Archive for month: June, 2020

IBC and related reforms: Where do MSMEs Stand?

The MSME industry, colloquially referred to as the power engine of the economy has been a focal point of several reforms over the years. The recent reforms w.r.t. MSMEs and the Insolvency and Bankruptcy Code, 2016 (“Code’) has altered the stance of MSMEs, both as creditors and debtors. In this article, we shall discuss some significant reforms/ amendments w.r.t. MSMEs (due to COVID, or otherwise), and those under the Code and analyse the cumulative impact of these reforms on the sector in the prevailing scenario

Bringing pre-packs to India: a discussion on the way forward

“Pre-packs”, though yet to be born, have raised the expectations high. Reasons are obvious – the package is supposed to offer a lucrative combination of all the benefits of a ‘reorganisation/resolution plan’ as otherwise available only under formal insolvency proceedings with the added benefit of ‘speed’.

Pre-pack framework, as studies show, is not always contained in the statutory machinery. One of the close examples is UK. There the pre-pack arrangement is guided by insolvency practice statement, rather than a legislative framework.

In the Indian context, with some unique features, our insolvency regime stands differently from other jurisdictions – say, section 29A, and more importantly, section 32A.

Also, we already have certain debt restructuring tools in vogue – schemes of arrangement, and the apex bank’s framework for resolution of stressed framework. So, how do we welcome pre-packs, such that it serves the intended purpose? Surely enough, the pre-pack framework has to imbibe all the ‘good things’ which a formal insolvency framework has, and also offer something ‘over and above’ the existing options of debt restructuring.

The article sees these aspects and proposes what can be the optimal way of adopting pre-packs in India.

Covered bonds and the COVID disruption

-Vinod Kothari

Last year, the European Covered Bonds Council celebrated 250th anniversary of covered bonds[1]. That year also marked a substantial increase in global volumes of covered bonds issuance, which had been flat for the past few years. However, no one, joining the 250 years’ celebration, would have the COVID disruption in mind

With a history of more than 250 years now, covered bonds would have withstood various calamities and disruptions, both economic and natural, over the years. Covered bonds have not seen defaults over all these years. Will they be able to sustain the COVID disruption as well, given the fact that the major countries where they have been used extensively, have all suffered COVID casualties or infections, in varying degrees? In addition to the challenging credit environment, covered bonds will also be put to another question – does this device of refinancing mortgages in Europe hold the answer to sustaining continuous funding of home loans, thereby mitigating the impact of the crisis?

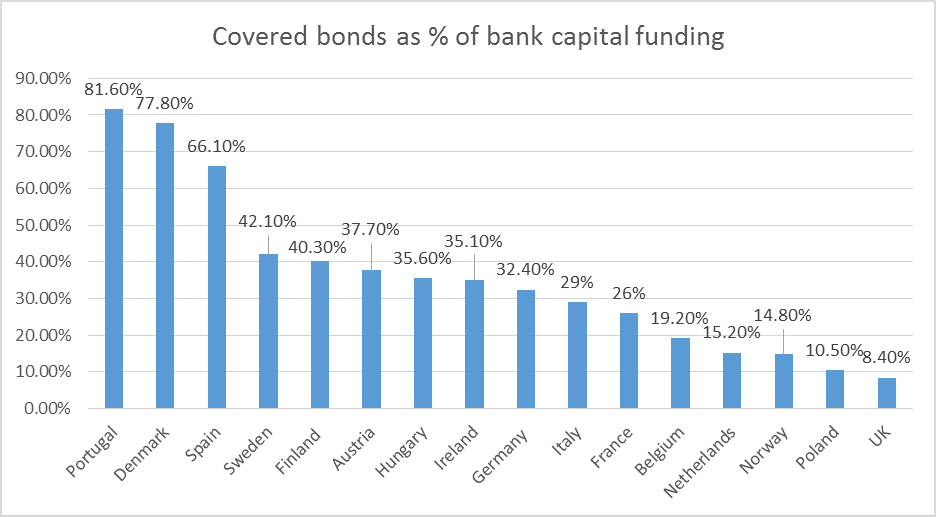

While, over the years, the instrument has been talked about (and less practiced) in lots of jurisdictions over the world, EU countries are still the bastion for covered bonds. About 82% of the world’s Euro 2.50 trillion dollar outstanding covered bonds are issued by EU entities.

