Two notifications issued under the Tamil Nadu Money Lending Entities (Prevention of Coercive Actions) Act, 2025 are in the news, as they lay down the registration framework for money-lending entities operating in Tamil Nadu. We have already clarified in our earlier write-up that the TN Act does not apply to NBFCs therefore there is no question of them going ahead and registering under the same. However, the provisions dealing with coercive recovery practices are very much applicable to NBFCs and unfortunately are quite widely worded as well.

At first glance, this may appear to be a double whammy for NBFCs. On the one hand, NBFCs are already subject to detailed recovery and customer conduct requirements prescribed by the RBI. Notably, RBI has also proposed a uniform framework on recovery practices across all REs which we had covered here. On the other hand, the Tamil Nadu legislation introduces state-level consequences where recovery practices are alleged to be “coercive”. In our view, if an NBFC follows the RBI framework in letter as well as spirit, it is unlikely to face any difficulty under the State law.

That said, given the fact that a defaulter would never be happy with any recovery measures, it is quite possible that NBFCs face complaints by borrowers in terms of recovery action under section 20. Section 21 provides for severe criminal consequences. Defaulting borrowers may be a bit more active or aggressive than lenders who have been defaulted against. For example, even while the Act is being comprehended, there is already a case registered under sections 20 and 21 against a recovery agency.

One might then ask who exactly is intended to be covered under the Act, given that banks (commercial as well as cooperative) and NBFCs are outside the registration framework. It so appears that informal money-lending activities and so-called ‘loan sharks’ are quite active in the State. It has historically taken legislative steps to curb such practices. For instance, the State had earlier enacted the Tamil Nadu Prohibition of Charging Exorbitant Interest Act, 2003 to deal with usurious interest-charging practices. The present law continues that policy objective by requiring such money-lending entities to register before carrying on lending activities.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-13 17:49:072026-03-13 18:05:25Not Registration but Caution: What Tamil Nadu Coercive Actions Law Means for NBFCs

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-13 17:26:312026-04-06 11:12:47Call for papers - Wadia Ghandy Awards for Structured Finance Research

The Telecom Regulatory Authority of India (TRAI) has mandated the use of the 1600-series numbering for service and transactional voice calls by entities regulated by RBI (including NBFCs), SEBI, and PFRDA, to curb financial frauds through mis-selling and unauthorised communications. The Reserve Bank of India has aligned with this via a notification dated January 17, 2025, titled Prevention of financial frauds perpetrated using voice calls and SMS – Regulatory prescriptions and Institutional Safeguards (‘Circular’), requiring NBFCs to use ‘1600xx’ series for such calls to existing or prospective customers. Considering that the 1600 series numbers had been mandated by TRAI to be adopted within 1st March, 2026 for NBFCs having asset size less than Rs. 5000 crore and 1st January 2026 for NBFCs having asset size more than Rs. 5000 crore, it becomes important to understand whether all NBFCs are required to adopt this or the adoption is activity specific. In this article we discuss the implementation and adoption of the 1600 number series.

Objective

The Telecom Commercial Communications Customer Preference Regulations, 2018 (‘TCCCPR’) was brought in with the purpose of curbing unsolicited commercial communications and towards ensuring that all customer communications are made through verified and approved numbers. Pursuant to this TRAI brought in the Notification to complement its earlier issued notification dated 23 December, 2024, for government and entities in the BFSI sector (including NBFCs), suggesting a phased-wise adoption plan for using the 1600 series numbers. Further, TRAI also clarified in its Notification that adoption of 1600 series by BFSI entities will:

“(a) be a major tool to curb promotional calls made in the guise of service and transactional calls, which often result in spam and potential scams; and;

(b) provide BFSI entities a distinct identity segregating them from other callers and will also enable consumers to make informed decisions regarding call acceptance;”

Pursuant to the TRAI notification on phase-wise adoption of 1600-series by BFSI sector entities, regulated by RBI, SEBI and PFRDA (‘Notification’), the RBI on 17 January, 2025 mandated all NBFCs (including HFCs) to use the ‘1600xx’ numbering series for the purpose of making any transaction/service calls. Further, under the Circular, the RBI also clarified that the use of 1600 series numbers would help in curbing online and other frauds for the BFSI customers.

Compliance Requirement

The requirement towards adoption of the 1600 number series for making transactional and service calls stems from the requirement of Regulation 3 of the TCCCPR which states that:

“Commercial communications through network of Access Providers.-

(1) Every Access Provider shall ensure that any commercial communication using its network takes place only using registered headers or the number resources allotted to the Senders from special series assigned for the purpose of commercial communication.

(2) No Sender, who is not registered with any Access Provider for the purpose of sending commercial communications under these regulations, shall make any commercial communication, and in case, any such Sender sends commercial communication, all the telecom resources of such Sender may be put under suspension or may also be disconnected as provided under these regulations”

Further the term “commercial communication” has been defined under Regulation 2(i) of the TCCCPR and is defined as:

“means any voice call or message using telecommunication services, where the primary purpose is to inform about or advertise or solicit business for

(A) goods or services; or

(B) a supplier or prospective supplier of offered goods or services; or

(C) a business or investment opportunity; or

(D) a provider or prospective provider of such an opportunity;

Explanation:

For the purposes of this regulation it is immaterial whether the goods, services, land or opportunity referred to in the content of the communication exist(s), is/are lawful, or otherwise. Further, the purpose or intent of the communication may be inferred from:

(A) The content of the communication in the message or voice call

(B) The manner in which the content of message or voice call is presented

(C) The content in the communication during call back to phone numbers presented or referred to in the content of message or voice call; or the content presented at the web links included in such communication.”

Hence “Service Call” as defined under Regulation 2(bh) of the TCCCPR falls under the definition of commercial communication.

Do all NBFCs need to comply?

The above obligation under Regulation 3 of TCCCPR applies only to entities acting as “senders” who initiate or cause such commercial communications using telecommunication services, regulated by TRAI, to a “customer”. This suggests that entities which:

do not have any customer outreach or customer interface, or

have customer outreach or customer interface functions; however, do not use any calling service regulated by TRAI for communicating with the customers

would not qualify as “Senders” under the TCCCPR. Consequently, the mandate requiring the use of the 1600 series would not be applicable to such entities in practice.

The core intent of the RBI and TRAI is fraud prevention through identification of legitimate BFSI transactional calls. While the mandates as stated in the Circular encompasses all NBFCs regulated by the RBI to adopt the 1600 series, regardless of the asset-size or activity, regulatory compliance is assessed on substance over form, that is to say, the obligation to adopt 1600 series comes into picture only when an NBFC proposes to engage in (or causes) servicing/transactional voice calls or SMS with its customers.

NBFCs with zero history of such communications or NBFCs who are not intending to engage in such communications utilizing the telecommunication service regulated by TRAI, pose no fraud vector through the usage of such communication channels and thus have no practical compliance burden. Therefore for such NBFCs, proactive adoption is neither required nor operationally relevant until customer-facing communications commence or the NBFCs wish to communicate with the customers, utilizing the telecommunication services regulated by TRAI.

Does this compliance mandate extend to transactions with group entities?

The requirement relating to the use of the 1600 series numbering framework under the TCCCPR must be interpreted in light of the regulatory purpose underlying the framework introduced by TRAI. The 1600 series numbering framework has been introduced primarily to enable recipients of service and transactional voice calls to distinguish legitimate communications from telemarketing calls and to mitigate risks associated with unsolicited commercial communications and telemarketing-related frauds. In the context of intra-group lending arrangements, service-related communications are undertaken pursuant to an existing commercial relationship between entities forming part of the same corporate group. Such communications are typically operational or administrative in nature, including communications relating to servicing, monitoring or administration of an existing lending facility. These communications arise from pre-existing contractual arrangements and are not directed towards outreach or solicitation of customers or members of the public.

