SEBI proposals to ease overheated SME IPO market

SEBI proposes amendments in ICDR and LODR Regulations owing to recent concerns around SME listing

– Sakshi Patil, Executive and Sourish Kundu, Executive| corplaw@vinodkothari.com

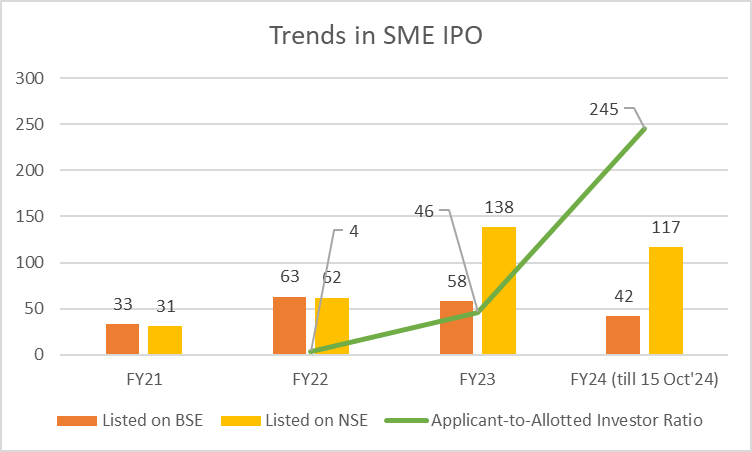

SME IPOs are constantly increasing at an evergrowing rate, with 31 companies listed on SME in FY 21-22 to a total of 138 companies listed in FY 23-24, and 117 companies already listed on SME as of the current FY (till 15th October, 2024) on NSE alone. Not only the number of SME IPOs, the investor participation in such IPOs has also increased substantially, with the applicant to allotted investor ratio from 4X in FY 22 to 46X in FY23 and 245X in FY24. A data on the SME listings during the current and previous FY suggests that, while majority of listed SMEs have booked listing gains, approx 20-30% of such entities have subsequently witnessed a price drop (39 out of 224 companies listed on NSE, 26 out of 91 companies listed on BSE1).

The recent surge in SME IPOs over the last few years, including substantial investor participation in such IPOs, coupled with the recent regulatory concerns w.r.t. diversion of issue proceeds, funding to shell companies, misinflation of revenues etc. has required a re-look into the existing regulatory universe under which SMEs are listed and operate post listing. In August 2024, an advisory was also issued by SEBI regarding investment in the securities of entities listed on SMEs. NSE rolled out stricter eligibility criteria effective September 1, 2024. Greater emphasis on positive cashflow pre listing (w.e.f. Sept 1), capping of 90% over issue price during special pre-open session for SME IPO (w.e.f. July 4) signal the emphasis for investor protection. Following the same, a Consultation Paper has been issued by SEBI, proposing amendments to the provisions of ICDR and LODR Regulations, with a view to strengthen the pre and post-listing requirements for SMEs. Key proposals include restricting the access of SME Exchange to informed investors, and ensuring such IPOs serve the original purpose of making finance available to SMEs for their business growth, and not for funding the promoters’ requirements.

A brief of the 27 proposals, as against the existing requirements and our comments are presented below:

| Particulars | Existing requirement | Proposal under CP | Rationale and Our Comments |

|---|---|---|---|

| Stricter eligibility conditions for SME IPO | |||

| Ineligibility conditions for IPO (Proposal 8) | Currently based on PromotersDirectors Selling shareholders in some cases. | To be extended to promoter group as well. | SME companies are closely held by promoter and promoter groups. Hence, any action against the promoter group may also have a significant bearing on the issuer. |

| Additional eligibility requirements for SME IPO(Proposal 9A & 9B) | Firm/ LLP converted into company can apply for IPO without any cooling period – track record requirements are considered on a combined basis. | Co. which has been converted from LLP or partnership firm, shall be in existence for at least 2 yrs, with restated financial statements post conversion drawn in accordance with Schedule III of CA, 2013.Cooling off of 2 years in case of change of promoter, or introduction of new promoter acquiring 50% or more shareholding prior to filing of DRHP. | Helps in bringing a clearer picture of financial position post conversion. Cooling period in case of change in promoter is to bring steadiness in IPO.Track record should be based on the effective management of new promoter(s) and not past promoter(s). |

| Operating profits (EBIDTA)(Proposal 11) | Positive. | Rs. 3 cr for at least 2 out of 3 immediately preceding FYs. | To ensure financial viability of the company. Our Comments: NSE additionally mandates positive Free cash flow to Equity (FCFE) for at least 2 out of 3 financial years preceding the application. |

| Conversion of Pre-IPO outstanding convertible securities before IPO(Proposal 20) | Conversion not mandatory | Conversion mandatory | In line with the requirement for Main Board IPO. Provides clarity to investors on the company’s capital structure before they invest. |

| Structure of IPO and allotment | |||

| Minimum issue size(Proposal 10) | Not specified | Rs. 10 cr | To ensure companies with significant growth potential access the market.Loans and alternative funding sources typically cater to smaller amounts.Is aligned with BSE’s and NSE’s requirement for Main Board listing. |

| Offer for sale(Proposal 4A & 4B) | No restriction | Dual limits proposedOFS restricted upto 20% of issue size and for selling shareholders, OFS shall not exceed 20% of pre-issue shareholding on a fully diluted basis. | To prevent use of SME listing for dilution of promoter stake. |

| Face value(Proposal 12) | Not Specified | Rs. 10/- per share for existing issued capital and proposed new shares to be issued. | To enable better comparison amongst various issuers. |

| Minimum application size (Proposal 1) | Rs. 1 lakh | Rs. 2 lakh with existing minimum allocation of 35% (book-build issue)/ 50% (fixed price issue) to RIIs, ORRs. 4 lakh (resulting in deletion of RII category for minimum allocation requirements). | Limit participation of retail investors (bidding for upto Rs. 2 lakhs) to protect interest of smaller retail investors;Attract investors with risk taking appetite; Enhance the overall credibility of the SME segment. |

| Minimum no. of allottees (Proposal 3) | 50 | 200 | To ensure sizeable no. of investors Provide liquidity |

| Allotment methodology for Non – institutional investors (NII) category (Proposal 2) | Proportional allotment for NIIs | Draw of lots for minimum bid lot to NIIs divided into 2 categories: ⅓ rd of allocation for application size upto 10L⅔ rd of allocation for application size exceeding 10L | Align allocation methodology with Main Board IPO; Proportional allotment may encourage over-leveraging, over statement of interest and thus at times encourage mispricing. |

| Objects of issue & utilisation of proceeds | |||

| Raising funds for General corporate purpose (GCP) and unidentified acquisition (Proposal 7A & 7B) | GCP < – 25% of issue sizeGCP + unidentified acquisition < – should not exceed 35% of issue size | GCP restricted to lower of 10% of issue size or Rs. 10 cr;Prohibition on raising funds for unidentified acquisition | To reduce the risk of misuse of issue proceeds |

| Repayment of loan of promoter/ promoter group as an object of issue(Proposal 14) | No express prohibition. | Not allowed | To ensure that funds raised through IPO are used for business growth, not for repayment of promoters’ liabilities |

| Funding for working capital (Proposal 15) | No specific requirement | Mandatory statutory auditor certificate on a half-yearly basis for use of working capital funds raised exceeding Rs. 5 Crore, with disclosure of the same in financial statements. | Ensures that working capital funds are appropriately used Our Comments: The requirement of statutory auditor’s certificate is proposed to be made mandatory for all SME IPOs where a monitoring agency is not required to be appointed (see below). A specific mandate for working capital monitoring may not serve any additional purpose. |

| Monitoring of issue proceeds (Proposal 5A, 5B & 5C) | Monitoring agency mandatory if issue size >100 cr | Monitoring agency mandatory if: Issue size >20 cr ORObject of issue includes:funding subsidiary, repay loans/ borrowing of the subsidiary investment in JV/ subsidiaryacquisition In other cases, utilization certificate from statutory auditor on half-yearly basisPlace before AC and board Submit to stock exchange | Reduce risk of misuse or diversionBring more transparency for investors and accountability for issuer Our Comments: Presently, Reg 32(5) of LODR requires statutory auditors to certify the statement w.r.t. Utilisation of funds on an annual basis. The proposal will additionally require the same to be done on a half-yearly basis, in cases where a monitoring agency is not required to be appointed. |

| Disclosure of sources in case of requirement of having firm arrangement of finance for a project(Proposal 16) | No such requirement | Sanction letter to be disclosed in draft offer document and offer document where partial funding is by bank/NBFCs. | Additional diligence and disclosure for investors w.r.t. project appraisal by financial institutions. |

| Exit opportunity for dissenting shareholders in case of change in objects(Proposal 23) | No specific provision | Post-listing exit opportunity for dissenting shareholders in case of changes in the objects or terms, in line with Main Board provisions | Protects the interests of dissenting shareholders, ensuring they have an exit option in case of significant changes post-listing. |

| Promoter contribution and lock-in requirements | |||

| Lock-in of promoter holding(Proposal 6A & 6B) | Minimum Promoter Contribution (MPC) – 3 yrs Excess holding – 1 yr | MPC – 5 yrsExcess – Lock in on 50% to be released after 1 yr and;For remaining 50% to be released after 2 yrs. | To ensure that entire holding is not diluted post the lock in periodTo ensure promoter continues to have skin in game till company is on SME Exchange |

| Securities ineligible for MPC(Proposal 24) | No clarification w.r.t. adjustment of price for corporate action | Price per share for determining MPC eligibility should be adjusted for corporate actions (e.g., bonus, stock split) | Clarifies the pricing mechanism and ensures fairness in determining MPC eligibility, preventing manipulation through corporate actions. |

| Other additional disclosures | |||

| Disclosure of senior level management(Proposal 17) | KMP and SMP details are required to be disclosed in offer document | Disclosure of senior-level employees (e.g., head of sales, plant head, etc.), with their experiencesAdditional disclosure on ESIC/EPF detailsSite visit by merchant banker to form part of DD report and included in material inspection documents in offer document. | Better disclosure w.r.t. Employee strength of the company |

| Merchant banker fees(Proposal 18) | No requirement to disclose issue related fees | Merchant banker fees, by any name, to be disclosed in RHP | Increased transparency – presently such costs exceeds 30-40% of issue size, defeating the primary purpose of fundraising |

| Public comments on DRHP (Proposal 19) | No requirement. | At least 21 days’ for public comments; Disclose on website of SEs and lead managers;Public announcement in 3 newspapers – English, Hindi and regional. | Allows the public to provide feedback during draft offer document stage instead of opening of offer |

| Due diligence certificate by merchant banker(Proposal 21) | Required at the time of submission of offer document to SEs. | Mandatory submission to SE at the time of filing draft offer document. | Ensures that the due diligence process is completed and certified before the public sees the draft offer document. |

| Migration to Main Board | |||

| Migration from SME to Main Board(Proposal 13) | Post-issue face value of capital > Rs. 25 crores pursuant to fresh issue. | Where listed SME is not eligible to migrate, fund raising to be still permitted beyond Rs. 25 crores, subject to compliance with corporate governance norms and disclosure requirements under LODR. | Ensures that company can remain listed on SME platform having post issue face value more than 25cr with light touch of regulations applicable to them related to LODR |

| Corporate Governance Requirements | |||

| Related Party Transactions(Proposal 25) | Exempt from Reg 23 pursuant to Reg 15(2)(b). Compliance as per Companies Act applicable: Meaning of RP [as per section 2(76)]Approval of AC (for all RPTs)Approval of Board (for specified transactions if not in ordinary course or arm’s length)Approval of shareholders (for material RPTs requiring board approval as above) | Reg 23 to be made applicable to SME listed entities.De minimis exemption continues for smaller listed entities [Reg 15(2)(a)]Material RPTs based on turnover thresholds (10% of annual consolidated turnover)Absolute limits of Rs. 1000 crores not applicable. | Enhanced requirements to mitigate risk of circular transactions and abusive RPTs |

| Quarterly corporate governance report [Reg 27](Proposal 26) | Not applicable | Quarterly disclosure w.r.t. composition and meetings of the board and its committees to the stock exchange(s) | Harmonize disclosure requirements for SME and Main Board entitiesEnhancing transparency on functioning of board and committee Our comments: The CP mentions about disclosure of board and committees, however, it is not clear as to whether the other disclosures as are applicable to Main Board entities under the corporate governance report, is also proposed to be extended to SMEs |

| Periodic filings to stock exchanges(Proposal 27) | Half yearly filing of:: Shareholding pattern [Reg 31], Statement of deviation(s) or variation(s) [Reg 32],Financial Results [Reg 33] | To be made on a quarterly basis, at par with Main Board listed entities. | Reflects the financial health and fund utilization by companies; Aligned with requirements applicable to the Main Board. |

Our related resources:

- NSE tightens eligibility criteria for SME listing on NSE Emerge

- BSE and NSE SME Exchange Platforms: Big Opportunities for Small Companies and growing India

- The basics of bringing an IPO

- Based on market data as on 15th October, 2024. Taken from SEBI CP

↩︎

Enhanced role of CRAs in technical defaults by issuers

Compliance-o-meter: From abstraction to structured granular assessment

– Vinod Kothari and Payal Agarwal | corplaw@vinodkothari.com

In risk assessment, effectiveness testing, compliance management, or other areas where qualitative assessment is required, one may be making abstract statements like: we have very effective controls; we have strong risk management practices; we have the best of the practices in compliance management, etc. However, very often, these may be pure abstractions. How do we use a structured approach which may allow us to give a more granular, methodical approach to benchmark ourselves?

Unlike quantitative parameters, there are no set methods or approaches to qualitative assessment. However, every qualitative assessment is also backed by identifying the elements that need to be studied, the ingredients or the check points in each of these elements, the weights of the respective elements in the overall assessment framework, assignment of scores based on the weights and observations for each of the checkpoints, eventually coming to an aggregate score. That is, a purely qualitative assessment may be converted into a score sheet.

One may create one’s own methodology; here is a suggested one. Before proceeding with the methodology, one may submit that the same methodology that may be used for effectiveness assessment may also be used for risk assessment. A good score in effectiveness is a positive indicator; a high score in risk assessment is a threat.

The suggested assessment methodology involves:

- Identification of elements: Every assessment can be decomposed into the elements underlie it. Take a very easy example of, say, quality of board minutes prepared in a large company. The quality is purely an abstraction, which can be granularly split into, at the least, the timeliness of minuting, the comprehensiveness, ease of understanding, compliance with the law and standards, etc. Similarly, if one refers to the effectiveness of controls on insider trading, one may decompose the overall control into several elements such as identification of UPSI, sharing of UPSI, management of Designated Persons, codes and policies etc. Note that the more granular the elements are, the better is it for the final result.

- Weights of the elements: The next point to understand is whether each of the elements are equally weighted, or do they have differential relevance or importance in the overall matter being assessed. For example, if the subject matter of assessment is “quality of minuting”, compliance with law and standards may be perceived as having a higher weight than, say, comprehensiveness or ease of understanding. The task of assigning weights may, once again, become qualitative – therefore, it is necessary to have a methodical approach towards the weights as well. The weights may be determined based on, in descending order, whether the element may result in penal consequence or reputational loss, whether it may undermine controls or the correctness or reliability of the subject matter, whether it is good to have but not must to have, etc.

- Ingredients or check points for each element: The check-points for each element need to be an even more granular list of activities, processes, policies, etc that make up the respective element. For instance, in the context of PIT controls, the check points under DP management may include the manner of categorizing DPs, periodicity of updating the list of DPs, maintenance of DP database etc.

- Scores: Once the base work w.r.t. creation of the assessment list is done, actual scores are required to be assigned based on the level of performance of the company on the given check-point. Depending on whether the assessment is a risk assessment, compliance assessment or process review, a scoring parameter may be created, for instance:

| Scoring Parameter | |

| Not compliant/ no practice exists for the same | 0 |

| Meeting minimum compliance/ practice | 1 |

| Good Practices (indicates industry practice) | 2 |

| Gold Practices (indicates leadership practices) | 3 |

- Weighted score: The scores allotted to each check-point has to be multiplied with the weights assigned to each check point, to arrive at the weighted score of the respective checkpoint. For instance, assume there are five checkpoints in an element, the weighted score can be derived as below:

| Check-points | Weights | Scores | Weighted Score |

| A1 | 3 (maximum) | 1 | 3 |

| A2 | 2 | 0 (minimum) | 0 |

| A3 | 3 | 3 (maximum) | 9 |

| A4 | 3 | 2 | 6 |

| A5 | 1 (minimum) | 2 | 2 |

| Total | 12 | 20 |

- Maximum score and actual score: The weighted score obtained against each checkpoint of an assessment element sums up to form the actual score of such element. The same is to be compared against the maximum score for such an element, and expressed as a percentage. For instance, in the aforesaid table, the actual score of the element, let’s say ‘A’, that is made up of ‘A1’ to ‘A5’ sums up to 20. The maximum score that can be obtained for the said element ‘A’ is maximum score for a check-point (3) multiplied by the maximum weight (3), i.e., 9 multiplied by the total number of checkpoints (5), i.e. 45. Based on the aforesaid, the percentage score of the element can be calculated as = (Actual score/ Maximum score)*100.

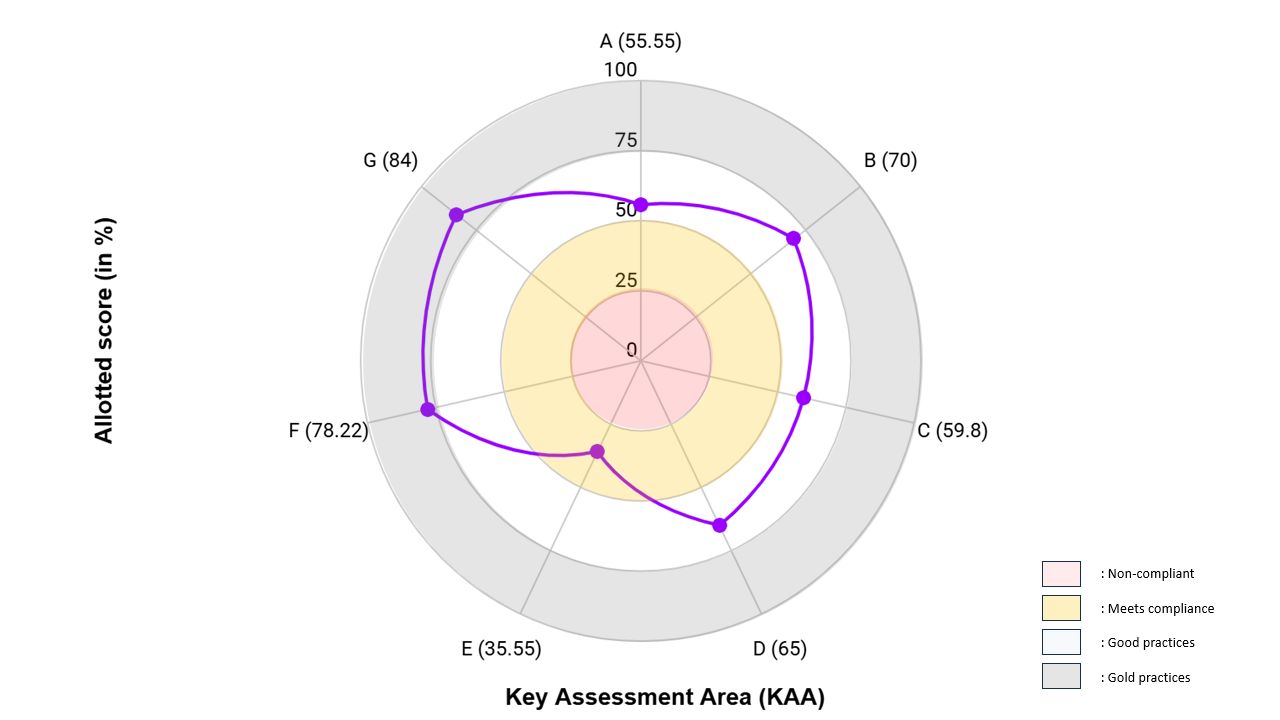

- Radar chart: Once the scores are assigned, and the percentage score for each element has been calculated, the same can be expressed in the form of a radar chart. Below is an example of a compliance radar:

In the picture above, (0-25) is the area of non-compliance, depicting lapses in meeting the minimum legal requirements. (26-50) is the area of meeting the minimum compliance with law, (51-75) indicates that the company is moving towards the general industry practices, and a score beyond 75 shows that the company is adopting leadership practices in the respective compliance area.

A risk assessment chart may be similarly formed, wherein, a higher score indicates a higher level of risk. Also see an article on Compliance Risk Assessment.

Other Related Resources –

RBI & SEBI roll out process for reclassification of FPI’s holding to FDI

– Vinita Nair, Senior Partner & Prapti Kanakia, Manager | corplaw@vinodkothari.com | November 15, 2024

Classification of foreign investments as Foreign Direct Investment (‘FDI’) or foreign portfolio investment is critical for determining the compliance applicable. A person resident outside India may hold foreign investment either as FDI or as foreign portfolio investment in any particular Indian company. Investments by Foreign Portfolio Investors (‘FPIs’) registered with SEBI is mainly governed by the investment restrictions and thresholds provided in SEBI (FPIs) Regulations, 2019 and Part C of SEBI Master Circular for FPIs. Pursuant to Reg. 20 (7) of SEBI regulations, a single FPI (including its investor group[1]) can invest upto 10% of the total paid- up equity capital on a fully diluted basis of the company. In case of breach of this threshold, the FPIs get 5 trading days from the date of settlement of the trades resulting in the breach to correct the position, in terms of the SEBI Regulations as well as Rule 10(1) of FEM (Non-Debt Instruments) Rules, 2019 (‘NDI Rules’), failing which the entire investment is considered as FDI and procedure prescribed by SEBI in Para 17 of Part C of the SEBI Master Circular is required to be followed i.e.:

- Follow extant FEMA rules & RBI prescribed norms in this regard;

- No further foreign portfolio investment in that company;

- FPI to inform respective custodians of the choice who in turn will report this to SEBI, depositories and the issuer;

- Sale of these securities permitted only through the route they were acquired & LEC reporting by custodian.

SEBI unveils new reforms for Debenture Trustees

SEBI proposes to ease HVDLEs from equity linked CG norms

Several proposals on the way to ease compliance

-Pammy Jaiswal, Partner & Sourish Kundu, Executive (corplaw@vinodkothari.com)

Introduction:-

The applicability of CG norms (on a COREX basis) was extended to HVDLEs i.e. entities having an outstanding value of listed non-convertible debt securities of Rs. 500 Crore and above, by SEBI vide its notification dated 7th September, 2021. Following the extension thread for mandatory applicability of Corporate Governance (CG) norms under SEBI Listing Regulations (LODR) on High-Value Debt Listed Entities (HVDLEs) from FY 23-24 to FY 24-25 and again postponing it from 1st April, 2025, SEBI released another Consultation Paper (CP) on 31st October, 2024 containing several proposals to ease the compliance burden of HVDLEs. A similar CP was issued earlier on 8th October, 2024 to review the CG norms primarily focusing on related party transactions (RPTs) [Our analysis on the same can be read here].

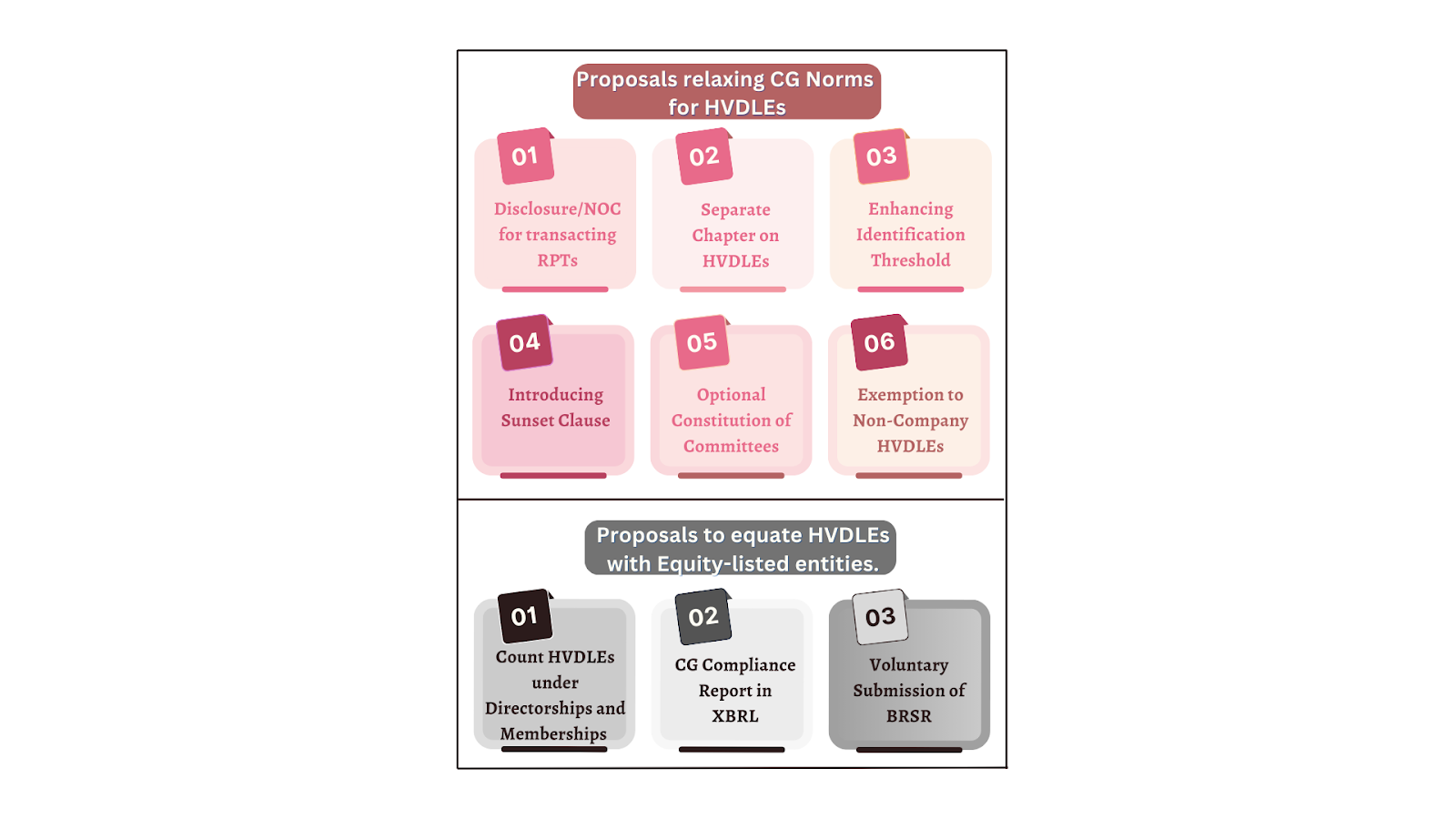

While the intent behind the CG norms being made applicable was to protect debenture holders and assimilate corporate governance amongst such issuer entities, the complexities associated with its implementation hindered the ease of doing business and increased the compliance burden manifold. The current CP delves into the comments received on the previous proposal as well as the issues that HVDLEs have been facing in practically implementing the CG norms (i.e. Regulations 16 to 27 of LODR, 2015). While it discusses the much needed and critical areas (CG chapter, mandatory committees, RPTs, etc.) where HVDLEs can be considered to be relieved and not be kept on the same pedestal as that of the equity listed entities, however, for some provisions (included for max no. of directorship, committee membership, XBRL filings, etc.), HVDLEs have been proposed to be roped in at par with entities with their specified securities listed. While each of the proposals have been discussed in detail below, a snapshot of the same can be seen in the diagram below:

Proposals relaxing CG Norms for HVDLEs

- Providing In-Principle Declaration or obtaining No-Objection Certificate (NOC) from NCD holders in connection with RPTs:

One of the most crucial concerns for HVDLEs was the impossibility of compliance when it came to securing approvals for RPTs. The same was highlighted by SEBI in its earlier CP dated 8th February, 2023 wherein it was mentioned that 104 out of 138 HVDLEs as of 31st March, 2022, comprised of shareholders with more than 90% of them being related parties (RPs).

The current proposal is set against a reference to a banking transaction wherein the lender reserves the right to allow the borrower to enter into any transaction that might be unfavorable to the lender such as entering into RPTs. Thus, HVDLEs being of the nature of a borrower and the debenture holders being the lenders, it is paramount to protect the latter’s interests by enforcing such provisions as may be necessary and safeguarding them through a debenture trustee.

In view of the same, the proposition has the following features:

- Either provide an upfront declaration in the offer document with respect to the amount of RPTs proposed to be entered over the tenure of the NCDs along with the percentage of the same when compared with the issue size or obtain an NOC from the debenture trustee, who in turn needs to obtain it from the debenture holders (the majority not being related to the issuer) for all the material RPTs as and when they are required to be transacted;

- VKCo Comments – Until the fine print of the regulations is rolled out, it is understood that only the broader limits of the estimated RPTs are required to be mentioned unless otherwise finer details are required which can become extremely difficult for these entities.Further, for the alternative requirement, there does not seem to be any incentive to first approach the debenture trustee and thereafter the trustee to approach the NCD holders, which can actually be done directly.

- monitoring of the issue proceeds by a credit rating agency; and

- declare the following in the offer document upfront and be maintained over the tenure of the NCDs:

- debt-equity ratio,

- debt service coverage ratio;

- interest service coverage ratio and;

- such other financial/ non-financial covenants

- VKCO Comments – Both the aforesaid proposals do not serve the exact purpose of maintaining controls over RPT. Also, these are also reflected in the financials to some extent.

- Introduction of a separate chapter for the governance of HVDLEs

LODR in its present form consists of 12 Chapters, each having its purpose and application. As far as the CG norms are concerned, HVDLEs are required to follow the provisions primarily centered around equity listed entities which, inter alia, relate to the composition of the Board of Directors, the constitution of various specialized committees, stipulations regarding RPTs and so on. Having said that, these provisions are not completely relatable to HVDLEs since the majority of these entities are purely debt listed without any other security being listed. Accordingly, it has been proposed to introduce a separate chapter on CG norms for HVDLEs distinct from the existing one for equity listed entities.

VKCO Comments: While this proposal is noteworthy, however, instead of rolling out a new chapter, there could have been certain modifications in the existing regulations by way of a proviso to align with the needs of an HVDLE. Further, one also needs to wait to see the fine print of the provisions once the same is issued.

- Increase in threshold for being identified as an HVDLE

Based on the data provided by NSDL as of 31st March, 2024, the number of pure debt listed entities with an outstanding of more than Rs. 500 crores is 166 (comprising of an aggregate outstanding of Rs. 13.54 lakh crores), of which 112 entities are those having an outstanding of more than Rs. 1,000 crores (comprising of an aggregate outstanding of Rs. 13.16 lakh crores).

Further, referring to SEBI’s circular dated 19th October, 2023 in which the threshold limit of outstanding long-term borrowing was enhanced from Rs.100 crore to Rs.1,000 Crore for the purpose of being identified as a Large Corporate called for introspection at the existing threshold of being identified as an HVDLE. Aligned with its objectives of tightening the regulatory regimes for debt listed entities and at the same time promoting ease of doing business in the corporate bond market, the proposal suggests doubling the limit from the present threshold of Rs. 500 crores to Rs. 1,000 crores.

VKCo Comments: The proposal to enhance the extant threshold is encouraging in terms of governing the maximum value of outstanding debt while at the same time achieving the same without bearing the burden of compliance by an increased number of purely debt listed entities. Subsequently, effective implementation of such a proposal aligns it with the identification criteria of Large Corporates.

- Introduction of “sunset provisions” for non-applicability of CG norms:

The extant Regulation 3(3) of SEBI (LODR), 2015 provides for the applicability of the CG norms even when the value of the outstanding debt securities falls below the specified threshold forever. The same is in contradiction with respect to the period of applicability as compared to its equity counterpart wherein Regulation 15(2)(a) provides that the norms will have to be complied till such time that the equity share capital or net-worth of the listed entity falls and remains below the specified threshold for a period of three consecutive financial years. Accordingly, for the purpose of aligning the non-applicability, a similar sunset provision for HVDLEs too has been proposed. The proposal outlines that the CG norms shall continue to remain in force for HVDLEs till such time the value of outstanding debt listed securities (reviewed on the cutoff day being 31st March of every financial year) reduces and remains below the defined limits for a period of three consecutive financial years and further ensuring compliance within a period of six months from the date of a subsequent increase in the value above the trigger. The proposition also provides for disclosing such compliances in the Corporate Governance compliance report to be submitted on and following the third quarter of the trigger.

VKCO Comments: The proposal is welcome since it clearly sets the HVDLEs free from the barrier of once an HVDLE so always an HVDLE. This proposal sets a clear nexus between the compliance and the size of the debt outstanding, for the protection of which in the very first place, the compliance triggered.

- Certain mandatory committees made optional

Regulations 19, 20 and 21 of LODR mandate the constitution of the Nomination and Remuneration Committee (NRC), Stakeholders Relationship Committee (SRC) and Risk Management Committee (RMC) respectively and provide for their composition, the number of meetings to be held, quorum, duties and responsibilities, among other things. The proposal recognises the difficulties of constituting multiple committees by HVDLEs and therefore, extends the option of either establishing such committees or ensuring delegation and discharge of their functions by the Audit Committee in the case of NRC and RMC and by the Board of Directors in case of SRC.

VKCo Comments: Given the close construct of debt listed entities, it is often observed that the constitution of such committees becomes more of a hardship than in smoothening compliance and discussing specific matters. Accordingly, it looks appropriate to redirect the functions of NRC and RMC to the Audit Committee and that of the SRC to the Board.

- Exemption to entities not being a Company

Several entities are not incorporated in the form of companies and therefore, are regulated by specific acts of the Parliament. The rationale behind this move lies in the fact that the administration of these entities is governed by such specific Acts subject to approval from the concerned Ministries. An exclusion on similar lines was granted to equity listed entities by way of Regulation 15(2)(b) which was later omitted w.e.f. 1s September, 2021 vide notification dated 5th May, 2021.

Further, it is awaited as to how effective and permanent such an exemption would be, but SEBI’s working group has proposed for dispensation of entities like NABARD, SIDBI, NHB, EXIM Bank and such other entities fulfilling the criteria as laid out above and application of CG norms to the extent that it does not violate their respective regulatory framework formulated by the concerned authorities.

VKCo Comments: While SEBI refers to the introduction of similar exclusion for equity listed entities, however, it has also mentioned the subsequent amendment wherein the same was omitted. In any case, the instant proposal is a welcome change since it will help such entities to give preference to their principal statutes and not an ancillary one like LODR.

Proposals to equate certain CG Norms for HVDLEs to that of equity listed entities:

- Count HVDLEs under no. of directorships, and memberships of Committees:

The extant provisions of Regulation 17A of LODR and Section 165 of the Companies Act, 2013 limit the number of directorship positions that a person can hold, with appropriate sub-limits being set out with respect to public companies and equity listed companies. Similarly, Regulation 26 of the SEBI (LODR), 2015 places ceiling limits on the number of memberships and chairmanships that a person can hold in committees across all listed entities, with explicit exclusion for such positions held in HVDLEs.

The instant proposal is for including the directors in HVDLEs as well as committee membership and chairpersonship positions held in HVDLE just as equity listed entities are included.

The same has been proposed in view of the fact that directorship is a significant position in any company and therefore, multiple directorships beyond a reasonable limit are likely to inhibit the ability of a person to allocate appropriate time to play an effective role in delivering its responsibilities including the timely repayment of debt..

Further, the initial proposal for inclusion of HVDLEs in max no. of directorship allows a period of six months or till the next AGM to ensure compliance.

VKCO Comments: The rationale completely aligns with the proposal made and seems to be justified.

- Compulsory filing of CG Compliance Report in XBRL format:

Pursuant to Regulation 27(2), which mandates the submission of a quarterly report on complying with CG norms by listed entities, the format of the report has been supervised by Annexure 3 under Section II-B of the Master Circular for compliance with the provisions of SEBI (LODR), 2015 by listed entities in case of equity listed entities and Annexure VII-A under Chapter VII of the Master Circular for listing obligations and disclosure requirements for Non-convertible Securities, Securitized Debt Instruments and/or Commercial Paper in case of HVDLEs. The issue arises from the practice adopted by HVDLEs in the instant case, where filings made on the website of the stock exchange have been made in PDF format thereby affecting the readability and clause-wise compliance monitoring. Unlike the above-mentioned proposals which aim at bringing about relaxations for HVDLEs, this particular proposal tightens the regime by binding the XBRL format that is consistent with what is being filed by equity listed entities, for the report to be submitted on a quarterly basis.

VKCo Comments: This proposal is with an objective to align and standardize the filing of quarterly CG compliance report for bringing parity as in the case of equity listed entities.

- Voluntary submission of Business Responsibility and Sustainability Report (BRSR):

This proposal originates from SEBI’s endeavour to inculcate good CG practices in HVDLEs, to be at par with equity listed entities. It is supported by Regulation 34(2)(f) which requires the top 1,000 listed entities (based on market capitalization) to include a BRSR in their annual report. It is pertinent to note in this respect that publishing of BRSR by HVDLEs is voluntary and not a mandatory requirement unless such an HVDLE also satisfies the criteria of the above-stated regulation.

VKCo Comments: The inclusion of a voluntary provision in the legislation with respect to a comprehensive report like BRSR is not likely to be submitted given the huge details under the BRSR. However, an opportunity to submit BRSR can be a game changer for an HVDLE from the perspective of being able to raise funds based on its reporting standards in this regard.

Concluding Remarks:

The proposal under the CP provides hope for a breather when it comes to compliance with CG norms and at the same time introduces certain new requirements to maintain uniformity whether it is for the XBRL filing or inclusion of directorship and committee membership as well as chairmanship in an HVDLE for the max no. of such positions. It will also be interesting to see what is rolled out under the new chapter for HVDLEs as well as the fine print of provisions as far as RPT controls are concerned.

Refer to our related resources below:

SDD non-compliance to entail stringent action from exchanges

Lavanya Tandon, Executive | corplaw@vinodkothari.com

Our related resources on the topic-

DPs to furnish periodic & continual disclosures for units of its own mutual fund to AMC

Shaivi Bhamaria, Associate & Sakshi Patil, Executive | corplaw@vinodkothari.com

Loading…

Loading…

Refer to our related resources below: