Not sure if any cake was cut[1], but NBFC regulation turned 60, on 1st Feb., 2024. It was on 1st Feb., 1964 that the insertion of Chapter IIIB in the RBI Act was made effective. This is the chapter that gave the RBI statutory powers to register and regulate NBFCs.

1964: Insertion of regulatory power

What was the background to insertion of this regulatory power? Chapter IIIB was inserted by the Banking Law (Miscellaneous Provisions) Act, 1963. The text of the relevant Bill, 1963 gives the object of the amendment: “The existing enactments relating to banks do not provide for any control over companies or institutions, which, although they are not treated as banks, accept deposits from the general public or carry other business which is allied to banking. For ensuring more effective supervision and management of the monetary and credit system by the Reserve Bank, it is desirable that the Reserve Bank should be enabled to regulate the conditions on which deposits may be accepted by these non-banking companies or institutions. The Reserve Bank should also be empowered to give to any financial institution or institutions directions in respect of matters, in which the Reserve Bank, as the central banking institution of the country, may be interested from the point of view of the control of credit policy.”

Therefore, there were 2 major objectives – regulation of deposit-taking companies, and giving credit-creation connected directions, as these entities were engaged in quasi-banking activities.

On January 15, 2023, the Reserve Bank of India (RBI) published a draft Framework titled “Draft Framework for Self-Regulatory Organisation(s) in the Fintech Sector” (‘Framework’) with the objective of eliciting feedback and gauging stakeholder expectations. In this article we analyse the said Framework which in our view is targeted more towards the unregulated FinTech sector and recommend why an SRO should opt for a recognition from the RBI.

The FinTech sector is booming and is a market disruptor as well as facilitator, based on the report published by Inc42, the estimated market opportunity in India fintech is around $2.1 Tn+ and currently there are 23 FinTech “unicorns” with combined valuation of $74 Bn+ and 34 FinTech “soonicorns” with combined valuation of $12.7Bn+.

The main functions of the FinTech sector includes providing solutions to Regulated Entities (REs) both as outsourced information technology providers as well as acting as lending services (such as customer acquisition, KYC task, servicing, etc.). The sector, however, not being under the direct supervision of the RBI may pose significant risks toward customer protection, data privacy, cyber security, grievance handling, internal governance, financial system integrity. In this respect the introduction of the Framework of Self-Regulatory Organisation(s) in the FinTech Sector (SRO-Ft) remains a welcome move where the SRO-FT would act as an instrument of self-regulation for the market participants, which may include both regulated and unregulated entities, by coming out with its own policies, codes of conducts etc. which are aligned with the industry standards, best practices and expectations/ recommendations of the RBI and other sector regulators. However it should be noted that due to lack of legislation, the RBI does not have have any jurisdiction over the FinTech sector (Discussed in details in Section 2 of this Article) vis-a-vis their SRO, unless the SRO’s voluntarily submit to the jurisdiction of the RBI and the same has also been envisaged under Para 3 of the directions under the head “Introduction” of the draft Framework under discussion.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2024-01-24 16:53:062024-01-31 12:13:13Regulatory oversight over Self Regulatory Organisations in the Fintech Sector

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kothari Consultantshttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari Consultants2024-01-23 15:40:002024-02-05 13:19:40RBI (Commercial Paper and Non-Convertible Debentures of original or initial maturity upto one year) Directions, 2024

Reserve Bank of India (RBI) has recently announced amendments to the Credit and Investment concentration norms, specifically targeting Base and Middle Layer Non-Banking Financial Companies (NBFCs). The circular, dated January 15, 2024, brings about notable changes aimed at ensuring uniformity and consistency across NBFCs while computing the concentration norms.

What has RBI done?

