SEBI approves the reduction of face value to Rs. 10000 for privately placed debt securities

Palak Jaiswani, Manager & Lavanya Tandon, Executive | corplaw@vinodkothari.com

Loading…

Loading…

Palak Jaiswani, Manager & Lavanya Tandon, Executive | corplaw@vinodkothari.com

Loading…

Insider Trading Regulations amended in line with Consultation Paper

Heta Mehta | Executive | corplaw@vinodkothari.com

The concept of Trading Plan (‘TP’) that existed since May 2015 continued to remain unpopular due to the stringent conditions laid down in the Insider Trading Regulations. The framework was set to be reviewed based on empirical evidence and feedback post introduction and determine if SEBI needs to dilute or increase the regulatory requirement. In order to make it more realistic and captivating, SEBI’s Working Group suggested reforms vide Consultation Paper dated 24th November, 2023[1] that was approved by SEBI in its board meeting held on March 15, 2024. SEBI (Prohibition of Insider Trading) (Second Amendment) Regulations, 2024 notified on June 25, 2024 will be effective from September 24, 2024. As a concept, it is not unique to India, globally, both the US and UK have similar TP concepts with some or the other variations when compared to our legislation. This article discusses the amendments, including the rationale provided in the CP, relevant points discussed in the SEBI Board meeting and our analysis on the same.

Read more →Team corplaw | corplaw@vinodkothari.com

Loading…

Refer to our related resources below:

Team Corplaw | corplaw@vinodkothari.com

Loading…

Also, refer to our related resources below:

| Register here |

Loading…

Other resources on the amendment:

Ankit Singh Mehar, Senior Executive and Khushi Hariyani, Executive | corplaw@vinodkothari.com

Loading…

Also see our related resources:

– This version: 21st May, 2024

Team Corplaw | corplaw@vinodkothari.com

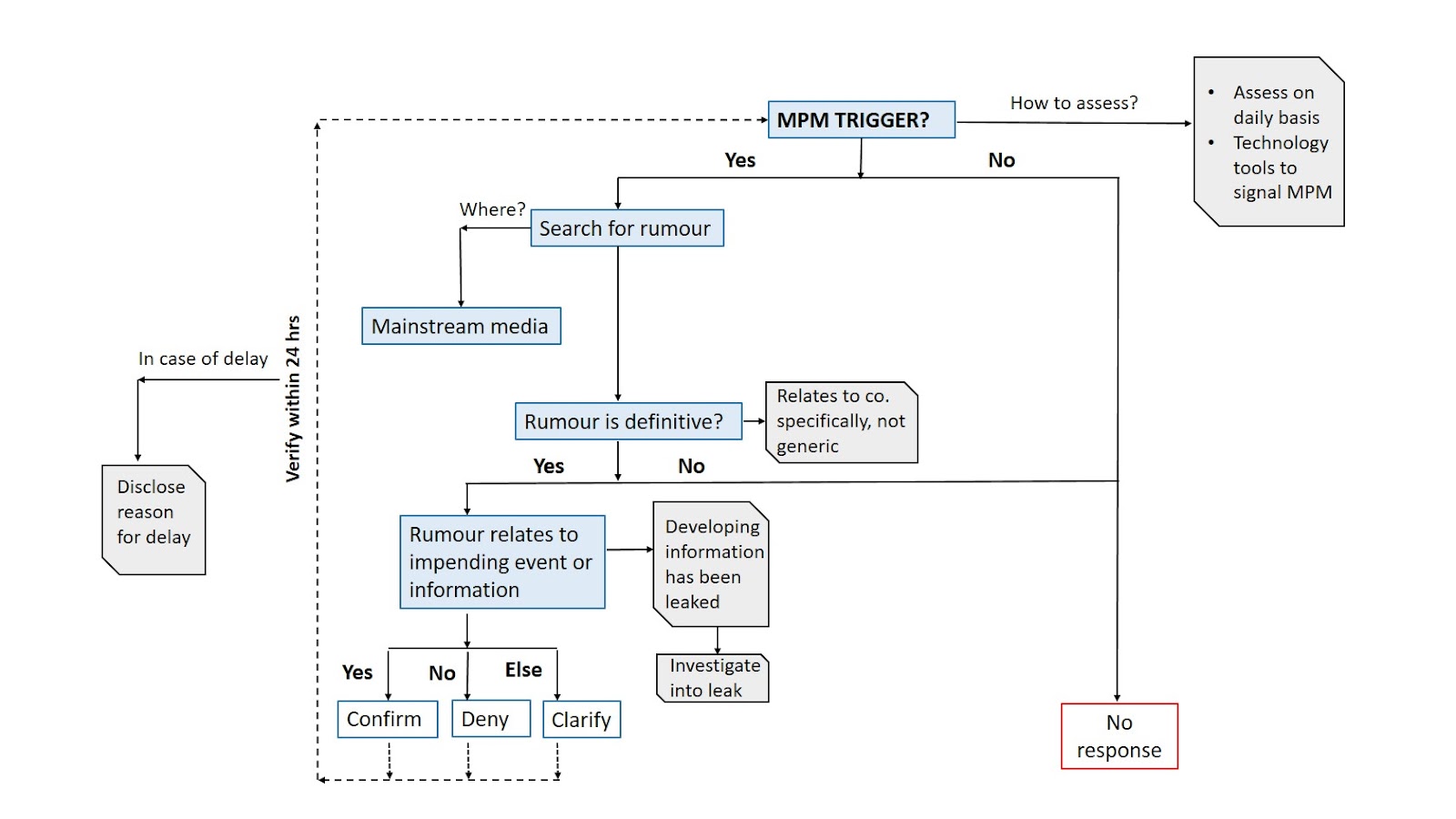

| Given the significance of the amendments, we are organizing an online workshop on Verification of Market Rumours by listed entities and other related amendments on Monday, 27th May, 2024. Details of workshop can be accessed here Register here |

Regulatory instruments and standards on rumour response:

What is the change? And applicable from when?

| Price range of the listed equity shares | Percentage variation in share price which shall be treated as material price | ||

| Benchmark index movement (+/-) is less than 1% at 9.30 am | Benchmark index movement (+/-) is greater than 1% at 9.30 am, and MPM is in the same direction as the Index change | In cases not covered by column on LHS | |

| Rs. 0 to 99.99 | ≥ 5% | ≥ 5% + % change in Benchmark index at 9:30 am) or Band hit | ≥ 5% |

| Rs. 100 to 199.99 | ≥ 4% | ≥4% + % change in Benchmark index at 9:30 am) or Band hit | ≥ 4% |

| Rs. 200 and above | ≥ 3% | ≥3% + % change in Benchmark index at 9:30 am) or Band hit | ≥ 3% |

[Note – Where a prior intimation of Board meeting of the company has been given under Reg 29 of LODR for such “impending” event or information, the company need not respond to the rumour till the conclusion of the Board meeting.]

In the Table below, we take few situations to understand the applicability of verification of market rumour:

| MPM | Impending specific event under reg. 30 | Rumour in mainstream media | Verification of rumour by company required? |

| Yes | Yes | Yes | Yes |

| Yes | No | Yes | Yes, as the existence of MPM by itself satisfies the condition for rumour verification |

| Yes | Yes | No | No, there is no rumour to be verified. The company may disclose based on the information/event reaching the appropriate stage. |

| Yes | No | No | There is no rumour to be verified. |

| No | Yes | Yes | Rumour verification is not required, but the general principles of disclosure of events or information at an appropriate stage will be followed. |

Also see our related resources:

– Mahak Agarwal | corplaw@vinodkothari.com

– Updated on December 13, 2025

The broad spectrum of the definition of Related Party Transactions (RPTs) under the Listing Regulation, continues to be an error prone area in terms of compliance. A recent SEBI ruling1 has further strengthens this aspect where the phrase ‘transfer of resources, services or obligations’ has been explained in an extremely new dimension with a commendable insight from the authorities which again shows that the regulators can no more be restricted by the imaginary boundaries placed by the corporates when it comes tightening the loose ends of corporate governance.

This article delves into the basis which the Regulators considered for concluding a mutual understanding and agreement between related parties to be an RPT notwithstanding the contention of the company. The essential question of law involved in this case was whether the allocation of certain products and geographic areas between RPs constitutes an RPT. The article contains our analysis of SEBI’s order and highlights the recent order passed by the SAT upon appeal in the matter, reaffirming the said stand.

Read more →SEBI mandates ongoing due diligence for investors and investments made by AIFs

-Vinita Nair, Senior Partner and Lavanya Tandon, Executive | corplaw@vinodkothari.com

May 03, 2024 (updated on October 9, 2024)

Background

SEBI had raised concerns relating to evergreening of loans, circumvention of FEMA norms, QIB regulations and other concerns on regulatory arbitrage by Alternative Investment Funds (‘AIFs’) in its Consultation Paper issued in January, 2024. SEBI also recorded 40+ cases wherein the structure of AIF had been abused and used to circumvent extant financial sector regulations. Read our analysis in the article ‘AIFs ail SEBI: Cannot be used for regulatory breach’ dated January 31, 2024. Further, RBI had also barred all regulated entities (REs) with respect to their investments in AIFs, discussed in our article.

Subsequent to receipt of public comments, the proposal to mandate due-diligence (‘DD’) of investors and each of the investments made by the AIF was approved in the SEBI Board meeting held on March 15, 2024. SEBI notified SEBI (Alternative Investment Funds) (Second Amendment) Regulations, 2024 effective from April 25, 2024 amending Reg. 20 of the SEBI (Alternative Investment Funds) Regulations, 2012 (‘AIF Regulations’) dealing with general obligations thereby requiring every a. AIF, b. investment manager of the AIF, c. KMP of the AIF, and d. KMP of the investment manager, to exercise specific DD with respect to their investors and investments in order to prevent facilitation of circumvention of such laws as may be specified by SEBI from time to time.

The list of laws, thresholds and conditions for DD, reporting requirements etc. has been provided in SEBI circular dated Oct 8, 2024 (‘SEBI Circular’). DD is required to be carried out prior to making of investments as per implementation standards formulated by Standard Setting Forum for AIFs (‘SFA’) and published on websites of the industry associations which are part of the SFA, i.e., Indian Venture and Alternate Capital Association (‘IVCA’), PE VC CFO Association and Trustee Association of India.

Scope of laws covered under the ambit of due diligence

The list of laws provided in the SEBI Circular comprises of the following:

Timing, thresholds for DD, reporting requirements

Pursuant to the SEBI Circular, the due diligence for various investors and investments is required to be carried out by a. AIF, b. investment manager of the AIF, c. KMP of the AIF, and d. KMP of the investment manager in accordance with the Implementation Standards. The table below indicates in brief the criteria, checkpoints and timelines for conducting due diligence along with the consequences of the outcome.

| Sr. No | Objective intended to be achieved by investors through investments in AIF scheme | Regulations/ Directions/ Norms applicable | Applicability of requirement of DD for every scheme of AIF (refer Note 1) | Checkpoints for manager for specific DD | Timing of DD | Consequence of outcome of DD & reporting requirements, if any |

|---|---|---|---|---|---|---|

| 1 | Benefits designated for QIBs | ICDR and other SEBI Regulations | If an investor, or investors belonging to the same group, contribute(s)50% or more to the corpus of the scheme. | Manager to check if such if investor/ investors of the same group is/are:(i) QIBs themselves or,(ii) Entities established, owned or controlled by the Central Government or a State Government or the Government of a foreign country, including central banks and sovereign wealth funds.Note: Where such investor is an AIF or fund set up in IFSC or outside India, above check to be carried out on a look through basis. | Prior to availing benefits available to QIBs | Refer Note 2 below for existing investments & Note 3 for proposed investments.Manager to provide confirmation to SE or lead manager or merchant banker on this. |

| 2 | Benefits designated for QBs | Under SARFAESI Act | If an investor, or investors belonging to the same group, contribute(s)50% or more to the corpus of the scheme. | Same as above | Prior to making any investments or availing benefits | Refer Note 2 below for existing investments & Note 3 for proposed investments. |

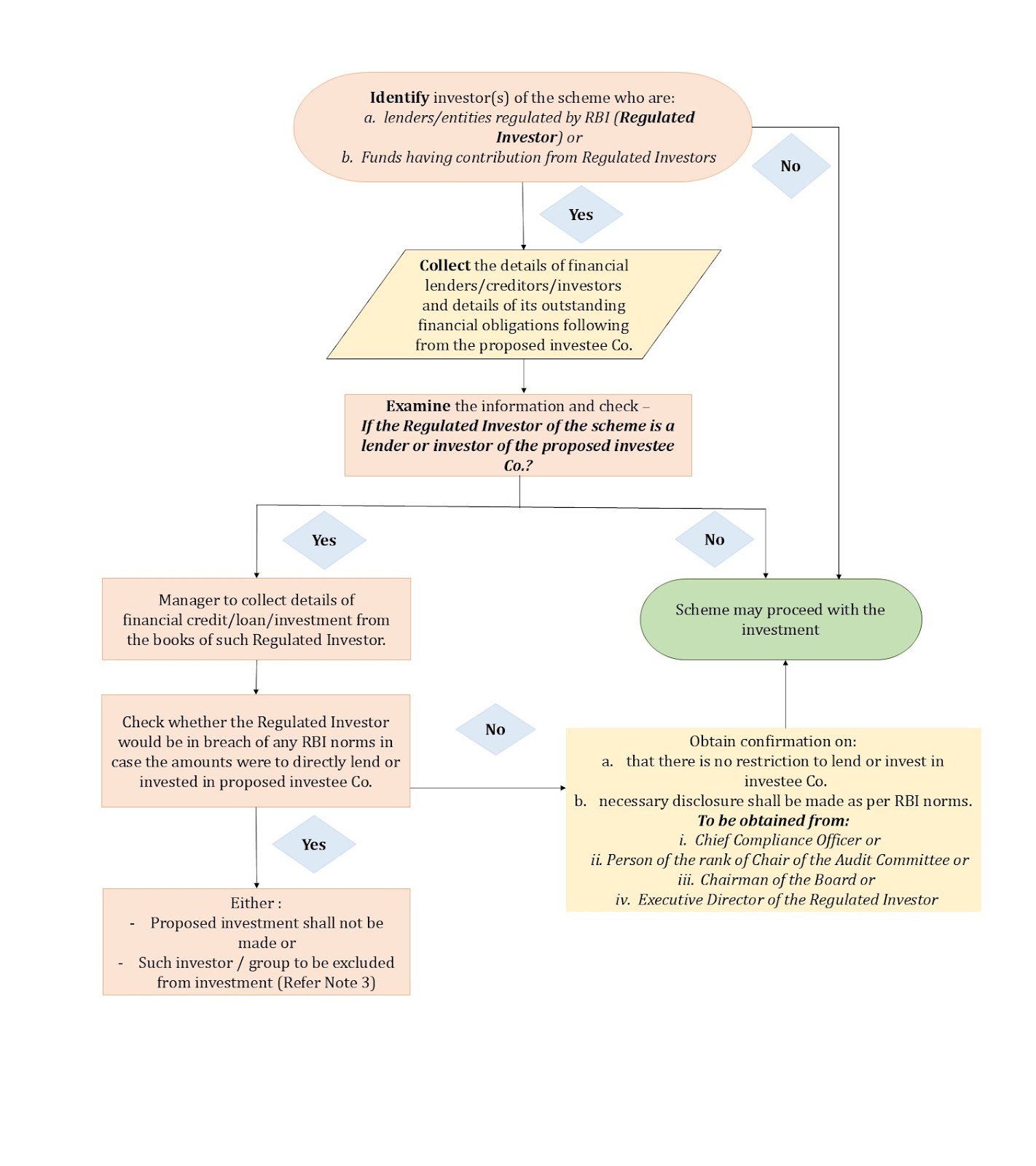

| 3 | RBI regulated lenders/ entities ever-greening their stressed loans/ assets & circumventing RBI norms | RBI norms on Income Recognition, Asset Classification, Provisioning and Restructuring of stressed loans/ assets | (a)whose manager or sponsor is an entity regulated by RBI; or,(b)that has investor(s)regulated by RBI who:(i)individually or along with investors of the same group contribute(s) 25% or more to the corpus of the scheme; or(ii) is an associate of the manager/ sponsor of the AIF;(iii) has majority or veto power [by itself, or through its representatives/ nominees] in voting over decisions of the investment committee set up by the manager to approve investment decisions of the scheme.Note: where investor is an AIF or fund set up in IFSC or outside India, criteria check to be carried out on a look through basis. | Refer Note 4. | Prior to making any investments, to avoid indirect investment by RBI regulated lender/ entity. | Refer Note 2 below for existing investments & Note 3 for proposed investments. |

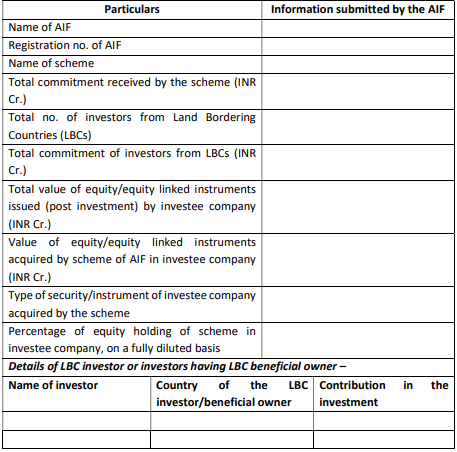

| 4 | Investment from countries sharing land border with India | FEMA (NDI) Rules, 2019 | Where 50% or more of the corpus of the scheme is contributed by investors (a)who are citizens of/are from/are situated in a country which shares land border with India; or(b)whose beneficial owners, as determined in terms of Rule 9 (3) of the PMLA (Maintenance of Records) Rules, 2005, are citizens of/are from/are situated in a country which shares a land border with India. | If the proposed investment would result in the scheme holding 10 % or more of equity/equity-linked securities issued by the company (on a fully-diluted basis), the manager to check details stated in the previous column, by collecting information on the country of investors and their beneficial owners. | Prior to making any investment | Refer Note 2 below for existing investments & Note 5 for proposed investments. |

Note 1: same group’ shall mean ‘related parties’ and ‘relatives’ as defined in SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

Note 2:

For Sr nos 1 to 3: DD requirement is applicable for existing investments too, held by AIF schemes as on October 8, 2024:

For Sr no. 4: Reporting is required to be made for existing investments held by AIF schemes as on October 8, 2024 if the scheme holds 10% or more of equity/ equity-linked securities on a fully-diluted basis, to AIF’s custodian on or before April 07, 2025 in the format prescribed by SFA.

Note 3:

Consequence of not satisfying requirements of DD checks specified by SFA for proposed investments in case of Sr nos 1 to 3:

Note 4:

Note 5: Details of investment, which would result in the scheme holding 10% or more of equity/ equity-linked securities on a fully-diluted basis, to be reported to the custodian within 30 days of investment, in the below format specified by SFA.

DD requirement – one-time or ongoing?

As discussed in the SEBI BM Agenda, the purpose of the due-diligence check is to prevent facilitation of any circumvention of provisions of financial sector regulators, which cannot be a time specific check. An entity who intends to circumvent can design the structure in such a way that, at a later date post investment, it acquires the units of AIFs post investment, such as buying the units of an existing investor or by acquiring control over the existing investor entity, as per prior arrangement. Accordingly, it has been indicated that due diligence around investors and investments will be an ongoing one.

Applicability of DD – prospective or retrospective?

As per the SEBI circular this is applicable for existing and prospective investments. Refer Note 2 above.

Obligations of Custodian to the AIF

Power of AIF to exclude an investor

As per SEBI Circular, in cases where the outcome of DD is not satisfactory, in that case the AIF will either have to exclude the investor or investor group or abstain from making the proposed investment.

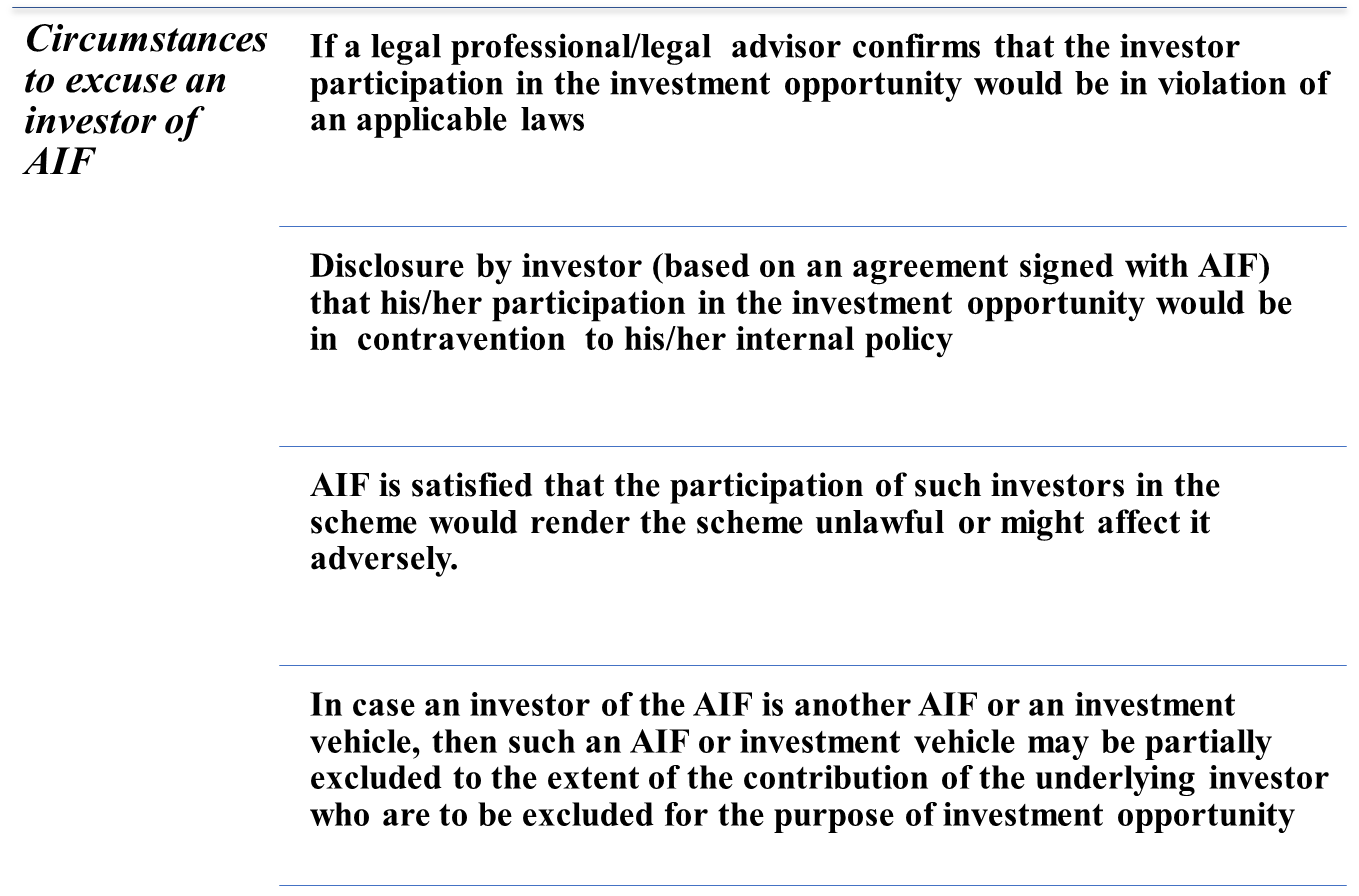

Dealing with power to exclude an investor, in April 2023 SEBI had issued ‘Guidelines with respect to excusing or excluding an investor from an investment of AIF that empowered an AIF to excuse its investor from participating in a particular investment in the following circumstances:

Figure 1: Circumstances to excuse an investor of AIF

Conclusion

The present amendment and SEBI Circular lays an onerous burden on the AIF, manager and KMP of the AIF and the manager. The DD requirement has become effective from October 8, 2024 and applies to existing investments as well. The AIFs have an actionable of evaluating the existing investments in the scheme in the light of the present amendment and ensure reporting in next 6 months. The obligation of on-going due diligence will result in a compliance burden, but is justified given the intent of law as “quando aliquid prohibetur ex directo, prohibetur et per obliquum” i.e. things that cannot be done directly should not be done indirectly either. AIFs will continue ‘trust, but verify’ using the DD standards for due diligence. The trustee/ sponsor of the AIF is required to ensure that compliance status of this amendment is reported to SEBI in the ‘Compliance Test Report’ prepared by the manager in terms of Chapter 15 of Master Circular for AIFs.

Our other resources: