Full Day Workshop on Securitisation, Transfer of Loans and Co-lending

28th May, 2026

Register Here : https://forms.gle/maTWJ2kBowndrLVS8

Loading…

Loading…

Our Other Upcoming events:

28th May, 2026

Register Here : https://forms.gle/maTWJ2kBowndrLVS8

Loading…

Our Other Upcoming events:

Register: https://forms.gle/VBeA2EmkC92QUmK79

– Team Corplaw | corplaw@vinodkothari.com

Continuing with the spree of regulatory changes brought in 2025, RBI has issued Amendment Directions on Lending to Related Parties by Regulated Entities. Separate notifications have been issued for each regulated entity, based on the draft Directions for lending and contracting with related parties issued on 3rd October, 2025. We discuss the changes brought in for commercial banks by way of the RBI (Commercial Banks – Credit Risk Management) – Amendment Directions, 2026 and RBI (Commercial Banks – Financial Statements: Presentation and Disclosures) – Amendment Directions, 2026.

| Point of comparison | CRM Amendment Directions | Listing Regulations | Companies Act |

| Scope of coverage | Loans, non-funded facilities, investment in debt securities | Any transfer of resources, obligations or services | Contracts as enumerated u/s 188 (1) |

| Meaning of related party | Directors, KMPs, promoter, their relatives, entities in which either of them have specified interest (partnership, shareholding, control, etc).Does not include Company’s own holding company, subsidiaries or associates | Wide definition, including sec 2 (76) of CA, accounting standards, promoter, promoter group entities, shareholders with 10% or more shareholding | As defined in sec. 2 (76), primarily including directors, KMPs, their relatives, private cos where such persons are a director or member, public companies with directors’ 2% shareholdings.Includes entity’s own subsidiaries, associates, JVs, holding company |

| Concept of “reciprocally related party” | In line with the statutory restrictions, includes directors/relatives on the boards of other banks, AIFIs, trustees of mutual funds set up by other banks | Does not exist; however, a purpose-and-effect test exists whereby surrogate transactions may be covered. | Does not exist |

| Primary approving body | Committee on Lending to Related Parties, or the Board | Audit Committee | Audit Committee; or the Board |

| Shareholders’ approval | Not required | Required if crossing materiality threshold | Required if not on in ordinary course of business+ arm’s length, and crossing materiality threshold |

| Materiality threshold | Being linked with a single loan exposure, ranges from Rs 5 crores to Rs 25 crores depending on Bank’s capital | Being aggregated for transactions during a FY, ranges from 10% of the entity’s consolidated turnover to Rs 5000 crores based on consolidated turnover of the entity | Usually based on 10% of turnover or net worth (depending on transaction type) |

Simrat Singh | finserv@vinodkothari.com

Asset classification under RBI regulations has always been anchored to the borrower, not to individual loan facilities. Once a borrower shows repayment stress in any exposure, it is no longer reasonable to treat the borrower’s other obligations as unaffected; prudence requires that all other facilities to that borrower reflect the same level of stress. Even the insolvency law reinforces this borrower-level approach to default by allowing CIRP to be triggered irrespective of whether the default is owed to the applicant creditor or not (see Explanation to section 7 of the IBC).

This borrower-level approach is not unique to India. Globally, the Basel framework also defines default at the obligor level – the core idea being that credit stress is a condition of the borrower, not of a single loan. In other words, when a borrower sneezes financial distress, all his loans catch a classification cold.

Under the earlier 2020 framework for priority sector co-lending between banks and NBFCs, each RE applied its own asset classification norms to its respective share of the co-lent loan (see para 13 of 2020 framework). This allowed situations where the same borrower and same loan could be classified differently in the books of the two co-lenders. While operationally convenient, this approach sat uneasily with the borrower-level logic of RBI’s IRACP norms and diluted the consistency of credit risk recognition in a shared exposure.

The 2025 Directions [now subsumed in Para B of the Reserve Bank of India (Non-Banking Financial Companies – Transfer and Distribution of Credit Risk) Directions, 2025] resolve this inconsistency by requiring uniform asset classification across co-lenders at the borrower level (see para 124 reproduced below for reference).

124. NBFCs shall apply a borrower-level asset classification for their respective exposures to a borrower under CLA, implying that if either of the REs classifies its exposure to a borrower under CLA as SMA / NPA on account of default in the CLA exposure, the same classification shall be applicable to the exposure of the other RE to the borrower under CLA. NBFCs shall put in place a robust mechanism for sharing relevant information in this regard on a near-real time basis, and in any case latest by end of the next working day.

