Performance of NBFCs in 2016-17

By Mayank Agarwal (finserv@vinodkothari.com)

2016-17 could be summed up as a year of ‘Coming of age’ for Non-Banking Financial Institutions(NBFIs) as they finally fulfilled their potential by displaying a resilient performance against the backdrop of revised regulatory frameworks, widened credit gap due to sluggish performance by banking institutions and providing specialized services to the sector to which they cater. As per the recently released ‘Trend and Progress of Banking in India’ report by RBI,[1] NBFCs have given a stiff competition to established banks in the country, having finally edged ahead in the financial credit race in the country as their portfolio of loans grew at 14.9% during the first half of 2017-18, compared to 6.2% in the case of banks. The share of NBFCs in the total credit granted by NBFCs as well as Banks rose from 9.5% in 2008 to 15.5% as of March 2017, thus showing the increasing popularity of NBFCs as a source of finance. The credit granted by NBFCs as a percentage of GDP rose to 8%, displaying their significance in the country’s financial ecosystem. While the bank credit reached a historical low during 2016-17, NBFCs recorded an increased credit performance during the same year, highlighting the growing popularity in the country.

The recently released ‘Trend and Progress of Banking in India’ report by RBI gives a detailed outlook on the performance of financial entities in India. In this article, we would like to present a comprehensive review of the operations and milestones achieved by NBFCs in the year gone by and the Fintech revolution that has made its way into the country in the past year.

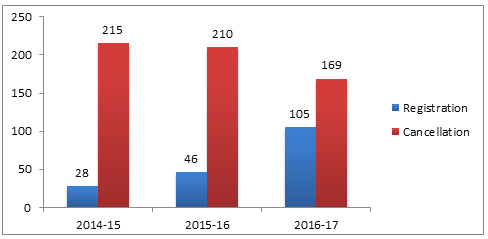

Registration and Cancellations

With a total of 11,522 NBFCs in the country, RBI recognises the importance of such entities that possess expertise in their respective niche and thus facilitate greater financial inclusion of entities operating in such sectors. With this view in mind, RBI has been constantly tweaking the law in order to create a level playing ground in the country and bring NBFCs on par with established Banking institutions in the country.

Although the number of NBFCs in the country has marginally fallen compared to the past year due to introduction of stricter norms and revised criteria of Net Owned Funds, they continued to build on the strong momentum displayed during the past years and further expanded their portfolio during the current year.

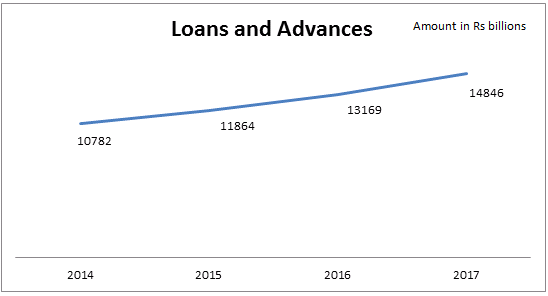

Statistical growth

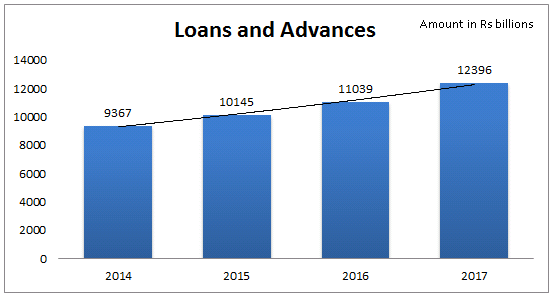

The amount of loans advanced in the year rose to Rs. 14,846 billion, growing at a faster pace of 12.7% as compared to the previous year. Such rise has helped bridge the credit gap in the Country and reduced the dependence on banking institutions, thus providing an alternate source of finance to the people and allowing lower credit rated individuals and entities to avail financing as well.

The sector picked up pace as percentage rise in loans advanced increased by 2% compared to the same in the previous year. This rise was mainly on account of subdued performance by banks due to events such as Demonetisation and implementation of resurrective actions such as Prompt Corrective Action (PCA) and Asset Quality Review(AQR) by RBI. The fact that NPAs account for around 12% of the total loans advanced by banks has further paralysed the sector and allowed NBFCs to gain the upper hand. This is also evident by the fact that Bank borrowings by NBFCs fell sharply during the year, falling by around 7%.

Sectoral Analysis

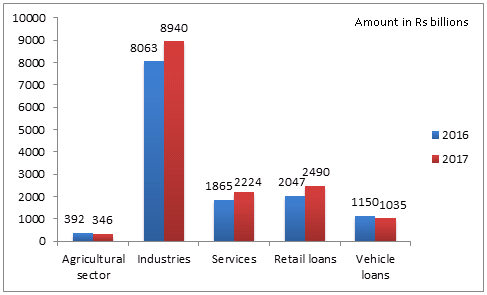

A sector-wise breakdown of performance by NBFCs highlights that the retail sector raised the highest amount of credit from NBFCs, followed by services and agricultural sector. The rise in retail sector credit was on account of financing credit card receivables, which surged due to demonetisation and to facilitate paperless transactions. Demonetisation had its drawbacks as well as credit to agricultural sector faltered due to disruption in the cash intensive supply chain in the country. The same was seen in the case of automobile financing as it fell by 10% during the year. Loans to the Micro and Small sized firms, however, showed a remarkable rise of around 55% as Banks shied away from lending to such young and un-established firms.

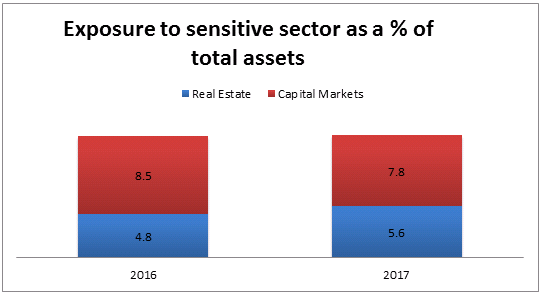

Exposure to sensitive sector as a percentage of Total Assets rose marginally during the year. The structure altered as contribution to Real Estate sector increased while that to Capital markets fell marginally.

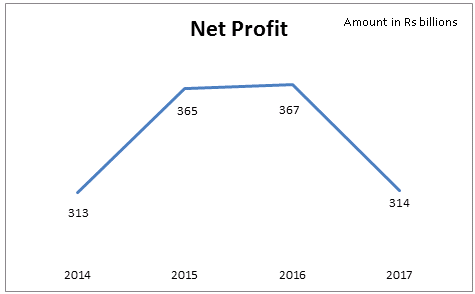

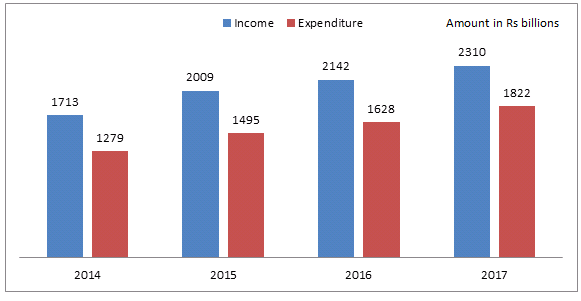

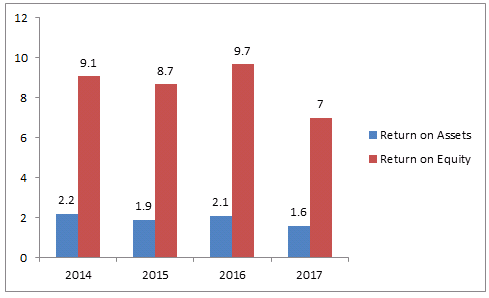

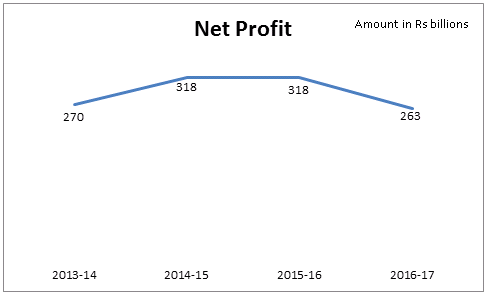

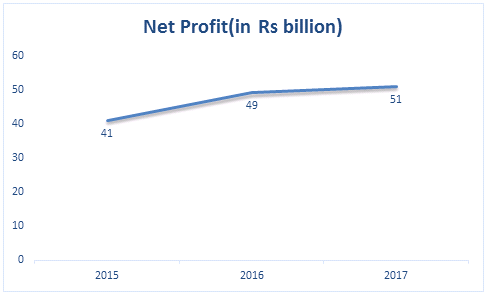

Financial Performance of NBFCs

While net profits had plateaued during the past 2 years, there was a notable downfall in profits during the current year as NBFCs recorded a significant fall of 14.44% compared to the previous year despite a rise in revenue.

This dragged the profitability ratios down as well.

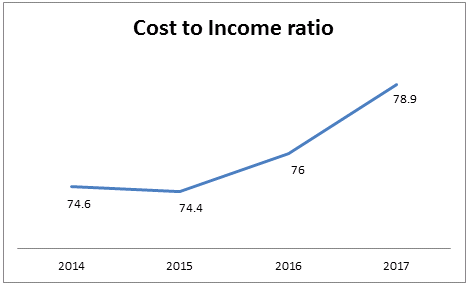

This downfall in profits could be attributed to the increased provisioning norms introduced by RBI as well as increasing public funding raised by the NBFCs. The increase in cost to income ratio by around 3.81% further highlights the deteriorated operational efficiency of NBFCs.

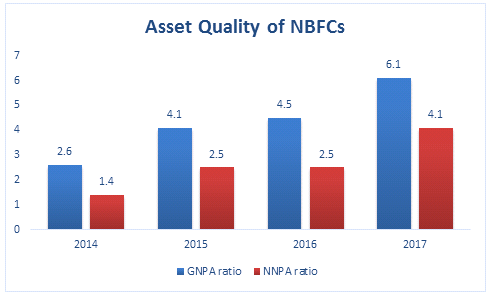

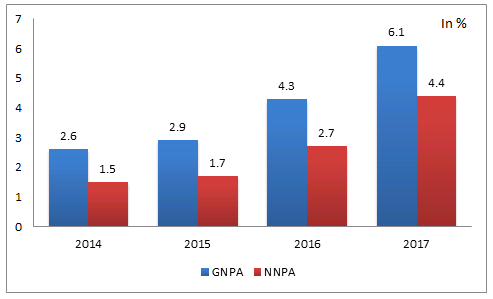

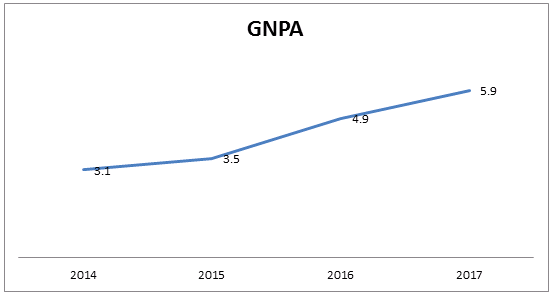

Asset Quality

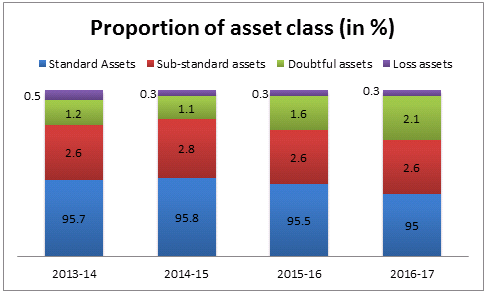

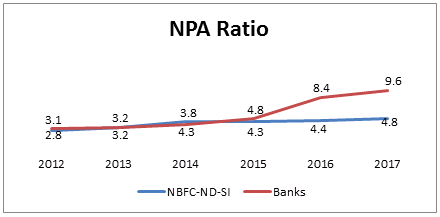

Banks were not the only financial entities burdened with huge stressed assets, as NBFCs also noted a marginal fall in their asset quality. While percentage of standard assets reduced, that of doubtful assets rose. Such deterioration could be associated with the subdued industrial environment in the country. Both the GNPA and NNPA ratio increased in comparison to the previous year, amounting to 6.1% and 4.1% respectively. Such rise also came as a result of higher recognition norms that is being implemented in a phased manner.

The report further categorizes NBFCs into Non-Deposit taking Systemically Important entities(NBFC ND-SI) and Deposit taking entities(NBFC-D).

NBFC-ND-SI

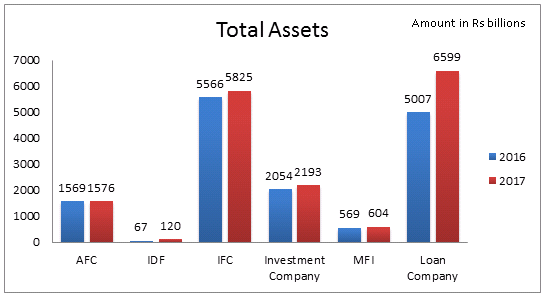

NBFC-ND-SIs accounted for 86% of the total asset size of NBFCs in the country. Infrastructure Finance Companies(IFC) constituted nearly 40% of the total loans extended by NBFC-ND-SI. Although the number of these companies fell sharply by more than 50% as compared to the previous year due to the higher asset size compliance of Rs. 5 billion or more from the previous threshold of Rs. 1 million, the Balance Sheet figures nonetheless grew on account of muted bank credit growth.

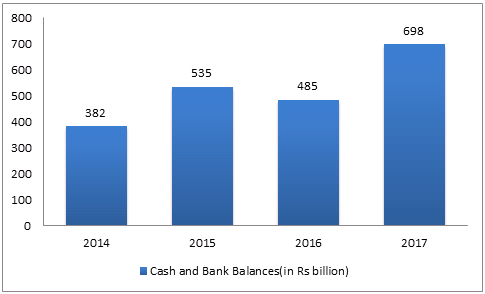

There was also a marked increase in Investments and Cash and Bank balances as these institutions decided to retain funds and invest in high yield instruments instead.

There was a fall in both Operating Profit as well as Net Profit, with the latter displaying a notable downfall of around 17.3%.

The overall GNPA as a percentage of Gross Advances of such entities as amounted to around 6.1% while the percentage of NNPA came to around 4.4%, almost double from the previous year.

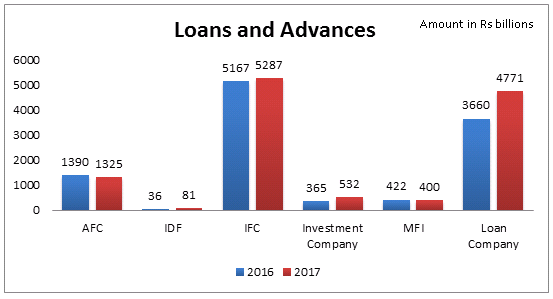

The sector maintained its healthy growth over the years and performed even better during 2017, increasing its loan disbursals by almost 12.3% totalling to Rs. 12,396 billion. Such rise in rate of loan disbursals could be attributed to remarkable growth registered by Loan Companies(LCs) during the year, which has been highlighted in the chart below, showing the category-wise breakdown of the loan and advances during the year.

The fact that the NPA ratio of Banks is almost twice more that of NBFC ND-SI goes to show just why one sector stagnated during the year while the other one continued to grow.

Sources of funding

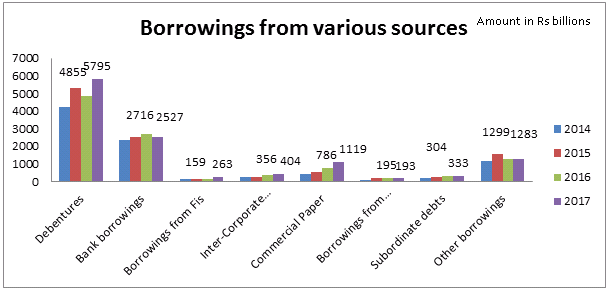

Debentures continued to remain the preferred source of raising funds by NBFC ND-SI as borrowings from Banks regressed during the year. Commercial Paper also emerged as a popular source of short-term finance as the number of issuance showed a notable rise.

NBFC-D

The number of Deposit taking NBFCs reduced by around 12% to total to 178 entities during 2016-17, mainly on account of the higher NOF threshold imposed by RBI. They accounted for 14% of the total assets and 16.2% of the total credit portfolio of NBFCs as at the end of March, 2017.

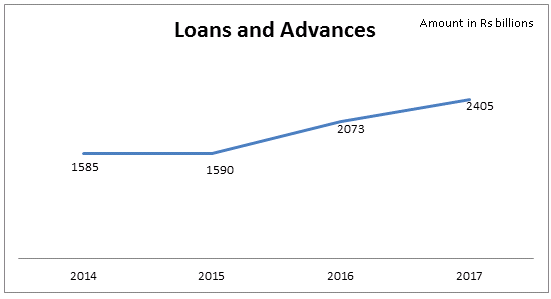

This category of NBFCs was no different to the rest of the sector as it posted a strong 16% Y-o-Y growth in loans and advances during the year, totalling to Rs. 2,405 billion. Transport operators MSME enterprises and Retail market were the centre of focus for such NBFCs throughout the year.

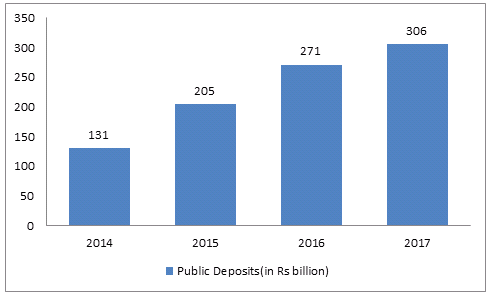

Deposits constituted 11.1% of the total funds of NBFC-D as on 31st March, 2017. While borrowings from Banks fell by around 7%, those from Debentures and Financial Institutions grew sharply as NBFCs looked to diversify their source of funding and reduced reliance on the over-burdened banking sector.

Notably, deposits, advances as well as investments of Asset Finance Companies (AFCs) fell as compared to the previous year due to the fall in number of companies because of the mandatory levy of obtaining a credit rating in order to be constituted as a deposit taking NBFC. The increase in limit for acceptance of deposits from 1.5 times to 4 times of the Net Owned Funds also contributed to this fall.

LCs, however, displayed a strong growth in operations as the rise in deposits slowed down by approximately 22% and both advances as well as investments rose by approximately 22% and 91% respectively during the same period.

The Net Profit of NBFC-D grew marginally and failed to maintain its pace as compared to the previous years as the expenditures grew at a higher rate as compared to Incomes.

A fall in volumes of vehicle loans and agricultural equipment led to deterioration of asset quality in such sectors and thus contributed to the rise in GNPA ratio of NBFC-D, mainly AFC, who have significant exposure to such sector.

Performance of fintech industry: Special coverage

Financial Technology services finally became the centre of attention in the financial landscape of the Country during 2016-17. Implementation of Pradhan Mantri Jan Dhan Yojana(PMJDY), India Stack platform, Start-Up India programme and development of cashless payment systems such as Unified Payments Interface(UPI) are all initiatives that are aimed at promoting paperless services and facilitate seamless integration of financial services into the grassroots of the country.

In the past year, steps were taken to provide for a conducive environment for the development of Fintech in India so as to provide an alternative to physical currencies and revolutionize the way transactions are carried out in the country. The recognition of Peer-to-Peer lending platforms as a category of NBFCs was a major step towards promotion of Fintech services in the country. RBI recognises the fact that Fintech services are the need of the hour given the uptick in number of MSMEs in the Country, who are unable to attain loans by reputed Banks.

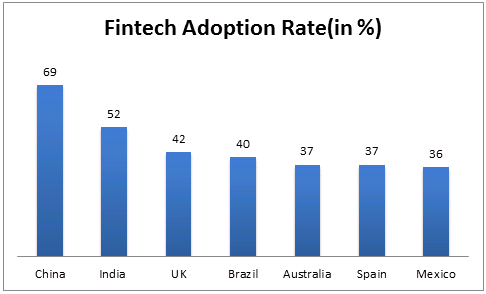

An EY FinTech Adoption Index[2] notes that globally, India remains the second fastest Country to adopt FinTech services, with cost-efficiency, time-efficiency, convenience and friendly user interface being the main reasons behind it.

Inefficiency in the existing IT framework worldwide has contributed to the growing popularity of Fintech services universally. The RBI, having noted such reasons, is not only improving the current IT framework of financial entities in the country, but also supervising the actions of Fintech services both on a global as well as domestic scale and accordingly devising norms to counteract any risk posed by implementation of such services, which have been stated below.

| Benefits | Risks |

| a. Decentralisation and increased intermediation by non-financial entities

b. Greater efficiency, transparency, competition and resilience of the financial system c. Greater financial inclusion and economic growth, particularly in emerging market and developing economies. |

a. Micro-financial risks such as credit risk, leverage, liquidity risk, maturity mismatches and operational risks, especially cyber and legal risks

b. Macro-financial risks such as unsustainable credit growth, increased interconnectedness or correlation, procyclicality and contagion incentives for greater risk-taking by incumbent institutions. |

Despite there being a notable progress in activity in the Fintech sector, the size of credit disbursal in the Indian Fintech market remains a fraction of figures reported by other countries. The Financial Stability Board report on Fintech Credit highlights how far behind India lags compared to its global peers.

| Countries | 2013(amount in USD million) | 2015(amount in USD million) |

| China | 5547 | 99723 |

| USA | 3757 | 34324 |

| UK | 906 | 4126 |

| Japan | 79 | 326 |

| Australia | 12 | 276 |

| Germany | 48 | 205 |

| France | 59 | 201 |

| Canada | 8 | 71 |

| South Korea | 1 | 38 |

| Singapore | 0 | 21 |

| India | 4 | 20 |

Such lag is understandable given the fact that Fintech services have only just started to become popular in the country. Not only will Fintech gradually improve the overall operational efficiency in the country, but also help in establishing a comprehensive credit database which would help avoid any mismatch in credit assessment. Although there is substantial amount of technological risk associated with such structural change, keen oversight by the RBI as seen currently will help mitigate fears of any such risk.

Conclusion

The Indian Financial Ecospace could be summed up as a black and white image as two extreme opposites distinguished the space during the year. On one hand, the balance sheet of the Banking sector remained neck-deep in Non-Performing Assets which dented their operational as well as financial results. On the other hand were the Non-Banking Financial Entities that filled the space vacated by Banks and upheld the debt market in the Country. While the amount of Bank credit witnessed a record low, credit by NBFCs continued to peak during the year.

While the past few years could be categorised as growth stage, 2016-17 could be labelled as the year in which NBFCs finally entered into the maturity phase of their lifespan and established a strong foothold in the country’s financial ecospace.

Despite facing a reduction in quantity, the quality of operations remained a positive as NBFCs capitalized on the dismal condition of the Banking sector and reacted positively to the regulatory reforms introduced by the RBI. While the spike in operations came at a cost as financials came under stress, nonetheless the future remains optimistic for this sector with further safeguards being key.

The year was somewhat of a pivot for NBFCs as the MSME sector witnessed a spurt in disbursements during the year while automobile loans and loans to agricultural sector remained lower in comparison. The ability to tap into niche markets and provide specialized services was the focal reason behind the growth in operations.

Sources of funding too witnessed a change as Debentures and public deposits gained popularity while Bank borrowings declined on the back of adverse performance.

In its report, RBI has noted that while the sector is still far from the desired position, constant introduction of regulatory amendments and keen oversight is sure to further optimise the state of NBFCs in the country. Risk assessment remains a critical area of development for the sector, as noted by the Financial Stability Report issued by RBI.

The woeful state of Banking sector remains a lesson for the financial heads of the country and a picture they would like to avoid in case of the booming NBFC sector. The introduction of refined laws is a step in the right direction and would certainly lead to avoiding any such circumstance.

[1] https://rbidocs.rbi.org.in/rdocs/Publications/PDFs/0RTP20161778B7539711F14E088A31D52351BF6440.PDF

[2] http://www.ey.com/Publication/vwLUAssets/ey-fintech-adoption-index-2017/$FILE/ey-fintech-adoption-index-2017.pdf

Leave a Reply

Want to join the discussion?Feel free to contribute!