It is also relevant to note that the concept of “customer interaction” in financial sector regulation is generally understood to refer to engagement with external counterparties in the ordinary course of a regulated entity’s business. Where the interaction is confined to entities within the same corporate group, particularly where there is overlap in shareholding, management or control, the relationship is fundamentally different from a typical lender-customer relationship involving members of the public. Such intra-group arrangements are internal or strategic in nature and do not involve the kind of public-facing engagement that ordinarily triggers consumer protection considerations.

Further, intra-group lending arrangements are typically bespoke and undertaken based on the specific funding requirements of the relevant group entity, rather than pursuant to standardized loan products offered to the market. The terms of such transactions are usually determined on a bilateral basis and may be subject to internal governance processes, including board-level or audit committee/credit committee for related party transactions, oversight applicable to related party transactions. Accordingly, the information asymmetry and imbalance of bargaining power that consumer-protection frameworks seek to address are generally absent in such arrangements.

In addition, communications between group entities are ordinarily carried out through established internal or pre-identified channels, given the ongoing commercial relationship and the shared governance structure within the corporate group. Consequently, the risk of telemarketing-related frauds or unsolicited commercial communications, one of the principal concerns that the 1600 series framework seeks to address, is significantly weakened in the case of intra-group interactions.

In light of the above, service-related communications undertaken by an NBFC with a group entity in connection with an existing intra-group lending arrangement may not ordinarily invoke the regulatory concerns that the 1600 series framework is intended to address. Hence, where loans are provided to group entities, for the purpose of engaging in service calls the requirement of adoption of 1600 series numbers may not be required.

To further mitigate the risk, if any, which may arise during the above transactional communications, BFSI sector entities may send all transactional and service-related messages to group entities (or other third-party borrowers) via official email IDs. This approach further ensures non-applicability of the 1600-series requirements under TCCCPR, as email communications operate outside TRAI-regulated telecom networks for voice calls and SMS. Official emails provide a verifiable, auditable trail-aligned with RBI’s emphasis on digital record-keeping—while minimizing fraud risks through domain-based authentication and internal governance protocols for related-party interactions.

Does the same logic apply to Wholesale/Non-retail Lending outside the group?

The rationale exempting intra-group transactions from the 1600-series requirement extends analogously to wholesale or non-retail lending to external corporate borrowers, where service and transactional communications occur through pre-identified single points of contact (SPOCs). Loan agreements in such arrangements explicitly designate SPOCs on both lender and borrower sides, establishing a closed-loop communication channel that eliminates the anonymity exploited by fraudsters in retail contexts.

This structure inherently mitigates the spam and scam risks targeted by TRAI/RBI mandates, as borrowers rely on contractual contact details rather than unverified calls. Consequently, imposing the 1600-series here would serve little practical purpose, as the pre-existing verification framework under commercial contracts aligns with the substance of TCCCPR’s fraud-prevention objectives. NBFCs engaged solely in such lending face no operational need for 1600 numbers unless expanding into public-facing retail activities.

That said, per the strict wording of the TCCCPR Regulations, “service calls” qualify as commercial communications under Regulation 2(bh) when made via regulated telecom networks, requiring use of registered headers or special series like 1600xx under Regulation 3 . Thus, while the logic may not align perfectly with fraud-prevention intent in closed SPOC setups, BFSI sector entities must comply to avoid penalties such as telecom resource suspension-prioritising form alongside substance.

Conclusion

While the 1600-series mandate imposes a uniform compliance layer on BFSI sector entities to combat fraud via identifiable transactional calls, its practical applicability hinges on actual customer-facing communications under TCCCPR. Entities without retail outreach or public interfaces bear no operational burden, as the regulation targets external “senders” exploiting telecom networks for solicitation or service interactions.

Intra-group transactions further fall outside this scope, given their internal, contractual nature devoid of consumer protection risks like information asymmetry or spam. Adoption also remains unnecessary for non-communicating entities, preserving regulatory substance over form.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-13 13:27:212026-03-13 13:27:22Adopting 1600-Number Series- Preventive Measure or Burden?

The relevance of “arm’s length assessment” in any related party transaction is non-negotiable. Arm’s length is a consideration that runs across all corporate transactions, including those with unrelated parties. However, where the party itself is at arm’s length, that is, unrelated, the question of the transaction terms being other than arm’s length does not surface. In case of related parties, going by the very nature, the party is not at arm’s length, which is precisely why the need to establish arm’s length arises.

Typically, companies will have hundreds of transactions with unrelated parties. Obviously enough, these hundreds cannot be having a uniform price. It does not require elaboration to say that in business reality, prices have a range, and not a single price. When companies try to justify their impugned transactions with a related party, the practice quite often is to pull one value out of the range of values with unrelated parties, juxtapose that with the proposed RPT, and thus find a justification for the arm’s length.

Is one value out of the range of values sufficient to establish arm’s length? Or does AL have to be the central tendency (that is, a median or modal value) out of the range? This is the point that this article tries to deal with.

Additionally, the article also deals with the meaning of arm’s length beyond pricing, ways of establishing arm’s length where comparables are not available to the company, compliances and consequences pursuant to non arm’s length transactions.

This brings us to the more basic question of what exactly is the “arm’s length terms”, and can it be established based on terms comparable at any specific point of the arm or is it the length of the arm that matters – based on which the middle point of the distribution becomes the ideal indicator of arm’s length.

Meaning of arm’s length: How the regulators define the term?

There is no explicit mention of arm’s length under SEBI LODR. An explanation under section 188 of CA, 2013 refers to the term as follows:

‘The expression “arm’s length transaction” means a transaction between two related parties that is conducted as if they were unrelated, so that there is no conflict of interest.’

The standards on auditing (SA 550 pertaining to Related Parties) also defines the term as:

A transaction conducted on such terms and conditions as between a willing buyer and a willing seller who are unrelated and are acting independently of each other and pursuing their own best interests.

Therefore, in order to consider a transaction to be at an arm’s length, two elements are important:

The transaction is undertaken on terms similar to those between unrelated parties, and

There is no conflict of interest, that is, the transaction is undertaken independently, in the best interest of the entities in question.

Similarity of terms with unrelated parties: are outliers good comparables?

While considering comparables to establish arm’s length, companies often cherry pick a few transactions at similar terms with non RPs. But how difficult is it to engineer a near favourable transaction with a non RP? These transactions may be termed very differently from the majority of the transactions and yet appear to be comparables.

Illustrating the problem with Outliers

Let us consider this illustration where a company sells a product to its non RP customers at varying prices and its RP at Rs. 651. The management presents 4 transactions of series A (Rs. 650) to C (Rs. 652), done with unrelated parties, as comparable transactions, which establish the RPT to be at arm’s length. The audit committee is obviously not doing a full fledged factual examination, and therefore, may not even get into transactions of series D (Rs. 655) to F (Rs. 657) where most (25) of the transactions are placed.

Given the above diversity, can a transaction at Rs. 651, a value at an extreme left of the above frequency distribution, still be an arm’s length value? The key question is – does arm’s length justification come from just one from a range of values, or from the central tendency in the range?

Arm’s length is a question that is not limited to CA or LODR. Arm’s length considerations span over Income-tax law, GST law, audit framework, etc. In fact, corporate governance is all about transacting with arm’s length valuations. We will not even expect corporate laws to provide detailed guidance on whether the arm of the arm’s length can be long enough to pick an extreme value, or does it have to be the elbow of the arm, that is, the hump in the middle.

The Income Tax Laws provides some guidance

The Income Tax Act provides several methods to determine arm’s length pricing for a transaction, of which, one shall pick the most appropriate:

Comparable Uncontrolled Price Method: Price charged in a comparable uncontrolled transaction is identified and adjusted for differences, if any.

Resale price method: price at which property/services obtained from an associated enterprise is resold to an unassociated enterprise – adjusted by a normal gross profit margin in a CU transaction, expenses, and differences, if any.

Cost plus method: Direct/indirect costs are increased by an adjusted mark-up to such costs. Adjusted mark-up is normal gross profit mark-up arising in an uncontrolled comparable transaction adjusted for differences, if any.

Profit split method: Combined net profit is split amongst enterprises in proportion to relative contributions. Relative contribution is evaluated on the basis of reliable external market data – unrelated enterprises performing comparable functions.

Transactional net margin method: The net profit margin (computed in relation to costs incurred, sales effected, etc.) arising in a comparable uncontrolled transaction is adjusted for differences.[1]

Where the most appropriate method is any method from (a) to (c) or (e) that leads to several values being possible ALPs, a dataset shall be constructed of such values. This is the guidance we get from Income Tax Rules:

If the dataset consists of at least 6 values, a range of ALPs shall be considered from the 35th to the 65th percentile of this range.[2]

If the actual price of the transaction is outside this range, the median of the range shall be considered as the ALP for the purpose of tax assessment[3].

This would easily eliminate the outliers. Cherrypicking of transactions would not work here since the majority of the transactions must be placed as comparables before the audit committee.

What if the transaction is priced at the other extreme of the range, in our example above, say, at a price of Rs. 661. Because the transaction is that of a sale, selling at more than moderate prices is in the interest of the entity. . Yet, the RPT would not be at arm’s length. The Report of the Expert Group on Transfer Pricing Guidelines provides the rationale:

‘It must be emphasised that even a transfer price more favourable to the company than an arm’s length price is problematic. This is so because

(a) valuation is impacted by the possibility that the related party may demand an arm’s length price in the future and

(b) the threat to charge an arm’s length price in future could become a form of poison-pill/blackmail.’

Typically, once a price is determined to be arm’s length, it is arm’s length for either party to the bargain. Arm’s length is all about equilibrium, and equilibrium perfectly balances the interests of either party. The other way of saying this is that what is not arm’s length from the counterparty’s perspective should not usually be arm’s length from the perspective of the other party.

The Indian Judiciary on selection of comparables

The Indian Courts scrutinise comparables used to determine the ALP with a fine tooth comb. In the case of CIT v. Mentor Graphics (Noida) Pvt. Ltd., the ITATnoted how selecting comparables with wide differences in operating margins is faulty. On appeal, the Delhi High Court held that where the profit level indicator of just one comparable out of a set is lower than the tax assessee, the transaction cannot be at arm’s length.

The Global View

The OECD Transfer Pricing Guidelines[Para A.7.3] discourage considering extreme comparables and require the rationale for picking such transactions to be examined. The reason might be a defect in comparability or exceptional conditions being met by an otherwise comparable third party; not dissimilar to engineering favourable transactions with non RP.

The USA’s Electronic Code of Federal Regulations provides that to increase the reliability of comparables, an interquartile range from 25th to 75th percentile of a set of comparables must be used[4]. See Ukraine as well. The Codefurther provides that arbitrary selection of a comparable that corresponds to an extreme point in the range is unlikely to be at arm’s length.

Several other countries consider a range of comparables to determine ALP instead of a single comparable which may fall on the extreme end of a range of comparables. See Norway, Switzerland, Bulgaria.

Other aspects of arm’s length RPTs

Price is, but only, an element in the determination of arm’s length criteria for a transaction. The arm’s length assessment, in fact, is based on all the applicable terms of a transaction, as is customarily offered to an unrelated party, vis-a-vis its comparison with a related party.

An illustrative list of checkpoints for assessing arm’s length for various categories of transactions follow:

Nature of transaction

Relevant factors for assessment

Examples for discussion

Granting of loans

Credit profile of the borrower, Interest rate/basis of arriving at interest rate, Tenure, Security and security cover, Penal charges, Other covenants, Cost of funds to the lender company, End use of loan,Outstanding exposures,

Power Bank Ltd. gives loan to A Pvt. Ltd. a company in which its director holds control without any prepayment charges and to other borrowers with similar profiles with heavy prepayment charges. This failure to levy prepayment charges indicates that the transaction may not be at arm’s length.

Providing guarantee in favour of RP

Credit worthiness, Past defaults by the debtor,Obligations undertaken pursuant to guarantee agreement,Margin involved

Nofin Ltd. (a NBFC) has a policy of not providing guarantee on behalf of persons with any default in repayment in the past 3 years. However, it provides a guarantee on behalf of its related party which has defaulted twice in the past 3 years. This indicates that the transaction may not be at arm’s length.

Availing borrowings

Cost of borrowing Security covenantsPre payment charges

A Ltd. (RP) lends to B Ltd. on the condition of a security cover of 50% as against requirement of 1.25 X for other borrowers. The security cover is grossly lacking; hence, even if the lending/ borrowing rate is arm’s length, the terms of security are not.

Sale of goods

Pricing, Credit terms including advance receipts, Other covenants, Alternative options available

A Ltd. provides a credit period of 4 months to all its customers, except its RPs, where the period extends to over a year. Not only this, past records show that the RP has not paid for earlier sales, and new sales are made without interruption. his unusual credit period indicates that the transaction is not at arms’ length, even though at the same price..

Purchase of goods

Pricing, Credit terms including advance payments, Other covenants, Alternative options available

A Ltd. does not pay in advance for purchase of any goods other than those purchased from its RP. This unusual advance payment indicates that the transaction is not at arms’ length even though at the same price.

Lease/ sub-lease of premises

Rent charged (including terms for period increment), Security deposit, Tenure; lock-in period, exit rightsApportionment of common maintenance charges

Y Ltd. has provided a part of its premises on rent to X Ltd. (a subsidiary) without security deposit as against the market practice of 3 months’ deposit. While the rental may be in line with the market, the absence of security deposit indicates that the transaction may not be at arm’s length.

How about unique transactions which do not have comparables?

Companies usually pick transactions with non RPs to establish arm’s length of RPTs. But as it so often occurs in group structures, how can arm’s length be established where the transaction is carried out exclusively with the RP? Sharing of premises, software, payment of brand usage fees are all transactions that do not have market comparables; the sole reason for carrying out such transactions is the counterparty being a RP.

Arm’s length terms in case of unique transactions is not a problem that does not have a solution. In fact, even in case of unrelated parties, there are often transactions which are tailored, specific or unique in nature. The assessment of fairness of pricing and terms of the transaction gets into several factors:

Burden and benefit analysis: What is the sacrifice, burden or cost incurred by either party to the transaction, and what is the benefit obtained by either. The idea is to at least equate the benefit with the burden. Consider, for example, the use of brand name or flagship name. The basis for charging a licensing fee is that the user entity gets the advantage of the reputation, brand value or goodwill associated with the flagship name or brand. Instead of a complete greenfield start, it gets the backing of an established name. Hence, the analysis will be: what is the profitability, revenue potential, borrowing cost or other outgo of the entity using the name, as compared to other similar starters which do not have the benefit of the name.

Cost split: In case of sharing of resources, the possible solution may be to split the costs on the basis of a relevant parameter. The relevant parameter will differ on the basis of the expense: for example, in case of using office space, it may be the headcount. In the case of IT resources, it may be transactional volume. Cost allocation techniques may be used here. Is it important to charge a mark-up on the costs? In our view, no, because neither party is doing resource sharing with a view to mark profits.

Benchmarking studies: If there are instances of similar or nearly similar transactions, it may be useful to benchmark the transaction against industry similars. The availability of data may be a challenge; but sometimes, even an anecdotal evidence may be useful. This is precisely how one would have got an assurance of fair pricing: for example, if you are engaging a consultant for a complex, one-off project, you would get comfort that you are not being over-charged by asking a few peers.

The simple rule is: if the RPT is originated, negotiated, priced and finalised using the same rigour, discipline, independence of approach and process as would have been deployed in case of any other transaction, we are doing what the law/regulations expect. On the contrary, if it is the relationship which is playing on the transaction, we clearly have an issue.

Conclusion

RPT controls have become an all-time favourite subject of the regulators. The recent surge in actions against the use of abusive RPT structures makes it evident that the relevance of RPT controls is expected to only increase ahead. With arms’ length considerations forming an integral part of RPT controls, moving from cherrypicking comparables to presenting appropriate comparables at the median of the range has become all the more important.

[1] Sec. 92C of the Income Tax Act, 1961 read with rule 10B of the Income Tax Rules, 1962 corresponding to section 165

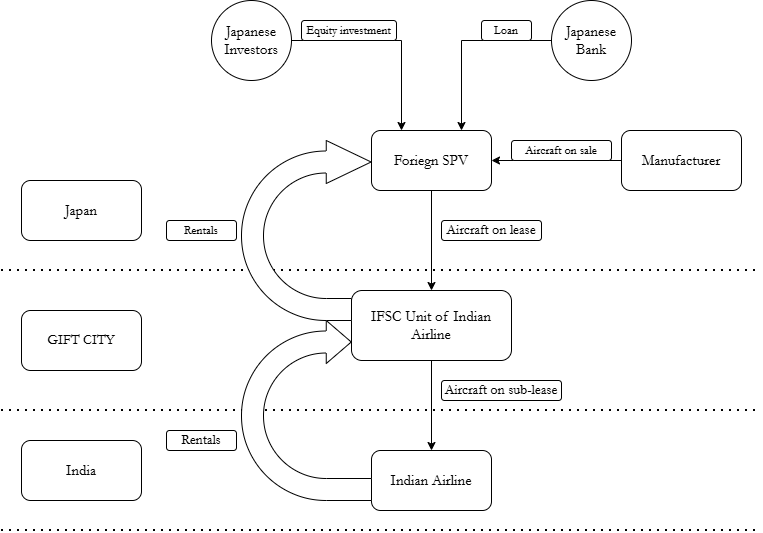

IndiGo has reportedly entered into a transaction to lease two aircraft through a Japanese Operating Lease with Call Option (JOLCO) structure, marking the first instance of an Indian airline accessing Japanese equity-backed aircraft financing. The structure involves Japanese investors and banks funding the acquisition of the aircraft through a leasing special purpose vehicle (SPV), which then leases the aircraft to the airline through a GIFT City based entity. This development comes barely a month after India notified the Protection of Interests in Aircraft Objects Rules, 2026, in January 2026 under an Act having the same name. The statute was itself notified in April 2025. Separately, India had made amendments to insolvency laws to fall in line with the Cape Town Convention [see MCA Notification dated 03.10.2023]. Notably, India had signed the Convention in the year 2008.

The Cape Town Convention is all about creditor protection by providing clear and swift remedies to secure their interests in high value mobile equipment such as aircrafts. These legislations gave domestic legal effect to Cape Town Convention and its Aircraft Protocol Rules (discussed below). Aircraft lessors globally value their ability to repossess an aircraft if the airline in a domestic jurisdiction has suffered an insolvency event. The legal certainty of lessor’s rights is a major factor in international leasing transactions. This legal certainty, though already vindicated in rulings such as Kingfisher1 could have been a major factor in consummation of this deal.

In this write-up, we briefly examine the JOLCO structure, the rationale for structuring the arrangement as an operating lease to enable depreciation benefits for the lessor and the importance of the Cape Town Convention in facilitating such cross-border aircraft leasing transactions.

Introduction

Leasing is one of the most common ways of financing acquisition of aircraft by the global aviation sector. The share of leased aircraft has increased significantly over time, rising from around 10% of the global fleet in the 1970s to nearly 58% by the end of 2023. Against this global average, India exhibits an even higher reliance on leasing, with approximately 80% of its commercial aircraft fleet being leased.

India’s aviation sector has witnessed rapid growth in recent years. The country has emerged as one of the fastest-growing aviation markets in the world, recording around 241 million air passengers in 2024, making it the fifth-largest aviation market globally. Not only has air travel become a very commonly used mode of travel in a prosperous country, the Country has also enabled major infrastructural facilities by adding new airports, expanding existing ones, etc. The number of operational airports in India has increased from 74 in 2014 to about 163 by 2025.

Thus, leasing plays a dominant role in India’s aviation sector, with the majority of airline fleets being leased rather than owned. Historically, this market has been heavily reliant on overseas leasing hubs such as Ireland, with aircraft acquisitions commonly financed through structures such as export credit supported Loan Covered Risk Amount (LCRA) financing. Recognising this dependence, the Government of India launched Project RAFTAAR under the Ministry of Civil Aviation to develop an aircraft leasing ecosystem at GIFT City, with a working group of industry experts that included Mr. Vinod Kothari, which gave various proposals aimed at promoting aircraft leasing from India. (The report can be read here). The green shoots from this strategic initiative have now clearly started growing and blooming, with the number of registered aircraft lessors in IFSC growing to 33, which has leased 242 aviation assets including 90 aircrafts and 67 engines as on March 2025.

The JOLCO structure

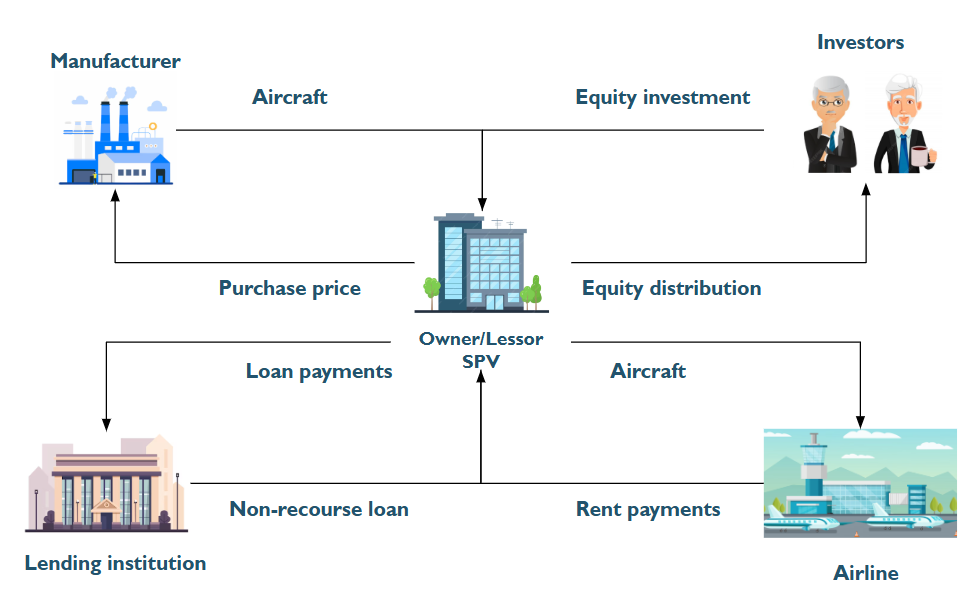

A JOLCO transaction involves Japanese equity investors (institutions, HNIs etc.) and banks financing the acquisition of an aircraft through a SPV. The investors invest in the SPV through a Tokumei Kumiai structure which essentially grants a tax-pass through to the SPV, allowing the investors to claim income/losses of the SPV and depreciation on the SPV assets. The SPV uses the equity and bank debt to purchase the aircraft from the manufacturer and subsequently leases the aircraft to the airline (in the present case to the GIFT City WOS of the airline which will then sub-lease it to the airline) under a long-term operating lease arrangement with tenure of 8-10 years.

The airline pays periodic lease rentals to the SPV (in present case to GIFT City WOS which then in turn pays to the SPV) [see Fig 2 below], which are applied towards servicing the bank debt and providing returns to the equity investors. The structure includes a call option in favour of the airline, allowing it to purchase the aircraft at a pre-agreed price at the end of the lease term. The main advantage of this structure for the lessor-investors is the tax relief availed by them under Japanese tax laws (discussed below) and for the lessee, the reduced lease rentals as compared to other models.

While the structure includes a call option in favour of the airline, this does not necessarily convert the lease into a finance lease. The call option is not a bargain purchase option, but is exercisable at a pre-agreed price that reflects the expected fair value of the aircraft at the end of the lease term. Since ownership does not automatically transfer and the option price is not nominal, the residual value risk/asset based risk remains with the lessor during the lease term. Accordingly, the arrangement continues to be characterised as an operating lease, allowing the lessor to retain tax ownership and claim depreciation under Japanese tax laws. Another reason for incorporating a call option is that the investors typically have no operational capability or commercial intent to take delivery of the aircraft at the end of the lease term. Since the aircraft is owned purely as a financial investment, the investors generally prefer that the airline either extend the lease or exercise the purchase option. The call option therefore provides a practical exit mechanism for the investors at the end of the lease period. The other conditions of the lease agreement, such as redelivery, are also designed so as to ensure that the call-option is exercised.

Rationale for selecting it as operating lease

JOLCO is an operating lease, which means the lessor SPV retains the risks and rewards of the asset. This retention is critical from a tax perspective, as it enables the Japanese investors to claim depreciation on the aircraft under Japanese tax rules. Japanese tax rules permit a declining balance depreciation method that front-loads expense recognition. For aircraft assets, the rates enable up to 20% depreciation2 annually which means that in the initial years the investors can claim a substantial amount of depreciation. This is contrasted with the typical tenure of the lease period which is around 10 years. For instance, if an aircraft costing USD 100 million allows depreciation deductions of USD 40 million over the initial 3 years, the rentals during the corresponding period will be much lesser, leaving the difference as a tax shelter. This depreciation expense, net of the lease rentals, will be offsetted against the investors’ taxable domestic income in Japan, generating tax benefits that form a significant component of the investors’ overall return. Since part of the return in JOLCO is derived from these tax claims, the investors are able to accept relatively lower lease rentals, reducing the effective financing cost for the airline. Interest payments on the loan are also tax deductible for the investors.

Fig 1: Structure of a JOLCO deal

A finance lease structure would not achieve the same outcome, as it transfers the risks and rewards of ownership to the lessee and may be characterised as a financing arrangement rather than a true lease. In such cases, the economic ownership of the asset may be regarded as residing with the user of the asset i.e. the airline, which could disallow the ability of the lessor investors to claim depreciation on the aircraft.

Role of GIFT CITY

In the present JOLCO deal, the aircraft is expected to be leased by the Japanese SPV to the airline’s IFSC-based wholly owned subsidiary at GIFT City, which will then sub-lease it to the airline. Routing the transaction through GIFT City instead of a direct transaction between the Indian airline and foreign lessor ensures no tax leakage. The same is explained below:

If the aircraft were leased directly by the Japanese SPV to IndiGo, the lease rentals would be characterised as ‘royalty’ for the use of industrial equipment under Section 9(1)(vi) of the Income Tax Act, 1961. Since the payer is an Indian resident and the aircraft is used in India, such royalty is deemed to accrue or arise in India, triggering withholding tax of 10% under Section 195;

The insertion of an IFSC leasing entity at GIFT City helps mitigate this tax friction through provisions introduced specifically to develop India as an aircraft leasing hub:

First, when the Indian airline pays lease rentals to the IFSC leasing entity, those payments do not attract withholding tax where the IFSC unit is availing the tax holiday under Section 80LA;

Second, royalty income received by a non-resident lessor from the IFSC unit engaged in aircraft leasing is exempt from tax in India [see section 10(4F)]. As a result, lease rentals paid by the IFSC entity to the Japanese SPV would not be taxable in India;

Third, the IFSC also provides capital gains relief for transfer of aircraft leased by IFSC units, enabling tax-efficient exit of the asset at the end of the lease cycle. In addition, the Government of Gujarat has waived stamp duty on aircraft leasing and financing transactions executed in IFSC, reducing transaction costs at the state level.

For cross-border aircraft leasing transactions, lenders and lessors place much weightage on their ability to repossess the aircraft in the event of airline default. Financers require legal certainty that their ownership or security interests can be quickly enforced if payments stop. The Cape Town Convention on International Interests in Mobile Equipment establishes a uniform framework for registering and enforcing such interests including mechanisms such as time-bound possession. The importance of such protections became evident during the Go Air Insolvency where aircraft lessors faced significant difficulty repossessing aircraft due to the moratorium under the IBC (See our article on Go Air insolvency and Cape Town Convention here).

In April 2025, India enacted the Protection of Interests in Aircraft Objects Act, 2025 and notified its rules in January 2026, giving domestic legal effect to the Cape Town Convention and its Aircraft Protocol Rules. The legislation is intended to align India’s aviation financing framework with global standards and facilitate quicker repossession and enforcement of lessor rights, improving investor confidence in leasing transactions involving Indian airlines. Upon a combined reading of the 2023 notification and the Protection of Interests in Aircraft Objects Act, 2025, the moratorium under Section 14 of the IBC will not prevent enforcement of rights in respect of aircraft objects covered under the Cape Town framework. Consequently, upon default by the lessee, creditors and lessors may exercise the remedies available under Articles 8 to 10 of the Cape Town Convention, including repossession, deregistration and export of the aircraft. This was important specially since the NCLAT ruling of Go Air3 upheld the moratorium on Go Air, which left international lessors in a limbo.

DVB Aviation Finance Asia PTE Ltd. v. Directorate General of Civil Aviation, WP (C) 7661/2012 ↩︎

Tegwan, 2025, Indian Journal of Law and Legal Research – ISSN: 2582-8878 ↩︎

SMBC Aviation Capital Ltd. v. Interim Resolution Professional of Go Airlines (India) Ltd., (2023 SCC OnLine NCLAT 230) ↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-12 16:20:432026-03-12 16:26:15Japanese Capital Takes Flight in Indian Skies: India’s First JOLCO Leasing Deal

The RBI on March 10, 2026 introduced the Reserve Bank of India (Commercial Banks – Prudential Norms on Capital Adequacy) Third Amendment Directions, 2026 (“Amendment”). The Amendment mainly aims to:

Clarify how banks should calculate Counterparty Credit Risk (CCR) for derivative and similar transactions.

Align Indian capital adequacy rules with international standards (like Basel III Framework).

Ensure banks maintain adequate capital for risks arising from derivative exposures.

The notable items included in the Amendment are as follows:

CCR must be calculated on a consolidated basis

A commercial bank needs to comply with the capital adequacy ratio requirements at two levels – the standalone (solo) level and the consolidated (group) level. For capital adequacy at consolidated level, all banking and other financial subsidiaries except the subsidiaries engaged in insurance and any non-financial activities (both regulated and unregulated) need to be fully consolidated. The Amendment provides that for computation of capital requirement on a consolidated basis, a bank shall consider the CCR exposures of all such entities.

