Use of digital platforms for tapping the early stage or ongoing funding is being seen more often than before, and quite obviously so, in a networked world where crowdsourcing and crowd placing of almost everything is the norm[1]. Several well-known platforms have been showcasing the immense potential to raise funds for start ups from either private equity investors, reaching very often to retail investors too. Some TV shows that showcase investing in start-ups have become the talk of the town; people who raised funding through these shows are seen as celebrities. In such an environment, if one opens the rulebook to say that crowdsourcing of funds by a company is a breach of the law and attracts huge penalties, one may be seen with disdain. However, one needs to note the provisions of sec. 42 (7) of the CA 2013, and five recent penalty orders of the RoC Delhi which, with detailed reasoning, has imposed stiff penalties running into crores for breach of these provisions.

This article explains what is the code of rules for private placements, what are the situations where this code may be breached, in what circumstances the RoC Delhi’s order found the practices legally untenable, etc. However, the author cannot close the article without discussing how start-ups with no past history or a balance sheet to present, but with a promising business plan, can still reach out to a group of people other than friends and families, because holding a different view will be to kill enterprise and innovation.

The Guidelines for Corporate Governance (‘2016 Guidelines’) for insurers in India have been around for close to a decade now. These Guidelines were initially brought as an update to the then 2009 Guidelines for the purpose of aligning the same with the extensive changes to the governance of companies brought about by the Companies Act, 2013. As such, the new Guidelines were framed to be mostly in line with the Act of 2013 except certain provisions such as requiring the CEO to be a WTD of the Board (where the chairman is NED), prescribing fit and proper criteria for directors, requiring certain additional committees, having only profit criteria for CSR applicability, etc.

Through the years, these Guidelines have served as a valuable source of direction in ensuring corporate governance for insurers; laying down guidance for the composition, roles and responsibilities of the Board, functions of various Board Committees, appointment and remuneration of KMPs, disclosures in financial statements, etc.

There has been a growing emphasis on sustainability across various sectors including finance, especially, with a growing mandatory requirement of disclosure of sustainability practices by companies around the world. Various sustainability-linked finance products are designed to promote the ESG objectives of the borrower while providing financial solutions.

Traditionally, loans have remained the most common way of raising finance, and sustainable finance is no exception to the same. These loans may be labelled as green loans, social loans, sustainable loans etc. Various organisations have issued voluntary guiding principles around the same[1]. A commonality in these loans is the restriction on the “use of proceeds” – that are directed towards the green, social or sustainable objectives of the borrower. Another form of sustainable finance through loans is Sustainability-linked Loans (SLLs), where the loan contains certain sustainability-linked terms. Contrary to typical green finance products, which allocate funds for designated green projects or assets, SLLs align the loan conditions with the sustainability performance of the borrower.

Other instruments of raising sustainable finance can be through the issuance of labelled bonds or GSS+ bonds. Read more about the same in our article – Sustainable finance and GSS+ bonds. One of the more recent innovative ways of financing sustainability objects of the borrower can be through Sustainability-linked derivatives.

March 21, 2024 (original article dated October 31, 2023)

SEBI Circular, effective 1st November 2023, required FPIs to provide the details of their beneficial owners without applying any threshold in the shareholding or on layers of intermediate entities until all the natural persons are identified. An enabling provision to this effect had also been inserted as Reg. 22(6) in SEBI (Foreign Portfolio Investors) Regulations, 2019 effective from 10th August 2023. SEBI vide circular dated 27th July, 2023, had also mandated all non-individual FPIs to obtain Legal Entity Identifier (LEI) number by 23rd January 2024[1]. However, LEI could not address the requirement of additional disclosures as the LEI data stops at the parent entity level and does not provide the details of natural persons in control of the entity.

As to what could be the trigger for these regulatory changes may be anybody’s guess, but tacitly, the SEBI circular dated 24th August, 2023[2] (Circular) introducing some significant changes in beneficial ownership details by FPIs, made several admissions. It seemingly admitted that the disclosure of beneficial ownership by FPIs took advantage of technicalities by structuring the holding of natural persons to less than 10%. It also admitted that several FPIs had concentric investments in a single corporate group, making it apparent that these FPIs were used as conduits for investing in a single entity, and therefore, there may be affiliation between the FPIs and the controlling shareholders.