Therefore, where one co-lender classifies its share of a co-lent exposure as SMA or NPA, the other co-lender must apply the same borrower classification to its share of the same exposure. It was an extension of RBI’s long-standing borrower-wise classification principle into a multi-lender structure.

However, the wording of paragraph 124 has, in practice, been interpreted by some lenders in a much narrower manner. The phrase “under the CLA” has been read to mean that the classification of the other co-lender’s share would change only if the borrower defaults on the co-lent exposure itself. On this interpretation, where a borrower defaults on a separate, non-co-lent loan, lenders may in their books follow borrower level classification but they need not share such information with the co-lending partner since there is no default in the co-lent loan.

This approach, however, runs contrary to the regulatory intent and represents a classic case where the literal reading of a provision is placed in conflict with its underlying purpose. Market practice reflects this divergence. Traditional lenders have generally adopted a conservative approach, applying borrower-level classification across exposures irrespective of whether the default arises under the CLA. Certain other lenders, however, have taken a more aggressive position, limiting classification alignment strictly for defaults under the co-lent exposure. The conservative approach is more consistent with RBI’s prudential framework and intent, which has always treated credit stress as a condition of the borrower rather than of a particular loan structure.

Once borrower-level classification is accepted as the governing principle, the consequence is straightforward: any other exposure that a co-lender has to the same borrower must also reflect the borrower’s SMA or NPA status, even if that exposure is not part of the co-lending arrangement. Let us understand this by way of examples.

Scenario 1: Multiple Loans, No Co-Lending Exposure

A borrower has three separate loans:

Although A, B and B may be co-lending partners with each other in general, none of the above loans are under a co-lending arrangement (CLA).

Treatment: Since there is no co-lent exposure to the borrower, paragraph 124 of the Directions does not apply. Each lender classifies and reports its own loan independently, as per its applicable asset classification norms. There is no obligation to share asset-classification information relating to these loans among the lenders.

Scenario 2: One Co-Lent Loan and Other Standalone Loans

A borrower has three loans:

Case A: Default under the Co-Lent Loan

If B classifies its 80% share of L1 as NPA:

Case B: Default under a Non-Co-Lent Loan by any one of the Co-Lenders

If A classifies L2 as NPA:

Case B: Default under a Non-Co-Lent Loan of a Third Lender

Assume L3 is classified as NPA by C, while L1 and L2 remain standard.

Note that borrower-level asset classification and information sharing activates only where there is a co-lending exposure to the borrower. Once such an exposure exists, any default in any loan of a co-lender triggers borrower-level classification across all exposures of that lender, including standalone loans. However, lenders with no co-lending exposure to the borrower remain outside this information-sharing loop. May refer the below chart for more clarity:

Fig 1: Decision chart for asset classification of loans under co-lending

To make borrower-level classification work in practice, the 2025 Directions require co-lenders to put in place information-sharing arrangements. Any SMA or NPA trigger must be shared with the other co-lender promptly and, in any case, by the next working day. It requires aligned IT systems so that both lenders update their books on the borrower at the same time, or as close to real time as possible.

The 2025 Directions reinforce a long-standing regulatory principle: credit stress belongs to the borrower, not to a specific loan or lender. Uniform borrower-level classification and timely information sharing are essential to preserve consistency in risk recognition across co-lenders. While this increases operational complexity, it aligns co-lending practices with RBI’s prudential intent.

See our other resources on co-lending.

Youtube: https://youtu.be/XofD9zmBGxQ

Loading…

Register your interest here: https://forms.gle/cfHXEVc39B4g14ek6

A 5th December 2025 RBI amendment has introduced significant changes to the manner in which business activities may be allocated among banks and entities within banking groups, including NBFCs, HFCs, securities broking entities, AMCs, and others. These changes impact all banks with non-banking subsidiaries or associates, as well as all NBFCs, HFCs, and related entities forming part of banking groups.

Some of the requirements come into effect as early as 31st March 2026, creating an urgent need for impacted entities to reassess, restructure, or reposition their business models and inter-group arrangements.

We intend to examine these developments in depth. Given the nature and implications of the amendment, the session will include active interaction with seasoned banking and finance professionals.

You are invited to express your interest in joining this interactive discussion, scheduled for December 15th, 2025 | 6:00 p.m. onwards | YouTube & Zoom Live.

