Shorn of tax benefit, MLDs now face tax deduction on payouts

Dayita Kanodia | Executive

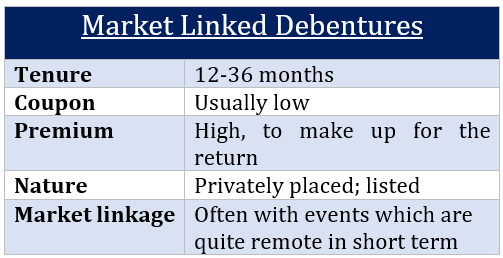

Background

The Finance Bill, 2023[1], has quite nearly caused the demise of the so-called “Market-Linked Debentures” (MLDs)[2]. The changes made pursuant to the Finance Bill, 2023, took away what seemed to be a strong reason for popularity of MLDs, i.e., the tax arbitrage.

Prior to the change, listed MLDs had the advantage of being exempt from the withholding tax under section 193 of the Income Tax Act, 1961, as well as being taxed at 10% as Long Term Capital Gains (LTCG) tax, if held for at least 12 months.

Finance Bill, 2023 inserts a new section 50AA to the Income Tax Act, 1961, which makes MLDs to be taxed at slab rates as a short term capital asset in all cases at the time of transfer or redemption on maturity, irrespective of the period of holding, therefore losing out on the earlier lower LTCG rate of 10%.

In addition, the earlier exemption from withholding tax on listed debentures has now been removed pursuant to an amendment in section 193, which means that interest paid on listed debentures would now be subject to withholding tax with effect from April 01, 2023[3].

Read more →