Briefly stated, the changed norms required FPIs, which have either (a) 50% or more of their Indian equity AUM in a single corporate group; or (b) hold along with investor group more than INR 25,000 Crore of equity AUM in Indian markets, to disclose their beneficial ownership, drilled down to the natural person level, irrespective of the percentage of holding, unless eligible for exemption.

These requirements, though effective from 1st November 2023, gave a time frame of 90 calendar days for existing FPIs to re-adjust their holdings. Meaning, FPIs had time till 29th January 2024 to realign their investment within the threshold prescribed in order to avoid providing the details of the beneficial owner as required under the Circular. Post 29th January 2024, FPIs whose investment continued to exceed the threshold as mentioned above were required to disclose the details of beneficial owners within 30 trading days ending on 12th March 2024, which if not provided led to cancellation of the FPI registration license and in the interim, blocking of account for further purchase of equity securities and restricted voting rights in investee companies.

Mandatory Beneficial Ownership (‘BO’) disclosure

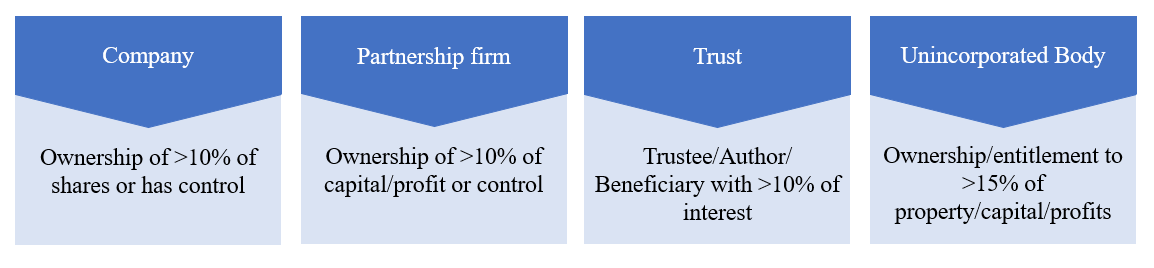

The new norms differed from the erstwhile norms, where BO disclosure was required if a natural person’s beneficial holding exceeded the threshold as prescribed under PML (Maintenance of Records) Rules 2005, as indicated below:

The new norms required mandatory disclosure of BO, irrespective of the percentage of holding by the BO. No matter how many layers of entities covered the identity of the BO, FPIs had to identify the natural persons holding any ownership, economic interest, or exercising control, if the FPIs fall in either of the 2 categories discussed below, unless exempted.

FPIs covered under the Circular

(a) Single Corporate Group focused FPIs:

If, instead of investing in a diverse pool of assets, an FPI has concentrated into a single corporate group, there are apparent concerns that the FPI is being used as a facade for making investments into a single entity. Thus, if on an AUM basis, more than 50% of the AUM of an FPI is in a “single corporate group”, the FPI has to provide the BO disclosure unless exempted (refer discussion below).

Intent: As per SEBI BM Agenda, the intent is to ensure there is no circumvention of minimum public shareholding norms or disclosures under SAST Regulations or investing funds routed through land border sharing countries and therefore, the need to obtain granular information around the ownership of, economic interest in, and control of FPIs with concentrated equity holdings in single companies or corporate groups.

Meaning of single corporate group: SEBI did not provide any clarity on single corporate group and left it to the stock exchanges/depositories. Rather than limiting to the existing law, BSE/NSE[3] identified a single corporate group more practically. Apart from entities having common control i.e. holding, subsidiary, associate, joint venture, and entities where promoters have major shareholding, entities which are mentioned on the website or in the annual report of the entity as a group company, have also been considered as a part of the group.

Basis this definition, BSE on its own identified the companies forming part of a single corporate group and asked the listed entities to confirm the name of the group as identified by BSE by sending communication in terms of Para 16 of the SEBI Circular that requires Stock exchanges/ Depositories to maintain a repository containing names of companies forming a part of each single corporate group and disseminate the same publicly on their websites[4].

