Archive for year: 2026

Representation for issues related to RBI (Commercial Banks – Credit Risk Management)(Amendment) Directions, 2026

Leading to the world of LBOs: RBI opens up acquisition finance

Vinod Kothari, Payal Agarwal and Simrat Singh | finserv@vinodkothari.com

The RBI recently opened the avenues for banks to provide funding for acquisitions. For domestic banks, enabling changes were made vide Amendment Directions on Capital Market Exposure dated 13.02.2026, covered in our write up here, and for global banks, the enabling amendments were made in ECB Regulations by relaxing the end-use restrictions vide notification here, covered in our write up here.

This write up discusses what is acquisition finance, what are the global structures and risks, and whether India will now be ushered in the new, arguably risky world of leveraged finance.

What is acquisition finance?

Acquisition finance, known by various names such as M&A finance, leveraged finance, LBO finance, etc is globally practiced by banks. Wherever there are inflexibilities or restrictions on banks lending for acquisitions, the gap has given room for private credit lenders, special situation funds and alternative investment funds to chip in – which is what accounts for the sharp rise in private credit funds. See our article on private credit AIFs here.

LBO financing added to approximately US $214 Billion globally for 2024. As per a 2024 S&P report, banks funded only about 23% of LBO financing globally with private debt players covering the other 77%. The reasons for such reduced share for banks include intensive capital charge applicable to banks, lower profitability on such loans and over-leverage risks (see discussion below).

Source: S&P Global

How is acquisition finance structured?

The end-use of acquisition finance is the control or significant holding over the target. Therefore, quite naturally, the collateral for acquisition finance are the shares of the target. Taking the collateral is intuitive, but the issue is, how is the loan repayment structured? The most logical way to structure an LBO is to align the loan repayment with the residual cash flows from the target. Hence, it is returns on equity from the target that pay the loan.

Lenders may quite structure the loan with the possibility of refinancing the acquisition, such that the initial funding term is not as long as the payback period of the target is. For example, a company borrows ₹500 Crores to acquire a business generating ₹100 Crores annually, repays only ₹20 Crores of loan each year for 5 years, leaving ₹400 Crores outstanding at maturity, which it then refinances with a new ₹400 Crores loan instead of fully repaying from operating cash flows. The key risk in such a case would be refinancing risk i.e. if credit markets tighten, the company may be unable to roll over the ₹400 Crores at maturity. There is also interest rate risk, as the new loan may be available only at a higher cost, increasing the debt burden.

Acquisition finance is quite risky, as it is funding the residual return which itself is impacted by all the risks of the target’s business; any downturn in performance directly impairs debt servicing capacity. It is a leverage created on structure, which itself is leveraged. Therefore, lenders may quite often be comfortable with the strength of the acquirer’s own business, etc. But the standalone strength of the cash flows of the target’s business is the ultimate comfort for an LBO investor.

Debt tranching in acquisitions

Usually a LBO is undertaken by multiple lenders so as to cut down on individual exposure and risk further and in such cases each lender may have varying risk and return expectations. In such a multi-lender LBO, instead of issuing one big, uniform loan, the capital stack is layered into tranches with different priority, pricing, maturity and covenants. Therefore, there can be senior and mezzanine debt, with tranches itself within these such as high-yield debt within the mezzanine tranche. The senior tranche typically ranks first in repayment and is secured against the company’s assets and cash flows, carrying lower interest with tighter covenants and amortization requirements.

Below this sits the mezzanine or subordinated debt, which ranks junior in the repayment waterfall, bears higher interest to compensate for greater risk. This is usually provided by non-banks and is secured by second-lien and may also be partially unsecured..

Equity sits at the bottom of the capital structure and represents the residual ownership in the company. It has no fixed repayment or guaranteed return; instead, equity holders receive whatever value remains after senior and mezzanine debt are fully repaid. Because it is last in priority, equity bears the highest risk and absorbs first losses if the company underperforms.

However, equity also captures all upside beyond debt obligations. As leverage increases, the amount of equity invested decreases, which magnifies potential returns if the company performs well and is sold at a higher value.

Sometimes, subordinated tranches may also carry a PIK or pay-in-kind feature, which implies that the periodic interest will not be serviced, but will be added to the outstanding exposure.

This layered structure allows risk to be allocated according to each lender’s appetite, reduces the overall cost of capital by pricing safer debt more cheaply and increases total borrowing capacity without overexposing any single lender.

The following chart is an illustration of a typical LBO capital structure with a bank (senior) debt of 50%, high yield debt is 15%, mezzanine is 15% and common equity is 20%. (source: hold.co):

Risks in acquisition finance

Acquisition finance is risky because it combines ownership transition, financial leverage and forward-looking projections all in one. The risks are interlinked; operational underperformance quickly becomes financial stress. Few of the risks for the lender are as follows:

Over-leverage risk: The acquisition is funded with high debt relative to cash flows. A small decline in earnings can disproportionately hurt repayments. For example, a company acquired at 6x EBITDA (₹600 debt on ₹100 EBITDA). EBITDA drops 20% to ₹80. Leverage jumps from 6.0x to 7.5x overnight.

Acquisition finance combines operating leverage (extent of fixed costs in the operating cashflows, from which the residual cashflows will arise) and financial leverage (such residual cash flows being financed by debt which carries fixed interest burden). That is what makes acquisition finance a bunch of two mutually exacerbating risks. Typically, the presence of operating leverage is balanced by keeping the financial leverage low: however, in this case, the two forms of leverage co-exist.

Projection/business case risk: Acquisition pricing may be based on forecasted synergies, ie , the combined disproportionate increase when the target comes into the group as well as growth, or margin expansion that may not materialize.

Beyond the above, financially, acquisition finance also faces valuation and cyclicality risk if the business was acquired at peak multiples or during an economic upcycle. Operationally, some of the risks in a typical M&A deal may also loom for the lender such as inadequate due diligence, top-talent attrition and integration issues.

Acquisition finance versus leveraged finance:

The two terms quite often overlap, but both refer to distinct aspects of a lending transaction. Acquisition finance specifically refers to purpose; leveraged finance, though mostly used for acquisitions, refers to the prevalence of high leverage, lower rating and cashflow-based funding structure.

Some definitions of “leveraged finance” may be pertinent, for instance, a 2021 thematic note by EBA on leveraged loans refers to a loan as ‘leveraged’, if some of the given conditions are met:

- high indebtedness of the borrowing firm (e.g. debt to earnings before interest, taxes, depreciation and amortisation (EBITDA) ratio of four times (4x) or higher);

- below investment grade credit rating for the loan (or borrower) (i.e. below BBB);

- loan purpose to finance an acquisition (e.g. leveraged buyouts);

- presence of a private equity sponsor (e.g. financing of borrowers owned by financial sponsors);

- high loan spread at issuance.

This is based on a combination of definitions used by various regulators and data providers.

A definition based on combination of various aspects as per the policies prevalent in the financial sector industry was also given in the 2013 guidelines published by the US FRB as follows:

- Proceeds used for buyouts, acquisitions, or capital distributions.

- Transactions where the borrower’s Total Debt divided by EBITDA (earnings before interest, taxes, depreciation, and amortization) or Senior Debt divided by EBITDA exceed 4.0X EBITDA or 3.0X EBITDA, respectively, or other defined levels appropriate to the industry or sector.

- A borrower recognized in the debt markets as a highly leveraged firm, which is characterized by a high debt-to-net-worth ratio.

Transactions when the borrower’s post-financing leverage, as measured by its leverage ratios (for example, debt-to-assets, debt-to-net-worth, debt-to-cash flow, or other similar standards common to particular industries or sectors), significantly exceeds industry norms or historical levels.

The end-use of leveraged finance are variegated: including mergers, acquisitions, re-capitalizations, refinancings, and equity buyouts, as well as for business and product line buildouts and expansions, whereas, acquisition finance has limited end-use.

Waves of regulatory concerns on leveraged finance:

Regulatory concerns on leveraged finance have been coming in waves – they come and recede.

The oft-quoted “warning” was issued by the IMF in 2018 in its Global Financial Stability Report. The concerns lie in the ever-increasing volume of leverage loans coupled with deteriorating underwriting standards and credit quality as well as strong investor demands, resulting in fewer investor protection covenants. The BIS also raised concerns on the rise of the leveraged loans causing an increasing default rate in the US.

