Tracking Your Material Risks – Importance of Risk Register for NBFCs

– Subhojit Shome | finserv@vinodkothari.com

Introduction

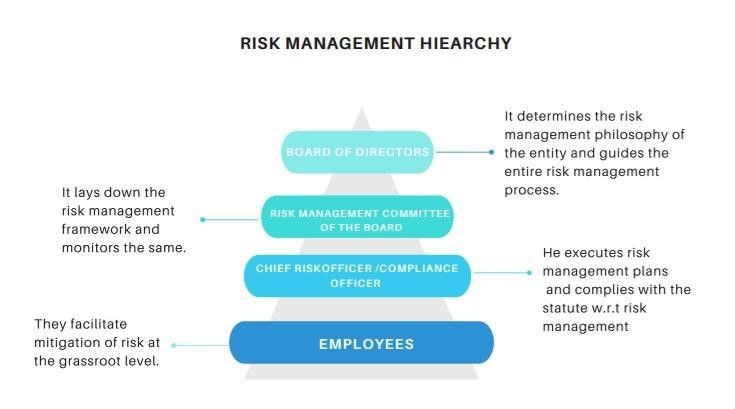

A Non-Banking Financial Company (NBFC), like other financial intermediaries, operates in a risk-intensive environment where credit, operational, technology, liquidity and regulatory exposures evolve continuously. To manage these effectively, regulators and international standard-setters increasingly expect institutions to maintain a clear, documented, and continuously updated risk inventory. This document—commonly called a risk register—forms the backbone of an NBFC’s risk management framework. Standards such as ISO 31000 emphasise that organisations must maintain structured documentation of risks, controls and monitoring processes, while the Basel Committee recognises the importance of tools that consolidate information for oversight by senior management and boards. The Reserve Bank of India (RBI), through its compliance, operational risk, outsourcing, and information technology governance guidelines, also implicitly requires NBFCs to maintain evidence of risk identification, assessment and monitoring. Together, these expectations make a risk register not just a good practice, but an essential governance artefact.

This article explains what risk registers are, outlines the material risks relevant to NBFCs, describes the contents and structure of effective risk registers, discusses the merits of consolidated versus separate registers, and demonstrates how risk registers are used in practice.

What is a Risk Register?

ISO 73:2009 Risk management—Vocabulary defines a risk register as – record of information about identified risks. A risk register is a structured record that captures an organisation’s identified risks, the causes and consequences of those risks, the controls in place to manage them, the effectiveness of those controls, and the actions planned to further mitigate them. It is not merely a compliance document but a living tool that helps decision-makers view exposures at a glance, track risk levels, and allocate resources. The concept and practice are consistent with ISO 31000’s emphasis on systematic identification, assessment and treatment of risk.

For an NBFC, which must demonstrate proactive risk management under multiple RBI frameworks—including the SBR Master Directions, the operational risk guidance note, outsourcing guidelines, digital lending rules, and IT governance expectations—the register is foundational evidence of risk awareness and accountability.

Figure 1: An illustrative Snapshot of a Risk Register

Risks for Which NBFCs Should Maintain Registers

An NBFC typically faces a wide spectrum of material risks that require structured tracking. The most prominent among these is credit risk, arising from borrower defaults and delinquencies, portfolio deterioration and concentration exposures. NBFCs must also track liquidity risks, especially given their reliance on market borrowings and investor confidence. Operational risks, defined by Basel and adopted by the RBI as losses due to failed processes, people, systems or external events, form a substantial part of an NBFC’s potential vulnerabilities—from frauds and system outages to process gaps.

With increasing digitisation, IT and cybersecurity risks have become highly material. RBI’s guidelines on information technology governance frameworks require NBFCs to implement ongoing monitoring and incident tracking mechanisms, all of which depend on clear risk documentation. Similarly, third-party and outsourcing risks, emphasised by both RBI, are significant given NBFCs’ reliance on technology partners, collection agencies, loan service providers and outsourcing arrangements. NBFCs must also account for regulatory and compliance risks, model and data risks, and conduct and reputational risks that emerge from customer interactions and business practices. Finally, strategic and ESG-related risks are gradually gaining prominence in supervisory expectations.

Components of a Risk Register

Although institutions may customise formats, an effective risk register should contain certain core elements. Each entry should describe the risk clearly, including its causes, potential business impact, and the business unit or process where it arises. It should include an inherent risk assessment (before considering controls) and a residual risk assessment (after controls). Controls must be recorded along with their owners and the results of recent effectiveness testing. The register should also assign a responsible risk owner at a senior level to ensure accountability. Key Risk Indicators (KRIs), where relevant, should be linked to the risk entry along with thresholds, recent values and escalation triggers. Finally, each risk entry should reflect remediation actions, timelines and review dates to ensure the register remains a dynamic management tool rather than static documentation.

An actionable risk register should be concise, structured, and linked to governance and reporting. Recommended fields include:

Figure 2: Contents of a Risk Register

What an Enterprise-Wide Risk Register Looks Like

An enterprise-wide risk register (EWRR) consolidates the institution’s major risks across all business lines into a single, coherent view. In practice, this register acts as the central dashboard for senior management and the Board. It includes credit, operational, cyber, market, liquidity, compliance, strategic and reputational risks, each summarised in a uniform format. The EWRR provides an aggregated view of risk severity, risk levels, and concentration areas. For example, it may highlight that operational risks linked to IT outages are trending upward, or that credit risk concentration in a specific sector has crossed internal appetite thresholds.

Importantly, the EWRR does not replace detailed sub-registers maintained by specialised teams; instead, it integrates their findings. Basel supervisory materials emphasise consolidation as essential for Board oversight, and the EWRR serves precisely that purpose.

Separate Risk Registers vs an Enterprise-Wide Register

NBFCs often question whether it is more effective to maintain a single enterprise-wide register or individual registers for each risk category. Two common approaches exist: maintaining one enterprise-wide register (single source of truth) or maintaining focused registers (e.g., Operational Risk Register, Credit Risk Register) with a roll-up to an enterprise view. Both approaches are widely accepted; choice depends on size, complexity and risk-data capabilities.

In practice, the most effective approach is hybrid. Individual registers—for credit, operational, cyber/IT, third-party risk and others—allow specialised teams to capture detailed technical information, testing results, and granular observations. These feed into the enterprise-wide register, which provides the Board and CRO with clear, aggregated insights. Maintaining only the EWRR risks leads to oversimplifying important technical details, while relying exclusively on separate registers makes it difficult to achieve the consolidated oversight that regulators and Boards expect.

The best practice is to have a centralized ownership of taxonomy and scoring methodologies for the specialised risk registers and the EWRR. This is in accordance with para 32 of the Principles for Effective Risk Data Aggregation and Risk Reporting (BCBS), which states –

A bank should establish integrated data taxonomies and architecture across the banking group, which includes information on the characteristics of the data (metadata), as well as use of single identifiers and/or unified naming conventions for data including legal entities, counterparties, customers and accounts.

This fits in well with the hybrid approach where specialized registers maintained for detailed tracking but using a common data definition may be conveniently aggregated into a governance-level enterprise register containing material risks, owners, KRIs and status for Board reporting.

Applications of a Risk Register in Practice

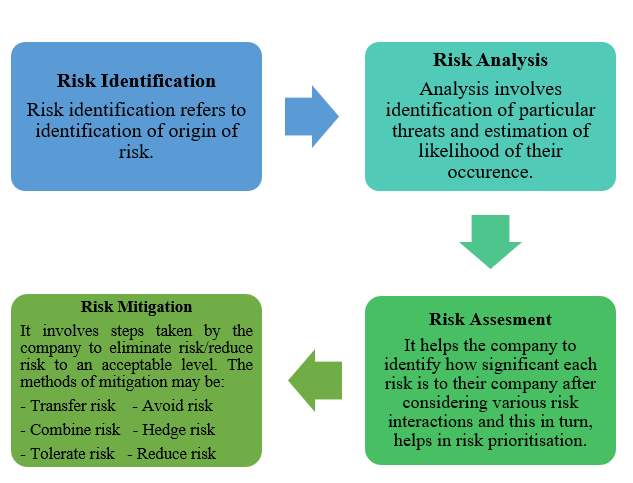

Risk registers influence nearly every stage of the risk management lifecycle. They support risk identification during new product assessments, process reviews and internal audit findings. They allow risk measurement through inherent/residual scoring and KRIs, ensuring early detection of deteriorating risk conditions. They facilitate the evaluation of controls, since internal audit and risk teams use the register as the primary record of what controls exist and how effective they are. Action plans arising from incidents, audits or supervisory observations are also tracked through the register, making it a central management tool.

Regulations call for a number of risk assessments including compliance risk assessment, ML/ TF risk assessment, information technology and cybersecurity risk assessment, outsourcing risk assessment, identification and assessment of operational risks, etc. NBFCs draw on the risk registers to supply the list of risk events, their inherent likelihood and consequence and provide the residual risks remaining with the company.

Risk registers are also a prerequisite for risk based internal audit. Risk registers, containing the list of internal controls, risk events and levels of inherent and residual risk, along with the Board’s risk appetite statement and tolerance limits form the basis of formulating the internal audit coverage. For more information on audit coverage refer to our write up here.

For reporting, the register forms the basis of periodic risk reports, senior management dashboards and regulatory submissions where required. During supervisory reviews, the RBI often tests whether an NBFC can produce documented evidence of risk identification, control ownership, monitoring and remediation—exactly what a well-maintained register provides. In this way, the risk register becomes both a governance mechanism and a demonstration of compliance readiness.

RBI outsourcing directions emphasise documentation of material outsourcing arrangements and evaluation of outsourcing risk. A risk register is the optimum tool for such third-party risk management to track and escalate both foreseeable and actual outsourcing incidents and due-diligence findings.

Conclusion

For NBFCs, maintaining risk registers is not merely a procedural obligation; it is a critical part of the organisation’s risk culture and governance framework. International standards (ISO 31000), global supervisory principles (Basel Committee), and regulatory expectations all converge on the need for structured, documented, and regularly monitored risk inventories. A robust risk register—supported by discipline, clear ownership and periodic review—enables NBFCs to anticipate threats, strengthen controls, improve decision-making and satisfy supervisory expectations. As NBFCs continue to scale, digitalise and partner with third-party ecosystems, the importance of maintaining comprehensive, dynamic and enterprise-aligned risk registers will only grow.

Our other resources on risk management:

- Operational Risk Assessment for NBFCs : Understanding The Basics

- Risk Management Policy: A Tool Of Risk Management

- Operational Risk Management – A Guidance Note

- Revamped Fraud Risk Management Directions

- Enterprise Risk Management

- Understanding Risk Management Framework in NBFCs

- A Need To Integrate Operational Risk Management & Resilience