(b) Large sized FPIs:

FPIs with an AUM of more than INR 25,000 crore, either individually or along with their investor group[5], may pose a systematic risk in the Indian markets. It will be more concerning if such FPIs are tacitly controlled by unfriendly nations, and therefore, SEBI mandated BO disclosure from such FPIs too.

Intent: As per SEBI BM Agenda, the intent was to examine from the perspective of DPIIT Press Note 3 of April 17, 2020 (although not applicable to FPI investments), if the FPI route could potentially be misused to circumvent the stipulations of the same and disrupt the orderly functioning of Indian securities markets by their actions by having a substantial number of investors from countries that share land borders with India. It is likely that the FPI with a large Indian equity portfolio may itself be situated out of a non–land bordering country, the first level/ intermediate investors in such FPIs may be based out of land–bordering countries. This reiterated the need to obtain granular information around the ownership of, economic interest in, and control of such FPIs.

Exemption from BO disclosure

Single Corporate Group (‘SCG’) focused FPIs

Investment in SCG is insignificant compared to global investment

There might be cases where the FPI has taken exposure over an SCG only, however, may have investments globally as well and the percentage of Indian investments might be quite less when compared with its overall global investment. In such a scenario, there are fewer chances of FPIs being used as a conduit for avoiding compliance or hiding the identity of the BO. Therefore, the FPIs which are holding more than 50% of their Indian AUM in an SCG and such investments are less than 25% of their global AUM, are exempt from providing the BO disclosure.

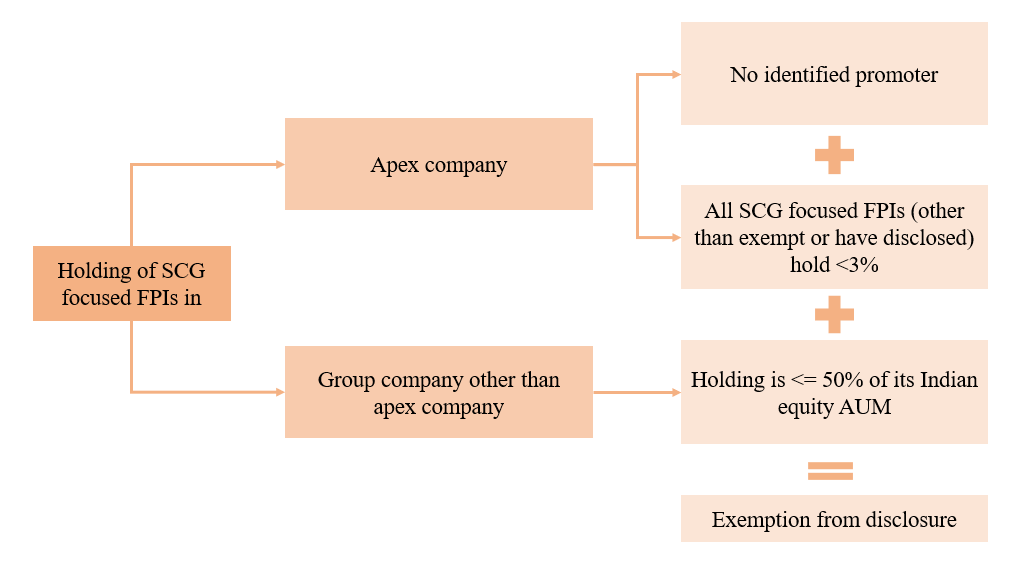

No identified promoter in SCG

SEBI vide circular[6] dated 20th March, 2024, further exempted SCG focused FPIs meeting the following conditions:

The apex company does not have identified promoter;

Such FPI holds not more than 50% of its India equity AUM in the corporate group, after excluding its holding in the apex company with no identified promoter.

The composite holdings of all such FPIs (having SCG exposure) in the apex company with no identified promoter, is less than 3% of its total equity share capital,

Intent: As per the Consultation Paper the intent is that if FPI has exposure in SCG with no identified promoter in the apex company, there is no risk of circumvention of minimum public shareholding provision and may be exempted from the disclosure requirement. Further, there is a possibility that even though the apex company itself has no identified promoter, the FPI might still hold a significant part of its portfolio in group companies that have an identified promoter and therefore if their holding in the group is not significant exemption can be granted.

Figure 2: Exemption from disclosure requirement in case there is no promoter in SCG

Large sized FPIs,

FPIs whose Indian AUM is more than INR 25,000 crore and their investments in India are less than 50% of their overall global investments are exempt from providing such disclosure since the probability of such FPIs being used as a facade to obtain control over Indian markets is quite less.

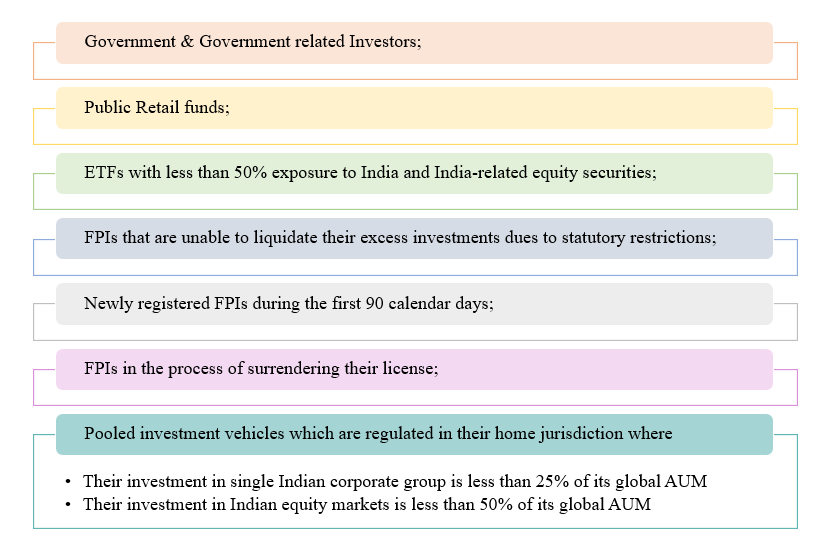

General Exemption

FPIs that have a wide investor base or are backed by the government or government related investors do not pose any risk to Indian markets or the probability is quite low, and therefore the following categories of FPIs are exempt from providing BO disclosure. Also, if the investors in FPI fall under the below mentioned categories, then identification of BO for such investors will not be required. In case the constituents of Large sized FPIs fall under below mentioned category, their holding will also not be aggregated with their investor group to calculate the limit of Rs. 25,000 Crore.

