Introduction to FEMA (NDI) Rules, 2019 and recent amendments

For relevant questions discussed during the webinar, click here.

For relevant questions discussed during the webinar, click here.

Ambika Mehrotra & Ankit Vashishth

In line with various other relaxations introduced by the Securities and Exchange Board of India (‘SEBI’), amid the global pandemic, it has now come up with a Circular dated 21st April, 2020 [1]granting temporary relief under certain provisions of the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (‘ICDR regulations’) in respect of Rights Issue. The rights issues opening on or before March 31, 2021 will get benefited from the said Circular.

It goes without saying that during the period of this of economical breakdown, the industrial undertakings are in need of funds for various purposes. In this hour of crisis, SEBI’s move seems to ease out the stringent requirements in the statues which hamper the facility of raising funds by companies especially through rights issue.

The amended provisions broadly serve the intent of having a relatively flexible eligibility criteria for a fast track rights issue and lesser chances of refund of the amount in case of non- receipt of subscription amount.

A snapshot of the relaxations and their impact is enlisted below: –

| Relevant Regulation

|

Pre- amendment | Post-amendment | Impact Analysis |

| 99(a) | the equity shares of the issuer have been listed on any stock exchange for a period of at least three years immediately preceding the reference date

|

the equity shares of the issuer have been listed on any stock exchange for a period of at least eighteen months immediately preceding the reference date

|

Relaxation in the pre-condition with respect to listing of equity shares from 3 years to 18 months. |

| 99(c ) | the average market capitalisation of public shareholding of the issuer is at least two hundred and fifty crore rupees

|

the average market capitalisation of public shareholding of the issuer is at least one hundred crores

|

Companies with smaller market size i.e. more Rs. 100 crore and above also permitted to enter into Fast Track Issue. |

| 99(f) and its proviso | the issuer has been in compliance with the equity listing agreement or the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, as applicable, for a period of at least three years immediately preceding the reference date:

Provided that if the issuer has not complied with the provisions of the listing agrîment or the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, as applicable, relating to composition of board of directors, for any quarter during the last three years immediately preceding the reference date, but is compliant with such provisions at the time of filing of letter of offer, and adequate disclosures are made in the letter of offer about such non-compliances during the three years immediately preceding the reference date, it shall be deemed as compliance with the condition; |

the issuer has been in compliance with the equity listing agreement or the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, as applicable, for a period of at least eighteen months immediately preceding the reference date:

Provided that if the issuer has not complied with the provisions of the listing agreement or the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, as applicable, relating to composition of board of directors, for any quarter during the last eighteen months immediately preceding the reference date, but is compliant with such provisions at the time of filing of letter of offer, and adequate disclosures are made in the letter of offer about such non-compliances during the three years immediately preceding the reference date, it shall be deemed as compliance with the condition;

|

The timeline for being in compliance with listing regulations has been reduced from 3 years to 18 months.

This is in line with the requirement under Regulation 99(a) wrt listing of equity shares for a period of atleast 18 months instead of 3 years. |

| 99(h) | No show-cause notices have been issued or prosecution proceedings have been initiated by the SEBI and pending against the issuer or its promoters or whole-time directors as on the reference date. | No show-cause notices, excluding under adjudication proceedings, have been issued by the SEBI and pending against the issuer or its promoters or whole-time directors as on the reference date.

In cases where against the issuer or its promoters/ directors/ group companies,

i. a show cause notice(s) has been issued by the Board in an adjudication proceeding or

ii. prosecution proceedings have been initiated by the Board; necessary disclosures in respect of such action (s) along-with its potential adverse impact on the issuer shall be made in the letter of offer. |

Regulation 99(h) restricts the company to make fast track rights issue in case there had been any show-cause notices or prosecution proceedings issued/initiated against the company/ its promoters/ WTDs.

The temporary relaxation however allows the company to be eligible for rights issue to the extent where adjudication proceedings or prosecution proceedings in respect of the above as well as the group companies are concerned, on making the required disclosures in this regard and its adverse impact, in the letter of offer |

| 99(i) | the issuer or promoter or promoter group or director of the issuer has not settled any alleged violation of securities laws through the consent or settlement mechanism with the Board during three years immediately preceding the reference date;

|

The issuer or promoter or promoter group or director of the issuer has fulfilled the settlement terms or adhered to directions of the settlement order(s) in cases where it has settled any alleged violation of securities laws through the consent or settlement mechanism with the Board. | Prior to the relaxation, any violation in the securities laws by the issuer/ promoter/ promoter group/ director made the issuer ineligible. This however has now been relaxed to permit the issue in case the above violators, having violated the securities laws at anytime during the past have fulfilled the settlement terms or followed the directions under the settlement order(s) |

| 99(j) | The equity shares of the issuer have not been suspended from trading as a disciplinary measure during last 3 years immediately preceding the reference date. | The equity shares of the issuer have not been suspended from trading as a disciplinary measure during last 18 months immediately preceding the reference date. | In line with Regulation 99(a) and (f) |

| 99(m) | There are no audit qualifications on the audited accounts of the issuer in respect of those financial years for which such accounts are disclosed in the letter of offer | For audit qualifications, if any, in respect of any of the financial years for which accounts are disclosed in the letter of offer, the issuer shall provide the restated financial statements adjusting for the impact of the audit qualifications.

Further, that for the qualifications wherein impact on the financials cannot be ascertained the same shall be disclosed appropriately in the letter of offer. |

Prior to the Circular, any qualification in the audit report led to ineligibility. This condition has now been re-framed to make the companies eligible on providing the restated financial statements adjusting for the impact of the audit qualifications or providing clarifications in case such impact cannot be ascertained |

| Relevant Regulation

|

Pre- amendment | Post-amendment | Remarks |

| 86(1) | The minimum subscription to be received in the issue shall be at least ninety per cent. of the offer through the offer document. | The minimum subscription to be received in the issue shall be at least seventy five percent of the offer through the offer document.

Provided that if the issue is subscribed between 75% to 90%, issue will be considered successful subject to the condition that out of the funds raised atleast 75% of the issue size shall be utilized for the objects of the issue other than general corporate purpose. |

The minimum subscription amount has been reduced from 90% to 75%.

However, the Circular seems to put another restriction on the utilization of atleast 75% of the funds for the objects of the issue other than general corporate purpose if the actual subscription goes beyond 75% but within 90% of the offer. |

| Relevant Regulation

|

Pre- amendment | Post-amendment | Remarks |

| Applicability of the Regulations:

3(b) |

rights issue by a listed issuer; where the aggregate value of the issue is ten crore rupees or more;

|

rights issue by a listed issuer; where the aggregate value of the issue is twenty-five crores or more;

|

The conditions prescribed in Chapter III of ICDR Regulations shall not apply in case of Rights Issue carrying an issue size of less than Rs. 25 crores. |

|

Proviso to Reg. 3 |

Provided that in case of rights issue of size less than ten crore rupees, the issuer shall prepare the letter of offer in accordance with requirements as specified in these regulations and file the same with the Board for information and dissemination on the Board’s website. | Provided that in case of rights issue of size less than twenty-five crore rupees, the issuer shall prepare the letter of offer in accordance with requirements as specified in these regulations and file the same with the Board for information and dissemination on the Board’s website. | The change is made considering the revised limit of applicability of the Regulations for a rights issue. |

|

60 |

Unless otherwise provided in this Chapter, an issuer offering specified securities of aggregate value of ten crore rupees or more, through a rights issue shall satisfy the conditions of this Chapter | Unless otherwise provided in this Chapter, an issuer offering specified securities of aggregate value twenty-five crore rupees or more, through a rights issue shall satisfy the conditions of this Chapter. | The change is made considering the revised limit of applicability of the Regulations for a rights issue. |

In addition to the above Circular, SEBI has also issued another circular on the same date i.e. April 21, 2019[2] for granting one-time relaxation on the basis of the representations received from various stakeholders with respect to the opening of issue period within 12 months from the date of issuance of the observations by SEBI, for an Initial Public Offer (IPO), Further Public Offer (FPO) or Rights Issue as per Regulation 44, 140 and 85 respectively of the ICDR Regulations, expiring during this period of lockdown i.e. between March 1, 2020 and September 30, 2020 to be extended by 6 months, from the date of expiry of the above-mentioned observations received from SEBI.

However, the extension to this issue opening period shall be granted on obtaining an undertaking from lead manager of the issue confirming compliance with Schedule XVI of the ICDR Regulations with respect to the nature of changes in the offer document which require filing of updated offer document, while submitting the updated offer document to SEBI.

These temporary relaxations will surely bring in a sigh of relief for the stakeholders including the companies intending to raise funds through rights issue, during this interim period of disruption due the outbreak of COVID-19, considering the stagnancy of operations in the country.

Read our related articles below –

SEBI ICDR Regulations, 2018– Snapshot on changes in rights, bonus, QIP and preferential issue;

SEBI (ICDR) Regulations, 2018-Key Amendments;

Covid-19 – Incorporated Responses | Regulatory measures in view of COVID-19.

[1] https://www.sebi.gov.in/legal/circulars/apr-2020/relaxations-from-certain-provisions-of-the-sebi-issue-of-capital-and-disclosure-requirements-regulations-2018-in-respect-of-rights-issue_46537.html

[2] https://www.sebi.gov.in/legal/circulars/apr-2020/one-time-relaxation-with-respect-to-validity-of-sebi-observations_46536.html

-Munmi Phukon, Pammy Jaiswal and Richa Saraf (corplaw@vinodkothari.com)

ICRA has published a report on 23.04.2020[1], listing out some 328 entities[2] who have availed or sought a payment relief from the lending institutions or investors. The list also includes names of such entities that have received an in-principle approval from investors in their market instruments (like non-convertible debentures)- prior to the original due date- for shifting the original due date ahead, but where a formal approval from the investors was received either after the original due date or is still pending to be received.

Earlier, Securities and Exchange Board of India (SEBI) had, vide circular no. SEBI/ HO/ MIRSD/ CRADT/ CIR/ P/ 2020/53 dated 30.03.2020[3], addressed to the credit rating agencies (CRAs), granted certain relaxation from compliance with certain provisions of the circulars issued under SEBI (Credit Rating Agencies) Regulations, 1999 due to the COVID-19 pandemic. The circular stipulated that appropriate disclosures in this regard shall be made in the press release, seemingly, the report published by ICRA is a part of the disclosure requirement specified by SEBI.

In view of the COVID crisis, companies in large numbers are approaching investors or will be approaching investors for restructuring of the debentures, therefore, it becomes pertinent to discuss- how the restructuring is carried on? whether a meeting of debenture holders will be required to be convened? what will be the consequences if the restructuring is not done? and other related questions. Below we discuss the same.

In financial terms, “default” means failure to pay debts, whether principal or interest. Under ISDA Master Agreement[4], failure by the party to make, when due, any payment is listed as an event of default and one of the termination events. However, the ISDA Master Agreement provides that in case of a force majeure event, payments can be deferred. Most of the standard agreements, contain specific clauses pertaining to force majeure, where the party required to perform any contractual obligation is required to intimate the other party as soon as it becomes aware of happening of any force majeure event. While in some cases, due to impossibility of performance, the agreement itself is frustrated; in some other cases, the obligations are merely deferred till the event persists.

Our article “COVID- 19 and The Shut Down: The Impact of Force Majeure” can be accessed from the link: https://vinodkothari.com/2020/03/covid-19-and-the-shut-down-the-impact-of-force-majeure/

A debenture holder has several options available in case of default: (a) insolvency proceedings; (b) enforcement of security interest; (c) proceedings for recovery of debt due. Below we discuss the same:

– Right to call for meeting of debenture holders: Rule 18 (4) of the Companies (Share Capital and Debentures) Rules, 2014 stipulates that the meeting of all the debenture holders shall be convened by the debenture trustee on:

– Right to make an application before NCLT: Section 71(10) of the Companies Act, 2013 provides that on failure of the company to redeem the debentures on the date of their maturity or failure to pay interest on the debentures when it is due, an application may be filed by any or all of the debenture holders or debenture trustee, seeking redemption of the debentures forthwith on payment of principal and interest due thereon.

– Application under IBC: Section 5(7) of IBC defines a “financial creditor” to mean any person to whom a financial debt is owed and includes a person to whom such debt has been legally assigned or transferred to, and Section 5(8) of IBC defines “financial debt” as a debt along with interest, if any, which is disbursed against the consideration for the time value of money and includes any amount raised pursuant to any note purchase facility or the issue of bonds, notes, debentures, loan stock or any similar instrument. Thus, debenture holders are treated as financial creditors for the purpose of IBC and may exercise all the rights as available to a financial creditor.

As per Section 6 of IBC-“Where any corporate debtor commits a default, a financial creditor, an operational creditor or the corporate debtor itself may initiate corporate insolvency resolution process in respect of such corporate debtor in the manner as provided under this Chapter”. Accordingly, the debenture holders (whether secured or not) may apply for initiation of corporate insolvency resolution process against the company under Section 7 of IBC. In fact the Central Government has, vide notification no. S.O. 1091(E) dated 27th February, 2019, notified that such right may also be exercised by the debenture holder, through a debenture trustee.

– Right to enforce security interest: The right of foreclosure is a counter-part of right of redemption. Just like a company has a right of redeeming the security after payment of debt amount, a secured debenture holder has a right of foreclosure or sale in case of default in redemption. In the case of Baroda Rayon Corporation Limited vs. ICICI Limited[5] and in Canara Bank vs. Apple Finance Limited[6], Bombay High Court upheld the right of the debenture trustee to sell off the properties of the company for the benefit of the debenture holders.

Here, it is pertinent to understand how the debenture holders shall exercise the right of foreclosure. The law distinguishes between security interests based on the nature of the collateral. For instance, in case of security interests on immovable properties, Chapter IV of Transfer of Property Act, 1882 applies. Further, the security interest, in case of secured debentures, can be enforced in the following manner: (a) In case the debenture holder is a bank/ financial institution, as per the provisions of Securitisation and Reconstruction of Financial Assets and Enforcement of Securities Interest Act, 2002; and (b) In case the debenture holder is not a bank/ financial institution, as per the common law procedures.

– Other remedies: Any default in the terms of the debentures is a breach of contract, and the debenture holder may sue the company for breach of contract as per the provisions of Contract Act, 1872, and further seek for compensation as per the terms of the debenture, or in absence of specific term in the agreement, compensation may be claimed as per the provisions of Section 73 of the Contract Act, 1872.

In view of the COVID pandemic one of the issue that was arising was that the issuers of debt instruments who were not able to fulfil the obligations as per the terms of the debentures or redeem the same on the maturity date were running to courts for seeking interlocutory reliefs, seeking to restrain the debenture holders from exercising any rights against the defaulting issuer. In the case of Indiabulls Housing Finance Ltd. vs. SEBI[7], the petitioner prayed for an ad interim direction to restrain any coercive action against it, with respect to the repayment to be made by it to its non-convertible debenture holders. In the said case, granting the prayer, the Hon’ble Delhi High Court directed maintenance of status quo with respect to the repayments to be made by the petitioner to the NCD holders.

Further, there was a lack of clarity on how rating and valuation of a security would be revised in view of the default or the restructuring? Therefore, SEBI has issued the following circulars:

With respect to recognition of default, the circular stipulates that CRAs recognize default based on the guidance issued vide SEBI circular dated May 3, 2010[9] and November 1, 2016[10], however, based on its assessment, if the CRA is of the view that the delay in payment of interest/principle has arisen solely due to the lockdown conditions creating temporary operational challenges in servicing debt, including due to procedural delays in approval of moratorium on loans by the lending institutions, CRAs may not consider the same as a default event and/or recognize default.

In the context of COVID, the restructuring of debentures shall mean nothing but deferral of the date of redemption. The terms of the debentures, including the maturity date, etc is specified in the terms of issuance. The terms of issuance also provides how the variation in terms can be effectuated. Therefore, it is pertinent that to make any changes in terms of debentures, the relevant clauses in the issuance terms are considered.

In terms of Reg. 59 (2) of the SEBI LODR Regulations, 2015, any material modification to the structure of debentures in terms of coupon redemption etc. are required to approved by the Board of Directors and the debenture trustee (DT). Further, in terms of Reg. 59(1), prior approval of the stock exchange(s) shall also be required for such material modification which shall be given by the stock exchange(s) only after obtaining the approval of the Board and the DT.

In addition to the approval as aforesaid, in terms of Regulation 15(2)(b) of SEBI DT Regulations, DT is required to call a meeting of the debenture holders on happening of any event which in the opinion of the DT affects the interest of the holders. Similar provision is there in the Companies (Share Capital and Debenture) Rules, 2014 also [sub- rule (4) of Rule 18].

Unlike the requirements of obtaining shareholders’ consent by way of special/ ordinary resolution for various matters including variation of rights thereof, there is no explicit provision for obtaining of a consent of the debenture holders for restructuring of the debentures under the Companies Act, 2013 (‘CA 13’). However, the provisions of SS 2 being, mutatis mutandis, applicable to a meeting of debenture holders also, all the provisions w.r.t convening/ conducting of general meeting such as, sending of notice, explanatory statement etc. as applicable to general meetings shall apply to the meeting of debenture holders.

However, looking at the current crisis situation, where calling of a physical meeting is not possible, and issuers will be required to hold the meeting of the debenture holders, in case consent by e-mail is not possible due to the large number of debenture holders, through video conferencing mode. The modalities for participation (like voting, two-way communication, recording, etc.) and other compliances related of sending of notices etc. may be in the manner clarified by the MCA Circular dated 13.04.2020[13].

In a nutshell, the procedural requirements to be followed for restructuring of debentures shall be as provided hereunder.

| S. No

|

Relevant Provisions | Actionable/ Compliance | Remarks |

| 1. | Regulation 50 (3) of LODR Regulations | Prior intimation to the stock exchange (SE) for the meeting board of directors, at which the restructuring is proposed to be considered.

|

2 working days in before the board meeting.

(excl. date of intimation and date of meeting) |

| 2. | Sec. 173 of CA 13 | BM to be convened by the Company for proposed restructuring including the revised terms subject to approval of the stock exchanges and the debenture holders.

|

Through VC considering the COVID 19 Guidelines issued by the Govt. Our FAQs in this regard may be found at : https://www.google.com/url?q=https://vinodkothari.com/2020/03/board-meetings-during-shutdown/&sa=D&source=hangouts&ust=1587820272757000&usg=AFQjCNEictCwK_-LNnlH7oiB1GMmdRzO6w

|

| 3. | Regulation 59(2)(a) of LODR Regulations

|

Obtain approval of the DT | Before applying to SEs. |

| 4. | Regulation 59 of the Listing Regulations | Seek prior approval from the stock exchange

|

After taking the consent of the board of directors and DT.

|

| 5. | Regulation 15(2) of DT Regulations, 1993 | Separate meeting of debenture holders to be called for deferment in repayment due to liquidity crunch in the hour of crisis.

|

The meeting may be called by the company itself or through the DT.

Since the scope of SS 2 issued by ICSI includes meetings of debenture holders also, the company will have to observe the requirements of SS 2 in convening the meeting of debenture holders. However, considering the current crisis situation, such meeting may be convened through VC facility as clarified by MCA Circular dated 13th April, 2020. Our FAQs in this regard may be found at https://vinodkothari.com/2020/04/general-meetings-by-video-conferencing-recognising-the-inevitable/

|

| 6. | Regulation 51 (2) of the Listing Regulations | Intimation to the stock exchanges being an action that shall affect payment of interest or redemption of NCDs

|

ASAP but not later than 24 hours of Board decision. |

In usual circumstances, if any variation is carried out in the debenture terms, the parties enter into an addendum, amending the clauses contained in the debenture subscription agreement (and also, in the trust deed/ security documents, if required), however, given the current scenario and the lock down, it is not possible for parties to sign and execute the agreements. Since the restructuring already has the approval of the majority debenture holders, it is deemed that the resolution “overrides the terms of issuance”. Thus, in our view, the resolution passed by the debenture holders approving the restructuring should suffice, and modification in the agreements may not be required.

[1] https://www.icra.in/Rationale/ShowRationaleReport/?Id=94320

[2] The rating agency has stated that the list is not a comprehensive one, as information about some rated entities are not readily available as of now, and separate disclosures will be made w.r.t. such entities.

[3]https://www.sebi.gov.in/legal/circulars/mar-2020/relaxation-from-compliance-with-certain-provisions-of-the-circulars-issued-under-sebi-credit-rating-agencies-regulations-1999-due-to-the-covid-19-pandemic-and-moratorium-permitted-by-rbi-_46449.html

[4] https://www.sec.gov/Archives/edgar/data/1065696/000119312511118050/dex101.html

[5] 2002 (2) BomCR 608, (2002) 2 BOMLR 915, 2003 113 CompCas 466 Bom, 2002 (2) MhLj 322

[6] AIR 2008 Bom 16, (2007) 77 SCL 92 Bom

[7]https://images.assettype.com/barandbench/2020-04/6ec54849-0188-4fe3-a841-88c2861124d5/Indiabulls_vs_SEBI.pdf

[8]https://www.sebi.gov.in/legal/circulars/mar-2020/relaxation-from-compliance-with-certain-provisions-of-the-circulars-issued-under-sebi-credit-rating-agencies-regulations-1999-due-to-the-covid-19-pandemic-and-moratorium-permitted-by-rbi-_46449.html

[9] https://www.sebi.gov.in/legal/circulars/may-2010/guidelines-for-credit-rating-agencies_1467.html

[10]https://www.sebi.gov.in/legal/circulars/nov-2016/enhanced-standards-for-credit-rating-agencies-cras-_33585.html

[11]https://www.sebi.gov.in/legal/circulars/apr-2020/review-of-provisions-of-the-circular-dated-september-24-2019-issued-under-sebi-mutual-funds-regulations-1996-due-to-the-covid-19-pandemic-and-moratorium-permitted-by-rbi_46549.html

[12] https://www.sebi.gov.in/legal/circulars/sep-2019/valuation-of-money-market-and-debt-securities_44383.html

[13] http://www.mca.gov.in/Ministry/pdf/Circular17_13042020.pdf

Please click below for youtube presentation on the above topic:

Our other content related to COVID-19 disruption may be referred here: https://vinodkothari.com/covid-19-incorporated-responses/

Our other articles relating to restructuring on account of COVID-19 disruption may also be viewed here:

Our presentation can be viewed here – https://vinodkothari.com/2021/09/structuring-of-debt-instruments/

-Vinod Kothari (vinod@vinodkothari.com)

Economic recoveries in the past have always happened by increasing the supply of credit for productive activities. This is a lesson that one may learn from a history of past recessions and crises, and the efforts made by policymakers towards recovery. [See Appendix]

The above proposition becomes more emphatic where the disruption is not merely economic – it is widespread and has affected common life, as well as working of firms and entities. There will be major effort, expense and investment required for restarting economic activity. Does moratorium merely help? Moratorium possibly helps avoiding defaults and insolvencies, but does not help in giving the push to economic activity which is badly needed. Entities will need infusion of additional finance at this stage.

The usual way governments and policy-makers do this is by releasing liquidity in the banking system. However, there are situations where the banking system fails to be an efficient transmission device for release of credit, for reasons such as stress of bad loans in the banking system, lack of efficient decision-making, etc.

In such situations, governments and central banks may have to do direct intervention in the market. Governments and central banks don’t do lending – however, they create institutions which promote lending by either banks or quasi-banks. This may be done in two ways – one, by infusion of money directly, and two, by ways of sovereign guarantee, so as to do credit risk transfer to the sovereign. The former method has the limit of availability of resources – governments have budgetary limitations, and increased public debt may turn counter-productive in the long-run. However, credit risk transfer can be an excellent device. Credit risk transfer also seems to be creating, synthetically, the same exposure as in case of direct lending by the sovereign; however, there are major differences. First, the sovereign does not have to go for immediate borrowings. Second and more important, the perceived risk transfer, where credit risk is shifted to the sovereign, may not actually hit in terms of credit losses, if the recovery efforts by way of the credit infusion actually bear fruit.

The write-up below suggests a product that may be supported by the sovereign in form of partial credit risk guarantee.

For the sake of convenience, let us call this product a “wrap loan”. Wrap-around mortgage loans is a practice prevalent in the US mortgage market, but our “wrap loan” is different. It is a form of top-up loan, which does not disturb the existing loan terms or EMI, and simply wraps the existing loan into a larger loan amount.

Let us assume the following example of, say, a loan against a truck or a similar asset:

| Original Loan amount | 1000000 | |||

| Rate of interest | 12% | |||

| Tenure | 60 | Months | ||

| EMIs | ₹ 22,244.45 | |||

| Number of months the loan has already run | 24 | Months | ||

| Number of remaining months of original loan term | 36 | Months | ||

| Principal outstanding (POS) on the date of wrap loan | ₹ 6,69,724.82 | |||

For the sake of convenience, we have not considered any moratorium on the loan[1]. The customer has been more or less regular in making payments. As on date, he has paid 24 EMIs, and is left with 36. Now, to counter the impact of the disruption, the lender considers an additional loan of Rs 50000/-. Surely, for assessing the size of the wrapper loan, the lender will have to consider several things – the LTV ratio based on the increased exposure and the present depreciated value of the asset, the financial needs of the borrowers to restart his business, etc.

With the additional infusion of Rs 50000, the outstanding exposure now becomes Rs 719725/-. We assume that the lender targets a slightly higher interest for the wrapper part of the loan of Rs 50000, say 14%. The justification for the higher interest can be that this component is unsecured. However, we do not want the existing EMI, viz., Rs 22244/- to be changed. That is important, because if the EMIs were to go up, there will be increasing pressure on the revenues of the borrower, and the whole purpose of the wrap loan will be frustrated.

Therefore, we now work the increased loan tenure, keeping the EMIs the same, for recovering the increased principal exposure. The revised position is as follows:

| POS on the date of wrap loan | ₹ 6,69,724.82 | ||

| Additional loan amount | 50000 | ||

| Interest on the additional loan | 14% | ||

| Blended interest rate | 12.139% | ||

| Revised loan tenure | 39.39 | months | |

| total maturity in months (rounded up) | 40 | months | |

| Number of whole months | 39 | months | |

| Fractional payment for the last month | ₹ 8,664.67 | ||

Note that the blended rate is the weighted average, with interest at the originally-agreed rate of 12% on the existing POS, and 14% on the additional amount of lending. The revised tenure comes to 39.39 months, or 40 months. There will be full payment for 39 months, and a fractional payment in the last month.

Thus, by continuing his payment obligation for 3-4 more months, the borrower can get Rs. 50000/- cash, which he can use to restart his business operations.

The multiplier impact that this additional infusion of cash may have in his business may be substantial.

Now, we bring the key element of the structure. The lender, say a bank or NBFC, will generally be reluctant to take the additional exposure of Rs 50000, though on a performing loan. However, this may be encourage by the sovereign by giving a guarantee for the add-on loan.

The guarantee may come with minimal actual risk exposure to the sovereign, if the structure is devised as follows:

The whole structure may be made more practical by moving from a single loan to a pool of loans. The sovereign guarantee may be extended to a pool of similar loans, with a prescription of a minimum number, maximum concentration per loan, and other diversity parameters. The moment we move from a single loan to a pool of loans, the sharing of losses between the sovereign and the originator will now be on a pool-wide basis. Even if the originator takes a first loss share of, say, 10%, and the sovereign’s share comes thereafter, the chances of the guarantee hitting the sovereign will be very remote.

And of course, the sovereign may also charge a reasonable guarantee fee for the mezzanine guarantee.

Since the wrapper loan is guaranteed by the sovereign, the lender may hope to get risk weight appropriate for a sovereign risk. Additional incentives may be given to make this lending more efficient.

‘The first set of tools, which are closely tied to the central bank’s traditional role as the lender of last resort, involve the provision of short-term liquidity to banks and other depository institutions and other financial institutions. A second set of tools involved the provision of liquidity directly to borrowers and investors in key credit markets. As a third set of instruments, the Federal Reserve expanded its traditional tool of open market operations to support the functioning of credit markets, put downward pressure on longer-term interest rates, and help to make broader financial conditions more accommodative through the purchase of longer-term securities for the Federal Reserve’s portfolio.’[2]

‘During a financial crisis, such “liquidity shock chains” can operate in reverse. Firms that face tightening financing constraints as a result of bank credit contraction may withdraw credit from their customers. Thus, they pass the liquidity shock up the supply chain; that is, their customers might cut the credit to their customers, and so on…..Thus, the supply chains might propagate the liquidity shocks and exacerbate the impact of the financial crisis.’[3]

Therefore, many of the policy remedies proposed to alleviate credit crunches were, in fact, used during the early stages of the 2008 financial crisis to mitigate potential credit availability problems. These remedies included capital infusions into troubled banks, the provision of liquidity facilities by the Federal Reserve, and, in the initial stress test, a primary focus on raising bank capital rather than allowing banks to shrink assets to maintain, or regain, required capital ratios.[4]

‘First, the effect of credit supply on value added is not detectable in the years before the great recession, indicating that credit supply is more relevant during an economic downturn. Second, the reduction in credit supply also explains the decline in employment even if the estimated effect is lower than that on value added. As a result, we can also detect a significant impact on labor productivity, while there is no effect on exports and on firm demographics. Third, the role of credit supply does vary across firms’ size, economic sectors, degree of financial dependence and, consequently, across geographical areas. Specifically, the impact is concentrated among small firms and among those operating in the manufacturing and service sectors. The impact is also stronger in the provinces that depend more heavily on external finance’[5]

[1] In fact, the wrap loan could have been an effective alternative to the moratorium

[2] https://www.federalreserve.gov/monetarypolicy/bst_crisisresponse.htm

[3] http://siteresources.worldbank.org/INTRANETTRADE/Resources/TradeFinancech01.pdf

[4] https://www.bostonfed.org/-/media/Documents/Workingpapers/PDF/economic/cpp1505.pdf

[5] https://www.bancaditalia.it/pubblicazioni/temi-discussione/2016/2016-1057/en_tema_1057.pdf

Our other content relating to COVID-19 disruption may be referred here: https://vinodkothari.com/covid-19-incorporated-responses/

Our FAQs on moratorium may be referred here: https://vinodkothari.com/2020/03/moratorium-on-loans-due-to-covid-19-disruption/

-Sikha Bansal & Megha Mittal

The past year has seen several reforms and amendments in the insolvency framework, be it enforcement of provisions for individual insolvency, or inclusion of FSPs under the insolvency regime. Additionally, Committees have been actively working on two extremely relevant aspects which presently the Code does not provide for- Group Insolvency and Cross Border Insolvency.

In our presentation (link given below) we have tried to collate the recent amendments and the workings of the Committee reports so as to provide a one-stop reference for reforms as on Mar’20- see here

-Financial Services Division (finserv@vinodkothari.com)

Unprecedented crises call for unprecedented measures; the good thing is that all regulators are responding soon enough to the need for tweaking regulations, valuation rules, provisioning norms, accounting norms, and so on, to allow companies to adjust themselves to the new world that we are being ushered in.

SEBI has come up with a Circular no SEBI/HO/IMD/DF3/CIR/P/2020/70 dated 23rd April, 2020[1] (Circular), to the effect that mutual funds will not have to treat restructuring of a debt security as a case of “default”. With this, the funds have been able to avert having to make as much as 50% provision for what was deemed as a case of default.

It is notable that there have been court rulings whereby companies have evoked the “force majeure” clause to seek breather to repayment of debt securities[2].

Given the sensitiveness of the situation, this Circular has come as breather for a lot of financial sector entities, especially the ones actively engaged in securitisation, and ofcourse mutual funds. This write-up intends to first set a context to the Circular and then discuss the potential impact of the Circular.

A circular on valuation of money market and debt securities[3] issued by SEBI stated that “Any extension in the maturity of a money market or debt security shall result in the security being treated as “Default”, for the purpose of valuation”.

As per the valuation norm, mentioned above, mutual funds are required to take a haircut on the value of debt securities declared as default. In this regard, AMFI[4] has issued benchmarks for haircuts, based on which the valuation agencies are required to consider haircut as high as 50%, thereby reducing the value of the securities to half.

This circular turned out to be a major stumbling block for the mutual funds while extending the tenure of PTC transactions vis-à-vis the RBI’s moratorium on term loans in the wake of COVID 19 pandemic. The same has been discussed at length in the following section.

On March 27, 2020, the Reserve Bank of India (RBI) introduced COVID-19 Regulatory Package[5] which provided for moratorium on payment of instalments for term loans falling due between 1st March, 2020 and 31st May, 2020[6]. The moratorium has to be extended to all the loans, irrespective of whether they have been sold off by the originators by way of securitisation or direct assignment.

The moratorium as per the RBI’s framework, forced the originators to alter the payout structures originally agreed with the investors under PTC/ DA transactions, so as to pass on effect of moratorium to the investors as well. However, the problem arose when the matter was placed before mutual funds. The mutual funds are major investors in PTCs, representing approximately 43% of securitisation issuances in India[7]. The mutual funds became wary of any extension or modification in the terms of the PTCs, due to apprehensions on valuation losses due to reasons discussed earlier in this write-up.

This created a deadlock between the originators and mutual funds (as investors). On one hand, there was a pressure on the originators to extend moratorium across all the borrowers, on the other hand, the mutual funds were apprehensive in accepting the revised terms due to a potential valuation loss.[8]

Considering the situation, the SEBI issued the Circular to address the issues with respect to valuation of debt securities.

Restructuring by deferral of the maturity is something that may be done in case of debentures as well. Debentures may have been (a) private placed; or (b) publicly offered. The former is the more common route for mutual funds to invest.

Any change in the terms of issue amounts to modification of rights of debenture-holders. There is no provision under the Companies Act or SEBI regulations dealing with modification of rights of debenture-holders. Therefore, such modification can be done subject to and in accordance with the terms of issue.

Typically, in case of private placement, the consent of debenture-holders, either directly or through the debenture trustees, is required to be obtained. On the part of the Company, the power to modify the terms usually reside with the Board of Directors or are delegated by the Board to a Committee or a person or persons.

In case of publicly offered debentures, in addition to obtaining the above mentioned consent, compliance with provisions of SEBI LODR Regulations is also required to be ensured.

If these conditions are fulfilled, a bond issuer may be able to get the consent of the investors without the investors having to provide deep haircuts on account of a deemed default.

Due to the obvious outcome of reduction in value of the assets, the mutual funds, as investors of debentures or PTCs, had been rejecting the proposals of issuers/originators/servicers as the case maybe with respect grant of moratorium to the borrowers. Mostly the Mutual Funds which are major investors in PTCs have been denying the grant of moratorium benefit to the borrowers owing to the reduction in value of AUM that would follow. With introduction of this Circular, the problem of taking deep haircuts on the value on account of deemed default stand resolved.

Mutual Funds are now expected to give a green signal on grant of moratorium by lenders. This would help to finally meet the objective of providing relief to the country at the time of the current crisis.

[1] https://www.sebi.gov.in/legal/circulars/apr-2020/review-of-provisions-of-the-circular-dated-september-24-2019-issued-under-sebi-mutual-funds-regulations-1996-due-to-the-covid-19-pandemic-and-moratorium-permitted-by-rbi_46549.html

[2] Our write-up dealing with Force Majeure clauses in agreements may be referred here: https://vinodkothari.com/2020/03/covid-19-and-the-shut-down-the-impact-of-force-majeure/

[3] https://www.sebi.gov.in/legal/circulars/sep-2019/valuation-of-money-market-and-debt-securities_44383.html

[4] https://docs.utimf.com/v1/AUTH_5b9dd00b-8132-4a21-a800-711111810cee/UTIContainer/Standard%20Hair%20Cut%20matrix__AMFI20190606-110846.pdf

[5] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11835&Mode=0

[6] Our detailed FAQs relating to the moratorium may be viewed here: https://vinodkothari.com/2020/03/moratorium-on-loans-due-to-covid-19-disruption/

[7] https://vinodkothari.com/2020/01/shadow-banking-in-india/

[8] Issue discussed at length in a virtual conference organised by Indian Securitisation Foundation: Agenda and minutes may be referred on the following links:

https://vinodkothari.com/2020/04/minutes-of-the-isf-virtual-conference/

-SEBI’s Order in Yes Bank promoters indicates long arm of the provision

Munmi Phukon | Partner | Vinod Kothari & Company

While structuring of instruments like debentures, parties resort to various covenants in order to protect the interests of the investors and also to reflect the intent and purpose of the parties more specifically. One fairly commonplace practice with promoters of Indian listed companies to raise funds on the strength of their shareholding in their companies. It is often observed that, in structuring such transactions, companies find innovative ways of creating pseudo security interests on shares. Therefore, a careful analysis of the documentation entered into by the parties is required to conclude whether the covenants amount to creation of an encumbrance or not.

SEBI has recently dealt with such a case[1], in which SEBI throws some light on what could constitute an encumbrance for the purpose of SEBI (SAST) Regulations, 2011 (Regulations). SEBI considered the covenants mentioned in the debenture trust deed (DTD) executed by the promoter entities of the listed entity at the time of issuance of NCDs and held the promoters liable for non-disclosure of the encumbrance created on the shares held in the listed entity.

SAST Regulations are considered to be a social welfare legislation. The aim and intent of the Regulations is to protect the interest of the investors and ensuring market integrity. That is why, the Regulations recognise the importance of event based and periodic disclosures, specifically by the promoters of the entity, through Regulation 29 to 31 thereof. It has always been seen as a measure for ensuring better corporate governance which in turn enables the regulators and stock exchanges to monitor the transactions of the promoters.

Transactions involving promoters’ shares are considered crucial in order to ensure transparency as regards the ownership/ control of the target company as well as price discovery of the shares in an informed manner. The genesis of the requirements of such disclosures arose in the beginning of 2009 when SEBI made it mandatory by amending the provisions of the erstwhile Regulations.

Later, similar requirements were provided in the revamped SAST Regulations vide Regulation 31 which requires the promoters to disclose about the shares of the target company encumbered by them on a yearly basis to the stock exchange(s) where the shares of the target company are listed and also to the target company. The promoters have also been mandated, by virtue of an amendment made in the said Regulation, to give declaration to the audit committee of the target company and the stock exchange(s) on a yearly basis about not having any encumbrance.

Further, SEBI vide its Circular dated 7th August, 2019[2] read with its Press Release-PR No.16/2019[3] requires the promoters to disclose to the stock exchange(s) and the target company, the detailed reasons for encumbrance if the combined encumbrance by the promoter along with PACs with him equals or exceeds, a) 50% of their shareholding in the target company; or b) 20% of the total share capital of the target company and also any positive changes therein thereafter within two working days from the creation of such encumbrance.

Furthermore, Regulation 29 requiring disclosure of acquisition/ disposal of shares of the target company by an acquirer on meeting certain threshold, interestingly, also provides that shares taken by way of encumbrance shall be treated as an acquisition, and shares given upon release of encumbrance shall be treated as a disposal and shall also require disclosure. In this context, it is pertinent to note if the pledgee/creditor gets voting rights also or has the right to cause the shareholder to vote as per the instructions of the creditor, the transaction would well amount to acquisition of control and hence, triggering the Regulation 3 as well.

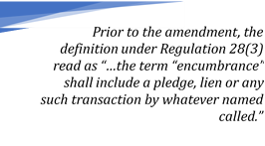

The term ‘encumbrance’ is defined under Regulation 28(3) of the SAST Re gulations. Further, there has been an amendment to the existing definition w.e.f 29th July, 2019 vide SEBI (Substantial Acquisition of Shares and Takeovers) (Second Amendment) Regulations, 2019[4]. Evidently, the text of the existing definition signifies that it is an inclusive explanation and not an exhaustive one keeping the same open to different interpretations.

gulations. Further, there has been an amendment to the existing definition w.e.f 29th July, 2019 vide SEBI (Substantial Acquisition of Shares and Takeovers) (Second Amendment) Regulations, 2019[4]. Evidently, the text of the existing definition signifies that it is an inclusive explanation and not an exhaustive one keeping the same open to different interpretations.

SEBI had tried to clarify the broad definition through its FAQs that, non- disposal undertaking (NDU) will be covered under the purview of ‘encumbrance’. The FAQs also clarified that NDUs may, inter alia, include the following:

“- not encumbering shares to another party without the prior approval of the party with whom the shares have been encumbered;

As mentioned above, the existing text of the definition has been expanded. As claimed by SEBI itself, the amendments have been made in the context of recent concerns w.r.t. promoter/ companies raising funds from Mutual Funds/ NBFCs through structured obligations, pledge of shares, non- disposal undertakings, corporate/ promoter guarantees and various other complex structures, which reads as below:

“(3) For the purposes of this Chapter, the term “encumbrance” shall include,

The Order of SEBI seems to be an attempt of making an interpretation of certain clauses of the debenture trust deeds (DTDs) entered into by the promoter entities in the context of the then definition of ‘encumbrance’ provided u/r 28(3). SEBI found the following clauses in the DTDs and construed the same as creation of encumbrance on the shares of the listed company:

SEBI contended that the covenants related to maintenance of asset cover/ borrowing cap at all times restrict the abilities of the borrowers/ promoters to dispose of the shares of the listed entity held by them. Therefore, the same should be considered as encumbrance for the purpose of Regulation 28(3). Further, the requirement of obtaining prior approval/ consent of the debenture holders before disposing of the shares tantamount to be a non- disposal undertaking as clarified vide the FAQs which include not encumbering shares to another party without prior approval of the party with whom the shares have been encumbered.

In two passages in Salmon on Jurisprudence, 12th Edition, at Page 241 under the sub-heading “Rights in re propria and rights in re aliena” the learned author has stated thus:

“Rights may be divided into two kinds, distinguished by the civilians as Jura in re propria[5] and jura in re aliena[6]. The latter may also be conveniently termed encumbrances, if we use that term in its widest permissible sense. A right in re aliena or encumbrance is one which limits or derogates from some more general right belonging to some other person in respect of the same subject -matter. All other are jura in re propria.”

At Page 242 the learned author has observed as follows:

“it is essential to an encumbrance that it should in the technical language of our law, run with, the right encumbered by it. In other words, the document and the servant rights are necessarily concurrent. By time it is meant that an encumbrance must follow the encumbered right into the hands of new owners, so that a change of ownership will not free the right from the burden imposed upon it. If this is not so — if the right is transferable free from the burden — there is no true encumbrance.”

Thus, the true test of an encumbrance is the concurrence of the right with property – that the right attaches to property and travels along with it. Salmon has discussed encumbrances elaborately and mentions 4 types of encumbrances: leases, servitudes, security interests, and trusts. A lease confers a right to use the property. Servitude is a right to the limited use of the property such as the right of way or easements. Security interests (including mortgages) are encumbrances vested in a creditor. A trust is the obligation attached to property to hold it for the benefit of another.

Madras High Court also in the matter of M. Ratanchand Chordia And Ors. vs Kasim Khaleeli[7] held as below:

“The word “Encumbrances” in regard to a person or an estate denotes a burden which ordinarily consists of debts, obligations and responsibilities. In the sphere of law it connotes a liability attached to the property arising out of a claim or lien subsisting in favour of a person who is not the owner of the property. Thus a mortgage, a charge and vendor’s lien are all instances of encumbrances. The essence of an encumbrance is that it must bear upon the property directly and in-directly and not remotely or circuitously. It is a right in re aliena circumscribing and subtracting from the general proprietary right of another person. An encumbered right, that is a right subject to a limitation, is called servient while the encumbrance itself is designated as dominant.”

The following important features of encumbrances arise from the discussion above:

Negative Lien is used in banking parlance for a borrower to undertake not to create any charge on his property without the consent of the lender.

A negative pledge covenant does not give the negative pledgee a security interest or, in general, any other right in the debtor’s property.

It was held in Knott[8] that Negative Pledgee’s remedies are purely contractual and that the covenant confers no right in the property.

The generally accepted view as mentioned before is that the negative pledge does not create a proprietary or security interest and is therefore not registrable. [Tracy Hobbs, The Negative Pledge: A Brief Guide, 8(7) J.I.B.L.269 (1993)]

A “springing lien” refers to lien granted in the future by a debtor (borrower or lessee) in favor of its creditors whereby the right conferred on the lender springs into a full-fledged lien or pledge either on the happening of certain events, or the discretion of the person holding the pledge.

Whether a so-called springing lien will amount to encumbrance or security interest will depend on intent of parties. If the debtor is free to deal with the subject matter before the trigger events that transform a springing lien into full-fledged lien have taken place, it cannot be said that the lien is an obligation attached to property. Therefore, it will not amount to encumbrance. However, if the lien comes attached with restrictions on sale, it will amount to encumbrance, because the combination of restriction on sale, and automatic attachment of a right on the asset that cannot be sold, in conjunction, will amount to a passable burden on property.

As discussed earlier, an encumbrance carries certain features along with it. A mere restraint on sale or negative covenant is not an encumbrance. Having said so, SEBI’s view in this context may not be in line with the jurisprudence of encumbrance.

However, it is seen that SEBI has been constantly endeavoring to expand the scope of the disclosure requirements, in the wake of various corporate governance failure recently witnessed by the country. SEBI, realizing the recent concerns w.r.t. promoters raising funds through structured obligations, pledge of shares, NDUs and various other complex structures and its impact on the corporate governance structures, had amended the meaning of encumbrance provided in Regulation 28(3). The said amendment has been made to include all such structures including any restriction on the free and marketable title to shares, by whatever name called, whether executed directly or indirectly or any covenant, transaction, condition or arrangement in the nature of encumbrance, by whatever name called, whether executed directly or indirectly.

Considering the amended definition of the term ‘encumbrance’, apparently, SEBI’s intent gets clearer that it wants to include all the possible arrangements/ structures which may carry a potential dilution in the promoter holding. The views held by SEBI are still open for a contest before the Securities Appellate Tribunal.

Read our related articles:

For more updates, please visit our website.

[1] https://www.sebi.gov.in/enforcement/orders/mar-2020/adjudication-order-in-respect-of-two-entities-in-the-matter-of-yes-bank-ltd-_46477.html

[2] https://www.sebi.gov.in/legal/circulars/aug-2019/disclosure-of-reasons-for-encumbrance-by-promoter-of-listed-companies_43837.html

[3] https://www.sebi.gov.in/media/press-releases/jun-2019/sebi-board-meeting_43417.html

[4] https://www.sebi.gov.in/legal/regulations/jul-2019/securities-and-exchange-board-of-india-substantial-acquisition-of-shares-and-takeovers-second-amendment-regulations-2019_43812.html

[5] Right over one’s own property

[6] Right over someone else’s property

[7] https://indiankanoon.org/doc/548843/

[8] Knott v. Shepherdstown Manufacturing Co. 5 S.E. 266 (W. Va. 1888)

-Analysis of SAT ruling in the matter of Canning Industries Cochin Limited

Read our related write ups below –

Revised, stringent private placement framework becomes effective: a step-by-step guide to compliance

Revamping private placement mechanism

Comparison and Mapping of Rule 14 of PAS Rules dealing with Private Placement

Video lectures –

Further Issue of Shares | Overview of Basic Concepts

Lecture 2 | Private placement of securities | Power of 30 | Vinod Kothari & Company

-Financial Services Division (finserv@vinodkothari.com)

The Reserve Bank of India (RBI) introduced an amendment[1] to Master Direction – Know Your Customer (KYC) Direction, 2016 (‘KYC Directions’)[2] requiring Regulated Entities (REs) to carry out money laundering (ML) and terrorist financing (TF) risk assessment exercises periodically. This requirement shall be applicable with immediate effect and the first assessment has to be carried out by June 30, 2020.

Carrying out ML and TF risk assessment is a very subjective matter and there is no thumb rule to be followed for the same. There is no uniformity on procedures of risk assessment, however, they may be guided by a set of broad principles. The following write-up intends to explore guidance principles enumerated by international bodies and suggest principles to be followed by financial institutions in India, specifically NBFCs, for carrying out risk assessment exercise.

The concept of ML and TF risk assessment arises from the recommendations of Financial Action Task Force (FATF). FATF has also provided detailed guidance on TF Risk Assessment[3]. Due to the inter-linkage between ML and TF, the guidelines also serve the purpose of guiding ML risk assessment. TF risk is defined as-

“A TF risk can be seen as a function of three factors: threat, vulnerability and consequence. It involves the risk that funds or other assets intended for a terrorist or terrorist organisation are being raised, moved, stored or used in or through a jurisdiction, in the form of legitimate or illegitimate funds or other assets.”

Based on FATF recommendations, many jurisdictions have prepared and published risk assessment procedures. India is yet to come up with the same.

For example, the National risk assessment of money laundering and terrorist financing[4] is the guidance published by the UK government. It provides sector specific guidance for risk assessment. The sector specific guidance is further granulated keeping in view the specific threats to certain parts of the sector.

The guidance provided by the Republic of Serbia[5] is a generalised one providing broad guidance to all sectors for risk assessment.

In Germany, financial institutions are classified on the basis of potential risk of ML/TF identified by them (considering the factors such as location, scope of business, product structure, customers’ profile and distribution structure) and the intensity of supervision by regulator is based on such risk categorisation.

The risk assessment of a financial sector entity such as an NBFC, need not be complex, but should be commensurate with the nature and size of its business. For smaller or less complex NBFCs where the customers fall into similar categories and/or where the range of products and services are very limited, a simple risk assessment might suffice. Conversely, where the loan products and services are more complex, where there are multiple subsidiaries or branches offering a wide variety of products, and/or their customer base is more diverse, a more sophisticated risk assessment process will be required.

Based on the guiding principles provided by the FATF and specific guidance issued by FATF for banking and financial sector[6], the process of risk assessment by NBFCs may be divided into following stages:

The risk assessment shall begin with collecting of information on a wide range of variables including information on the general criminal environment, TF and terrorism threats, TF vulnerabilities of specific sectors and products, and the jurisdiction’s general AML capacity

The information may be collected externally or internally. In India, Directorate of Enforcement is the body which deals with ML and TF matters and has collection of information and list of terrorists. Further, the information may also be obtained from Central Bureau of Investigation.

Based on the information collected, jurisdiction and sector specific threats should be identified. Threat identification should be based on the risks identified on the national level, however, shall not be limited to the same. It should also be commensurate to the size and nature of business of the entity.

For individual NBFCs, it should take into account the level of inherent risk including the nature and complexity of their loan products and services, their size, business model, corporate governance arrangements, financial and accounting information, delivery channels, customer profiles, geographic location and countries of operation. The NBFC should also look at the controls in place, including the quality of the risk management policy, the functioning of the internal oversight functions etc.

This stage involves determination of the how the identified threats will impact the entity. The information obtained should be analysed in order to assess the probability of risks occurring. Based on the assessment, ML/TF risks should be classified as low, medium and high impact risks.

While assessing the risks, following factors should be considered:

The NBFCs should complement this information with information obtained from relevant internal and external sources, such as operational/business heads and lists issued by inter-governmental international organisations, national governments and regulators.

The risk assessment should be approved by senior management and form the basis for the development of policies and procedures to mitigate ML/TF risk, reflecting the risk appetite of the NBFC and stating the risk level deemed acceptable. It should be reviewed and updated on a regular basis. Policies, procedures, measures and controls to mitigate the ML/TF risks should be consistent with the risk assessment.

Once potential TF threats and vulnerabilities are identified, the next step is to consider how these interact to form risks. This could include a consideration of how identified domestic or foreign TF threats may take advantage of identified vulnerabilities. The analysis should also include assessment of likely consequences.

Post the analysis of threats and vulnerabilities, the NBFC must develop and implement policies and procedures to mitigate the ML/TF risks they have identified through their individual risk assessment. Customer due diligence (CDD) processes should be designed to understand who their customers are by requiring them to gather information on what they do and why they require financial services. The initial stages of the CDD process should be designed to help NBFCs to assess the ML/TF risk associated with a proposed business relationship, determine the level of CDD to be applied and deter persons from establishing a business relationship to conduct illicit activity.

While entering into a relationship with the customer, carrying out Customer Due Diligence (CDD) is the initial step. It is during the CDD process that the identity of a customer is verified and risk based assessment of the customer is done. While assessing credit risks, financial entities should also assess ML/TF risks. The CDD procedures and policies should suitably include checkpoints with respect to ML and TF.

The risk classification of the customer, as discussed above, should also be done based on the CDD carried out. The CDD procedure, apart from verifying the identity of the customer, should also go a few steps further to understand the nature of business or activity of the customer. Measures should be taken to prevent the misuse of legal persons for money laundering or terrorist financing.

In case of medium or high risk customers, or unusual transactions, the entities should also carry out transaction due diligence to identify source and application of funds, beneficiary of the transaction, purpose etc.

NBFCs should document and state clearly the criteria and parameters used for customer segmentation and for the allocation of a risk level for each of the clusters of customers. Criteria applied to decide the frequency and intensity of the monitoring of different customer segments should also be transparent. Further, the NBFC must maintain records on transactions and information obtained through the CDD measures. The CDD information and the transaction records should be made available to competent authorities upon appropriate authority.

Some examples of enhanced and simplified due diligence measures are as follows:

Enhanced Due Diligence (EDD)

- obtaining additional identifying information from a wider variety or more robust sources and using the information to inform the individual customer risk assessment

- carrying out additional searches (e.g., verifiable adverse media searches) to inform the individual customer risk assessment

- commissioning an intelligence report on the customer or beneficial owner to understand better the risk that the customer or beneficial owner may be involved in criminal activity

- verifying the source of funds or wealth involved in the business relationship to be satisfied that they do not constitute the proceeds from crime

- seeking additional information from the customer about the purpose and intended nature of the business relationship

Simplified Due Diligence (SDD)

- obtaining less information (e.g., not requiring information on the address or the occupation of the potential client), and/or seeking less robust verification, of the customer’s identity and the purpose and intended nature of the business relationship

- postponing the verification of the customer’s identity

Ongoing monitoring means the scrutiny of transactions to determine whether the transactions are consistent with the NBFC’s knowledge of the customer and the nature and purpose of the loan product and the business relationship.

Monitoring also involves identifying changes to the customer profile (for example, their behaviour, use of products and the amount of money involved), and keeping it up to date, which may require the application of new, or additional, CDD measures. Monitoring transactions is an essential component in identifying transactions that are potentially suspicious. Monitoring should be carried out on a continuous basis or triggered by specific transactions. It could also be used to compare a customer’s activity with that of a peer group. Further, the extent and depth of monitoring must be adjusted in line with the NBFC’s risk assessment and individual customer risk profiles

The NBFCs should have the ability to flag unusual movement of funds or transactions for further analysis. Further, it should have appropriate case management systems so that such funds or transactions are scrutinised in a timely manner and a determination made as to whether the funds or transaction are suspicious. Funds or transactions that are suspicious should be reported promptly to the FIU and in the manner specified by the authorities. There must be adequate processes to escalate suspicions and, ultimately, report to the FI.

Adequate internal controls are a prerequisite for the effective implementation of policies and processes to mitigate ML/TF risk. Internal controls include appropriate governance arrangements where responsibility for AML/CFT is clearly allocated and there are controls to test the overall effectiveness of the NBFC’s policies and processes to identify, assess and monitor risk. It is important that responsibility for the consistency and effectiveness of AML/CFT controls be clearly allocated to an individual of sufficient seniority within the NBFC to signal the importance of ML/TF risk management and compliance, and that ML/TF issues are brought to senior management’s attention.

NBFCs should check that personnel they employ have integrity and are adequately skilled and possess the knowledge and expertise necessary to carry out their function, in particular where staff are responsible for implementing AML/CFT controls. The senior management who is responsible for implementation of a risk-based approach should understand the degree of discretion an NBFC has in assessing and mitigating its ML/TF risks. In particular, it must be ensured that the employees and staff have been trained to assess the quality of a NBFC’s ML/TF risk assessments and to consider the adequacy, proportionality and effectiveness of the NBFC’s AML policies, procedures and internal controls in light of this risk assessment. Adequate training would allow them to form sound judgments about the adequacy and proportionality of the AML controls.

Once assessed, the impact of the risk shall be recorded and measures to mitigate the same should be provided for. The information that forms basis of the risk assessment process should be timely updated and the entire risk assessment procedure should be carried out in case of major change in the information.

The compliance officer of the NBFC should have the necessary independence, authority, seniority, resources and expertise to carry out these functions effectively, including the ability to access all relevant internal information. Additionally, there should be an independent audit function carried out to test the AML/CFT programme with a view to establishing the effectiveness of the overall AML/CFT policies and processes and the quality of NBFC’s risk management across its operations, departments, branches and subsidiaries, both domestically and, where relevant, abroad.

[1] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11873&Mode=0

[2] https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=11566

[3] https://www.fatf-gafi.org/media/fatf/documents/reports/Terrorist-Financing-Risk-Assessment-Guidance.pdf

[4] https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/655198/National_risk_assessment_of_money_laundering_and_terrorist_financing_2017_pdf_web.pdf

[5] https://www.nbs.rs/internet/english/55/55_7/55_7_4/procena_rizika_spn_e.pdf

[6] http://www.fatf-gafi.org/media/fatf/documents/reports/Risk-Based-Approach-Banking-Sector.pdf

Our other write-ups on NBFCs may be viewed here: https://vinodkothari.com/nbfcs/

Write-rps relating to KYC and Anti-money laundering may also be referred: