Archive for year: 2021

An Odd Scheme: Case for exclusion of schemes of arrangement from scheme of liquidation

Sikha Bansal, Partner

The Article below has also been published on the IndiaCorplaw Blog, see here

The concerns around section 230 schemes in the background of insolvency proceedings under the Insolvency and Bankruptcy Code, 2016 (IBC) have been partly addressed with the ruling of Supreme Court (SC) in Arun Kumar Jagatramka v. Jindal Steel and Power Ltd. The SC has held that the prohibition contained in section 29A should also attach itself to a scheme of compromise or arrangement under section 230 of the Companies Act, when the company is undergoing liquidation under the auspices of IBC. Reason being: proposing a scheme of compromise or arrangement under section 230 of the Companies Act, while the company is undergoing liquidation under the provisions of the IBC, lies in a similar continuum.

Earlier, there were several rulings of NCLAT which allowed schemes of arrangement during liquidation – for instance, see S.C. Sekaran, Y. Shivram Prasad, etc. After such rulings, the IBBI (Liquidation Process) Regulations were amended to include Regulation 2B, which also state that “a person, who is not eligible under the Code to submit a resolution plan for insolvency resolution of the corporate debtor, shall not be a party in any manner to such compromise or arrangement.” Read more →

Remunerating in a lean year: Statutory amendments for minimum remuneration to independent directors now effective

Payal Agarwal | Executive (payal@vinodkothari.com)

Highlights

Introduction

Independent directors (IDs) are a crucial part of corporate governance structure; however, their remuneration is currently solely by way of sitting fees and a “profit-linked” commission[1]. Profit is something which is completely dependent on business models, a whole matrix of internal and external factors, and something like a Covid-crisis will evidently leave a whole lot of companies in India and elsewhere into the red. In these circumstances, how do companies remunerate independent directors, to reward them for the time they spend and the responsibilities they shoulder.

To resolve this difficulty, amendments were made vide the Companies (Amendment) Act, 2020.While most of the sections of the Amendment Act were made effective on 28th September 2020, the sections relating to remuneration of NEDs and IDs were not been made applicable since the same was required to be adequately supplemented by corresponding amendments in Schedule V of the Act as well. However, just before the Covid-ravished FY 2021 was to end, MCA has put into effect the amended sections 149(9) and Section 197(3) and simultaneously brought amendments in Schedule V of the Act.

Effects of the amendments

These amendments will enable companies to adequately remunerate their NEDs and IDs for their efforts. Contrary to the rigidity in the erstwhile provisions, which had a complete bar on payment of remuneration to NEDs and IDs in absence of profits, these amendments enable companies to pay minimum remuneration to NEDs and IDs even at times of losses/ inadequate profits. Note that there always was a provision for minimum remuneration in case of EDs.

Applicability

- Private companies are not covered by the ceilings of managerial remuneration. Hence, private companies are completely outside the purview of the restriction.

- Public companies, both listed and unlisted, will be covered by the amendment.

- The amendment is of enabling nature. It does not mandate companies to remunerate their NEDs and IDs. So, companies may, if they so desire, remunerate their IDs and NEDs in the year of inadequate profits, or losses.

- The amendment applies to all NEDs and IDs.

- The amendment pertains to the “profit-linked” commission. That does not mean the commission as originally proposed had to be profit-linked. Even if the commission was a fixed amount, it will still be covered by the ceiling given in second proviso to sec. 197 (1). Hence, any commission is necessarily profit-linked.

- The amendment is effective immediately. That means companies may make use of the amended provisions for FY 2020-21.

- The amendment does not lead to an automatic variation in the remuneration policy or shareholders’ resolution. In essence, the amendments are of enabling nature: within the ambit of the amended provisions, companies may take corporate action to remunerate their NEDs and IDs. The actions have to be taken by the companies in question, which may include remuneration policy, appropriate shareholder resolutions, etc.

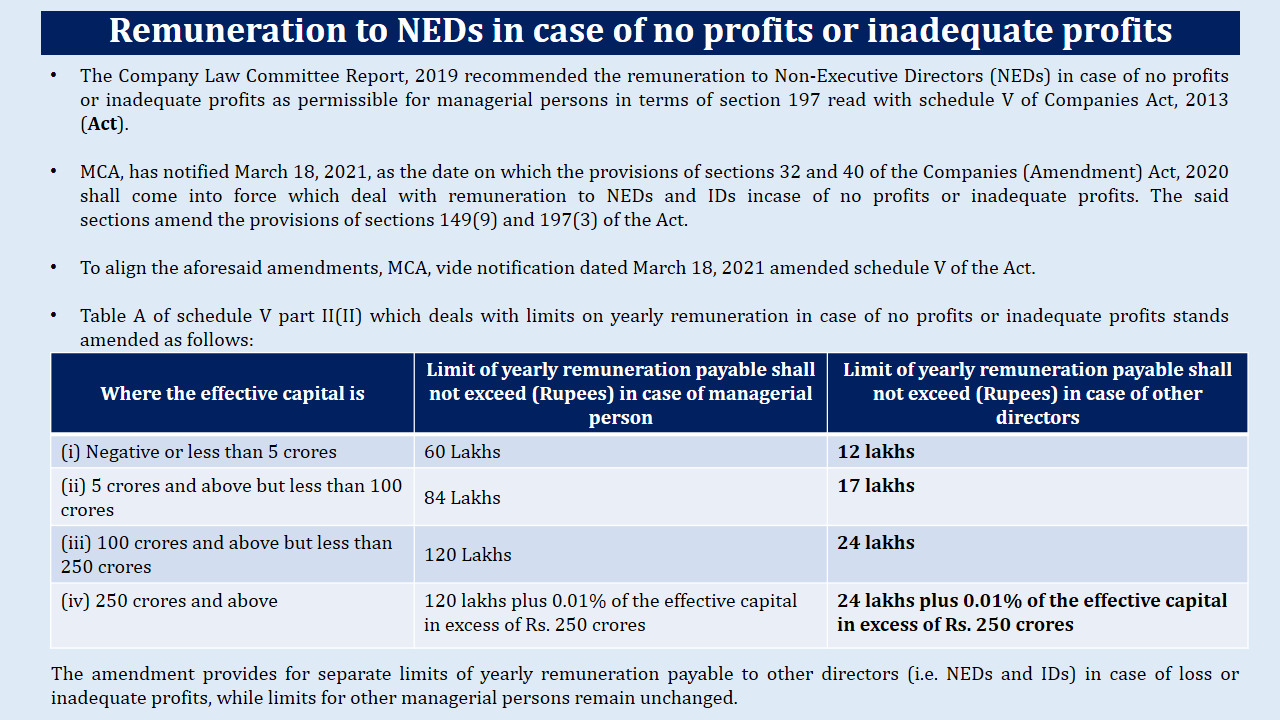

Amendments to Schedule V – maximum limits on remuneration of “other directors” specified

Part II of Schedule V of the Act deals with the remuneration of “managerial personnel”. In this connection, please note that “managerial personnel” refers to managing director, manager and whole-time director of the company. Now, with the present amendment to the Schedule, part II has become applicable on the “other directors” as well. The term “other directors” has been clarified in the amendment notification itself by way of an explanation which states,

“For the purposes of Section I, II and III (relevant parts that have been amended) the term “or other director” shall mean a non-executive director or an independent director.”

Section II of Part II of the Schedule specifies maximum remuneration that can be paid to a director, be it a managerial personnel or otherwise. For directors other than the managerial personnel, the remuneration has been specified at an amount almost 1/5th of that permissible to the managerial personnel.

The result of bringing IDs within the scope of Schedule V is that whereas the IDs would have been receiving very low remuneration in comparison to their roles and responsibilities in an organisation due to inadequacy of profits, the IDs will have a chance of getting a fair remuneration.

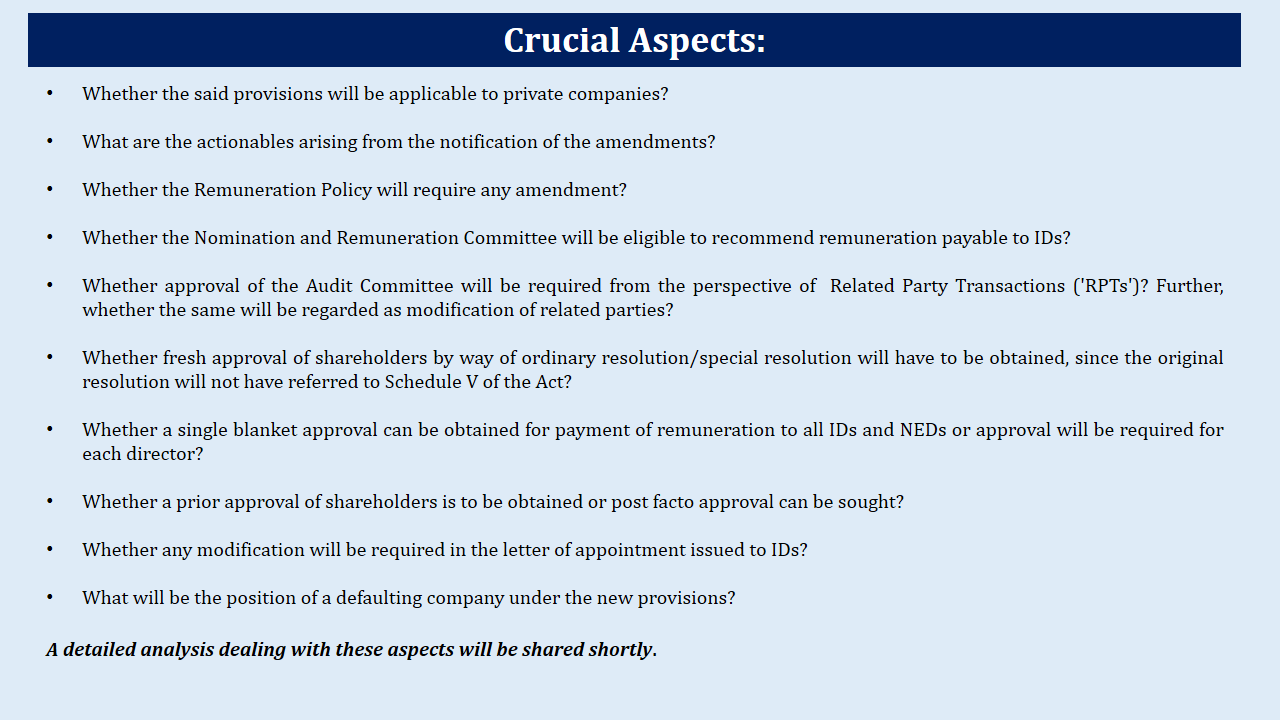

Questions relevant to the amendments

Various questions arise out of the amendments, such as –

- Will the amendments require modification in existing remuneration policy?

- Can the NEDs and IDs be paid remuneration in excess of those specified in Schedule V?

- Whether a single approval can suffice for the remuneration of all NEDs and IDs or such resolutions will have to be approved separately for the individual directors?

- Whether NRC will be eligible to recommend remuneration payable to IDs?

- Whether a prior approval of shareholders will be required or whether post facto approval may be obtained?

Answers to these and other relevant questions revolving around the aforesaid amendments has been dealt with in our detailed FAQs and can be accessed here.

Conclusion

The role of non-executive and IDs is very crucial to a company. The professional expertise of NEDs in their specific fields brings requisite value to a company. Considering the role played by IDs in effectively balancing the conflicting interest of the company and its stakeholders and bringing independent judgement to the Board’s decisions, it would be unfair if they are not paid adequately for the efforts put by them in the effective conduct of business.

Further, in the present scenario, amidst the economic breakdown worldwide, many companies may not be able to earn the profits as expected, or might be facing losses as well. In such circumstances, the aforesaid amendments were a necessity.

However, the erstwhile provisions had no scope of payment of remuneration to them in case of loss. With the aforesaid amendments coming into force, the companies will be able to compensate their non-executive and IDs well, even in case of no/inadequate profits.

Our other articles on the related topics can be read here –

[4] https://vinodkothari.com/2020/03/remunerating-neds-ids-in-low-profit-yrs/

[5] https://vinodkothari.com/wp-content/uploads/2019/09/Manangerial-Remuneration_IMTB-_26.08.pdf

[1] SEBI has recently in its consultation paper on review of regulatory framework applicable to IDs suggested that profit-linked commissions should be barred and shall be substituted by higher sitting fees or issue of stock options. Please refer to our article for broader understanding of the same.

Risk-based Internal Prescription for Audit Function

Qasim Saif | Executive (finserv@vinodkothari.com)

Updated as on June 11, 2021

Introduction

It is a well-known fact that an independent and effective internal audit function is of special importance to all corporates for mitigation of their risk. And it has increased importance for a financial sector entity as it provides for reasonable assurance to the board and its senior management regarding the quality and effectiveness of the entity’s internal control, risk management, and governance framework.

Given the current relatively uncertain economic environment which has put significant pressure on debt servicing capabilities of corporates and businesses, there is a need to critically examine the existing portfolio and take an account of the related risk management and accounting practices.

This on-going stressed situation coupled with the uncertain economic environment and the increased global regulatory watch requires financial institutions to critically evaluate the quality of their regulatory submissions, risk model, capital adequacy, and conduct in the financial markets.

In recent times, Non-Banking Financial Companies (NBFCs) / Urban Co-operative Banks (UCBs) have grown in size and have become systemically important in the economy given their increased participation in the financial credit market. Just like banks, NBFCs and UCBs face similar risks by virtue of being engaged in financial intermediation activities, hence, it makes sense that their internal audit systems should also broadly align while keeping in mind the principle of proportionality.

Applicability

Earlier this year, RBI had issued RBIA Framework for Strengthening Governance Arrangements for commercial banks, local area banks, small finance banks, and payment banks on 7th January 2021[1].

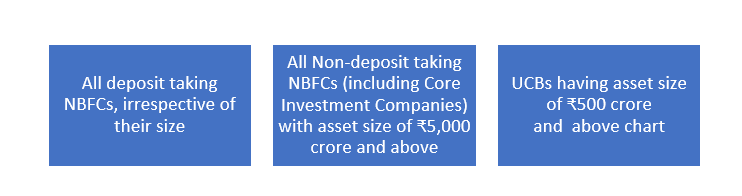

To increase focus on the risk management function of NBFCs/UCBs, the RBI on 3rd February 2021[2] issued a circular prescribing the requirement for Risk-Based Internal Audit (RBIA Framework). The requirements prescribed under the circular are to be implemented by 31st March 2022.The said circular is applicable on-

The framework for NBFCs and UCBs draws largely from the framework for banks.

The circulars clearly indicates that RBI is now accepting a more stringent attitude towards risk management and audit, specifically given the challenges faced due to Covid -19. It seems like Covid-19 acted as a wake-up alarm to increase focus on risk management and its mitigation by financial sector entities.

Applicability on Housing Finance Companies (HFCs)

The RBI circular did not specifically state the applicability of RBIA Framework on HFCs. Hence the same was open for interpretation by the stakeholders and so there were 2 different school of thoughts on this. First is that since HFCs are also a class of NBFCs so the circular should also be applicable on HFCs. However, a counter interpretation was that the Master Direction for Housing Finance Company (which assembles all applicable regulations at one place) which was notified on February 17, 2021[3] (after the given 3rd February circular), did not include compliance with RBIA Framework. Accordingly, the coverage of the RBIA Framework did not seem to be applicable on HFCs. The interpretation by the stakeholders resultied in diverse practices in the market.

However, RBI on 11th June, 2021 has issued a circular stating “On a review, it has been decided that the provisions of the aforesaid circular (circular dated 3rd February, 2021) shall be applicable to all deposit taking HFCs, irrespective of their size and non-deposit taking HFCs with asset size of ₹5,000 crore and above.

Considering the above clarification from RBI, HFCs shall now be required to be undertake Risk Based Internal Audit and put in place RBIA framework by June 30, 2022.

Risk Based Internal Audit: A Sub-set of Risk Management Framework

An essential characteristic of an effective RBIA Framework would be that it should be a connecting link between various components of risk management framework and should provide for reasonable assurance that organisation’s internal controls, risk management, and governance related systems and processes are adequate to deal with risk faced by it.

The internal audit function should ideally be targeted towards contributing to the overall improvement of the organization’s governance, risk management, and control processes using a systematic and disciplined approach.

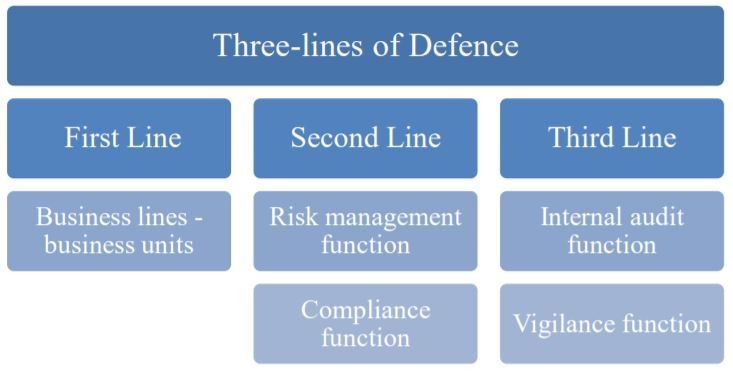

The circular provides that internal audit function is an integral part of sound corporate governance and is considered as the third line of defence. The inference for different lines of defence for risk management may be drawn from the RBIA circular for Banks, which provides as follows-

Based on the recent developments and emerging trends, the focus areas for robust internal audit should ideally inter-alia the following components-

The internal audit function in NBFCs/UCBs has generally been concentrated on accounting requirements and regulatory compliance etc. However, considering the market developments, testing limited to these factors may not be sufficient. Therefore, the current framework includes, above aspects along with, an evaluation of the risk management systems and control procedures in various areas of operations. This will help in anticipating areas of potential risks and mitigating such risks.

The RBIA should be conducted based on a RBIA plan which is required to be formulated after considering the elements of risk management framework of the entity.

Actionable

As mentioned above, reasonable amount of time is provided to NBFCs/UCBs to prepare for effective implementation of the RBIA Framework, that is, by 31st March 2022. However, though the requirements are to be complied by the end of next financial year, the preparedness for the same must be initiated immediately. A list of actionable on the part of NBFCs/UCBs has been provided below for reference:

Role and responsibilities of functionaries

It is a well understood notion that to get a particular task done, a fixed responsibility centre should be set-up, this enables proper implementation and also increases the efficiency of the implementation. Considering the same RBI has prescribed for responsibilities of senior management, Board and Audit committee to ensure proper implementation of RBIA Framework. The allotted role and responsibilities shall be as follows-

Board of Directors / Audit Committee of Board

The Board of Directors (the Board) / Audit Committee of Board (ACB) of NBFCs/UCBs shall have the primary responsibility of overseeing the internal audit function in the organization. The major responsibility of the Board and ACB would be to establish and further review the RBIA systems.

The RBIA policy is to be formulated with the approval of the Board and would be disseminated widely within the organization. The policy should be consistent with the size and nature of the business undertaken, the complexity of operations and should factor in the elements of internal audit. The ACB and Board would further review the performance of RBIA and shall also formulate and maintain a quality assurance and improvement program that covers all aspects of the internal audit function.

Senior Management

The senior management shall be responsible for implementation of the systems established by the board and ACB.

The senior management shall ensure adherence to the internal audit policy guidelines as approved by the Board and development of an effective internal control function that identifies, measures, monitors, and reports all risks faced. The senior management shall ensure audit reports is placed before the ACB/Board. Further, a consolidated position of major risks faced by the organization shall be presented at least annually to the ACB/Board, based on inputs from all forms of audit.

The senior management shall also be responsible for establishing a comprehensive and independent internal audit function that should promote accountability and transparency. It shall ensure that the RBIA Function is adequately staffed with skilled personnel of right aptitude and attitude who are periodically trained to update their knowledge, skill, and competencies.

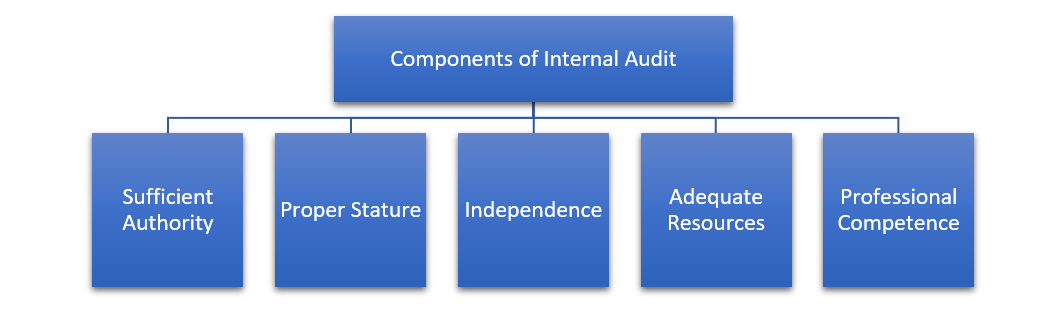

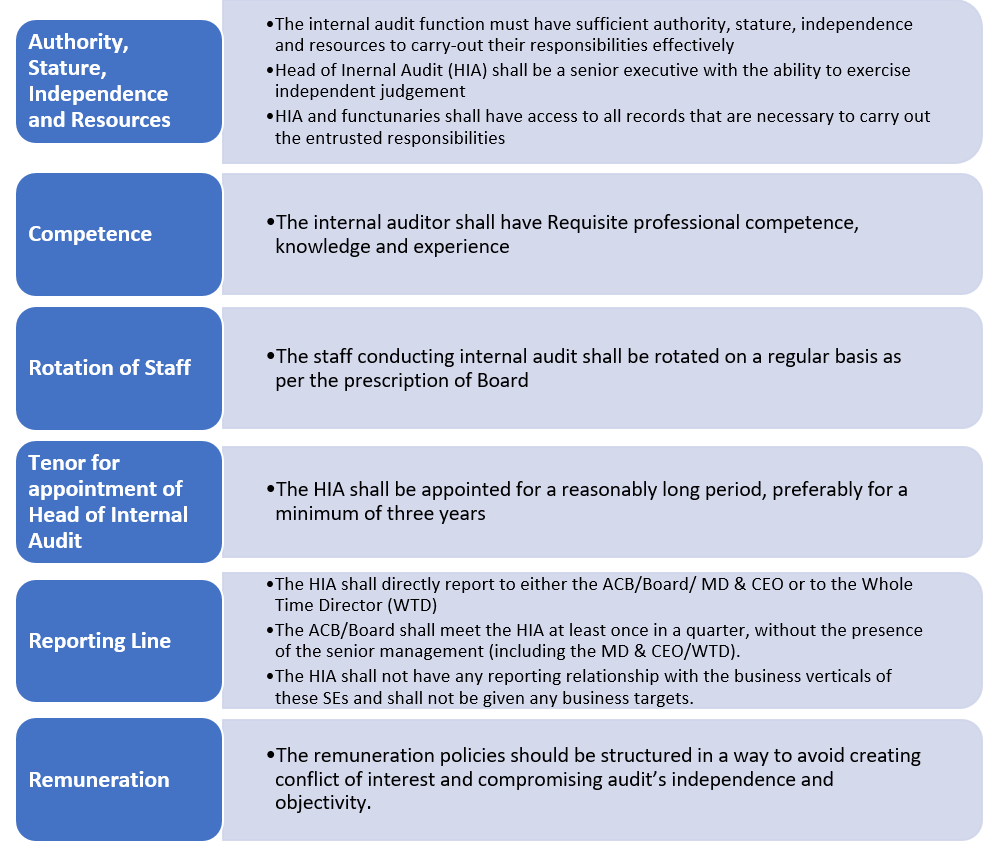

Internal Audit Function: Major Elements

The RBIA Framework broadly provides for a comprehensive internal audit function the major elements and their requirements are summarised as follows-

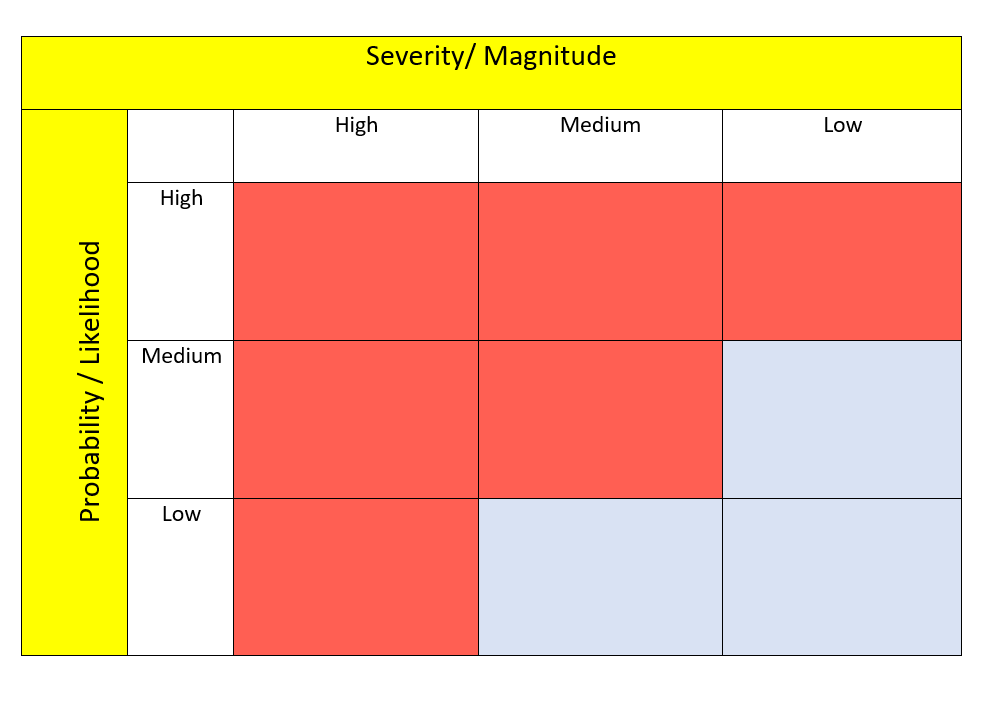

Risk Matrix

A risk matrix is a matrix that is used during risk assessment to define the level of risk by considering the category of probability or likelihood as against the category of consequence severity. This is a simple mechanism to increase visibility of risks and assist in management decision making.

The circular requires that the RBIA function should consider risk matrix while setting up action plan. Further, certain risk mentioned shall be given enhanced attention during the RBIA, the matrix and areas of focus are marked red in graph below-

Outsourcing of the Internal Audit Function

The internal audit function cannot be outsourced. However, where required, experts including former employees can be hired on a contractual basis subject to the ACB/Board being assured that such expertise does not exist within the audit function of the NBFC/UCB. Any conflict of interest in such matters shall be recognised and effectively addressed.

Monitoring and follow up

Monitoring and follow-up actions form an integral part of entire internal control system to ensure effective functioning of the procedures. Accordingly, the process as well as findings under the RBIA Framework should be regularly monitored. The said responsibility lies with the Board and Senior Management, as discussed above.

[1] https://www.rbi.org.in/scripts/NotificationUser.aspx?Id=12011&Mode=0

[2] https://rbidocs.rbi.org.in/rdocs/PressRelease/PDFs/PR10365F8B4F9BF8FE4A209F3BD7FD1D62B7D9.PDF

[3] Our write up on the topic “RBI consolidates directions for Housing Finance Companies https://vinodkothari.com/2021/02/rbi-consolidates-directions-for-housing-finance-companies/”

[4] Our write up on the top “Risk management policy” https://vinodkothari.com/2021/10/risk-management-policy-a-tool-of-risk-management/

Fragmented framework for perfection of security interest

Introduction An interesting question of law came up for consideration by way of appeal before National Company Law Appellate Tribunal (NCLAT) in Volkswagen Finance Private Limited v. Shree Balaji Printopack Pvt. Ltd.[1] The brief facts of the case involved a car financing company, which extended a car loan to the corporate debtor. The car financier […]

Conflicting provisions on CSR applicability under CA, 2013 & CSR Rules

CSR Rules require further tailoring to fit

CS Ajay Kumar K V | Vinod Kothari and Company

Corporate Social Responsibility (‘CSR’) framework in India has always been adaptive to changing times and has witnessed quite an evolution. The basic idea behind the CSR provisions was to promote responsible and sustainable business philosophy at a broad level and to encourage companies to come up with innovative ideas and robust management systems to address social and environmental concerns of the local area and other needy areas in the country.

Despite the evolution and series of amendments, certain provisions in the Companies (Corporate Social Responsibility Policy) Rules, 2014 (‘CSR Rules’) continue to conflict with the requirements under section 135 of the Companies Act, 2013 (‘CA, 2013‘). This article discusses two of such conflicting provisions relating to CSR applicability.

As per Section 135 (1) of Companies Act, 2013, CSR provisions were originally applicable to companies meeting the thresholds of INR 500 crore net worth or INR 1000 crore turnover or INR 5 crore net profit during any financial year. The meaning of the term ‘any financial year’ was clarified by MCA to imply any of the three preceding financial years. This was amended vide the Companies (Amendment) Act, 2017 (‘CAA, 2017’) thereby shifting the applicability on companies meeting any of the aforesaid criteria during the immediately preceding financial year, on the basis of recommendation made by High-Level Committee on Corporate Social Responsibility (‘HLC-CSR’)1. Further, in terms of Section 384 (2) of CA, 2013 CSR provisions are applicable to foreign companies as well.

Conflicting provision under CSR Rules

-

On Applicability [Rule 3 (1)]

Rule 3 (1) of CSR Rules provides that a company including its holding or subsidiary, and a foreign company defined in Section 2 (42) of CA, 2013 fulfilling the criteria specified under Section 135 (1) of CA, 2013 are required to comply with CSR related provisions.

Section 135 (1) is absolutely clear on the applicability par. Therefore, the intent to include holding and subsidiary company of a company that meets the criteria is unclear. If the holding or subsidiary company independently meets the criteria specified under Section 135 (1), only then it will be required to comply with CSR related provisions. The applicability cannot be linked with applicability of the Section 135 (1) to the holding or subsidiary company.

-

Cessation of Applicability [Rule 3 (2)]

In terms of Section 135 (1) read with Section 135 (5), companies meeting the aforesaid criteria during the immediately preceding financial year are required to constitute CSR Committee and spend in every financial year, at least 2% of the average net profits of the company made during the three immediately preceding financial years. Consequently, companies not meeting any of the aforesaid criteria during the immediately preceding financial year are not required to ensure CSR related compliances[1].

However, Rule 3 (2) continues to provide a time frame of 3 consecutive financial years as an eligibility to discontinue ensuring compliance under Section 135. The said provisions have become redundant after enforcement of CAA, 2017. Relevant extract of HLC-CSR is as under:

“The Companies (Amendment) Act, 2017 has amended the eligibility criteria as being based on financial parameters of the ‘immediately preceding’ financial year instead of three immediately preceding financial years prevalent until then. Rule 3(2) of the Companies (CSR Policy) Rules, 2014 specifies that companies which cease to be eligible under Section 135(1) of the Act for three consecutive financial years shall not be required to comply with provisions of Section 135.

In view of the 2017 amendment, Rule 3(2) is redundant. “

Power of Central Government to revise thresholds

The Report of the Company Law Committee in 2019[2] based on the experience gained from the industry recommended the revision of the net worth/ turnover/ net profit thresholds specified in Section 135(1) from time to time to suit the changing requirements of the economy. The extracts of the committee note were;

“The Committee noted the merit in ensuring that static financial thresholds do not come in the way of corporate-driven socio-economic development and environmental conservation. In order to keep such revision process timely, the Committee recommended insertion of suitable provisions in the Section 135(1), which would enable the Central Government to enhance such limits by way of rules.”

However, the provisions of the Companies Act, 2013 do not provide for enabling power to the Central Government to revise the statutory thresholds framed 8 years back.

Conclusion

Prior to enforcement of CAA, 2017, the applicability was required to be ascertained based on the net-worth, turnover and net profits during any of the three preceding financial years. Therefore, Rule 3(2) of CSR Rules also provided a similar timeline for determining inapplicability of the CSR related provisions.

However, pursuant to amendment in Section 135 (1) by way of CAA, 2017 the Company is required to ascertain applicability by referring to the net-worth, turnover and net profits during the immediately preceding financial year. Accordingly, the inapplicability provided in Rule 3 (2) also was required to be aligned with amended Section 135 (1). Despite the deletion recommended by HLC-CSR, the provisions reflect under CSR Rules. Accordingly, companies need not wait till deletion of Rule 3 (2) as the same is anyways redundant post enforcement of amendment made in Section 135 (1).

Further, Rule 3 (1) of CSR Rules does not provide any additional clarity on the applicability and should be suitably amended. Lastly, enabling power to review static thresholds may also be inserted in Section 135 (1) of CA, 2013.

[1] https://www.mca.gov.in/Ministry/pdf/CSRHLC_13092019.pdf

[2] https://www.mca.gov.in/Ministry/pdf/CLCReport_18112019.pdf

Our other material on CSR can be accessed through the below link: