ECL Framework for Banks: Key Highlights

See our article A[U]n Expected Injury: ECL is here, likely to hurt bank profits and retained earnings in FY28 for an in-depth analysis.

See our article A[U]n Expected Injury: ECL is here, likely to hurt bank profits and retained earnings in FY28 for an in-depth analysis.

Team Finserv | finserv@vinodkothari.com

The new ECL framework marks a major regulatory shift for India’s banking sector; it has been long overdue, and therefore, there was no case that the RBI could have deferred it further; pleadings to defer the implementation were rejected by the regulator. It comes coupled with regulatory floors for provisions, which would cause a major increase in provisioning requirements over the earlier requirements. Our assessment, on a very conservative basis, is that the first hit to Bank P/Ls will be at least Rs 60000 crores in the aggregate.

This is in addition to fair valuation requirement on upfront adoption, as on 1st April, 2027. While a vaguely worded part in para 19 was inserted on suggestions of the stakeholders, if interest rates have moved up since the date of the original loan, there will be almost a sure case of upfront valuation loss, which will eat up retained earnings.

RBI had come up with a draft framework on ECL pursuant to the Statement on Developmental and Regulatory Policies, wherein it indicated its intention to replace the extant framework based on incurred loss with an ECL approach. The final regulations were notified on 26th April and are applicable w.e.f 1.04.2027 i.e., for FY 27-28. The manner of implementation will be that all loans as on 1st April 2027 will be fair valued, and all new loans/financial instruments originated or acquired on or after 1st April 2027 will be subject to ECL provisions. See the highlights of the final regulations here.

A major impact that the directions will have on the Banking sector is the need to maintain increased provisioning pursuant to a shift from an incurred loss framework to the ECL framework. Under the earlier framework, banks made provisions only after a loss has incurred, i.e., when loans actually turn non-performing. The newECL model, however, requires banks to anticipate potential credit losses and set aside provisions for such anticipated losses.

Banks presently classify an asset as SMA1 when it hits 30 DPD, and SMA2 when it turns 60. Both these, however, are standard assets, which currently call for 0.4% provision. Under ECL norms, both these will be treated as Stage 2 assets, which calls for a lifetime probability of loss, with a regulatory floor of 5%. Thus, the differential provision here becomes 4.6%.

Once an asset turns NPA, the present regulatory requirement is a 15% provision; the ECL framework puts these assets under Stage 3, where the regulatory minimum provision, depending on the collateral and ageing, may range from 25% to 100%. Our Table below gives a more granular comparison.

| Type of asset | Asset classification | Existing requirement | New requirement w.e.f 1.04.2027 | Difference |

|---|---|---|---|---|

| Farm Credit, Loan to Small and Micro Enterprises | SMA 0 | 0.25% | 0.25% | – |

| SMA 1 | 0.25% | 5% | 4.75% | |

| SMA 2 | 0.25% | 5% | 4.75% | |

| NPA | 15% | 25%-100% based on Vintage | 10%-85% based on Vintage | |

| Commercial real estate loans | SMA 0 | 1% | Construction Phase -1.25% Operational Phase – 1% | Construction Phase -0.25% Operational Phase – Nil |

| SMA 1 | 1% | Construction Phase -1.8125% Operational Phase – 1.5625% | Construction Phase -0.8125% Operational Phase – 0.5625% | |

| SMA 2 | 1% | Construction Phase -1.8125% Operational Phase – 1.5625% | Construction Phase -0.8125% Operational Phase – 0.5625% | |

| NPA | 15% | 25%-100% based on Vintage | 10%-85% based on Vintage | |

| Secured retail loans, Corporate Loan, Loan to Medium Enterprises | SMA 0 | 0.4% | 0.4% | – |

| SMA 1 | 0.4% | 5% (0.4% for loans against FD, NSC, LIC and KVP) (2.5% for direct exposures to/guaranteed by State Governments) | 4.6% No change for loans against FD, NSC, LIC and KVP | |

| SMA 2 | 0.4% | 5%(0.4% for loans against FD, NSC, LIC and KVP) (2.5% for direct exposures to/guaranteed by State Governments) | 4.6% No change for loans against FD, NSC, LIC and KVP | |

| NPA | 15% | 25%-100% based on Vintage 10%-100% for loans against FD, NSC, LIC and KVP and for direct exposures to/guaranteed by State Government) | 10%-85% based on Vintage | |

| Exposures under various schemes of Credit Guarantee Fund Trust for Micro andSmall Enterprises (CGTMSE), Credit Risk Guarantee Fund Trust for Low IncomeHousing (CRGFTLIH) and National Credit Guarantee Trustee Company Ltd (NCGTC) | SMA 0 | 0.4% | 0.25% | 0.15% |

| SMA 1 | 0.4% | 0.25% | 0.15% | |

| SMA 2 | 0.4% | 0.25% | 0.15% | |

| NPA | No provision for the guaranteed portion. NPA provisioning as per extant guidelines for the portion outstanding in excess of the guarantee (Only when the Governmentrepudiates its guarantee when invoked) | 10%-100% based on vintage for secured and guaranteed portion 25%-100% based on vintage for unsecured and unguaranteed portion (Only if the claims are not settled with ninety datesfrom the due date of the loan) | ||

| Home Loans | SMA 0 | 0.25% | 0.25% | 0.15% |

| SMA 1 | 0.25% | 1.5% | 1.25% | |

| SMA 2 | 0.25% | 1.5% | 1.25% | |

| NPA | 15% | 10%-100% based on Vintage | (-)5% – 85% based on Vintage | |

| LAP | SMA 0 | 0.4% | 0.4% | – |

| SMA 1 | 0.4% | 1.5% | 1.1% | |

| SMA 2 | 0.4% | 1.5% | 1.1% | |

| NPA | 15% | 10%-100% based on Vintage | (-)5% – 85% based on Vintage | |

| Unsecured Retail loan | SMA 0 | 0.4% | 1% | 0.6% |

| SMA 1 | 0.4% | 5% | 4.6% | |

| SMA 2 | 0.4% | 5% | 4.6% | |

| NPA | 25% | 25%-100% based on Vintage | 0%-75% based on Vintage |

The actual impact of such additional provisioning will be a hit of more than 3% to the profit of banks. Based on the RBI Financial Stability Report of FY 24-25, the current level of SMA and NPA is estimated to be ₹3,78,000 crores (2%) and ₹4,28,000 crores (2.3%), respectively.

Accordingly, an additional provision of approximately ₹ 18,000 crores (4.6% of SMA volume) and ₹ 42,000 crores (10% of NPA volume) will be required for SMA and NPA respectively, leading to a total impact of at least ₹60,000 crores. This estimate has been arrived at by considering the % of NPAs and SMA-1 & SMA-2 portfolios of banks. The actual impact may be higher, as lot of loans may be unsecured, and may have ageing exceeding 1 year, in which case the differential provision may be higher.

It may be noted that while the draft directions allow Banks to add back the excess ECL provisioning to the CET 1 capital, it does not neutralize the immediate profitability impact, as the additional provisions would still flow through the profit and loss account.

How do we expect banks to smoothen this hit that may affect the FY 27-28 P/L statements? We hold the view that it will be prudent for banks, who have system capabilities, to estimate their ECL differential, and create an additional provision in FY 25-26, or do technical write-offs.

Effective Interest Rate requirement applies to all loans effective 1st April, 2027

ECL does not come alone; it comes along with the Ind AS 109 companion – the requirement to compute effective interest rate (EIR) for all financial assets and financial instruments. How does EIR requirement differ from the existing rate of interest/internal rate of return approach? Because EIR has the impact of amortising loan acquisition costs or upfront fees. Currently, banks could have taken the upfront earnings such as processing or origination fees/costs directly to revenue – these will now have to part of the EIR computation. More than impacting the profit number, EIR creates a significant impact on loan management systems, as it results in dual computations – the accounting balances and the customer LMS balances are likely to be different.

Upfront recognition of fair value changes

Para 19 requires that on 1st April, 2027, that is, the date of first adoption, all financial assets and instruments will be fair valued, and the fair value changes (gains or losses) will be adjusted against retained earnings. This is consistent with the principles of first time adoption of Ind AS.

On stakeholder representation, the RBI added this part to Para 19:

Where facts and circumstances indicate that the transaction has been undertaken on terms such that the fair value of the financial asset is not materially different from its carrying cost, the same shall be presumed to be the best evidence of fair value.

What does this imply? If the terms of the financial facility have remained the same, does it mean no fair valuation has to be done? Surely no, at least in our opinion. Any fair value change in fixed rate instruments happens for two reasons: change in credit spreads (rating changes, credit quality changes, etc), or change in rate of interest. If there is a facility extended, say at a rate of interest of 8%, whereas the prevailing rate of interest for a borrower of similar credit standing has moved up to 10%, will there be a fair value decrease? Surely yes.

There are lots of loans which were extended during Covid or periods of low interest rates, which are still continuing. In all such cases, fair value losses are imminent.

The meaning of the para above can only be that if the terms of the original facility are similar to what they would currently be, then the fair value will not have to be computed.

See our other resources:

Simrat Singh and Jeel Ranavat | Finserv@vinodkothari.com

The RBI has proposed an overhaul of the existing prepaid payment instruments (PPI) framework through its draft Master Direction, 2026. The changes aim to, inter-alia, simplify classification, tighten cash usage, restrict cross border payments etc. In this note, we discuss some of the key proposals of the draft master directions.

Two overarching categories are proposed:

With a view to curb ‘loan-loaded PPIs’, it is proposed that credit cards can now be used only for Special Purpose PPIs, while General Purpose PPIs are limited to bank account debit, cash or another PPI. This signals a clear intent to ring-fence credit-backed spending to specific use cases. See our resource around loan loaded PPIs here.

The draft introduces a procedural clarification by requiring non-bank PPI applicants to submit a certificate from their statutory auditor confirming compliance with the minimum net worth criteria of ₹5 Crores. While the threshold itself remains unchanged, earlier a CA certificate was required; the draft now specifically mandates certification by the statutory auditor in a prescribed format..

Cash usage sees the biggest tightening. Cash loading for Full-KYC PPIs is reduced from ₹50,000 to ₹10,000 per month, pushing higher-value transactions towards bank-linked digital modes. The move appears designed to curb anonymity and improve traceability.

Peer-to-peer transfer (i.e. transfer to another person’s bank account or PPI) limits have been standardised. Instead of differentiated limits based on beneficiary registration, a flat cap of ₹25,000 per month is now proposed.

While earlier regulations relied on outstanding balance caps, the draft introduces an explicit ₹2 lakh monthly debit limit for Full-KYC PPIs. In substance, this aligns with the existing ceiling but adds clarity on usage.

Banks issuing PPIs will no longer require prior approval if they are already qualified to issue debit cards. A prior intimation to RBI will be sufficient, allowing faster product launches. This acknowledges that regulated banks already meet baseline prudential standards.

This significantly reduces time-to-market and reflects regulatory reliance on the existing prudential and compliance standards applicable to banks. The change is expected to enhance agility, support faster product innovation, and strengthen banks’ participation in the digital payments ecosystem.

For non-bank issuers, the process is simplified with perpetual authorisation and removal of the explicit in-principle approval stage. The timeline for submission post-regulatory NOC is also relaxed to 45 days from the earlier requirement of 30 days. The draft is silent on the earlier requirement of submitting a System Audit Report (SAR) at the time of authorisation. However, an IS Audit report is proposed to be submitted annually by the issuer.

The draft revises the methodology for computing interest on the core portion by moving from a fortnightly to a monthly calculation framework. Instead of averaging 26 lowest fortnightly balances, issuers will now compute the average of 12 lowest monthly outstanding balances, with the minimum one-year operational requirement continuing. This change appears to be a pragmatic step towards operational simplification, reducing computational intensity while aligning the framework with more conventional monthly cycles. While the earlier explicit restriction on availing loans against such deposits is not reiterated, the fiduciary nature of PPI funds implies that pledging or leveraging customer balances would, in our view, remain impermissible.

In contrast to tightening elsewhere, the framework for foreign users is expanded. The UPI One World wallet will now be available to all foreign nationals and NRIs, with a higher ₹5 lakh monthly usage limit.

This step is aimed at making UPI more accessible to international users, especially inbound travellers who often face challenges in using domestic payment systems. By enabling seamless, wallet-based access to UPI, the framework improves convenience and enhances the overall payment experience in India.

A key change is the blanket removal of cross-border transaction capability for PPIs. Earlier, AD-1 bank issued PPIs could be used for limited overseas transactions. The draft eliminates this entirely, narrowing the scope of PPIs.

Closed system PPIs continue to remain outside regulation but marketplaces are explicitly excluded from claiming this status. The definition of “merchant” has been broadened, removing the requirement of contractual acceptance. Small PPIs will now expire after 24 months with mandatory balance transfer in case the same has not been converted into Full-KYC PPI, instead of merely restricting further credits.

See our existing resources on PPI:

Register your interest: https://forms.gle/csBgaWLpmantMK4d8

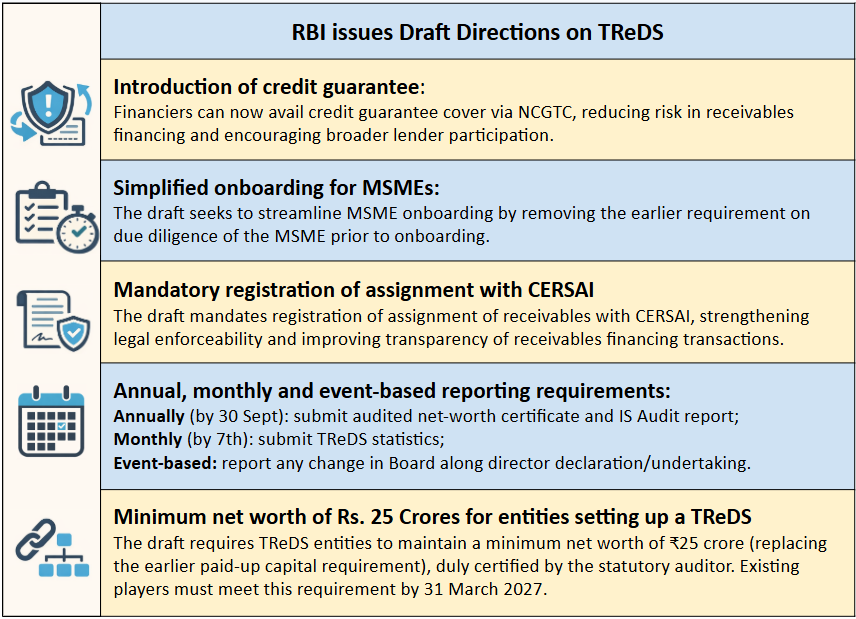

RBI has released draft Reserve Bank of India (Trade Receivables Discounting System) Directions, 2026, proposing a comprehensive overhaul of the existing TReDS framework. These draft directions, if notfied, will replace all existing directions and circulars on TReDs.

Below are the 5 key changes proposed:

🔹Introduction of credit guarantee:

Financiers are now permitted to avail credit guarantee cover (via NCGTC) for exposures on TReDS. This is a significant step towards de-risking receivables financing and encouraging wider participation by lenders. Notably, RBI had already expanded the ecosystem in 2023 by permitting insurers as participants to provide credit insurance cover for such exposures.

🔹 Simplified onboarding for MSMEs:

In line with the Governor’s statement, the draft seeks to streamline MSME onboarding by removing the earlier requirement on due diligence of the MSME prior to onboarding.

🔹 Mandatory registration of assignment with CERSAI:

The draft mandates (earlier recommended) registration of assignment of receivables with CERSAI, strengthening legal enforceability and improving transparency of receivables financing transactions.

🔹Annual, monthly and event-based reporting requirements:

Annually (by 30 Sept): submit audited net-worth certificate and IS/Cyber Security Audit report.

Monthly (by 7th): submit TReDS statistics.

Event-based: report any change in Board along with director declaration/undertaking.

🔹Minimum net worth of Rs. 25 Crores for entities setting up a TReDS

The draft requires TReDS entities to maintain a minimum net worth of ₹25 crore (replacing the earlier paid-up capital requirement), duly certified by the statutory auditor. Existing players must meet this requirement by 31 March 2027.

Link to the draft directions: https://lnkd.in/gkuHNJW9

– Vinod Kothari & Chirag Agarwal | finserv@vinodkothari.com

Volumes of securitisation (which, of course, have always included bilateral assignments or so-called DA transactions) fell by 6% in FY 26, if the origination volume by Reliance group entities in the first half were to be excluded. However, the market has shown more originator diversity, with an increasing share of smaller issuers, including those tasting the market for the first time.

The dip in volumes is because of the larger issuers who were prominently absent or subdued – Shriram Finance as the largest issuer having raised on-balance sheet liquidity, and banking companies. However, the share of gold loans went up sharply, largely due to the sharp increase in gold prices and gold lending, Microfinance companies went more for securitisation, rather than direct assignment transactions.

For anyone studying the Indian securitisation market, it is important to note the following:

Overall, in a stressful global scenario, securitisation has stood firm. Non financial sector entities have shown increasing willingness to tap the market. Of course, SEBI regulations have to be more enabling.

Below, we give a detailed overview of the securitisation market, including a discussion on the asset classes.

Securitisation volumes have been largely driven by NBFCs, which recorded a 30% year-on-year increase in value. In contrast, originations by banks have declined significantly.

Among asset classes, vehicle loans (including commercial vehicles and two-wheelers) accounted for 50% of securitisation volumes (vs 47% in the corresponding period last fiscal). Mortgage-backed loans accounted for about 28% of securitisation volume (vs 37% in the last FY).

Vehicle loan-backed securitisations dominated the market, both in terms of number of deals and total value, reaffirming the sector’s strong position. This is consistent with the growth trend in vehicle loan originations during FY 25.

In addition to vehicle loans, originators also securitised receivables from a diverse set of underlying asset classes during Q4, including:

The continued diversification in underlying asset classes highlights the evolving maturity of India’s securitisation market and growing investor appetite across segments. The break-up of securitisation volumes across various asset classes have been presented below:

Securitisation of Vehicle Loans

The issuance volume for vehicle loan securitisation during FY26 was approximately ₹1.26 lakh crores. Most of the transactions were structured as single-tranche issuances. However, a few exceptions featured more layered structures comprising senior and equity tranches, or senior, mezzanine, and equity tranches.

In terms of credit ratings, the tranches were rated between A- and AAA. Notably, the senior tranches in the majority of transactions received high investment-grade ratings, typically falling within the AA+ to AAA range. This indicates strong investor confidence and reflects the underlying credit quality of the asset pools, supported by adequate credit enhancement mechanisms.

Further, replenishing structures were also observed commonly during FY26. These variations indicate growing sophistication in transaction structuring within the vehicle loan securitisation space, aimed at catering to different investor preferences, improving credit protection, and aligning with originator risk appetite. As the market matures, further innovation in structuring and risk mitigation features can be expected.

In terms of credit enhancements, most vehicle loan securitisation transactions during the last quarter of FY26 featured: cash collateral (CC) and overcollateralisation (OC), with the Excess Interest Spread (EIS) serving as the first layer of loss absorption.

Securitisation of Microfinance Loans

During FY26, the MFI sector has seen a revival after a period of stress during FY 25 and FY 24. This has been due to better credit underwriting of lenders, improving performance trends and granular pool characteristics. Further, after a period of stress, the lenders relied on time-tested borrowers rather than exploring new markets leading to higher average ticket size of loans. This has led to a growth in the volumes of securitisation of microfinance loans during FY26. The PTC issuance volume of microfinance institutions increased to 14% of total PTC issuance in FY26 from 6% of total PTC issuances in FY25. Most of the transactions were structured as a single tranche securitisation.

Further, most microfinance loan securitisation transactions during the quarter featured credit enhancement through two primary mechanisms: CC and overcollateralisation OC, with the EIS serving as the first layer of loss absorption.

Securitisation of pool of loans backed by Home Loans & LAP

The volume of mortgage backed securitisation has been low both in terms of number as well as in terms of amount of issuance. As compared to FY25, the total MBS issuances dropped to 28% of total issuance from 37%. The transactions featured a common waterfall matrix and had received an overall rating of AAA.

In terms of credit enhancement, CC and OC has been provided as a credit enhancement with the EIS serving as the first layer of loss absorption.

Securitisation of Gold Loans

Gold loan securitisation volumes in H2FY26 stood at approximately ₹18,500 crore, significantly higher than the ₹5,000 crore recorded for the whole of FY25.

The jump in gold lending securitisation may be due to increase in gold prices and resultant increase in the value of the collateral. As a result of this valuation spike, average ticket sizes have increased, indicating that as gold valuations rise, consumers are leveraging higher-value loans to meet their financing needs. Another reason for the increased origination may be removal of LTV restriction in case of income generating gold loans.

Securitisation of Unsecured Loans

As per rating rationales published by Care the securitisation volumes of unsecured loans (both personal and business) increased during FY26. Investors in unsecured loan transactions, are preferring the PTC route, due to the support provided by external enhancement. CC and OC have also been provided as a credit enhancement with the EIS serving as the first layer of loss absorption.

RBI has vide its Press Releases – Reserve Bank of India proposed to review methodology for identification of NBFCs in Upper Layer. The key changes are as follows:

It may be noted that NBFCs belonging to the banking group are also required to comply with the compliance requirements applicable to Upper Layer NBFCs (except the listing requirement). Our article on compliances to be followed by such NBFCs in the banking group can be seen here.

A crucial question that arises here is whether the consolidation criteria (multiple NBFCs in the group) be applicable in this case as well to determine the asset size? Though as per prudence, it should apply, to avoid surpassing the regulatory intent, however, the same is specifically not applicable as per the SBR Directions (refer para 21) .

It may be noted that the category of NBFC is not a pre-condition, hence, the list of UL NBFCs would include not just NBFC-ICCs but also HFCs, CICs, deposit taking NBFCs, and not even Govt. NBFCs

Once the proposed criteria are implemented and the new list of Upper Layer NBFCs is notified by the RBI, entities classified as NBFC-UL will face certain immediate implications, in addition to specific corporate governance norms. The central point of discussion is how these requirements might impact the growth plans of large NBFCs.

While CET 1 is currently manageable for most existing UL entities, aggressive growth plans could potentially make this a constraining factor for larger NBFCs newly classified as UL.

Leverage ratio would have been an issue if the entity was engaged in derivatives transactions. However, most of the NBFCs in India are not very active in this space.

The applicability of the large exposure framework may be a real concern. Large exposure framework looks at economic interdependence as the basis of classification into group risk. There is an absolute limit that the single party exposure cannot be more than 20% of Tier 1 capital (including quarterly audited profits) and 25% in case of a group of counterparties.

Team Finserv | finserv@vinodkothari.com

Following the consolidation action undertaken by the Department of Regulations (DoR) in November 2025, the Department of Supervision has now undertaken a comprehensive exercise to consolidate existing standalone circulars issued by RBI in supervisory domain into function-wise, entity-specific consolidated Directions for easier navigation and application. The supervisory instructions have been organised into distinct Directions for each type of RE on each supervisory function.

