This article discusses the key changes in the regulatory requirements for the payment of dividends by banks.

Adjusted PAT: A risk-adjusted base for dividend distribution

Dividend has to be paid as a percentage of adjusted PAT. Adjusted PAT is the PAT of the financial year for which the dividend is proposed to be paid minus 50% of Net NPA as on March 31 of the financial year for which the dividend is to be paid. By linking dividend payouts with asset quality, the framework ensures that banks with higher stressed assets retain a larger portion of earnings rather than distributing them as dividends.

Maximum Permissible Dividend Payable

Under the earlier directions, whether a bank could declarate dividend or not depended, inter-alia, on a matrix combining CRAR and NNPA ratios and the maximum dividend payout ratio was capped at 40% of net profit, depending on capital adequacy and asset quality.

The Dividend Directions replace the earlier CRAR-NNPA based matrix with a CET1 capital ratio bucket framework. Under the new system, banks fall within the various ranges of CET1 capital buckets (10 in total), each prescribing the maximum percentage of dividend that may be declared out of Adjusted PAT. At the same time, the overall dividend distribution is capped at 75% of PAT.

An illustration of the computation of the maximum permissible dividend payable is shown below:

(₹ in crores)

Total Assets

500000

PAT

3000

Net NPA (NPA – Prov)

500

Adjusted PAT (PAT – 50%* NNPA)

2,750

CET 1 Capital (end of PY)

12%

Dividend allowed (new directions) [max of (30%*Adj. PAT) or (75% of PAT)]

825

Dividend allowed (erstwhile directions) (35%*PAT)

1050

Ineligible Profits for the payment of dividends

The Directions identify 4 kinds of profits that cannot be used for payment of dividends or remittance of profits:

Extra-ordinary or exceptional profits: banks cannot distribute one-time or abnormal profits. The definition of exceptional profits has to be taken from the applicable accounting standards. Banks will therefore have to ascertain the items which lead to extraordinary profits and exclude them while declaring dividends. Any profits from activities or transactions that are not in the ordinary course of business will therefore have to be excluded.

Overstatement of PAT flagged by auditor: If the audit report contains a modified opinion indicating overstatement of PAT, the overstated portion cannot be used for dividend payments.

Unrealised gains on level 3 financial instruments: RBI (Commercial Banks – Classification, Valuation and Operation of Investment Portfolio) Directions, 2025 provides that dividends cannot be paid out of net unrealised gains recognised in the Profit and Loss Account arising on fair valuation of Level 3 investments on its Balance Sheet. The same has now been specified under the Dividend Directions as well.

Reversal of excess provisions or unrealised gains from transfer of loans/ SRs guaranteed by GoI: In terms of the RBI (Commercial Banks – Transfer and Distribution of Credit Risk) Directions, 2025, the non cash component of the excess provision remaining with the bank at the time of transfer (Excess provision minus cash received as consideration for transfer) cannot be used for the payment of dividend. Further, with respect to the SRs guaranteed by the GOI, it has been provided that any unrealised gain recognised in the Profit and Loss Account on account of fair valuation of such SR investments shall be deducted from CET 1 capital, and no dividends can be paid out of such unrealised gains.

Changes in Eligibility Criteria

The earlier directions required banks to maintain CRAR of at least 9% for the preceding two financial years and the relevant financial year, along with an NNPA ratio below 7%, and permitted dividends only out of current year profits.

The revised framework removes the NNPA threshold and historical CRAR requirements and instead adopts a simple prudential condition, ie., Banks must be in compliance with regulatory capital requirements and must continue to remain compliant even after the proposed dividend payment. In addition, the bank must have a positive Adjusted PAT for the relevant financial year in which the dividend has to be paid.

Other Relevant Changes

Board Oversight

The Dividend Directions require the Board to evaluate certain factors before approving the declaration of dividend. In particular, the Board must consider RBI supervisory findings relating to divergence in asset classification and NPA provisioning, the statutory auditor’s report including any modified opinion or emphasis of matter, the bank’s current and projected capital position vis-à-vis regulatory capital requirements and the bank’s long-term growth plans.

Definition of Dividend

Dividend has been clarified to mean to include interim dividend as well. Further, it shall consider dividend payable on equity shares and excludes dividend on Perpetual Non-Cumulative Preference Shares (PNCPS). Dividend payable on compulsorily convertible preference shares will, however, be included.