European banks’ dependence on covered bond funding

European banks have a substantial dependence on covered bonds. Germany, where covered bonds have widely been regarded as a “fixture of German banking”, account for nearly 32% of the total capital market funding. In some countries, albeit with smaller bank balance sheets, the number goes up to as high as 78 – 81% [See Graph].

Figure 1 source: https://www.spglobal.com/_media/documents/spglobalratings_spglobalratings-coveredbondsprimer_jun_20_2019.pdf

If covered bonds were to prove resilient to the crisis, the investors’ confidence in these bonds, which have so had several regulatory privileges such as lower risk weights, will stand justified. On the other hand, if the bonds were to prove as brittle as some of their issuing banks, the claim to 250 years of unblemished vintage will be put to question.

Robustness of covered bonds

Covered bonds have a dual recourse feature – the issuer, and the underlying pool, in that order. Covered bonds are generally issued by mortgage-lending banks in Europe. Therefore, a default of covered bonds may occur only the issuing banks face the risk of default. Even if that were to happen, the extent of over-collateralisation in the cover pool may be sufficient to hold the bondholders safe. The recourse that the bondholders have against the loan pool is further strengthened by inherent support in a mortgage loan in form of the LTV ratio.

After the Global Financial Crisis and the introduction of Basel III norms, the capital of EU banks has generally strengthened. Data published by European Central Bank shows that European banks have a common equity tier 1 [CET 1] ratio of about 14.78%, as against the regulatory minimum of 4.5%. Therefore, the issuer banks seem to be poised to withstand pressure on the performance.

Past instances of default

Robustness of covered bonds is not the only factor which has kept them standing over all these years – another very important factor is sovereign support. European sovereigns have been sensitive to the important of covered bonds as crucial to maintain the flow of funds to the housing sector, and hence, they have tried to save covered bonds from defaulting.

In the period 1997 to 2019, out of covered bonds, there have been 33 instances of default by covered bond issuers, in various other on-balance sheet liabilities. However, these issues did not default on their covered bonds[2].

There are several regulatory incentives for covered bonds. Central banks permit self-issued covered bonds to be used as collateral for repo facilities. ECB also permits covered bonds as a part of its purchase program. In addition, there are preferential risk weights for capital requirements.

Rating downgrades in covered bonds correlate with sovereign downgrades

Rating agency Moody’s reports [16th April, 2020 report][3] that the potential for rating downgrades for covered bonds was strongly correlated with the ratings of sovereigns. “for countries with Aaa country ceilings, the average 12-month downgrade rate between 1997 and 2019 was 6.5% for covered bonds and 15.5% for covered bond issuers. However, in countries with lower country

ceilings, representing lower sovereign credit quality, the average 12-month downgrade rate increased to 24% for covered bonds and 25% for covered bond issuers”.

Rating agency Fitch also had a similar observation – stating that the rating downgrades for covered bonds were mostly related to sovereign downgrades, as in case of Greece and Italy.

Risk of downgrades in covered bonds

Risk of downgrades in covered bonds arises mainly from 2 reasons: weakening health of issuer banks, and quality of the underlying mortgage pools. Mortgage pools face the risks of reducing property prices, strain on urban incomes and increase in unemployment levels, etc. Over-collateralisation levels remain a strength, but unlike in case of MBS, covered bonds lean primarily on the health of the issuer banks. As long as the bank in question has adequate capital, the chances that it will continue to perform on covered bonds remain strong.

At the loan level, LTV ratios are also sufficiently resilient. Moody’s report suggests that in several jurisdictions, the LTV ratios for European covered bonds are less than 60%.

