Industry Standards Note on Minimum information to be provided to the Audit Committee and Shareholders for approval of Related Party Transactions (as revised) dated June 26, 2025 (“RPT ISN”).

Applicability of RPT ISN

with effect from 1st September, 2025 (‘Effective Date’)

Approval of AC

Approval of shareholders (in case of material RPTs)

Date of execution of RPTs

Applicability of RPT ISN

Before Effective Date

Before Effective Date

After Effective Date

Not Applicable

Before Effective Date

After Effective Date

After Effective Date

Not Applicable

After Effective Date

After Effective Date

After Effective Date

Applicable

Any subsequent material modification, renewal, ratification etc. after the Effective Date should require detailed disclosures as per RPT ISN

Exemption from applicability of RPT ISN

Exempted RPTs: RPTs exempt from approval requirements under Reg 23(5) of LODR

Small value RPTs: Transactions with a related party for an aggregate value of upto Rs. 1 crore in a FY

RPTs placed for quarterly review under Reg. 23(3)(d).

Minimum information to AC divided into 3 parts

Part A – Minimum information of the proposed RPT, applicable to all RPTs (Para A1 to A5)

Part B – Additional information applicable to proposed RPTs of specified nature (Para B1 to B7)

Part C – Additional information applicable to Material RPTs (as per Reg 23 of LODR) of specified nature (Para C1 to C6)

Certification requirement to AC (‘KMP certificate’)

From

CEO/ Managing Director/ Whole-time Director/ Manager and

CFO of the listed entity

To the effect that

RPTs proposed to be entered are in the interest of the listed entity

Role of AC

To review the certificate – the fact to be disclosed in the notice to shareholders

Minimum information to shareholders

Information as may be required under CA, 2013

Information as placed before AC in terms of RPT ISN

AC may approve redaction of commercial secrets and such other information that would affect competitive position of listed entity

Subject to affirmation that, in its assessment, the redacted disclosures still provide all the necessary information to the public shareholders for informed decision making

Justification as to the transaction in the interest of the listed entity

Basis for determination of price and other material terms and conditions of RPTs

Affirmation that AC has reviewed the KMP certificate on proposed RPTs

Disclosure of approval of AC and recommendation of board

Web-link and QR code of third-party reports/ valuation report, if any, considered by AC

Role of Management

Management to provide information against each line-item

Indicate NA, where field is not applicable along with reason for non-applicability

Comments/ decision of AC

AC may provide comments on any line-item, based on its discretion

Rationale to be disclosed, in case an RPT is not approved

Comments and rationale to be minutised

Furnishing of valuation/ third party report

To be furnished to AC, if any

Web-link and QR code to be disclosed in shareholders’ notice, if considered by AC

Our analysis of the detailed disclosure requirements on relevant line-items are being collated in the form of FAQs. Keep checking our website for more.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2025-06-27 14:19:322025-06-27 14:51:17Tailored to Fit Practically: Disclosure for RPTs under Revised Industry Standards

Starting a company often means wearing multiple hats. In these early stages, many founders structure their compensation through Employee Stock Option Plans (“ESOPs”) rather than traditional salaries. This arrangement makes perfect sense when resources are tight and every rupee earned needs to be reinvested into growth of the company. ESOPs align founders’ interests with the company’s long term success.

But here’s when things get complicated: the companies grow and prepare to go ‘public’; the founders find themselves classified as “promoters” under SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (“ICDR Regulations”). With more risks than rewards, they find themselves in a position, where their earlier ESOP grants, reflecting the growth of the company built by them, though perfectly valid during the grant, may now be taken away.

Recognising this unfair situation, at its meeting held on June 18, 2025, SEBI has approved an amendment providing regulatory relief for founders of companies who hold ESOPs and are subsequently classified as promoters at the time of an IPO. The amendment seeks to clarify the position of ESOPs and other share based benefits, granted to promoters and promoter group members prior to categorisation as such, and permit the exercise of such grants even after listing of the company.

While the amendments seek to enable founders in IPO-bound companies to avail of the share based benefits granted to them, the language of the explanation falls short of the intent. In this article, we discuss the need for the amendments in line with the existing scenario, how the amendments seek to meet the need and the gap that remains.

Proposal laid down in Consultation Paper

The proposal approved by SEBI in its recent BM is based on the proposal contained in its consultation paper dated March 20, 2025 to include an explanation under Regulation 9(6) of SBEB Regulations.

As per the Para 3.5.1 of the Consultation paper, SEBI had proposed to include an explanation may be inserted under regulation 9(6) of SBEB Regulations which would state:

Explanation 2: an employee, identified as a “promoter” or “promoter group” in the draft offer document filed by a company in relation to an initial public offering, who was granted options, SARs or other benefits under any scheme prior to being identified as a “promoter” or “promoter group”, as the case may be, shall be eligible to continue to hold, exercise or avail any such option, SAR or benefit, in accordance with its terms and granted, prior to one year from the date when the Company (i.e. its’ Board) decides to undertake Initial Public Offering and, in compliance with these Regulations.

The proposed explanation provides a clarification with respect to holding or exercise of share options or other similar benefits granted to an employee, identified as promoter/ promoter group in the DRHP, subject to the following conditions:

The grant of options or benefits must have been made prior to the employee being identified as a ‘promoter’ or ‘promoter group’; and

The grant must have occurred at least one year prior to the Board’s decision to undertake an IPO.

These conditions have been discussed in detail in the later part of this article. Before that, it is necessary to understand the need for the amendment.

Need for the amendment: prohibition on promoters holding ESOPs

An explanation to Rule 12(1) of the Companies (Share Capital and Debentures) Rules, 2014 excludes a promoter or a person belonging to the promoter group from the definition of ‘employee’, in the context of eligibility for grant of ESOPs.

However, pursuant to Companies (Share Capital and Debentures) Third Amendment Rules, 2016 Dated July 19, 2016, a proviso has been added to the aforesaid explanation that provides an exemption for start-up companies up to ten years from the date of its incorporation or registration. Therefore, in case of a start-up, a promoter or member of promoter group may also be issued ESOPs upto 10 years from the date of its incorporation.

Similar prohibition applies to a listed entity, as per Reg 2(1)(i) of SEBI (Share Based Employee Benefits and Sweat Equity) Regulations, 2021, pursuant to which, an employee does not include a promoter or a person belonging to promoter group. There is no exemption for a start-up company under the said Regulations.

Founder or promoter : a question of identity

The term ‘promoter’ is defined in an almost similar fashion in both Companies Act, 2013 (“ and ICDR Regulations. As per the definition, there are three limbs to the definition of promoter, being:

Promoter by proclamation: that is, the person who is named as promoter in the offer documents or the annual return.

Promoter by control: that is, a person having control over affairs, whether as shareholder, director or otherwise, directly or indirectly.

Promoter by absentee control: that is, by orchestrating the affairs of the company by giving instructions to the board of directors, which the latter is accustomed to adhere to.

Further, the term ‘promoter group’, is not a defined term under the Companies Act, 2013 and hence, may be open to interpretation.

On the question of whether or not every founder may be considered as promoters, what needs to be understood is that while the founder may be the one who initiates the idea of the start-up, it may so happen that subsequent to new investors coming in, the founder may gradually lose his powers to control the affairs of the company. The board becomes independent, the private equity investors get to have a call in various matters, and the powers get diluted, pursuant to which the founder may not be recognised as a promoter after all.

However, the stock exchanges apply various additional criteria for considering a person as ‘promoter’, some of which may categorise a Founder as promoter, regardless of whether the same is holding ‘control’ in the company or not.

For instance, as per news reports[1], the guidance issued by NSE for promoter categorisation in case of an IPO-bound company, requires founders to be categorised as promoters if:

They hold a position or have the right to be nominated, as a director or KMP/SMP; and

They have a collective shareholding of 10% or more of the equity shares (including options which are vested till the date of listing) of the company, either directly or through any legal entities or persons controlled by such founder or his/her immediate relatives.

Therefore, even when a founder may not be holding ‘control’ in a company, he may be categorised as a promoter by holding options if they are crossing the 10% threshold.

Fate of ESOPs issued to founders, later turned promoters

The SBEB Regulations, as discussed above, do not allow promoters to hold ESOPs or other share based benefits in a listed entity. Although applicable to listed entities, the compliance is required to be ensured at the stage of filing of DRHP, and hence, IPO-bound companies are also covered.