Since the Global Financial Crisis in 2008, regulators have, time and again, taken policy decisions to regulate the risks emanating from leveraged lending. In the context of US, reference may be made of a 2013 Interagency Guidance on Leveraged Lending read with the 2014 FAQs thereon setting out the expectations from financial institutions w.r.t. leveraged loans. In fact, guidelines for leveraged financing were issued in the US as early as in April 2001, subsequently replaced by the 2013 version.

Regulatory directives have been issued by the EU, coupled with a 2017 Guidance on Leveraged Transactions by the European Central Bank to address the risks of excessive leverage. The ECB Guidance lays down the minimum expectations from the credit institutions on leveraged transactions. A March 2019 briefing states that the 2017 guidance issued by ECB seems less effective than expected. It also refers to the warnings issued by international institutions as well as the US and EU authorities in relation to the potential risks of leveraged finance.

However, come the end of 2025, at least the US regulators have withdrawn their regulatory statements on leveraged finance, leaving it for banks to use their own prudence. The agencies, in fact, went to term leveraged finance as vital: “Leveraged lending plays a vital role in the U.S. financial system. It provides a wide range of businesses, including those that are highly indebted or highly leveraged or that have low obligor ratings..” It said the 2013 guidelines were overly restrictive and led to reduced activity by US banks.

The 2025 Global Financial Stability Report, however, continues to highlight the vulnerabilities associated with leveraged financing and the degrading credit quality: “Despite the wave of restructurings, liquidity remains strained among the more vulnerable borrowers in the leveraged loan and private credit markets. This has contributed to an increase in borrower downgrades”. “In reality, default rates, especially for leveraged loans, have been climbing, even though some of the defaults are voluntary liability management exercises, including debt exchanges…”

Impact of the RBI move

Are banks bracing up to jump into acquisition finance? Therefore, is the growing segment of the AIF market, private performing credit, going to be put to challenge?

In our estimate, it will be quite sometime before banks will really pose a competition to the fund industry. At the end of the day, banks are highly rule-driven, with multiple layers of approval processes and very tight corporate governance structures. Banks have RBI supervisors breathing down the neck. Acquisition finance needs flexibility, fast turnaround, structuring skills and bespoke terms which may be difficult for banks to match. At the same time, it is also important to note that most of the private credit funds also have a bank behind. Therefore, the move surely adds to the funding muscle that private credit funds will now enjoy – they will be able to “syndicate” acquisition finance by roping in bank lenders to take a share. In essence, it is a cake that will be shared. We also see distinct possibilities of structured funding transactions with banks taking a senior slice, and AIFs taking the role of a deal maker and risk taker.

Will the RBI move set the sails for leverage financing in India? There are several reasons to contend that the RBI’s move is far more conservative than expected by the typical leveraged finance landscape:

- First, the RBI expects the acquirer’s rating to be at least BBB- (where the acquirer is an unlisted company), whereas leveraged finance is mostly below investment grade;

- Second, the RBI has put a limit of D/E at consolidated level of 3: 1, leveraged finance, definitionally as well as by its very structure, works on higher levels of leverage;

- Third, Section 19(2) of the Banking Regulation Act, 1949 imposes a limitation on banks by restricting them from holding shares in any company, whether as owner, pledgee or mortgagee, beyond 30% of the company’s paid-up share capital or 30% of the bank’s own paid-up capital and reserves, whichever is lower. Since leveraged buyouts commonly involve acquisition of controlling stakes with shares offered as primary security, this statutory cap constrains the extent to which banks can take equity as collateral, thereby further tempering the scope for large-ticket LBO financing.

- Lastly, the apparent text of the RBI regulations on acquisition finance suggest that acquisition finance is permitted only to non-financial companies which also excludes a Core Investment Company (CIC) hence barring CICs from availing acquisition finance under the RBI framework.

Factoring DLG into ECL: Relief, But Not A Free Pass

Vinod Kothari & Chirag Agarwal | finserv@vinodkothari.com

RBI had earlier directed NBFCs to compute expected credit loss (ECL) without considering the impact of any default loss guarantees (DLGs) obtained from its lending service provider (LSP). We had published a short note explaining why this position was debatable (See our article on the topic here) and had also made a formal representation to RBI on the issue.

Back to the present, RBI has issued an amendment to the IRACP Directions, 2025 (dated February 13, 2026), permitting lenders to factor in DLG while determining provisions under the ECL framework across all stages.

Further, RBI has also specified that upon every event of invocation of DLG, the DLG cover reduces to the extent of invocation. Accordingly, REs shall recompute their ECL provisioning requirements across stages, after duly adjusting for the reduced DLG cover.

With these clarifications now in place, the next question that arises is: How should Regulated Entities (REs) appropriately factor DLG into their ECL computations? The article below discusses the above question at length.

How to factor in DLG in ECL computation?

Let us understand this in simple terms. Suppose a lender estimates that the expected loss on a loan pool is 3.8%. If the lender has received a guarantee of 5%, backed by fixed deposits that are lien-marked in its favour. The guarantee is sufficient to cover the expected loss. In such a case, effectively, the lender does not expect to bear any loss. On the other hand, if the expected loss is 6.8% and the guarantee covers only 5%, then the lender’s net expected loss would be the balance 1.8%.

However, this adjustment assumes that the guarantee will actually be honoured when required. A guarantee does not, however, eliminate risk completely; it merely shifts the risk of default or loss from the borrower to the guarantor, up to the guaranteed amount.

DLG & bankruptcy remoteness

The DLG guidelines specify the forms in which a DLG can be obtained. DLG can be accepted in any one of the following forms:

- Cash deposited with the RE;

- Fixed Deposit maintained with a Scheduled Commercial Bank with a lien marked in favour of the RE;

- Bank Guarantee in favour of the RE

Accordingly, DLG can only be obtained in fully funded forms, thus eliminating any question of incurring credit loss on such a guarantee. Does that mean that even in case of insolvency of the DLG provider the lender will have the right to invoke the guarantee? The answer to this is negative. Because unlike in the case of bankruptcy-remote SPV, the guarantor is an operating entity, and is prone to the risk of insolvency.

In case of initiation of insolvency proceedings, all the assets of an insolvent entity form part of the insolvency administration/liquidation estate and are beyond the reach of the creditors. The proceeds from the realisation of assets are paid to the creditors in accordance with the waterfall mechanism as specified under section 53 of the IBC, 2016 .

Accordingly, it becomes important to determine how each permitted form of DLG would be treated in the event of insolvency of the DLG provider.

- Cash deposited with RE: The cash deposited with the lender is actually a liability held in the books till the same is invoked. As per Section 36 of IBC 2016, assets that may or may not be in possession of the corporate debtor including but not limited to encumbered assets form part of the liquidation estate. Accordingly, cash deposited by the DLG provider with RE would form part of the liquidation estate of the guarantor.

- Lien marked FD: Similar to cash deposited with RE, the lien marked FD will also form part of the liquidation estate.

- Bank Guarantee: In the case of a bank guarantee, the credit exposure effectively shifts from the original guarantor to the issuing bank. Given that scheduled commercial banks are subject to stringent regulation and supervision, the risk of insolvency in banks is generally remote. Accordingly, the probability of default in such a structure is unlikely to be impacted.

So, even if the DLG is structured as a funded guarantee, the actual invocation can become complicated if the DLG provider goes into insolvency before such invocation. In such a situation, the lender may not be able to simply invoke the guarantee and take the money. Instead, it may have to submit its claim and wait for distribution under the insolvency process, where payments are made in the statutory priority order.

Under the waterfall mechanism, secured creditors rank alongside workmen’s dues. Now, in most DLG structures, the guarantor is a fintech entity or a co-lender. These entities typically do not have significant workmen-related liabilities. This may mean that the lender’s priority position is relatively stronger.

Further, the actual invocation process of the DLG should also be considered. For instance, cash held with the lender can be easily invoked and adjusted as compared to a lien-marked FD or bank guarantee, where there could be procedural delays.

Illustration: Consider a loan pool of ₹100 crore where the gross ECL rate is estimated at 6.8% (for the static pool covered by the guarantee), resulting in a gross ECL of ₹6.8 crore. The lender has a DLG cover of 5% of the pool (₹5 crore), structured as a lien-marked fixed deposit provided by a fintech sourcing partner. While the DLG is funded, there remains a risk that the guarantor may become insolvent. The first relevant question here is whether we will take a probability of default (PD) as per Stage 1 (12 months PD), or Stage 2/3 (lifelong PD). While the guarantor in question is not in default at all, however, given that the 6.8% ECL is a combination of Stage 1 as well as Stage 2/3 loans, in our view, the PD for the guarantor, to remain conservative, should be the lifelong PD over the tenure of the loans. Let us assume a 20% Probability of Default (PD) for the guarantor. Next question is assessment of Loss Given Default (LGD). As discussed above, the lender has the benefit of full security in form of lien on the fixed deposit, however, there may be depletion of the same on account of first priority in the waterfall, that is, costs of insolvency and bankruptcy process. On a conservative basis, we may, therefore, assume a 10% LGD. Thus, the expected loss on the DLG cover would therefore be 20% × 10% = 2%.

As a result, the ECL computation may now be:

= 5%*2% + 1.8% = 1.9%

Based on the aforesaid discussion, in our view, while the guarantee is funded the lender may have to adjust the probability of default to factor in the risk of insolvency, particularly where the guarantee is funded in the form of a cash deposit or a lien marked FD.

Which funded form of DLG is most suited?

As per the analysis, the various options of funded DLG can be ranked basis the maximum consideration allowable for ECL computation:

- Bank guarantee: Being bankruptcy remote and easiest to invoke

- Cash deposit: May have to consider the risk of guarantor’s bankruptcy but the invocation would be easier

- Lien marked Fixed Deposit: May have to consider the risk of guarantor’s bankruptcy and invocation may involve procedural delays

However, given that there will not be a sizable or material difference in the quantum of counter guarantee risk, the selection of the options for ECL computation may not be significant.

Can we help this situation?

One of the ways to mitigate the risk of insolvency is by structuring the guarantee in such a way that the guarantee may be invoked upon the occurrence of an adverse material change in the financial condition of the guarantor. In other words, other than the occurrence of losses in the pool, if there are events of default such as adverse material change, insolvency of the guarantor etc., the lender may invoke the guarantee.

Early invocation upon identifiable stress on the part of the guarantor could help the lender realise the guarantee amount before the commencement of insolvency proceedings.

However, such clauses must be appropriately incorporated and drafted in the DLG agreement to ensure the following:

- A clear definition of “adverse material change”

- Identifiable trigger events

- Clarity on invocation mechanism

Impact of DLG invocation on ECL computation

RBI has also provided a clarification that upon every event of invocation of DLG, the DLG cover reduces to the extent of invocation. Accordingly, REs would be required to recompute their ECL provisioning requirements across stages, after duly adjusting for the reduced DLG cover.

Pool-based guarantees presuppose that the pool is static. This is purely intuitive because if the pool is dynamic, new loans will continue to enter the pool, and therefore, the guarantor’s exposure will keep spreading over a continuing flow of new loans.

Where the pool is static, the loans gradually get repaid (amortised) over time. As borrowers repay their instalments, the outstanding amount of the loan pool keeps reducing. Since the exposure is shrinking, the ECL on that pool will also typically reduce over time, assuming normal performance. Therefore, whether the utilisation of the DLG on account of pool defaults may cause the ECL computation to increase? This may be so for 2 reasons: one, usual terms of DLG invocation will be the full amount of the defaulted loan will be recovered (due to escalation of the entire principal outstanding). Thus, while the performing loans amortise over time, the non-performing loans are fully recovered once they reach “default”, causing the utilisation of the DLG to run faster than the amortization of the performing loans. Second reason is that once the pool actually starts defaulting, there may be a reason to provide higher estimates of probability of default as well.

Integral part of the contractual terms: Is DLG required to form part of the loan agreement?

Para 36A of the IRAC Directions read with the principles under Ind AS 109 provides that credit enhancements may be considered while computing ECL only where such enhancements are “integral to the contractual terms.” The expression “integral to the contractual terms” is taken from the definition of “credit loss” in Ind AS 109. Credit losses are measured after considering the expected cashflows from an asset. Those cashflows will factor in the recovery of any collateral, or credit enhancements, as long as the said credit enhancement is integral to the contractual terms.

What exactly is the meaning of “integral to the contractual terms”? Are we expecting the guarantee (DLG in the present case) to be a part of the terms of the loan contract? That would never be the case, as the so-called guarantee (which may legally be regarded as an indemnity contract) is a bilateral contract between the lender and the DLG provider. Neither is the borrower aware of the guarantee, nor is it desirable to have the borrower know of the guarantee, for obvious reasons.

IFRS 9 uses the same language. US ASC has more elaborate discussion on this. Para 326-20-30-12 says:

The estimate of expected credit losses shall reflect how credit enhancements (other than those that are freestanding contracts) mitigate expected credit losses on financial assets, including consideration of the financial condition of the guarantor, the willingness of the guarantor to pay, and/or whether any subordinated interests are expected to be capable of absorbing credit losses on any underlying financial assets. However, when estimating expected credit losses, an entity shall not combine a financial asset with a separate freestanding contract that serves to mitigate credit loss. As a result, the estimate of expected credit losses on a financial asset (or group of financial assets) shall not be offset by a freestanding contract (for example, a purchased credit-default swap) that may mitigate expected credit losses on the financial asset (or group of financial assets)

There has been a significant discussion on whether the benefit of a guarantee or credit enhancement which is not a part of the contractual terms of the loan can be factored in ECL computation. From discussions before the IASB, as back as in 2018, two conditions for recognising the benefit of credit enhancements were discussed:

- part of the contractual terms; and

- not recognised separately by the entity.

The second condition is easy to understand. For example, if the risk of default is hedged by a credit default swap, the value of the same, amounting to a derivative, is separately recognised. Hence, the question of factoring the same while computing ECL does not arise. However, the first condition, relating to contractual terms of the asset, still remains vague.

One may try to get some clues in the US FASB discussions, where para 326-20-30-12 has been interpreted in technical interpretations. In addition, there is a definition of “freestanding contracts” under the Glossary of ASC 326:

A freestanding contract is entered into either:

a. Separate and apart from any of the entity’s other financial instruments or equity transactions

b. In conjunction with some other transaction and is legally detachable and separately exercisable.

The “forming integral part of the contractual terms” does not warrant the principal contract to provide for the guarantee or the credit enhancements. Insisting on the same will be counter-intuitive, except in case of trilateral contracts. However, the conditions indicate that the guarantee or credit enhancement integrates and becomes an inseparable part of the underlying loan or group of loans. For example, if the group of loans was to be transferred, is it such that the benefit of the guarantee may stay iwth the originator and loans may be transferred, or the guarantee travels along with the loans? If the latter is the case, there is no doubt that in reality, the guarantee has become an embedded part of the loan transaction.

Another factor may be the contractual association between the loan cashflows and the payout from the credit enhancements. Some relevant considerations:

- Is the guarantee specific to the contractual cashflows from the loans?

- Does the guarantor pay what the original loan asset would have paid, or pays independent of the contractual cashflows?

- If the lender subsequently recovers the cashflows from the asset, is the payout from the guarantee restored back to the guarantor?

The presence of these factors will suggest the integration or embedding of the guarantee into the contractual cashflows from the loans.

Conclusion

While the recent amendment by the RBI brings welcome clarity by allowing DLG to be factored into ECL computation, lenders must approach this carefully and realistically. A DLG can reduce the expected loss, but it does not make the risk disappear, as the DLG provider itself faces the risk of insolvency. The form of the guarantee, its enforceability, and the possibility of invocation- all of these matter in assessing the true level of protection. REs should not treat DLG as a mechanical deduction from ECL, but as a risk mitigant that requires thoughtful evaluation, continuous monitoring, and recalibration as the pool amortises and the cover reduces.

See our other resources:

First Securitisation of Bitcoin-backed Loans: The Beginning of a New Asset Class

Vinod Kothari and Simrat Singh | Finserv@vinodkothari.com

Ledn, a Cayman Islands based bitcoin-backed lender, has originated what is believed to be the first securitisation of bitcoin-backed loans. It is a pool of about $ 199 million bitcoin-backed loans, with a first loss piece of $ 11 million, roughly 6% of the pool.

Rating agency S&P assigned BBB (sf) rating to Class A, which has 20% credit support, and B-(sf) to Class B with 6% support.