Reporting Mechanism

A bank paying dividend or remitting profits to the head office will be required to report details as per the format prescribed under Annex II of the Dividend Directions. The report is required to be furnished to the DoS within a fortnight of declaration of dividend / remitting profits to head office. Earlier, such a report was required to be furnished to the DoR.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-11 13:32:162026-03-11 14:22:54Profit, Prudence and Payouts: New RBI Regulation for Dividends by Banks

An August 2025 Informal Guidance by SEBI for Welspun Corp Limited sought to clarify the applicability of contra trade on release of pledge. However, it goes on to say that: “…in case of creation of pledge/ revocation, the beneficial ownership does not change till pledge is invoked”. While the IG was specific to revocation of pledge, this seems to be creating a confusion on the contra trade restrictions on creation of pledge. In this article, we discuss the nature of pledge as a trade, and applicability of trading related restrictions on various stages of pledge. Also see a detailed article on treatment of various stages of pledge as trading under PIT Regulations.

Is pledge a trade?

Answer is yes

Trading means dealing in securities in any form [Reg 2(1)(l) of PIT Regulations]

Explanation to the definition expressly includes “pledging”

Creation of pledge may be considered equivalent to disposal/ intent to dispose the shares

Is release of pledge a trade?

Technically, a release (or so-called revocation) of a pledge is also a trade. However, given there is no change in beneficial ownership, there is no concern, at least from a contra trade perspective

There is no actual acquisition or intent to acquire shares, it is mere restoring back the position as it was prior to the creation of pledge

The shares are coming back to the person who was the beneficial owner of such shares previously.

Is invocation of pledge a trade?

No, since invocation of pledge is not at the discretion of the holder of shares

Invocation results in actual disposal of shares, however, related compliances w.r.t. such shares are undertaken at the stage of creation of pledge itself

Examples to understand contra-trade on pledge

Any opposite trade within 6 months of a prior trade attracts violation of contra-trade, except in case of specific waiver for a bona fide purpose. We discuss various combinations of trades within a span of 6 months to understand whether such trades attract contra-trade restrictions.

Transaction 1

Transaction 2

Is it contra-trade?

Can a waiver be granted by CO?

Purchase of shares (Buy)

Creation of pledge (Sell)

Yes, opposite trades within 6 months

Yes, if the DP is able to demonstrate the urgency and bona fide nature of such transaction

Creation of pledge (Sell)

Purchase of shares (Buy)

Yes, opposite trades within 6 months

In such a case, it is very difficult to prove bona fide of the subsequent trades of purchase of shares after creation of pledge.

Creation of pledge (Sell)

Release of pledge

No, since the release of pledge does not result in an opposite trade per se, it is incidental to the primary trade of pledge creation and only restores back the position as it was prior to creation of pledge.

NA

Release of pledge

Creation of pledge with another person (Sell)

No

Yes, if the DP is able to demonstrate the urgency and bona fide nature of the underlying transaction for which the pledge is to be created

Purchase of shares (Buy)

Invocation of pledge (Sell)

No, since the invocation of pledge is not at the discretion of the shareholder. The relevant act of disposal of shares is taken into account as a “trade” upon creation of pledge itself, and hence, not considered as “trade” again, upon such invocation.

NA

Invocation of pledge (Sell)

Purchase of shares (Buy)

NA

What is a bonafide purpose in the case of a pledge?

How does the Compliance officer verify/ensure that the purpose of the pledge is bonafide?

There cannot be any sure or one-size-fits-all response to this. Pledge is not for its own sake; pledge for an underlying transaction, which may be margin trading facility, borrowing, etc. The Compliance Officer should see whether that underlying transaction is within the regular business or activity of the pledgor. Whether the pledge is limited to the shares of the listed entity or has other securities? Whether the pledgee is an entity which is engaged in providing similar facilities to several unrelated entities? Whether the timing of the pledge is not indicating the advantage of a price spurt, etc.

Compliances applicable to various stages of pledge

The applicability of contra trade restrictions on the various stages of pledge are tabulated hereunder:

Stage of pledge

Nature of trade (Acquisition/ Disposal)

Pre-clearance required?

TWC applicable?

Contra-trade restrictions applicable?

Remarks

Creation of pledge

Disposal

Yes

No, if the trade is bona fide

Yes

While creation of pledge amounts to trade, exemptions from TWC and contra trade may be availed if the trade is for bona fide purpose.