While the Regulations exclude the promoters from the definition of an employee eligible for the receipt of ESOPs, it does not clarify the treatment of options that are already granted to promoters, prior to such classification. This led to a confusion in case of options issued to Founders-turned-Promoters, putting the fate of such granted options in a grey area.

In case a view is taken that such options need to be liquidated, and the benefits thus accruing, has to be foregone, at the time of identification as a promoter, the same would not be justified. It is not on their own wish to become a promoter, and since the options are part of the remuneration of the Founders as employees, granting them an immunity for such options is needed.

Decoding the conditions for exemption

1. Grant of options prior to identification as promoter or promoter group

The purpose of the amendments is to primarily cover the ‘founders’ of start-up companies, where it would be typical to give share based options to incentivise the founders and as a remuneration against the services offered by such employees.

As discussed above, there may be situations where a person, though a founder of the company, was not categorised as promoter under CA, 2013. However, pursuant to the categorisation conditions followed by the SEs, during filing of DRHP, may get covered as a ‘promoter’ or ‘promoter group member’.

The explanation refers to grant of share based benefits, prior to being identified as a “promoter” or “promoter group”, and thus, refers to such employees/ founders who were not categorised as promoter/ promoter group prior to grant of options.

However, consider the case of a founder of a start-up who was identified as a promoter since inception, but was granted ESOPs pursuant to the exemption available to start-ups under CA, 2013. If the company later decides to go for listing, it remains unclear whether such ESOPs would remain valid under this proposed explanation. This is because, technically, the first condition requiring that the ESOP grant be made before the individual was identified as a promoter, is not satisfied in such cases.

This condition risks contradicting the very objective of the amendment, which is to safeguard pre-IPO entitlements granted to founders while ensuring regulatory safeguards for promoters are maintained at the time of listing. The start-up related exemption, as available to the promoters under CA, 2013 is with the objective of permitting the founders, whether promoter or otherwise, to be benefitted from the growth of the company and be entitled to share based benefits.

2. Grant must have occurred at least one year prior to the Board’s decision to undertake an IPO

The condition requires the options or other benefits to have been granted at least 1 year prior to the board’s decision of undertaking an IPO. The clause provides a cooling off period between the grant of options and the company’s IPO decision, so as to prevent situations where companies might quickly issue ESOPs or other share based benefits to promoters just before going public, thus taking benefit in ingenuine cases.

The one year requirement is a reasonable safeguard, as it helps protect the interest of public shareholders and ensure that such grants are made in advance to genuine employees only as a reward for their contribution to the company and not as an opportunistic benefit tied to the IPO.

Conclusion

While SEBI’s proposal to introduce an explanation under Regulation 9(6) of the SBEB Regulations is a well-intended step towards addressing the gaps affecting founders of start-ups, its current framing leaves room for ambiguity.

The final wording of the amendment, once notified, will be pivotal in determining whether this balance between protecting founders’ rights and maintaining necessary safeguards for promoters. It is hoped that SEBI will clearly address this issue in the final version, so that the real purpose of the amendment is not lost in technical wording.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-25 18:40:062025-06-26 10:34:39ESOPs for founders: Well intended relief, garbled by language?

Here is a tale of three families, and trust, almost every business family in the country may fit in the tale. (All names are completely hypothetical.)

Family One – Jaani family, owning large number of listed companies in the country. Ashok, son of the founder, got married to Rani, daughter of the founder of Maani family.

Maani family – once again another leading industrial houses in the country. Rani, daughter of the founder, has two siblings – Prashik, and Vimla. Prashik runs the family’s businesses. Vimla got recently married to Varun, from Dhyaani family.

Camera shifts to Dhyaani family, where Vimla got married to Varun. Relations are made between equals – hence, Dhyaani family is no less in stature than the Maani family and the Jaani family.

All the families have variety of listed and unlisted companies in their control. In most cases, shareholdings of operating entities are through investing vehicles, which are held in the name of individuals of the families.

Given the definition of “promoter group”, Ashok is a promoter. Ashok’s wife, Rani is obviously an “immediate relative” and hence a part of promoter group.

By definition (if we read it to mean parents, brother, sister and child of the spouse too), Rani’s father, the founder of the Maani family, becomes a part of the “promoter group” for Jaani family. So also will be Prashik. Vimla, though married in Dhyaani family, being sister of Rani, will also be part of “promoter group”.

Now look at the consequences. All bodies corporate where 20% shareholding is held by the individuals of Maani family – founder, Prashik and Prashik’s mother, will form part of the promoter group of the Jaani family.

We don’t stop here – all entities where Vimla, now a part of Dhyaani family, will also need to identify bodies corporate where she holds 20%, and these entities will be reported as a part of the PG for Jaani family.

The same process will have to run for Maani family and Dhyaani family – hence, the focus may actually shift over to the country’s business tycoons one by one.

The sweep of the definition of “promoter group” may have had its own intent, but it cannot be stretched to include सगे सम्बन्धी where there is no evidence of commonality. Sadly enough, SEBI rules require a listed company to list out the names of all such सगे सम्बन्धी entities, no matter whether there is a shareholding overlap or not. And all these entities will be identified as “related parties” too.

Our other resources on promoter/promoter group can be accessed below:

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kotharihttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari2025-06-25 12:59:572025-07-17 13:29:08Yeh Rishta kya kahlaata hai! – the strange case of "promoters-in-law"

Probably the first in India, green securitisation has finally found an entry with the recent issuance of pass-through certificates backed by residential rooftop solar loan receivables in India. The loans were originated by a ‘green-only’ NBFC focussed on climate-positive lending. The present issuance is in the form of green collateral securitisation – since the securitised receivables qualify as ‘green’. Further, given the activities of the originator, it seems that the same may qualify to be a green capital securitisation, with the freed capital of the originator being utilised towards creation of green assets.

Notably, as per a recent publication of Climate Policy Initiative, the Global Landscape of Climate Finance 2025, India has been ranked as the leading country in the South Asia region in terms of mobilisation of climate finance (as per the data for 2023). Green securitisation may act as a catalyst to the growth of green finance in India. See a whitepaper on the same here.

A broader concept in the context of climate finance is sustainable securitisation, our whitepaper on the same can be accessed here. The recent guidelines of SEBI also permits the issuance and listing of sustainable securitised debt instruments, based on the recommendations of the Working Group constituted for the review of SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008, chaired by Mr. Vinod Kothari. An article on the concept of sustainable SDIs may be accessed here.

The evolution of Electronic Trading Platform (‘ETPs’) is rooted in the market’s need for speed, efficiency, and enhanced transparency in dissemination of trade information. Traditional floor based trading methods struggled with sluggish processes, limited data dissemination, and inefficiencies that couldn’t pace with a global financial landscape. In response, industry players and regulators recognised the need for a digital overhaul, a system that could streamline trade execution, provide real-time market data, and foster a more accurate price discovery mechanism. This led to the emergence of specialised platforms, such as those designed for government securities trading, where primary dealers are entrusted with membership and operations. One such platform is ETP.

An ETP is a computarised system that facilitates the buying, selling and management of a wide range of financial instruments (listed down below). These platforms enable real-time market data dissemination, order execution, and efficient trade processing. For instance, in India, platforms such as the NDS-OM (Negotiated Dealing System – Order Matching) are well-known examples that specialize in government securities (g-sec) trading. Other entities include various bank-operated ETPs such as BARX operated by Barclays Investment Bank (international) and proprietary systems developed by financial institutions such as 360TGTX operated by Three Sixty Trading Networks (India) Pvt. Ltd.

Entities operating ETPs facilitating transactions in eligible instruments,under the New ETP Directions,

Grandfathering clause:

Any entity already authorised under the Erstwhile ETP Directions shall deemed to have been authorised under the New ETP Directions, or

any action already taken under the Erstwhile ETP Directions “shall be deemed to have been taken” under the New ETP Directions.

In practical terms, operators need not re-submit applications, seek fresh authorisations or revisit past actions as long as compliant under the Erstwhile ETP Directions.

Effective Date:

Effective immediately i.e. from June 16, 2025.

All about Electronic Trading Platforms (‘ETPs’)

Before going ahead to analyse the changes let us understand what ETPs are. ETPs are electronic systems, other than recognised stock exchanges, on which transactions in eligible instruments are contracted. But why would someone prefer trading on ETP rather than other exchanges/ platforms such as stock exchanges? ETPs offer eligible entities multi-instrument trading platforms (dealing with money-market, G-Secs, FX, swaps etc.) with tailored tenures and faster settlement process while stock exchanges cater to listed equities and futures with standardised contracts, retail participation and fixed trading hours.

Who operates these electronic systems?

Any entity as defined in the New ETP Directions incorporated in the form of a company and authorised by the RBI in this regard can operate an ETP. Currently, there are 12 authorised ETP operators under the Erstwhile ETP Directions who shall continue to operate under the New ETP Directions.

Types of ETP: Single Dealer Platform v. Multi-Dealer Platform

Basis

Single Dealer Platform

Multi-Dealer Platform

Seller

A single bank or financial institution

Several banks and financial institutions

Pricing

Tailored pricing from one provider.

Competitive pricing with options from several liquidity providers.

Liquidity

Low

High

Liquidity source

Provided by a single bank or institution.

Aggregated liquidity from multiple banks/institutions.

Customisation

Tailored interfaces and services designed for specific clients.

More standardized interfaces across multiple dealers; less tailored.

Execution quality

Stable and consistent execution within one controlled environment

Best execution can be sought across multiple quotes and providers

Suitability

Clients who value a close banking relationship and prefer a dedicated, controlled trading environment

Clients who want to compare and execute trades across a range of prices and liquidity providers

Example

NDS-OM, operated by Clearcorp Dealing Systems (India) Ltd., provides a secondary market platform for government securities owned by RBI

360TGTX, operated by Three Sixty Trading Networks (India) Pvt. Ltd., provides a platform for trading in FX Spot, Forwards, Swaps and Options

Players on ETP

Primary Dealers- In 1995, the RBI introduced the system of PDs in the Government Securities (G-Sec) Market. The objectives of the PD system are to strengthen the infrastructure in G-Sec market, development of underwriting and market making capabilities for G-Sec, improve secondary market trading system and to make PDs an effective conduit for open market operations (OMO).

The RBI currently extends various facilities to the PDs to enable them to fulfill their obligations, including memberships of electronic dealing, trading and settlement systems (NDS platforms/INFINET/RTGS/CCIL).

PDs are classified as below:

Standalone Primary Dealers- NBFC-ML

Bank Primary Dealers- Scheduled Commercial Banks and Central Banks- National and International

Basis

Standalone Primary Dealer

Bank Primary Dealers

Entity Structure

Operate as independent legal entities, often registered as NBFCs or as dedicated subsidiaries/joint ventures.

Operate as a departmental function within a scheduled commercial bank (or its branch, including foreign banks).

Regulatory Framework

RBI guidelines

RBI Guidelines and bank specific norms

Business focus

Primarily focused on government securities trading and related activities, often with more flexibility to diversify (e.g., underwriting, trading derivatives).

The primary dealer function is one element of a larger suite of banking services and is more integrated with the bank’s overall operations.

Operational Independence

Greater operational autonomy, being solely focused on the government securities market

Functions as an integral part of the bank’s operations, with decisions influenced by the broader business strategy of the bank

PDs registered with RBI

SBI DFHI Limited

Bank of Baroda, Bank of America

Traders

Analysis of Change

Having understood the nomenclature, we may proceed to analyse the changes and what they mean for Regulated Entities. The primary change and intent of the Draft Directions was to curb unregulated entities and platforms, specifically offshore platforms dealing with foreign exchange trading involving inshore/ domestic investors. Please note that foreign exchange instruments have been a part of eligible instruments, however, due to not being defined, the question whether such offshore ETPs would be covered, was always a question. The Draft Directions recommended certain changes, however, the major change was bringing offshore ETPs under the domain of RBI. However, the finalised New ETP Directions do not deal with this aspect.

While the RBI largely accepted the foundational architecture proposed in the draft, it has revised certain provisions to provide clarity in many areas, especially around risk and operational aspects which are now expressed in more precise terms along with addition of new provisions around enforcement and transitional mechanisms.

Highlights of Major Changes:

Expanded applicability to include outsourcing entities under the purview of the New ETP Directions in essence

Carve out to single dealer banks and Standalone Primary Dealer (‘SPD’)

Transition to an electronic application process: Moving away from physical submission, the application process is now streamlined through the PRAVAAH portal

Quarterly and annual reporting requirements for the operators introduced mandating regular updates thereby tightening regulatory oversight

Framework for data preservation and sharing post-authorisation

Comparison at a Glance:

Area

Erstwhile ETP Directions

New ETP Directions

Implications

Application process for authorisation

Physical submission

Through PRAVAAH Portal of RBI

Streamlining the process, enhancing accessibility, efficiency, and real-time tracking for applicants as well as regulators

Quarterly reporting

No such requirement

Quarterly reporting on functioning of ETPs by Operators (details covered below)

Operators to provide periodic updates on operational performance, ensuring regulatory oversight

Annual Reporting

No such requirement

Annual reporting on compliance of the New ETP Directions and terms and conditions prescribed (details covered below)

Operators to yearly confirm their adherence to updated regulatory guidelines and contractual conditions

Eligibility Criteria

Did not apply to ETPs operated by SCBs

Apply to all the entities including SCBs operated ETPs (except exemption covered below)

Banks must now play by the same rulebook as other operators, additionally Public Sector Banks shall have to incorporate (or spin off) a Companies Act vehicle, infuse requisite capital and adhere to technological standards. Until now, Public Sector Banks that operate an ETP slipped neatly around the RBI’s “company‐only” eligibility gate. The New ETP Direction takes away that privilege. From the day the change takes effect, every ETP, bank-owned or not must meet the same bar

Preservation, access and use of data

Did not have a provision for treatment of data in the event of cancellation of authorisation

Specifies the requirement to share data, along with form and manner, with the RBI or any agency in the event of cancellation of authorisation as may be called upon by the RBI or any other agency.

Enhanced regulatory oversight and post-termination accountability on operators

Definition of ‘Entity’

“….an agency formed as a ‘company’ and incorporated under the Companies Act, 2013 (or earlier acts)”

“….any person, natural or legal.”

Language of the New ETP Directions seems to widen the scope of entity, however reading the impact along with para 6(f)(iii), it only brings the outsourcing entities under the widened scope

Grandfathering Rule

Not needed (first issue)

All licenses/actions under Erstwhile ETP Directions shall be treated as valid

No fresh registration required

Exemption

ETPs operated by banks for their customer on a bilateral basis as long as no market is being created for the securities

Carve out to SCBs (including branches of Foreign Banks operating in India) and SPDs wherein the bank or the SPD operating the electronic system is the sole quote/price provider and a party to all transactions contracted on the system.

Banks and SPDs can operate proprietary trading platforms without the full weight of the standard compliance requirements set for multi-dealer platforms. This can streamline their internal processes and reduce regulatory and technological burdens.Acting as the sole quote provider makes these institutions both the operator and counterparty. This can improve execution speed and reduce inter-dealer friction.A single market maker model may lead to faster execution but can constrain competitive pricing, potentially resulting in wider spreads if the operator does not face rival pricing pressures from other dealers.While banks and SPDs gain efficiency due to lesser compliances, they must remain vigilant about disclosure and transparency requirements to avoid any adverse effects on market integrity.Banks and SPDs may develop more tailored platforms, exclusive systems to capture niche market segments.Synchronization with global norms that treat single-dealer platforms as an extension of the dealer’s book and not that of an exchange.

Reporting Requirements:

These new requirements shall have to be complied with along with the existing reporting requirements under the Erswhile ETP Directions from the effective date of the New ETP Directions. Accordingly, the first quarterly report shall be required to be submitted on or before 15th July, 2025 and the annual report shall be submitted on or before 30th April, 2026. The manner of reporting by ETP operators as per the New ETP Directions has been listed below:

Reporting Requirement

Reporting Authority

Frequency

Format

Timeline

New

Functioning of the platform, including but not limited to the following points:Events resulting in disruption of activities, during the quarter, if anyInstances of market abuse, during the quarter, if anyDetails about any material change in trading procedure or technology carried out during the quarter

On or before 15th day of the month following the quarter

Compliance with the New ETP Directions and terms and conditions prescribed at the time of authorisation

RBI

Annually

Not specified

on or before the 30th of April of the succeeding financial year

Data relating to activities on the ETP

RBI

Post cancellation of authorisation

As may be prescribed

As may be prescribed

Existing

Transaction information

Trade repository or trading platform

As may be prescribed

As may be prescribed

As may be prescribed

Other report, data and/or information as required by RBI

RBI

As may be prescribed

As may be prescribed

As may be prescribed

Data/information

Any agency as required by Indian Laws

Not specified

Not specified

Not specified

Event resulting in disruption of activities or market abuse

RBI

Event-based

Not specified

Not specified

Conclusion:

By introducing defined protocols for risk management, data governance and reporting, the updated framework seeks to close existing regulatory gaps. Key provisions of the New ETP Directions include, amongst others, a clear exemption for single–dealer platforms and a streamlined application process via the PRAVAAH portal. These measures ensure legal continuity. Ultimately, this transformative framework not only reinforces the integrity of the trading ecosystem but also cultivates an environment conducive to innovation.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-23 19:18:342025-06-23 19:33:47Master Direction on ETPs: Key Changes & Compliance Guide

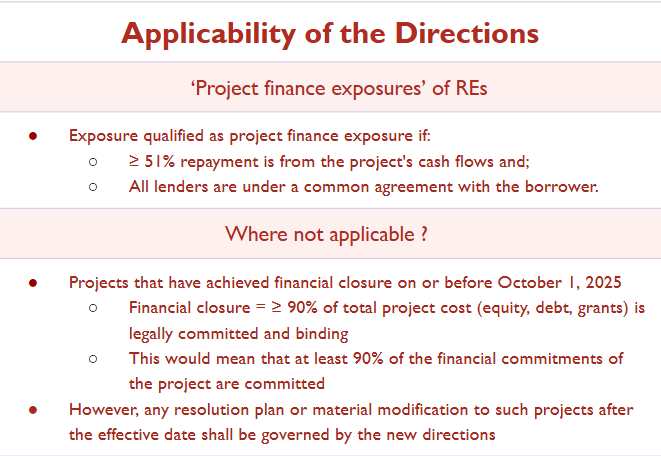

Project loans, used to finance large infrastructure and industrial ventures like highways, power plants and railways etc., are fundamentally different from regular business or personal loans. Unlike typical loans that are repaid from either the borrower’s existing operations and balance sheet (in case of the former) or the borrower’s own credit worthiness (in case of the latter), project loans are forward-looking: they primarily rely on cash flows of the project, generated onlyafterthe project becomes operational. Because of this, delays in project completion due to various factors such as land acquisition issues and regulatory delays which may be beyond the control of the developer are common. These may arise from. Such delays, though being routine and not necessarily indicating borrower’s stress, triggered adverse asset classifications under the existing rules.

When the RBI introduced its 2019 prudential framework to enable early recognition and time bound resolution of stressed assets, it excluded such project loans from its scope (see para 25). As a result, these continued to be governed by old norms, specifically para 4.2.5 of the 2015 IRCAP and later, para 3 of Annex III under the RBI SBR Directions. However, these norms did not reflect the unique risks faced by project finance especially during the construction phase.

To address these issues, the RBI released the Draft Project Finance Directions in May 2024, proposing a dedicated regulatory framework tailored to project loans. The Project Finance Directions(‘Directions’) have been issued on 19 June, 2025. This article explores the need for such a framework, the changes brought in the regulatory regime, and their impact on borrowers and lenders.

Project finance vs other kinds of finance

In corporate lending, credit decisions are primarily based on the borrower’s balance sheet strength, existing cash flows and overall financial health. where the lender primarily assumes credit risk

In contrast, in project finance, repayments as well as the primary security depend primarily on the successful implementation and projected cash flows of a specific project, rather than the borrower’s overall financial position. Accordingly, the lender takes two different risks:

Project riski.e. the risk that the project may face commencement delays due to factors like regulatory bottlenecks, land acquisition issues or construction delays and;

Credit riski.e. the risk of inadequacy of cashflows to make the scheduled contractual payouts.

Importantly, in project finance, delays in cashflows often happen due to non-credit factors linked to project execution, mainly project delays. As a result, automatic downgrading of classification due to any project delay may not only fail to provide a true risk profile of the loan but also cause increased provisioning burden on the lender.

Overview of the Directions

The Directions deal with the following broad aspects:

Classification of projects and project finance;

Prudential requirements for extending project loans including:

Provisioning requirements;

Conditions for sanction, disbursement and monitoring.

Resolution and restructuring of project loans

Either due to stress;

Extension/ delays in DCCO.

Applicability

Classification of ‘project’ and ‘project finance’

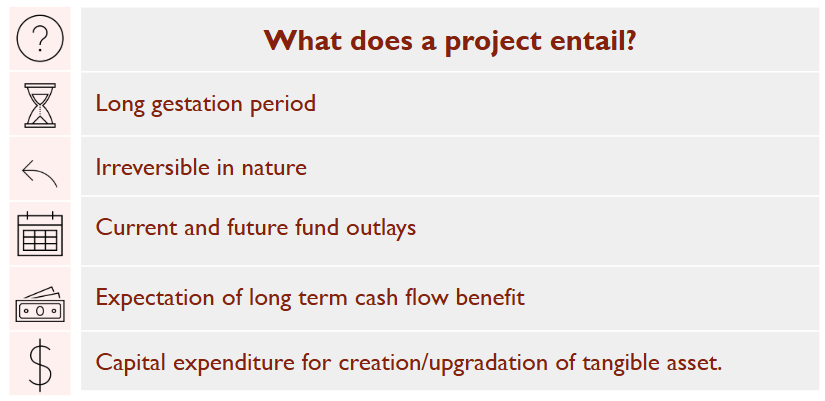

Under the Directions, a project is defined as to involve capital expenditure for the creation, expansion or upgradation of tangible assets or facilities, with the expectation of long-term cash flow benefits [see para 9(l)], with the following features:

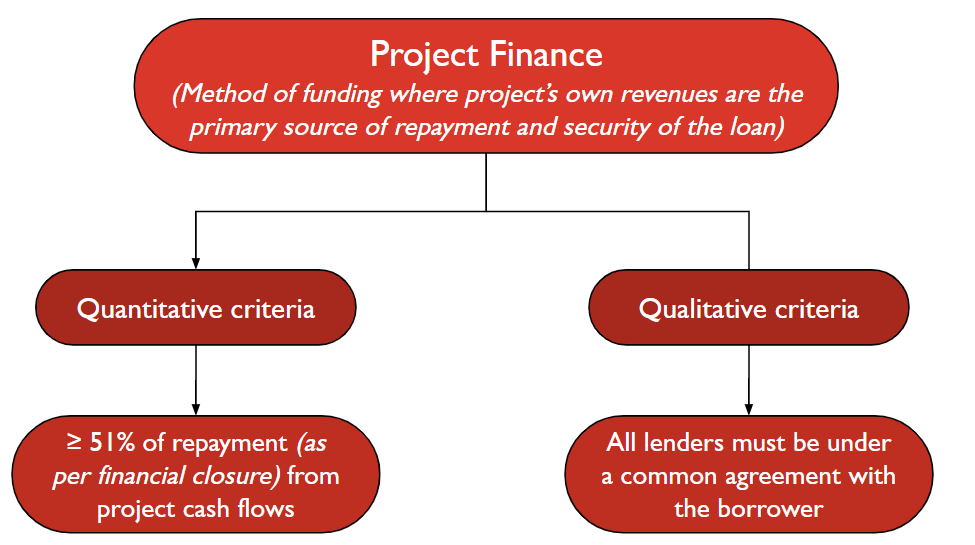

Project finance is a method of funding where the project’s cash flows/ revenue own revenues are the primary source of repayment as well as the and security for the loan [see para 9(m)].

It can be:

Greenfield (new project);

Brownfield (existing project enhancement).

To qualify as project finance under the Directions:

Note: Loan terms can differ across lenders if agreed by all parties

The earlier definition of project finance under the SBR Directions was generic and vague, referring merely to a “project loan” as any term loan extended for setting up an economic venture. The Directions have provided more clarity on what would be considered as project finance and have linked it to the definition of project finance under the Basel Framework, while also providing a quantitative threshold of 51%.

Project finance envisages the lender’s exposure in a project, which is typically in the process of being set up. The repayment will be from the project cashflow i.e. the payout structure is connected with the commencement of commercial operations of the project. The lending is based on the projected cash flows of the project rather than the balance sheet of the developer. It is distinct from asset finance, where loans are backed by existing assets generating income. Further, project finance differs from a working capital loan/general corporate purpose loan where the latter is towards financing the working capital needs of the developer entity based on the overall health of the entity.

Would it mean that project loans cannot have any other collateral and must solely rely on the project as the security? The answer is negative since the threshold specified allows to have other/ additional collateral, say, personal guarantee of the developer etc., however, the primary security shall be the project cashflows.

Other important terminology

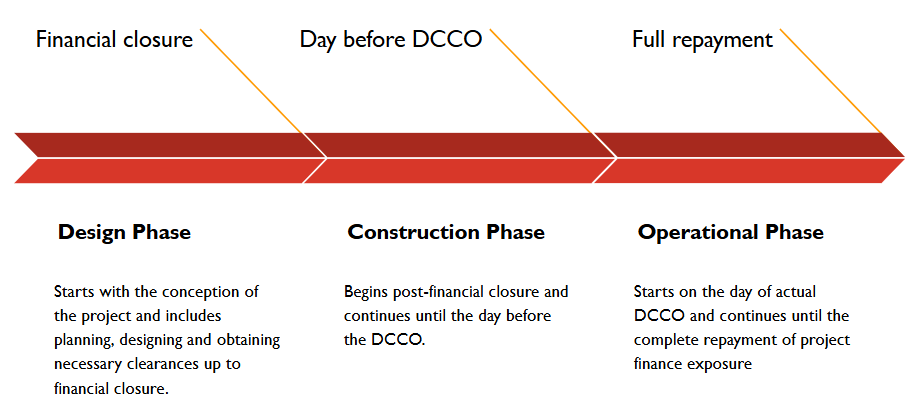

DCCO

The Date of Commencement of Commercial Operations (DCCO) is a key milestone in project finance, marking the transition from construction to operational phase when a project begins to generate revenue.The Directions recognises three forms of DCCO. [see Para 9(e) to (m)]

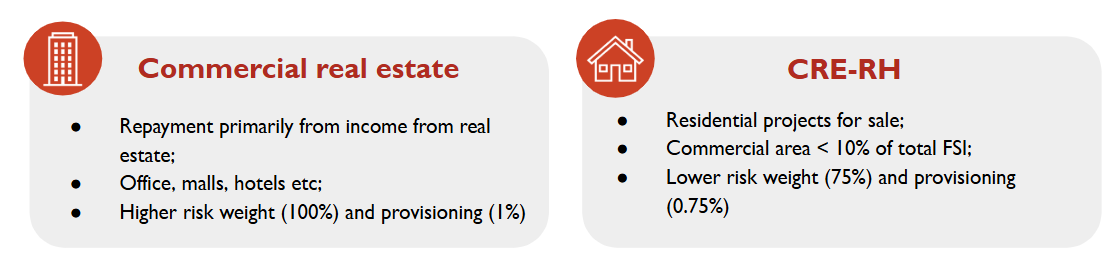

CRE and its sub-category CRE-RH

Defined in Directions on Classification of Exposures as Commercial Real Estate Exposures, CRE refers to loans or exposures where repayment primarily depends on income generated by the real estate asset itself. This typically includes office spaces, malls, warehouses, hotels and multi-family housing complexes that are leased or sold in the open market. Since CRE is a sub-head of project finance, it also follows similar characteritics of project finance i.e.both repayment of the loan and recovery in case of default are closely tied to the cash flows from the real estate asset such as rental income or sale proceeds. [see para 9(b)]. The definition is aligned with the definiton of income-producing real estate (IPRE) under Basel norms. Our article discussing CRE can be assessed here. https://vinodkothari.com/2023/04/commercial-real-estate-lending-risks-and-regulatory-focus/

Commercial Real Estate – Residential Housing (CRE-RH) [see para 9(c)]

Since residential housing projects generally pose lesser risk and volatility compared to commercial properties, the RBI created a distinct sub-category within CRE called CRE-RH vide notification dated June 21, 2013. CRE-RH includes loans given to builders or developers for residential housing projects meant for sale.To classify as CRE-RH, the project must be predominantly residential and commercial components like shops or schools should not exceed 10% of the total built-up area (FSI). If the commercial area crosses this 10% threshold, the entire project will be CRE. This distinction isn’t just semantic, it has regulatory benefits. Since CRE-RH are subject to lower risk due to various reasons such as diversified cash flows and lower dependency on a single occpnt, RBI has assigned lower capital risk weights i.e. 75% to CRE-RH compared to standard CRE 100% and lower provisioning provisioning requirements (0.75% vs. 1%).

Prudential requirements

Provisioning requirements

In the context of project finance, where risks vary across different phases of a project’s lifecycle, a one-size-fits-all provisioning approach throughout the project life may not be relevant. .

Under the SBR, provisioning norms made no distinction between the construction and operational phases of a project. A uniform provisioning rate was applied i.e. 0.75% for CRE-RH and 1% for CRE while other loans were provisioned at 0.4% irrespective of whether the project was just starting construction or had already begun generating revenue. This approach, while simple, failed to reflect the heightened risks associated during the construction phase , such as delays, cost overruns, or regulatory hurdles.

To address this gap, the Draft Directions, proposed a conservative approach calling for a 5% provision during the construction phase and 2.5% during the operational phase, with the operational rate reducible to 1% if following conditions were met:

the project demonstrated positive net operating cash flows sufficient to service all current repayment obligations, and

there was a minimum 20% reduction in long-term debt from the level outstanding at the time of achieving DCCO.

These draft norms were considered overly harsh, particularly for long-gestation infrastructure projects where cash flows stabilise gradually.

Taking stakeholder feedback into account, the Directions adopted a more balanced g structure as follows:

Project type

Construction Phase

Operational phase – after commencement of repayment interest and principle

Commercial real estate (CRE)

1.25%

1%

CRE – Residential Housing

1%

0.75%

Other projects

1%

0.40%

DCCO deferred projects:

Additional provisioning to be maintained depending on the type of project:0.375% per quarter for infra projects0.5625% per quarter for non-infra projects

NPA project finance accounts

As per extant instructions

Provisionig for existing projects

Continued to be governed by extant norms;If resolution is done for any fresh credit event or change in terms occur after the effective date of these directions, then provisioning as per these Directions

RBI’s draft proposal for lower risk-weights for high quality infrastructure projects

The RBI has issued a draft amendment to the Scale Based Regulations, 2023 on 27th October, 2025, proposing a lower risk weight framework for ‘High-Quality Infrastructure Projects’. Once finalised, the provisions would be applicable from April 1, 2026, or from an earlier date when adopted by an NBFC in entirety. The intent of the amendment is to recognise and incentivise lending to stable, well-performing infrastructure projects by prescribing reduced risk weights for such exposures. Under the draft, “High-Quality Infrastructure Projects” are defined as infrastructure projects meeting all of the following conditions:

The project has completed at least one year of satisfactory operations post achievement of the actual DCCO;

The exposure is classified as ‘standard’ in the books of the lender;

The obligor’s revenue depend on one main primary counterparty, which shall be the Central Government or a Public Sector Entity, and the contractual terms ensure certainty of payment, such as through availability-based1 or take-or-pay arrangements2;

The contractual provisions offer strong creditor protection such as escrow of cash flows, legal first charge on project assets and other appropriate safeguards in case of early termination;

The obligor has adequate internal or external funding arrangements to meet current and future working capital or other funding needs, as assessed by the lender;

The obligor is restricted from undertaking actions detrimental to creditors, such as raising additional debt secured by the project’s cash flows or assets without lender’s consent.

Projects meeting all of the above criteria will qualify as high-quality infrastructure assets and will attract lower risk weights, as follows:

50%, where the obligor has repaid at least 10% of the sanctioned amount;

75%, where the obligor has repaid at least 5% but less than 10% of the sanctioned amount.

If a project subsequently fails to meet any of the qualifying conditions, it will cease to be treated as a high-quality asset and will instead attract the standard risk weight of 100% applicable to regular infrastructure exposures.

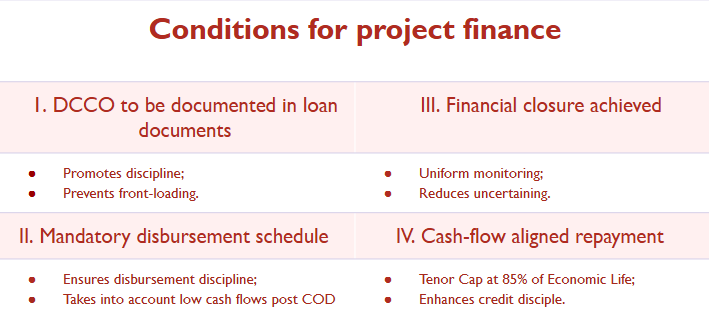

Conditions of project finance

The onus is on the lender to ensure that the following conditions are met before extending any project finance. These conditions will ensure that the facility is structured prudently and is aligned with the implementation as well as cash flows of the project, thereby mitigating both credit as well as project risk. The requirements are more or less similar to the earlier Directions.

Repayment schedule during operational phase is designed to factor initial cash flows

Repayment tenor, including the moratorium period, if any, shall not exceed 85% of the economic life of a project.

This means there is a mandatory 15% tail period i.e. if the project has an economic life of 20 years and the loans are to be repaid in 17 years, the last 3 years are the tail period.Tail period gives comfort to the lender that in case of any default or delay in repayment by the time of maturity, there is still some period left to recover dues from the project cash flows after the scheduled loan maturity.

Would this mean that a borrower cannot obtain a top-up loan after the expiry of 85% of the loan tenure?

The requirement applies to loans with all kinds of tenures, either short or long.

One borrower, multiple lenders

If a project is financed by more than one lender, RBI mandates that the DCCO, whether original, extended or actual, shall be the same across all lenders. This will ensure that:

DCCO is uniform across all lenders

Project progress as well as any delays are uniform across all lenders

Uniform asset classification, preventing any lender from having a different provisioning status.

To ensure balanced risk sharing, the Directions have put consortium lending limits (Para 15): Where projects are under-construction:

Aggregate exposure of all lenders is ≤ ₹1,500 crore: each lender shall hold at least 10% of total exposure;

For projects with exposure > ₹1,500 crore: each lender must hold at least 5% or ₹150 crore, whichever is higher.

These caps essentially require participating lenders to hold sufficient skin in the game and thereby promote responsible credit appraisal as well as avoid risk from being concentrated in a few lenders, especially where other lenders have negligible exposure and hence, less incentive to ensure monitoring.

Inter-lender transfer

These minimum exposure norms will not apply to operational phase projects;

In design or construction phase, lenders are permitted buy/sell exposure only under syndication arrangements as per TLE, and within the exposure limits

In operational phase, exposures can be freely transferred as per TLE norms.

This may be because construction and pre-operational stages are inherently more uncertain and riskier, and therefore, the regulator requires lenders who are willing to remain committed and not exit easily to avoid creating instability.

Project lifecycle – 3 different phases

A project has been divided into 3 phased viz Design, Construction and Operational.

Why does this classification matter?

The regulatory framework treats each phase differently for various risk, compliance and prudential reasons.

Disbursement discipline (Para 21)

Disbursal of funds must be linked to project completion milestones i.e. completion of phases.

Lenders must also track progress in equity infusion and other financing sources as agreed at financial closure

Asset classification (Para 22 & 29)

In design and construction phases, loans can be classified as NPA based on recovery performance, as per IRACP norms.

Once an account is classified as NPA, it can only be upgraded after demonstrating satisfactory performance during the operational phase

Resolution trigger (Para 23)

If any credit event (e.g., default) occurs with any lender during the construction phase, a collective resolution process is triggered

Provisioning norms (Para 32)

Provisioning rates are higher for projects under construction

Once the project enters the operational phase, provisioning reduces, reflecting lower credit risk.

Mandatory requirements before sanctioning a project finance loan: (13)

Achievement of financial closure and documentation of original DCCO;

Project specific disbursement schedule vis a vis stage of completion is included in loan agreement

Post DCCO repayment schedule designed to factor initial cash flows

Prudential conditions related to disbursement and monitoring:

Lender to ensure the following:

Clearances are obtained by the lender:

All requisite approvals/clearances for implementing/constructing the project are obtained before financial closure.(examples: environmental clearance, legal clearance, regulatory clearances, etc.)

Approvals/clearances contingent upon achievement of certain milestones would be deemed to be applicable when such milestones are achieved.

Availability of sufficient (prescribed) minimum land/right of way with the lender before disbursal of funds

This would mean that lender must ensure that the builder executing the project has either:

Ownership of the land (through purchase, lease etc.) or

Legal rights to use/access the land i.e. Right of Way.

For PPP projects, disbursal of funds to occur only after declaration of the appointed date.

Except where non-fund based facilities are mandated by the concessioning authority as a pre-requisite for declaration of the appointed date itself;

Disbursal to be proportionate

To stages of completion of project, infusion of equity or other sources of finance and receipt of clearances

Lender’s Independent Engineer/Architect to certify the stages

Creation and maintenance of a project finance database (see para 37):

Every lender to capture and maintain, on an ongoing basis, project specific information relating to:

Debtor and project profile;

Change in DCCO;

Credit events other than deferment of DCCO;

Specifications of project

Any updation shall be made within 15 days from any change in information;

Necessary systems to be placed within 3 months from the effective date ie by 1st January, 2026

Resolution of Project Loans

Prudential norms for resolution

Lender to monitor performance of project on on-going basis;

Expected to initiate a resolution plan well in advance.

Collective resolution to be initiated by the lenders in case credit event happens with any one lender

In case of any credit event;

Lender to report the same:

to the Central Repository of Information on Large Credit and;

to all other lenders, in case of consortium lending.

Lender to take a review of debtor account within 30 days.

Inter creditor agreement and decision to implement a resolution plan may be done during this period.

Implement the resolution plan within 180 days from the end of the review period.

Resolution plans involving extension of DCCO

Paragraphs 26 to 28 provide a structured framework under which project loans may continue to be classified as ‘standard’ despite delays in project completion, provided specific conditions are met. The objective is to offer flexibility to lenders and borrowers in addressing genuine project delays or cost escalations, without triggering an immediate downgrade to NPA so long as the resolution is timely and prudently implemented.

Permitted DCCO deferment

The DCCO may be deferred, with a corresponding adjustment in the repayment schedule. However, such deferment is subject to the following maximum limits:

Up to 3 years for infrastructure projects

Up to 2 years for non-infrastructure projects (including commercial real estate)

Cost overrun associated with the DCCO deferment:

A cap of 10% of the original project cost, over and above Interest During Construction (IDC)

The overrun must be financed through a Standby Credit Facility sanctioned at the time of financial closure

Post-funding, key financial metrics such as the Debt-Equity ratio and credit rating must remain unchanged or show improvement in favour of the lender

Deferment in DCCO associated with change in scope and size

Rise in project cost (excluding cost overrun) is at least 25% or more of the original project outlay

Reassessment of project viability by the lender before approving the revised scope and DCCO

If the project has an existing credit rating, the new rating must not deteriorate by more than one notch; if unrated and aggregate lender exposure is ₹100 crore or more, the revised project must obtain an investment-grade rating

This benefit of maintaining ‘Standard’ classification due to a change in scope can be availed only once during the project’s life

Resolution plan (‘RP’) deemed successfully implemented only if:

Necessary documentation completed within 180 days from the end of the Review Period and;

Revised capital structure and financing terms are duly reflected in the books of both the lender and the borrower.

Immediate downgrading to NPA if the resolution plan is not implemented within the timeline and conditions above

Once NPA, account can be upgraded only after:

Satisfactory performance post actual DCCO, in case of non-compliance with conditions of resolution plan;

Successful implementation of resolution plan, in case of non-implementation of RP within the specified time.

See a detailed PPT on the Project Finance Directions here

A contractual model where the project earns fixed payments from the counterparty based on the asset’s availability and performance, irrespective of actual usage or demand ↩︎

A contract under which the buyer agrees to pay for a specified quantity of output (e.g., power, gas, water) whether or not it actually takes delivery, ensuring predictable cash flows for the project. ↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-23 16:44:502025-10-28 18:11:30Balancing flexibility and discipline: Analysis of RBI’s Project Finance Directions, 2025

Alternative Investment Funds (AIFs) have come up as a regulators’ favourite in the recent years with both SEBI and RBI tightening regulatory controls around the same within their respective domains. The use of AIF as regulatory arbitrage in recent years calls for such strict regulatory boundaries. The growth of AIFs appears quite decent, with statistics showing a cumulative investment of Rs. 5.38 lac crores made by AIFs, against Rs. 5.63 lac crores of funds raised (as on 31st March, 2025). Compared to the market size as at the end of 31st March, 2023, the market has grown by more than 50% as at the end of 31st March, 2025. Category II AIFs occupy the highest share, with Category III AIFs following suit. As the market size increases, so does the regulatory supervision.

This article deals with the regulatory requirements for AIFs that find their first-time mandatory applicability during FY 25-26, and would form a part of the Compliance Test Report (CTR) to be issued for FY 25-26 (see later part of this article).

Certification requirements for key investment team of Manager of AIF

Vide a 2023 amendment, the active schemes of AIFs as on 13th May, 2024 and those launched on or after 10th May, 2024 are required to have at least one key personnel in the key investment team of its Manager, with relevant certification as specified by SEBI. The NISM certification requirement, prescribed on 13th May, 2024, as extended, is required to be complied latest by 31st July, 2025.

Holding investments in dematerialised form

AIFs have been mandated to hold investments in dematerialised form, subject to certain relaxations. The timelines, as extended videcircular dated 14th February, 2025, attract dematerialisation requirements as below:

Date of investment by AIF

Applicability of dematerialisation

Inapplicability of dematerialisation

Dematerialisation to be ensured by

On or after 1st July, 2025

Mandatory

Scheme of an AIF whose: Tenure ends on or before 31st October, 2025 orExtended tenure as on 14th February, 2025

Immediately

Prior to 1st July, 2025

Not applicable, except: If investee company is mandated under applicable law to facilitate dematerialisation (for e.g. – CA, 2013 requires mandatory dematerialisation of shares except in case of small company or WoS of public company etc)AIF exercises control over the investee company, either on its own or along with other SEBI regd. intermediaries mandated to hold investments in demat form

On or before 31st October, 2025

Due diligence of investors and investments of AIF

An April 2024 amendment to the AIF Regulations, followed by a circular dated 8th October, 2024 read with the Implementation Standards formulated by the Standard Setting Forum for AIFs (‘SFA’) requires an AIF to carry out various due diligence checks through its Manager and its Key Management Personnel (KMP) with respect to investors and investments of the AIF, to prevent facilitation of circumvention of the specified regulatory frameworks. The scope and requirements for the due diligence has been detailed in our article and further elaborated in the form of FAQs (read here).

In addition to the ongoing due diligence requirements, a one-time due diligence was required for existing investments as on the date of the Circular (8th October, 2024), the report of which was required to be submitted to the custodian on or before 7th April, 2025.

Cybersecurity and Cyber Resilience Framework (CSCRF)

The Cybersecurity and Cyber Resilience Framework (CSCRF), notified vide the circular dated 20th August, 2024 as revised vide the circular dated 30th April, 2025, categorises AIFs based on the AUM at manager level. Accordingly, the following categorisation follows:

Corpus of all AIFs, VCFs and their schemes managed by a manager

Categorisation under CSCRF

> Rs. 10000 crores

Mid-size REs

3000 crores < AUM < 10000 crores

Small-size REs

< Rs. 3000 crores

Self-certification REs

The classification w.r.t. Qualified REs (the topmost categorisation) does not apply in case of AIFs.

The timeline for compliance with the requirements as per the CSCRF is 30th June, 2025 (as extended by the circular dated 28th March, 2025) based on which cyber audit is to be conducted from FY 25-26 and the report shall be submitted to SEBI.

Consequence of non-compliance: negative reporting in Compliance Test Report

The manager of AIF is required to report the compliances with various applicable provisions of the AIF Regulations read with the circulars made thereunder, on an annual basis. CTR is submitted within 30 days from the end of the financial year, to the sponsor and trustee (in case AIF is set up as a trust). The trustee/ sponsor provides their comments on the CTR to the manager within 30 days from the receipt of CTR, based on which the manager shall make necessary changes and provide a response within the next 15 days.

A significant aspect of the CTR is that any violation observed by the trustee/ sponsor is required to be intimated to SEBI, as soon as possible.

RBI, through a series of circulars (dated 19th December 2023 and 27th March 2024 respectively), regulates the investments made by the RBI-regulated entities in AIFs, putting a prohibition on the regulated entities from making investments in any scheme of AIFs which has downstream investments either directly or indirectly in a debtor company of such an entity. Draft Directions have been issued recently, proposing to permit investments by RBI-regulated entities upto a certain percentage of the corpus of the AIF scheme. Read more about the same here. Once notified, the same would relax the investment norms for RBI regulated entities in AIFs.

Further, SEBI has, in its meeting held on 18th June 2025, approved certain amendments for AIFs, particularly for angel funds. This aims to strengthen the regulatory regime around investments by angel funds considering the abolishment of angel tax in India, while also relaxing certain investment norms by such angel funds. Further, SEBI has approved co-investment schemes that may be offered by Cat I and Cat II AIFs, facilitating co-investment to accredited investors of a particular scheme of an AIF, in unlisted securities of an investee company where the scheme of the AIF is making investment or has invested. The AIF Regulations presently permits co-investments through a co-investment portfolio manager.

Thus, the approach of regulators seems to be gradually softening, attempting to bring a balance between regulatory supervision and ease of business considerations.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-21 18:54:072025-06-21 18:54:08Regulatory landscape for AIFs: what’s new?

– Easing ESOPs for IPO-bound companies, relaxations to SEBI regd. intermediaries, providing clarity for uniformity of practices

– Team Corplaw | corplaw@vinodkothari.com

Various proposals have been approved by SEBI in its Board meeting dated June 18, 2025, pertaining to various relevant regulations. The approved changes may impact various market participants – listed entities as well as IPO-bound companies, SEBI registered intermediaries and regulated entities such as REITs, Invits, AIFs, FPIs, etc. We briefly discuss some of the important proposals as approved by SEBI.

Relief for promoters in IPO-bound companies: easing rules on ESOPs and offer for sale

Relaxation in eligibility norms with respect to Offer for Sale (OFS) in IPO (see Consultation Paper here)

Exemption from minimum holding period of 1 year extended to equity shares arising from conversion of Compulsory Convertible Securities (CCS), where such CCS were acquired pursuant to an approved scheme (earlier limited to equity shares) to assist in reverse flipping (i.e. shifting the country of incorporation from a foreign jurisdiction to India) [Reg 8 & 105 of ICDR Regulations].

Enabling Minimum Promoter Contribution (MPC) by Relevant Persons (apart from promoter) through equity shares arising from conversion of fully paid-up CCS

Relevant Persons comprise of AIFs, FVCIs, Scheduled Commercial Banks, PFIs, insurance cos etc.

Founders-turned-promoters can retain share based benefits, ESOPs granted 1 year prior to filing of DRHP (see Consultation Paper here)

Brings relaxation for treatment of options granted prior to becoming a promoter, which was otherwise required to be liquidated

Dematerialisation of shares: pre-IPO and post-listing requirements

Mandatory dematerialization of securities held by critical pre-IPO shareholders before filing of DRHP (see Consultation Paper here):

Following categories covered:

Promoter Group

KMPs

Directors

Employees

Selling Shareholders

QIBs

Senior Management

Financial sector entities

To reduce volume of physical shares

CA, 2013 also requires mandatory dematerialisation of holding of promoters, directors and KMP of companies prior to undertaking any share based corporate action [Rule 9A and 9B of Companies (Prospectus and Allotment of Securities) Rules]

Corporate actions by listed entities in dematerialised form only

For shares to be issued pursuant to consolidation/split of face value of securities and scheme of arrangements

CA, 2013 already requires companies to issue shares in dematerialised form only

Fund raising mandatory for social enterprises registered with SSE, relaxations in eligibility conditions for registration

Mandatory fund raising through SSE

Registration to lapse if social enterprise registered with SSE does not raise funds within 2 years from registration

Definition of “Not for Profit Organization” expanded [Reg 292A(e) of ICDR]

Trusts registered under Indian Registration Act, 1908 permitted (extant regulations refer to Indian Trusts Act, 1882 and a trust registered under the public trust statute of the relevant state)

Charitable society registered under relevant state Act (extant regulations covered only society registered under the Societies Registration Act, 1860)

Companies registered under Section 25 of the erstwhile Companies Act, 1956 (clarity provided since extant regulation refers to section 8 of 2013 Act)

List of eligible activities expanded to align with Schedule VII of the Act, 2013 (pertaining to CSR activities)

Criteria of 67% of total activities reflecting in eligible activities (through revenues, expenditure or total customer base) relaxed

To be applicable only to “for profit social enterprises”

Annual disclosures bifurcated into financial and non-financial disclosures

Different timelines to be prescribed for such disclosures

CP prescribes the extant 60 days’ period for non-financial disclosures, and upto 31st October after end of FY for financial disclosures

Self-reporting of Annual Impact Report instead of certification from Social Impact Assessor

For social enterprise that has not raised funds through the SSE

Change in nomenclature of “Social Impact Assessment Firm” to “Social Impact Assessment Organization”(SIAO) and eligibility conditions for the SIAO prescribed

SIAO to is permitted to conduct social impact assessment provided they have at least two social impact assessors in full time employment

Having an and such impact assessors have experience of at least 3 years of conducting social impact assessment.

Social impact assessor to sign the report if SIAO does not have 3 years’ track record

Revamping of regulatory framework for Angel Funds under AIF Regulations

Mandatory registration of Angel Investors as Accredited Investors(AI)

Attracts independent verification of investor status

Recent CP dated June 17, 2025 proposes certain flexibilities under the accreditation framework.

Grandfathering of earlier investments as non AI, and implementation through glide path

Accredited Investors included as Qualified Institutional Buyer in ICDR for investments in Angel Funds.

Relaxation in investment norms by angel funds in investee company

Floor and cap relaxed from Rs. 25 lacs to Rs. 10 lacs, and from Rs. 10 crores to Rs. 25 crores respectively

Concentration limits of 25% per investee company removed.

Follow on investments permitted in investee company, though may no longer be start-up

Scheme may now have more than 200 AIs

Minimum continuing interest of Sponsor/ Manager at investment level instead of Fund level

higher of 0.5% of investment amount or Rs. 50,000

Earlier the commitment was required to be maintained at a fund level only

SEBI regulated entities enabled to carry out activities not regulated by SEBI

Merchant Bankers and Debenture Trustees have been permitted to carry out activities not regulated by SEBI within the same legal entity subject to following conditions:

DT may undertake activity within the purview of any other financial sector regulator (FSR), subject to compliance with the regulatory framework specified by such regulator

For activities not within the purview of SEBI or other FSR, the same shall be fee-based and non-fund-based activity and pertain to FSR

Had been previously required to hive off such activities pursuant to SEBI Board Meeting decision in December, 2024

Custodians permitted to carry out other financial services under the regulatory oversight of other financial sector regulators within the same legal entity

subject to having adequate mechanisms to address issues of conflicts of interest

Non-bank associated custodians offering services which are not overseen by any financial sector regulator to :

Disclose clearly that such activities are outside the purview of, and without recourse to SEBI

Set up distinct strategic business units (SBUs) for undertaking activities not under the purview of SEBI with adequate mechanisms to address issues of conflicts of interest

Clarity of responsibilities and uniformity measures for DTs

Specifying rights of DT and corresponding obligations on issuer under LODR

To enable DT in enforcing its rights

Enabling provisions for providing format for model debenture trust deed (DTD) [Refer Annexure-1 of Consultation paper dated Nov 04, 2024 for the model DTD as proposed by SEBI]

Modification in manner of utilization of Recovery Expense Fund (REF) (see an article on REF here)

Elaboration of list of expenses for which REF can be utilised

To provide ease to DTs to take prompt action upon default by listed entity

Relaxations in regulatory norms for REITs and InvITs [see consultation paper dated May 02, 2025]

Definition of ‘public’ under REITs / InvITs to be amended to include related parties of the sponsor, investment manager/manager and project manager to qualify as public if such related parties are Qualified Institutional Buyers

Relevant for determination of minimum public holding

Related party of REIT/ InvIT viz. sponsor, sponsor group, investment manager, project manager are not regarded as ‘public’

Adjustment of negative net distributable cash flows generated by the Holdco against cash received from the SPVs

Net cash flow post adjustment to be distributed to unitholders

Alignment of timelines of submission of various reports including quarterly reports, valuation reports with the timelines for submission of financial results.

Reduction of minimum allotment lot for privately placed InVITs to INR 25 lacs from INR 1 crore to align with the trading lot in secondary market.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-21 12:05:272025-06-21 12:07:33SEBI approves a mix of reforms for regulated entities

A seemingly benign, innocuous and long standing definition of “promoter group” in SEBI (ICDR) Regulations, 2018 (‘ICDR Regulations’) is suddenly seeming to put to trial family relationships, by forcing spouse-side relations to share the details of entities owned by the spouse’s family – even when they have no stake or involvement in the listed company. Those entities will now have to be disclosed as a part of the “promoter group” entities of either family.

This definition has been there ever since in the ICDR Regulations, but the instant focus on the definition springs from SEBI FAQs dated April 23, 2025, on the disclosure of the entity forming part of the promoter group in terms of regulation 31(4) of LODR Regulations. This FAQ, being no. 19, assumes effect for the shareholding pattern due to be filed for the quarter ending June 2025 and onwards, and requires listed companies to disclose the names of all “promoter group” entities, irrespective of whether such persons or entities have any say or shares in the host company’s business.

Definition of Promoter Group

At the root of the issue lies in Regulation 2(1)(pp) of the ICDR Regulations, which defines “promoter group” to include “immediate relatives.” The term “immediate relatives” is further defined to include any spouse of that person, or any parent, brother, sister, or child of the person or of the spouse.

Spouse-side relations

The interpretational dilemma stems from the phrase “or of the spouse.” Does this qualify only the child of the spouse (the last relation mentioned), or extend to all relations of the spouse—i.e., the spouse’s parents, siblings, and children?

Spouse-side entities

The concern becomes more acute considering that any body corporate in which an immediate relative holds 20% or more equity must also be disclosed as part of the promoter group. If “immediate relative” includes all spouse-side relations, this leads to impractical over-disclosure – stretching the PG list way too far.

Is it sensible, or practical?

Consider the scenario where members of two distinct listed business families marry. Should both families – and their associated entities – be classified as part of each other’s promoter group, despite having no shareholding, control, or influence? This interpretation seems to stretch both logic and intent.

While reclassification under Regulation 31A of LODR may later be used, the very inclusion appears misplaced from the outset.

An interpretation of convenience: limit it to the child of the spouse

A more reasonable interpretation is to read “or of the spouse” as qualifying only the child of the spouse. This interpretation aligns with cases like a step-child, who is more likely to be financially dependent or influenced by the promoter / the spouse of the promoter.

Similar definition in other sebi regulations

Note that this phrase “or of the spouse” has been used in other sebi regulations as listed hereunder:

As per Regulation 2(1)(pp) of ICDR Regulations,

(pp) “promoter group” includes:

i) the promoter;

ii) an immediate relative of the promoter (i.e. any spouse of that person, or any parent, brother, sister or child of the person or of the spouse); and

As per Regulation 2(l) of the Takeover Regulations

(l) “immediate relative” means any spouse of a person, and includes parent, brother, sister or child of such person or of the spouse;

As per Regulation 2(f) of PIT Regulations

(f) “immediate relative” means a spouse of a person, and includes parent, sibling, and child of such person or of the spouse, any of whom is either dependent financially on such person, or consults such person in taking decisions relating to trading in securities;

Same phrase, different uses

While the same phrase “or of spouse” is used across various SEBI Regulations for defining “immediate relative”, the implications differ depending on the regulatory context.

Regulation reference

Immediate context

Consequent impact

ICDR

The definition of promoter group includes immediate relatives

Promoter Group: The list of promoter group does not end at listing out the immediate relatives. As per reg 2(1)(pp)(iv), all such entities where such immediate relative holds 20% stake of the equity share capital, also becomes part of the promoter group. In short, the longer the list of immediate relatives, the longer is the list of promoter group. Related Parties As per reg 2(zb) of LODR, all promoter and promoter group of a listed entity is a related party. Accordingly, this additional list of promoter group arising from spouse -side relations also becomes related party of the listed entity.

PIT Regulations

Immediate relative of the designated person (DP): The definition of immediate relative in PIT is coupled with specific conditions of such relative being financially dependent or consulting the DP for trading decisions

Such immediate relative is covered by the Code of Conduct to prevent insider trading in the securities of the listed entity and is required to comply with it.

Takeover Regulations

Immediate relatives are deemed to be ‘Persons acting in concert’ (PAC) with the promoter unless proven otherwise.

Transactions between the immediate relatives are exempted under regulation 10 of the Takeover Regulations.

While the purpose for each of the above may be different, however, the underlying regulatory rationale remains the same, i.e persons who are closely knit, by blood, marriage, or association (where there is commonality of objective and / or commonality of interest with the promoter group) – any action with respect to shareholding in the listed company among such person / by one of them, is to be treated as the action by the same PG.

Judicial precedents

In the informal guidance provided to Promoters of D B Corp Ltd, in relation to transfer of shares between ‘immediate relatives, SEBI provided that –

f) Further, as per the definition of ‘immediate relative’ stated above such term shall also mean any spouse of a person and shall include brother of the spouse. Therefore, the proposed transfers at para 4(b) also appears to be between entities who are ‘immediate relative.