For the first time, cryptocurrency collateral has been converted into a rated, tranched capital markets instrument. Bitcoin exposure, historically confined to exchanges and wallets, has been structured into bankruptcy-remote securities assessed by a mainstream rating agency. More importantly, the deal demonstrates that Bitcoin price volatility, custody mechanics and automated liquidation frameworks can be modelled within established credit enhancement and subordination structures.

Lending against crypto collateral

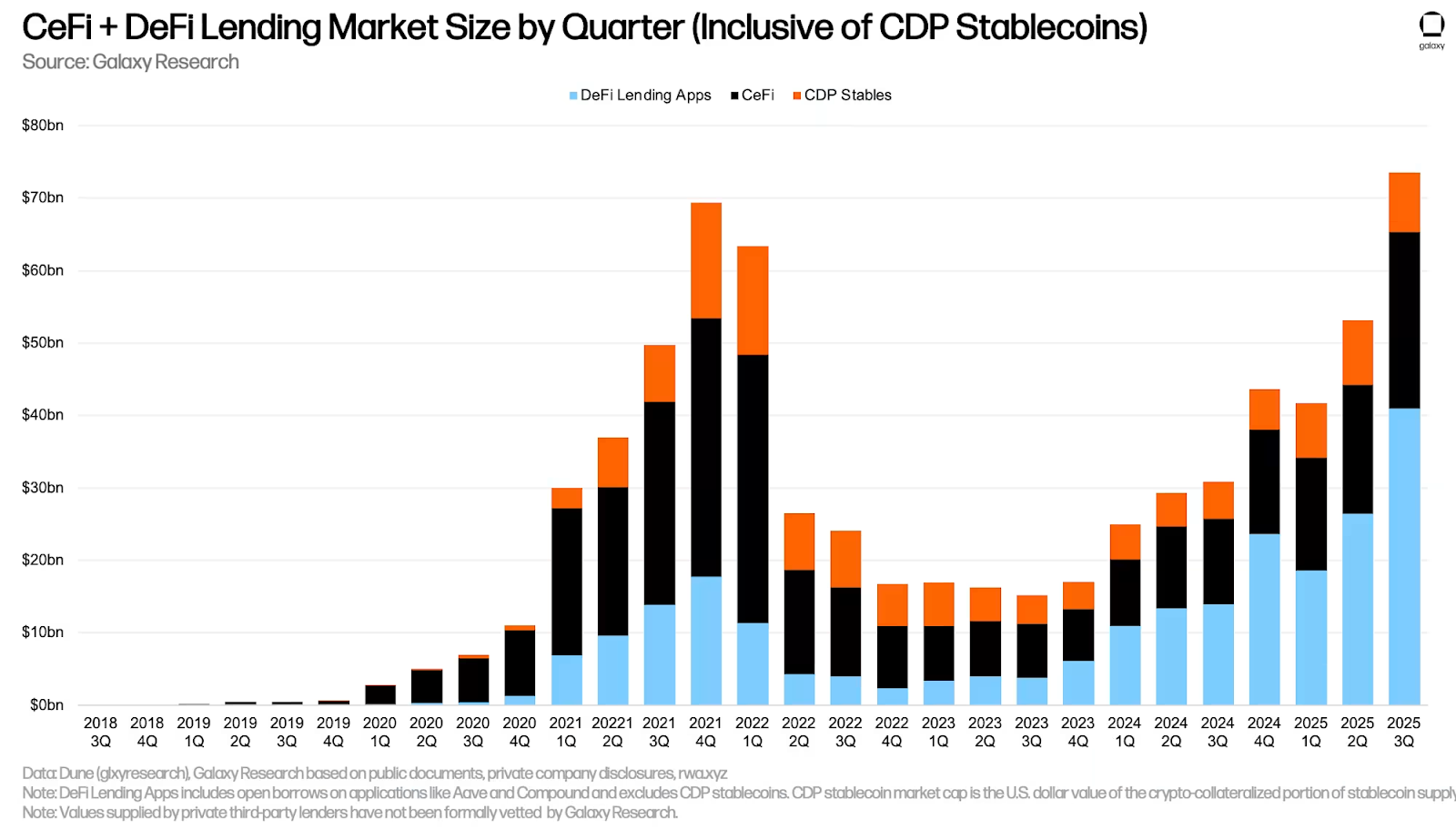

The market for collateralised lending against crypto currencies, according to a November 25 report by Galaxy, grew to reach a record volume of $ 73.6 billion by the end of Q3, 2025. This includes decentralised finance (DeFi) and centralised finance (CeFi) (see discussion below). DeFi uses smart contracts built on public blockchains to create a loan transaction if certain conditions are met; it creates a pledge that liquidates the currency if the specific LTV ratio is breached. Hence, the lending is almost like auto-triggered leverage on the crypto holding. In Defi, users retain custody of their assets and interact directly with protocols via crypto wallets. (See our article on DeFi here). CeFi, or better known as centralised lending is like the usual process of applying for a loan, qualifying for one, accepting the terms and then getting into a contract. Of course, the lending happens on specialised lending platforms, such as Binance or Coinbase.

On-chain and off-chain

As per IMF, crypto lending and borrowing is mostly channeled through crypto exchanges/financial digital platforms both centralized and decentralized, specialized in this business. The lending and borrowing through centralized (e.g., Nexo) and decentralized (e.g., Aave) platforms is also generally known as off-chain and on-chain lending, respectively. In the context of lending through centralized platforms, off-chain refers to the fact that the lending process and transactions are managed off the blockchain by a central entity. In contrast, lending through decentralized platforms is considered on-chain because it leverages smart contracts on a blockchain to facilitate lending and borrowing transactions. More importantly, on-chain transactions are actively facilitated by the platform which will ensure sufficient liquidity from depositors is available for lending

| Feature | Centralised Finance | Decentralised Finance |

| Intermediary | Centralised platform | No intermediary (protocol based) |

| Custody | Platform holds asset ie off-chain | Assets are held on-chain |

| Execution | Managed internally | Smart contract based automatic execution |

| Transparency | Limited since it depends on internal systems | Fully on-chain and therefore more transparent |

| Liquidation | Platform manager | Auto triggered via smart contracts |

| User experience | Simpler | Relatively more technical |

Regulatory concerns

Cryptocurrencies raise several regulatory concerns globally. Regulators are primarily focused on investor protection, given the extreme price volatility, risk of fraud, exchange failures and lack of clear legal recourse for users. Financial stability risk is another key concern, particularly as crypto markets grow in size and interlinkages with traditional financial institutions increase. Authorities also highlight AML, CFT and sanctions-evasion risks due to the pseudo-anonymous and cross-border nature of crypto transactions. Additional concerns include regulatory arbitrage, governance weaknesses at crypto platforms, custody and operational risks and the lack of uniform global standards regarding whether crypto should be treated as a currency, commodity, security or digital asset

In India, cryptocurrencies are not recognised as legal tender and are not considered currency under the law. The RBI has consistently expressed concerns regarding financial stability, monetary policy transmission, consumer protection, and illicit-flow risks. In April 2018, the RBI issued a circular prohibiting regulated entities from providing services to crypto businesses; however, this circular was set aside by the Supreme Court in Internet and Mobile Association of India v. RBI [Writ Petition (Civil) No.528 of 2018]. Despite the judgment, the RBI has maintained a cautious stance, warning that private cryptocurrencies may pose macroeconomic and systemic risks and advocating for strong regulatory oversight.

Most major crypto lending platforms are headquartered or legally domiciled in a small group of crypto-friendly financial jurisdictions rather than in countries that prohibit digital asset activity. A significant concentration is in the United States, particularly for larger, venture-backed platforms that target institutional or retail markets. Many crypto lenders are also structured through Cayman Islands and the British Virgin Islands due to flexible corporate law and tax breaks. In Asia, Singapore and Hong Kong have emerged as major hubs because they provide licensing regimes for virtual asset service providers and clearer regulatory frameworks for crypto trading and custody.

The United Arab Emirates (especially Dubai under the Virtual Assets Regulatory Authority or VARA) has become a fast-growing base for crypto exchanges and lenders due to its purpose-built digital asset regulatory regime. In Europe, activity is increasingly concentrated in jurisdictions aligned with the EU’s markets in Crypto-assets Regulations or MiCA framework, including countries like Germany and France, which offer regulated pathways for crypto custody and lending. Finally, Switzerland (Zug’s “Crypto Valley”) remains an important hub due to early legal recognition of digital assets and a mature fintech regulatory environment.