Other Resources:

– Vinod Kothari | finserv@vinodkothari.com

The new dispensation implemented from 5th December 2025 implies that lending business, obviously carried in the parent bank, needs to be allocated between the bank and the group entities so as to avoid overlaps. The bank will have to take its business allocation plan, at a group level, to its board, by 31st March 2026.

The RBI’s present move has certain global precedents. Singapore passed an anti-commingling rule applicable to banking groups way back in 2004, but has subsequently relaxed the rule by a provision referred to as section 23G of the Banking Regulations. However, the approach is not uniformly shared across jurisdictions.

We are of the view that as the decision works both at the bank as well as the NBFC/HFC level, the same has to be taken to the boards of the respective NBFCs/HFCs too.

Businesses which currently overlap include the following:

In our view, banks will have serious concerns in meeting their priority sector lending targets, unless they decide to keep priority sector lending business in the bank’s books. Priority sector lending is quite often much less profitable, and the NBFCs in the group are able to create such loans at much higher rates of return due to their delivery strengths or customer franchise. As to how the banks will be able to originate such loans departmentally, will remain a big question.

There are other implications of the above restrictions too:

In case of several non-lending products such as securities trading, demat services, etc., the approach may be easier. However, lending services constitute the bulk of any bank’s financial business, and group NBFCs and HFCs are also evidently engaged in lending. Hence, there may be a delicate decisioning by each of the boards on who does what. Note that this choice is not spasmodic – it is a strategic decision that will bind the entities for several years.

The factors based on which banks will have to decide on their business allocation may include:

Talking about pass through certificates, there is a complicated question as to whether the investment limits imposed by the 5th Dec. 2025 amendment on aggregate investments in group entities will include investment in pass through certificates arising out of pools originated by group entities. In our view, the answer is in the negative, as the investment is not originator, but in the asset pools. However, if the bank makes investment in the equity tranche or credit enhancing unrated tranches, the view may be different.

Banks are heading shortly in the last quarter of a year which is laden with strong headwinds. In this scenario, facing business allocation decisions, rather than business expansion or risk management, may be more challenging than it may seem to the regulators.

Other resources:

– Dayita Kanodia | finserv@vinodkothari.com

RBI on December 5, 2025 issued RBI (Commercial Banks – Undertaking of Financial Services) (Amendment) Directions, 2025 (‘UFS Directions’) in terms of which NBFCs and HFCs, which are group entities of Banks and are therefore undertaking lending activities, will be required to comply with the following additional conditions:

The requirements become applicable from the date of notification itself that is December 5, 2025. Further, it may be noted that the applicability would be on fresh loans as well as renewals and not on existing loans. The following table gives an overview of the compliances that NBFCs/HFCs, which are a part of the banking group will be required to adhere to:

| Common Equity Tier 1 | RBI (Non-Banking Financial Companies – Prudential Norms on Capital Adequacy) Directions, 2025 | Entities shall be required to maintain Common Equity Tier 1 capital of at least 9% of Risk Weighted Assets. |

| Differential standard asset provisioning | RBI (Non-Banking Financial Companies – IncomeRecognition, Asset Classification and Provisioning) Directions, 2025 | Entities shall be required to hold differential provisioning towards different classes of standard assets. |

| Large Exposure Framework | RBI (Non-Banking Financial Companies – Concentration Risk Management) Directions, 2025 | NBFCs/HFCs which are group entities of banks would have to adhere to the Large Exposures Framework issued by RBI. |

| Internal Exposure Limits | In addition to the limits on internal SSE exposures, the Board of such bank-group NBFCs/HFCs shall determine internal exposure limits on other important sectors to which credit is extended. Further, an internal Board approved limit for exposure to the NBFC sector is also required to be put in place. | |

| Qualification of Board Members | RBI (Non-Banking Financial Companies – Governance)Directions, 2025 | NBFC in the banking group shall be required to undertake a review of its Board composition to ensure the same is competent to manage the affairs of the entity. The composition of the Board should ensure a mix of educational qualification and experience within the Board. Specific expertise of Board members will be a prerequisite depending on the type of business pursued by the NBFC. |

| Removal of Independent Director | The NBFCs belonging to a banking group shall be required to report to the supervisors in case any Independent Director is removed/ resigns before completion of his normal tenure. | |

| Restriction on granting a loan against the parent Bank’s shares | RBI (Commercial Banks – Credit Risk Management) Directions, 2025 | NBFCs/HFCs which are group entities of banks will not be able to grant a loan against the parent Bank’s shares. |

| Prohibition to grant loans to the directors/relatives of directors of the parent Bank | NBFCs/HFCs will not be able to grant loans to the directors or relatives of such directors of the parent bank. | |

| Loans against promoters’ contribution | RBI (Commercial Banks – Credit Facilities) Directions,2025 | Conditions w.r.t financing promoters’ contributions towards equity capital apply in terms of Para 166 of the Credit Facilities Directions. Such financing is permitted only to meet promoters’ contribution requirements in anticipation of raising resources, in accordance with the board-approved policy and treated as the bank’s investment in shares, thus, subject to the aggregate Capital Market Exposure (CME) of 40% of the bank’s net worth. |

| Prohibition on Loans for financing land acquisition | Group NBFCs shall not grant loans to private builders for acquisition and development of land. Further, in case of public agencies as borrowers, such loans can be sanctioned only by way of term loans, and the project shall be completed within a maximum of 3 years. Valuation of such land for collateral purpose shall be done at current market value only. | |

| Loan against securities, IPO and ESOP financing | Chapter XIII of the Credit Facilities Directions prescribes limits on the loans against financial assets, including for IPO and ESOP financing. Such restrictions shall also apply to Group NBFCs. The limits are proposed to be amended vide the Draft Reserve Bank of India (Commercial Banks – Capital Market Exposure) Directions, 2025. See our article on the same here. | |

| Undertaking Agency Business | Reserve Bank of India (Commercial Banks – Undertaking of Financial Services) Directions, 2025 | NBFCs/HFCs, which are group entities of Banks can only undertake agency business for financial products which a bank is permitted to undertake in terms of the Banking Regulations Act, 1949. |

| Undertaking of the same form of business by more than one entity in the bank group | UFS Directions | There should only be one entity in a bank group undertaking a certain form of business unless there is proper rationale and justification for undertaking of such business by more than one entities. |

| Investment Restrictions | Restrictions on investments made by the banking group entities (at a group level) must be adhered to. |

Read our write-up on other amendments introduced for banks and their group entities here.

Other resources:

Simrat Singh | finserv@vinodkothari.com

Operational risk, as defined by the Basel framework, refers to the possibility that a financial institution’s routine operations may be disrupted due to failures in processes, systems, people, or external events. While historically treated as secondary to credit and market risk, it has increasingly become a central focus of risk management, particularly for institutions with complex operations, heavy technology dependence, extensive outsourcing, and stringent regulatory obligations. Reflecting this shift, the RBI’s 2024 Guidance Note on Operational Risk Management and Resilience expands its expectations for operational risk management to all NBFCs.

Having previously discussed the guidance note (refer here), this article now explains the fundamentals of operational risk assessment and outlines its process.

Operational risk poses unique challenges because many of the events that cause losses arise from internal factors, making them difficult to generalise or predict. Large operational losses are often viewed as rare, which can make it difficult to get sustained management attention on the steady, routine work required to identify issues and track trends1. Operational risks typically stem from people, processes, systems and external events, ironically, the same resources essential for running the business. Unlike credit and market risk which are modelled and hedged, operational risks are often idiosyncratic, event-driven and subject to human, process and system failure.

Financial institutions operate with complex processes, large transaction volumes, strict regulatory reporting requirements and often heavy dependence on technology, outsourcing arrangements and third-party service providers. Because of this, operational failures, such as system glitches, fraud, compliance breaches or breakdowns in business continuity, can result in substantial financial losses, regulatory sanctions, reputational harm and other disruptions to business operations.

Given these risks, regulators have placed growing emphasis on the measurement and management of operational risk. Based on our experience, RBI has frequently raised queries regarding the operational risk frameworks of NBFCs during its supervisory inspections. Under Basel II, for instance, banks using the Advanced Measurement Approach were required to maintain strong, demonstrable operational risk management systems. Recognising the importance of operational risk, the Bank of England’s FSA0732 report, which is applicable on banks and large investment firms, requires firms to record the top ten operational risk loss events for each reporting year. This provides a clear view of what went wrong, where it occurred and the scale of the financial impact.

In its guidance note for operational risk, RBI at many places underscored the importance for risk assessment. One such example is given below:

Principle 6: Senior Management should ensure the comprehensive identification and assessment of the Operational Risk inherent in all material products, activities, processes and systems to make sure the inherent risks and incentives are well understood. Both internal and external threats and potential failures in people, processes and systems should be assessed promptly and on an ongoing basis. Assessment of vulnerabilities in critical operations should be done in a proactive and prompt manner. All the resulting risks should be managed in accordance with operational resilience approach.

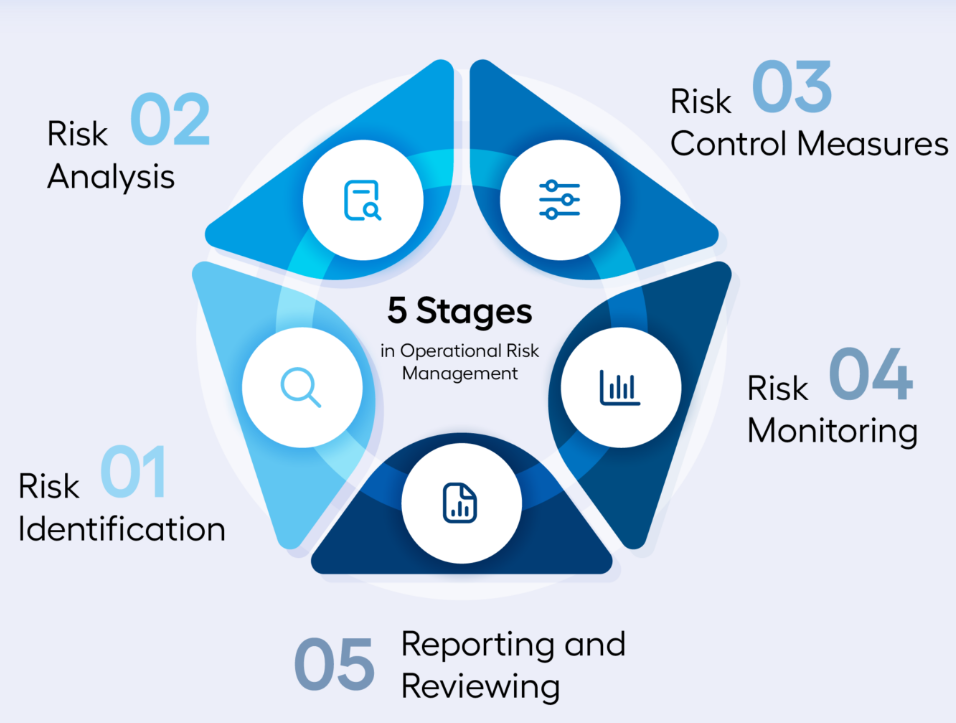

6.1 Risk identification and assessment are fundamental characteristics of an effective Operational Risk Management system, and directly contribute to operational resilience capabilities. Effective risk identification considers both internal and external factors. Sound risk assessment allows an RE to better understand its risk profile and allocate risk management resources and strategies most effectively.

Figure 1: Operational Risk Assessment Process

Risk identification means figuring out what exactly you need to assess. It involves recognising the different risk sources and risk events that may disrupt your business. A risk source is the underlying cause, something that has the potential to create a problem. A risk event is when that problem actually occurs. For example, a weak password is a risk source, while a data breach caused by that weak password is the risk event.

As per the RBI’s Guidance Note, REs are expected to take a comprehensive view of their entire “risk universe”. This means identifying all categories of risks, traditional or emerging, that could potentially affect their operations. These may include insurance risk, climate-related risk, fourth- and fifth-party risks, geopolitical risk, AML and corruption risk, legal and compliance risks, and many others. The underlying expectation is simple: an RE should systematically identify everything that can go wrong within its business model, processes, people, systems, and external dependencies, and ensure that no material source of risk is overlooked.

There are many ways to identify risks. You may use questionnaires, self-assessments by business or functional heads, workshops with staff involved in risk management, or you may review past failures within the company. Industry reports, experiences of peers, and linking organisational goals to potential obstacles can also reveal important risks. You can even look at upcoming strategic initiatives and think ahead about the risks that may arise when these changes are implemented.

Every organisation has its own risk profile. A lender may worry about borrowers not repaying, untrained staff, biases in an AI underwriting model, IT system failures, employee fraud, or suppliers not delivering on time. These risks should be recorded in a risk register, but it is important that this register reflects your business. A company offering only physical loans may not face digital lending risks, and should not simply copy any generic list. The goal is to identify risks that genuinely matter to your day-to-day operations.

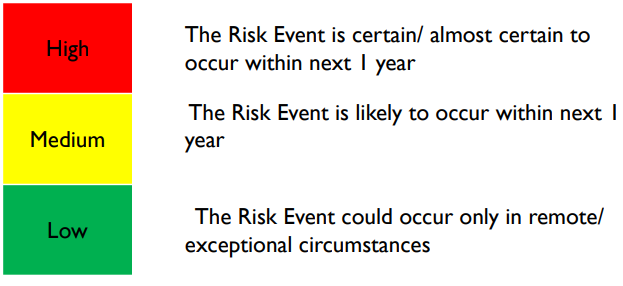

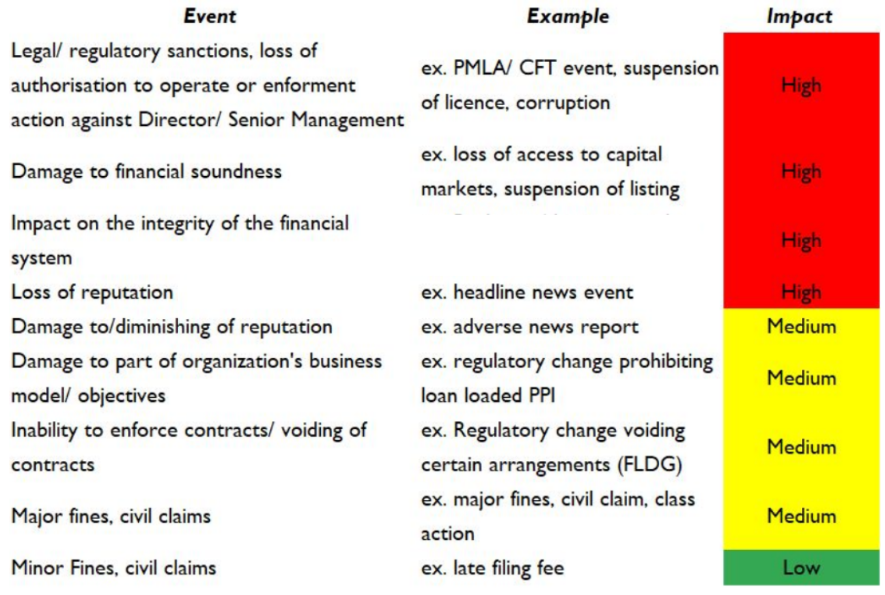

Once you know which risks matter, the next step is to assess each of them. For every risk, ask yourself two basic questions:

Figure 2: Illustrative likelihood assessment criterias

Figure 3: Illustrative impact assessment of risks

These two questions help you understand how serious the risk is inherently (inherent risk level) i.e, before considering whether you have any controls in place. Note that at this stage, you’re only interested in the natural level of risk that exists ignoring any controls you might already have.

Once the inherent risks are understood, the next step is to look at how these risks are currently being managed. These risk-reducing efforts are your controls or mitigation measures. Controls are simply the actions, checks, or processes already in place to lower the likelihood or impact of a risk. For example: Is your underwriting model checked for bias? Are board committees meeting regularly? Do you have proper maker–checker checks in your V-CIP process? Controls can take many forms such as policies, procedures, tools, system checks, reviews, or even day-to-day practices followed by employees. In essence, a control is any measure that maintains or modifies risk and helps the organisation manage it more effectively.

After evaluating the controls, you can determine the residual risk i.e. the level of risk that remains even after your mitigation measures have been applied. Residual risk shows whether the remaining exposure is acceptable or whether additional controls are needed. By definition, residual risk can never be higher than inherent risk. Generally, residual risk can be interpreted as follows:

| Category | Risk Source | Risk event | Root cause | Likelihood | Consequence | Level of inherent risk | Control Effectiveness | Level of Residual Risk |

| People Risk | Employees / Staff | Employee fraud, misappropriation, or collusion | Weak internal controls, poor background checks | Highly Likely | Medium | High | Weak | HIGH |

| Information Technology & Cyber Risk | IT Infrastructure / Systems | System downtime or core platform failure | Server outage, inadequate IT resilience | Possible | Low | Low | Strong | LOW |

| Process & Internal Control Risk | Onboarding / KYC Processes | Non-compliance with KYC or onboarding procedures | Inadequate verification, manual errors | Possible | High | High | Adequate | MEDIUM |

| Legal & Compliance Risk | Outsourcing / LSP Arrangements | Non-compliance in outsourcing / LSP arrangements | Weak SLA oversight, inadequate due diligence | Unlikely | Low | Low | Adequate | LOW |

