GST on Corporate Guarantees: Understanding the new regime

– Payal Agarwal, Associate | corplaw@vinodkothari.com

The debate around levy of GST on corporate guarantee extended without or with inadequate consideration has been settled with the insertion of sub-rule (2) to Rule 28 of the Determination of Value of Supply Rules (“Valuation Rules”), effective from 26th October, 2023. Sub-rule (2) of Rule 28 specifies a deemed value for provisions of corporate guarantee to a related person subject to certain conditions. Now, vide another notification dated 10th July, 2024, amendments have been made to the said sub-rule, to ease out the provisions with respect to value of corporate guarantee given to a related person.

Effective date of the amendment

Sub-rule (2) of Rule 28 has been notified and made applicable w.e.f. 26th October, 2023. The amendments made under sub-rule (2), vide the July 2024 notification, has also been made applicable retrospectively, i.e., w.e.f. 26th October, 2023. Hence, sub-rule (2) of rule 28 applies to a corporate guarantee issued or renewed on or after 26th October, 2023.

Understanding the terminology

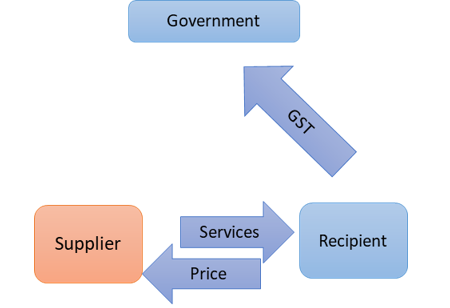

In usual financial parlance, the guarantor provides a guarantee to a lender (or other person to whom certain obligations or performance is owed), in favour of a borrower (or obligant, owing performance obligations). The guarantor is the giver of the guarantee, the lender is the receiver of the guarantee and the person for whom the guarantee is given is the beneficiary of the guarantee.

However, in GST parlance, it is important to understand that the language is from the viewpoint of “supply of services”. Hence, the guarantor is the supplier of the service, the borrower or beneficiary is the recipient of the service, and the lender is actually not a party to the supply, but has a relevance as the rules relate to who the guarantee is given.

Hence, importantly, the receiver of the supply in GST parlance is not the lender, but the borrower.