A detailed analysis of the drafts for NBFCs has been covered here-

| Proposed Draft | Existing Circulars | Applicability | Key Changes |

|---|---|---|---|

| Reserve Bank of India (Non-Banking Financial Companies – Compliance Function) Directions, 2026 | Compliance Function and Role of Chief Compliance Officer (CCO) – NBFCs Streamlining of Internal Compliance monitoring function – leveraging use of technology | NBFCs, including HFCs, in the ML and UL. | No major changes.It has been clarified that in the absence of a new product committee, the CCO shall be required to evaluate all new products before they are launched. |

| Reserve Bank of India (Non-Banking Financial Companies – Cybersecurity, Technology: Risk, Resilience and Assurance) Directions, 2026 [IT Directions] | Master Direction – Information Technology Framework for the NBFC Sector (IT Framework)Reserve Bank of India (Information Technology Governance, Risk, Controls and Assurance Practices) Directions, 2023 (IT Governance) | All NBFCs | CICs were not required to comply requirements of IT Governance Framework, the draft IT Directions now mandate CICs to comply with the IT baseline technology standardsFor NBFCs with asset size below ₹ 500 cr-Chapter IV of IT Directions:Use of public key infrastructure (PKI) for ensuring confidentiality of data, access control, data integrity has been made mandatory (earlier recommendatory)Timeline of reporting of cyber incidents to RBI specified as 6 hours (IT Framework did not contain any such timeline)Use of Digital Signature to authenticate electronic records has been made mandatory (earlier recommendatory)For NBFCs with asset size above ₹ 500 cr-Chapter IV of IT Directions, has specified that IT capacity requirements are now to be ensured by ITSC |

| Reserve Bank of India (Non-Banking Financial Companies – Digital Payment Security Controls) Directions, 2026 | Master Direction on Digital Payment Security Controls | Card issuing NBFCs | There is additional expectation that Risk and Control Self Assessment (RCSA) shall be conducted by vendors as well and such RCSA should be evaluated by the Credit-Card issuing NBFC.Credit-Card issuing NBFCs are required to comply with a number of technical standards for card payment security. Status of compliance with these standards are to be reported to the ITSC for deliberation and appropriate action. |

| Reserve Bank of India (Non-Banking Financial Companies – Fraud Risk Management) Directions, 2026 | Master Directions on Fraud Risk Management in Non-Banking Financial Companies (NBFCs) (including Housing Finance Companies) FAQs on Master Directions on Fraud Risk Management in Regulated Entities (REs), 2024 | NBFC-ML, NBFC-UL,NBFC-BL having asset size ₹500 crores and aboveHFCs. | No Change. FAQs integrated with the circular. |

| Reserve Bank of India (Non-Banking Financial Companies – Internal Audit Function) Directions, 2026 | Risk-Based Internal Audit (RBIA) | All Deposit taking NBFCs and HFCs Non-Deposit taking NBFCs and HFCs with asset size of ₹5,000 crore and above | No Change |

| Reserve Bank of India (Non-Banking Financial Companies – Statutory Audit) Directions, 2026 | Guidelines for Appointment of Statutory Central Auditors (SCAs)/Statutory Auditors (SAs) of Commercial Banks (excluding RRBs), UCBs and NBFCs (including HFCs) FAQs on Guidelines for Appointment SCAs/ SAs of Commercial Banks (excluding RRBs), UCBs and NBFCs (including HFCs) | NBFCs and HFCs having asset size ₹1000 crores and above | No Change. FAQs integrated with the circular. |

| Reserve Bank of India (Non-Banking Financial Companies – Supervisory Returns) Directions, 2026 | Master Direction – Reserve Bank of India (Filing of Supervisory Returns) Directions – 2024 LIST OF RETURNS SUBMITTED TO RBI | All NBFCs (excluding HFCs) | Change in name of return DNBS09 from DNBS09-CRILC Weekly– RDB return to DNBS09- Return on Defaulted Borrowers.Quarterly return on Large Exposure Framework to be filed quarterly by all NBFCs in the Upper Layer – The earlier requirement was reporting of 10 largest exposures of the entity as against the proposed requirement of reporting the top 20 largest exposures. Change in nomenclature of returns on fraud reporting:FMR-I to FMRFMR-III to FUAFMR-IV to FMR 4Form A Certificate is now proposed to be filed online instead of filing in hard copy/ via email.It is proposed that hard copy of returns (hand/post/courier) or email submissions would not be accepted (i.e., would not be deemed to have been submitted by the NBFC) unless specifically prescribed.Additional returns to be filed by SPDs specified. |

| Reserve Bank of India (Non-Banking Financial Companies – Miscellaneous) Supervisory Directions, 2026 | Implementation of ‘Core Financial Services Solution’ by Non-Banking Financial Companies (NBFCs)Fair Practices Code for Lenders – Charging of InterestCoverage of customers under the nomination facilityPrompt Corrective Action (PCA) Framework for Non-Banking Financial Companies (NBFCs) | Chapter III – All NBFCs including HFCs and MFIsChapter IV – Deposit Taking NBFCs (excl. HFCs)Chapter V- Deposit taking, Non-Depositaking, in Middle, Upper and Top Layers including CICs but excluding NBFCs not accepting/ intending to accept public funds. | The phased manner timelines for implementation of CFSS has been removed since the circular is now effective |

| Reserve Bank of India (Non-Banking Financial Companies – Auditor’s Report) Directions, 2026 | Master Direction – Non-Banking Financial Companies Auditor’s Report (Reserve Bank) Directions, 2016 Provisions related to DNBS-10 (SAC) in Master Direction – Reserve Bank of India (Filing of Supervisory Returns) Directions – 2024 | Applicable to every auditor of an NBFC | Clarified that the auditor is now obligated to report to the RBI instances of non-compliance with all applicable extant directions issued by RBI. Other than the above, no major change except updation of references. |

Kunal Gupta, Executive | corplaw@vinodkothari.com

In order to encourage defaulting companies to either complete their long pending statutory filings or opt for an exit or dormant status, the Ministry of Corporate Affairs (‘MCA’), vide Circular dated January 24, 2026, has come up with ‘Companies Compliance Facilitation Scheme, 2026’ (‘CCFS, 2026’). This scheme offers one time immunity to eligible companies (detailed below) in two key ways: (a) updating statutory filings with reduced additional fees; and (b) enabling inactive or defunct companies to opt for dormancy or closure at lower fees. These benefits are available from April 15, 2026, to July 15, 2026.

This write-up discusses the applicability of the CCFS, 2026 and related concerns.

All companies are eligible to avail benefit of CCFS, 2026, except the following-

As mentioned above, the window to avail the benefit under the CCFS , 2026 is for a limited period of 3 months, i.e from April 15, 2026 to July 15, 2026. That is, the companies, intending to avail the benefit under CCFS, 2026 shall have to file the requisite forms within the aforesaid period, failing which, normal fees along with additional fees without any concession will be applicable.

Section 403 of the Companies Act, 2013 read with Companies (Registration Offices and Fees) Rules, 2014 provides that in case of delayed filing of statutory forms, an additional fee of Rs. 100 per day is payable for each day during which the default continues, subject to such limits as may be prescribed. Consequently, non-compliant companies may be required to pay substantial additional fees for the delayed filing of annual forms, over and above the normal filing fees.

The CCFS, 2026 provides a one- time window to all the eligible companies (discussed above) that have failed to file their statutory documents (refer list below), particularly, annual returns and financial statements, to –

Under CCFS 2026, immunity and fee concessions are available in respect of the following e‑forms-

| E- Form | Particulars |

| Under Companies Act, 2013 read with relevant rules made thereunder: | |

| MGT-7 / MGT-7A | For filing annual return |

| AOC-4 / AOC-4 CFS / AOC-4 NBFC (Ind AS) / AOC-4 CFS NBFC (Ind AS) / AOC-4 (XBRL) | For filing financial statements |

| ADT-1 | For intimation about the appointment of auditor |

| FC-3 / FC-4 | For filing annual accounts / annual return by foreign companies in India |

| Under Companies Act, 1956 read with relevant rules made thereunder: | |

| 20B | For filing annual return by a company having share capital |

| 21A | For filing particulars of annual return for the company not having share capital |

| 23AC / 23ACA / 23AC – XBRL / 23ACA – XBRL | For filing Balance Sheet and Profit & Loss account |

| 66 | For submission of Compliance Certificate with the RoC |

| 23B | For Intimation for appointment of auditors |

Response: Yes, the company would still be eligible to avail the benefits of CCFS, 2026, provided 30 days have not elapsed from the date of receipt of the adjudication notice.

Response: Yes, such a company may, under CCFS, 2026, either regularise its default by completing all pending filings at the concessional additional fees, or opt for an exit route by applying for striking off or for dormant status, subject to fulfilment of the specific conditions and procedures prescribed for those options

Response: Yes. Rule 4 of the Companies (Removal of Names of Companies from the Register of Companies) Rules, 2016 mandates filing overdue financial statements and annual returns up to the financial year-end when the company ceased business operations. CCFS, 2026 provides some relaxation on filing fees of STK-2 but does not exempt compliance with striking-off prerequisites.

Response: No, CCFS, 2026 specifically rules out companies which have already filed Form STK-2 u/s 248(2) of CA, 2013 from taking benefit under this scheme.

Response: A section 8 company cannot opt for striking off u/s 248.

Response: In this case, since an SCN has already been issued on 1 March 2026 for non-filing of AOC-4 and MGT-7 for FY 2022–2025, the company would not be eligible to claim immunity or relief under CCFS, 2026.

Response: No, as of now, benefits under CCFS 2026 can be availed by companies only.

As an initiative to improve compliance level and ensure that the corporate registry reflects correct and up-to-date data, MCA has come up with this one-time Scheme. It’s a wake-up call for non-compliant companies to regularise themselves by updating their filings at the lowest additional fees, or to opt for dormancy or strike-off with ease at concessional filing fees. Companies should seize this opportunity to achieve statutory compliance, avoid future penalties, and contribute to a transparent business ecosystem.

Manisha Ghosh, Assistant Manager | finserv@vinodkothari.com

In the world of finance, where EMIs reign is supreme, a quiet revolution is brewing. For decades, the EMI—a fixed, predictable monthly payment—has been the default repayment option in case of loans. This repayment model aligns well with the cash-flow profile of salaried borrowers, whose income is credited at predictable monthly intervals. A fixed monthly outflow is therefore rational and manageable for the borrower. But what happens when there are borrowers who don’t live by the calendar?

In India there also exists a substantial segment of borrowers with fluctuating income streams such as taxi drivers, gig workers, small traders, daily wage earners, contract-workers, etc. Their earnings are typically received on a daily or near-daily or weekly basis and may fluctuate based on demand, seasonality, or operational variables. For such a category of borrowers, imposing a lump-sum monthly repayment obligation may create liquidity stress. People with irregular income may find it difficult to set aside a large lump sum to honor the obligation on the due date, even if their total earnings over the month are sufficient. As a result, they may lead to missed payments not because they lack income or resources, but because their cash flow does not align with the repayment schedule.

To address this structural mismatch between income frequency and repayment frequency, banks and NBFCs have been exploring the option of Equated Daily Instalments (“EDIs”). Under an EDI structure, the repayment obligation is broken into smaller, more frequent daily amounts, theoretically aligning repayment with the borrower’s earning cycle and smoothing liquidity issues.

There is no regulatory prohibition under the RBI framework preventing lenders from offering daily repayment options in their loan products. In fact, the RBI’s Key Fact Statement (KFS) format prescribed under the Responsible Lending Conduct Directions acknowledges not only EMIs but has referred to the term Equated Periodic Instalments (‘EPI’), which has a broader meaning.

The use of the term EPI indicates that repayment need not necessarily be structured on a monthly basis. Rather, lenders are permitted to determine an appropriate repayment frequency whether daily, weekly, fortnightly, or monthly depending on the loan product and borrower profile. The repayment frequency is arrived at by considering the source of income, cashflows of the borrower; this ensures that servicing of such loans is aligned with the borrower’s income profile and does not create any undue financial burden or pushes the borrower towards a debt trap.

Irrespective of the repayment frequency, the issue of fairness in lending still needs to be examined. In case a borrower is required to make repayments every single day, any small disruption in income will be considered as a default and have an immediate impact on the borrower’s performance. For example, if the borrower falls sick or is unable to work for a few days, their daily income may stop. In such a case, they may miss one or more installment payments. Since the due date arises daily under an EDI structure, even one missed payment can start the DPD count, and the delay will continue to add up to the repayment obligation until the payment is made.

This situation will have adverse implications not just for the borrower but also for the lender. The borrower’s credit record may worsen quickly, even if the income disruption is temporary. At the same time, the lender may see rising delinquencies in its portfolio.

While EDIs may help in synchronising repayment with daily income, they provide very little cushion to borrowers in case of unforeseen and unexpected events resulting in default in repayment. Lenders may instead consider a weekly repayment model, where borrowers can collect and accumulate their daily earnings and repay the lender on a weekly basis.

A weekly installment structure provides the borrower with a limited but meaningful cushion. If the borrower is unable to earn on a particular day, they still have the remaining days of the week to generate income and arrange the repayment amount. This flexibility reduces the likelihood of an immediate default and offers a more balanced approach between daily and monthly repayment models.

From an operational perspective, daily repayments also create practical challenges. The lender would need to monitor DPD status every day, carry out daily accounting entries, and reconcile payments continuously. For a large number of borrowers, this can become difficult and resource-intensive. Further, if collections are done manually or through agents, missed payments may require daily follow-ups. This increases recovery costs and may create borrower stress or reputational risks for the lender.

Having said that, this kind of arrangement is restricted under the digital lending regulations. Paragraph 10(2) of the RBI (NBFC- Credit Facilities) Directions, 2026 mandates that all loan servicing and repayments must be executed directly by the borrower into the regulated entity’s bank account. The framework expressly prohibits the use of pass-through or pool accounts of any third party, including those of a Lending Service Provider (‘LSP’).

Accordingly, under the current digital lending regime, repayments cannot be routed through an intermediary. This makes such a model difficult to implement for loans that are originated digitally.

The choice of repayment frequency should not be driven by convention alone, but by the borrower’s income pattern and capacity to absorb short-term shocks. EDIs attempt to bridge this gap, but a rigid daily obligation can expose borrowers to immediate default in the event of even minor income disruptions.

At the same time, daily repayment structures increase operational and monitoring burdens for lenders. Therefore, the focus should be on designing repayment models that balance flexibility with discipline. Structures such as weekly repayments, grace periods, or limited flexibility mechanisms may provide a more sustainable balance. Ultimately, a well-designed repayment model protects both borrower credit health and lender portfolio quality, reinforcing the broader principles of responsible and fair lending.