| External Fraud Risk | Borrowers / External Parties | Borrower fraud – identity theft, fake borrowers, or collusion | Forged documents, weak KYC | Possible | Low | Low | Strong | LOW |

| Model / Automation / Reporting Risk | Data Aggregation / Systems | Failure in data aggregation across systems for regulatory returns | System inconsistencies, poor data governance | Highly Likely | Medium | High | Strong | LOW |

| Reputation Risk / Customer Experience | Customer Communication / Sales Practices | Miscommunication of terms or conditions to customers | Poor training, unclear communication scripts | Possible | Medium | Medium | Weak | MEDIUM |

Figure 5: An illustrative Snapshot of Operational Risk Assessment

Understanding residual risk helps decide where further action is required and where the organisation may still be vulnerable.

The goal, therefore, is to move away from a simple “tick-box” approach and make the operational risk assessment truly tailored to the organisation. For ML and above NBFCs, the ICAAP requirement to set aside capital for operational risk is useful, but it covers only a narrow part of what operational risk really involves. A comprehensive assessment goes much further by examining the strength of the entity’s internal controls and how effectively they manage real-world risks. If the residual risk exceeds the organisation’s tolerance level, it should trigger a closer look at those controls and prompt corrective action. Ultimately, the focus should be on building a risk framework that is meaningful, proactive, and aligned with how the organisation actually operates. The ultimate goal is therefore to develop ‘operational resilience’ which as per Bank of England3 is the ability of firms and the financial sector as a whole to prevent, adapt, respond to, recover from, and learn from operational disruptions.

Our other resources on risk management:

Simrat Singh & Sakshi Patil | finserv@vinodkothari.com

India’s lending landscape is evolving from traditional, branch-led lending to digital and now “phygital” models, involving multiple intermediaries connecting borrowers and lenders. For regulated entities (REs), three different terms referring to loan intermediaries are commonly seen: Lending Service Providers (LSPs), Direct Selling Agents (DSAs) and Referral Partners.

At first glance, these roles may appear similar since all “bring in business.” But as far as the RBI is concerned, the difference determines how much regulatory oversight the lender must exercise over these participants. This article attempts to answer who’s who in this lending chain, and more importantly, where a simple referral ends and a regulated lending function begins.

In the digital lending framework, the most central participant is the LSP who are engaged by the REs to carry out some functions of RE in connection with its functions on digital platforms. These LSPs may be engaged in customer acquisition, underwriting support, recovery of loan, etc. The RBI’s Digital Lending Directions, 2025 define an LSP as:

“An agent of a RE (including another RE) who carries out one or more of the RE’s digital lending functions, or part thereof, in customer acquisition, services incidental to underwriting and pricing, servicing, monitoring, or recovery of specific loans or loan portfolios on behalf of the RE, in conformity with the extant outsourcing guidelines issued by the Reserve Bank.”

The emphasis on the term “agent” is crucial since being an agent becomes a precondition to becoming an LSP. An agent is a person employed to act for another; to represent another in dealings with third persons within the overall authority granted and can legally bind the principal by their actions (more discussion on agency later). This distinguishes an agent from a mere vendor or service provider who delivers a contracted service but has no authority to affect the principal’s relationship with third parties and neither is subjected to a degree of control from the principal.

DSAs, though not formally defined by the RBI, their appointment, conduct and RE’s oversight on them is governed by Annex XIII of the SBR Directions (Instructions on Managing Risks and Code of Conduct in Outsourcing of Financial Services by NBFCs) for NBFCs and by Guidelines on Managing Risks and Code of Conduct in Outsourcing of Financial Services by Banks for Banks. DSAs operate largely in physical or “phygital” lending models, focusing on loan sourcing. They represent the lender while dealing with potential borrowers. However, their functions are narrower than those of an LSP. A DSA’s role typically ends with lead generation and preliminary documentation, without involvement in underwriting, servicing or recovery. While the DSA is an agent, it plays a more limited role in the lending value chain and has minimal borrower-facing obligations post origination.

Referral Partners perform the most limited role. They simply share leads or basic borrower information with the lender and have no authority to represent or bind the lender. Their role is confined to referral i.e. the providing the first nudge to the lender. They are treated as independent contractors or service providers, not agents and operate under commercial referral agreements. The RE does not exercise control over their operations, nor is it responsible for their actions beyond the agreed referral activity. The distinction lies not in what they do (introducing borrowers) but in what they cannot do i.e. represent the lender or perform any of its lending functions.

The most important question then arises “How does one determine whether a person is an LSP, DSA, or a referral partner?”. All three may assist in borrower acquisition, but the answer might lie in distinguishing referring from representing. To be classified as an LSP (or even a DSA), the person must first be the agent of the RE, not just a vendor or service provider. The test of agency has been laid down in the Supreme Court’s decision in Bharti Cellular Ltd. v. Commissioner of Income Tax1. The Court, in para 8, observed that the existence of a principal–agent relationship depends on the following elements:

Further, the Court clarified in para 9 that the substance of the relationship, not just its form, determines whether agency exists. If a person is neither authorised to affect the principal’s relationship with third parties nor under its control, and owes no fiduciary obligation, the person is not an agent, regardless of what the contract calls them.

Similarly, in Bhopal Sugar Industries v. Sales Tax Officer2, the Supreme Court had observed that the mere word ‘agent’ or ‘agency’ is not sufficient to lead to the inference that parties intended the conferment of principal-agent status on each other. Mere formal description of a person as an agent is not conclusive to show existence of agency unless the parties intend it so hence, “the true relationship of the parties in such a case has to be gathered from the nature of the contract, its terms and conditions, and the terminology used by the parties is not decisive of the said relationship.”

On the aspect of supervision and control, the Supreme Court in para 40 of the Bharti Cellular ruling stated:

An independent contractor is free from control on the part of his employer, and is only subject to the terms of his contract. But an agent is not completely free from control, and the relationship to the extent of tasks entrusted by the principal to the agent are fiduciary….The distinction is that independent contractors work for themselves, even when they are employed for the purpose of creating contractual relations with the third persons. An independent contractor is not required to render accounts of the business, as it belongs to him and not his employee.

In lending transactions, therefore, the relevant considerations to determine whether an agency exists or not may be:

To illustrate the difference between LSP/DSA and Referral Partner, consider a simple example. You stop at your neighbourhood paanwala for your regular paan or pack of mints. Between the faded ads for mobile recharges and UPI QR codes, one new poster catches your eye “Need a personal loan? Look No Further ! Fast approvals”. Curious, you ask if the shopkeeper has joined the finance world. Smiling, he replies, “Arre nahi sahib, I just share numbers! You give me your name and phone number, I’ll send it to my guy. If your loan gets approved, I get a small tip!” No exchange of KYC documents, no app, no credit score. Now, does this make the paanwala an LSP under the Digital Lending Directions? He may appear as performing a part of the customer acquisition function of the lender so should he now comply with outsourcing norms, data protection protocols and grievance redressal requirements? Of course not.

The paanwala is a pure referral partner. His role ends with introducing a potential borrower to a contact connected to a lender. He does not represent the lender, verify or collect documents, underwrite, service, or recover loans, nor can he legally bind the lender through his actions. Mere referral, without agency and without performing a lending function, does not make one an LSP. Passing a phone number over a cup of chai does not amount to digital intermediation.

| Basis | Referral Partner | LSP |

|---|---|---|

| Scope of activity | Limited to sharing leads with the lender | Performs one or more of the lenders functions w.r.t in customer acquisition, services incidental to underwriting and pricing, servicing, monitoring, recovery |

| Access to prospective customer’s information and documents | Only basic contact information necessary for the lender to approach the customer for the loan is shared | To the extent relevant for carrying out its functions |

| Representation | Does not represent the RE | Represents the RE |

| Agency & Principal | Not an agent | Appointed as an agent |

| DLG | Cannot provide | Can provide (in case of Digital Lending and Co-lending) |

| Applicability of Outsourcing Guidelines | Not applicable | Applicable |

| Mandatory due diligence before appointment | Not applicable | Applicable |

| Appointment of GRO | No such requirement | LSP having interface with borrower needs to appoint a GRO |

| Right to audit | No right of RE | RE has a right |

| Disclosure on the website of the lender | Not applicable | Applicable |

Table 1: Distinction between Referral Partner and LSP

As digital lending continues to expand in India, ensuring that every intermediary’s role aligns with its true legal character is essential. The key in determining the true nature of the relationship would ultimately rest on the contractual terms that must reflect the true nature of the relationship. Misclassifying these entities can expose lenders to compliance risks under RBI’s outsourcing and digital lending guidelines.

Our resources on the same: