By Saloni Mathur (finserv@vinodkothari.com)

Introduction

There has been a shift in the paradigm of the performance of the direct selling agents. The role and responsibilities of the direct selling agents have witnessed a revolution, where they are required to comply with certain codes as prescribed by the government from time to time, and follow certain practises while discharging their responsibilities. The RBI’s master directions[1]on the outsourcing norms have put stringent compliances on the service providers while discharging their functions, and increased responsibility and monitoring on the part of the non-banking financial companies. The question that arises here is whether those non- banking companies complying with the outsourcing guidelines, fall under the ambit of the direct selling guidelines also and if they, then what is the nature of the applicability of these direct selling guidelines on them.

According to a report on the Indian direct selling industry published by FICCI and KPMG, the direct selling market in India has grown at a CAGR of 16 per cent over the past five years to reach INR75 billion today.[2] Due to this unprecedented rise in direct selling industry and the growth of a large distribution base, major scams have been witnessed over the years in reputed companies owing to the nature of marketing methods adopted by them.

The Government of India, Ministry of consumer affairs, food and public distribution, department of consumer affairs, vide its notification number F.No.21/18/2014-IT (vol II) dated 09th September, 2016 modelled certain guidelines on the direct selling regulating the business of direct selling and the multi-level marketing.

This article is an attempt to envisage the rationale behind these guidelines and the applicability of these guidelines on the direct selling agents and the various compliances that are required to be made by the direct selling entities and the direct sellers.[3] Further this article also takes into account the concept of Multi-level marketing and the pyramid schemes with reference to the applicability on the direct selling agents.

Rationale behind the launch of the Scheme

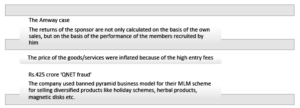

The direct selling industry has brought about with itself a huge reservoir of marketing, selling and distribution base for the goods and services, which has given rise to various fraudulent practises in the marketing and the distribution system. Instances can be drawn from the famous Amway and the Qnet case where entire money in the chain was earned only through the recruitment of new members and adding more participants to the channels of distribution, rather than the actual sale of the goods and services. Though the Amway was convicted of “illegal pyramid scheme” it could finally escape all criticism under the umbrella of the “the Amway safeguard rules”. However, the case has left strong marks of scepticism in the validity of the direct selling business.

The companies which were engaged in multi-level marketing were carrying out various frauds through the recruitment of large number of participants in the system. Thus, a need was felt where a robust system of direct selling guidelines was required to protect the interest of the consumers.

Defining the Pyramid and the MLM schemes

Defining the Pyramid Scheme

“Pyramid Scheme” as defined in the guidelines mean a multi layered network of subscribers to a scheme formed by subscribers enrolling one or more subscribers in order to receive any benefit, directly or indirectly, as a result of enrolment, action or performance of additional subscribers to the scheme. The subscribers enrolling further subscriber(s) occupy higher position and the enrolled subscriber(s) lower position, thus, with successive enrolments, they form multi-layered network of subscribers.

The key feature of the pyramid is that as the entrants in the last layer of the pyramid continue to get more and more participants who pay money. By way of this a hierarchy is created and the sponsor who holds the top most position is the recipient of the highest commission. The Amway case is the perfect example of the “illegal Pyramid scheme” where the purpose of the scheme was to make money through recruiting more distributors at various levels.

The pyramid scheme is illegal in India under the Prize chits and Money Circulation Schemes (banning) act, 1978. Hence there is a non-applicability of this scheme.

Following are some of the key constituents of the Pyramid Schemes

High registration fees

The basic quality of a pyramid scheme is that there is a high registration and entry fees upfront that the participants in the scheme have to pay. The entry fee is so high that the participants holding top position get a very high commission fees.

Goods sold at a price higher than the fair value and a higher quantity that is generally sold in the market

The goods and services under the pyramid schemes are not sold at the fair value. Fair value means the price at which the goods and services are generally available in the market. If the goods are sold to the consumers at a price higher than what is a general fair market price, it is a pyramid scheme. Similarly, if the goods are sold at a quantity higher than what is expected to be consumed by, or sold, resold to consumers, it will constitute to be a pyramid scheme. The price of the goods and services have a higher component of commission cost rather than the actual product price. The price of the product generally has 70% commission cost and remaining 30% cost of the product.

The level of unsold inventory

Under the pyramid schemes the unsold inventories of the participants is not generally brought back by the distributor.

Emphasis on the recruitment of more members

There is a greater emphasis on the recruitment of more members rather than promoting and distributing the product. The purpose here is to fetch higher commissions for the sponsors at the top most level.

No material contract between the direct selling entity and the direct seller

There is no material agreement entered between the direct selling entity and the direct seller on buy back, refund, repurchase policy of the unsold inventory.

No cooling off period

There is no cooling off period given to the direct sellers up to which they can cancel the contract.

Defining the Multi-level Marketing (MLM) scheme

In an MLM structure, multi-level marketing or the network marketing are used to sell the products directly to the consumers in which the salesmen are compensated not only for the work done by them but also for the sales of the people who have joined the company through them.[4]

The main purpose of the MLM scheme is to ensure wide distribution of the products or services and the intent is to sell the product through a network of wide range of distributors. Thus, it is just a marketing strategy unlike a fraudulent pyramid scheme where there are tangible distribution of the goods and services.

Comparing the MLM and the ‘Pyramid’

The big difference between multilevel marketing and a pyramid scheme is in the way the business operates. The entire purpose of a pyramid scheme is to get distributors’ money and then use it to recruit other distributors. The entire purpose of MLM is to move the product and ultimately achieve the sales of the product. The theory behind MLM is that the larger the network of distributors in a chain, the more products the business will be able to sell. Therefore, whether it is a pyramid scheme or an MLM approach depends upon the legality of the schemes and the purpose behind their operation as the Pyramid scheme is illegal.

Defining key concepts under the ‘direct selling guidelines 2016’

‘Direct selling’ has been clearly defined in regulation 6 which means marketing, distribution and the sale of the goods or providing of any services as a part of network of direct selling other than under a pyramid scheme.

Thus, what constitutes to be a direct selling is based on four conditions i.e direct selling has to be marketing, distribution, and selling of the goods and services as a part of network of direct selling. Thus all the four conditions need to be qualified simultaneously for determining direct selling. Thus, a direct selling agent, if restricts its services only to marketing of products and not to selling and distribution would not be required to comply with these guidelines.

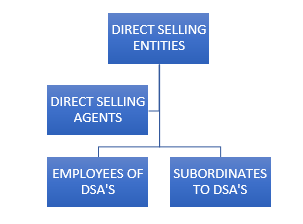

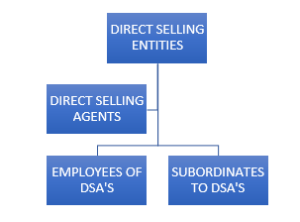

Similarly, the network is defined as an arrangement of intersecting horizontal and vertical lines. To be a network it is therefore necessary that there is a hierarchy of a direct selling agents such that there is a superior subordinate relationship at all levels of distribution

The ‘network of direct selling’ means a network of direct sellers at different levels of distribution who may recruit or sponsor further levels of the direct sellers, who they then support. “Network of direct selling” shall mean any system of distribution or marketing adopted by a direct selling entity to undertake direct selling business and shall include the multi-level marketing method of distribution.

This network of direct sellers also includes the multi-level marketing method of distribution.

Thus, network of direct selling shall be hierarchical. Single level of distribution would not constitute any network.

Comparing the network, the Pyramid and the MLM

The network may be at a horizontal level also. For example, if there is one direct selling entity selling goods and services through a single level of the direct sellers, all at the same level shall constitute a network. However, Pyramid necessarily has to be a vertical hierarchy such that there should a superior subordinate relationship. Multi-level marketing shall have to a be a legal marketing strategy and not a fraudulent scheme.

Understanding the applicability of the scheme

The applicability of the above guidelines on the direct and selling agents have to be checked from the following facts:

This scheme is applicable on the following companies.

- Companies engaged in marketing as well as selling and distributing the products simultaneously under the network of direct selling.

- All the multi-level marketing schemes such that there are different levels of distribution and the participants are at different distribution levels. Here the participants at the same level of distribution shall not be required to comply with the scheme.

- Company carrying its operations through a hierarchical multi-level system.

- Companies appointing the direct selling agents in such a way, such that they are sponsoring or carrying out recruitment further so that a large network of distribution is created

- Companies that have relevant clauses in the outsourcing agreement and which specifically reflect the outsourcing or subcontracting of the service to the third parties.

- Companies requiring direct selling agents to pay high membership fees and greater entry costs.

Non-Applicability of the guidelines to Pyramid schemes and companies having only one level of distribution

The guidelines shall not be applicable to the pyramid scheme. This is because these schemes are generally money-making schemes and not any legal marketing strategy. This comes from the fact that pyramid schemes are generally created not to market the products, but to create a distributor base for earning large money through promotion. Thus, the direct selling guidelines take a legal view and apply to only legal MLM schemes and direct selling.

Further the companies having only a horizontal distribution base such that they are not recruiting or sponsoring further levels in the chain shall be kept out of the purview of these guidelines.

Quick compliance checklist for direct selling guidelines 2016

- All direct selling companies in India shall submit an undertaking to the department of the consumer affairs within 90 days from 12th September 2016.

- Direct seller cannot receive remuneration or incentive for the recruitment/enrolment of the new participants.

- Direct sellers can only receive remuneration derived from the sale of goods or services

- Direct seller shall carry its identity card and not visit the customers premises without prior intimation/approval.

- Direct selling company cannot force its direct sellers to purchase more goods or service than they can expect to consume or sell.

- Direct selling company cannot demand any entry fee/registration fee.

- Company must provide every participant written contracts describing the material terms (buy back, re-purchase policy, cooling period, warranty and refund policy.

- Mandatory orientation session with accurate information for the newly recruited direct selling agents

- There shall be prohibition of the pyramid scheme and the money circulation scheme.

- There shall be a monitoring authority to deal with the issues related to the direct selling.

Conclusion

There is no scepticism regarding the benefits of the direct selling guidelines on the interest of the consumers in prevention of the frauds against them, however comprehending the applicability of these directions is a hard nut to crack for various entities who are in a dilemma to comply with these guidelines. The guidelines do not specifically state the extent of the applicability; however, they do give certain apparent indications to the entities to whom these guidelines shall be applicable.

Thus, any company desirous of increasing their distribution base for selling wide range of products or services and who intend to do it by creating a hierarchical distribution that requires further outsourcing and recruitment shall be required to comply with the guidelines. Further the outsourcing agreement between the DSA and the service provider shall clearly state the provisions regarding contracting and the sub-contracting, subsequent to which only a network of distributors could be created.

[1] https://rbidocs.rbi.org.in/rdocs/notification/PDFs/NT87_091117658624E4F2D041A699F73068D55BF6C5.PDF

[2] https://www.souravghosh.com/blog/direct-selling-guidelines-2016/

[3] https://consumeraffairs.nic.in/sites/default/files/file-uploads/direct-selling/Direct%20Selling%20Guidelines%20Final%20_0.pdf

[4] https://www.icsi.edu/WebModules/LinksOfWeeks/JuneCS_2014.pdf