For Middle Layer NBFCs (NBFC-MLs) :

In addition to the use of Credit Default Swaps (‘CDS’), RBI has now allowed NBFC MLs to offset the aggregate exposure with the following additional Credit Risk Transfer (CRT) instruments:

Cash margin/caution money/security deposit held as collateral on behalf of the borrower against the advances for which right to set off is available;

It is pertinent to note that, as per para 84 of the SBR Directions, already requires the NBFC for the purpose of assignment of risk weight to net off the amount of cash margin/ caution money/security deposits held as collateral against the advances out of the total outstanding exposure of the borrower.

Central Government guaranteed claims which attract 0 per cent risk weight for capital computation;

State Government guaranteed claims which attract 20 per cent risk weight for capital computation; and

Guarantees issued under Credit guarantee Schemes of Credit Guarantee Fund Trust for Micro and Small Enterprises, Credit Risk Guarantee Fund Trust for Low Income Housing and individual schemes under National Credit Guarantee Trustee Company Ltd

The Omnibus Framework is in response to a vacuum located between Regulators and the ever-evolving industry dynamic. The RBI had proposed a draft and later finalised the framework, for Self-Regulatory Organisations (SROs) indicating a willingness to enter a collaborative approach to regulatory frameworks.

The Omnibus Framework, taking the increasing number of regulated entities and their growing scale of business into consideration recognises the lack of sufficient industry standards for self-regulation. Identifying this need and being aware of the futility of increasing the burden on regulatory bodies like the RBI, SEBI, or IRDA, (in this case, specifically: the RBI) the framework finds a middle ground by recognising self-regulation amongst members of various industry entities.

What are Self-Regulatory Organisations? What do they Do?

Self-Regulatory Organisations (SRO) are not-for-profit organisations that attempt to bridge the gap between regulation and industry-specific requirements.

In the Indian context, the most popular example remains the Association of Mutual Funds India, or the AMFI, an entity incorporated under Section 8 of the Companies Act 2013 as a not-for-profit organisation with the stated intent to act as a facilitator between the Regulatory Body of SEBI/RBI/the Government of India and the Mutual Fund ecosystem. It also aims at formulating standards or “best practices” which shall in turn become the industry status quo for all members to follow and live by. The AMFI also acts as a licensing body for all Mutual Fund distributors in India as per the duties assigned to it by the SEBI.[1] MFIN (Mutual Fund Investment Network) is another example of a successful SRO infrastructure in India. With the emergence of the FinTech Sector in India: Section 8 companies like FACE and DLAI have cropped up with both significant membership and the aim to establish industry standards and Codes of Conduct. The current omnibus[2] offers these institutions the opportunity to get regulatory sanction from the RBI.

The Omnibus Framework defines its intent by stating:

“Self-Regulatory Organisations (SROs) enhance the effectiveness of regulations by drawing upon the technical expertise of practitioners and also aid in framing/ fine- tuning regulatory policies by providing inputs on technical & practical aspects, nuances and trade-offs involved. SROs can also help in fostering innovation, transparency, fair competition, and consumer protection. In sum, self-regulation shall complement the extant regulatory/ statutory framework for better compliance, in letter and spirit.”

To enable the SRO to fulfill the above obligations, the Omnibus Framework gives power to the SROs to frame necessary standards or codes within the regulatory framework prescribed by RBI. The adoption of the code, however, should not be a substitution for adhering to the necessary RBI Regulations.

What is the purpose of an SRO? Why do they exist?

As per the Omnibus Framework, SROs are expected to primarily act as an interface between the regulatory body and regulated entities. Thus, one of their primary duties extends toward collecting and providing relevant industry-specific data[3] to the Reserve Bank to aid more efficient policy making. Apart from this SROs are also expected to foster greater research, promote compliance practices, ensure inclusive development and effectively act as an industry representative before the regulatory body.

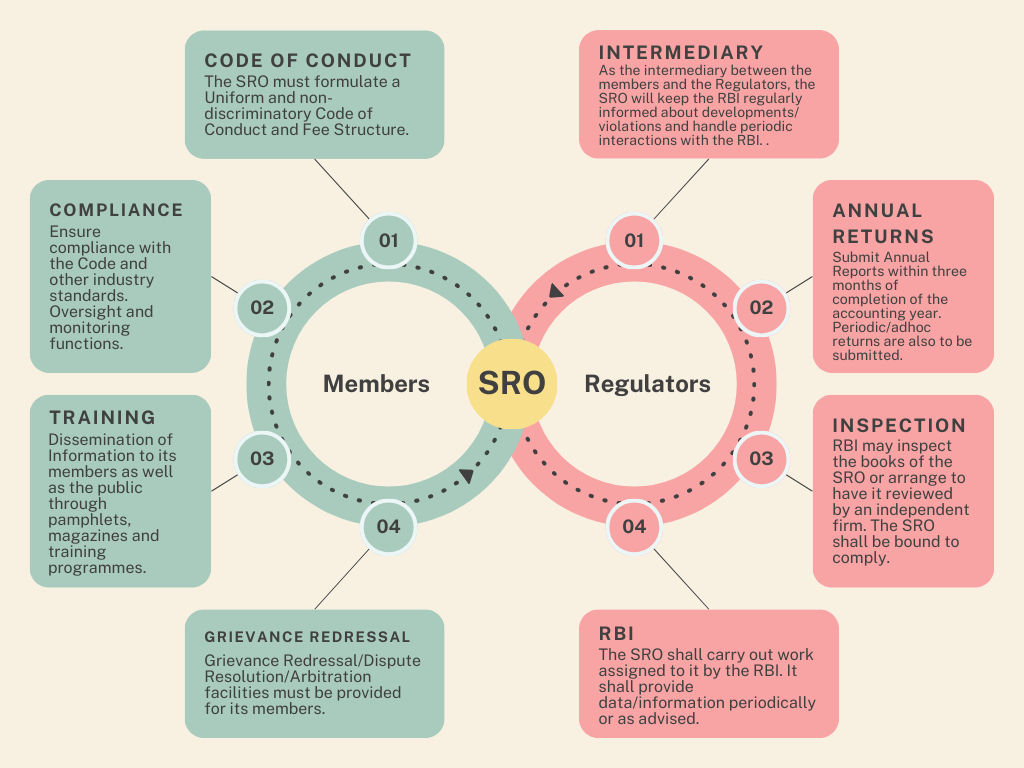

SROs have certain general objectives, as well as specific responsibilities to be undertaken toward both its members as well as the RBI that gives it its credibility. Their responsibilities can be construed in a trifecta of general and specific duties, with specific duties being toward their members and the regulatory body to whom they represent their members. The Omnibus Framework defines “members” as the Regulated Entities which accept the membership of SRO.

Figure 1 SRO General Objectives

[Clause(s) 6 and 7 of the Omnibus Framework]

Through the establishment of “best practices” and industry benchmarks that may be emulated by most if not all entities in a particular industry and recognising that it may be impossible for the average pedestrian to undertake thorough due diligence independently, the SRO acts as a “stamp of approval” toward the validity and trustworthiness of a particular entity. To ensure that the SRO in itself is reliable, they may be subject to periodic audits by the regulatory body, and are also required to submit their annual reports to the Reserve Bank within three months of completion of the accounting year.

They are also required to frame a code of conduct that should be adhered to by their members, provide periodic sector-specific information through bulletins, pamphlets and magazines to increase awareness amongst its members, establish grievance redressal and dispute resolution mechanisms for its members and also educate the public about the grievance redressal mechanisms available to them. The Omnibus Framework allows the SROs to counsel, caution, reprimand, and expel the members as a consequence of violation of the code established by it. However, such consequences cannot result in the imposition of a monetary penalty on the member.

