At present, in India, there exists a framework for securitisation of standard assets only. in September, 2021 the RBI issued the ‘Master Direction – Reserve Bank of India (Securitisation of Standard Assets) Directions, 2021’ (‘SSA Directions’)[1], which deals with standard asset securitisation. Under the SSA Directions, the definition of standard assets does not include non-performing loans, i.e., only those assets with a delinquency up to 89 days, would qualify for securitisation under the SSA directions.

For assets that turn non-performing, i.e., 89+ days-past-due (‘DPD’), including those that retain the classification as the borrower has not been able to clear all his past arrears, the same can, at present, be sold under the Master Direction – Reserve Bank of India (Transfer of Loan Exposures) Directions, 2021 (‘TLE Directions’)[2], which has a framework for sale of stressed assets (which includes non-performing assets). Technically, there is a process of “securitisation” of non-performing loans (‘NPLs’), by issuing “security receipts” (‘SRs’) against the same; however, the framework for issue and investing in SRs is quite different, and is normally not captured as a part of securitisation in the industry parlance[3].

Assets sold through the TLE route require a complete arm’s length sale, without any credit support from the seller and there is typically no tranching. This results in substantial haircuts on these stressed loan pools. Further, most of the NPLs that face a problem in the current scenario are retail loans or re-performing loans (see discussion on re-performing loans later). These retail pools are not normally sold under the ARC route since ARCs lack the capability in this specific asset class and are more suited towards wholesale transactions.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2023-01-02 16:45:072023-02-17 18:56:27Full Day Workshop on Securitisation and Transfer of Loans

It has been a brisk year in terms of activity – a busy regulator kept all regulated entities busier. This year marked the initiation of a new SBR framework for NBFCs – hence there was a lot of buzz in terms of understanding the new regulatory framework. The names of 16 Upper layer entities were declared by the RBI – consisting of 5 HFCs, 10 NBFC-ICCs, one CIC[1]. As is the design, UL entities are treated at par with banks in terms of regulatory intensity –hence, there is a LEF (large exposure framework), differential provisioning norms in case of standard assets, CET-1 capital requirement, mandatory listing etc.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kotharihttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari2022-12-29 17:17:512022-12-29 17:33:372022 in retrospect: Regulatory activity in the financial sector

Loan sourcing, co-lending, transfer of loans, securitisation

Please note that registration for the workshop is closed, thank you for the overwhelming support! Do express your interests by filling this form: https://forms.gle/qoUwx99aV1acELSp6

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2022-12-09 16:52:452022-12-19 19:17:26Full Day Workshop on Partnering in lending (Mumbai)

On December 5, 2022, the RBI silently made some significant changes and updated the RBI (Securitisation of Standard Assets) Directions, 2021 (‘SSA Directions’). It is difficult to understand if these amendments are pursuant to some consultation, or feedback gathered from supervisory experience. The three significant changes seem to be mutually disconnected, though some of the amendments are related to the amendments made, on the same date, to the RBI (Transfer of Loan Exposures) Directions, 2021 (‘TLE Directions’) too.

We deal with the three amendments, and their implications, below:

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2022-12-01 17:39:002022-12-13 15:10:13Full Day Workshop on Partnering in lending:

A comprehensive treatise, running over 1000 pages, on four contemporary topics in structured finance.

Key highlights of the book: – Delves deep to create fundamental understanding of the topic, evolving conceptual clarity. – Discusses global practices, along with specific focus on Indian market. – Blend of legal, accounting and regulatory discussions, while fully explaining the underlying financial structures. – Evolution as well as temporal developments discussed, to allow readers to understand the trajectory and future path of the instruments. – Sufficient discussion on structuring. Use of spreadsheet-based examples to provide practical understanding. Spreadsheets underlying the computations can be accessed on a URL.

The table below provides the rate of stamp duty applicable on assignment of receivables in major states across India:

State

Stamp Duty

Andhra Pradesh

0.1% of the loan securitized or debt assigned with underlying securities subject to maximum limit of Rs.1 Lakh. [1]

Assam

8.25 percent.

Bihar

0.1% of the loan securitized or debt assigned with underlying securities subject to maximum limit of Rs.1 Lakh[2].

Chhattisgarh

0.1% of the loan securitized or with underlying securities subject to maximum limit of Rs.1 Lakh[3].

Delhi

one rupee for every one thousand rupees or part thereof, of the loan securitized or the debt assigned with underlying securities, subject to a maximum of Rs 1 lakh.[4]

Goa

8 percent.

Gujarat

Bombay Stamps Act, 1958 (as applicable to the state of Gujarat) , No. GHM – 98-221H.STP/1096/2527/H.1. In exercise of the powers conferred by Clause (a) of Section 9 of the Bombay Stamp Act. 1958 (Bom LX of 1958), the Government of Gujarat hereby reduces the duty with which an instrument of securitisation of Loans or the Assignment of Debt with underlying securities is chargeable under Article 20(a) of Schedule 1 to the said Act, to ten paise for every rupees 100 or part thereof of the loan securitised or debt assigned with underlying securities’ subject to a maximum of rupees 1 lakh[5].

Haryana

Approx. 12.5% for conveyance amounting to sale for immovable property and 6.25% for other conveyances.

Karnataka

Karnataka Stamp Act, 1957.The Government of Karnataka, Department of Stamps & Registration have specified that that with effect from 1st April 1999, ‘Deeds relating to assignment of receivables in the process of securitisation will be charged to a reduced duty of 0.1% subject to a maximum of Rs. One Lakh.’[6]

Madhya Pradesh

Stamp duty of 7.5% of amount of debt assigned.

Maharashtra

Bombay Stamp Act, 1958. ‘Order dated 11th May 1994, No. STP. 1094/CR-369/(C)-M-1 – In exercise of the powers conferred by Clause (a) of Section 9 of the Bombay Stamp Act, 1958 (Bom. LX of 1958), the Government of Maharashtra hereby reduces with effect from 1st April 1994 the duty with which an instrument of securitisation of Loans or Assignment of Debt with underlying securities is chargeable under Clause (a) of Article 25 of Schedule 1 to the said Act, to ‘Fifty Paise’ for every rupees 500 or part thereof of the loan securitised or debt assigned with underlying securities subject to a maximum of Rs 1 lakh and in case of instrument of Assignment of Receivables in respect of use of credit cards to ‘Two Rupees and Fifty Paise for every rupees 500 or part thereof.’ subject to a maximum of Rs 1 lakh.[7]

Manipur

7 percent.

Meghalaya

upto Rs 50,000 – 4.6%, more than Rs 50,000 and upto Rs 90,000 – 6%, more than Rs 90,000 and upto Rs 1,50,000 – 8% , More than Rs 1,50,000 – 9.9%.

Nagaland

7.5 percent.

Odisha

0.1% of the amount or value of the consideration set forth in the said instrument.[8]

Punjab

3 percent.

Rajasthan

In exercise of the powers conferred by sub-section (1) of section 9 of the Rajasthan Stamp Act, 1998 (Act No. 14 of 1999) and in supersession of this department’s Notification No. F.4(4) FD/Tax/2015-230 dated March 9, 2015, the State Government, stamp duty chargeable on the instrument of debt assignment executed in respect of performing assets (standard assets) is charged at the rate of 0.15 percent of the amount of debt subject to maximum of rupees five lacs.[9]

Tamil Nadu

In exercise of the powers conferred by clause (a) of sub-section (1) of], the governor of Tamil Nadu hereby reduces the duty chargeable under the said act to ten paise for every Rs 100or part thereof the market value of the property which is the subject matter of conveyance, subject to the maximum of Rs 1 lakh, in respect of the instruments providing for transfer of non-performing assets or assignment of debt with or without underlying securities whether movable or immovable or intangible. in favour of reconstruction companies under SARFAESI act ,2002. the notifications appended to this order will be published in an extraordinary issue of Tamil Nadu government gazette dated 4-3-2005.

The stamp duty was reduced to 5% vide notification no. 297/XXVII (9)/2011/Stamp-61/2009 dated May 31, 2011 issued by the Department of Finance, State of Uttarakhand and is currently applicable. However, the said exemption is applicable only upto the value of the property being 25 lakhs. In the event the value exceeds 25 lakhs, then upto 25 lakhs, the stamp payable will be reduced by 25% i.e. 3.75% of market value will be payable, and above 25 lakhs, the stamp duty will be paid at 5% of market value.

[1] Notification G.O.Ms. No.305 dated 29.03.2004 issued by Registration and stamps Department, Government of Andhra Pradesh. This shall apply to ARC’s.

[2] Notification S.O.No.-1/M1-126-2004/2904 dated 29.12.2004 issued by Department of Registration, Government of Bihar. This shall apply to ARC’s.

[3] Notification No./F10-9-2004-C.T.-(R) –V-(32) dated 28.02.2004 issued by Financial and Planning Department {Commercial Tax (Registration) Department}, Government of Chhattisgarh.

[8] 1. Notification No. Stamp-6/05/35723/R. dated 31.08.2005 issued by Revenue Department, Government of Orrisa. 2. Notification No. Stamp-6/05/35723/R. dated 31.08.2005 issued by Revenue Department, Government of Orrisa.

[10] Notification No.K.N.5-1023/11-2005-500(137)-2003 dated 15.03.2005 as amended by No.K.N.5-1389/11-2005-500(137)/2003 dated 29.03.2005 issued by Kar Evam Nibandhan Anubhag-5, Government of Uttar Pradesh.

[11]Notification No.2307-F.T. dated 02.07.2004 issued by Finance (Revenue) Department, Government of West Bengal.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-06-01 15:54:342022-06-01 16:12:25Stamp Duty on Assignment of Receivables

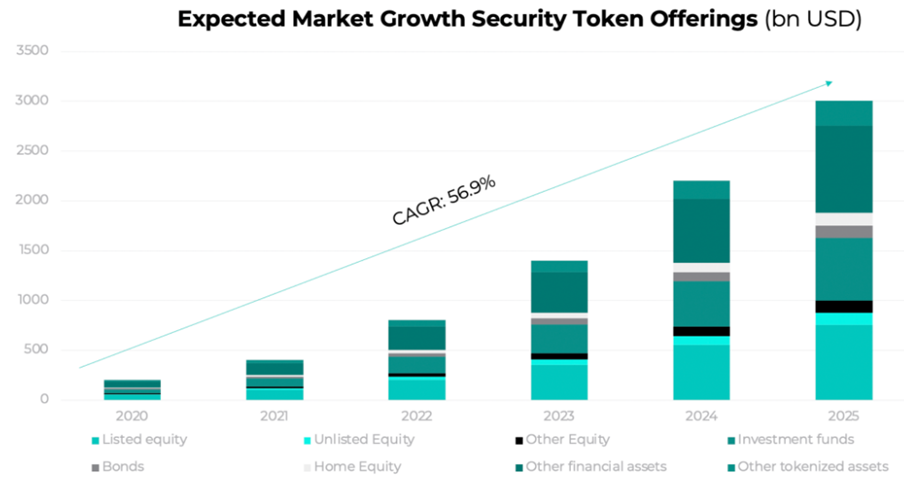

As per a Forbes article[1] published in early 2021, DeFi and Security Token Offerings (STO) had scaled new heights with 2020 being “a banner year for capital formation and secondary trading” using security tokens. DeFi applications were reported to be prevalent across 15 countries around the world (including the major developed economies) and 39 of the top 100 largest banks in the world were reportedly working on security tokens or blockchain applications. Expert estimates[2] predict the security tokens industry to surpass the market volume for cryptocurrencies in the next five years and in terms of issue proceeds, the global security token market reaching $3 billion by 2025.

Figure 1: Estimated Growth of Security Token Offerings (STO)[3]

Blockchain-based tokens can be described as digitally scarce units of value the characteristics and circulation of which are prescribed via computer code.[4]

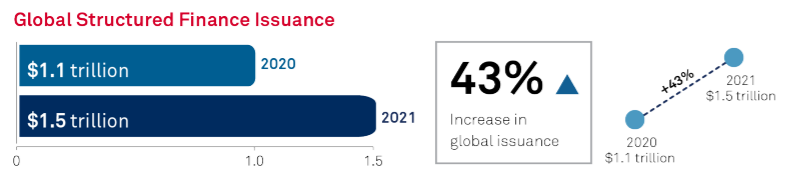

The structured finance space exhibited robust growth during 2021, as the world entered the COVID-19 endemic period. This growth was largely driven by supportive regulatory and policy initiatives aimed at overcoming the negative economic effects of the pandemic, the emergence of green finance initiatives and a general rise in economic activity.

Figure 1: Snapshot of Global Structured Finance Issuance[1]Read more →

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-03-04 15:08:512022-08-12 15:48:41Global Securitisation Markets in 2021: A Robust Year for Structured Finance