Add-on Factors for Derivative Contracts

The amendment substantially replaces the table (Table 16) containing the add-on factors used to calculate potential future exposure for derivative contracts.

Banks must apply “add-on factors” based on the nature of the contract and the remaining maturity. The revised table is as follows:

Clarification on Resetting Contracts

The Amendment notes that if a derivative contract settles exposure periodically and gets reset to zero value after such settlement then banks should treat the remaining maturity as the time until the next reset date, not the full life of the contract. This remaining maturity (“residual maturity”) should be used to pick the Add-on Factor. For interest rate contracts, however, which have residual maturities of more than one year and meet the aforementioned reset criteria, the add-on factor shall be subject to a floor of 0.50 per cent. The Amendment provides for a lower floor for interest rate contracts compared to that specified previously (1.0 per cent).

Capital Requirement for Clearing Members

The Amendment notes that if a bank is a clearing member of an exchange or clearing corporation it must calculate and maintain CCR capital charge, as per the extant norms, for equity and commodity derivatives cleared for clients.

Clarification of Commodity Categories

The Amendment clarifies what is included under the terms Precious Metals and Other Commodities in Table 16.

Precious Metals

Other Commodities

– Silver – Platinum – Palladium

– Energy contracts – Agricultural commodities – Base metals (e.g., aluminium, copper, zinc)

Risk Weight for Exposure to Clearing Houses

If a bank trades through a Qualifying Central Counterparty (QCCP), the exposure should get a 2% risk weight. This applies when the bank:

Trades for itself, or

Clears trades for clients and is liable for client losses if the QCCP defaults.

However, no capital is required if:

The bank has no legal obligation to compensate the client, and

The bank has a written legal opinion confirming this position.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-11 18:47:032026-03-11 18:47:04Treatment of Counterparty Credit Risk - RBI Revises Directions for Banks

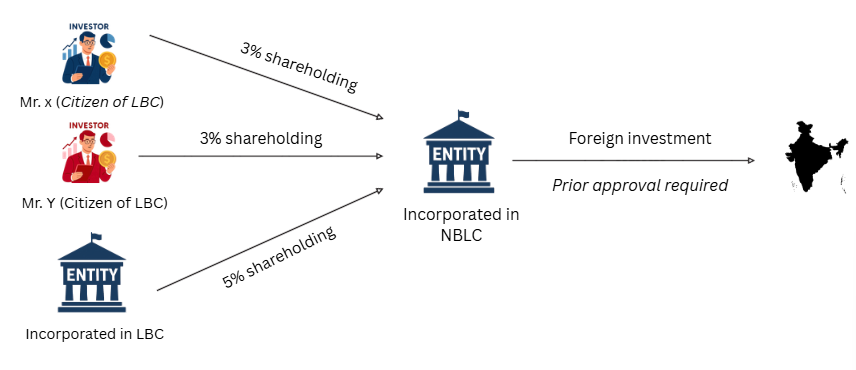

A 15th March 2026 Press Note from Department for Promotion of Industry and Internal Trade (DPIIT) implements the cabinet decision to align investments from land-border countries (LBCs) with “beneficial owner” definition of PMLA. Accordingly, where investments come from a non-LBC, where beneficial ownership traces back to LBC, either to a citizen of LBC or an entity set up there, the investments will be allowed only in approval mode. In our view, even if there are multiple such citizens or entities, the amendment requires an aggregation of the investments of all LBC citizens or entities.

The 15th March DPIIT Press note 2 (‘PN2’) was preceded by a decision of Central Government, on March 10, 2026 (‘CG press release’) relaxing the restrictions placed in 2020 on FDI from countries sharing land-border with India (LBC) by (a) prescribing a strict approval timeline of 60 days in case of specified sectors/activities of manufacturing in capital goods, electronic capital goods, electronic components etc and (b) by allowing certain investments under automatic route where the investors have non-controlling LBC Beneficial Ownership of up to 10%. The objective is to facilitate ease of doing business and attract FDI inflows especially in critical sectors.

Effective date of amendment

DPIIT issued Press Note 2 of 2026 dated March 15, 2026 (PN2) amending the Consolidated FDI Policy with respect to eligible investors (Para 3.1.1). PN2 shall take effect from the date of notification of amendment in NDI Rules. A corresponding amendment in Rule 6 of the FEMA (Non-Debt Instruments) Rules, 2019 (‘NDI Rules’) was notified and published in gazette on May 2, 2026. Accordingly, the amendment takes effect from May 2, 2026.

Background

Since April 2020, in terms of rule 6 of NDI Rules and FDI Policy, prior approval of the government is required for any investment made by an entity from LBC or where the beneficial owner of an investment into India (a) – is situated in LBC; or (b) is a citizen of such LBC. Likewise, any transfer of ownership of existing or future FDI that results in the beneficial ownership of the investment shifting to a person who is a citizen of, or situated in, a LBC also requires prior government approval.

These requirements were notified pursuant to Press Note No 3 dated April 17, 2020 and subsequent notification of FEMA (Non Debt Instruments) Amendment Rules, 2020. Refer to our earlier write-up titled India seals its borders to corporate acquisitions dealing with the said press note. Our earlier you-tube video covering the overview of FDI can be accessed here.

In order to meet the objectives of Aatmanirbhar Bharat and increase FDI inflows, India has decided to revisit the restrictions placed during Covid pandemic to curb opportunistic takeovers/acquisitions by Chinese companies. In this article we discuss the changes approved and notified by way of PN2 and amendments made in NDI Rules effective May 2, 2026.

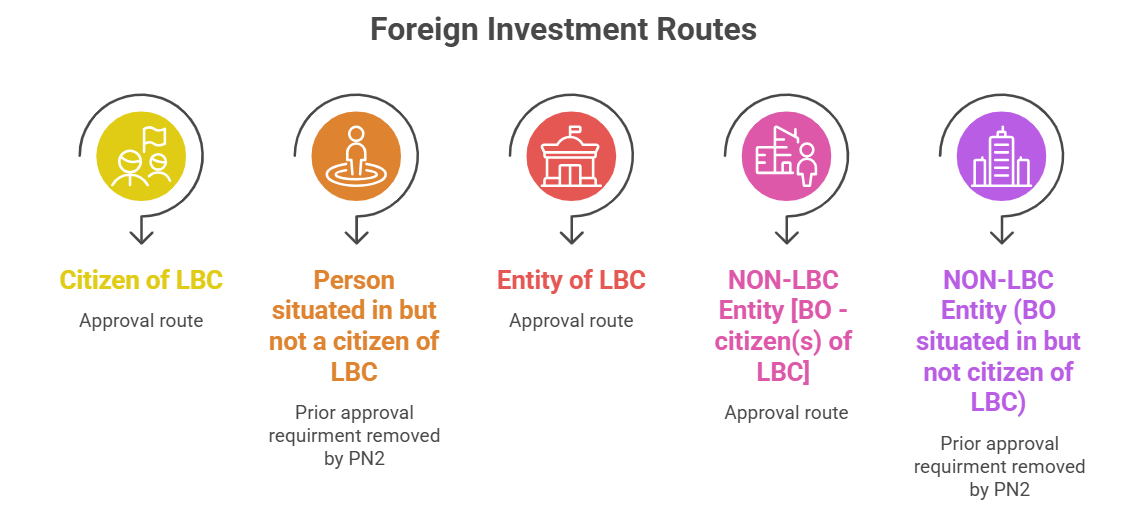

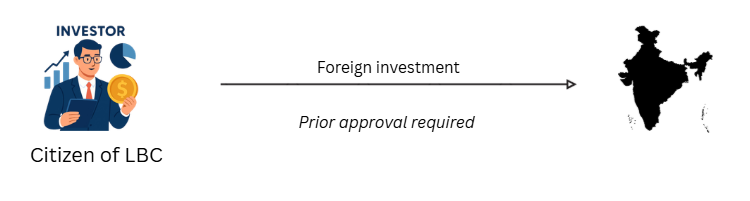

Investments received from LBC

Prior approval of the government is now required for any investment made by an entity or citizen from LBC. The approval requirement also extends to investments made in India where the beneficial owner of an investment into India is a citizen of LBC.

The restriction arising on account of being ‘situated in LBC’ has been deleted. This relaxes the requirement for individuals of different nationalities situated in LBC investing in India or receiving ESOPs from Indian companies, as they will no longer require government approval.

Accordingly, the amended position is as under:

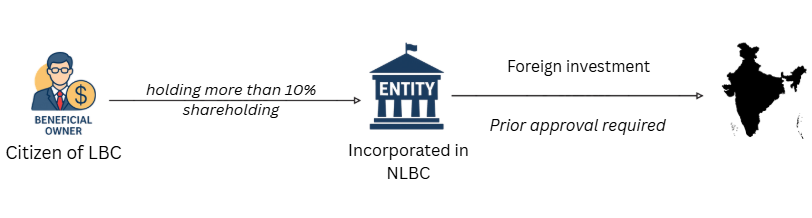

Investments received from non – LBC with BO of investments based in LBC

Prior approval of the government is now required for any investment by PROI from non-LBC, where the beneficial owner of an investment into India is a citizen/entity of LBC.

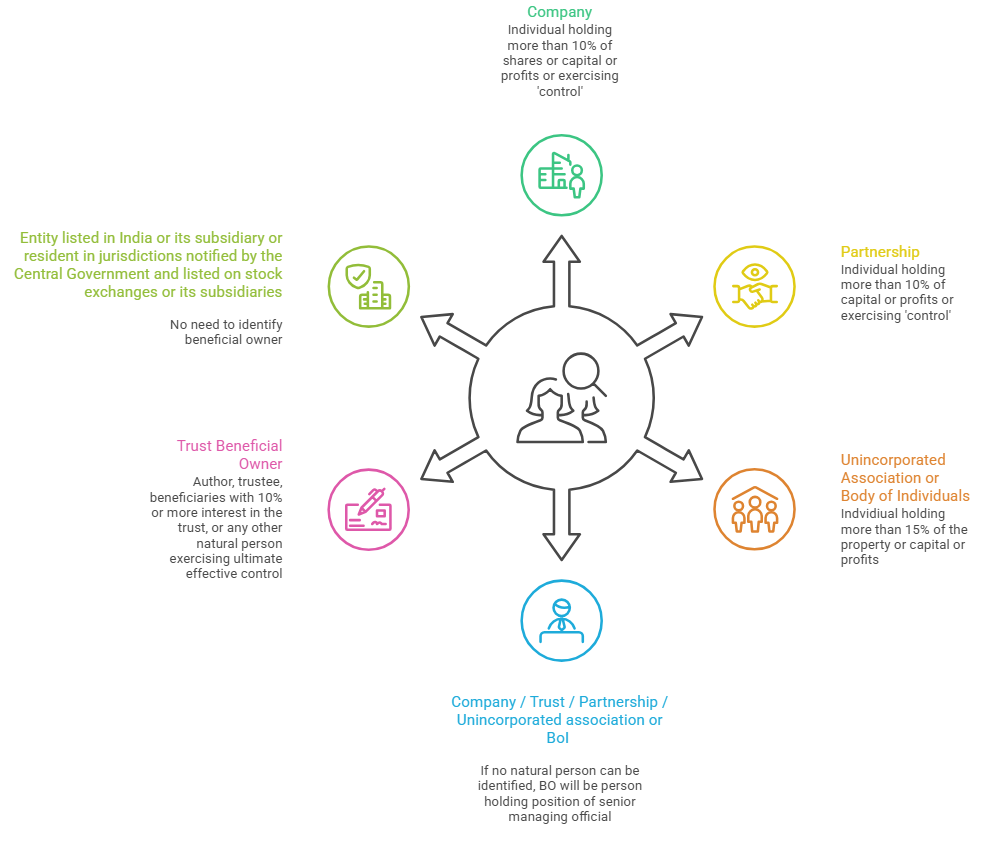

Meaning of ‘beneficial owner of an investment into India’:

Let us first understand the meaning of “investor entity”.

It means the beneficial owner(s) of the investor entity incorporated or registered in a country other than LBC. Manner of identifying the beneficial owner(s) of the investor entity will be as discussed below in Clause 4.

Applicability in case of transfer of ownership

Prior approval is required for any direct or indirect transfer of ownership of existing or future FDI in an Indian entity that results in the beneficial ownership of the investment into India shifting to an entity or a citizen of LBC.

Scope of ‘beneficial owner’ (BO)

As per PN 2 and NDI Rules, the manner of identifying BO is aligned with Section 2(1)(fa) of the Prevention of Money-laundering Act, 2002 read with Rule 9 (3) of Prevention of Money Laundering (Maintenance of Records) Rules, 2005 (PML Rules). The reference to PML rules is mainly for the thresholds (refer below).

BO will be construed as vested with the LBC if the citizen(s) of LBC or entity (ies) incorporated/ registered with LBC has/ have the ability to hold rights/ entitlements in excess of thresholds under PML rules or exercise control over the investor entity or ultimate control over the investee i.e the Indian entity in any manner:

directly or indirectly,

individually or cumulatively,

independently or collectively,

whether acting together or otherwise.

Whether holdings by different citizens or entities of LBC to be aggregated?

In our view, yes. The intent is to allow investments from entities where the investors from LBC hold a non-controlling interest. Therefore, one will have to consider all investments put together. The approval requirements have been further clarified by way of following illustrations:

Illustration 1

Illustration 2

Illustration 3

Illustration 4

One might argue that if neither of the persons referred above i.e. Mr. X or Mr. Y or Entity incorporated in LBC, are qualifying as ‘beneficial owners’ under PMLA Rules on a standalone basis, then why do we need to aggregate their shareholding?

Here, reference needs to be made to the language of the proviso to Para 3.1.1.(c) of the FDI Policy and Explanation 2 to NDI Rules, which requires considering the rights/entitlements held – directly or indirectly, individually or cumulatively, independently or collectively, whether acting together or otherwise. The language seems to indicate that aggregation needs to be done irrespective of whether the person in question is acting independently or collectively or whether they are acting together or otherwise. Hence, in our view, one has to consider if investors of the Non-LBC with BO from LBC cumulatively hold in excess of the prescribed thresholds.

Ambit of ‘beneficial owner’under PMLA

Investments with non-controlling stake permitted under Automatic route

As per Para 3.1.1(d) of the amended FDI Policy, investments from an investor entity having any direct or indirect ownership by a citizen or an entity of LBC not requiring prior government approval shall be subject to reporting requirements as per the SOP laid down by DPIIT and prescribed by RBI.

Investments by Multilateral Bank or Fund of which India is a member

The amended proviso to Rule 6 (a) of the NDI Rules clarifies that any Multilateral Bank (like World Bank, Asian Development Bank, Asian Infrastructure Investment Bank, New Development Bank etc.) or Fund (like International Monetary Fund, International Fund for Agricultural Development etc) of which India is a member shall not be treated as an entity of a particular country, nor any country would be treated as beneficial owner of any investments made by such Bank/Fund in India. This was not provided in PN2 and clarified vide amendment in NDI Rules.

Other proposals approved in the CG press release pending notification

Fixed 60 days timeline for government approval for critical sectors

Presently, the timeline for obtaining government approval for FDI ranges between 12–14 weeks.

In cases where the investee entities are engaged in the specified sectors / activities concerning manufacturing of Capital goods, Electronic capital goods, Electronic components, Polysilicon and ingot-wafer etc. a timeline of 60 days shall be adhered to for government approval, in view of the criticality. The list will be provided by DPIIT. The majority shareholding and control of such Investee entities should be with the residents.

The Government will continue to assess the proposals on a case to case basis and accord approval. Recently, an electronics manufacturer company received MEITY approval for receiving investment of 26% in a joint venture from a Chinese investor.

Way forward

As discussed in the CG press release, the existing restrictions to cases where LBC investors only have non-strategic, non-controlling interests were seen as adversely affecting investment flows from investors including global funds such as PE/ VC funds. By loosening the said restrictions cautiously, greater FDI inflows and speedier fundraising can be encouraged, particularly into startups and deep techs while protecting the nation’s security interests. The relaxed norms aim to increase access to technology, facilitate ease of doing business for Indian entities and strengthen India’s position as an attractive destination for investment and manufacturing.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-11 18:00:302026-05-04 13:01:13Open but Guarded Gates: Relaxations for Border-Country Investments

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-11 16:00:442026-03-11 16:25:01Navigation Roadmap through New Consolidated RBI Directions – Presentation for NBFCs

Over time, RBI has received multiple representations from NBFCs seeking a review of the provisions and clarity on certain aspects for the computation of Owned Funds and Tier I capital. In response, RBI has reviewed the relevant directions and guidelines and has now proposed a set of clarifications and revisions aimed at aligning capital computation with the latest available financial position.

RBI had issued Draft Amendment Directions vide its press release dated January 13, 2026, on ‘Clarification on Owned Fund / Tier 1 Capital computation for NBFCs / ARCs and applicability to “Credit / Investment Concentration” Norms’ proposing amendments to various relevant Master Directions. The said proposals have now been notified by the Reserve Bank of India through its press release dated March 10, 2026.

Tier 1 is the core component of an NBFC’s regulatory capital. The same is arrived at by deducting exposure taken in group companies and other NBFCs (to the extent the same exceeds 10% of the owned funds) from the owned funds. NBFCs are required to maintain 15% of their risk-weighted assets as capital, in the form of Tier 1 and Tier 2, on an ongoing basis. In addition to maintaining the capital adequacy, Tier 1 capital also serves as an important benchmark to compute the maximum exposure an NBFC can take in a single borrower/group of borrowers.

Analysis of the proposed changes

Owned Fund forms a key component of regulatory capital and includes free reserves, which, in simple terms, represent accumulated profits retained by an NBFC and available for unrestricted use. By including adjusted quarterly profits in the Owned Fund, NBFCs will be allowed to factor in profits earned during the current financial year without having to wait for completion of the year-end audit.

However, crucial points that comes to light on the reading of the above mentioned amendments are:

Inclusion of quarterly profits has been specifically included in the computation of owned funds for the purpose of determining the capital adequacy.

Tier 1 capital for the purpose of concentration risk management is to be seen from the last available financial statements (audited or subject to limited review). Here, the definition of Tier 1 capital has to be referred from the capital adequacy directions; further, the same shall be based on the latest audited financial statements.

Accordingly, based on the above, it can be said that while determining Tier 1 capital for calculating the maximum exposure an NBFC can take, both adjusted quarterly profits as well as any capital raised during the year will be considered. However, for the purpose of capital adequacy, only adjusted quarterly profits have been included. There is no clarity being provided for the inclusion of capital raised during the quarter for capital adequacy computation. This creates a distinction between the two provisions with respect to the computation of Tier 1 capital. There is therefore a requirement to provide further clarity on the same since there seems to be no proper rationale for such divergence.

It is also pertinent to note that the amendments are introduced in the definition of owned funds and thus affects the Tier 1 capital of an NBFC. However, the minimum net owned funds (NOF) that NBFCs are required to maintain is governed by section 45-IA(7)(i) of the RBI Act, 1934. These amendments therefore do not have any impact on the NOF computation.

Further, an additional procedural requirement has been introduced for recognising capital augmentation while computing exposure limits. Specifically, the amended definition of Tier 1 capital provides that,

“2) Paragraph 4 (8) shall be replaced by:

“Tier 1 capital” shall have the same meaning as given in Chapter II of the Reserve Bank of India (Non-Banking Financial Companies – Prudential Norms on Capital Adequacy) Directions, 2025. However, for the purpose of concentration norms, the NBFC shall obtain an external auditor’s certificate on completion of the augmentation of capital and submit the same to the Department of Supervision of the RBI before reckoning the additions to capital funds.”

This clarification further reinforces the distinction noted earlier in the draft amendments. Accordingly, even though an NBFC may raise fresh capital during the year (for instance, through issuance of shares or infusion of additional equity), such capital cannot immediately be used for expanding exposure limits under the concentration norms. Before counting the increased capital, the NBFC must:

Complete the capital augmentation process (actually receive the funds).

Obtain a certificate from its external auditor confirming that the capital increase has been completed.

Submit that certificate to the RBI’s Department of Supervision.

Only after abiding by this process can the NBFC include the additional capital in Tier 1 capital for calculating concentration limits.

Earlier, as per the RBI Circular dated April 19, 2022, RBI permitted the inclusion of current-year profits in CET 1 capital, which was applicable only to NBFCs classified in the Upper Layer. Thus, other NBFCs were not specifically allowed to consider such quarterly profits as a part of their owned funds.

The inclusion of quarterly profits as a part of the owned funds and consequently in Tier 1 capital is subject to certain conditions (adjusted quarterly profits):

The quarterly financial statements are subjected to limited review by the statutory auditors, and

The profits included are reduced by the average dividend paid during the preceding three financial years.

Further, any losses incurred during the year should also be fully reduced from the owned funds.

Illustration:

In a simple illustration, an NBFC-ML earns a profit of ₹ 4 crores up to Q3 of FY 25-26. Let’s assume the average dividend paid during the last three years is ₹3 crore per annum.

Position under the Existing Norms:

Only audited, year-end profits could be considered as a component of the Owned Fund for capital computation. Thus ₹4 crore profits earned during the current year (up to December 2025) could not be included in free reserves and consequently under Owned Funds.

Proposed amendment:

Under the draft amendment, adjusted quarterly profits are permitted to be included in free reserves and Owned Fund, computed as per the below formula:

EPt = NPt – 0.25 *D*tWhere:EPt = Eligible profit up to quarter ‘t’ of the current financial year, t varies from 1 to 4NPt = Net profit up to quarter ‘t’D = average dividend paid during the last three years

In our example,

NPt = ₹4 crores (profit up to Q3)

D = ₹3 crore (average dividend of last three years)

t = 3 (up to December)

EP = 4−(0.25×3×3) = 1.75

Hence, ₹1.75 crore can be taken as an eligible profit for capital computation.

Amendments to Tier I Capital for credit/investment concentration norms

“The applicable Tier 1 Capital for compliance with the norms stated in paragraphs 13 and 14 above, shall be determined based on the NBFC’s latest available financial statements (audited or subject to limited review).”

“Tier 1 Capital shall be as defined in paragraph 10 of the RBI (NBFC – Prudential Norms on Capital Adequacy) Directions, 2025.”

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-11 14:17:002026-03-11 14:21:17RBI clarifications on computation of Tier 1 capital