Figure 2: Responsibilities Towards Members and Regulators

Clause(s) 8 and 9

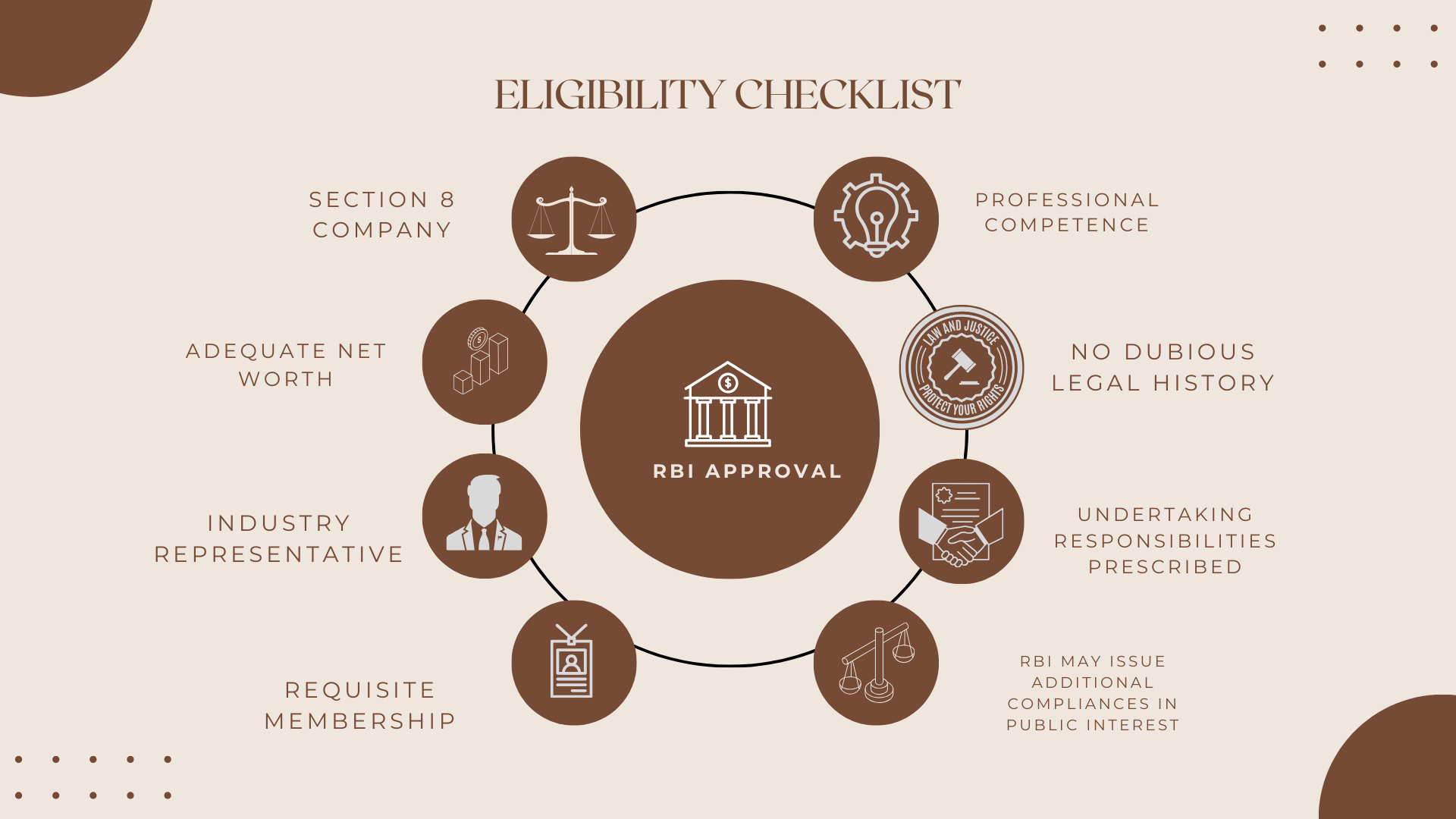

What are the eligibility criteria for forming an SRO?

Figure 3: Eligibility Criteria for SRO Recognition

Further, the Omnibus Framework specifies that the shareholding of an applicant should be sufficiently diversified. The applicant will not be eligible if an entity either singly or acting in concert holds 10% or more in the paid-up share capital of the applicant.

Who are the key stakeholders?

The RBI envisions the present omnibus primarily for entities regulated by the RBI. The SRO, once it receives its Letter of Recognition from the RBI will consequently impact the institutions/entities that comprise the sector it is representative of.

Thus, in the present context, some of the primary stakeholders are:

Banking and Financial Institutions: As the RBI framework is directly impacting regulated entities, the Banking and Financial Institutions Sector becomes the primary stakeholders as they need to ensure compliance with the new standards.

Industry Associations: As the Omnibus Framework aims to solemnise industry bodies and associations for responsible growth in the Financial Sector, these bodies will need to comply with the new framework. These bodies need to comply with the new standards as well as ensure that their members are similarly compliant. For e.g.:

DLAI (Digital Lenders Association of India): Comprising over 80 members and involved in over $5 Billion in annual disbursements, DLAI’s stated objective remains the support of development and best practices in the Digital Lending Industry.

FACE (FinTech Association for Consumer Empowerment): A Section 8 Company, stated to be a “Self-Regulatory industry body of fintech lenders” FACE aims to establish an ecosystem of responsible lending and borrowing.

Figure 4: Stakeholder Action Items

Regulated Entities are advised to proactively comply with emerging industry and governance standards, as well as emerging trends or shifts in interpretation of applicable guidelines/regulations/laws. It is recommended that REs promptly align with these standards, effectively articulate their challenges, and ensure full compliance to maintain industry integrity and operational excellence.

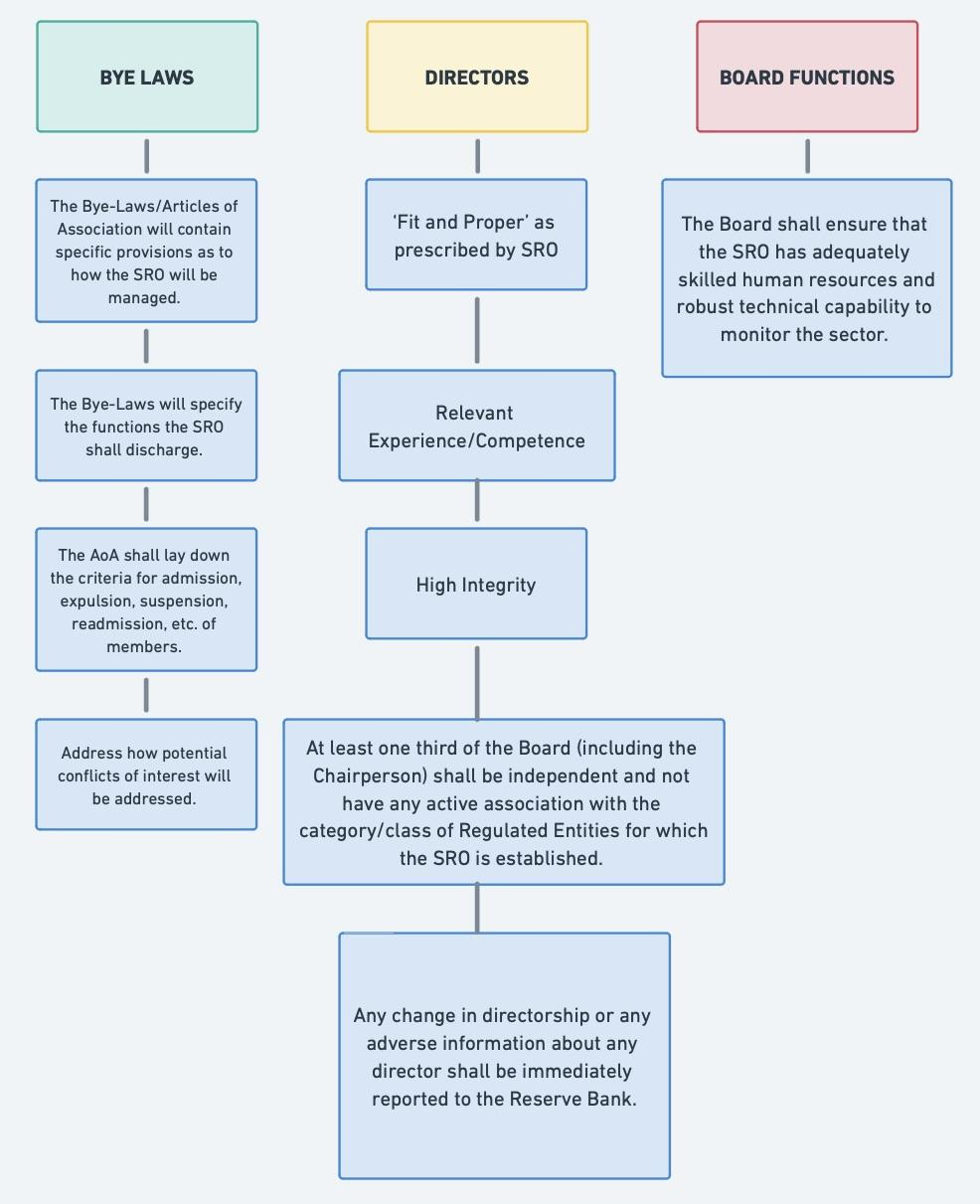

SRO Governance

To ensure a systemic and reliable mode of self-governance, and the ideal operational excellence envisioned above, the SRO in itself, must be reliable. Thus, SROs are subject to certain stringent governance standards.

Figure 5: SRO Governance Mechanism

The Omnibus Framework requires the Board of SROs to frame a policy on the rotation of directors for important positions in the Board of SROs.

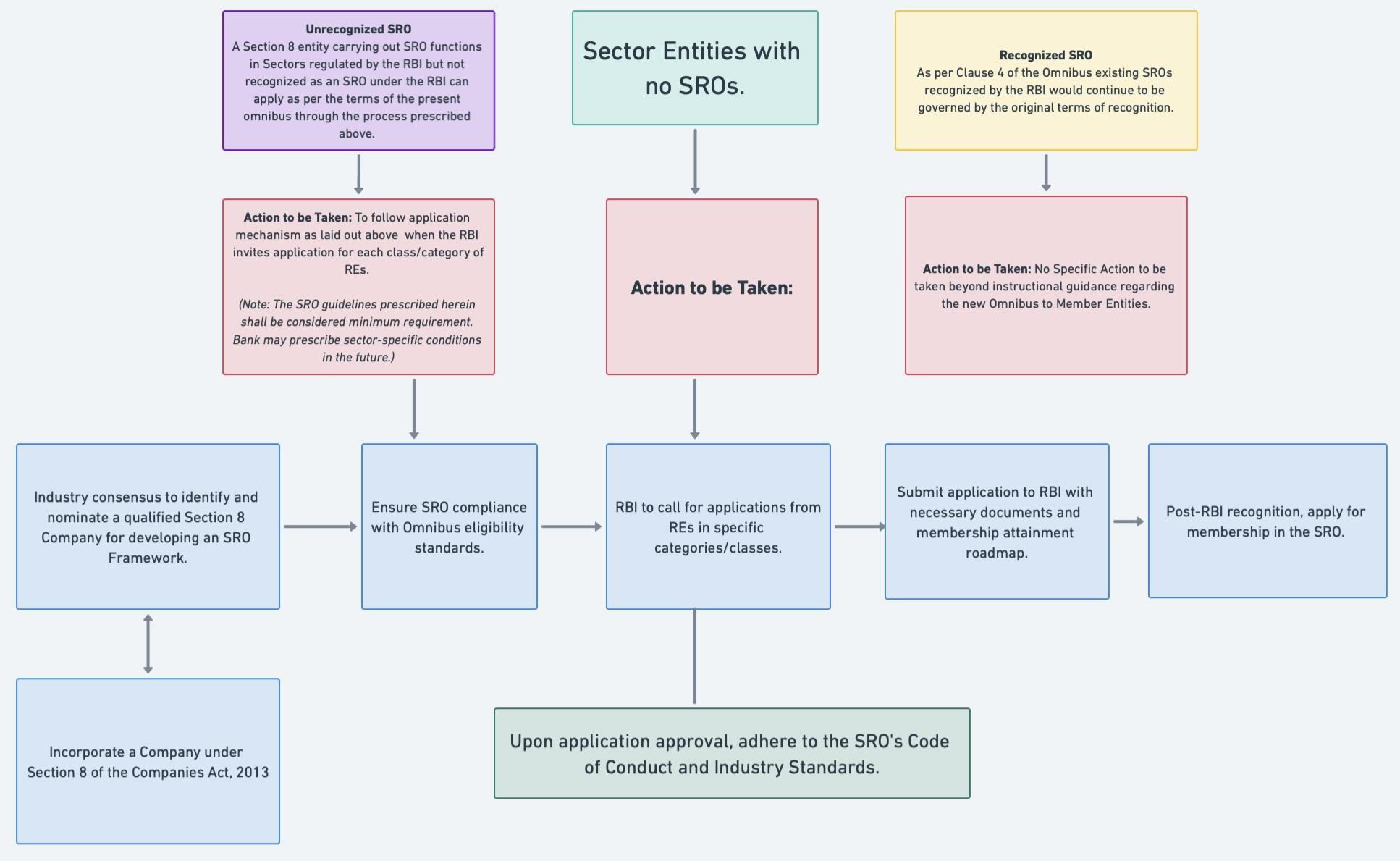

How does an entity get recognised as an SRO?

For an entity to be recognised as an SRO it must receive a “Letter of Recognition” from the Reserve Bank. To receive the same, it is required that the SRO submit certain documents to the RBI including but not limited to: A copy of its Memorandum of Association and Articles of Association, details regarding the constitution of its board: its duties, and mode of discharge of obligations. It shall contain the roadmap to achieve minimum membership as prescribed by the RBI within prescribed timelines (which shall not be greater than two years from the date of recognition) and any such further documents as may be necessary. Whilst membership should ideally be achieved by the time of application itself, if not, a clear roadmap on achieving the requisite membership should be provided. The RBI may stipulate a timeline (not exceeding two years) within which this should be achieved.

Membership in SROs shall be voluntary for the members.

Application that does not fulfil criteria liable to be rejected. A fifteen day window, commencing from date of dispatch of intimation from RBI, will be provided to the applicant for rectification.

Figure 6: SRO Application Process

Way forward:

In summary, SROs are the necessary bridge between the regulatory body and the industry. They represent the industry to the regulatory body and interpret directions issued by the regulatory body to the industry so as to ensure consensus and uniformity in interpretation.

Whilst the Omnibus Framework is fairly comprehensive and takes most relevant factors into account, some clarifications and further considerations are required as presented herein:

There is no specific provision as to how many SROs shall be recognised per sector/vertical. As the objective of the SRO is primarily to act as a facilitator between industry bodies, ensure consensus in interpretation and represent the interests of the industry before regulatory bodies, the objective may be defeated if the sector is populated by too many SROs. This issue warrants more comprehensive and detailed attention.

The Omnibus Framework characterises the relationship between the SRO and RBI as an “allyship”. However, further clarification is necessary to define the specific terms and nature of this relationship.

It is essential to clearly delineate the status of Section 8 Companies that undertake SRO functions but fail to secure recognition from the RBI, ensuring a comprehensive understanding of the implications and subsequent procedural actions.

Introducing a mechanism whereby SROs shall grant accreditation to compliant members could also be beneficial and serve dual purposes: it would incentivise new members to join and simultaneously enhance the SRO’s credibility. This practice could also foster an atmosphere of competitive excellence in governance.

It is also imperative that issues of conflict of interest are comprehensively and meticulously addressed to pre-empt potential challenges and maintain operational integrity

[1] However, it is to be noted that the current Omnibus does not make any specific mention of licensing activities that may be carried out by SROs in the future. At this stage it is difficult to predict whether licensing powers similar to AMFI will be granted to other SROs.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2024-01-17 12:30:552024-03-30 17:38:18Decoding the New Norm

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2024-01-01 20:39:172024-01-04 13:42:46RBI mandates appointment of an Internal Ombudsman by NBFCs

The Reserve Bank of India (RBI) on 28th December, 2023 issued a circular amending the Master Direction on Transfer of Loan Exposures (MD-TLE) to exempt the Minimum Holding Period (MHP) requirement in case of transfer of receivables arising from factoring business.

The circular further prescribes eligibility for exemption, providing that:

The residual maturity of the receivables at the time of transfer should not exceed 90 days; and

Proper credit appraisal of the drawee should have been conducted by the transferee as provided under clause 10 and 35 of MD-TLE

It shall further be noted that, factoring business, can only be undertaken by eligible regulated entities, hence the transferee’s in case of transfer of factoring receivables can be only be entities eligible for factoring business which are:

NBFC-Factors

NBFC-ICC having specific licence for carrying out factoring business; and

Entities identified under section 5 of the Factoring Regulation Act, 2011, viz. banks, and body corporates established under an Act of Parliament or State Legislature, or a Government Company

Before the specific amendment, a view could have been taken that factoring of receivables not being a loan, did not fall within the ambit of MD-TLE. The amendment has in a way clarified two things:

Transfer of factoring receivables shall be covered under the MD-TLE;

The MHP requirement shall not be applicable in case the residual maturity of receivables is less than 90 days.

In case the residual maturity is more than 90 days, the MHP shall be applicable along with all other provisions of the MD-TLE

Intent behind exemption from Minimum Holding Period requirement

In accordance with MD-TLE any transfer of economic interest in a loan account/pool by regulated entities could only be undertaken after a prescribed period of 3 months in case of loans with tenure less than 2 years and 6 months in case of other loans has elapsed. The intent being to restrict REs from originating loans with the sole intent to transfer the same.

The primary intent behind this amendment is to foster and enhance the secondary market operations associated with receivables acquired through ‘factoring business’. By exempting the MHP requirement for eligible transferors, RBI aims to encourage greater liquidity within the factoring industry.

Anticipated impact of the amendment

Promoting an active secondary market would attract more participants, specifically the secondary market would help REs to work on their core competencies, such as eligible NBFCs may be able to originate assets in their specific niche which can be then transferred to banks or other large NBFCss for utilising their low-cost pool of funds.

Factoring business in India has been an underperformer, removal of such bottlenecks shall help REs optimising their business and in turn facilitating easier working capital finance for MSMEs.

Conclusion

To provide a little thrust to lagging factoring business in India, RBI has exempted transfer of factoring receivables from the requirement of MHP under the MD-TLE

The said move can assist in larger participation and increased liquidity in the factoring industry.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Qasim Saifhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngQasim Saif2023-12-29 16:59:282023-12-29 16:59:29Transfer of factoring receivables exempted from MHP

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kotharihttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari2023-11-18 19:16:482023-11-18 19:16:48Workshop on RBI Circular on Regulatory Measures on Consumer Credit by Banks & NBFCs

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kothari Consultantshttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari Consultants2023-11-17 16:42:072023-11-17 17:11:27Workshop on RBI Circular on Regulatory Measures in Consumer Credit by Banks & NBFCs