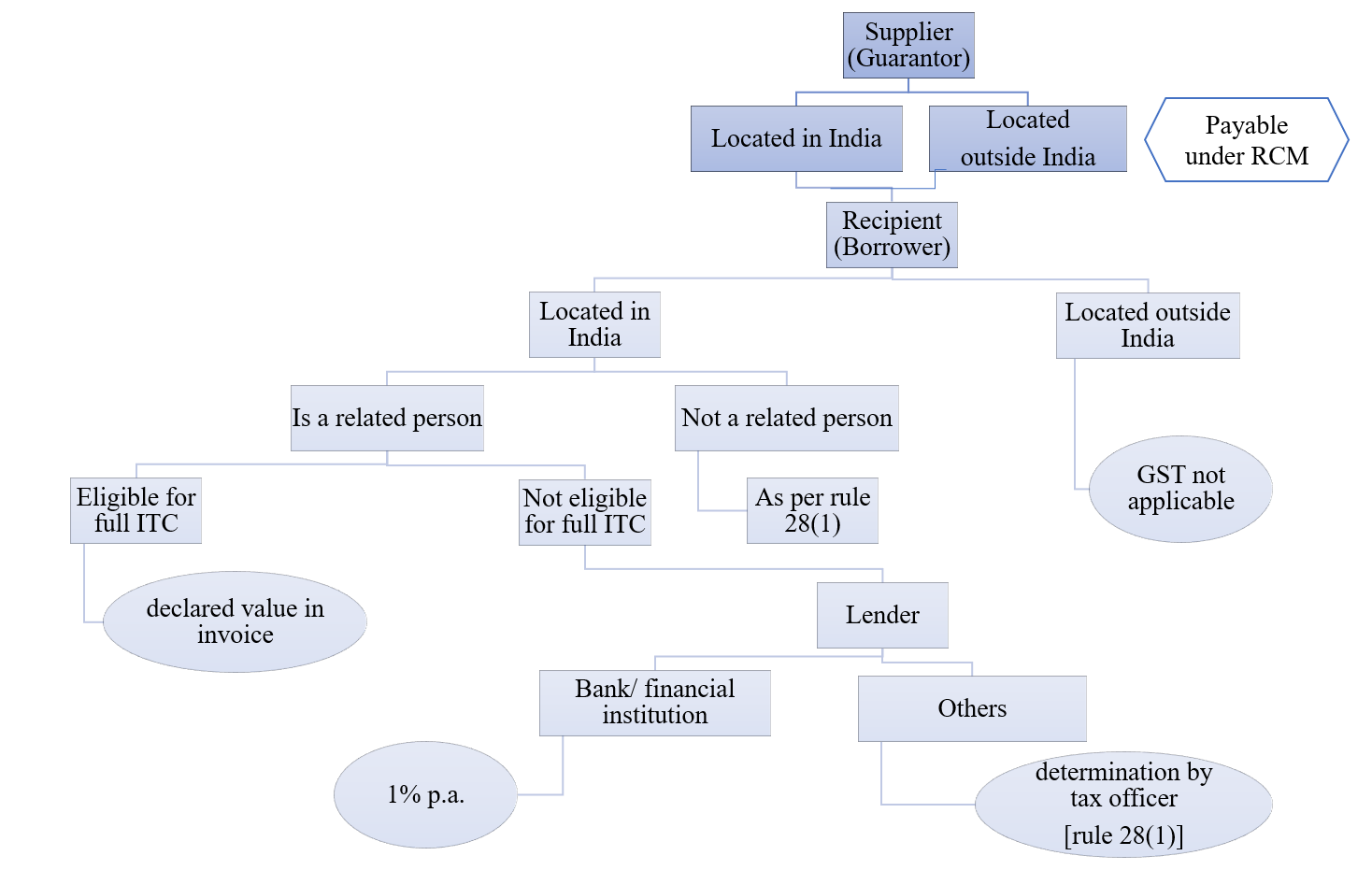

Value of supply of corporate guarantee for related persons

With the amendments coming into force, there are three ways the value of supply of service, i.e., issue of corporate guarantee, is to be determined, based on the nature of the recipient and the lender:

- As per the deemed value of the supply

- As per invoice value of the supply

- As per determination by the tax officer

The below chart summarises the same:

(a) Value of corporate guarantee as per deemed value under rule 28(2)

Rule 28 prescribes the value for supply of goods and services between distinct persons or related persons. In view of the common practice among related persons to provide corporate guarantee at nil consideration, sub-rule (2) was inserted under rule 28 to explicitly provide for a deemed value of consideration in case of supply of corporate guarantee. The same has been further amended vide the July amendment.

Sub-rule (2), as amended, reads as below:

“Notwithstanding anything contained in sub-rule (1), the value of supply of services by a supplier to a recipient who is a related person, located in India, by way of providing corporate guarantee to any banking company or financial institution on behalf of the said recipient, shall be deemed to be one per cent of the amount of such guarantee offered per annum, or the actual consideration, whichever is higher.”

The deemed value provided under the said rule is 1% p.a. of the amount of guarantee offered, where no consideration is charged, or the actual consideration is lower than the aforesaid threshold. However, the said deemed value is applicable only where the following conditions are met:

- Recipient of the service (i.e., the borrower) is a related person of the supplier (i.e., the guarantor),

- Recipient of the service is located in India (since GST is not levied on export of services),

- Recipient of the service is not eligible for full ITC, and

- Corporate guarantee has been provided to a banking company or financial institution[1]

(b) Value of corporate guarantee as per declared value in the invoice

A new proviso has also been inserted to sub-rule (2) of rule 28 vide the July amendment to ease out the GST implications on corporate guarantees. Pursuant to the said amendment, the deemed value of corporate guarantee will not apply, and the declared value in the invoice is taken as the value of the corporate guarantee, where the recipient of the service, i.e., the borrower is eligible for full ITC.

A similar proviso exists under sub-rule (1) of rule 28 as well. However, sub-rule (2) begins with a non-obstante clause, and thus, sub-rule (1) becomes non-existent for corporate guarantees between related persons to the banks/ financial institutions.

Hence, prior to the present amendment, for corporate guarantee between related persons, the relief with respect to invoice value was not available, and hence, GST was leviable on the basis of the deemed value. However, the amendments being applicable retrospectively, for recipients eligible for full ITC, benefit of invoice value will be available for corporate guarantees issued or renewed on or after 26th October, 2023.

Persons eligible for full ITC

Section 16 of the CGST Act specifies the eligibility and conditions for availing ITC. Where a person is eligible for a claim of full ITC, the value of supply of corporate guarantee will be based on the invoice value instead of the deemed value.

Here, it is important to note that the proviso refers to “full ITC”, and hence, eligibility for availing ITC u/s 16 is not enough, the recipient should be eligible for “full ITC”. The meaning of eligibility for full ITC is controversial, with some advance rulings on the subject[2]. In view of the aforesaid, it appears that the benefit of the proviso may not be available for a banking company or financial institution availing the option of 50% ITC as per sub-section (4) of section 17 of the CGST Act, as well as other persons providing exempt supplies. In essence, if the borrower (note, borrower is the recipient of the service) is a bank or financial institution or an entity providing exempt supplies, for whose borrowings a guarantor, being a related person, has given a guarantee, the deemed value will be applicable.

(c) Value of corporate guarantee determined by tax officers under rule 28(1)

Rule 28(2) being a specific provision for value of corporate guarantee between related persons, valuation as per sub-rule (1) will apply only in cases where sub-rule (2) is not applicable. Sub-rule (1) is a general provision, applicable to supply for any goods or services between distinct or related persons. Under the said sub-rule, the value of corporate guarantee will be based on the determination by the tax officer (refer our article on the same here).

Hence, the same will be applicable only in cases where value of supply as per (a) and (b) above does not apply.

Applicability of deemed value on FLDG arrangements

First Loss Default Guarantee or FLDGs[3] are arrangements that do not involve the borrower, the guarantee is usually given by the supplier (i.e., the DLG provider) to the lender. As such, unlike guarantee which is a tripartite contract between the guarantor, borrower and the lender, FLDG is more like an indemnity, involving only two parties – the indemnifier (i.e., the guarantor) and the indemnified (i.e., the lender). The borrower being out of the picture, the applicability of deemed value of corporate guarantee, if at all, would arise if the guarantor and the lender are related persons. However, going by the nature of FLDG – being an indemnity rather than a guarantee – sub-rule (2) of rule 28 does not seem to be applicable. However, if the transaction is between related persons, the recipient of the service being an NBFC, it is important to ensure that the terms of the service are based on arms’ length consideration.

Conclusion

With the recent amendments in the GST regime applicable on corporate guarantees to related persons, the deemed value of supply for levying GST on corporate guarantee does not apply, if consideration is being charged by the guarantor and the recipient is eligible to claim full ITC. Market valuation principles do not apply, and hence, one may further want to circumvent the provisions by charging guarantee commission at negligible value, thereby, avoiding a higher GST charge. However, that does not preclude the RPT consideration under corporate laws, that require at least companies to ensure that any related party transaction is undertaken at arm’s length terms including pricing, and hence, the guarantee commission charged from a related party should also be based on the same principle.

[1] The meaning of financial institution is to be taken from section 45-I(c) of RBI Act, 1934.

[2] See a few advance rulings on the subject by West Bengal AAR, Tamil Nadu AAR.

Also see a few articles on the subject: https://www.livelaw.in/law-firms/law-firm-articles-/input-tax-credit-central-goods-services-tax-rules-cgst-act-itc-tlc-legal-243111

https://taxguru.in/goods-and-service-tax/meaning-full-input-tax-credit-2nd-proviso-rule-28.html

[3]Structured Default Guarantees – https://vinodkothari.com/2022/09/structured-default-guarantees/

See our FAQs on default loss guarantee here – https://vinodkothari.com/2023/06/faqs-on-default-loss-guarantee-in-digital-lending/