Additionally, in several European jurisdictions, the regulatory requirement stipulate non-performing loans either to be replaced by performing loans, or not to be considered for the purpose of collateral pool.

Unused notches of rating upliftment

A covered bond rating may rise by several notches, because of a combination of factors, including issuer resolution framework, jurisdictional support, and collateral support[4]. Either because of the strength of the pool, or because of the legislation support, or because of both. However, in any case the issuer’s credit rating is already strong, say, AAA, the notching up that could potentially have come has not been used at all. This is what is referred to as “unused notches”.

In order to assess the ability of covered bonds to withstand the pressure on the issuer bank’s rating will be the extent of unused notches of rating upliftment. In a report dated 25th March, 2020[5], rating agency S&P gave data about unused notches of rating upliftment of covered bonds in several jurisdictions. These ranged between 1 to 6 in many countries, thus pointing to the ability of the covered bond issuances to withstand rating pressures.

Conclusion

We are at the cusp of the disruption in global economies caused by the COVID pandemic. Any assessment of the impact of the crisis on capital market instruments may verge on being speculative. However, current signals are that the 250 years of history of performance does not face the risk of a collapse.

Links to our other resources on covered bonds –

http://vinodkothari.com/wp-content/uploads/Introduction-to-Covered-Bonds-by-Vinod-Kothari.pdf

vinodkothari.com/wp-content/uploads/covered-bonds-article-by-vinod-kothari.pdf

[1] 29th August, 1769, Frederick the Great of Prussia signed an order permitting the issuance of a landowners’ cooperative. It was in 1770 that the first German pfandbrief was issued. Going by this, the 250th anniversary should actually be this year.

[2] See Moody’s report here: https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBS_1117861

[3] https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBS_1221857

[4] Rating agency Standard and Poor’s, for example, considers at least 2 notches for resolution framework, three notches for jurisdictional support, and four notches for collateral support.

[5] https://www.spglobal.com/ratings/en/research/articles/200325-global-covered-bonds-assessing-the-credit-effects-of-covid-19-11402802

Transacting by exception: Listed cos in India give substantive carve outs for RPTs

The article has been published in ICSI – WIRC-E Newsletter (June-July 2020 edition):

Refer page 43 of ICSI – WIRC-E Newsletter

Webcasting in virtual AGM

by Smriti Wadehra & Qasim Saif

(smriti@vinodkothari.com) (executive@vinodkothari.com)

Background

MCA considering the COVID-19 pandemic and the social distancing norms issued by the Government, realized that conducting physical AGM by companies within the prescribed timeline shall be difficult for this financial year. Accordingly, the Ministry vide its circular dated 5th May, 2020 has permitted holding of Annual General Meetings (AGM) through video conferencing[1] for all meetings conducted during the calendar i.e. till 31st December, 2020. The said circular read with previous circulars dated 13th April, 2020[2] and 8th April, 2020[3] prescribed a detailed procedure as to how companies can conduct their general meetings virtually.

While these circulars dealt with various perplexities arising from the thought of virtual general meetings, however, there was still some clarification pending on applicability of other requirements applicable on companies, for instance, the requirement of webcasting under regulation 44(6) of SEBI (Listing Obligation and Disclosure Requirements) Regulation, 2015.

We discuss the same as below.

Webcast vs Video conferencing

The very basic differentiation in the term webcast and video conferencing is that, the former only provides one-way participation rights but the later provides for a two-way communication. In reference to providing webcasting facility during the AGM, the shareholders can only watch and listen to the proceedings of the meeting but cannot participate in voting or ask queries whereas in video conferencing the shareholders have complete participation as in case of a physical general meeting. Webcasting is merely “live streaming” of the AGM.

Intent of webcast

The requirement for providing webcast facility was recommended by Kotak Committee[4] on Corporate Governance which provided:

“Reg 44A. Meetings of shareholders

The top 100 listed entities by market capitalization, determined as on March 31 of every financial year, shall provide one-way live webcast of the proceedings of all shareholder meetings held on or after April 1, 2018”

The aforesaid recommendation was in addition to the recommendation w.r.t. e-voting facility which as per the existing provision of law, is closed at 5 p.m. of the previous day of the meeting, however, the committee recommended to shift the closure of e-voting facility to the day of meeting itself. The intent behind the recommendation was that the e-voting timeline expires before the meeting is held, accordingly, shareholders not attending the meetings in person are unable to take into account discussions at the meeting in order to make informed decisions.

Whereas, SEBI accepted the recommendations made by the Kotak Committee on 9th May, 2018 w.r.t. webcasting facility and inserted a new sub-regulation, however, the recommendation w.r.t e-voting is still in draft form. The provisions relating to webcast were made applicable to top 100 listed entities from 1st April, 2019.

The whole intent of conducting annual general meetings is the indispensable right to the shareholders of companies to meet the directors and auditors of the Company, at least once in a year. This has been the feature of corporate laws over the decades – based on the fact that the “managers” (directors) at least face the “owners” (shareholders) once. The law therefore, mandates physical meetings. However, with the rise of technology, call it necessity or evolution, the law embraced e-voting as a recognised means of voting (but not participation). Later, SEBI introduced the concept of providing one-way webcast facility for shareholders so as to increase participation of shareholders at meeting (though one-way).

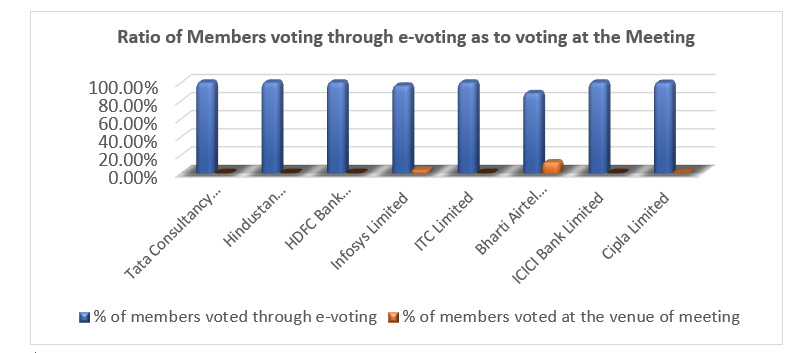

The data shows that attendance of shareholders at AGMs is even less than 5% of total number of shareholders at Meeting. Further, most of the shareholders (especially those residing in state other than where the AGM is conducted) find it more feasible to vote by way of e-voting. In the data[5] below, we can observe that on an average 95% of members of some well reputed companies vote through e-voting while on-site voting percentage is negligible. Therefore, it can be said, that the members do not really depend on meeting discussions to take a decision. However, webcast enables them to be apprised of the conduct of the meeting, shareholder queries, concerns, etc. raised at the meeting, etc.

Globally, countries like United States of America, Canada, United Kingdom, France, China and many such countries have permitted conducting meeting through video conferencing during the crisis. Further, the concept of webcasting is new for India. However, for many foreign countries including those named above have included providing of webcasting facility in shareholder’s meeting as a requirement of law.

Webcast facility in virtual AGM, whether required?

Now, the question is, where the AGM has itself gone ‘virtual’ (as mentioned above), is there really a requirement of webcasting? Note that SEBI has not provided any relaxation from webcasting as such.

It may be noted that video conferencing is nothing but participation through electronic means by shareholders remotely i.e. other than the venue of AGM. Therefore, where the company has already provided the facility of video conferencing to shareholders, webcast may not actually be needed. The purpose which the webcast intends to serve (dissipation of conduct of meeting) is well-served by the video-conferencing. In fact, in webcast the shareholders get only participation rights i.e. to hear and view the proceedings of meeting. However, in case of virtual AGM, the shareholders are provided with two-way participation rights i.e. can speak as well. Hence, provided two options, the shareholders will mostly opt for the latter.