Figure 3: List of exempted FPI

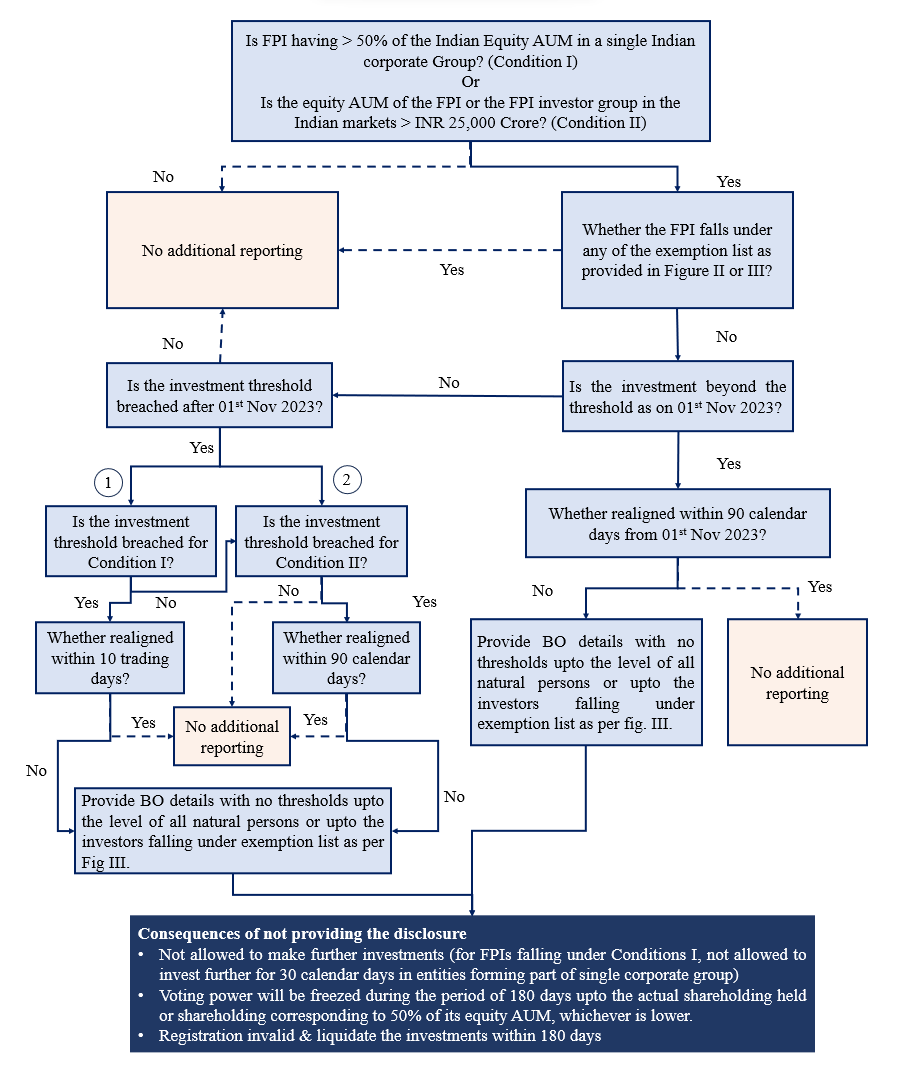

The below figures provide a gist of the scenarios where FPIs are required to provide the disclosure

Figure 4: Flowchart depicting the scenarios that would warrant additional disclosures

Responsibility of DDPs/Depository

The FPIs are put under the obligation to ensure compliance with the SEBI Circular, i.e. providing the BO disclosure and monitoring the concentration limit in a single corporate group and the equity investments in India. Additionally, DDPs are also required to monitor the same and intimate the FPIs wherever they breach the criteria and once the registration of FPI is invalidated as a result of non-disclosure, the Depository will intimate the investee listed company to freeze the voting rights of such FPIs to the extent of actual shareholding or shareholding corresponding to 50% of its equity AUM on the date its FPI registration is rendered invalid, whichever is lower (refer the example below).

To ensure that there is no regulatory arbitrage amongst DDPs, a standard operating procedure (SOP)[7] has been framed & followed by all the DDPs to independently validate the conformance of FPIs with the conditions and exemptions prescribed. The SOP is based on the application of the core principles of minimising Type II errors i.e. where legitimate FPIs and their investors face challenges of onerous regulatory requirements) without adding to Type I errors i.e., where FPIs that may be breaching regulations, circumvent the need to make disclosures that would bring such breaches to light, through the ‘trust – but verify’ route.

Responsibility of a Listed Entity

The FPIs whose registration is rendered invalid as a result of non-disclosure are restricted from casting their vote and it is the responsibility of investee listed company to ensure that the voting rights of such FPIs are freezed to the extent of actual shareholding or shareholding corresponding to 50% of equity AUM on the date its FPI registration is rendered invalid, whichever is lower. The said information will be provided by the depository to the investee listed entity/its RTA. The following example clarifies calculation of extent of shareholding to be freezed.

Eg. FPI XYZ has 60 shares of Company A and 40 shares of Company B as on May 13, 2024, and the FPI fails to make the additional disclosures, thereby rendering its FPI registration invalid from May 13, 2024. Thereafter, FPI’s voting rights shall be restricted to shareholding corresponding to 30 shares of Company A and 20 shares of Company B.

Suppose as on July 01, 2024, the FPI has liquidated some shares and holds 15 shares of Company A and 30 shares of Company B. As on this date, the FPI will be able to exercise voting rights corresponding to 15 shares of Company A but only 20 shares of Company B (maximum permissible voting rights in Company A).[8]

The listed entities were required to intimate the details of their corporate group to the stock exchanges and any change is to be intimated within 2 working days of the effective date of such change[9].

The non-compliant FPIs are also restricted from purchasing further equity shares, however, the responsibility is not upon the listed entity to not issue equity shares to such FPIs. The DDPs/Custodian will block the account of FPIs for further purchases and they cannot participate in any corporate action which increases the equity shareholding such as rights issue, FPOs, etc. However, credit as a result of any involuntary corporate actions such as bonus issue, scheme of arrangement, etc will be allowed.

Conclusion

SEBI had stated that there cannot be sustained capital formation without transparency and trust. The Circular is a move to foster trust and increase transparency in the Indian Capital markets. The Circular does not seem to be a hindrance to genuine FPIs, though operational challenges might be faced by the FPIs in identifying the BOs.

[1] 180 days from the date of issue of the SEBI Circular.

[2] The said circular was approved in the SEBI Board meeting dated 28th June, 2023

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Prapti Kanakiahttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngPrapti Kanakia2024-03-22 13:33:522024-03-22 13:38:03Single Corporate Group focused FPIs & Large value FPIs to disclose granular details of beneficial ownership

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-03-21 23:19:472024-03-22 11:42:41Fractional property shares: Come either as Small REIT, or wind up

Navigating the world of fundraising for startups is no easy feat. This becomes all the more challenging for a pre-revenue start-up which cannot have a valuation. Amongst the several fundraising options available to a start-up, one of the budding and lesser-known sources happens to be iSAFE.

Origin

iSAFE, short for, India Simple Agreement for Future Equity, was first introduced in India by 100X.VC, an early-stage investment firm. This move was inspired by US’s ‘Simple Agreement for Future Equity (‘SAFE’)’, an alternative to convertible debt and the brainchild of an American start-up incubator. SAFE is a financing contract between a startup and an investor that grants the investor the right to acquire equity in the firm subject to specific activating events, such as a future equity fundraising.[1]

So far as the success of SAFE in India is concerned, being neither debt (since they do not accrue interest), nor equity (since they do not carry any dividend or shareholders’ rights) or any other instrument, it could not carve its place in India and was cornered as a mere contingent contract with low reliability and security. On the contrary, iSAFE happened to be the game changer in the Indian context, being a significantly modified version of SAFE.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00mahakagarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngmahakagarwal2024-03-21 11:10:152024-03-21 11:10:16The iSAFE option to start up funding: Legality and taxation

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-03-17 22:55:342024-03-17 23:17:18SEBI approves uniform approach for market rumour verification, eases on-going compliance requirement for listed companies, eases norms for IPO/ fund raising, AIFs, relaxes requirement for FPI & extends timeline for HVDLE on March 15, 2024

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-03-15 11:54:232024-04-11 10:50:27Mandatory bond issuance by Large Corporates: FAQs on revised framework

In a recent Supreme Court ruling in the matter of Association for Democratic Reforms & Anr. v/s Union of India, Electoral Bond Scheme (EBS/ Scheme) was declared as unconstitutional, including certain amendments to section 182 of the Companies Act, 2013 (“CA”), amended vide the Finance Act, 2017 as arbitrary and violative of the Constitution of India (COI).

Naturally, a question arises: What is wrong? Contributions to political parties? No. It is only the opacity of the recipient which has been hit. Hence, if companies have contributed, they couldn’t have kept a shroud of secrecy over the same.

Two, if companies had to disclose, and the amendments on 2017 are now junked, does it mean companies have to go back and disclose? It doesn’t seem so. In fact, the apex court itself has taken care of the actionables and put the burden of disclosure on the Election Commission of India (ECI).

Corporate houses, apparently, the largest contributors to electoral bonds, have expressed concerns on what will be the implications of the ruling on donor companies. Several questions arise – What has been declared unconstitutional and what is still valid? What would be the fate of the political donations already made? What actionables arise on a company having made donations to political parties through electoral bonds or otherwise? In this write-up, the author has attempted to analyze the same in light of the 232-pager ruling.

Section 182 of CA – Pre and Post Finance Act 2017

In order to understand what has been rendered unconstitutional and why, let us analyse the provisions of section 182 of CA as it stood prior to the amendment pursuant to Finance Act 2017 v/s how it stands today.

Particulars

Position prior to Finance Act, 2017

Position post Finance Act, 2017

Whether unconstitutional as per SC ruling?

Limits on political contribution – Proviso to Sec 182(1)

Aggregate value of contribution to political parties cannot exceed 7.5% of 3-years’ average net profits

No maximum limit on political contributions

Yes. The SC concluded removal of limits to be “manifest arbitrariness” for removing a classification without recognising the harms thereof.

Disclosure in financial statements – Section 182(3)

Contributor company to disclose names of each parties against the total amount contributed to such parties

Only total amount contributed to be disclosed, without disclosing names

Yes. The SC concluded this to be an “essential” information for effective exercise of voting, and hence, non-disclosure as an infringement to the right of information of voter under Article 19(1)(a) of COI

Mode of contribution – Section 182(3A)

New insertion pursuant to Finance Act

Political contributions to be made only through banking channels (account paying cheque/ bank draft/ ECS) and through instruments issued under a scheme for political contributions (electoral bonds)

No impact. However, the Electoral Bond Scheme has been declared to be unconstitutional.

Consequences for donor companies

The SC ruling does not declare “political donations” per se as unconstitutional or invalid, what is rendered violative of constitutional rights is the Electoral Bond Scheme and the amendments to section 182 of CA vide Finance Act, 2017 permitting unlimited and anonymous contributions to political parties.

The legal implications of declaring a statute unconstitutional has been discussed in various rulings in the past, such as, reBehram Khurshid Pesikaka v. State of Bombay, and others. These say the consequences are dealt with by the court only. In the present matter of Electoral Bond Scheme, the SC has directed SBI and the Election Commission of India to disclose the details of contributions received through electoral bonds, and refund the non-encashed amounts to the donor.

In essence it does not seem apt that any burden will be cast upon companies for going by a law which was valid till it was scrapped. Hence, no adverse implications should follow for the donor companies. However, for the sake of its corporate duty, a company which has contributed in the past may now do a disclosure in the forthcoming annual report. Thus, The omission of disclosure of particulars of political donations made along with names of the parties, between FY 2017-18 to FY 2022-23, may be made good by companies in the financial statement for the FY 2023-24 giving details of contribution made along with names of the political parties for each of the previous financial years, along with the current FY 23-24.

Principle of “manifest arbitrariness”

Having reference to various rulings and judicial precedents, the SC has summarized that the doctrine of “manifest arbitrariness” can be imposed to strike down a provision. Such a proposition can be applied where:

the legislature fails to make a classification by recognizing the degrees of harm, and

the purpose is not in consonance with constitutional values.

In the context of permitting unlimited contribution to political parties, on the grounds of removing classification between donations by “individuals” v/s “companies”, or between “loss making companies” and “profit making companies”, the degree of potential harm has been ignored. Section 182 was enacted to curb corruption in electoral financing, however, the amendment allowed companies, incorporated for a specific purpose as per their MoA, to contribute unlimited amounts to political parties without any accountability and scrutiny. This may also facilitate incorporation of “shell companies” solely for the purpose of making such political contributions and permit undue influence of companies in the electoral process, thus violating the principle of free and fair elections and political equality.

The hon’ble SC has ruled the deletion of maximum limit as “violative” of COI and “manifestly arbitrary” for not recognising the degrees of harm in removing the classification between –

Political donations by “companies” and “individuals” where the ability to influence electoral process is much higher with the former, since “Contributions made by individuals have a degree of support or affiliation to a political association. However, contributions made by companies are purely business transactions, made with the intent of securing benefits in return.”

“Profit-making” and “loss-making companies” for the purposes of political contributions, since “it is more plausible that loss-making companies will contribute to political parties with a quid pro quo and not for the purpose of income tax benefits.”

The present SC ruling quashes the anonymous political donations and the amendments in CA permitting unlimited corporate donations to political parties. Political donations are not unconstitutional, however a company, making such donations, shall ensure the same does not result into emptying the resources of the company while also ensuring transparency in disclosure of such political donations in its financial statements for the right of information of the concerned shareholders as well as larger stakeholder and voter base.