Regulatory round up: Corporate Law updates for the year 2023

Loading…

Loading…

| Regulatory round-up 2023: Link to YouTube videos | ||

| Part I | Listing Regulations | https://www.youtube.com/watch?v=RJbGM9AGu2Y |

| Part II | SEBI Regulations and other miscellaneous regulatory developments | https://www.youtube.com/watch?v=UTuEgXAkYW0 |

| Part III | MCA | https://www.youtube.com/watch?v=luRn7NcI_PU |

| Part IV | SEBI amendments relating to corporate debt | https://www.youtube.com/watch?v=u2FGSfsyQOM |

| Part V | Regulatory round-up for NBFCs | https://www.youtube.com/watch?v=H82D3t38nio |

Felicitation Meet and Panel Discussion on Corporate Governance – from 1988 to Now

Loading…

Snippet on credit of existing & issue of new units of AIFs in demat form

Sanya Agrawal | corplaw@vinodkothari.com

Loading…

Presentation on Significant Beneficial Owners (for companies & LLPs)

Team Corplaw | corplaw@vinodkothari.com

Loading…

Our article corner on SBO: https://vinodkothari.com/article-corner-on-sbos/

Checklist for change in share transfer agent

Anushka Vohra, Senior Manager & Ankit Singh Mehar, Executive | corplaw@vinodkothari.com

Loading…

SEBI Consultation Paper (CP) to ease trading plans by company insiders

Sanya Agrawal | corplaw@vinodkothari.com

Loading…

Our detailed article on the topic can be read here

Link to our PIT resource centre: https://vinodkothari.com/prohibition-of-insider-trading-resource-centre/

SEBI proposals to ease trading plans by company insiders

-Consultation paper proposes to rationalise the existing framework under insider trading

Anushka Vohra | Senior Manager

corplaw@vinodkothari.com

Background

The concept of trading plan was introduced for the first time in the SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’). The rationale for introducing the same, as indicated in the Report of the High Level Committee constituted for the purpose of reviewing the erstwhile 1992 Regulations, chaired by Mr. N.K. Sodhi, was that there may be certain persons in a company who may perpetually be in possession of UPSI, which would render them incapable of trading in securities throughout the year. The concept of trading plan would enable compliant trading by insiders without compromising the prohibitions imposed in the PIT Regulations.

Trading plan means a plan framed by an insider (and not just a designated person) for trades to be executed at a future date. Trading plan is particularly suitable for those persons within the organization, who may by way of their position, seniority or any other reason, be in possession of UPSI at all times. Since, the PIT Regulations prohibit trading when in possession of UPSI, trading plans are an exemption to such prohibition. In order to ensure that the insiders while formulating the trading plan do not have possession to UPSI, cooling-off period of 6 months has been prescribed in the PIT Regulations. As per Reg. 5(1) of the PIT Regulations, the trading plan has to be presented before the compliance officer of the company for approval. As per sub-regulation (3), the compliance officer has to review the trading plan and assess for any violation of the PIT Regulations. If at the time of formulation of trading plan, there was no UPSI or later on a new UPSI was generated, then the trading can be carried out as per the trading plan, even if the new UPSI has not been made generally available.

When the trades are executed as per trading plan, certain provisions of the PIT Regulations are exempted viz. trading window restrictions, pre-clearance of trades and contra trade restrictions.

SEBI has issued a Consultation Paper on November 24, 2023 for inviting public comments on the recommendations of the Working Group (‘Report’) to review provisions related to trading plans.

This article discusses the proposed amendments to the framework of the trading plan as mentioned in the Consultation Paper.

Challenges in the present framework

The Report discusses that during the last 5 years only 30 trading plans have been submitted annually by the insiders, which indicates that the trading plans are not very popular.

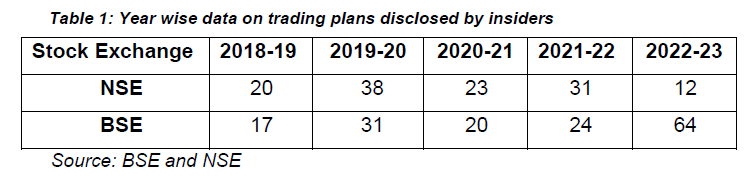

The year wise data on trading plans as mentioned in the Report is given below:

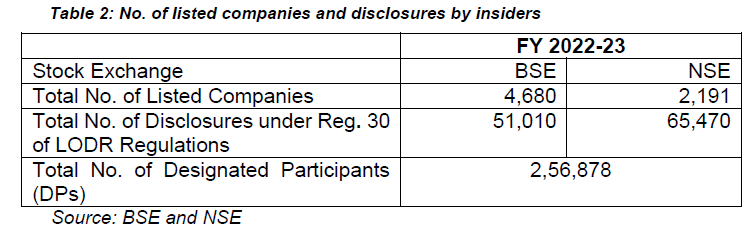

The data w.r.t. number of listed companies and DPs during FY 2022-23 is also given below:

The above clearly shows that during FY 2022-23, the number of designated persons among the listed companies was around 2,56,878 and there were only infinitesimal trading plan received by the exchange(s).

Further, the five features of the trading plan as highlighted in the Report are as under:

(i) can be executed only after 6 (six) months from its public disclosure;

(ii) are required to cover a period of at least 12 (twelve) months;

(iii) must be disclosed to the stock exchanges prior to its implementation (i.e., actual trading);

(iv) are irrevocable; and

(v) cannot be deviated from, once publicly disclosed.

As evident from above, while the concept has been into existence since 2015, trading plans have not been very popular owing to certain restrictive conditions viz. mandatory execution of the same even if the market prices are unfavorable for an insider, inability to trade for a reasonable period around the declaration of financial results and mandatory cooling off period of 6 months etc.

Proposed amendments

- Cooling-off period

Cooling-off period means gap between the formulation and public disclosure of the plan and actual execution of the plan. Reg. 5(2) of the PIT Regulations presently provides a cooling-off period for 6 months as the period of 6 months was considered reasonable for the UPSI that may be in the possession of the insider while formulating the trading plan to become generally available or any new UPSI to come into existence.

This period is proposed to be reduced to 4 months. The Report states that as per the current requirement, the insiders have to plan their trade 6 months ahead which may not be favorable, considering the volatility in the markets. It was proposed to either reduce the period or to do away with it.

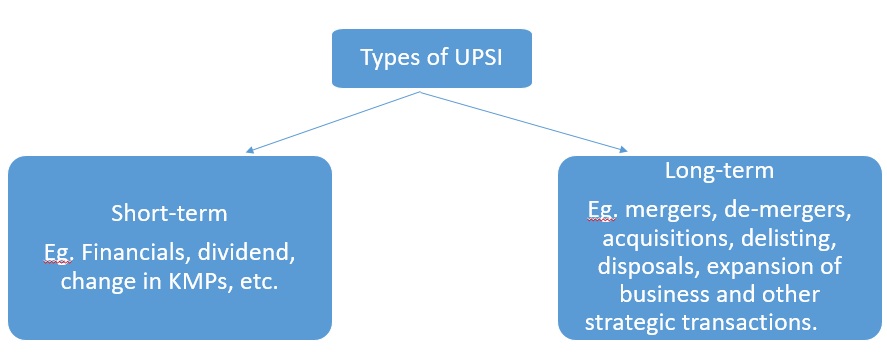

The Report classifies UPSI into two types; short-term UPSI and long-term UPSI to ascertain the time within which the UPSI is expected to become generally available.

The Report further highlights that in case of short-term UPSI, a period of 4 months would be sufficiently long for it to become generally available.

In case of long-term UPSI, the Report refers back to proviso to Reg. 5(4) according to which the insider cannot execute the trading plan if the UPSI does not become generally available.

The Report also gives reference to the cooling-off period for trading plans in the US, where SEC introduced the cooling-off period only in December 2022.

- Minimum coverage period

Reg.5(2)(iii) states that a trading plan shall entail trading for not less than 12 months. A period of 12 months was specified to avoid frequent announcements of trading plans. This again provides a very long period for insider to execute their trading. This period is proposed to be reduced to 2 months.

- Black-out period

As per Reg 5(2)(ii), trading plan cannot entail trades for the period between the twentieth trading day prior to the last day of any financial period for which results are required to be announced by the issuer of the securities and the second trading day after the disclosure of such financial results. This period is known as the black-out period.

The Report states that this period forms a significant part of the year, considering 4 quarters and hence it is proposed to omit the same.

The Report also discusses the potential concerns that may arise on removing the black-out period. The Working Group noted that the same is addressed by the cooling-off period and non alteration of plan once approved and disclosed.

- Price limit

As per Reg. 5(2)(v) of the PIT Regulations, the insider can set out either the value of trades to be effected and the number of securities to be traded along with the nature of the trade, intervals at, or dates on which such trades shall be effected.

The Working Group noted that there was no price limit that the insider could mention. The Report recommends a price limit of 20%, up or down of the closing price on the date of submission of the trading plan.

- Irrevocability

As per Reg. 5(4), the trading plan once approved shall be irrevocable and the insider will have to mandatorily implement the plan without any deviation from it. This puts the insider in a disadvantageous position as he has to execute the trades (buy / sell) even when the price is not favorable.

As per the proposed amendment, where the price of the security is outside the price limit set by the insider, the trade shall not be executed. The plan will be irrevocable only where no price limit is opted for.

- Exemption from contra-trade restrictions

As per Reg. 5(3) of the PIT Regulations, restrictions on contra trade are not applicable on trades carried out in accordance with an approved trading plan.

The Working Group deliberated that it is difficult to envisage a reasonable and genuine need for any insider to plan two opposite trades with a gap of less than 6 months. The Report states that the insider may misuse the exemption for undertaking a contra position. Therefore, the exemption is proposed to be omitted.

- Disclosure of trading plan: timeline & content

As per Reg. 5(5), upon approval of the trading plan, the compliance officer has to notify the plan to the stock exchange(s). However, presently there is no specific timeline indicated. The Working Group recommends disclosure within 2 trading days of the approval of the plan. Further, it recommends disclosure of the price limit as well.

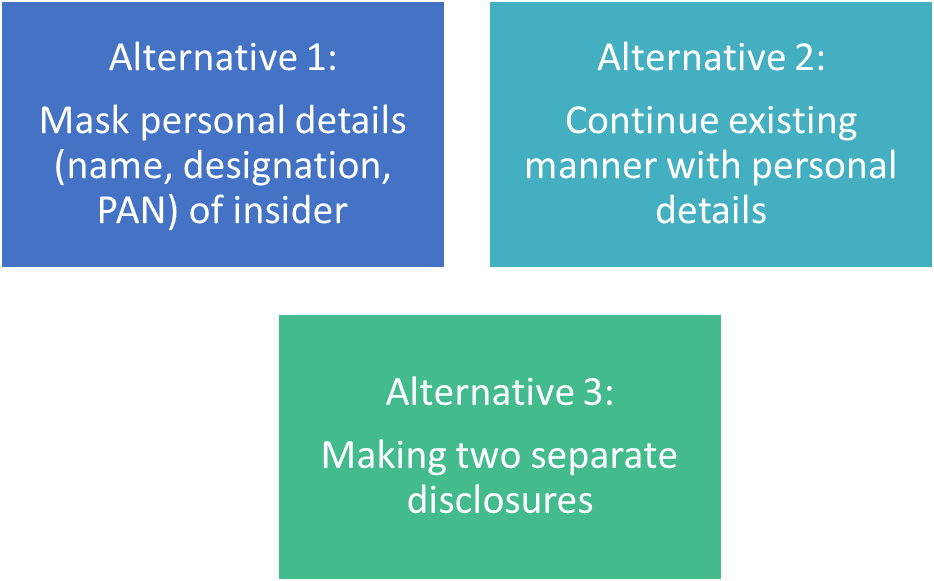

While the format of the trading plan will be rolled out basis discussion with the market participants, the Consultation Paper, basis the recommendations of the Working Group on protecting the privacy of the insiders by masking the personal details, discussed three alternatives of disclosure, as under:

It was discussed that disclosing personal details of the insiders publicly may raise privacy and safety concerns for senior management and insiders and not disclosing personal details to the stock exchange(s) would lead to misuse / abuse of trading plans by other insiders. That is, a trading plan submitted by one person may instead be used by someone else.

Having discussed the above, the Consultation Paper suggests alternative 3 i.e. making two separate disclosures of the trading plan; (i) full (confidential) disclosure to the stock exchange and (ii) disclosure without personal details to the public through stock exchange. Further, these separate disclosures may have a unique identifier for reconciliation purposes.

Concluding remarks

The proposed amendments indicate a welcome change as it attempts to plug the gaps prevalent in the erstwhile framework and offers flexibility to the insiders. At the same time, the Compliance officer will have to remain mindful of any scope for potential abuse by the insiders, while approving the same.One will have to await the actual amendment, basis the receipt of public comments, to ascertain if trading plans are all set to become popular and more frequent.

Our resources on the topic:

Link to our PIT resource centre: https://vinodkothari.com/prohibition-of-insider-trading-resource-centre/