FAQs on Structured Digital Database

Loading…

Loading…

Our other materials on the topic:

Loading…

Our other materials on the topic:

– Team Corplaw | corplaw@vinodkothari.com

Consultation Paper on Applicability of SEBI PIT Regulations to MF units

Loading…

Proposals include stock broker registration, 6 months lock-in after allotment by an issuer

Growth of investor interest in fixed income investment options is a sign of maturity of a market. Indian investors have traditionally been looking at securities markets for equity-type returns and use mutual funds, bank deposits etc. for fixed returns. However, in recent years, the avenues for fixed income investing in corporate bonds, P2P lending platforms, various types of collective investment schemes such as property shares[1], etc. have flourished. Hence, as investors become active and aware, they no longer limit themselves to mutual funds. Investors are now moving to debt trading platforms, which is the subject matter of SEBI’s Consultation Paper on Online Bond Trading Platforms[2] (‘Paper’). Due to stringent requirements for debt listing, the number of issuances, the number of listed debt issuances to the public is relatively low. Considering the growing investor interest, the lack of volumes of public issuances and limitations of trading of bonds through electronic bond platforms, several platforms started offering listed and unlisted debt securities to investors. This is what we are referring to as “debt trading platforms” here.

Read more →– Sikha Bansal, Partner & Shraddha Shivani, Executive | corplaw@vinodkothari.com

Pledge[1], hypothecation, mortgage – these are all forms of security interest[2], albeit with different features. Although the common objective of any form of security interest is to create a right in rem[3] (rather than in personam[4]) in favour of the lender, the effectiveness of the security interest would depend on the extent of overarching rights created by such security interest in favour of the lender. In another article[5], we have drawn a quick snapshot of the characteristics of each form of security interest. For instance, in hypothecation, the lender does not have any right of possession or any beneficial interest in the property, and the lender’s rights are limited to cause a sale on default; on the other hand, a mortgage (depending upon the type) may have far better rights – including the right to have the title, beneficial interest, etc. In fact, as we discuss elaborately in this article, a mortgage has several motivations for the lender.

However, a conventional notion around mortgages has been that the concept of ‘mortgage’ is only applicable to immovable property. This common view arises in view of explicit provisions under the Transfer of Property Act, 1882 (‘TP Act’). On the other hand, there are no written/codified provisions on mortgage of movable property. It is not that the Courts have not discussed and debated on the same. There have been ample opportunities before the Courts (as this article highlights), wherein Courts have upheld mortgages of movable properties as well. As such, it cannot be said that there has not been any decisive jurisprudence around the subject, however, the recent ruling of Supreme Court in PTC India Financial Services Limited v. Venkateshwar Kari and Another strongly revives the discussion and reinforces the argument that ‘mortgage of movables’ is perfectly possible, although not exactly in terms of the Contract Act; however, under common law principles of equity and natural justice. In fact, in his book Securitisation, Asset Reconstruction and Enforcement of Security Interests, Vinod Kothari, has discussed about ‘chattel mortgages’.

Here, it is important to understand the relevance of this discussion. As we discuss below, a mortgage is seen as the strongest form of security interest – a pledge or a hypothecation create much lesser rights in favour of the secured lender. Hence, from a lender’s perspective, it is always beneficial to have ‘better’ rights in terms of beneficial interest and control. Also, mortgages can be of various kinds (as discussed below), hence, the parties may have the flexibility to structure and opt for a suitable form of security interest.

The article thus, studies the jurisprudence around mortgage of movable property, and the principles which must be followed in order to effect the same. The article also studies how the PTC India ruling has revived the discussion around mortgage of movables. However, before we do so, it would be extremely important to understand the features of a mortgage and how a mortgage can be used as a superior tool of security interest.

Read more →CS Prapti Kanakia, Manager and Samarth Batta, Executive | corplaw@vinodkothari.com

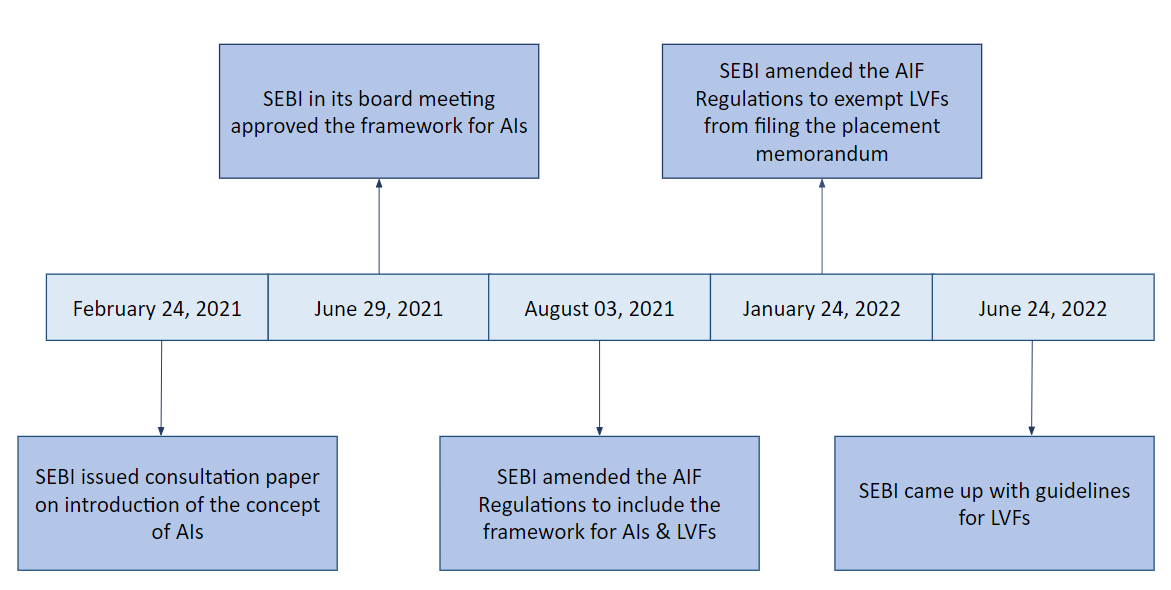

In a recent Circular[1], SEBI has come up with the Guidelines for Large Value Funds for Accredited Investors (LVFs) and requirement for appointment of compliance officer for managers to Alternative Investment Funds[2] (AIFs). SEBI had introduced the concept of LVFs alongwith the concept of Accredited Investors (AIs) in August, 2021. A brief timeline showing the evolution of the framework of AIs in India is as follows:

AI also known as qualified investor/professional investor/ experienced investor are a class of investors who have in-depth market knowledge and high risk bearing capacity to take an informed investment decision. Since, these AIs are well informed investors, therefore, the intermediaries providing services to these investors are given regulation-light regime i.e. less regulatory oversight & relaxed compliance requirement by SEBI.

Read more →– Pammy Jaiswal, Partner and Neha Malu, Executive | corplaw@vinodkothari.com

Additionally invites comments on the applicability in case of units of pooled investment vehicle

Vinita Nair | Senior Partner, M/s Vinod Kothari & Company

– Vinita Nair | Senior Partner, Vinod Kothari & Co. | corplaw@vinodkothari.com

Hon’ble Supreme Court, in the matter of PTC India Financial Services Limited v. Venkateshwar Kari and Another (‘PTC India ruling’), brought out a very important distinction between the meaning of ‘beneficial owner’ under the Depository law, and the right of the pledgee/ pawnee/ security interest holder) to cause the sale of goods pledged by pledgor/ pawnor in terms of the rights arising under the pledge[1]. The PTC India ruling inter-alia holds that “beneficial ownership” in the context of the Depositories Act should not be confused with beneficial ownership in law. Getting registered as a “beneficial owner” in terms of Section 10 of Depositories Act, 1996 read with Regulation 58 (8) of the SEBI (Depositories and the Participants) Regulations, 1996[2] (‘Depository law’) does not amount to any transfer of title to the pawnee – it is merely a procedural precondition to sale by the pawnee. It further stipulates that there is no concept of ‘sale to self’ by the pledgee and that the pledgee is bound by the two options provided under Section 176 of the Indian Contract Act, 1872 (‘ICA, 1872’), viz., right to bring a suit against the pawnor and retain the goods pledged as collateral security, or sell the thing pledged on giving reasonable notice to the pawnor and sue for the balance, if any. This ruling triggers the need to review current practice followed by companies and also validity of orders pronounced by Securities Appellate Tribunal (‘SAT’) and SEBI from time to time w.r.t. pledge.

The Apex Court referred to the decision of Securities Appellate Tribunal (‘SAT’) in the matter of Liquid Holdings Private Limited v. The Securities Exchange Board of India[3] where SAT held that the banks being recorded as beneficial owners of the shares pursuant to invocation of pledge became the members of the target company and subsequent transfer of the said shares by the banks back to the appellants resulted in purchase by the appellants attracting the open offer obligations under SEBI (Substantial Acquisition and Takeovers) Regulations, 1997 [Repealed by SEBI (Substantial Acquisition and Takeovers) Regulations, 2011] (‘Takeover Code’). The Apex Court observed that SEBI should examine the provisions of Depository law and the Takeover Code to avoid discord or ambiguity resulting in instability or confusion especially on applicability of Takeover Code when the pawnee exercises his right to be recorded as a ‘beneficial owner’, while reserving his right to sell the pledge. Additionally, in the author’s view, there is an equal need to examine the applicability of SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’) in the context of pledges[4], for reasons discussed in the latter part of this article.

Read more →By Vinod Kothari, Managing Partner, Sikha Bansal, Partner and Shraddha Shivani, Executive | corplaw@vinodkothari.com

The Supreme Court ruling in PTC India Financial Services Limited v. Venkateshwar Kari and Another is significant in many ways – not that it categorically rewrites the law of pledges which is settled with 150 years of the statute[1] and even longer history of rulings, but it surely refreshes one of the predicaments of a pledge. Importantly, since most of the pledges of securities currently are in the dematerialised format, it brings out a very important distinction between the meaning of ‘beneficial owner’ under the Depository law, and the right of the pledgee (a.k.a. pawnee or security interest holder) to cause the sale in terms of the rights arising under the pledge. Also, very importantly, the SC dwells upon the essential principle of equity of redemption in pledges and renders void any provision in the pledge agreement which allows the pledgee to make a sale of the pledged article without notice to the pledgor, or to forfeit the pledged article and convert the same as pledgee’s own property. There are also observations in the ruling that seem to give an indefinite time to the pledgee for the sale of the pledged property – this is a point that this article discusses at some length.

Read more →– Vrinda Bagaria | corplaw@vinodkothari.com

This article seeks to broadly explain the principle of a pledge and deals primarily with use of ‘pledge’ as a mode of creation of security on shares of a company to secure liabilities of the company.

A ‘pawn’ or a ‘pledge’ is a bailment of personal property as a security for some debt or engagement. Under the Indian Contract Act, 1872[1] (“Contract Act”), pledge has been defined as:

“the bailment of goods as security for the payment of a debt or performance of a promise is called pledge”.

Further, the definition of bailment as provided in Section 148 of the Contract Act reads as:

“the delivery of goods by one person to another for some purpose upon a contract that they shall, when the purpose is accomplished, be returned or otherwise disposed of according to the directions of the person delivering them”.

Thus, a pledge constitutes the delivery of goods by the pawnor to the pawnee as a security under a contractual obligation that the goods shall be returned or disposed off as per pawnor’s direction on the debt being discharged or the fulfilment of the obligation.

Read more →