Overview of RBI (Project Finance) Directions, 2025

Link to the YouTube video – https://www.youtube.com/watch?v=uCbe66Amk9w

Our article on the RBI (Project Finance) Directions, 2025

Link to the YouTube video – https://www.youtube.com/watch?v=uCbe66Amk9w

Our article on the RBI (Project Finance) Directions, 2025

Harshita Malik, Executive | finserv@vinodkothari.com

The evolution of Electronic Trading Platform (‘ETPs’) is rooted in the market’s need for speed, efficiency, and enhanced transparency in dissemination of trade information. Traditional floor based trading methods struggled with sluggish processes, limited data dissemination, and inefficiencies that couldn’t pace with a global financial landscape. In response, industry players and regulators recognised the need for a digital overhaul, a system that could streamline trade execution, provide real-time market data, and foster a more accurate price discovery mechanism. This led to the emergence of specialised platforms, such as those designed for government securities trading, where primary dealers are entrusted with membership and operations. One such platform is ETP.

An ETP is a computarised system that facilitates the buying, selling and management of a wide range of financial instruments (listed down below). These platforms enable real-time market data dissemination, order execution, and efficient trade processing. For instance, in India, platforms such as the NDS-OM (Negotiated Dealing System – Order Matching) are well-known examples that specialize in government securities (g-sec) trading. Other entities include various bank-operated ETPs such as BARX operated by Barclays Investment Bank (international) and proprietary systems developed by financial institutions such as 360TGTX operated by Three Sixty Trading Networks (India) Pvt. Ltd.

On June 16, 2025, the RBI issued Master Direction – Reserve Bank of India (Electronic Trading Platforms) Directions, 2025 (‘New ETP Directions’) in supersession of the Electronic Trading Platforms (Reserve Bank) Directions, 2018 dated October 05, 2018 (‘Erstwhile ETP Directions’). This was based on the feedback received on the Draft Directions issued on April 29, 2024.

In practical terms, operators need not re-submit applications, seek fresh authorisations or revisit past actions as long as compliant under the Erstwhile ETP Directions.

Effective immediately i.e. from June 16, 2025.

Before going ahead to analyse the changes let us understand what ETPs are. ETPs are electronic systems, other than recognised stock exchanges, on which transactions in eligible instruments are contracted. But why would someone prefer trading on ETP rather than other exchanges/ platforms such as stock exchanges? ETPs offer eligible entities multi-instrument trading platforms (dealing with money-market, G-Secs, FX, swaps etc.) with tailored tenures and faster settlement process while stock exchanges cater to listed equities and futures with standardised contracts, retail participation and fixed trading hours.

Any entity as defined in the New ETP Directions incorporated in the form of a company and authorised by the RBI in this regard can operate an ETP. Currently, there are 12 authorised ETP operators under the Erstwhile ETP Directions who shall continue to operate under the New ETP Directions.

| Basis | Single Dealer Platform | Multi-Dealer Platform |

|---|---|---|

| Seller | A single bank or financial institution | Several banks and financial institutions |

| Pricing | Tailored pricing from one provider. | Competitive pricing with options from several liquidity providers. |

| Liquidity | Low | High |

| Liquidity source | Provided by a single bank or institution. | Aggregated liquidity from multiple banks/institutions. |

| Customisation | Tailored interfaces and services designed for specific clients. | More standardized interfaces across multiple dealers; less tailored. |

| Execution quality | Stable and consistent execution within one controlled environment | Best execution can be sought across multiple quotes and providers |

| Suitability | Clients who value a close banking relationship and prefer a dedicated, controlled trading environment | Clients who want to compare and execute trades across a range of prices and liquidity providers |

| Example | NDS-OM, operated by Clearcorp Dealing Systems (India) Ltd., provides a secondary market platform for government securities owned by RBI | 360TGTX, operated by Three Sixty Trading Networks (India) Pvt. Ltd., provides a platform for trading in FX Spot, Forwards, Swaps and Options |

The RBI currently extends various facilities to the PDs to enable them to fulfill their obligations, including memberships of electronic dealing, trading and settlement systems (NDS platforms/INFINET/RTGS/CCIL).

