Ease of Exit of Businesses in India

‘Doing business’ is not only about seamless starts or how less cumbersome the journey can be – it is also about the certainty of freedom to exit, as and when needed. As such, a sound framework for exit is quintessential for businesses – viable or non-viable. A company might opt to liquidate itself voluntarily, or go for a scheme of merger or amalgamation or even striking off. At the same time, it must be noted that exit may not be always voluntary – sometimes, it may be forced upon the business, for example, in case of insolvent companies, creditors may prefer to liquidate the entity rather than drag it as a going concern. Some of the important considerations in making a choice are – solvency of the company, position of assets and liabilities, extent of judicial involvement, extent of flexibility in the conduct of the process, professional involvement, time involved, and costs. With the judicial authorities being clogged with cases, we may need to reinvent the infrastructural framework and take steps to make the exit process easier. The article discusses the aspects as above.

- This Article has been published in the April, 2020 issue of Chartered Secretary, issued by the Institute of Companies Secretaries of India, available at- https://www.icsi.edu/media/webmodules/linksofweeks/ICSI-April_2020.pdf

Regulator’s move to repair the NBFC sector

-Mridula Tripathi

The evolving impact on people’s health has casted a threat on their livelihoods, the businesses in which they work, the wider economy, and therefore the financial system. The outbreak of this pandemic is nothing like the crisis faced by the economies in the year 2007-08 and imperils the stability of the financial system. The market conditions have forced traders to take aggressive steps exposing the system to great volatility thereby resulting in crashing asset values. Combating the pandemic and safeguarding the economy, the financial sectors across the globe have witnessed numerous reforms to hammer the aftermaths of the global crisis. Read more →

SEBI’s proposal to aid financially “stressed” companies

-Proposal for relaxation in pricing norms for preferential issue and making an open offer

Henil Shah | Executive

Introduction

In layman’s term, a company with falling share prices, inability to pay off its obligations is said to be a company with financial distress. It’s safe to say that for such a company, one of the foremost priority is to secure a source of funds in order to fund their operations to upturn its economic conditions thereby avoiding Insolvency/Bankruptcy. Keeping the same view in mind, the Securities and Exchange Board of India (‘SEBI’) deliberated the matter to its Primary Market Advisory Committee (‘PMAC’), which identified the following key issues to be addressed in order to assist the financially stressed companies to raise funds:

- Criteria for determining a company as stressed

- Determination of a reasonable price for preferential allotment

- Exemptions from open offer obligations under the SAST Regulations

Based on the recommendations given by PMAC, SEBI on April 22, 2020 released a Consultation paper “Pricing of preferential issues and exemption from open offer for acquisitions in companies having stressed assets”[1] seeking public comments till May 13, 2020.

Rationale behind the proposed changes

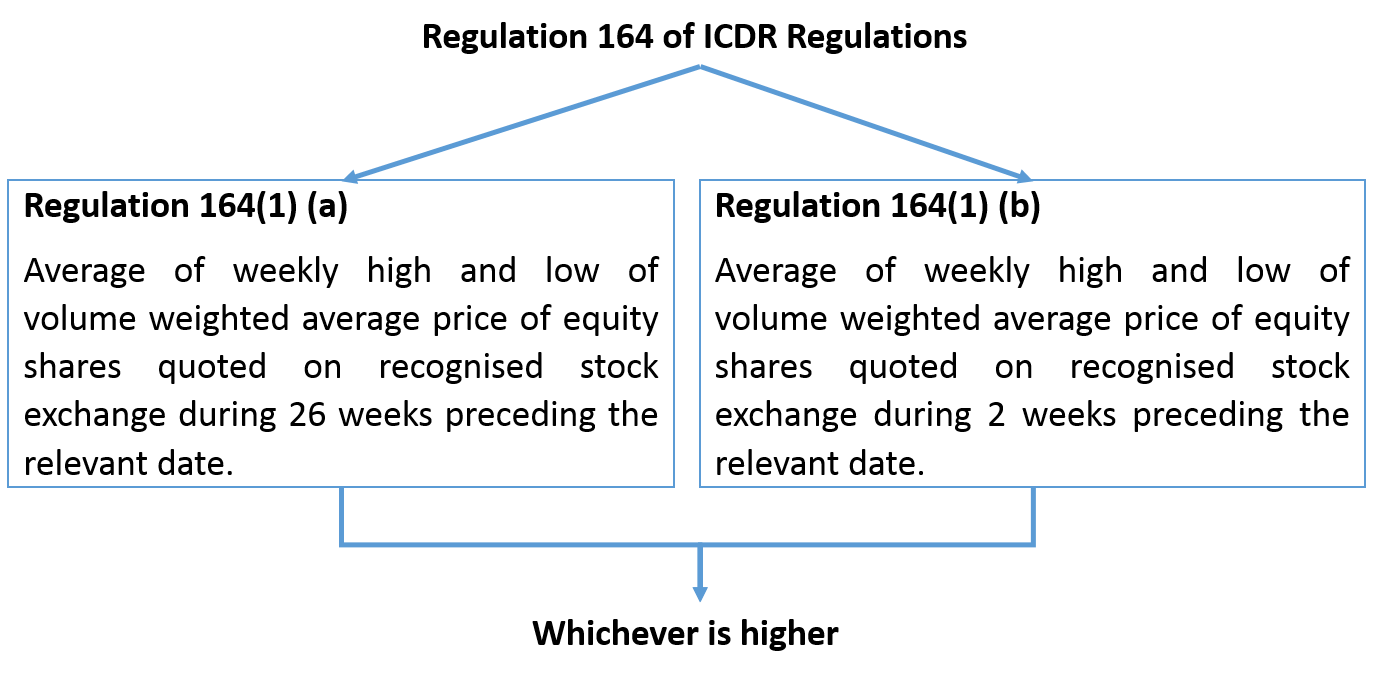

One of the key modes of raising funds by a company especially a financially distressed company is by way of preferential issue of equity shares or convertible instruments. Knowing the probable investors ready to invest in the company makes preferential issue one of the most commonly used ways for raising funds. For a listed company, under a preferential issue, the issue price has to be determined as per the pricing provisions of Chapter V of SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (“ICDR Regulations”). The ICDR Regulations provides the pricing mechanism for both frequently traded shares and infrequently traded shares. In case of frequently trades shares, the price shall be determined as per the provisions of Regulation 164(1) (a) & (b) of the ICDR Regulations which are as follows.

i. Onerous pricing mechanism

Considering the continuous falling prices of the shares over a period of 26 weeks due to the company being in stress, the determination of the price as per the pricing mechanism provided in Regulation 164(1)(a) becomes too onerous for the investor. Further, the price under Regulation 164(1)(a) is much higher than that as determined as per Regulation 164(1)(b). Hence, the pricing mechanism acts as a major deterrent for the investors from subscribing to the shares offered under the preferential issue.

ii. Exemptions only to 5 QIBs restricting investor pool

Though the ICDR Regulations allow issuance to QIBs at a price determined as per regulation 164(1) (b) however, the same is restricted to only 5 QIBs and is not applicable to the investors other than QIBs thereby restricting the investor pool.

iii. Open offer obligations for the acquirer

Another roadblock which the issuers tend to face is from the view point of the investors i.e. an incoming investor who has an impending burden on complying with an open offer obligation in case where the subscription to the preferential offer leads to the triggering of the open offer obligations under SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011(‘SAST Regulations’).

As per the extant provisions, the acquisition pursuant to a resolution plan approved under the Insolvency and Bankruptcy Code, 2016 is exempted from meeting the open offer obligations but no such exemption has been provided in case for acquisition in the financially distressed entity which are not under any resolution plan.

Therefore, where the listed entity is already under distress and suffering from a financial crisis, huge open offer obligations and the cost involved therein discourage the probable investors from taking any controlling interest in such entity.

Rescue mechanism by way of proposed changes

What will be regarded as “stressed”?

It is proposed that only such listed companies which meet any 2 (two) of the following 3 (three) conditions will be determined as a “stressed” company and shall be able to avail the benefits while making an offer under preferential issue once the proposed changes come alive.

- A listed company which has made disclosure of defaults on payment of interest/ principal amount of loans from banks/ financial institutions and listed and unlisted debt securities for 2 consequent quarters in terms of the SEBI Circular[2] issued in this regard;

Default for the purpose of the above circular shall mean non –payment of interest or principal in full on the pre-agreed due date. Provided in case of revolving facilities default shall be considered when outstanding balance remains continuously in excess of the sanctioned limit or drawing power, whichever is lower for more than 30 days.

- Existence of Inter-Creditor agreement in terms of Reserve Bank of India (Prudential Framework for Resolution of Stressed assets) Directions 2019[3];

Inter-credit agreement in terms of the RBI directions stands for agreement executed among all the lenders of a defaulting borrower, providing for ground rules for finalisation and implementation of resolution plan in respect to the borrower.

- Credit rating of the listed instruments of the company has been downgraded to “D”.

Proposal for relaxed pricing norms under the ICDR Regulations:

Unlike the current pricing requirements as provided in Regulations 164(1) (a) & (b) for a preferential issue, the price of the shares to be issued by a stressed company as aforesaid shall be a price which shall not be less than the average of the weekly high and low of the volume weighted average prices of the related equity shares quoted on a recognised stock exchange during the two weeks preceding the relevant date.

Exemptions proposed under the SAST Regulations

Where due to the subscription of shares offered under preferential issue by a financially stressed company triggers open offer obligations as per SAST Regulations, the same shall be exempted.

Additional conditions for availing the exemptions

The Consultation Paper also provides for an additional set of requirements to be complied in case were the benefits of the proposed exemptions are to be availed.

- Persons/entities that are not part of the promoter or promoter group will not be eligible to participate in the preferential issue.

- Obtaining of shareholders’ consent for the exemption to make an open offer by the proposed investors along with the proposal of preferential issue. The shareholders’ approval shall be an approval of majority of minority excluding the promoters and promoter group and any proposed allottee that already hold securities in the issuer.

- Disclosure of the proposed use of the proceeds of such preferential issue in the explanatory statement. This requirement is nothing new as the provisions of regulation 163 of ICDR Regulations and Rule 13 of the Companies (Share Capital and Debenture) Rules, 2014 do provide for mandatorily mentioning object for which the preferential issue is being made in the explanatory statement of the notice.

- Appointment of a monitoring agency. Though there is no requirement of appointing a monitoring agency as per the provisions of chapter V (Preferential Issue) requirement of ICDR Regulations, the concept of the monitoring agency is not new as several chapters of the regulations provide for appointment and functions to be performed by the monitoring agency in case where offer size exceeds a predefined limit.

- Mandatory lock in requirements of shares issued on preferential basis for 3 years which is same as provided in chapter V (Preferential issue) requirement of ICDR Regulations.

Conclusion

Considering the stressed status of the company, it is believed that aligning the pricing requirement with that of pricing requirement in case of preferential issue to QIBs, shall effectively increase the pool of investors. Similarly, the proposed exemption from making of an open offer shall lessen the additional burden on an incoming investor to comply with the stringent requirements thereby attracting investors to put in money in such companies.

Accordingly, SEBI’s intention behind the proposed changes may be said to be a welcome move as it will definitely help the financially stressed companies to revive.

Our write up on prudential framework for resolution for stressed assets can be accessed at:

https://vinodkothari.com/2019/06/fresa/

Our other write ups can be accessed at: https://vinodkothari.com/category/corporate-laws/

[1] https://www.sebi.gov.in/reports-and-statistics/reports/apr-2020/consultation-paper-preferential-issue-in-companies-having-stressed-assets_46542.html

[2] https://www.sebi.gov.in/legal/circulars/nov-2019/disclosures-by-listed-entities-of-defaults-on-payment-of-interest-repayment-of-principal-amount-on-loans-from-banks-financial-institutions-and-unlisted-debt-securities_45036.html

[3] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11580&Mode=0

Special Liquidity Facility for Mutual Funds

By Anita Baid (finserv@vinodkothari.com)

[Posted on April 27, 2020 and updated on April 30, 2020]

The Reserve Bank of India (RBI) has been vigilantly taking necessary measures and steps to mitigate the economic impact of Covid-19 and preserve financial stability. The capital market of our country has also been exposed to the disruption. The liquidity strains on mutual funds (MFs) has intensified for the high-risk debt MF segment due to redemption or closure of some debt MFs. This was witnessed when Franklin Templeton Mutual Fund[1] announced the winding up of six yield-oriented, managed credit funds in India, effective April 23, citing severe market dislocation and illiquidity caused by the coronavirus. Sensing the need of the hour and in order to ease the liquidity pressures on MFs, RBI has announced a special liquidity facility for Mutual Funds (SLF-MF)[2] of Rs. 50,000 crore.

Under the SLF-MF, the RBI shall conduct repo operations of 90 days tenor at the fixed repo rate. The SLF-MF is on-tap and open-ended, wherein banks shall submit their bids to avail funding on any day from Monday to Friday (excluding holidays) between 9 AM and 12.00 Noon. The scheme shall be open from April 27, 2020 till May 11, 2020 or up to utilization of the allocated amount, whichever is earlier. An LAF Repo issue will be created every day for the amount remaining under the scheme after deducting the cumulative amount availed up to the previous day from the sanctioned amount of Rs. 50,000 crores. The bidding process, settlement and reversal of SLF-MF repo would be similar to the existing system being followed in case of LAF/MSF. Further, the RBI will further review the timeline and amount, depending upon market conditions.

As per the press release, the RBI will provide funds to banks at lower rates and banks can avail funds for exclusively meeting the liquidity requirements of mutual funds in the following ways:

- extending loans, and

- undertaking outright purchase of and/or repos against the collateral of investment grade corporate bonds, commercial papers (CPs), debentures and certificates of Deposit (CDs) held by MFs.

Accordingly, the funds availed by banks from the RBI at the repo window will be used to extend loans to MFs, buy outright investment grade corporate bonds or CPs or CDs from them or extend the funds against collateral through a repo.

The RBI has further vide its notification dated April 30, 2020, extended the regulatory benefits under the SLF-MF scheme to all banks, irrespective of whether they avail funding from the RBI or deploy their own resources under the scheme. Banks meeting the liquidity requirements of MFs by any of the aforesaid methods, shall be eligible to claim all the regulatory benefits available under SLF-MF scheme without the need to avail back to back funding from the RBI under the SLF-MF.

It is important to note that in terms of regulation 44(2) of the SEBI (Mutual Funds) Regulations, 1996[3], a MF shall not borrow except to meet temporary liquidity needs of the MFs for the purpose of repurchase, redemption of units or payment of interest or dividend to the unit holders and, further, the mutual fund shall not borrow more than 20% of the net asset of the scheme and for a duration not exceeding six months.

As per the aforesaid SEBI regulations, MFs should normally meet their repurchase/redemption commitments from their own resources and resort to borrowing only to meet temporary liquidity needs. Therefore, under the SLF-MF scheme as well banks will have to be judicious in granting loans and advances to MFs only to meet their temporary liquidity needs for the purpose of repurchase/redemption of units within the ceiling of 20% of the net asset of the scheme and for a period not exceeding 6 months. While banks will decide the tenor of lending to /repo with MFs, the minimum tenor of repo with RBI will be for a period of three months.

Similar to the incentives given to the banks in case of LTRO schemes, the following shall be available for banks extending funding under the SLF-MF-

- the liquidity support availed under the SLF-MF would be eligible to be classified as held to maturity (HTM) even in excess of 25% of total investment permitted

- Exposures under this facility will not be reckoned under the Large Exposure Framework (LEF)

- The face value of securities acquired under the SLF-MF and kept in the HTM category will not be reckoned for computation of adjusted non-food bank credit (ANBC) for the purpose of determining priority sector targets/sub-targets

- Support extended to MFs under the SLF-MF shall be exempted from banks’ capital market exposure limits.

The RBI’s move is much needed to ease the liquidity stress on the MF industry. However, as has been seen in the TLRTO 2.0 auctions, banks are taking a cautious approach before using this facility provided by RBI. However, it is expected that this will ensure easing of liquidity and also boost investor sentiment.

[1] With assets worth more than Rs 86,000 crore as of the end of March, Franklin Templeton is the ninth largest mutual fund in the country

[2] https://www.rbi.org.in/scripts/BS_PressReleaseDisplay.aspx?prid=49728

[3] Last updated on March 6, 2020- https://www.sebi.gov.in/legal/regulations/mar-2020/securities-and-exchange-board-of-india-mutual-funds-regulations-1996-last-amended-on-march-06-2020-_41350.html

Further Issue of Shares | Overview of Basic Concepts

Further issue of shares and security is the most basic and most frequently used activity by companies as well professionals, therefore, there is a need to be clear on the very basic concepts involved in it.

This presentation deals with discussing the basic concepts and at the same time critically discussing various issues involved like rights issue of convertible debentures, deemed public issue, overlap of section 62(1) (c) and section 42, etc. We hope you find this useful.

Please click here for the PPT used in the presentation.

Please click below to view the presentation:

https://youtu.be/IuT0oJOvLOQ

Restructuring of bonds during COVID-19 crisis

This presentation covers the procedural requirements for restructuring of bonds/debentures during COVID-19 crisis.

Please click below for the presentation:

Part-1:

Please click here for the PPT used in the presentation.

Cross Border Mergers

As the global economy becomes more and more intertwined, the trend of cross border mergers and amalgamations have accelerated..

In the presentation below, we discuss the concept of Cross border mergers in light of the extant provisions, and its practical aspects- Click here

An audio presentation of the same is also available at- https://youtu.be/jHVIajr2q00