The webcast, however, can be of relevance where the participation capacity is limited. In this regard, MCA circular dated 8th April, 2020 has prescribed minimum capacity allowance by companies conducting virtual AGM. For companies that are required to provide e-voting facility has to arrange capacity of minimum 1000 members at virtual AGM on first come first basis. This limit is minimum 500 members for companies not required to provide e-voting facility. Hence, the platform for conducting virtual AGM should provide for aforesaid minimum.

We all know that mostly large companies have lakhs of shareholders. Therefore, if companies restrict the entry of shareholders on first come first basis i.e. does not allow participation right to all shareholders in virtual AGM (due to software limitations, etc.), in that case webcast facility should be provided (if required). However, if companies do not restrict any shareholder from participation in virtual AGM and is open for all shareholders irrespective of the number, in such cases providing separate facility for webcast may turn out to be a futile exercise.

[1] http://www.mca.gov.in/Ministry/pdf/Circular20_05052020.pdf

[2] http://www.mca.gov.in/Ministry/pdf/Circular17_13042020.pdf

[3] https://www.mca.gov.in/Ministry/pdf/Circular14_08042020.pdf

[4] https://www.sebi.gov.in/reports/reports/oct-2017/report-of-the-committee-on-corporate-governance_36177.html

[5]Source: https://www.livemint.com/opinion/online-views/covid-19-need-to-re-look-at-pre-digital-era-compliances-under-companies-act-11588585274712.html

Presentation on Draft Directions on Securitisation of Standard Assets

Our related research on the similar topics may be viewed here –

- New regime for securitisation and sale of financial assets;

- Originated to transfer- new RBI regime on loan sales permits risk transfers;

- Comparison of the Draft Securitisation Framework with existing guidelines and committee recommendations;

- Comparison of the Draft Framework for sale of loans with existing guidelines and task force recommendations;

- Inherent inconsistencies in quantitative conditions for capital relief;

- Presentation on Draft Directions Sale of Loans;

- YouTube video of the webinar held on June 12, 2020.

Presentation on Draft Directions on Sale of Loans

Our related research on similar topics can be viewed here –

- New regime for securitisation and sale of financial assets;

- Originated to transfer- new RBI regime on loan sales permits risk transfers

- Comparison of the Draft Securitisation Framework with existing guidelines and committee recommendations;

- Comparison of the Draft Framework for sale of loans with existing guidelines and task force recommendations;

- Inherent inconsistencies in quantitative conditions for capital relief;

- Presentation on Draft Directions on Securitisation of Standard Assets;

- YouTube video of the webinar held on June 12, 2020.

Easing of DRF requirement

-by Smriti Wadehra

(smriti@vinodkothari.com)

-Updated as on 29th September, 2020

Pursuant the proposal of Union Budget of 2019-20, the MCA vide notification dated 16th August, 2019 amended the provisions of Companies (Share Capital and Debentures) Rules, 2014 [1].(You may also read our analysis on the notification at Link to the article) The said amended Rules faced a lot of apprehensions, especially, from the NBFCs as the notification which was initially expected to scrap off the requirement of creation of DRR for publicly issued debentures had on the contrary, rejuvenated a somewhat settled or exempted requirement of creation of debenture redemption fund as per Rule 18(7) for NBFCs as well.

As per the notification, the Ministry imposed the requirement for parking liquid funds, in form of a debenture redemption fund (DRF) to all bond issuers except unlisted NBFCs, irrespective of whether they are covered by the requirement of DRR or not. In this regard, considering the ongoing liquidity crisis in the entire financial system of the Country, parking of liquid funds by NBFCs was an additional hurdle for them.

Creation of DRR is somewhat a liberal requirement than creation of DRF, this is because, where the former is merely an accounting entry, the latter is investing of money out of the Company. Further, the fact the notification dated 16th August, 2019 casted exemption from the former and not from the latter, created confusion amidst companies. The whole intent of amending the Rule was to motivate NBFCs to explore bond markets, however, the requirement of parking liquid funds outside the Company as high as 15% of the amount of debentures of the Company was acting as a deterrent for raising funds by the NBFCs.

Considering the representations received from various NBFCs and the ongoing liquidity crunch in the economy of the Country along with added impact of COVID disruption, the Ministry of Corporate Affairs has amended the provisions of Rule 18 of Companies (Share Capital and Debenture) Rules, 2014 vide notification dated 5th June, 2020 [2]to exempt listed companies coming up with private placement of debt securities from the requirement of creation of DRF.

What is DRR and DRF?Section 71(4) read with Rule 18(1)(c) of the Companies (Share Capital and Debentures) Rules, 2014 requires every company issuing redeemable debentures to create a debenture redemption reserve (“referred to as DRR”) of at least 25%/10% (as the case maybe) of outstanding value of debentures for the purpose of redemption of such debentures. Some class of companies as prescribed, has to either deposit, before April 30th each year, in a scheduled bank account, a sum of at least 15% of the amount of its debentures maturing during the year ending on 31st March of next year or invest in one or more securities enlisted in Rule 18(1)(c) of Debenture Rules (‘referred to as DRF’). |

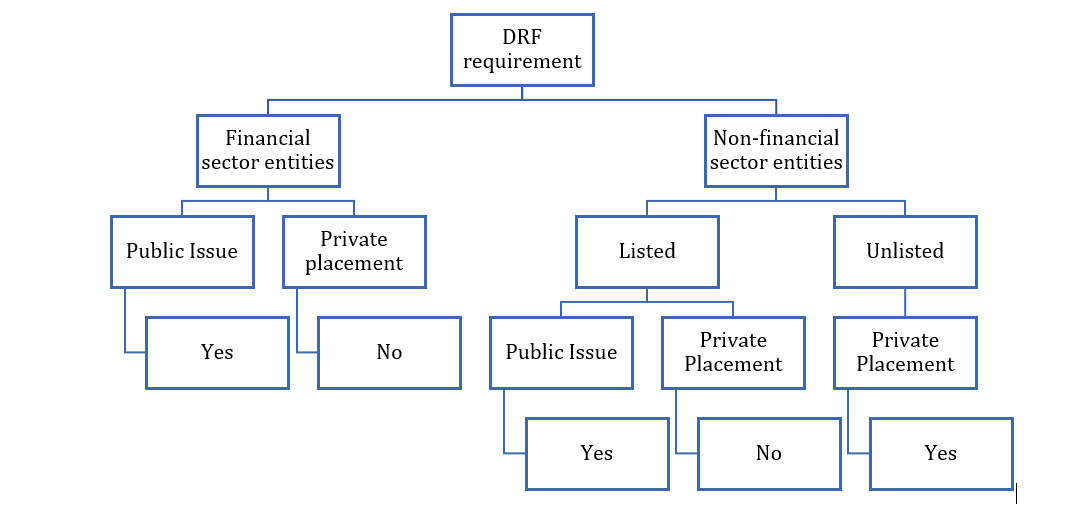

The notification has mainly exempted two class of companies from the requirement of creation of DRF:

- Listed NBFCs registered with RBI under section 45-IA of the RBI Act, 1934 and for Housing Finance Companies registered with National Housing Bank and coming up with issuance of debt securities on private placement basis.

- Other listed companies coming up with issuance of debt securities on private placement basis.

However, the unlisted non-financial sector entities have been left out. In a private placement, the securities are issued to pre-selected investors. Raising debt through private placement is a midway between raising funds through loan and debt issuances to public. Like in case of bilateral loan arrangements, but unlike in case of public issue, the investors get sufficient time to assess the credibility of the issuer in private placements, since the investors are pre-identified.

The intent behind DRF is to protect the interests of the investors, usually when retail investors are involved, with respect to their claims on maturity falling due within a span of 1 year. This is not the case for investors who have invested in privately placed securities, where the investments are made mostly by institutional investors.

Further, companies chose issuance through private placement for allotment of securities privately to pre-identified bunch of persons with less hassle and compliances. Hence, the requirement of parking funds outside the Company frustrates the whole intent.

Further, it is a very common practice to roll-over the bond issuances, hence, it is not that commonly bonds are repaid out of profits; the funds are raised from issuance of another series of securities. This is a corporate treasury function, and it seems very unreasonable to convert this internal treasury function to a statutory requirement.

Though, in our view, the relaxation provided in case of private issuance of debt securities is definitely a relief, especially during this hour of crisis, but we are not clear about the logic behind excluding unlisted non-financial sector entities.

Even though, the financial sector (76%) entities dominate the issuance of corporate bonds, however, the share of the non-financial sector entities (24%) is not insignificant. Therefore, ideally, the exemption in case of private placements should be extended to unlisted non-financial sector entities as well.

A brief analysis of the amendments is presented below:

Practical implication

Pursuant to the MCA notification dated 16th August, 2019, the below mentioned class of companies were required to either deposit or invest atleast 15% of amount of debentures maturing during the year ending on 31st March, 2020 by 30th April, 2020. This has been extended till 31st December, 2020 for this FY 2019-20 by MCA due to the COVID-19 outbreak. However, pursuant to the amendment introduced by MCA notification dated 5th June, 2020 the status of DRF requirement stands as amended as follows:

| Particulars | DRF requirement as MCA circular dated 16th August, 2019 | DRF requirement as per MCA circular dated 5th June, 2020 |

| Listed NBFCs which have issued debt securities by way of public issue | Yes. | Yes. Deposit or invest before 31st December, 2020 |

| Listed NBFCs which have issued debt securities by way of private placement | Yes | Not required as exempted. |

| Listed entities other than NBFC which have issued debt securities by way of private placement | Yes | Not required as exempted |

| Listed entities other than NBFC which have issued debt securities by way of public issue | Yes | Yes. Deposit or invest before 31st December, 2020 |

| Unlisted companies other than NBFC | Yes. | Yes. Deposit or invest before 31st December, 2020 |

Please note that the aforesaid shall be applicable from 12th June, 2020 i.e. the date of publication of the notification in the official gazette. In this regard, if for instance companies which have been specifically exempted pursuant to the recent notification, have already invested or deposited their funds to fulfil the DRF requirement may liquidated the funds as they are no longer statutorily require to invest in such securities.

Synopsis of DRR and DRF provisions[2]

A brief analysis of the DRR and DRF provisions as amended by the MCA notification dated 16th August, 2019 and 5th June, 2020 has been presented below:

| Sl. No. | Particulars | Type of Issuance | DRR as per erstwhile provisions | DRR as per amended provisions | DRF as per erstwhile provisions | DRF as per amended provisions |

| 1. | All India Financial Institutions | Public issue/private placement | × | × | × | × |

| 2. | Banking Companies | Public issue/private placement | × | × | × | × |

| 3.

|

Listed NBFCs registered with RBI under section 45-IA of the RBI Act, 1934 and HFC registered with National Housing Bank | Public issue | √

25% of value of outstanding debentures |

× | √ | √ |

| Private Placement | × | × | √ | × | ||

| 4. | Unlisted NBFCs registered with RBI under section 45-IA of the RBI Act, 1934 and HFC registered with National Housing Bank | Private Placement |

× |

× |

× |

× |

| 5.

|

Other listed companies | Public Issue | √

25% of value of outstanding debentures |

× | √ | √ |

| Private Placement | √

25% of value of outstanding debentures |

× | √ | × | ||

| 6. | Other unlisted companies | Private Placement | √

25% of value of outstanding debentures |

√

10% of the value of outstanding debentures |

√ | √ |

[1] http://www.mca.gov.in/Ministry/pdf/Circular_25032020.pdf

[2] This table includes analysis of provisions of DRR and DRF as per CA, 2013 and amendments introduced vide MCA notification dated 16th August, 2019 and 5th June, 2020.

Erstwhile provisions- Provisions before amendment vide MCA circular dated 16th August, 2019

Amended provisions- Provisions after including amendments introduced vide MCA circular 5th June, 2020

[1] https://www.mca.gov.in/Ministry/pdf/ShareCapitalRules_16082019.pdf