PDs are classified as below:

| Basis | Standalone Primary Dealer | Bank Primary Dealers |

|---|---|---|

| Entity Structure | Operate as independent legal entities, often registered as NBFCs or as dedicated subsidiaries/joint ventures. | Operate as a departmental function within a scheduled commercial bank (or its branch, including foreign banks). |

| Regulatory Framework | RBI guidelines | RBI Guidelines and bank specific norms |

| Business focus | Primarily focused on government securities trading and related activities, often with more flexibility to diversify (e.g., underwriting, trading derivatives). | The primary dealer function is one element of a larger suite of banking services and is more integrated with the bank’s overall operations. |

| Operational Independence | Greater operational autonomy, being solely focused on the government securities market | Functions as an integral part of the bank’s operations, with decisions influenced by the broader business strategy of the bank |

| PDs registered with RBI | SBI DFHI Limited | Bank of Baroda, Bank of America |

Having understood the nomenclature, we may proceed to analyse the changes and what they mean for Regulated Entities. The primary change and intent of the Draft Directions was to curb unregulated entities and platforms, specifically offshore platforms dealing with foreign exchange trading involving inshore/ domestic investors. Please note that foreign exchange instruments have been a part of eligible instruments, however, due to not being defined, the question whether such offshore ETPs would be covered, was always a question. The Draft Directions recommended certain changes, however, the major change was bringing offshore ETPs under the domain of RBI. However, the finalised New ETP Directions do not deal with this aspect.

While the RBI largely accepted the foundational architecture proposed in the draft, it has revised certain provisions to provide clarity in many areas, especially around risk and operational aspects which are now expressed in more precise terms along with addition of new provisions around enforcement and transitional mechanisms.

| Area | Erstwhile ETP Directions | New ETP Directions | Implications |

|---|---|---|---|

| Application process for authorisation | Physical submission | Through PRAVAAH Portal of RBI | Streamlining the process, enhancing accessibility, efficiency, and real-time tracking for applicants as well as regulators |

| Quarterly reporting | No such requirement | Quarterly reporting on functioning of ETPs by Operators (details covered below) | Operators to provide periodic updates on operational performance, ensuring regulatory oversight |

| Annual Reporting | No such requirement | Annual reporting on compliance of the New ETP Directions and terms and conditions prescribed (details covered below) | Operators to yearly confirm their adherence to updated regulatory guidelines and contractual conditions |

| Eligibility Criteria | Did not apply to ETPs operated by SCBs | Apply to all the entities including SCBs operated ETPs (except exemption covered below) | Banks must now play by the same rulebook as other operators, additionally Public Sector Banks shall have to incorporate (or spin off) a Companies Act vehicle, infuse requisite capital and adhere to technological standards. Until now, Public Sector Banks that operate an ETP slipped neatly around the RBI’s “company‐only” eligibility gate. The New ETP Direction takes away that privilege. From the day the change takes effect, every ETP, bank-owned or not must meet the same bar |

| Preservation, access and use of data | Did not have a provision for treatment of data in the event of cancellation of authorisation | Specifies the requirement to share data, along with form and manner, with the RBI or any agency in the event of cancellation of authorisation as may be called upon by the RBI or any other agency. | Enhanced regulatory oversight and post-termination accountability on operators |

| Definition of ‘Entity’ | “….an agency formed as a ‘company’ and incorporated under the Companies Act, 2013 (or earlier acts)” | “….any person, natural or legal.” | Language of the New ETP Directions seems to widen the scope of entity, however reading the impact along with para 6(f)(iii), it only brings the outsourcing entities under the widened scope |

| Grandfathering Rule | Not needed (first issue) | All licenses/actions under Erstwhile ETP Directions shall be treated as valid | No fresh registration required |

| Exemption | ETPs operated by banks for their customer on a bilateral basis as long as no market is being created for the securities | Carve out to SCBs (including branches of Foreign Banks operating in India) and SPDs wherein the bank or the SPD operating the electronic system is the sole quote/price provider and a party to all transactions contracted on the system. | Banks and SPDs can operate proprietary trading platforms without the full weight of the standard compliance requirements set for multi-dealer platforms. This can streamline their internal processes and reduce regulatory and technological burdens.Acting as the sole quote provider makes these institutions both the operator and counterparty. This can improve execution speed and reduce inter-dealer friction.A single market maker model may lead to faster execution but can constrain competitive pricing, potentially resulting in wider spreads if the operator does not face rival pricing pressures from other dealers.While banks and SPDs gain efficiency due to lesser compliances, they must remain vigilant about disclosure and transparency requirements to avoid any adverse effects on market integrity.Banks and SPDs may develop more tailored platforms, exclusive systems to capture niche market segments.Synchronization with global norms that treat single-dealer platforms as an extension of the dealer’s book and not that of an exchange. |

These new requirements shall have to be complied with along with the existing reporting requirements under the Erswhile ETP Directions from the effective date of the New ETP Directions. Accordingly, the first quarterly report shall be required to be submitted on or before 15th July, 2025 and the annual report shall be submitted on or before 30th April, 2026. The manner of reporting by ETP operators as per the New ETP Directions has been listed below:

| Reporting Requirement | Reporting Authority | Frequency | Format | Timeline | |

|---|---|---|---|---|---|

| New | Functioning of the platform, including but not limited to the following points:Events resulting in disruption of activities, during the quarter, if anyInstances of market abuse, during the quarter, if anyDetails about any material change in trading procedure or technology carried out during the quarter | RBI | Quarterly | Annex-2 of the New ETP Directions | On or before 15th day of the month following the quarter |

| Compliance with the New ETP Directions and terms and conditions prescribed at the time of authorisation | RBI | Annually | Not specified | on or before the 30th of April of the succeeding financial year | |

| Data relating to activities on the ETP | RBI | Post cancellation of authorisation | As may be prescribed | As may be prescribed | |

| Existing | Transaction information | Trade repository or trading platform | As may be prescribed | As may be prescribed | As may be prescribed |

| Other report, data and/or information as required by RBI | RBI | As may be prescribed | As may be prescribed | As may be prescribed | |

| Data/information | Any agency as required by Indian Laws | Not specified | Not specified | Not specified | |

| Event resulting in disruption of activities or market abuse | RBI | Event-based | Not specified | Not specified |

By introducing defined protocols for risk management, data governance and reporting, the updated framework seeks to close existing regulatory gaps. Key provisions of the New ETP Directions include, amongst others, a clear exemption for single–dealer platforms and a streamlined application process via the PRAVAAH portal. These measures ensure legal continuity. Ultimately, this transformative framework not only reinforces the integrity of the trading ecosystem but also cultivates an environment conducive to innovation.

-Sikha Bansal (finserv@vinodkothari.com)

The RBI has issued Draft Reserve Bank of India (Investment in AIF) Directions, 2025 (‘Draft Directions’), vide Press Release dated 19th May, 2025, marking a significant revision to the existing regulatory framework governing investments by regulated entities (REs) in Alternative Investment Funds (AIFs). These new directions, once finalised, will replace the existing circulars dated December 19, 2023 (“2023 Circular”), and March 27, 2024 (“2024 Clarification”) (collectively, referred to as “Existing Directions”), which currently govern such investments.

The Existing Directions prohibit REs from making investments in any scheme of AIFs which has downstream investments either directly or indirectly in a debtor company of the RE. In case of any such investment full provision is required to be maintained by the RE. Such prohibition is imposed to address the concerns of evergreening while making investments by an RE. See our analytical article on the same here.

However, the Draft Directions now propose to allow investment by the RE in such AIF upto 5% of the corpus of the AIF scheme. Any investment exceeding this 5% limit will require full capital if AIF has made debt investments in the debtor company. Note that these norms are entirely directed towards debt or debt instruments (whether at the RE level or the AIF level), as all sorts of equity instruments (equity shares, compulsorily convertible preference shares and compulsorily convertible debentures) are excluded – detailed discussion follows.

Below is a snapshot of what is going to change once the Draft Directions are finalised and notified, and certain important implications are discussed further:

| Particulars | 2023 Circular read with 2024 clarification | Draft Directions |

| Investment by REs in scheme of AIF | RE completely prohibited from investing in any scheme of AIF which has downstream investments in debtor company of the RE.Any investment already made had to be liquidated within 30 days of the issuance of the Circular. Similarly, where the RE had already invested, but AIF makes investment in a debtor company of RE, RE shall liquidate investments in AIF within 30 days. | To be allowed subject to individual and collective limits:Max. contribution of single RE to an AIF scheme – 10% of its corpusMax. contribution of multiple REs – 15% of its corpusSee illustrations later in this article. |

| Debtor company | Shall mean any company to which the RE currently has or previously had a loan or investment exposure anytime during the preceding 12 months. | Shall imply any company to which the RE currently has or previously had a loan or investment exposure (excluding equity instruments) anytime during the preceding 12 months. |

| Provisioning requirements | Inability to liquidate investments within 30-day liquidation period would entail 100% provisioning against such investments. | Investment by the RE in such AIF allowed upto 5% of the corpus of the AIF scheme, without looking into the form of downstream investments made by AIF. Hence, no provisioning required. If investment by RE exceeds 5%, it will require full capital, if downstream investments by AIF in debtor company are not permissible investments (see below). See illustrations later in this article |

| Provisioning required proportionately and not on entire investments | Provisioning is required only to the extent of investment by the RE in the AIF scheme which is further invested by the AIF in the debtor company, and not on the entire investment of the RE in the AIF scheme | Norms remain the same – RE shall be required to make 100 per cent provision to the extent of its proportionate investment in the debtor company through the AIF Scheme |

| Permissible forms of investments by AIF scheme in debtor company | Investment in equity shares (by AIF scheme in debtor company) were excluded from the prohibition by 2024 clarification. However hybrid instruments were still included. | All forms permitted, if investment by RE does not exceed 5%. Therefore, even debt investments by AIFs are permissible.Only equity shares, CCPS, and CCDs allowed, if investments by RE exceeds 5%. If AIF makes other forms of investments in debtor company, RE will have to provide for full capital.Note that, irrespective of the form of downstream investments by AIF in the debtor company, RE can take a maximum exposure of 10% in an AIF. |

| Priority distribution model | investment by REs in the subordinated units of any AIF scheme with a ‘priority distribution model’ shall be subject to full deduction from RE’s capital funds. Deduction shall be made from Tier I and II equally. | Norms remain the same. |

| Investment policy | No specific requirement | Investment policy to have suitable provisions to ensure that investments in an AIF Scheme comply, in letter and spirit, with the extant regulatory norms. In particular, such investments shall be subject to the test of evergreening. |

| Exemption by regulator | No specific enabling provision | Exempted category to be decided by RBI in consultation with GoI. |

Below are certain illustrations to explain the implications of the investment thresholds under Draft Directions:

| Scenarios | Implications under Draft Directions |

| Investment of Rs. 10 Crores by an RE in an AIF scheme having corpus of 50 crores | Cannot make since the threshold limit of 10% will be breached. |

| Investment of Rs. 5 Cr by an RE in an AIF scheme having corpus of 50 crores with other REs contributing Rs. 15 Cr | While the investment by the RE individually is within the limit of 10%, the collective investment is more than 15%. Hence, such an investment cannot be made by the concerned RE. Further, since the total investment of 15 cr by other REs will also breach the threshold of 15%, the investments will not be possible. |

| Investment of Rs. 5 Cr by an RE in an AIF scheme having a corpus of 50 Cr. The AIF in turn has a downstream debt investment in a debtor company of the RE. | Cannot be made since the limit of 5% will be breached. |

| Investment of Rs. 1 Cr by an RE in an AIF scheme having a corpus of 50 Cr. The AIF in turn has a downstream debt investment in a debtor company of the RE. | This constitutes only 2% of the corpus of the AIF scheme. Hence, permissible – even when the downstream investment of the AIF is a debt investment. |

| Investment of Rs. 5 Cr by an RE in an AIF scheme having a corpus of 50 Cr. The AIF in turn has a downstream equity investment in a debtor company of the RE. | Can be made as the downstream investment of the AIF is in equity of the debtor company. However, the maximum cap of 10% would apply to the RE. |

We had earlier indicated that the Existing Directions may need to be reviewed and softened. The Draft Directions take a step in the same direction – however, a few concerns may still remain open. For instance, the Draft Directions retain the outreach of these restrictions to all AIFs, and not only affiliated AIFs. In our previous article, we had discussed how the concerns as to evergreening, etc. would arise mostly in cases involving affiliated AIFs, and not those AIFs which are completely unrelated to the RE..Further, no distinction has been made between various categories of AIF – therefore, investments in any AIF (Cat I, II, III) would be governed by these directions.

– Team Finserv | finserv@vinodkothari.com

The RBI on September 30, 2024, flagged several concerns in gold lending practices of financial entities. Further, there were separate guidelines for banks and NBFCs leading to regulatory arbitrage and operational ambiguity. On April 09, 2025, the RBI introduced the Reserve Bank of India (Lending Against Gold Collateral) Directions, 2025 (Draft Directions).

The Draft Directions intend to:

In this write-up, we highlight the major changes for lenders, and particularly for NBFCs (The same are subsequently elaborated in the article).

Read more →Harshita Malik and Anshika Agarwal (finserv@vinodkothari.com)

-Subhojit Shome (subhojit@vinodkothari.com)

The tokenisation of real-world assets (RWA) using cryptographic technology is rapidly emerging as a transformative innovation in the financial ecosystem. Note here that the term RWA refers to all traditional assets including both real assets as well as traditional financial assets that exist in the physical world. By leveraging blockchain technology, tokenisation enables the representation of tangible assets, such as real estate, commodities, and artwork, or intangible assets like intellectual property, as digital tokens on a distributed ledger. This development is reshaping the way assets are managed, traded, and accessed, creating new opportunities and challenges.

RWA tokenisation has garnered attention due to several converging factors. Blockchain technology offers a streamlined alternative to traditional systems by reducing intermediaries, lowering transaction costs, and ensuring faster settlement times. Fractional ownership of high-value assets makes them accessible to a broader range of investors, enhancing market liquidity. Blockchain’s immutable nature provides a transparent record of transactions and ownership, reducing fraud and enhancing trust. Additionally, tokenised assets are borderless, enabling seamless cross-border trading and investment opportunities.

According to market reports, the capital locked in tokenised RWA is expected to touch $50 billion by the end of 2025 surpassing all previous records. In 2024, the ecosystem had achieved a 32% annual growth rate.

In this article, we look at the impetus behind this technology, its status of adoption in India and critical issues that act as roadblocks in its development.

The tokenisation market has witnessed significant advancements in a number of areas. Real estate tokenisation has enabled properties to be tokenised for fractional ownership, reducing entry barriers for smaller investors. Similarly, commodities like gold and other precious metals have been tokenised, providing an efficient means of trading and ownership. High-value artworks and collectibles are being tokenised to allow multiple investors to own shares in masterpieces. Tokenisation has also extended into private equity and debt markets, enabling innovative funding mechanisms and the development of secondary market opportunities. Moreover, the emergence of regulated tokenisation platforms in certain developed economies (e.g. the UK) underscores the growing maturity of this market.

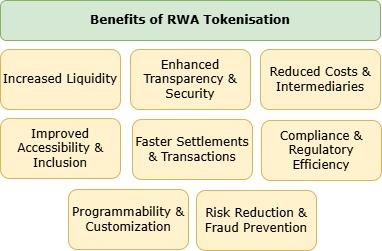

Figure 1: Benefits of Tokenisation of Real-World Assets using Blockchain

Fractional ownership creates liquidity in traditionally illiquid assets. It also democratises investment by enabling wider participation through reduced minimum investment thresholds. Here the emphasis is not on reduction of any regulatory investment threshold but rather, being represented in the digital world, RWA tokenisation allows infinitesimally fractional parts of an asset to be bought and sold. Cost efficiency is achieved by reducing reliance on intermediaries, which lowers transaction and administrative costs. Blockchain’s transparency increases trust and reduces fraud risks. Furthermore, smart contracts enable automation of compliance, dividend distribution, and other processes.

The process of RWA tokenisation broadly involves the following steps –

Figure 2: Process of RWA tokenisation

In the tokenisation process one may note that the custody of the underlying asset is separated from the ownership of the asset. While the ownership is represented by use of tokens, the underlying asset may need to be held with a custodian ‘off-chain’ (i.e. in the physical world).

However, tokenisation is not without challenges. Regulatory uncertainty remains a significant hurdle due to inconsistent global regulatory frameworks. Technology risks, such as cybersecurity concerns and vulnerabilities in smart contracts, could undermine trust. Market volatility is another concern, as tokens may experience higher price fluctuations compared to their underlying assets. Some tokenised assets may face illiquidity risks if the secondary markets lack sufficient depth. Additionally, legal ambiguity regarding ownership rights and the enforceability of tokenised claims persists in many jurisdictions.

Several key regulatory considerations must be addressed. Asset classification is crucial for defining whether tokenised assets are securities, commodities, payment instruments or another category altogether.

In India, regulatory uncertainty remains the key issue in the implementation of RWA tokenisation. Say, for instance, there is tokenisation of real estate in which the management of the property is overseen by the issuer or by a manager appointed by such issuer and fractional ownership units are offered for sale to retail investors. Such a transaction starts to take on the colour of a collective investment scheme and SEBI may intervene and mandate the issuer to register as such with the regulator. In the case of real estate these schemes can also be viewed as having a structure akin to a REIT especially SM REIT.

The SEBI is yet to notify any regulatory prescription specifically for the purposes of regulating crypto-assets and or token offerings to the retail public and it has been reported in the press1 that the securities market regulator has informed the Parliamentary Standing Committee on Finance that regulation of crypto-assets would be difficult given the nature of technology that sustains them. In the matter of, An RTI enquiry, as referenced in the matter of Appeal No. 4532 of 2021 filed by Rohith Methayil Rajagopal, was raised with the SEBI’s CPIO as to the stand of Regulator with regard to “digital trading and possession of Cryptocurrencies by the Indian Citizens” and if SEBI had any “legal document and its date that permits digital trading of Bitcoin / Cryptocurrencies in India”. The response of the CPIO, as affirmed by the appellate authority, was that it did not have the knowledge of either matter. Based on this one can conclude that the Regulator has not, yet, formalised its stance over dealings in crypto assets. Recently, however, the Regulator has expressed an openness to a multi-regulator based oversight framework for crypto-assets.2

There have been interest shown by mutual fund houses to invest in ETFs or indices on blockchain-based projects and crypto-assets and draft scheme information documents were filed with the Regulator. SEBI, however, has expressed its reservations3 on approving such funds/ fund of funds. Highlighting high degree of regulatory uncertainty when it comes to crypto-assets which is not an ideal situation either for business houses looking to raise funds using crypto-assets or for investors who have invested in such assets.

Another major inhibitor is the tax treatment of such tokenised assets. This is because given the construct of such token it will get classified as virtual digital asset under section 2(47A)4 of the Income Tax Act, 1961. The implication of this is that income on sale of such assets will get taxed at a flat rate of 30%. Other than the cost of acquisition, any other expenses incurred with respect to such assets are not allowed to be deducted while computing the income. Further, any loss from the transfer of such assets are also not allowed to be set-off against such income or under income computed under any provision of the act. Accordingly, such losses are also not allowed to be carried forward to any succeeding assessment years.

Recently, however, there has been some headway in asset tokenisation in Gujarat International Finance Tec-City (GIFT City) which may be poised to host India’s inaugural regulated platform for the tokenization of real estate and infrastructure assets. This initiative aims to democratize investment opportunities by enabling fractional ownership through digital tokens, leveraging blockchain technology to enhance liquidity and transparency in the sector. To this extent the IFSCA has constituted an ‘Expert Committee on Asset Tokenization’; the terms of reference of this committee are as follows –

Tokenisation is a transformative technology that has the capability to change the very nature of real world assets in the way they are managed and traded. The flow of capital into this sector is an indication of the potential of this sector in contributing to the economic growth of a country. In the formation of the working group on crypto-assets to reform US digit asset regulations, the US has taken stock of this development in the market and the need to make such technologies mainstream. It is encouraging to see India’s intention to move ahead with such innovation in the GIFT City. It is now time to wait and watch whether tokenisation will find acceptance in the economic mainstream and for this to happen a clear regulatory architecture has to emerge in India.

Team Finserv l finserv@vinodkothari.com

Loading…

Loading…

finserv@vinodkothari.com | corplaw@vinodkothari.com

An examination of the RBI Guidance Note on Operational Risk Management and Resilience

Subhojit Shome & Archisman Bhattacharjee | finserv@vinodkothari.com

Loading…

Related articles –

The who’s who of structured finance is joining the 12th edition of our flagship event, the Securitisation Summit on May 15, 2024, in Mumbai. Be shoulder-to-shoulder with leading originators, investors, lawyers, rating agencies, consultants, regulators, mediators, market makers, and everyone else who matters.

For details of the event and to book your seat, please visit our Summit page – HERE