Webcasting in virtual AGM

by Smriti Wadehra & Qasim Saif

(smriti@vinodkothari.com) (executive@vinodkothari.com)

Background

MCA considering the COVID-19 pandemic and the social distancing norms issued by the Government, realized that conducting physical AGM by companies within the prescribed timeline shall be difficult for this financial year. Accordingly, the Ministry vide its circular dated 5th May, 2020 has permitted holding of Annual General Meetings (AGM) through video conferencing[1] for all meetings conducted during the calendar i.e. till 31st December, 2020. The said circular read with previous circulars dated 13th April, 2020[2] and 8th April, 2020[3] prescribed a detailed procedure as to how companies can conduct their general meetings virtually.

While these circulars dealt with various perplexities arising from the thought of virtual general meetings, however, there was still some clarification pending on applicability of other requirements applicable on companies, for instance, the requirement of webcasting under regulation 44(6) of SEBI (Listing Obligation and Disclosure Requirements) Regulation, 2015.

We discuss the same as below.

Webcast vs Video conferencing

The very basic differentiation in the term webcast and video conferencing is that, the former only provides one-way participation rights but the later provides for a two-way communication. In reference to providing webcasting facility during the AGM, the shareholders can only watch and listen to the proceedings of the meeting but cannot participate in voting or ask queries whereas in video conferencing the shareholders have complete participation as in case of a physical general meeting. Webcasting is merely “live streaming” of the AGM.

Intent of webcast

The requirement for providing webcast facility was recommended by Kotak Committee[4] on Corporate Governance which provided:

“Reg 44A. Meetings of shareholders

The top 100 listed entities by market capitalization, determined as on March 31 of every financial year, shall provide one-way live webcast of the proceedings of all shareholder meetings held on or after April 1, 2018”

The aforesaid recommendation was in addition to the recommendation w.r.t. e-voting facility which as per the existing provision of law, is closed at 5 p.m. of the previous day of the meeting, however, the committee recommended to shift the closure of e-voting facility to the day of meeting itself. The intent behind the recommendation was that the e-voting timeline expires before the meeting is held, accordingly, shareholders not attending the meetings in person are unable to take into account discussions at the meeting in order to make informed decisions.

Whereas, SEBI accepted the recommendations made by the Kotak Committee on 9th May, 2018 w.r.t. webcasting facility and inserted a new sub-regulation, however, the recommendation w.r.t e-voting is still in draft form. The provisions relating to webcast were made applicable to top 100 listed entities from 1st April, 2019.

The whole intent of conducting annual general meetings is the indispensable right to the shareholders of companies to meet the directors and auditors of the Company, at least once in a year. This has been the feature of corporate laws over the decades – based on the fact that the “managers” (directors) at least face the “owners” (shareholders) once. The law therefore, mandates physical meetings. However, with the rise of technology, call it necessity or evolution, the law embraced e-voting as a recognised means of voting (but not participation). Later, SEBI introduced the concept of providing one-way webcast facility for shareholders so as to increase participation of shareholders at meeting (though one-way).

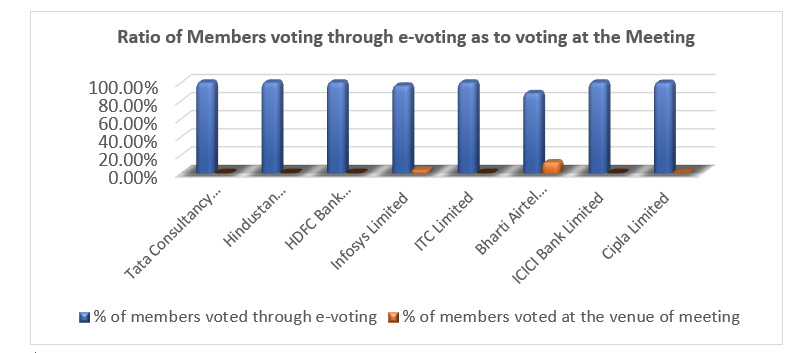

The data shows that attendance of shareholders at AGMs is even less than 5% of total number of shareholders at Meeting. Further, most of the shareholders (especially those residing in state other than where the AGM is conducted) find it more feasible to vote by way of e-voting. In the data[5] below, we can observe that on an average 95% of members of some well reputed companies vote through e-voting while on-site voting percentage is negligible. Therefore, it can be said, that the members do not really depend on meeting discussions to take a decision. However, webcast enables them to be apprised of the conduct of the meeting, shareholder queries, concerns, etc. raised at the meeting, etc.

Globally, countries like United States of America, Canada, United Kingdom, France, China and many such countries have permitted conducting meeting through video conferencing during the crisis. Further, the concept of webcasting is new for India. However, for many foreign countries including those named above have included providing of webcasting facility in shareholder’s meeting as a requirement of law.

Webcast facility in virtual AGM, whether required?

Now, the question is, where the AGM has itself gone ‘virtual’ (as mentioned above), is there really a requirement of webcasting? Note that SEBI has not provided any relaxation from webcasting as such.

It may be noted that video conferencing is nothing but participation through electronic means by shareholders remotely i.e. other than the venue of AGM. Therefore, where the company has already provided the facility of video conferencing to shareholders, webcast may not actually be needed. The purpose which the webcast intends to serve (dissipation of conduct of meeting) is well-served by the video-conferencing. In fact, in webcast the shareholders get only participation rights i.e. to hear and view the proceedings of meeting. However, in case of virtual AGM, the shareholders are provided with two-way participation rights i.e. can speak as well. Hence, provided two options, the shareholders will mostly opt for the latter.

The webcast, however, can be of relevance where the participation capacity is limited. In this regard, MCA circular dated 8th April, 2020 has prescribed minimum capacity allowance by companies conducting virtual AGM. For companies that are required to provide e-voting facility has to arrange capacity of minimum 1000 members at virtual AGM on first come first basis. This limit is minimum 500 members for companies not required to provide e-voting facility. Hence, the platform for conducting virtual AGM should provide for aforesaid minimum.

We all know that mostly large companies have lakhs of shareholders. Therefore, if companies restrict the entry of shareholders on first come first basis i.e. does not allow participation right to all shareholders in virtual AGM (due to software limitations, etc.), in that case webcast facility should be provided (if required). However, if companies do not restrict any shareholder from participation in virtual AGM and is open for all shareholders irrespective of the number, in such cases providing separate facility for webcast may turn out to be a futile exercise.

[1] http://www.mca.gov.in/Ministry/pdf/Circular20_05052020.pdf

[2] http://www.mca.gov.in/Ministry/pdf/Circular17_13042020.pdf

[3] https://www.mca.gov.in/Ministry/pdf/Circular14_08042020.pdf

[4] https://www.sebi.gov.in/reports/reports/oct-2017/report-of-the-committee-on-corporate-governance_36177.html

[5]Source: https://www.livemint.com/opinion/online-views/covid-19-need-to-re-look-at-pre-digital-era-compliances-under-companies-act-11588585274712.html

Leave a Reply

Want to join the discussion?Feel free to contribute!