Release of pledge

Acquisition

No

No

No

No change in beneficial ownership, and no actual acquisition/ disposal – mere restoration of the position prior to creation of pledge

Notice of invocation of pledge

NA

NA

NA

NA

No dealing in securities, mere notice specifying intent

Invocation of pledge

Disposal, however, continuation of the prior action of creation of pledge

No

NA

No

Invocation of pledge is done by the pledgee upon default. Once a pledge is created, the pledgor has no control over the invocation of such pledge upon default. Further, since creation of pledge is itself considered as ‘disposal’, the same shares cannot be considered to have been ‘disposed’ again, upon invocation.

Sale of pledged securities

Disposal, however, continuation of the prior action of creation of pledge

No (however, intimation to CO post sale, if not covered by System Driven Disclosure)

NA

No

Sale of pledged securities is done by the pledgee, and is not under the control of the pledgor. Further, since creation of pledge is itself considered as ‘disposal’, the same shares cannot be considered to have been ‘disposed’ again, upon sale.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-09 18:32:312026-03-12 09:49:20Span of Welspun: Is pledge/unpledge a trade under PIT?

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-07 18:39:272026-03-12 10:38:38IBBI proposes strengthening the CoC’s oversight and procedural clarity in CIRP

The recent press reports highlighting the RBI’s focus or nudge towards NBFCs regarding their lending practices, particularly those that raise concerns about evergreening of loans, demand a comprehensive analysis.

Extending further credit to a borrower already facing financial distress can be similar to the cautionary tale of an archer trying to locate a lost first arrow by shooting a second in the same spot, only to lose both. Similarly, if lenders take additional exposure on distressed borrowers, there is a risk of compounding existing defaults into a larger and unmanageable crisis.

Real estate developers often raise funds by offering flats under buy-back or assured return schemes, sometimes with a mandatory repurchase clause, or sometimes at the builder’s discretion. On the other hand, there may be people who genuinely want to acquire a home and live in it. In the former case, when the builder fails to repay the money or allot the flats, can such a lender don the garb of a homebuyer?

In the ruling of Mansi Brar Fernandes v. Shubha Sharma and Anr, the Supreme Court held that such investors lured by assured profits cannot be permitted to trigger CIRP as real estate allottees. Permitting such investors to invoke the insolvency process would undermine revival, destabilise projects, and prejudice genuine homebuyers. It was further held that investors seeking assured returns are essentially acting as speculative investors rather than genuine homebuyers; allowing them to initiate CIRP as allottees could enable recovery actions disguised as insolvency proceedings, thereby disrupting project completion and harming bona fide homebuyers.

But are such investors altogether debarred from seeking any remedy under the IBC against the builder? Will they not be considered as financial creditors in the capacity of depositors?

This article explores the positions of homebuyers with different commercial intentions under IBC and analyses whether real estate investors under buyback or assured return schemes may invoke CIRP against builders in the capacity of depositors.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-03-07 13:14:422026-03-07 18:42:05Homebuyers under BuyBack Scheme: Financial Creditors under IBC?

The new Bihar MFI Bill appears to have triggered first reactions, which, looking at stock prices of some of the players, are quite adverse. However, for regulated entities, it is important to chart out the next steps based on concrete and reasonably forecastable compliance obligations (given that it is still a Bill), rather than first impressions.

Given that Bihar has a deep penetration of microfinance (an estimated 16% of the nation’s share), and relative to other states, the income level of the rural population is low, as is that of financial literacy, the concerns of the State Govt seem to have been rooted in the increasing level of the bottom-of-the-pyramid indebtedness.

I. At a glance – some applicability for NBFCs and Banks

Avowed intent of the bill: The Bihar Micro Finance Institutions (Regulations of Money Lending and Prevention of Coercive Actions) Bill, 2026 (“Bihar MFI Bill” / “Bill”) was passed by the assembly on 26th February 2026, with an explicit intention to “prohibit coercive and unethical recovery practices, ensure transparent lending operations with fair interest rates, protect vulnerable borrowers from exploitation through comprehensive safeguards, and establish effective mechanisms for dispute resolution and borrower relief while maintaining a balanced regulatory framework that promotes financial inclusion”

Applicability on banks and NBFCs: While section 2(2) does appear to carve out an exception for regulated entities, it has been explicitly clarified under Section 2(3) of the Bill, that the provisions pertaining to “prohibition of coercive recovery practices”, “borrower protection measures”, and “fair recovery practices” shall apply to regulated entities such as Banks and NBFCs as well – insofar as they “engage in recovery of loans from borrowers within the State of Bihar”. Hence, the Bill contains provisions and compliances for Banks and NBFCs engaged in lending and loan recovery in the State of Bihar, no matter where the entity is registered or headquartered. Penalties for non-compliance are captured under Chapter VI of the Bill, and include imprisonment of up to three years, punishment under Section 108 of the Bharatiya Nyaya Sanhita (abetment of suicide), fines upto Rs five lakhs, etc. Directors’ and officers to be liable unless proved diligent: While attributing a corporate offence to a director/officer are quite common (usuallyprovided that the directors did not have a mere supervisory role, and acted in a way that directly connects their conduct to company’s liability, see herefor more), the Bill brings a specific provision [under Section 19] which goes to escalate the apparent responsibility for an offence under the Bill to “every director, partner, manager, or officer who was in charge of and responsible for the conduct of business at the time of violation”. Therefore, the only escape for the accused will be to prove that the person was clean, by evidencing that the offence occurred without such director/partner/manager/officer’s knowledge, and crucially, that they exercised the “due diligence” to prevent such a violation.

Hence, while commentators have duly observed that only the provisions pertaining to coercive recovery practices and the like are applicable to regulated entities (such as NBFCs), what must also be noted is the additional penalties by way of fines and imprisonment, introduced for a breach of the same.

How should one exercise this “due diligence” in a manner consistent with the RBI obligations? In the author’s view, creating an audit trail through the routine gap-assessments, ensuring Policy safeguards, ensuring that the recovery agents sign the code of conduct and are briefed on the same, etc, would be one such method.

II. Economic and social relevance of the Bill

Bihar’s portfolio: The changes, though applicable to a particular state, assume importance at a macro-level, because per data from September 2025, Bihar’s outstanding MFI portfolio stood at approximately 45,000 crores, and accounted for 16% of the nation’s market share (refer Equifax Report here) [1]. Hence, it has been stated to be the largest state in terms of NBFC-MFI’s AUM share (refer Care Edge Ratings Report here)[2]. Interestingly, the state’s population relative to the nation’s is an estimate of 9% (relying on census projections)[3], and the state contributes approximately 3% of the Nation’s GDP.

Impact of the Bill on NPAs, loan recoveries, and book-size: Some of the requirements under the Bill are consistent with the extant RBI regulations, whereas others impose more onerous standards, such as with respect to loan recovery practices, hours of contacting the borrower, lender-cap for the borrower, approaching the borrower at the workplace, etc. In the author’s view, such measures proposed to be implemented via the Bill, especially where ambiguous, may likely stall recoveries further, increase operational costs for lenders, and might balloon NPAs in the state (resulting also in higher provisioning for the Banks and NBFCs). It may also further lead to the shrinkage of loan books and present more difficulties for MFIs conducting business in the region to meet their qualifying asset criteria (as has emerged in recent times).

Microfinance is one business where, as proved empirically in many cases, if new lending shrinks, recoveries shrink much higher. Therefore, if the Bill results in slackening the growth of microfinance, it may result in a sharp drop in collection efficiency.

Recoveries may further be stalled by frivolous complaints launched by unscrupulous borrowers, under the provisions of the Bill, in order to evade recovery (refer Complaint Mechanism under Section 10).

Much ado about MFI lending: State money lending laws, which have existed ever since pre-Independence time, may have been enacted in a social setup where usury was a prominent mode of exploitation. However, over time, the RBI’s market conduct controls, including stipulations on fair lending practices, are at least intended to hold the market in good shape. In this situation, the attempts by some states to regulate what is already regulated by the RBI may appear to be an overdose. Readers may read our comprehensive comments on the recent Tamil Nadu Act, here, and the Karnataka Ordinance (which was subsequently approved as an Act), here. See also our analysis of state money lending laws here.

If the objective of the Act was to impose tighter standards on recovery practices and coercive practices, it is already well known in regulatory circles that the RBI has released the draft Responsible Business Conduct Amendment directions, applicable to various classes of regulated lenders, which deal with nuanced aspects pertaining to borrower’s privacy, how to approach them for recovery in the workplace, training of the recovery agents, etc.

Further, there is a mandate that all NBFC MFIs shall become members of at least one SRO recognized by RBI, and adhere to the guidelines thereof (see Para 46 of the 2025 NBFC-MFI Directions). These SRO guidelines/guardrails (from MFIN and Sa-Dhan, for instance), in addition to RBI regulation, which prescribe FOIR cap, recovery practices, loan disclosure obligations, and fair practices, also deal with issues such as evergreening, lender-cap, overindebtedness cap, etc. Hence, prudentially speaking, the utilitarian purpose sought to be achieved by such an Act (insofar as it is made applicable to regulated entities) remains to be understood.

III. Measures proposed via the Bill applicable to Banks and NBFCs

Below are the measures and compliances proposed to be introduced via the Bill, especially for Banks and NBFCs, lending in Bihar, and a note on whether or not they are envisaged to be pain points, viz-a-viz, the existing compliance obligations under RBI regulations.

Lenders conducting business in the region would be well advised to take note and ensure proactively that compliance audit and Policy measures are in place so their directors and KMPs may demonstrate that the “due diligence” required under Section 19 of the Bill has been conducted.

Kindly note: We have provided our readers with a snapshot of the same, extracting the most salient provisions. For a granular reading, the text of the Bill may need to be referred to.

Heading

Salient Details

Pain points and other views

Section 2(3) – Applicability to banks and NBFCs

Provisions which pertain to (i) prohibition of coercive recovery methods, (ii) borrower protection measures, and (iii) fair recovery practices shall apply to REs as well insofar as they are involved in the recovery of loans from the State of Bihar.

Section (5) – Transparency and disclosure obligations

The effective rate of interest should be prominently displayed in officers, brochures, website, and advertisements Shall not recover from the borrower towards interest in respect of any loans, an amount in excess of the principal amount. Cashbook and ledger to be maintained Loan application form to contain all information needed to make an informed decision and for meaningful comparison between offerings of other lenders Lenders to provide borrowers with a passbook or digital loan statement showing details and break-up of the loan, repayment schedule, and inform borrowers about the outstanding principal and interest amount after each loan repayment No lender shall charge any amount, fee, or penalty not explicitly captured in the pre-loan disclosure statement signed by the borrower A toll-free helpline to be established for grievance redressal available during all business hours and working days There are also additional disclosure requirements on “registered lenders” (i.e, lenders who have obtained registration under the Act) – but there is some opacity currently on whether or not it shall apply to RBI-regulated entities.

Given that provisions pertaining to display of interest rates, disclosure requirements, contents to be captured in loan application, fees and charges, and maintaining a helpline (akin to GRM) are already applicable to regulated lenders under RBI guidelines, we do not envisage they will be pain points. The requirement to not recover amounts in excess of the principal amount merely means that the interest charged on such facility must not exceed the principal. However, additional transparency norms, such as providing a specific notice on outstanding principal and interest amount after each loan repayment, would need to be adopted (which at present, are only applicable for floating ROI personal loans, under Para 31(6) of the Responsible Business Conduct Directions, for instance).

Section 5 – Submission of returns

Monthly returns: MFIs would need to submit monthly returns before the 10th of every month, providing a list of borrowers, the value of the loan amount, and the interest charged therein. Annual returns: MFIs would need to submit annual returns for the FY ending 31st March every year, to the registering authority, before the month of May of the next FY.

We do not envisage this being a pain point, as lenders shall already have mechanisms to track RBI reporting obligations

Multiple lending & over-borrowing

A borrower must not be a member of more than one self-help group or joint liability group Not more than two Micro Finance Institutions shall lend to the same borrower “There shall be a minimum period of moratorium between the grant of the loan and the due date of the repayment of the first installment. The moratorium shall not be less than the frequency of repayment. For Example:In the case of weekly repayment, the moratorium shall not be less than one week.” Recovery of loans made in violation of the recovery norms to be deferred till all existing loans are fully prepaidAll sanctioning and disbursal of loans to be done only at a central location

Some norms prescribed here, such as that not more than two MFIs shall lend to the same borrower (evergreening / over-indebtedness check), are even more stringent than those prescribed by the SROs under their guardrails (MFIN guardrails, for instance, caps it at 3 lenders).

Section 7 – Prohibition of coercive recovery practices

Lenders, their agents, employees, contractors, and representatives shall not engage, threaten, facilitate, or encourage: Physical coercion, violence, or intimidation Psychological harassment or mental torture – which includes notably: (i) calling the borrower before 7 AM or after 8:00 PM on weekdays, or anytime at all on Sundays and holidays without express written consent; and (ii) creating a public disturbance at the workplace of the borrower Digital harassment: Which includes disclosing or publishing personal information, financial information, or private data without express written consent Economic coercion – which includes notably: Interfering with the borrower’s workplace attendance, employment, or business operations, contacting employers/colleagues/business associates to “jeopardize” professional relationships, and compelling disposal of property under “duress”. Social pressure and community harassment – which includes notably: Pressuring the family members, friends, or neighbours to create social coercion for repayment Illegal and unethical recovery practices – which include notably: Attempting recovery from guarantors without following proper legal procedures

Recovery agents: Because this also applies to agents, contractors, and representatives (and hence would cover recovery agents) – in our view, the code of conduct to be signed by recovery agents would need to be drafted more granularly (refer to Responsible Business Conduct Directions). Weekdays and holidays: A more onerous standard than RBI regulations is introduced, whereby lenders are not to contact borrowers during the weekends or holidays. However, one will likely be unable to contact the borrowers in person for recovery during weekdays, either since they would be in their workplaces, and the same may be construed as an attempt to jeopardize workplace relationships, or creating a “public disturbance” at the workplace. Hence, recoveries will most likely be stalled if Borrowers cannot be contacted on Sundays or holidays without explicit consent.

IV. Question of Jurisdiction

Jurisdictional questions: In the author’s view, the aspect of whether or not such state money lending laws can apply to regulated lenders such as Banks and NBFCs appears to be settled in previous judgments of the Honourable Supreme Court. The Court had ruled on this in Nedumpilli Finance Company Ltd. v. State of Kerala (in the context of NBFCs, but on a principles basis applicable across other REs mutatis mutandis) that because the RBI Act and control over NBFCs are traceable to entries under List I of the 7th Schedule of the Constitution, Article 246(1) of the Constitution would come into play. This grants parliament exclusive law-making power over said entries. Further, Section 45Q of the RBI Act provides an overriding effect to Chapter III of the RBI Act (dealing with NBFCs), and regulations made thereunder (which are recognized to be of a statutory nature), over other laws.

As has been clarified in the above judgment, the RBI already regulates lenders like NBFCs from “cradle to grave”. As observed by the Hon’ble Supreme Court, unlike state enactments, which have a one-eyed approach of borrower protection, the RBI Act takes a holistic approach to lending business. And, “all activities of NBFCs automatically come under the scanner of the RBI. As a consequence, the single aspect of taking care of the interest of the borrowers, which is sought to be achieved by the State enactments, gets subsumed in the provisions of Chapter IIIB”

V. Next Steps

The Bill would be awaiting the Governor’s assent. Some prudential next steps (for regulated lenders), should the Bill be enacted, are:

Gap assessments: Given that there is a requirement for the directors and KMPs of the REs to have exercised due diligence in order to insulate from liability – in the author’s view – the routine internal compliance audits and gap assessments would also need to cover aspects under the Bill to create a demonstrable audit trail of periodic “due diligence”.

Income Assessment: Should be ensured that at the time of extending digital loans to borrowers in Bihar, as a part of the “economic profile assessment”, the (household) income details are clearly captured to determine which borrowers (based on household income criteria + secured/unsecured nature of loan) come under MFI category, and which do not – and an audit trail for the same should be maintained. This is to ensure that routine digital loans offered in Bihar do not inadvertently trigger compliance (and subsequently, penalties) under the Bill.

Calls and messages: Should be ensured that calls and messages are spaced out in a manner that they are not construed to be causing “mental distress” or “disrupting daily life”. Hence, ideally, the intervals of recovery calls may be consented to by the borrower and agreed upon at the time of the loan application.

Policy & Code of Conduct: The code of conduct and Policy for engagement of recovery agents would need to be made more granular and include the aspects under Section 7 of the Bill.

Consent notices: Contacting a borrower on a holiday or Sunday for recovery is not permitted without express written consent. Such consent may be taken at the time of the loan application itself.

‘Mahattva Series: Episode 2 | Microfinance: State of the Industry and Way Forward’ – For an insightful session, with participation from the heads of two of India’s most prominent MFIs, and moderated by Mr. Kothari: https://www.youtube.com/live/C0vTpo9wjVw?si=poHF8Pct-IadHcmD

Under the National Monetisation Pipeline (NMP) 2.0, released on February 23, 2026 NITI Aayog has proposed securitisation of ₹45,500 crore of future cash flows in the power sector as part of the overall ₹16.72 lakh crore monetisation target for 5 year period FY 2026-FY 2030.

The NMP was introduced in 2021, which provided a framework to unlock value from brownfield and greenfield public-sector assets and reinvest these resources into new infrastructure creation. NMP 1.0 achieved 90% of its ₹6 Lakh Crores monetisation target in the 4 year period FY 2021 – FY 2025. Now, NMP 2.0 seeks to carry forward this vision with a higher target and greater reserve of assets.

NMP 2.0 seeks to use a wide range of monetisation modes for raising finance, including InvITs, PPP user models, disinvestment, IPOs, FPOs, Leasing, private placement of securities, securitisation etc.

Securitisation as a mode of monetisation

Securitisation is being envisaged for the power sector since the sector has predictable and stable revenue streams ideal for securitisation. Further, securitisation would be suitable for operational PSU assets that do not require developmental or major operational support. The identified asset classes and targets are:

Operational hydro power stations of NHPC and SJVN – ₹12,000 crore;

Power Guarantee Corporation of India Limited (PGCIL) transmission assets – ₹33,500 Crores;

Under NMP 2.0, for securitisation to be counted as monetisation, transactions must comply with certain guidelines, including the following:

No charge on the PSU’s balance sheet;

No corporate guarantee;

Repayment backed solely by securitised cash flows;

Escrow mechanism for cash flow ring-fencing;

Proceeds earmarked for capex or debt reduction;

First charge on cash flows to lenders, with residual cash flows retained by the PSU.

The securitisation proceeds will be retained by the respective PSUs and deployed towards capital expenditure and capacity addition.

Mechanics and Regulatory Considerations

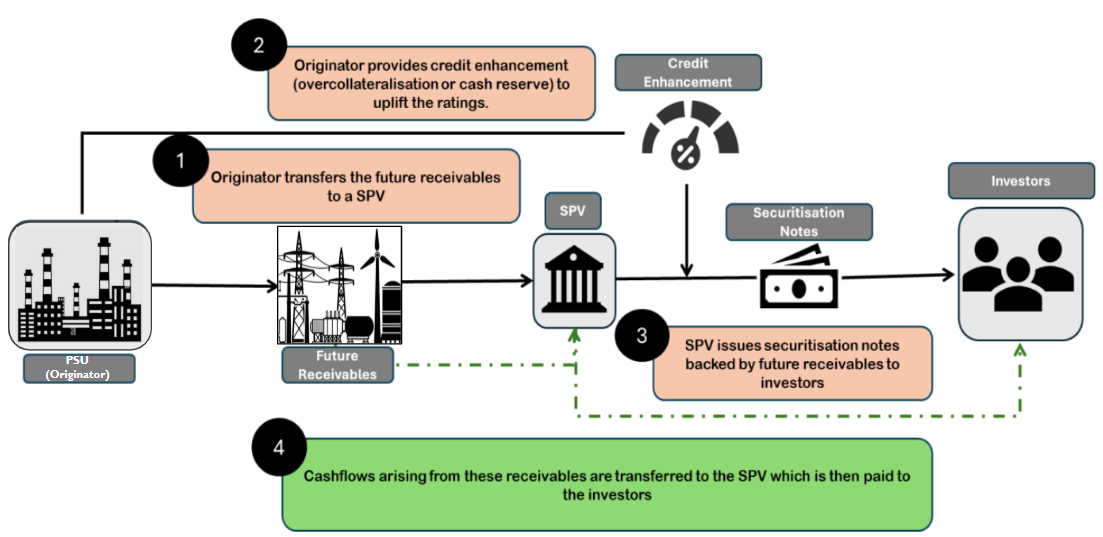

Securitisation under NMP 2.0 would essentially be a future flows securitisation; a topic we dealt with in our white paper. Under this, future cash flows are converted into tradable securities and the issuers can raise upfront capital from the issuance of these securities, effectively monetising their future income. The process generally involves the following steps:

Identification of Future Receivables: The originator (which would be the PSU in the present case) identifies a pool of receivables expected to arise over time.

Transfer to SPV: The rights to these future receivables are legally assigned or pledged to a bankruptcy-remote SPV. This separation ensures that the cash flows are shielded from the originator’s insolvency risk;

Structuring and Credit Enhancement: The SPV issues securities backed by the expected future flows.

Payment of interest and principal to the investors: The investors will need to be regularly serviced by cash flows generated from the underlying receivables. On maturity, the principal payments would also be made to the investors.

If the transaction is structured as per the conditions above, it may look like the following:

Typically the credit enhancement is overcollateralisation and structural credit enhancement by issuing multiple classes of notes (i.e. class A and B notes) is usually missing. There may be a DSRA/Cash reserve too to take care of any mismatches. See our write-up on future flows here.

Regulatory framework:

Future flow securitisation in India sits at the intersection of RBI and SEBI regulations, but does not fit neatly within either. The RBI’s SSA Directions apply only to RBI-regulated lenders (banks, NBFCs, financial institutions) and presuppose the transfer of existing financial assets. Therefore, securitisations under the NMP 2.0 where non-financial sector PSUs are involved will fall outside the SSA regime.

Further, in case capital market issuance or listing is contemplated, securitisation transactions fall under the SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008.

However, post the 2025 amendments, SEBI has defined eligible “debt/receivables.” Under this definition, only specified categories (such as mortgage debt, leasing receivables, trade receivables, rental receivables, etc.) are currently permitted. Accordingly, the assets under NMP 2.0 will not fall under the definition of eligible assets as per the SEBI SDI Framework unless specifically notified by SEBI.

Further, conditions such as obligor track record requirements and minimum holding period norms designed for traditional loan securitisations may be structurally incompatible with pure future receivable structures.

It may be noted that it is essential for a securitisation transaction to fall within the purview of either RBI’s SSA Directions or the SEBI SDI Framework from the purview of taxation.

Taxation is governed by Section 115TCA of the Income Tax Act, 1961, which grants pass-through status to securitisation trusts created under the RBI SSA Directions or SEBI SDI Framework. Income received by investors is thus taxed as if they had directly earned the underlying income, ensuring single-level taxation.

Therefore, if a future flow securitisation falls outside both the RBI and SEBI frameworks, the SPV may be taxed under general trust taxation principles, potentially at the maximum marginal rate. This creates a material tax inefficiency. Accordingly, for future flow securitisation to be viable at scale, regulatory eligibility under the SEBI SDI framework and, thereby, access to Section 115TCA pass-through treatment becomes critical.

Further, it may also be noted that under the SSA Directions, for making any investment in securitisation transactions which are outside the purview of the SSA Directions, full capital will need to be maintained.

This discourages banks from making investments in securitisation transactions outside the purview of the SSA Directions.

Accordingly, for the success of NMP 2.0, the following two amendments are necessary:

Amendment in the definition of eligible assets to permit future flows

Necessary amendment in the SSA Directions to encourage bank participation in the securitisation notes issued by non-financial sector entities.

InvITs

InvITs are used to monetise mature and revenue-generating brownfield assets, primarily in the road and power transmission sector, by transferring them into a trust that raises capital from institutional and retail investors. The sponsoring PSU (eg. NHAI) receives upfront proceeds from units issued by the InvIT. See our whitepaper on infrastructure securitisation here.

Notably, the NMP 2.0 also proposes monetisation of approx ₹3,35,000 Crores worth of highway assets under the InvIT/TOT models. This would be done through NHIT or another similar publicly listed InvIT.

Three types of highway stretches are identified for this purpose, along with respective monetisation targets:

Stretches where user fee is accruing to NHAI – ₹2,31,900 Crores;

Projects at the end of their concession periods – ₹60,000 Crores; and

Under-construction stretches where user fee will accrue to NHAI – ₹43,600 Crores.

Under the NMP, the total monetisation value under InvIT mode is calculated based on the market approach, i.e. funds raised by the InvIT against the underlying asset portfolio. In the case of highways, the proceeds from TOT and InvIT projects shall flow to NHAI and shall ultimately accrue to the Consolidated Fund of India.

Conclusion

Using future flow securitisation as a means for funding infrastructure has been common worldwide. Such transactions include the securitisation of metro ticket receivables in China, where the proceeds from the securitisation of future ticket receivables were used to repay the bank loans taken by the originator for building the metro infrastructure.1

Further, in Indonesia, toll road receivables were securitised to build the Jakarta-Bogor-Ciawi toll road.2

The NMP 2.0 proposes to use securitisation for financing. However, it is essential that necessary regulatory amendments be carried out to ensure sucess of this mode of financing and for promoting many more similar future projects.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2026-02-25 18:58:502026-02-25 18:59:11Watts to Wealth: NITI Aayog’s ₹45,500 Cr Securitisation Plan for power sector

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-02-23 17:56:552026-02-23 17:59:15Representation on the draft Amendment Directions for exemption from registration to eligible NBFCs