direct investment by the investor.

Ineligibility of investors

Defaulting, excused, or excluded investors of AIF cannot participate in CIV.

No such exclusion. This seems like a regulatory loophole.

Operational burden

CIV aggregates co-investors’ exposure; hence, only the Scheme appears on the capital table; Unified voting and simplification of compliance requirements for investees as well

Multiple co-investors appear directly on the investee company’s cap table. Closing times may be different, and operationally difficult for investors and investees to exercise voting rights and ensure compliances at each investor’s level.

Scope for co-investment

Managers can extend co-investment services to investors of any AIF managed by them (Sponsor may be same or different)

A Co-investment Portfolio Manager can serve only his own AIF’s investors, and others only if managed by him with the same sponsor

Ring-fencing of funds and investments

Separate bank & demat accounts for each CIV

Bank & demat account of investor

Leverage restrictions

CIV cannot undertake any leverage.

The PM cannot undertake leverage and invest.

Taxation

Tax pass through granted to Cat I & II AIFs make the investors directly liable to tax except on business income of the AIF

Capital gain and DDT payable by investor directly

Filing a shelf PM

Managers are required to file a separate Shelf PM for each CIV Scheme.

No such requirement

Conclusion

Much of the future trajectory of co-investments in India will depend on how both investors and managers weigh the relative merits of the PMS and CIV routes. While the PMS framework comes with higher compliance costs and additional registration requirements, the absence of a maximum cap on investments by the co-investors may still serve as a motivational factor for continued usage of the same. By contrast, the CIV framework seeks to simplify execution and preserve alignment with the parent AIF, although the 3 times’ cap on the co-investor’s share may be a hindrance for investors, thus making the CIV structure less attractive. Recently RBI had also issued Directions for regulated entities investing in AIFs with a view to curb evergreening and excessing investing in AIF structures (see our article on the same). The AIF Manager shall be cognizant of these restrictions in order to ensure there is no bypass through CIV.

Large institutional investors, sovereign funds and pension funds are likely to be the early adopters of CIV structures, given their scale, accredited investor status, and preference for alignment with fund managers. High-net-worth individuals (HNIs) and family offices, on the other hand, may still prefer the PMS route owing to its flexibility and direct exposure. Over time, the regulatory tweaking of these frameworks, if any and the appetite of investors for concentrated exposure will determine how the Indian co-investment landscape unfolds.

In private equity, the headline rate (e.g., 2% management fee, 20% carry) is what’s stated in the PPM, but the effective rate investors actually pay is usually lower. This depends on factors like fees on committed vs. invested capital, negotiated discounts or preferential terms, and lifecycle adjustments such as fee step-downs post-investment period. ↩︎

The J Curve represents the tendency of private equity funds to post negative returns in the initial years and then post increasing returns in later years when the investments mature. The negative returns at the onset of investments may result from investment costs, management fees, an investment portfolio that is yet to mature, and underperforming portfolios that are written off in their early days: Corporate Finance Institute↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-09-18 14:36:572025-09-18 17:12:59CIV-ilizing Co-investments: SEBI’s new framework for Co-investments under AIF Regulations

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-09-16 19:32:432025-09-22 13:00:22Payment Aggregators come under common code

– Approves major proposals easing institutional investments in IPOs, minimum offer size for larger entities, AIF entry, increased threshold for related party transaction approvals etc.

Relaxed norms for Related Party Transactions

Introduction of scale-based threshold for materiality of RPTs for shareholders’ approvals based on annual consolidated turnover of the listed entity

Annual Consolidated Turnover of listed entity (in Crores)

Approved threshold (as a % of consolidated turnover)

< Rs.20,000

10%

20,001 – 40,000

2,000 Crs + 5% above Rs. 20,000 Crs

> 40,000

3,000 Crs + 2.5% above Rs. 40,000 Crs

Revised thresholds for significant RPTs of subsidiaries

10% of standalone t/o or material RPT limit, whichever is lower.

Simpler disclosure to be prescribed by SEBI for RPTs that does not exceed 1% of annual consolidated turnover of the listed entity or Rs. 10 Crore, whichever is lower. ISN disclosures will not apply.

‘Retail purchases’ exclusions extended to relatives of directors and KMPs, subject to existing conditions

Inclusion of validity of shareholders’ approval as prescribed in SEBI circular dated 30th March 2022 and 8th April, 2022

Relaxation in thresholds for Minimum Public Offer (MPO) and timelines for compliance Minimum Public Shareholding (MPS) for large issuers (issue size of 50,000 Cr and above)

Reduction in MPO requirements for companies with higher market capitalisation

Relaxed timelines for complying with MPS

Post listing, the stock exchanges shall continue to monitor these issuers through their surveillance mechanism and related measures to ensure orderly functioning of trading in shares

Applicable to both entities proposed to be listed and existing listed entities that are yet to comply with MPS requirements

Following changes recommended in Rule 19(2)(b) of Securities Contracts (Regulation) Rules, 1957:

Post-issue market capitalisation (MCap)

MPO requirements

Timeline to meet MPS requirements (25%)

Existing provisions

Post amendments

Existing provisions

Post amendments

≤ 1,600 Cr

25%

NA

1,600 Cr < MCap ≤ 4,000 Cr

400 Crs

Within 3 years from listing

4,000 Cr < MCap ≤ 50,000 Cr

10%

Within 3 years from listing

50,000 Cr < MCap ≤ 1,00,000 Cr

10%

1,000 Cr and at least 8% of post issue capital

Within 3 years from listing

Within 5 years from listing

1,00,000 Cr < MCap ≤ 5,00,000 Cr

5000 Cr and atleast 5% of post issue capital

6, 250 Cr and 2.75% of post issue capital

10% – within 2 years 25% – within 5 years

If MPS on the date of listing <15%, then15% – within 5 yrs25% – within 10 yrs If MPS >15% on the date of listing, 25% within 5 yrs

MCap > 5,00,000 Cr

15,000 Cr and 1%of post issue capital, subject to minimum dilution of 2.5%

If MPS on the date of listing <15%, then15% – within 5 yrs25% – within 10 yrs If MPS on the date of listing >15%, 25% within 5 yrs

Mandatory equity dilution for meeting MPS requirement may lead to an oversupply of shares in case of large issues;

Dilution may impact the share prices despite strong company fundamentals.

Broaden participation of institutional investors in IPO through rejig in the anchor investors allocation

Following changes recommended in Schedule XIII of ICDR Regulations.

Merge Cat I and II of Anchor Investor Allocation to a single category of upto 250 crores. Minimum 5 and maximum 15 investors subject to a minimum allotment of ₹5 crore per investor.

Increasing the number of permissible Anchor Investor allottees for allocation above 250 crore in the discretionary allotment – for every additional ₹250 crore or part thereof, an additional 15 investors (instead of 10 as per erstwhile norms) may be permitted, subject to a minimum allotment of ₹5 crore per investor.

Life insurance companies and pension funds included in the reserved category along with domestic MF; proportion increased from 1/3rd (33.33%) to 40%

33% for domestic MFs

7% for life insurance companies and pension funds

In case of undersubscription, the unsubscribed part will be available for allocation to domestic MF.

To ease participation for large FPIs operating multiple funds with distinct PANs, which currently face allocation limits due to line caps

Given the recent deal size, most issuances fall within the threshold of Cat II or higher, limiting the relevance of Cat 1, therefore merge Cat 1 and Cat II

Including life insurance companies and pension funds:

Growing interest in IPOs, the amendment will ensure participation and diversify long term investor base.

Clarifications in relation to manner of sending annual reports for entities having listed non-convertible securities [Reg 58 of LODR]

For NCS holders whose email IDs are not registered

A letter containing a web link and optionally a static QR code to access the annual report to be sent

Instead of sending hard copy of salient features of the documents as per sec 136 of the Act

Aligned with Reg 36(1) (b) of LODR as applicable to equity listed cos

Currently, temporary relaxation was given by SEBI from sending of hard copy of documents, provided a web-link to the statement containing the salient features of all the documents is advertised by the NCS listed entity

Timeline for sending the annual report to NCS holders, stock exchange and debenture trustee

To be specified based on the law under which such NCS-listed entity is constituted

For e.g. – Section 136 of the Companies Act specifies a time period of at least 21 days before the AGM.

Light touch regulations for AIFs that are exclusively for Accredited Investors and Large Value Funds

Introduction of new category of AIFs having only Accredited Investors

Reduction of minimum investment requirements for Large Value Funds (LVFs) from Rs. 70 crores to Rs. 25 crores per investor

Lighter regulatory framework for AIs – only/ LVFs

Existing eligible AIFs may also opt for AI only/ LVF classification with associated benefits

Enhanced participation of Mutual Funds through re-classification of investment in REITs as ‘equity’ investments, InVITs to continue ‘hybrid’ classification

Results in REITs becoming eligible for limits relating to equity and equity indices

Entire limits earlier available to REITs and InVITs taken together now becomes available to InVITs only

In view of the characteristics of REIT & InVITts and to align with global practice

Expanding the scope of ‘Strategic Investor” & aligning with QIBs under ICDR

Extant Regulations cover: NBFC-IFCs, SCB, a multilateral and bilateral development financial institution, NBFC-ML & UL, FPIs, Insurance Cos. and MFs.

Scope amended to include: QIBs, Provident & Pension funds (Min Corpus > 25Cr), AIFs, State Industrial Development Corporation, family trust (NW > 500 Cr) and intermediaries registered with SEBI (NW > 500 Cr) and NBFCs – ML, UL & TL

Relevance of Strategic Investors:

Invests a min 5% of the issue size of REITs or INVITs subject to a maximum of 25%. Investments are locked in for a period of 180 days from listing

Such subscription is documented before the issue and disclosed in offer documents

to attract capital from more investors under the Strategic Investor category

to instil confidence in the public issue

SWAGAT-FI for FPIs: relaxing eligibility norms, registration and compliance requirements

Registration of retail schemes in IFSCs as FPIs alongside AIFs in IFSC

Both for retail schemes and AIFs, the sponsor / manager should be resident Indian

Alignment of contribution limit by resident indian non-individual sponsors with IFSCA Regs

Sponsor contributions shall now be subject to a maximum of 10% of corpus of the Fund (or AUM, in case of retail schemes)

Overseas MFs registering as FPIs may include Indian MFs as constituents

SEBI circular Nov 4, 2024 permitted Indian MFs to invest in overseas MFs/UTs that have exposure to Indian securities, subject to specified conditions

SWAGAT for objectively identified and verifiably low-risk FIs and FVCIs

Introduction of SWAGAT-FI status for eligible foreign investors

Easier investment assess

Unified registration process across multiple investment routes

Minimize repeated compliance requirements and documentation

Eligible entities (applicable to both initial registration and existing FPIs):

Govt and Govt related investors: central banks, SWFs, international / multilateral organizations / agencies and entities controlled or 75% owned (directly or indirectly) thereby

Public Retail Funds (PRFs) regulated in home jurisdiction with diversified investors and investments, managed independently: MFs and UTs (open to retail investors, operating as blind pools with diversified investments), insurance companies (investing proprietary funds without segregated portfolios), PFs

Relaxation for SWAGAT-FIs

Option to use a single demat account for holding all securities acquired as FPI, FVCI, or foreign investor units, with systems in place to ensure proper tagging and identification across channels

To tackle the problem of global investors in accessing Indian laws and regulatory procedures across various platforms, citing the absence of a centralized and comprehensive legal repository.

SEBI board decision for doubling the materiality threshold and make it scalar; lesser RPTs to need ISN details, plus other relaxations

Highlights:

Following a 32-pager consultation paper proposing significant amendments to RPT provisions, towards ease of doing business, rolled out by SEBI on August 4, 2025, several amendments have been approved by SEBI in its Board Meeting on 12th September, 2025 and the same will become effective in due course upon notification of the amendment regulations. We briefly discuss the approved changes with our analysis of the same.

Some of our comments on the proposals, as recommended to SEBI, have also been accepted in the approved decisions. Our comments on the Consultation Paper may be read here.

1. Materiality Thresholds: From One-Size-Fits-All to several sizes for the short-and-tall

A scale-based threshold mechanism has been approved, such that the RPT materiality threshold increases with the increase in the turnover of the company, though at a reduced rate, thus leading to an appropriate number of RPTs being categorized as material, thereby reducing the compliance burden of listed entities. The maximum upper ceiling of materiality has been kept at Rs. 5,000 crores, as against the existing absolute threshold of Rs. 1000 crores.

Materiality thresholds as approved in SEBI BM:

Annual Consolidated Turnover of listed entity (in Crores)

Approved threshold (as a % of consolidated turnover)

Maximum upper ceiling (in Crores)

< Rs.20,000

10%

2,000

20,001 – 40,000

2,000 Crs + 5% above Rs. 20,000 Crs

3,000

> 40,000

3,000 Crs + 2.5% above Rs. 40,000 Crs

5,000 (deemed material)

Back-testing the proposal scale on RPTs undertaken by top 100 NSE companies show a 60% reduction in material RPT approvals for FY 2023-24 and 2024-25 with total no. of such resolutions reducing from 235 and 293, to around 95 to 119. The 60% reduction may itself be seen as a bold admission that the existing regulatory framework was causing too many proposals to go for shareholder approval.

Our Analysis and Comments

With the amendments becoming effective, RPT regime is all set to be a lot relaxed, with the absolute threshold for taking shareholders’ approval to be doubled to Rs. 2000 crores. In addition, for larger companies, there will be a scalar increase in the threshold, rising to Rs. 5000 crores. A lot lesser number of RPTs will now have to go before shareholders for approval in general meetings.

In times to come, a multi-metric approach, depending on the nature of the transaction, may be adopted, drawing on a consonance-based criteria as seen in Regulation 30 of the LODR Regulations, thus offering a more balanced and effective approach. See detailed discussion in the article here.

2. Significant RPTs of Subsidiaries: Plugging Gaps with Dual Thresholds

Extant provisions vis-a-vis SEBI approved changes

Pursuant to the amendments in 2021, RPTs exceeding a threshold of 10% of the standalone turnover of the subsidiary are considered as Significant RPTs, thus, requiring approval of the Audit Committee of the listed entity. The following modifications have been approved with respect to the thresholds of Significant RPTs of Subsidiaries:

‘Material’ is always ‘Significant’: There may be instances where a transaction by a subsidiary may trigger the materiality threshold for shareholder approval, based on the consolidated turnover of the listed entity, but still fall below the 10% threshold of the subsidiary’s own standalone turnover. As a result, such a transaction would escape the scrutiny of the listed entity’s audit committee. This inconsistency highlights a regulatory gap and reinforces the need to revisit and revise the threshold criteria to ensure comprehensive oversight in a way that aligns with evolving group structures and scale of operations. RPTs of subsidiary would require listed holding company’s audit committee approval if they breach the lower of following limits:

10% of the standalone turnover of the subsidiary or

Material RPT thresholds as applicable to listed holding company

Alternative for newly incorporated subsidiaries without a track record: For newly incorporated subsidiaries which are <1 year old, consequently not having audited financial statements for a period of at least one year, the threshold for Significant RPTs to be based on lower of:

10% of aggregate of paid-up capital and securities premium of the subsidiary, or

Material RPT thresholds as applicable to listed holding company

Our Analysis and Comments

For newly incorporated subsidiaries, the Consultation Paper proposed linking the thresholds with net worth, and requiring a practising CA to certify such networth, thus leading to an additional compliance burden in the form of certification requirements. The SEBI BM refers to a threshold based on paid-up share capital and securities premium, and hence, certification requirements may not arise.

Further, the Consultation Paper proposed a de minimis exemption of Rs. 1 crore for significant RPTs of subsidiaries, thus, not requiring approval of the AC at the listed holding company’s level. However, the SEBI BM does not specifically refer to whether or not the proposal has been accepted, and hence, more clarity on the same may be gained upon notification of the amendment regulations.

Having said that, there is a need to revise and revisit the list of RPs of subsidiaries that gets extended to the listed holding company, thus attracting approval requirements for transactions with various such persons and entities, where there is absolutely no scope for conflict of interest. A Consultation Paper issued some time back on 7th February 2025 proposed extending the definition of related party under SEBI LODR to the subsidiaries of the listed entity as well. See an article on the same here. However, in the absence of any specific approval of SEBI on the same till date, such proposal seems to have been withdrawn by SEBI.

3. Tiered Disclosures: Balancing Transparency and Burden

Existing provisions vis-a-vis SEBI approved changes

The Industry Standards Note on RPTs, effective from 1st September, 2025 provides an exemption from disclosures as per ISN for RPTs aggregating to Rs. 1 crore in a FY. The amendments seek to provide further relief from the ISN, by introducing a new slab for small-value RPTs aggregating to lower of:

1% of annual consolidated turnover of the listed entity as per the last audited financial statements, or

Rs. 10 crore

In such cases, the disclosures will be required as per the Circular to be specified by SEBI. The draft Circular, as provided in the Consultation Paper, specifies disclosures in line with the minimum information as was required to be placed by the listed entity before its Audit Committee in terms of SEBI Circular dated 22nd November, 2021 ( subsumed in LODR Master Circular dated November 11, 2024), prior to the effective date of ISN. Upon the same becoming effective, disclosures would be required in the following manner as per LODR:

Value of transaction

Disclosure Requirements

Applicability of ISN

< Rs. 1 crore

Reg 23(3) of SEBI LODR and RPT Policy of the listed entity (refer FAQs on ISN on RPTs)

NA – exempt as per ISN

> Rs 1 crore, but less than 1% of consolidated turnover of listed entity or Rs. 10 crores, whichever is lower (‘Moderate Value RPTs’)

Other than Moderate Value RPTs but less than Material RPTs (specified transactions)

Part A and B of ISN

Yes

Material RPTs (specified transactions are material)

Part A, B and C of ISN

Yes

Other than Moderate Value RPTs but less than Material RPTs (other than specified transactions)

Part A of ISN

Yes

Our Analysis and Comments

The approved changes provide further relief from the task of collating a cartload of information as required under the ISN, subject to the thresholds as provided. While the introduction of differentiated disclosure thresholds aims to rationalise compliance, care must be taken to ensure that the disclosure framework does not become overly template-driven. RPTs, by nature, require contextual judgment, and a uniform disclosure format may not always capture the nuances of each case. It is therefore important that the regulatory design continues to place trust in the informed discretion of the Audit Committee, allowing it the flexibility to seek additional information where necessary, beyond the prescribed formats.

ISN: Standardising the way information is presented to audit committees

The whole thrust of the ISN is to harmonise and streamline the manner of presenting information to AC/shareholders while seeking approval.

It is good as a guidance or goal post, but does it have to become a regulatory mandate?

Where the manner of servicing food on the table becomes a mandate, the quality and taste will give precedence to form and mannerism.

4. Clarification w.r.t. validity of shareholders’ Omnibus Approval

Existing provisions vis-a-vis SEBI approvals

The existing provisions [Para (C)11 of Section III-B of LODR Master Circular] permit the validity of the omnibus approval by shareholders for material RPTs as:

From AGM to AGM – in case approval is obtained in an AGM

One year – in case approval is obtained in any other general meeting/ postal ballot

A clarification is proposed to be incorporated that the AGM to AGM approval will be valid for a period of not more than 15 months, in alignment with the maximum timeline for calling AGM as per section 96 of the Companies Act.

Further, the provisions, currently a part of the LODR Master Circular, have been approved to be embedded as a part of Reg 23(4) of LODR.

5. Exemptions & Definitions: Pruning Redundancies

Problem Statement

Proviso (e) to Regulation 2(1)(zc) of the SEBI LODR Regulations exempts transactions involving retail purchases by employees from being classified as Related Party Transactions (RPTs), even though employees are not technically classified as related parties. Conversely, it includes transactions involving the relatives of directors and Key Managerial Personnel (KMPs) within its ambit. Additionally, Regulation 23(5)(b) provides an exemption from audit committee and shareholder approvals for transactions between a holding company and its wholly owned subsidiary. However, the term “holding company” used in this context has remained undefined, leaving ambiguity as to whether it refers only to a listed holding company or includes unlisted ones as well.

Proposal in CP

The Consultation Paper proposed two key clarifications:

The exemption related to retail transactions should be expressly limited to related parties (i.e., directors, KMPs, or their relatives) to grant the appropriate exemption.

The exemption for transactions with wholly owned subsidiaries should apply only where the holding company is also a listed entity, thereby excluding unlisted holding structures from this relaxation

Our Analysis and Comments

Under the existing framework, retail purchases made on the same terms as applicable to all employees are exempt when undertaken by employees, but not when made by relatives of directors or KMPs. This has led to an inconsistent treatment, where similarly situated individuals receive different regulatory treatment solely on the basis of their relationship with the company. The proposed language attempts to streamline this by including such relatives within the exemption, but it introduces its own drafting concern.

The phrasing – “retail purchases from any listed entity or its subsidiary by its directors or its employees key managerial personnel(s) or their relatives, without establishing a business relationship and at the terms which are uniformly applicable/offered to all employees and directors and key managerial personnel(s)” – would have created a potential loophole. As worded, the exemption could be interpreted to cover purchases made on favourable terms offered to directors or KMPs themselves, rather than being benchmarked against terms applicable to employees at large. The intended spirit of the provision seems to be to exempt only those transactions where the terms are genuinely uniform and non-preferential. A more appropriate construction would make it clear that the exemption is intended to apply only where such transactions mirror employee-level retail transactions, not privileged arrangements for senior management.

VKCO Recommendations: We had provided our comments to SEBI on the following lines:

A minor drafting error has crept in the proposed language: retail purchases from any listed entity or its subsidiary by its directors or its key managerial personnel(s) or their relatives, without establishing a business relationship and at the terms which are uniformly applicable/offered to all directors and key managerial personnel(s). While the first part should refer to directors/ KMPs and their relatives, the second part should continue to refer to ’employees’, to ensure that the terms remain non-preferential, instead of introducing preferential treatment for senior management.

Approved amendment: The approved amendment, as mentioned in the SEBI BM press release, refers to “terms which are uniformly applicable/offered to all employees” in line with our recommendation above.

Regarding the exemption under Regulation 23(5)(b) for transactions between a holding company and its wholly owned subsidiary, a clarification has been inserted to provide the interpretational guidance that the term ‘holding company’ refers to the listed entity.

The relevance of the aforesaid clarification would primarily be in cases where the unlisted subsidiary of the listed entity enters into a significant RPT with its wholly owned subsidiary (step-down subsidiary of the listed entity). Pursuant to the aforesaid proposal, as approved, no exemption will be available in such a case.

Conclusion

SEBI’s August 2025 proposals, largely aimed at relaxation, have been approved in the September BM. Though in some cases, the ability to think beyond the existing track of the law seems missing, the amendments seem more or less welcoming, relaxing the RPT regime for listed entities. With the new leadership at SEBI meant to rationalise regulations, it was quite an appropriate occasion to do so. However, at many places, the August 2025 proposals are simply making tinkering changes in 2021 amendments and fine-tuning the June 2025 ISN. In sum, SEBI’s iterative approach to RPT governance demonstrates commendable responsiveness but calls for a holistic RPT policy road-map, harmonizing LODR regulations, circulars, and guidelines. Only a forward-looking, principles-based framework, will deliver the twin objectives of ease of doing business and investor protection in the long run.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-09-14 20:47:202025-09-14 21:12:15Relaxed Party Time?: RPT regime gets lot softer

– Barsha Dikshit and Sourish Kundu | corplaw@vinodkothari.com

Introduction

The recent notification of the Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2025, (‘Amendment’) by the MCA represents a significant move towards further declogging the burden of NCLTs and promoting a more business-friendly restructuring environment. By introducing minor procedural refinements and widening the classes of companies eligible for FTM, the amendments make this route accessible to a larger segment of the corporate sector.

The fast-track merger (FTM) route was introduced under Section 233 of the Companies Act, 2013 (“the Act”), allowing certain classes of companies to get the schemes approved by Regional directors having jurisdiction over the Transferee Company instead of filing of application/ petition before NCLTs having jurisdictions over transferor and transferee company and getting the same approved after following lengthy proceedings. Basically, the FTM route was designed to ease the burden of NCLTs, with a simplified process and a deemed 60-day timeline for completion, making it a quicker and a more cost-effective alternative.

This article explores the key changes introduced through Amendment, the opportunities they create for faster and more economical reorganisations, and the practical considerations and potential challenges that companies may face while opting for this route.

Additional classes of companies can opt for the fast-track route:

Section 233 of the Companies Act, 2013 read with Rule 25 of the CAA Rules, 2016, presently allows the following classes of companies to undertake mergers under the fast-track route:

Two or more small companies;

Merger between a holding company and its wholly-owned subsidiary;

Two or more start-up companies;

One or more start-up companies with one or more small companies.

Often referred to as the “RD Route” in general parlance, the key features of a FTM, include the elimination of NCLT approval, replaced instead by confirmations/approvals from the RoC, OL, members/creditors representing 90% in value, and lastly an order by the jurisdictional RD confirming such merger. [Read the procedure here]

The key change introduced is to extend the benefit of the RD route beyond the presently eligible companies to include the following additional classes:

Scheme of arrangement between holding (listed or unlisted) and a subsidiary company (listed or unlisted) – regardless of being wholly-owned

Until now, only mergers/demergers between WOS(s) and holding companies were permitted under the existing fast track route. However, pursuant to the recent Amendment, merger/demerger between subsidiaries (not limited to wholly-owned ones) and their holding companies are also allowed under FTM route. This effectively removes the ‘wholly-owned’ limitation and extends the benefit to any subsidiary, whether listed or unlisted.

However, it is worth noting that the fast track route will not be available in cases wherein the Transferor company (whether holding company or subsidiary) is a listed company. That is to say, while subsidiaries can be merged with/demerged into a holding company or vice versa under the fast track route, this is only permissible when the transferor company is not a listed company.

Scheme of arrangement between two or more Unlisted Companies

Another significant addition is to allow fast track schemes between two or more unlisted companies subject to certain conditions as on 30 days prior to the date of inviting objections from regulatory authorities u/s 233 (1) of the CA, 2013:-

None of the companies involved should be a section 8 company;

total outstanding loans, debentures and deposits for each company must be less than ₹200 crores , and

There must be no default in repayment of any such borrowings.

All the aforesaid conditions are required to be satisfied on two occasions viz. within 30 days prior to the date of inviting objections from the regulatory authorities u/s 233(1) and on the date of filing of declaration of solvency in form CAA-10. The latter is to be accompanied with a certificate of satisfaction of the conditions above, by the auditor of each of the companies involved, in a newly introduced form CAA-10A, which will form part of the annexure to the respective declarations of solvency.

It is pertinent to note here that no common shareholding, promoter group, or common control is required between the unlisted companies seeking to merge under this route. In other words, even completely unrelated unlisted companies can now opt for a fast track merger, provided they meet the financial thresholds and other prescribed conditions.

Scheme of arrangement between two or more Fellow subsidiaries

As of now, inter-group arrangements, like schemes between two or more fellow subsidiaries, were excluded from the purview of the FTM route. However, the Amendment now brings schemes between fellow subsidiaries – i.e., two or more subsidiary companies of the same holding company – within the scope of Section 233, provided that the transferor company(ies) is unlisted. Notably, the requirement of being unlisted is applicable only to the transferor company/ies. That is to say, the Transferee Company can be a listed company.

While the amendments have commendably widened the ambit of fast-track mergers to include mergers between fellow subsidiaries and step-down subsidiaries, a regulatory overlap with SEBI LODR framework may still persist. Under Regulation 37 of the SEBI LODR read with SEBI Master Circular dated June 20, 2023, listed entities are required to obtain prior approval from stock exchanges before filing a scheme of arrangement. This requirement is waived only for mergers between a holding company and its wholly-owned subsidiary.

Given that earlier fellow subsidiaries/ step down subsidiaries were not permitted to opt FTM Route, in an informal guidance, SEBI clarified that this exemption does not extend to structures involving step-down subsidiaries merging into the ultimate parent, thereby requiring compliance with Regulation 37 in such cases.

Accordingly, while the Companies Act now permits fellow subsidiaries and step-down subsidiaries to utilize the fast-track route, the benefit of exemption from prior SEBI/stock exchange approval may not be available, particularly in cases where the transferee company is listed. Unless SEBI extends the exemption framework, listed entities may still need to follow the standard approval process under Regulation 37, which could offset some of the intended efficiency gains of the FTM mechanism

Reverse Cross-Border Mergers involving Indian WOS of foreign companies

While cross-border mergers are governed under Section 234 of the Act and Rule 25A of the CAA Rules, it is amended to absorb the merger between a foreign holding company and an Indian wholly owned subsidiary, currently covered under sub-rule (5) of Rule 25A, into Rule 25 itself to make the index of companies eligible under the FTM route more comprehensive and complete.

The additional compliances applicable in such instances are the requirement to obtain prior approval from the RBI, and submission of declaration in form CAA-16 at the stage of submitting application, in case the transferor holding company happens to share a land border with India.

Implications and Potential Practical Challenges

NCLTs are overburdened with the Companies Act cases and IBC cases. As a result, scheme of arrangement cases often receive limited attention and are subject to significant delays. The recent amendments are undoubtedly a step forward in simplifying and accelerating mergers/ demerger processes. However, certain aspects of implementation may give rise to procedural challenges that warrants careful consideration: :

Seeking approval of shareholders and creditors particularly when the transferee company is a listed company

Section 233(1) of the Act requires approval of the members holding 90% of the total number of shares. This threshold has been observed to be onerous, not just practically, but also duly recognised in the CLC Report, 2022, as the requirement is approval by those holding 90%cent of the company’s total share capital and not 90% of shareholders present and voting. This threshold becomes particularly difficult to achieve in the case of listed companies and may significantly delay the approval process, thereby defeating the very objective of fast-tracking mergers.

This was a practical difficulty faced by companies going through this route, as the approving authority i.e. the RDs, of different regions, did not take a consistent approach, some of them warranting compliance with the letters of law. However, with practice it has been observed that obtaining approval of the requisite majority as present and voting is also accepted as sufficient compliance.

Here, it also becomes important to note that the approval threshold is more stringent in case of FTMs, as compared to arrangements under the NCLT route, which requires a scheme to be approved by three-fourths in majority in an NCLT convened meeting, but the same is again offset by the time and cost involved.

Scheme where transferor company(ies) / demerging undertaking has immovable properties

The NCLT, constituted under Sections 408 of the Companies Act, 2013, is a quasi-judicial body whose orders carry significant statutory weight and are widely recognized by authorities such as land registrars for purposes like property registration and mutation. Concerns may arise w.r.t. the validity of the RD’s order on such schemes. In this regard, it is to be noted that Regional directors function as an extended administrative arms of the Central Government and orders issued by the RD, are legally on par with those of the NCLT. However, an area of concern remains w.r.t. transfer of immovable property as such a transfer is required to be registered with the local registrars, where practically, RD approved schemes may not be having the same effect as that of NCLT approved scheme.

Deemed Approval within 60 Days

Section 233 (5) of the Act requires RD’s to either approve the Scheme within the period of 60 days from the date of receipt of scheme or to file an application before NCLT, if they are of the opinion that such a scheme is not in public interest or in the interest of the creditors.

The section also provides that if the RD does not have any objection to the scheme or it does not file any application under this section before the Tribunal, it shall be deemed that it has no objection to the scheme, and the Scheme will be considered as approved. This “deemed approval” mechanism is in line with international practices, where intra/inter-group restructurings are not typically required to undergo intensive regulatory scrutiny, and schemes are considered approved once sanctioned by shareholders and creditors. For instance, the Companies Act of Japan (Act No. 86 of July 26, 2005) and the Companies Act, 2006 (UK) does not require specific approval of any regulatory authority, except in certain specific circumstances.

It is also important to note that the RD does not have the power to reject a scheme outright. As held by the Bombay High Court in Chief Controlling Revenue Authority v. Reliance Industries Ltd., that the order of a Court itself constitutes an instrument as it results in the merger and vesting of properties inter-se the merging parties. In cases of deemed approval, there seems to be a gap on whether the shareholder and creditor approved scheme is to be itself construed as the instrument of transfer, as there is no explicit approval order of the RD sanctioning the scheme. On the other hand, if the RD believes the scheme is not in public or creditor interest, the appropriate course is to refer the matter to the NCLT. In such cases, the fast-track process effectively resets, and the scheme follows the standard route before the NCLT, potentially undermining the objective of speed and efficiency that the fast-track mechanism aims to achieve.

Power of RD vis-a-vis NCLT

For schemes sanctioned by the NCLT, any amendment or variation thereto can be carried out by making an application to the tribunal, by way of an interlocutory application, and NCLT, after considering the observations of the regulatory authorities, if any, has the power to pass necessary orders. That to to say, for the Schemes originally sanctioned by the NCLT, any amendment thereto will also be done by NCLT and not any other forum. Here, a question may arise as to whether the RD, which is the ultimate authority to approve fast track schemes, has similar power, or it has to refer the application seeking amendments to the schemes originally approved by it to the NCLT?

It is a settled principle of law that the authority having the power to approve, only has the authority to allow changes therein. Thus, in case of FTMs, if schemes are originally approved by RD, application for amendment thereto may also be preferred before the RD, unless, the RD itself is on the opinion that the matter requires consideration by the Hon’ble Tribunal.

Regulatory Approvals in Case of Cross-Border Mergers

Regulation 9(1) of the FEMA (Cross-Border Merger) Regulations, 2018, provides that mergers complying with the prescribed framework are deemed to have RBI approval. Yet, as a matter of process, notices of such schemes must now be served on all relevant regulators, including the RBI, SEBI, IRDAI, and PFRDA, for their comments or objections. This strengthens oversight but could also lengthen timelines, as companies may need to wait for regulator clearances before giving effect to the scheme.

Administrative Capacity of RD Offices

A further consideration is the capacity of RD offices to process the increased number of cases that the expanded FTM eligibility is expected to generate. While there are nearly 30 NCLT benches handling merger matters across India, there are only seven RDs, each with jurisdiction over multiple states and union territories. The RD already endowed with oversight of conversion of public company into private company, approval in case of alteration of FY, rectification of name, etc., in addition to the widened ambit of FTMs. This concentration of responsibility may create administrative bottlenecks, and timely disposal will be critical to preserve the efficiency advantage of the fast-track route.

Conclusion

The Amendments mark a progressive step towards making corporate restructurings quicker and more efficient by widening the scope of Fast Track Mergers, introducing financial thresholds for unlisted companies, and streamlining procedural requirements. Importantly, a specific clarification has now been inserted to state that these provisions shall, mutatis mutandis, apply to demergers as well, thereby removing any interpretational ambiguity on the subject, modifying the forms as well. If implemented effectively, these changes have the potential to substantially declog the NCLTs while giving companies a smoother, time-bound alternative for reorganizations.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-09-09 18:10:032025-09-11 11:06:11Widening the Net of Fast-Track Mergers – A Step Towards NCLT Declogging

The Reserve Bank of India (Digital Lending) Directions, 2025 (DL Directions), introduce the requirement for Regulated Entities (‘REs’) to report the Digital Lending Apps (DLAs) utilized by them on the CIMS Portal (Para 17). Moreover, there is now also a requirement for the Chief Compliance Officer or other designated officer to certify the compliance of these DLAs.

Simple as it may appear, this poses several questions such as: (i) Which entities exactly would need to be reported; (ii) Would entities with an indirect / lead-referral arrangement to the DLA also need to be reported; (iii) What about DLAs used in co-lending – which RE does the reporting?; and (iv) What compliances exactly need to be certified, since the regulations also require compliance of DLA with “extant regulatory instructions”.

In addition to the above, this also warrants discussion because the regulator has in recent news also been auditing the LSPs and is reportedly directly engaging with them. Therefore, the certification cannot be mere lip-service or a “tick-box” compliance, and must be founded on some substantive review of the DLA. Hence, we attempt to answer the above questions in our present write-up, beginning of course, with the contextual background for these compliances.

Background

As of April 2025, there are a reported 24 Fintech “unicorns” in India, with a combined estimated valuation of $125 Billion[1], and as of December 2024, Fintech lenders reportedly serve around 23 million consumers (from 14 million in December 2022).[2] Hence, with drivers such as reduced geographical barriers, quick onboarding, expedited underwriting and disbursements, fintech lending seems to be booming.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-09-08 14:19:092025-09-10 10:37:35Understanding the CCO’s Certification for DLAs: Digital Lending Directions, 2025

The SEBI Insider Trading Regulations (‘PIT Regulations’) explicitly rolled out the responsibilities for fiduciaries by amending the regulations in 2015. Subsequrently a separate Schedule C was inserted vide the SEBI (Prohibition of Insider Trading) (Amendment) Regulations, 2018 effective from April 01, 2019 which further outlined the responsibilities for fiduciaries. In the context of PIT Regulations, the term ‘fiduciaries’ refers to all such persons who are get to handle clients’ unpublished information (UPSI) in course of their business operations, such as bankers, merchant bankers, auditors, , law firms, analysts and consultants [refer Para 3.1. of the Report of Committee on Fair Market Conduct].

While banks, because of their role and functions, are likely to have access to UPSI of borrower listed entities, listed banks have two distinct strands of responsibility when it comes to curbing and eliminating insider trading practices. In the first place, since their own securities are listed, the requirements of drawing up internal controls for their Designated Person(s) (‘DPs’) become applicable beside the framing of Code of Fair Disclosure for any sharing of UPSI in a fair and symmetrical manner. The second responsibility comes up as being fiduciaries for other listed entities, being their borrowers. In the course of its dealings with other listed entities, several price sensitive information are shared with a concerned group of employees of a bank which may be price sensitive and unpublished and hence, the list of such borrower entities, and the list of the bank’s officers dealing with such entities, needs to be drawn up for maintaining the restricted list.

In this article, we have pointed out the unique position of listed banks when it comes to handling UPSI of other listed clients, its relevance, global scenario, judicial precedents and what should be the take and approach for such listed banks while handling UPSI for other such clients.

Uniqueness for banks to have access to UPSI

Banks would usually have a more regular, frequent access of such information about its clients, which may likely be in the nature of UPSI. These may include, for instance, :

Details of all major cash inflows or outflows of the listed entity, since the bank account through which such dealings are done is maintained with such banker

Monthly turnover or performance data is usually shared

Business projections are shared at the time of sanctioning, monitoring and renewal of financing facilities

Any stress conditions in the financial position of the listed entity etc.

The dealing officer for the listed clients would have an early access to such information, and hence, may be considered as ‘insider’, pending a public disclosure of such information by the listed entity.

The Chairperson of SEBI in his recent speech has also highlighted some purposes for which unpublished information may be shared with banks such as:

Sanctioning credit facilities – Before such financial entities sanction the credit facilities, it generally gets access to UPSI in the category of financial projections or any other relevant financial data.

Debt restructuring & Settlements – During debt restructuring negotiations or repayment settlements, sensitive data on a company’s liquidity position becomes available to the listed financial institutions.

Participation in the Committee of Creditors – When such financial institutions participate in the discussion of the Committee of Creditors for restructuring of stressed assets of other listed entities, they become aware of the strategic corporate decisions while they are unpublished.

The information asymmetry and access of UPSI with banks has also been indicated by the Sodhi Committee in the context of setting out principles for sharing of UPSI for due diligence purpose:

“45. In an ideal world, the information that is generally available about any listed company in the public domain ought to be adequate for any and every investment in its securities. However, that is neither a true position nor a correct expectation is evidenced by even listed companies having to write detailed offer documents and prospectuses for securities offerings such as rights issues and follow-on public offerings. Banks that lend for acquisitions would need to conduct due diligence on a company’s operations…”

While such sharing of UPSI is expected to be for legitimate purposes, however, having access to such information makes it imperative for the listed banks to have concrete and conscious lines of internal control so as to avoid any undue usage of UPSI of listed clients for the gain of such DPs in any manner.

Identification of Designated Persons while acting as fiduciary

The identification of DPs in a fiduciary capacity requires designating such persons, who may, on the basis of their function and role in the organization, may be considered to have the ability to or have access to UPSI in relation to the clients of such fiduciary. In the context of a bank in a fiduciary relationship with a listed entity, the select group of persons, identified as DPs, based on their relevant role and functions may involve, for instance:

Project finance team

Credit department

Restructuring department

Legal team etc.

This implies that all the DPs of the listed bank as identified in its own Code of Conduct for the purpose of its own internal controls need not be included in the list of DPs maintained by the bank against the securities listed out in the restricted list or the grey list. The latter is expected to be drawn up by the listed bank considering the outreach and access of UPSI by its concerned employees in the specific departments of the listed bank.

Bankers as fiduciaries: judicial precedents of putting liability

There have been a few recent instances of insider trading related adjudication by SEBI on listed banks of the country. However, these largely pertain to dealing in the listed scrips of the banks by their Connected Persons, and not necessarily on the failure of fiduciary duties of the banks. Having said that, much of the insider trading regulations in India are built upon its counterparts in other western countries, including the US, UK, Singapore, Australia, etc. The concept principally remains similar across jurisdictions, although the manner of putting controls may vary. Thus, in the context of fiduciary duties of bankers towards protection of inside information, reference may be made of the decisions of international courts.

In one of the orders passed by the Financial Conduct Authority addressed to Mr. Ian Charles Hannan, a senior investment banker at JP Morgan was found to have shared information of its client company which was listed on the London Stock Exchange.

In another matter of the Federal Court of Australia in ASIC v Citigroup Global Markets Australia Pty Ltd [2007] FCA 963, one of the employees of the investment bank was found to have dealt in the securities of its listed clients.

In Affiliated Ute Citizens v. United States, 406 U.S. 128, 146 (1972), the Bank was acting as a transfer agent for the sellers. The Bank employees (Gale and Haslem) induced the sellers of the UDC stock to dispose of their shares without disclosing to them material facts that reasonably could have been expected to influence their decisions to sell. Withholding of such information, used by the employees for their personal gains, was considered to be in violation of Rule 10b-5 of the SEC, which prohibits “any device, scheme, or artifice to defraud” in connection with securities transactions. The Court further held that the liability of the bank, of course, is coextensive with that of Gale and Haslem.

In SEC v. Cherif, 933 F.2d 403, 405 (7th Cir. 1991), the matter pertained to an ex-employee, employed in a department dealing with confidential information of the clients of the Bank, using his access card even post his termination of employment to deal in the securities of the listed clients on the basis of material non-public information. The department was engaged in providing financing for extraordinary business transactions such as tender offers and leveraged buy-outs and hence, in the possession of UPSI pertaining to the listed clients of the Bank. The SEC brought civil charges under Rule 10b-5 against Cherif for insider trading, and such charges were affirmed by the Court on the context that as a former employee, Cherif continued to owe the bank fiduciary duties, even after the Bank terminated his employment.

In United States v. Salman, 137 S. Ct. 420 (2016), the Court of Appeals, Ninth Circuit, affirmed the conviction by the jury trial on the grounds that the disclosure of inside information about the clients to the relatives constituted a breach of the fiduciary duty of the employee of Citigroup, acting as an investment banker for such clients The Court also cited the US SC in Dirks v. SEC, 463 U.S. 646 (1983), which states that:

The elements of fiduciary duty and exploitation of nonpublic information also exist when an insider makes a gift of confidential information to a trading relative or friend. The tip and trade resemble trading by the insider himself followed by a gift of the profits to the recipient.

Listed banks should get hyper or hiber(nate) over actionables?

Sensitisation of persons responsible for dealing with UPSI

SEBI Chairperson reiterated the importance of sensitizing the employees of listed banks on their roles and responsibilities as fiduciaries which shall give strength to the internal controls in the entity. In the absence of the above, drawing of internal controls by drafting a Code of Conduct or asking the DPs to seek pre-clerance or putting a trading window and a contra trade restriction, all of these will completely lose their relevance.

The importance of sensitisation and various means by which sensitisation can be done effectively has been discussed in Sensitization: The key to implementation of PIT Regulations. An effective sensitisation framework is not limited to creating awareness through training only, but extends to a follow-up exercise of evaluating the understanding towards such principles.

Relevance for fiduciaries to have a process for how and when people are brought ‘inside’ on sensitive transactions

As a part of the Code of Conduct, the fiduciaries are required to have a process for how and when people are brought ‘inside’ on sensitive transactions. This requires sensitising the recipients about their duties and responsibilities with respect to receipt of such information, the manner of dealing with the information and the liability that follows upon the misuse of such information. Further, the effective presence of Chinese walls in a bank also helps to restrict flow of information from one department to the other without having any legitimate purpose.

Concluding Remarks

In view of the far reaching negative impact of a breach of fiduciary’s duties under insider trading regulations on the capital markets, SEBI has tried to send out an alert call for over ambitious listed banks which may not realize the nature of flaws in this regard of failing as a fiduciary The requirement for a fiduciary to protect and uphold the confidentiality of its clients has been there under the PIT Regulations for approximately a decade. It has been seeking more and more attention by securing and exhibiting an exclusive mention under the PIT Regulations itself and getting listed companies including listed banks to draw up and implement robust internal controls.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-09-05 10:15:402025-09-06 11:34:59SEBI alerts banks to realize fiduciary duties for insider information

GST changes announced vide 56th meeting of the GST Council dated Sept 03, 2025 have brought cheers to the entire country; however, for lessees of motor vehicles where rates of GST have been reduced (the extent of reduction being from 5% to 10% in most of the cases – reduction of rate from 28% to 18%, and the doing-away of the compensatory cess in others), the lessees of motor vehicles have unusual reasons to be cheered. At the same time, lessors who have existing leases of motor vehicles will have some present value losses. This article explains.

Futuristically, this reduction in GST rates on automobiles can benefit both lessor and lessees, as hopefully, the demand for motor vehicles will increase, and so will opportunities of leasing. However, there is a surprise bumper for the lessees who have currently on-the-run leases of vehicles – their rates of GST, going forward, will come down, even though the vehicle may have been acquired prior to the 22th September, 2025. Thus, while for the rest of the country, one has to buy a car to enjoy the rate reduction, lessees of existing motor vehicles also stand benefitted. Our article explains how.

On the other hand, for lessors, there will be a present value loss. With reduced GST rates, the initial outlay for the lessor, paid at the time of acquisition of the vehicles, will take longer to be recovered in the form of lease rentals – hence, the lessors will suffer a present value loss.

On an estimate, roughly Rs 6000 crores to Rs 8000 crores of car leases are done by lessors in the country; the outstanding volume of leases may be almost Rs 20000 crores.

Post-22 Sept benefit for others; lessees of existing leases also stand benefited

For anyone else to take the benefit of the rate drop, you need to buy a vehicle on and from 22 Sept. 2025. However, for lessess of existing lease transactions, the reduction in GST rates from 28% to 18% translates into a financial benefit and they clearly stand benefitted from the reduced GST rates. Lease rentals billed on/ after Sept 22nd, will attract lower GST rates which implies total periodic payment by the lessee reduces.

Wondering why is it so? This is because while a lease is regarded as a “supply of service”, however, the rate of GST on leases of goods are aligned with the rate of tax on the sale of the respective goods. Hence, if the GST on cars is currently 28%, the rate of tax on lease of the car is also 28%, payable periodically as the rentals accrue. Thus, irrespective of the original purchase date of the vehicle, post 22nd September, the GST on existing leases will drop down, giving an unequalled bounty to the existing lessees.

Present value loss for lessors

When a lessor purchases a vehicle, he pays GST upfront at the time of purchase, on the entire purchase price of the vehicle. This GST paid becomes input tax credit for the lessor. On each periodic lease rental, he collects GST from the lessee. Lessor offsets this output GST collected from the lessor against the input tax credit. In case of lease transactions entered into before Sept 22, 2025, reduction in rates of GST would mean that lessor will need longer time to recover his input tax from the lessor.

The reason being the vehicle was purchased at the higher GST rate (for instance 28%) and the lessor could avail ITC accordingly. However, Sept 22, 2025 onwards, the output GST collected periodically would reduce, for instance, would be collected at the reduced rate of 18%.

Therefore, the lessor will now take longer to fully recover the input tax credit by offsetting it against a lower input tax.

The same can be understood with the help of below mentioned illustration. Let us assume that the lessor had purchased a vehicle before Sept 22, 2025 and paid GST @28%.

Particulars

Lease arrangement before Sept 22, 2025

Lease arrangement on/ after Sept 22, 2025

Impact

Cost of vehicle

11,40,000

11,40,000

No change

GST

= 1140000*28% = 319200

= 1140000*18% = 205200

Reduced by 1,14,000

Monthly lease rental

30,000

30,000

No change

Monthly GST collected

8,400 (28%)

5,400 (18%)

Reduced by 10%

Total GST collected in 12 months

1,00,800

64,800

Reduced by 36,000

Total lease revenue (incl GST)

4,60,800

4,24,800

Reduced by 36,000

Number of months taken to recover ITC

319200/8400= 38 months

205200/5400 = 38 months

In case of lease arrangement before Sept 22, the lessor was able to recover input tax of Rs 319200 in 38 months. Under the revised rates, the rate of GST on the existing leases will come down and will be Rs 5400 per month. Therefore, it will take almost 59 months to recover the ITC originally paid. Therefore, there will be a present value loss for existing leases, which would not have been priced by the lessors at the time of the original contract.

Changes under the automobile sector at a Glance

The supply of services involving the leasing, renting, or transfer of the right to use goods is liable to attract the same rate of GST and compensation cess (which is now removed) as applicable to the supply of similar goods involving transfer of title, i.e., a supply of goods. This provision forms the basis for applying goods-equivalent tax rates to leasing transactions, despite their classification as services under GST. For a detailed understanding of GST implications on lease transactions, you may refer to our article here.

Since it has been decided to end the compensation cess levy, the compensation cess rate is being merged with the GST so as to maintain tax incidence.

As per FAQ No. 35 of the FAQs on the decisions of the 56th GST Council held in New Delhi issued by the Ministry of Finance, currently mid-size and big cars attract 28% GST and compensation cess ranging from 17-22% which makes the overall tax incidence ranging from 45-50%. Since the new GST rate on mid-size and big cars will be 40% with no compensation cess, the overall tax incidence has reduced by 5%-10%.

S. No.

Description

Earlier rate

New rate

Rates reduced

1.

Petrol, LPG or CNG driven motor vehicles of engine capacity not exceeding 1200cc and of length not exceeding 4000 mm.

28%

18%

2.

Diesel driven motor vehicles of engine capacity not exceeding 1500 cc and of length not exceeding 4000 mm.

28%

18%

3.

Three wheeled vehicles

28%

18%

4.

Fuel Cell Motor Vehicles including hydrogen vehicles based on fuel cell technology

12%

5%

5.

Tractors (except road tractors for semi-trailers of engine capacity more than 1800 cc)

12%

5%

6.

Road tractors for semi-trailers of engine capacity more than 1800 cc

28%

18%

7.

Motor vehicles for the transport of ten or more persons, including the driver [other than buses for use in public transport, which exclusively run on Bio-fuels which is already at 18%]

28%

18%

8.

Motor cycles of engine capacity upto 350 cc

28%

18%

9.

Specified solar assets

12%

5%

Rates increased

10.

Station wagons, racing cars, petrol, LPG and CNG cars of engine capacity exceeding 1200 cc or length exceeding 4000 mm

28%

40%

11.

Diesel cars of either engine capacity exceeding 1200 cc or length exceeding 4000 mm

28%

40%

12.

Motor vehicles with both spark-ignition internal combustion reciprocating piston engine and electric motor as motors for propulsion, of engine capacity exceeding 1200cc or of length exceeding 4000 mm

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-09-04 17:16:072025-09-15 11:54:39GST changes: Double dhamaka for car lessees; lessors to have elongated input tax recovery