Navigating the world of fundraising for startups is no easy feat. This becomes all the more challenging for a pre-revenue start-up which cannot have a valuation. Amongst the several fundraising options available to a start-up, one of the budding and lesser-known sources happens to be iSAFE.

Origin

iSAFE, short for, India Simple Agreement for Future Equity, was first introduced in India by 100X.VC, an early-stage investment firm. This move was inspired by US’s ‘Simple Agreement for Future Equity (‘SAFE’)’, an alternative to convertible debt and the brainchild of an American start-up incubator. SAFE is a financing contract between a startup and an investor that grants the investor the right to acquire equity in the firm subject to specific activating events, such as a future equity fundraising.[1]

So far as the success of SAFE in India is concerned, being neither debt (since they do not accrue interest), nor equity (since they do not carry any dividend or shareholders’ rights) or any other instrument, it could not carve its place in India and was cornered as a mere contingent contract with low reliability and security. On the contrary, iSAFE happened to be the game changer in the Indian context, being a significantly modified version of SAFE.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00mahakagarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngmahakagarwal2024-03-21 11:10:152024-03-21 11:10:16The iSAFE option to start up funding: Legality and taxation

This quote by Beethoven remains relevant today, not only within the music industry but also in the realm of finance. In the continually evolving landscape of finance, innovative strategies emerge to monetize various assets. One such groundbreaking concept gaining traction in recent years is music royalty securitization. This financial mechanism offers investors a unique opportunity to access the lucrative world of music royalties while providing artists and rights holders with upfront capital.

The roots of this innovative financing technique can be traced back to the 1990s when musician David Bowie made history by becoming the first artist to securitize his future earnings through what became known as ‘Bowie Bonds’. This move not only garnered attention but also paved the way for other artists to follow suit. Bowie Bonds marked a significant shift in how music royalties are bought, sold, and traded.

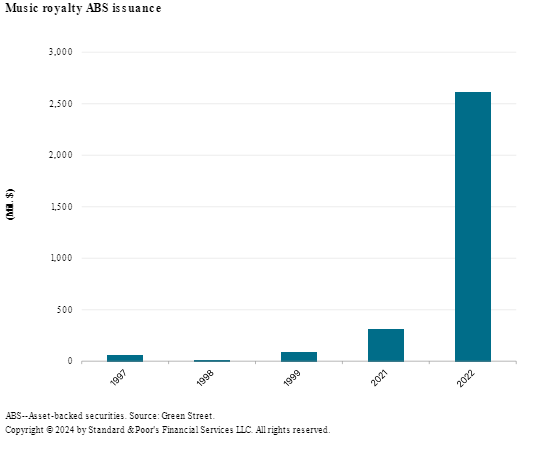

As per the S&P Global Ratings[1], the issuance of securities backed by music royalties totaled nearly $3 billion over the two-year span 2021-22. The graph below shows a recent surge in issuance of securities backed by music royalties.

Data showing the growth of Music Royalty Securitization

This article discusses music royalty securitization, its mechanics, benefits, challenges along with implications for the music industry.

Understanding Music Royalties:

Before exploring music royalty securitization, it’s essential to understand the concept of music royalties. In the music industry, artists and rights holders earn royalties whenever their music is played, streamed, downloaded, or licensed for use. These royalties are generated through various channels, including digital platforms, radio, TV broadcasts, live performances, and synchronization licenses for commercials, movies, and TV shows. However, it’s important to note that artists only earn royalties when their music is utilized, whether through sales, streaming, broadcasting, or live performances.

As a result, the cash flows from these royalties being uncertain are received over time and continue to be received for an extended period. Consequently, artists experience a delay in receiving substantial amounts from these royalties, sometimes waiting for several years before seeing significant income.

The Birth of Music Royalty Securitization:

Securitization involves pooling and repackaging financial assets into securities, which are then sold to investors. The idea is to transform illiquid assets, such as mortgage loans or in our case, music royalties, into tradable securities. Music royalty securitization follows a similar principle, where the future income generated from music royalties is bundled together and sold to investors in the form of bonds or other financial instruments.

Future Flows Securitization:

Music royalty securitization is a constituent of future flows securitization and therefore before discussing the constituent, it is important to discuss the broader concept of future flows securitization.

Future flows securitization involves the securitization of future cash flows derived from specific revenue-generating assets or income streams. These assets can encompass a wide range of future revenue sources, including export receivables, toll revenues, franchise fees, and other contractual payments, even future sales. By bundling these future cash flows into tradable securities, issuers can raise capital upfront, effectively monetizing their future income. Future flows securitization differs from the traditional asset backed securitization by their very nature as while the latter relates to assets that exist, the former relates to assets that are expected to exist. There is a source, a business or infrastructure which already exists and which will have to be worked upon to generate the income. Thus, in future flows securitization the income has not been originated at the time of securitization. The same can be summed up as: In future flow securitization, the asset being transferred by the originator is not an existing claim against existing obligors, but a future claim against future obligors.

Mechanics of Music Royalty Securitization:

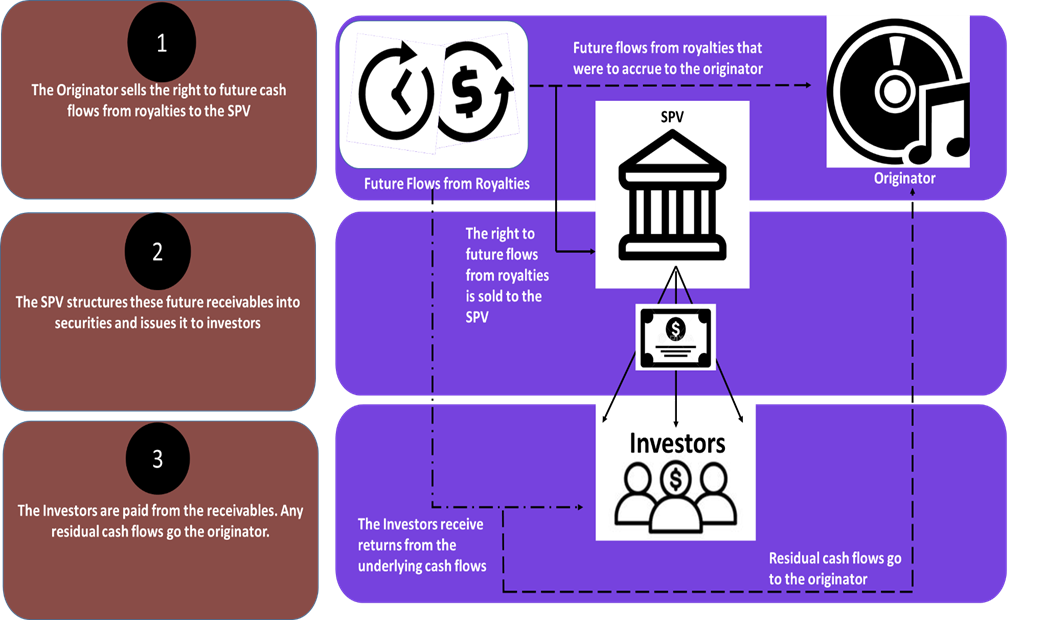

Music royalty securitization involves packaging the future income streams generated by music royalties into tradable financial instruments. The process begins with the identification of income-generating assets, which are then bundled into a special purpose vehicle (SPV). The SPV issues securities backed by these assets, which are sold to investors. The revenue generated from the underlying music royalties serves as collateral for the securities, providing investors with a stream of income over a specified period.

The process of music royalty securitization typically involves several key steps:

Asset Identification: Rights holders, such as artists, record labels, or music publishers, identify their future royalty streams eligible for securitization.

Valuation: A valuation is conducted to estimate the present value of the anticipated royalty income streams. Factors such as historical performance, market trends, and artist popularity are taken into account.

Selling the future flows: The future flows from royalties are then sold off to the Special Purpose Vehicle (SPV) to make them bankruptcy remote. The sale entitles the trust to all the revenues that are generated by the assets throughout the term of the transaction, thus protecting against credit risk and sovereign risk as discussed later in this article.

Structuring the Securities: These future cash flows are then structured into securities. This may involve creating different tranches with varying levels of risk and return.

Issuance: The securities are then issued and sold to investors through public offerings or private placements. The proceeds from the sale provide upfront capital to the rights holders.

Revenue Collection and Distribution: The entity responsible for managing the securitized royalties collects the revenue from various sources which is then distributed to the investors according to the terms of the securities.

Importance of Over-collateralization:

Over-collateralization is an important element in music royalty securitization. In music royalty securitization and in all future flows transactions in general, the extent of over-collateralization as compared to asset backed transactions is much higher. The same is to protect the investors against performance risk, that is the risk of not generating sufficient royalty incomes. Over-collateralization becomes even more important since subordination structures generally do not work for future flow securitizations. This is because the rating here will generally be capped at the entity rating of the originator.

Why go for securitization ?

Now the question may arise as to why an artist or a right holder of a royalty has to go for securitization of his music royalties in order to secure funding. Why cant he simply opt for a traditional source of funding ? The answer to this question is two folds:

Firstly, the originator in the present case generally has no collateral to leverage and hardly there will be a lender willing to advance a loan based on assets that are yet to exist.

Secondly even if they are able to obtain funding it will be at a very high cost due to high risk the lender perceives with the lending.

Music royalty securitization, could be his chance to borrow at a lower cost. The cost of borrowing is related to the risks associated with the transaction, that is, the risk the lender takes on the borrower. Now, this risk includes performance risk, that is the risk that the work of the originator does not generate enough cash flows. While this risk holds good in case of securitization as well, it however takes away two major risks – credit risk and sovereign risk.

Credit risk, as divested from the performance risk would basically mean that the originator has sufficient cash flows but does not pay it to the lender. This risk can be removed in case of a securitization by giving the SPV a legal right over the cash flow.

Sovereign risk on the other hand emanates only in case of cross-border lending. This risk arises when an external lender gives a loan to a borrower whose sovereign later on in the event of an exchange crises either imposes a moratorium on payments to external lenders or may redirect foreign exchange earnings. This problem is again solved by giving the SPV a legal right over the cash flows from the royalties arising in countries other than the originator’s, therefore trapping cash flow before it comes under the control of the sovereign.

The lack of these two types of risks might reduce the cost of borrowing for the originator; thus making music royalty securitization a lucrative option.

Accounting Treatment:

As discussed, there is no existing asset in a music royalty transaction. In terms Ind AS 39, an entity may derecognize an asset only when either the contractual rights to the cash flows from the financial asset have expired or if it transfers the financial asset. However, here asset means an existing asset and a future right to receive does not qualify as an asset in terms of the definition under Ind AS 32.

Accordingly, the funding obtained through the securitization of music royalties should be shown as a liability in books as the same cannot qualify as an off-balance sheet funding.

Regulatory Framework in India:

It is crucial to discuss the applicable regulatory framework on securitization currently prevalent in India and whether music royalty securitization would fall under any of these:

Master Direction – Reserve Bank of India (Securitization of Standard Assets) Directions, 2021(‘SSA Master Directions)

SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008 (SDI Framework)

Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002

While the SSA Master Directions primarily pertain to financial sector entities, and will not directly apply to this domain; however, there exists a possibility that the securitization of music royalties could fall under the purview of SEBI’s SDI Framework.

Music royalty securitization offers a range of benefits for both investors and rights holders:

Diversification: Investors gain exposure to a diversified portfolio of music royalties, potentially reducing risk compared to investing in individual songs or artists.

Steady Income Stream: Music royalties often provide a stable and predictable income stream, making them attractive to income-oriented investors, such as pension funds and insurance companies.

Liquidity: By securitizing music royalties, rights holders can access immediate capital without having to wait for future royalty payments, providing liquidity for new projects or business expansion.

Risk Mitigation: Securitization allows rights holders to transfer the risk of fluctuating royalty income to investors, providing a hedge against market uncertainties and industry disruptions.

Challenges and Considerations:

While music royalty securitization presents compelling opportunities, it also poses certain challenges and considerations:

Market Volatility: The music industry is subject to shifts in consumer preferences, technological disruptions, and regulatory changes, which can impact the value of music royalties.

Due Diligence: Thorough due diligence is essential to assess the quality and value of music assets, including considerations such as copyright ownership, market demand, and revenue potential.

Potential Risks:

Market Risk: Changes in consumer behavior, technological advancements, or regulatory developments could impact the value of music royalties.

Legal Risk: Disputes over ownership rights, copyright infringement, or licensing agreements could lead to litigation and financial losses.

Concentration Risk: Investing in a single music catalog or genre exposes investors to concentration risk if the popularity of that catalog or genre declines.

Cash Flow Variability: While music royalties can provide steady income, fluctuations in streaming revenues or changes in licensing agreements may affect cash flow stability.

Reputation Risk: The success of music royalty securitization depends on the ongoing popularity and commercial success of the underlying music assets. Negative publicity, controversies, or declining relevance can adversely affect investor confidence and returns.

Implications for the Music Industry:

While music royalty securitization presents exciting opportunities, it also raises certain considerations for the music industry:

Artist Empowerment: Securitization can empower artists by providing them with alternative financing options and greater control over their financial destiny.

Industry Evolution: The emergence of music royalty securitization could reshape the traditional music business model, fostering innovation and collaboration between artists, labels, and investors.

Way Forward

Music royalty securitization offers a compelling investment opportunity for investors seeking exposure to the lucrative music industry. By securitizing future royalty streams, music rights owners can unlock liquidity while providing investors with access to a diversified portfolio of music assets.

As the music industry continues to evolve, music royalty securitization is likely to play an increasingly prominent role in the financial landscape, providing new avenues for capital deployment and revenue generation. It has the potential to transform the rhythm of creativity into the melody of investment opportunity.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00executivehttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngexecutive2024-02-26 16:24:482024-03-14 13:07:56Securing the Beat: Tuning into Music Royalty Securitization

The Ministry of Finance, Government of India, through its Department of Revenue, has issued a draft Indian Stamp Bill, 2023[1] on 17th January, 2024 inviting public comments and suggestions within 30 days, with an intent to align it with the modern stamp duty regime. Once enacted, the Bill seeks to replace the Indian Stamp Act, 1899[2].

The Indian Stamp Act, 1899 is a fiscal legislation enacted for the purpose of generating revenue to the Government. Being enacted during the British era, the Act has undergone several amendments from time to time, however, most of the provisions still stand redundant, for instance, proviso under section 8(2) of the Act provides for the treatment of stamp duty on bonds, debentures or other securities issued by the local authority prior to 26th March, 1897, the Act at several places uses denomination of money in ‘anna’ which has no role in the present. Such transitional provisions hold no stand anymore, thus may be removed. Therefore, it has been proposed to modernise the legislation to enable it to deal with the present realities and objectives.

In this article, we have made an attempt to analyse the changes proposed.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00executivehttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngexecutive2024-02-07 17:55:042024-02-07 18:14:46Finance Ministry to modernize the Indian Stamp Act

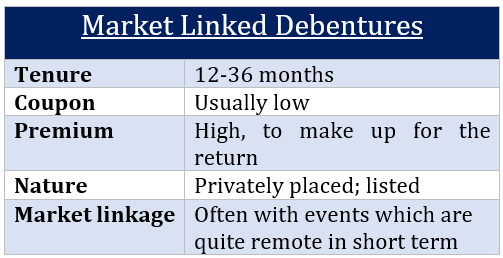

The Finance Bill, 2023[1], has quite nearly caused the demise of the so-called “Market-Linked Debentures” (MLDs)[2]. The changes made pursuant to the Finance Bill, 2023, took away what seemed to be a strong reason for popularity of MLDs, i.e., the tax arbitrage.

Prior to the change, listed MLDs had the advantage of being exempt from the withholding tax under section 193 of the Income Tax Act, 1961, as well as being taxed at 10% as Long Term Capital Gains (LTCG) tax, if held for at least 12 months.

Finance Bill, 2023 inserts a new section 50AA to the Income Tax Act, 1961, which makes MLDs to be taxed at slab rates as a short term capital asset in all cases at the time of transfer or redemption on maturity, irrespective of the period of holding, therefore losing out on the earlier lower LTCG rate of 10%.

In addition, the earlier exemption from withholding tax on listed debentures has now been removed pursuant to an amendment in section 193, which means that interest paid on listed debentures would now be subject to withholding tax with effect from April 01, 2023[3].

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2023-05-17 12:59:382023-05-17 12:59:39Shorn of tax benefit, MLDs now face tax deduction on payouts

Securitization transactions in India post the pandemic has seen significant improvement with volumes growing by 70% to Rs. 73000 crores in FY 2023 compared to Rs. 43000 crores in FY 2022.[1] This growth was also highlighted in one of our recent write up wherein it can be seen from the data laid down that despite the global slowdown in the world economy on account of the pandemic, the volume of securitization transactions in India gained a lot of popularity. Given the impetus of this fundraising mode, it is important to have a vibrant securitization market. This can be only achieved if the governing framework with respect to taxation does not impose an additional taxation burden on the parties. Through this article, the writer will be reviewing the stance of various courts by highlighting the principles with respect to the taxation of the parties involved in a securitization framework i.e. Originator, Special Purpose Vehicle(‘SPV’), and the Investors. For a better understanding of the framework of securitization, the readers can also refer to our Article on Securitization: A Primer.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00anirudhgroverhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pnganirudhgrover2023-04-17 23:28:442023-04-18 12:07:46Taxation in Securitisation: A judicial overview

Tax proposal to tax gains on MLDs as short-term capital gains

The Budget proposes that the capital gains on market linked debentures (MLDs) will be taxed as short term capital gain.

Presently, MLDs are mostly listed, and as listed securities they have 2 advantages:

First , there are exempt from withholding tax. This is one of the carve-outs in sec. 193

Secondly, the holding period for capital gain purposes is 12 months, as opposed to 36 months in case of normal capital assets. This comes from sec. 2 (42A) of the Act. Therefore, if a listed security is held for at least 12 months, and transferred or redeemed thereafter, the gain will be taxed as long term capital gain, with a rate as low as 10%.

Market linked debentures is a concept that prevails world-over, with different names such as equity-linked bonds, index-linked bonds, etc. However, in India, the issuance of MLDs was being exploited as a regulatory and tax arbitrage device.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Aanchal Kaur Nagpalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngAanchal Kaur Nagpal2023-02-01 15:45:402023-02-02 16:03:29Market-linked debentures: Is it the end of the market for them?

Flow of funds, just like a river, not only enriches its destination but also benefits all the stops it passes through. Having a financial hub, a stopover which enables routing billions and billions of global funds on a daily basis can definitely prove resourceful. London, New York, Singapore are some of the globally recognised financial centres, and needless to say these locations are at the forefront of financial development. India too has tried to tap into this with the setting up of GIFT-IFSC in Gujarat, and has tried to position itself as the next big global hub for financial transactions.

Through this write-up, the author tries to explain the concept of International Financial Services Centre and the applicability of domestic regulatory framework on entities set up therein.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Parth Vedhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngParth Ved2022-11-25 17:34:252022-11-29 18:03:29Financial entities in IFSC: A primer

Secondment of employees have become increasingly popular amongst corporate entities which enter into secondment arrangements to leverage the expert knowledge and specific skill sets. The seconded employees work on a deputation basis in the seconded companies they are seconded to which require their technical expertise on certain matters. Since the seconded employee works for the seconded company during the secondment period, a pertinent question arises on whether the seconded employee becomes an employee of the seconded company. If yes, then what are the likely implications in the context of service tax.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Neha Sinhahttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngNeha Sinha2022-11-21 12:05:222022-11-22 12:13:06Secondment contract as ‘services’: Supreme Court held under Indian taxation regime

Leasing industry in India started and grew, as in several other countries, with financial leasing. However, over last several years, it seemed as if financial leases had lost their relevance, for reasons discussed below. While activity in the leasing space was not very brisk, but whatever activity was there was seen mostly in operating leases. Operating leases were sold on the strength of either off-balance sheet treatment, or with lower monthly rentals, or residual value management etc. In case of financial leases, on the other hand, there seemed very little motivation.

Some recent developments seem to be rekindling the interest in financial leases, and if the tax ruling by the ITAT Chennai either goes unchallenged or is affirmed on further appeal, there may be just a new lease of life for financial leases. Coupled with other benefits such as bankruptcy remoteness etc., there may be strong reasons for looking at financial leases, both by lessors and lessees.

In financial year 2021-22, the volume of financial leasing reached to around 7% of the total leasing volumes in the country, compared to 20% in the financial year 16-17[1]. Considering the legal and regulatory construct in India, the reducing volumes of financial leasing make complete sense. However, the recent rulings on taxation of leases may reverse the long known reasons for not doing financial leases.

In this article, the author discusses the reasons why financial leases do not appeal to lessors and lessees and how the recent developments on the taxation aspects of leasing may seem to be bringing financial leases back to life.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kothari Consultantshttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari Consultants2022-09-20 18:55:082022-09-21 12:24:24Financial Leases getting a new lease of life?

Lawmakers might have put the best of efforts to frame the law in the clearest possible way, however, there may still be possibilities of diverse readings (and thus, diverse interpretations). Such a scenario is often addressed by the judiciary which, as and when circumstances arise, determines the questions arising out of law. However, there is also a possibility where the judiciary itself would render diverse interpretations on the same subject matter. This would, of course, lead to confusion and chaos.

A similar situation arose in the recent case of State Tax Officer v. Rainbow Papers Limited,[1] wherein the Hon’ble Supreme Court (‘SC’) dealt with the question as to whether the provisions of the Insolvency and Bankruptcy Code, 2016 (‘IBC’), specially section 53, overrides section 48 of the Gujarat Value Added Tax Act, 2003 (‘GVAT’). Section 48 of GVAT is a non-obstante clause and creates a statutory first charge on the property of the dealer in favour of tax authorities against any amount payable by the dealer on account of tax, interest or penalty for which he is liable to pay to the Government.

SC held that if the resolution plan excludes statutory dues payable to government or a government authority, it cannot be said to be in conformity to the provisions of IBC, and as such, not binding on the government. As such, the same must be rejected by the Adjudicating Authority. Further, section 48 of GVAT is not inconsistent with IBC and hence, it was held that IBC does not override GVAT. The SC went on to rule that by virtue of the ‘security interest’ created in favour of the Government under GVAT, the State is a ‘secured creditor’ as per the definition in IBC. Hence, as workmen’s dues are treated pari passu with secured creditors’ dues, so should the debts owed to the State be put at the same pedestal as the debts owed to workmen under the scheme of section 53(1)(b)(ii).

In the most humble view of the authors, the conclusions as above may not in consonance with the well-settled jurisprudence around the subject matter of conflict between IBC and tax statutes and the question of priorities between these, and may also not fit well with the construct of the IBC, the intent of the lawmakers and the Bankruptcy Law Reform Committee (‘BLRC’), as well as several judicial precedents set by SC itself, as discussed below. A plethora of rulings, including by SC itself, go on to hold that crown debts would be subordinate to the dues of secured creditors, and none of these rulings ever equated tax dues to secured dues. The authors thus, analyse the SC ruling in light of the construct of the IBC, intent of the lawmakers and policymakers, and various past precedents and offer their views as to how this ruling has actually reopened a can of worms and how it may impact success of ongoing and future resolution processes.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-09-08 16:13:382022-12-22 10:17:24Supreme Court ruling revives the quandary, holds tax authorities to be secured creditors