In short, most crypto lenders are located in jurisdictions that provide either (i) regulatory clarity with licensing pathways, or (ii) flexibility and structured-finance familiarity

How is the pledge of bitcoins registered?

Unlike land or securities, where a charge is perfected through a public registry or central depository, Bitcoin has no title registry on which a pledge can be recorded. A security interest over Bitcoin is, therefore, created contractually and perfected through control of the ‘private keys’. In practice, the borrower transfers the pledged Bitcoin into a segregated wallet held with a regulated custodian under a security and control agreement that prevents unilateral withdrawal and gives the secured party the right to direct liquidation of the Bitcoin held in that wallet upon default triggers.

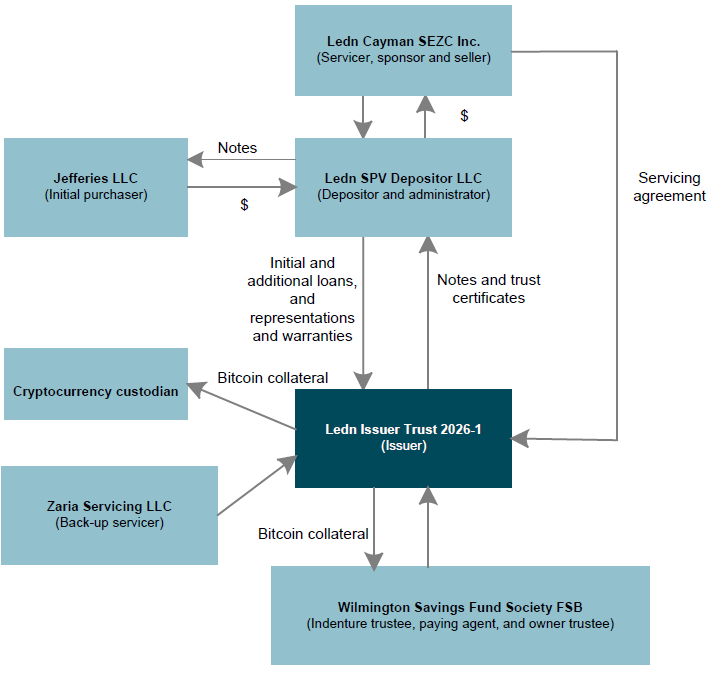

In the securitisation transaction at hand, this structure is embedded within a bankruptcy-remote issuer trust; the pledged bitcoin securing the underlying loans remains in custodian-controlled wallets, and the custodian agrees to follow the instructions of the trustee for investors.

Transaction Structure. Source: S&P Global

Why do borrowers take out a loan against crypto?

Borrowers might take crypto-backed loans to unlock liquidity without selling their crypto, preserving market exposure in case the crypto appreciates while avoiding a taxable disposal. Lenders market this explicitly (as “don’t sell your bitcoin”), because a loan does not trigger capital-gains events in many jurisdictions; selling does.

For example, in India, transfers of crypto [or Virtual Digital Asset (VDA) as defined in 2(111) of Tax Act, 2025] are taxed at a flat rate of 30% and subject to a 1% TDS as well (see section 194(1) and section 393 of Tax Act, 2025) which makes collateralised lending a much better alternative to an outright sale for investors seeking cash as it avoids a taxable transfer

Transaction structure

Underlying loans

The underlying collateral pool consists of 5,441 fixed-rate, balloon-style Bitcoin-backed loans extended to 2,914 borrowers, with an aggregate outstanding principal balance of approximately $199.1 million as of December 31, 2025 (’cut-off date’).

The loans are secured by approximately 4,078.87 BTC, which had an estimated fair market value of approximately $356.9 million at the cut-off date. This implies a weighted-average LTV of 55.78%, meaning the loans are materially overcollateralised at the borrower level.

While BTC collateral value (approx. $356.9 million) exceeds loan principal ($199.1 million), the securitised notes total $188 million ($160 million Class A + $28 million Class B). Credit enhancement to the notes is therefore driven by:

- Borrower-level overcollateralisation (WA LTV ~56%);

- Structural overcollateralisation of $11 million

- $199.1 million – ($160 million Class A + $28 million Class B)

- Subordination;

- A funded liquidity reserve ($9.4 million i.e. 5% of the outstanding note balance at closing);

Characteristics of underlying loans:

- Loan sizes range from $500 to $3,000,000;

- Interest rates range from 8.45% to 13.90%;

- Weighted-average interest rate: 11.80%;

- Weighted-average remaining term: ~8 months at cut-off;

- Maximum original tenor: 12 months

The loans are structured as bullet obligations, meaning borrowers repay principal and accrued interest in a single lump sum at maturity (or earlier via prepayment or liquidation). No scheduled amortisation occurs during the term.

If a borrower’s LTV rises to 80%, the loan is subject to liquidation through an automated engine that sells the BTC collateral to repay the loan.

Revolving Structure

The transaction features a 36-month revolving/reinvestment period. During this period, principal collections may be used to purchase additional eligible loans, subject to eligibility criteria and concentration limits. An initial $0.9 million funding account is available at closing to acquire additional loans. No principal is paid to noteholders during the revolving period unless an early amortisation event occurs. Such early amortisation triggers include:

- Servicer default;

- Effective advance rate exceeding 94%.

If triggered, the revolving period ends and principal begins to amortise sequentially (Class A first, then Class B).

Key sources of credit support include:

- Borrower-level overcollateralisation (WA LTV ~56%);

- Subordination;

- Liquidity reserve account;

- Funded at 5% of outstanding note balance at closing.

- Steps down over time

- Automated liquidation mechanism at 80% LTV

How does it address the volatility of Bitcoin prices

The transaction mitigates Bitcoin price volatility at both the loan and securitisation levels. At the loan level, underwriting is conservative, with loans originated at approximately 50% LTV, meaning borrowers pledge Bitcoin worth roughly twice the loan amount. As of the cut-off date, the pool had a weighted-average LTV of 55.78%. Margin notifications are issued at 70% and 75% LTV, and if LTV reaches 80%, the loan is automatically liquidated unless cured by additional collateral or partial repayment. This dynamic margin framework is designed to ensure that collateral is monetised well before LTV approaches 100%, thereby protecting principal.

At the securitisation level, protection is provided through multiple structural features. The collateral coverage is approximately 1.79x relative to loan principal, reflecting a substantial borrower-level cushion. In addition, the loan pool (~$199.1 million) exceeds the issued notes ($188 million), creating structural overcollateralisation of roughly $11 million. Subordination of the $28 million Class B notes beneath the $160 million Class A notes provides further credit enhancement, and a funded liquidity reserve of $9.4 million (5% of notes at closing) supports timely payment of interest and fees. While the underlying loans are short-term and bullet in nature, the transaction includes a revolving period, so volatility risk is managed primarily through LTV-triggered liquidation mechanisms and structural credit enhancement rather than tenor alone.

Conclusion

In jurisdictions where the legal status of cryptocurrency and its ownership remains uncertain or not expressly recognised, investor appetite for securities backed by crypto assets may be tempered. Questions around enforceability, custody and recognition of digital asset collateral could weigh on institutional participation. However, the relatively high interest rates associated with crypto-backed lending structures may prove attractive in yield-constrained environments.

For many investors, such securitisation offers an indirect pathway to participate in the economic upside of the cryptocurrency ecosystem, without holding the cryptocurrency directly and without assuming the operational, custody, or tax complexities associated with owning the asset itself. Whether this hybrid bridge between traditional capital markets and digital assets scales meaningfully will ultimately depend on regulatory clarity, investor risk tolerance and the continued maturation of crypto market infrastructure.

Lastly, the jurisdictional architecture is not incidental but foundational to transactions such as the present securitisation. A rated, bankruptcy-remote structure backed by Bitcoin-collateralised loans can emerge only where digital asset ownership, custody arrangements and enforcement mechanics are legally recognisable and commercially workable. The securitisation of bitcoin-backed loans is, ultimately, as much a product of regulatory geography as it is of financial engineering.

See our other resources:

- YouTube video: What is Securitisation?

- Tokenisation of Real World Assets – The Way Ahead for Creating Securities;

- Disrupting Traditional Card based Payments – Smart Contract based Payment Infrastructure using Stablecoin

- Cryptos: Are They Back in Business?;

- Security Token Offerings & their Application to Structured Finance;

- Decentralised Finances;

- Cryptocurrency on the path to Legalisation?;

- Cryptocurrency – A Cautionary Tale for India;

- Trustless System;

- Blockchain based lending; A peer-to-peer system;

- Financial Services firms foray into the metaverse.

RBI permits Leveraged Buy-Outs through Bank Finance

– Conditions for acquisition finance, prudential limits and new LTV requirements for various capital market exposures

– Payal Agarwal, Partner | payal@vinodkothari.com

– Updated on March 31, 2026

Capital markets are subject to higher fluctuations and volatility, and hence, Capital Market Exposures (CME) carry a higher risk, naturally requiring higher level of control and prudential norms by the regulator. In a move to permit Leveraged Buy-Outs (LBOs), RBI issued Amendment Directions on Capital Market Exposures on 13th February, 2026, bringing amendments in various applicable Directions, covering, inter alia, conditions on acquisition finance, revised LTV limits for lending against various securities, structured requirements for funding Capital Market Intermediaries (CMIs), prudential limits on Capital Market Exposures (CMEs) etc. Through a press release on 30th March 2026, RBI has deferred the applicability of the Amendment Directions, and has issued revised Directions to clarify on certain aspects relating to acquisition finance and exposures to capital market intermediaries.

The amendments were based on the Draft Reserve Bank of India (Commercial Banks – Capital Market Exposure) Directions, 2025 issued on 24th October, 2025. See an article on the Draft Directions here.

Effective Date

The applicability of the Amendment Directions have been deferred to 1st July, 2026 (from its original effective date of 1st April, 2026), however, may be adopted by a bank prior to that as well in its entirety.

Outstanding loans/ guarantees are permitted to run-down till maturity, however, any fresh loans/ guarantees or renewal of existing loans/ facilities shall be governed by the Amendment Directions.

Navigating through the Amendments

The amendments w.r.t. CMEs have been effected through issuance of the following Amendment Directions:

| RBI (Commercial Banks – Credit Facilities) Amendment Directions, 2026 [“CF Amendments”] | Conditions w.r.t. Acquisition Finance, Loan against eligible securities, and funding Capital Market Intermediaries |

| RBI (Commercial Banks – Concentration Risk Management) Amendment Directions, 2026 [“CRM Amendments”] | Components of investment exposures and credit exposures in CME and prudential ceilings, exclusions from CME ceilings and |

| RBI (Commercial Banks – Financial Statements: Presentation and Disclosures) – Third Amendment Directions, 2026 [“FS Amendments”] | Revised format of disclosure of exposure to capital markets |

| Reserve Bank of India (Commercial Banks – Undertaking of Financial Services) – Amendment Directions, 2026 [“UFS Amendments”] | Applicability of conditions on acquisition finance and lending against securities to NBFCs/ HFCs within a bank group. Also see an article on the same here |

Permitting Acquisition Finance by Banks

Chapter XI of the extant CF Directions dealt with “Acquisition Finance”. The existing provisions of the said chapter have been omitted and new provisions w.r.t. Acquisition finance has been incorporated therein, prescribing eligibility conditions and compliance requirements w.r.t. Acquisition Finance.

Meaning and Conditions for Acquisition Finance

Acquisition Finance has been defined as:

“Acquisition Finance” shall mean a financial facility or assistance provided to an eligible borrower entity for the purpose of acquiring control in a target company, (including through a scheme of amalgamation or merger). Such funding may also involve refinancing of existing debt of the target company if the refinancing is integral to the acquisition finance. [Para 4(1)(ia)]

The Revised Directions clarify that acquisition finance may be availed with respect to mergers and acquisitions as well.

The operating conditions are laid down in Chapter XI from Para 170A onwards.

Eligibility conditions: Acquiring company and Target company

|

Acquiring company* |

Target company |

Financing Parameters |

|

● Indian non-financial company, ● May be listed or unlisted, ● Networth > Rs. 500 crores ○ As per sec 2(57) of CA, 2013 ● 3 years’ track record of PAT ● Investment grade rating (BBB- or above) from a CRA [in case of unlisted Acquiring company]

Financial criteria to be satisfied at a standalone and consolidated basis |

● Domestic or foreign company ● Non-financial company ● Shall not be Related Party to Acquiring company (in case of first-time acquisition of control) ○ u/s 2(76) of CA, 2013 ○ includes entities under common control, common management, or common promoter group, whether directly or indirectly |

● Credit assessment based on combined balance sheet of Acquiring co and target co. ● Max 75% of acquisition value can be financed, ● Remaining by Acquiring company using own funds. ○ shall mean internal accruals, sale of assets or redemption of investments, or issuance of fresh equity ○does not include Proceeds of any borrowing; instruments having fixed repayment obligation or put option, any intragroup funding from borrowed funds ● Instruments through which control acquired by Acquiring company shall be free from any encumbrance ● Nature and extent of security cover to be determined by bank ● Post acquisition consolidated debt-equity ratio of Acquiring company shall not exceed 3:1 on a continuous basis |

*Acquisition finance may be extended to the subsidiary or SPV set up by the Acquiring company, based on the strength of the Acquiring company. In such cases, corporate guarantee from the Acquiring company shall be mandatory.

Note that, while the Directions allow funding of upto 75% of the acquisition value, the same is subject to a more stringent condition of the post-acquisition debt-equity ratio of 3:1. The ratio is based on the consolidated financial position of the Acquiring company together with the Target company, meaning, the same is not only based on the debt position of the Acquiring company, rather, the existing debt of the Target company is also required to be taken into account. This may, in effect, reduce the total amount of acquisition funding that may be availed by the Acquiring company.

Let us consider an example:

- Target Assets : 1000; Equity: 333, Debt: 666

- Acquirer buys 100% of Target company, and has no other assets. Debt: 250, Equity 83

- Consolidated balance sheet Debt becomes 916 against assets of 1000, resulting in the debt-equity ratio breaching the limits

Therefore, the 75% of acquisition value will mostly not be possible, except in cases where the Acquirer has a lower than 3:1 debt-equity ratio.

Charge on acquired stake: operation of section 19(2) of BR Act

Acquisition Finance contemplates creation of security over the securities of the Target company acquired by the Acquiring company. However, section 19(2) of the Banking Regulation Act, 1949 puts a restriction on the creation of charge on a controlling stake in a company. The section reads as:

(2) Save as provided in sub-section (1), no banking company shall hold shares in any company, whether as pledgee, mortgagee or absolute owner, of an amount exceeding thirty per cent. of the paid-up share capital of that company or thirty per cent. of its own paid-up share capital and reserves, whichever is less:

Since acquisition finance is limited to acquisition of “control”, a substantial stake would be involved in every case, especially, where 100% of the Target company is being acquired. Assuming 75% of the acquisition value is being financed by the bank, the condition w.r.t. not holding more than 30% of the paid-up share capital of the (target) company may stand breached. Hence, the Directions use the term “without prejudice to section 19(2) of the BR Act, 1949”, thus, permitting a bank to create charge on as many securities of the entity as is possible without a breach of the requirements under the BR Act. Additional collateral may be sought on the other unencumbered assets of the acquirer and/or target company, and promoter’s personal guarantee, as per the bank’s policy.

Purpose of financing

Permitted for acquiring equity stakes as strategic investments, either leading to

- acquisition of control through a single or a series of transactions within 12 months from first disbursal of acquisition finance, or

- increase in stake towards acquiring control over the target company, or

- acquisition of additional stake crossing substantial thresholds [26%, 51%, 75% or 90% of voting rights], in a target company where control already exists.

The meaning of control is to be taken from section 2(27) of CA, 2013 thus, meaning to include the right to appoint majority of the directors or to control the management or policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly, including by virtue of their shareholding or management rights or shareholders agreements or voting agreements or in any other manner;

The Revised Directions clarify that the scope of acquisition of target company includes:

- Acquisition by the Acquiring company directly, or

- On-lending to its Indian or overseas non-financial subsidiary for such acquisition.

Indirect control through target company

With respect to indirect acquisition of control over subsidiaries or joint ventures, through acquisition of control over the holding target company, the Revised Directions clarify that the criteria w.r.t. creation of potential synergies for the acquirer must be suitably assessed considering all such companies.

Further, the acquisition finance cannot be extended towards acquisition of a target company having any financial entity as its subsidiary or JV.

Inconsistency between conditions for Acquisition Finance and purpose of Acquisition Finance

In the context of first-time acquisition of control, the CF Amendments require that the Target company and Acquiring company shall not be related parties. This would make an Acquiring company to raise funds through Acquisition Finance for acquiring control in its associate, where it already holds significant influence, but not control.

Further, the acquisition of “control” should, generally speaking, mean at least more than 50% of voting rights is acquired by the Acquiring company, in which case, the 26% threshold as referred to as substantial stake in an existing controlled entity becomes meaningless.

While in case of NBFCs, a change in 26% shareholding is considered as change in control by the RBI, the same is not the case under CA, 2013 – which distinguishes between significant influence and control, and hence, the reference to the definition of control as per CA, 2013 in the CF Amendments has resulted in these inconsistencies.

Bridge Finance

As regards Acquisition Finance, in case of a listed Acquiring company, the condition w.r.t. funding 25% of acquisition value through internal accruals may be met through bridge finance, subject to the specified conditions.

The Directions define bridge finance as:

“Bridge Finance” shall mean financing a borrower for an interim period, not exceeding one year, for a legitimate business purpose where the borrower has a firm plan and capability to repay such loans by raising financial resources either through issuance of equity, debt or hybrid instruments or by divestiture/hive-off of a part of existing business/assets within the interim period.

The conditions for availing bridge finance are:

- Repayment of bridge finance shall be done through internal accruals or an equity issue or sale of assets

- Bridge finance provided by the bank shall be on a secured basis

- Shall not result in dilution of security coverage for acquisition finance

Valuation requirements

- Bank to independently assess acquisition value

- To be determined by bank-appointed valuer

- Based on guidelines prescribed under Reg 8(2)(e) of SEBI SAST Regulations for shares not frequently traded, viz., using valuation parameters including, book value, comparable trading multiples, and such other parameters as are customary for valuation of shares of such companies [for both listed and unlisted company].

- In case of unlisted company, based on lower of the valuation determined as above by two independent valuers

Prudential Norms and Other compliances applicable on Financing Banks

- Board-approved Policy on Acquisition Finance – incorporating underwriting benchmarks that address the structural complexities of such transactions, in particular relating to exposure limits, equity contribution, leverage multiples, and cash-flow certainty.

- Prudential ceilings on Acquisition Finance – not more than 20% of Bank’s eligible capital base within the aggregate ceiling of 40% on CMEs, both on solo and consolidated basis [Para 98A of CRM Directions]. Bank may adopt a lower ceiling based on its overall risk profile and corporate strategy.

- Disclosure in financial statements – disclosure of various forms of CMEs of the bank separately, including acquisition finance, with further segregation of bridge financing for meeting own fund requirements by acquiring companies and financing by overseas branches of the Indian banks etc [Para 10(5)(iia) of FS Directions]

Lending against Eligible Securities

- Board-approved Policy on lending against eligible securities – specify the criteria for selecting securities as collateral; determining portfolio-level as well as single borrower/group borrower limits; concentration limits for exposure to single securities; LTV/margins and haircuts for different securities; and rules for ongoing valuation and margin calls

- Lending to individuals, including non-commercial HUFs

| Loan-to-Value (LTV) requirements | ||

| Nature of security | CF Amendments | Existing Provisions |

| Government Securities. incl. T-Bills | As per Bank’s Policy | 75% in case of equity shares/ convertible debentures (50% if held in physical form) In other cases, determined by Bank itself |

| Sovereign Gold Bonds (SGBs) | As applicable to lending against gold/ silver collateral | |

| Listed shares and listed convertible debt securities | 60% | |

| Mutual Funds (excluding Debt MFs), Units of ETF (excluding commodity ETFs) and Units of REITs/InVITs | 75% | |

| Debt Mutual Funds | 85% | |

| Listed Debt Securities | 85% – AAA rated 75% – AA-BBB rated | |

| Prudential ceilings | ||

| Acquisition of securities in secondary market | Maximum upto Rs. 25 lacs | Upto Rs. 20 lacs (in case of dematerialised securities) Rs. 10 lacs (in case of physical) |

| Maximum cap on loans to individuals# | Upto Rs. 1 crore for eligible securities other than G-Sec, listed debt and units of debt mutual funds | – |

| IPO/ FPO/ ESOP financing# |

|

|

#The aforesaid limits are applicable at a banking system level as clarified by the Revised Directions.

Lending to Capital Market Intermediaries (CMIs)

- Meaning of Capital Market Intermediaries:

- regulated entities undertaking trade execution and market infrastructure services in capital markets, including broking, clearing, custody, market making or other incidental services

- shall not include Standalone Primary Dealers and Qualified Central Counterparty (QCCPs)

- does not include Collective investment schemes such as mutual funds. AIFs, REITs, InvITs, etc.

- Eligibility criteria for CMIs: shall be registered and regulated by a financial sector regulator, and in compliance with the prudential norms of such regulator

- Conditions w.r.t. Security:

- Facilities shall be fully secured, and the value of securities shall be adjusted for haircuts as appropriate based on nature of securities, with a minimum haircut of 40% for equity shares

- Any guarantee issued shall be secured with minimum collateral of 50% including at least 25% in cash

- Eligible securities and cash pledged shall belong to borrower CMI

Restrictions on lending for proprietary trading

The Revised Directions clarify the scope and exclusions from the restrictions on lending to CMIs for acquisition of securities on its own account, including for proprietary trading and investments. The following are permitted on a fully secured basis:

- Finance to approved market makers in equity and debt securities

- Working capital finance for warehousing of debt securities, including Government Securities, upto a maximum period of 45 days for fulfilling firm demand/request from its clients

- Other working capital facilities against a 100 percent collateral of cash, cash equivalents and Government Securities (including T-Bills)

Guarantee may also be issued by banks for proprietary trading subject to the facility being fully secured collateral of cash, cash equivalents and Government Securities (including T-Bills), out of which a minimum 50 per cent shall be cash or fixed deposits maintained with the lending bank. Banks to ensure that guarantees issued for non-proprietary purposes are not used to facilitate proprietary trading.

Concluding Remarks

The amendments are a positive step towards facilitating bank finance for strategic acquisitions by Indian companies, balancing the funding requirements for acquisitions with prudential norms for banks to provide for safeguards against ambitious risky funding exercises.s.

Not Just a Marketplace: Lender Primacy, Disclosures and Consent Architecture in Digital Loan Sourcing

– Archisman Bhattacharjee (finserv@vinodkothari.com)

| Key Themes and Takeaways Digital loan sourcing through DLAs is no longer a marketing function; it is a regulated gateway into the lending relationship. The regulatory framework under the Reserve Bank of India and the Digital Personal Data Protection Act, 2023 together reshape how sourcing interfaces must be designed. REs remain the principal and legally accountable lender, even where DLAs and LSPs perform front-end sourcing functions. Lender identity, branding, and role must be clearly disclosed to borrowers from the first interaction on the DLA. Multi-lender platforms must operate in a fair and transparent manner, with visibility of matched and unmatched lenders. Sourcing flows must be consent-driven, with purpose-specific, granular and non-bundled consents. Borrowers must be shown relevant privacy policies before any data is shared with an RE or any third party. REs are ordinarily the data fiduciaries; DLAs/LSPs usually act as data processors unless they independently determine purposes. Platforms must support practical exercise of data principal rights, including withdrawal of consent and deletion requests. Data retention, segregation, access control and localisation are central to compliant sourcing architecture. |

RBI Proposes Uniform Recovery Norms Across All Lenders

Tejasvi Thakkar and Simrat Singh | Finserv@vinodkothari.com

Introduction

Pursuant to the RBI’s stated intent in the Statement on Developmental and Regulatory Policies to harmonise the conduct of Regulated Entities in relation to loan recovery, comprehensive draft instructions have been proposed, to be effective from July 1, 2026, consolidating and rationalising the existing scattered provisions. The instructions are applicable to all NBFCs, excluding Mortgage Guarantee Companies, Core Investment Companies, NBFC-Account Aggregators, Standalone Primary Dealers, Non-Operating Financial Housing Companies, and NBFCs not having any customer interface. The key requirements of the proposed framework are summarised below:

Key highlights

Policy Requirement

REs shall formulate a separate policy on recovery of loan dues, engagement of recovery agents and taking possession of security. The policy shall, inter-alia, cover:

- Eligibility and due diligence criteria for engagement of recovery agents.

- Specified recovery activities permitted to be carried out.

- Code of Conduct requirements.

- Performance evaluation standards, inspection and control mechanism.

- Procedures and penal actions in case of non-compliance by recovery agents.

- Recovery procedures in case of demise of borrower.

- Mechanism to identify borrowers facing repayment difficulties and provide guidance on recourse options

- Incentive structures not inducing harsh recovery practices..

- Enforcement and possession framework including legal action not to be adopted as the first resort.

Issue: Whether this can be combined with the policy on Code of Conduct for DSAs/DMAs?

Our view: Since the present requirement specifically deals with recovery conduct, possession and enforcement of security interest, and engagement of recovery agents, the same should ideally be maintained as a separate policy. The DSA/DMA CoC policy deals largely with sourcing-stage conduct such as mis-selling and consequent compensation-related aspects. However, where there are overlapping requirements, NBFCs may structure the same within a broader conduct framework, divided into separate sections. However, it should remain distinct from the outsourcing policy.

Due diligence (DD) requirements

- Frame and implement a due diligence framework in line with the RBI Outsourcing Directions, 2025.

- RE to ensure that recovery agencies shall undertake due diligence and verification of their employees/representatives at the time of engagement and on a periodic basis. Policy to specify such periodicity and scope of verification.

Training Requirements

- Recovery agents shall mandatorily possess certification from the Indian Institute of Banking and Finance (IIBF) for debt recovery agents. (Aligned with the HFC Master Directions)

- Existing agents without certification shall obtain the same within one year from issuance of directions

Code of Conduct for recovery Agents

- REs shall put in place a CoC for recovery agents and employees engaged in recovery and obtain undertakings for adherence.

- The CoC shall include, inter alia:

- Fair and respectful treatment of borrowers.

- Sharing only limited borrower information necessary for recovery and preventing misuse.

- Mandatory documents to be carried (ID card, copy of recovery letter etc)

- Permissible hours of contact

- Place of contact rules

- Restriction on contacting third parties

- Detailed prohibition of harsh practices

- Borrower information confidentiality

- No recovery action where grievance is pending, unless found to be frivolous

- Recording of recovery calls with due borrower intimation.

Issue: Whether the CoC prescribed earlier under HFC Directions stands subsumed?

Our view: Yes. The earlier HFC provisions largely stand harmonised and subsumed within the present draft framework, except for certain differences which have been captured in the Annexure below.

Recovery agents shall be required to carry recovery notice, identity card and authorisation letter, and shall adhere to the following conduct requirements:

- Interact only with the borrower / guarantor and not approach relatives or other contacts; maintain civil behavior;

- Contact / visit borrowers only between 08:00 hours and 19:00 hours;

- Honour borrower’s request to avoid calls / visits at particular times in normal circumstances;

- Contact borrowers ordinarily at the place of their choice, failing which at residence, and thereafter at place of business / occupation.

- Avoid calls / visits during inappropriate occasions such as bereavement, calamities, marriage functions, festivals, etc.

- In case of microfinance loans, undertake recovery at a mutually decided designated place, with field visits permitted only upon repeated non-appearance.

- Ensure only duly authorised representatives visit borrower’s premises for recovery activities.

- Ensure any written communication to borrowers has RE’s approval.

- Promptly issue proper acknowledgement / receipt for collections made.

- Refrain from harsh practices, including use of abusive language, excessive or anonymous calls, intimidation or harassment, threats of violence, misleading representations, or intrusion into borrower’s privacy.

Grievance redressal mechanism

- Establish a dedicated recovery-related grievance redressal mechanism.

- Provide complete details of the Grievance Redressal Officer and the mechanism in all recovery communications and loan agreements.

- Define criteria for identification and closure of frivolous complaints with appropriate internal oversight.

Responsibilities of REs

REs shall:

- Prominently display an up-to-date list of empanelled recovery agents on all customer interface channels. Details to be provided

- names of agents,

- details of individuals engaged and

- period of engagement.

- Promptly intimate the termination of recovery agents to prevent unauthorised interaction.

- Inform borrowers of the details of the recovery agent at the time of forwarding cases for recovery through written communication (letter, SMS or email), and immediately notify any change in the recovery agent during the recovery process.

Possession of mortgaged / hypothecated assets

Loan agreements shall contain a legally enforceable possession clause, clearly disclosed at the time of execution. The agreement shall, inter alia, specify:

- Notice period and circumstances for waiver;

- Procedure for taking possession of security;

- Final opportunity to the borrower for repayment prior to sale/auction;

- Procedure for restoration of possession;

- Transparent process for sale or auction of the secured asset.

Periodic review, monitoring and control

REs shall put in place a management structure to monitor and control the activities of recovery agents and ensure that such agents refrain from actions that could harm the RE’s integrity and reputation. Accordingly, the RE should ensure:

- Appropriate monitoring and conduct provisions shall be incorporated in agreements with recovery agents.

- Remain fully responsible for the actions of recovery agents.

- Undertake periodic review of recovery mechanisms to learn from experience and effect improvements.

For Housing Finance Companies:

Most of the proposed requirements are not entirely new in substance for HFCs, as they were already reflected in the Guidelines for Engaging Recovery Agents under paragraph 170 of the RBI HFC Directions, 2025. The proposal now is to delete those HFC-specific guidelines and require HFCs to comply with the proposed Directions.

However, while the underlying principles remain largely consistent, the proposed Directions significantly strengthen and formalise the recovery framework. The approach shifts from principle-based guidance to a more structured, prescriptive, and compliance-oriented regime. The key changes are as follows:

- Mandatory written recovery policy: Under the HFC Directions, compliance was required with paragraph 170, but there was no express requirement to frame a consolidated written policy governing recovery of loans, engagement of recovery agents, and repossession of security. The proposed Directions now mandate a formal, documented recovery policy. Such policy must specifically cover eligibility criteria for engagement of agents, due diligence standards, performance evaluation parameters, inspection and audit mechanisms, and penal actions for non-adherence. This marks a shift from guideline-based adherence to a structured governance framework.

- Borrower distress identification mechanism: The HFC Directions required utilisation of credit counsellors in cases where a borrower was considered to “deserve sympathetic consideration,” which was discretionary and reactive in nature. The proposed Directions introduce a mandatory mechanism to identify borrowers facing repayment difficulties, engage with them, and provide guidance on available recourse. The regulatory trigger is the existence of repayment difficulty itself, rather than a subjective assessment of sympathy, thereby institutionalising borrower engagement.

- Explicit data governance controls: While the HFC Directions required training of recovery agents on respecting customer privacy, the proposed Directions go further by mandating that only limited borrower information be shared with recovery agents and that adequate safeguards be put in place to prevent misuse or unauthorised transfer of customer data. This introduces clearer data governance and accountability obligations.

- Restriction on initiating legal action as first resort: The HFC Directions did not prescribe any sequencing rule regarding enforcement remedies. The proposed Directions now expressly provide that legal action for recovery or enforcement of security shall not be initiated as a first resort, thereby imposing a structured progression in recovery measures.

Conclusion

Recovery is as vital to lending as disbursement, if not more. Credit often begins with a courteous engagement by the lender, but too often, the standards of professionalism seen at the time of sanction weaken at the stage of enforcement. The right to recover is unquestionable; harassment is not. The proposed Directions seek to correct this imbalance by requiring lenders to uphold the same standards of fairness, transparency and discipline during recovery as at the time of origination.

See our other resources:

Not a Broker, Not an Insurer: Welcome to the world of MGAs

- Manisha Ghosh and Abhishek Kumar Namdev | finserv@vinodkothari.com

Introduction

The insurance industry globally has witnessed the emergence of several hybrid operating models that do not fit neatly within traditional regulatory classifications. One such model is that of the Managing General Agent (‘MGA’), an entity that performs significant insurance functions such as underwriting and risk assessment, pricing of insurance products, binding of policies, etc on behalf of the insurer.

While MGAs are well-recognised in mature insurance markets such as the USA, UK and Canada, their position under Indian insurance law has recently begun to take shape. An MGA typically acts as a middleman between the insurer and the insured.

In this article, we dive into the functioning of an MGA and how it differentiates from the existing insurance intermediaries, prevalent in the insurance sector in India.

Read more →