12-Hour Certificate Course on Leasing

Register: https://forms.gle/VBeA2EmkC92QUmK79

Loading…

Register: https://forms.gle/VBeA2EmkC92QUmK79

– Vinod Kothari | finserv@vinodkothari.com

In India, we often say: upar wala sab dekhta hai (God sees it all). However, if I could do things which God the almighty does not or cannot see, I will be most happy to do those. Doing things off-the-balance-sheet is always equally tempting; structurers of Frankenstein financial instruments have already tried to bring ingenuity to explore gaps in accounting standards to create such funding structures where the asset or the relevant liability does not show on the books. Recently, a $ 27 billion bond issuance by an SPV called Beignet Investor, LLC may have the ultimate effect of keeping the massive investment done at the instance of Meta group kept off-the-balance-sheet.

Essentially, the deal involves issuance of bonds to the investors, the servicing of which is through the cash flows generated from the lease payments. Further, a residual value guarantee has been provided by the group entity which has again led to a rating upliftment for the bonds issued.

The essential structure of the transaction involves a combination of project finance, lease payments and a residual value guarantee to shelter investors from project-related risks, and use of an operating lease structure, apparently designed to keep the funding off the balance sheet of Meta group. It is a special purpose joint venture which keeps the funding liability on its balance sheet.

Let us understand the transaction structure:

The diagram below by provides for the transaction structure:

Of course, as one would have expected, the rating agency Standard and Poor’s that was the sole rating agency having given rating for the bonds, its report does not say the structure is off-the-balance sheet for the lessee, a Meta group entity. However, various analysts and commentators have referred to this funding as off-the-balance sheet. For example, Bloomberg report says “The SPV structure helps tech companies avoid placing large amounts of debt on their balance sheets”. Another report says that the huge debt of $ 27 billion will be on the balance sheet of Beignet, the JV, rather than on the books of Meta. An FT report says that bond was priced much higher than Meta’s balance sheet bonds, at a coupon of 6.58%, as a compensation for the off-balance sheet treatment it affords. A write up on Fortune also refers to this funding as off-the-balance sheet.

In fact, Meta itself, on its website, gives a clear indication that the deal was struck in a way to ensure that the funding is not on the balance sheet of Meta or its affiliates. Here is what Meta says:

“Meta entered into operating lease agreements with the joint venture for use of all of the facilities of the campus once construction is complete. These lease agreements will have a four-year initial term with options to extend, providing Meta with long-term strategic flexibility.

To balance this optionality in a cost-efficient manner, Meta also provided the joint venture with a residual value guarantee for the first 16 years of operations whereby Meta would make a capped cash payment to the joint venture based on the then-current value of the campus if certain conditions are met following a non-renewal or termination of a lease.”

Here, two points are important to understand – first, the operating lease/financial lease distinction, and second, the so-called residual value guarantee – what it means, and why it is opposite in the present case.

The distinction between financial and operating leases, the key to the off-balance sheet treatment of operating leases, was the product of age-old accounting standards, dating back to the 1960s. In 2019, most countries in the world decided to chuck these accounting standards, and move to a new IFRS 16, which eliminates the distinction between financial and operating leases, at least from the lessee perspective. According to this standard, every lease will be put on the balance sheet, with a value assigned to the obligation to pay lease rentals over the non-cancellable lease term.

However, USA has not aligned completely with IFRS 16, and decided to adopt its own version called ASC 842 for lease accounting. The US accounting approach recognises the difference between operating leases and financial leases, and if the lease qualifies to be an operating lease, it permits the lessee to only bring an amount equal to the “lease liability”, that is, the discounted value of lease rentals as applicable for the lease term.

As to whether the lease qualifies to be an operating lease, or financial lease, one will apply the classic tests of present value of “lease payments” [note IFRS uses the expression “minimum lease payments”], length of lease term vis-a-vis the economic life of the asset, existence of any bargain purchase option, etc. “Lease payments” are defined to include not just the rentals payable by a lessee, but also the minimum residual value. This is coming from para 842-10-25-2(d). The reading of this para is sufficiently complicated, as it makes cross references to another para referring to a “probable payment” under “residual value guarantees”. The reference to para 842-10-55-34 may not be needed in the present case, as the residual value agreed to be paid by the lessee is included in “lease payment” for financial lease determination by virtue of the very definition of financial lease. Therefore, it remains open to interpretation whether the leases in the present case are indeed operating leases.

Considering that the residual value guarantee from the parent company in the present case may not meet the requirements for its inclusion in “lease payments”, it is unlikely that the lease payments over any of the 4 year terms will meet the present value test, to characterise the lease as a financial lease. Also, the economic life of the commercial property in form of the data centers may be significantly longer than the 20 year lease period, including the option to renew. Hence, the lease may quite likely qualify as an operating lease.

In lease contracts, a residual value guarantee by the lessee is understandable as a conjoined obligation with fair use and reasonable wear and tear of assets. In the present case, if the lessee is a tenant for only 4 years, and the renewal thereafter is at the option of the lessee. If the lessee chooses not to renew the lease, the lessee is exercising its uncontrolled discretion available under the lease. So, what could be the justification for the parent company being called to make a payment for the residual value of the property? After all, the property reverts to the lessor, and whatever is the value of the property then is the asset of the lessor.

In the present case, it seems that the RVG comes under a separate agreement – whether that agreement is linked with the leases is not sure. However, for the holistic understanding of any complicated transaction, one always needs to connect all the dots together to get a a complete understanding of the transaction. If the lessee or a related party is paying for future rentals, it transpires that the understanding between the parties was a non-cancelable lease, and the RVG is a compensation for the loss of future rentals to the lessor. If that is the overall picture, then the lease may well be characterised as a financial lease.

A liability is what one is obligated to pay; a commitment to pay. The $ 27 billion liability for the bonds in the present case sits on the balance of the JV Company. However, the question is, ultimately, what is it that will ensure the repayment of these bonds? Quite clearly, the payment for the bonds is made to match with the underlying lease payments, with a target debt service coverage. In totality, it is the lease payments that discharge the bond obligation; there is nothing else with the JV company to retire or redeem the bonds. From this perspective as well, an off-balance-sheet treatment at the lessee or at the group level seems tough.

However, off-balance-sheet may not be the objective really. What matters is, does the structure insulate Meta group from the risks of the payments from the data center. From the available data, it appears that the project related risks, from delays in completion to non-renewal, are all taken by Meta. Therefore, even from the viewpoint of project-related risks, there do not seem to be sufficient reasons for any off-balance sheet treatment.

Disclaimer: The analysis in the write-up above is limited to the reading that could be done from write-ups/materials in public domain.

Other Resources:

– Devika Agrawal and Anshit Aggrawal, Executive (resolution@vinodkothari.com)

The determination of the nature of debt has been one of the primary tasks before a Resolution Professional/ Liquidator, and also for the stakeholders. The classification of debt is an important consideration since there exist only two types of debt under the Insolvency and Bankruptcy Code, 2016 (hereinafter referred to as “Code”), i.e., Operational Debt and Financial Debt, each with a significant set of rights and powers.

At the outset, one may think that the identification is a fairly simple job – loans and alike are financial debts, whereas those relating to supply of goods and services are operational in nature. Then, where does the confusion lie? The question of determination gains much importance for not-so-simple arrangements like lease transactions, which sit on the fence of being a financial transaction, and accordingly, the determination of financial versus operational nature will lead to consequent difference in rights and obligations.

In this article, the authors analyse the interface between the Code and lease transactions, and discuss the treatment of the leased assets or lease agreements/ transactions under the Code.

-Vinod Kothari and Sikha Bansal (finserv@vinodkothari.com)

Just as you may subscribe to digital content, cellphone services, or software-as-a-service, you may subscribe to a car, or home durables. The business of availing equipment as a subscription is growing monotonic and steep, and currently, in the realm of passenger vehicles, it is already a rage. A report by BCG estimates that the subscription market for passenger vehicles may achieve a penetration of 15% of new car sales, and volumes of about USD 30 to 40 billion, by 2030[1].

This article seeks to touch upon the fundamental understanding of subscription and how it is different (or not different?) from a lease. There are several other similar contracts – which may be looking elusively similar – asset capacity sharing contracts, asset timeshare contracts, etc. Each of these might have shades of difference; however, our present write-up focuses on subscription services for assets, versus lease transactions.

It is difficult to find a legal definition of the word “subscription” as the word is used in widely different contexts. “To subscribe” may mean to write your name or put your signature under a written document, (common example is ‘subscribing’ to a memorandum of a company). However, in the present context, the following dictionary meaning of ‘subscription’ would become relevant: “A written contract by which one engages to contribute a sum of money for a designated purpose, either gratuitously, as in the case of subscribing to a charity, or in consideration of an equivalent to be rendered, as a subscription to a periodical, a forthcoming book, a series of entertainments, or the like.”[2] Hence, a ‘subscriber’ is “a person who agrees to receive something on a regular basis, e.g. a newsletter, a newspaper, a delivery of goods, a subscriber to a mailing list.”

The context of this article is subscription to equipment – hence, the definition below from an Indiana law may be relevant: “‘subscription program’ means a subscription service that, for a recurring fee and for a limited period of time, allows a participating person exclusive use of a motor vehicle owned by an entity that controls or contracts with the subscription service. The term does not include leases, short term motor vehicle rentals, or services that allow short term sharing of a motor vehicle”. See, IND. CODE § 9-32-11-20(e) (2019)[3].

Under a vehicle subscription, a customer typically pays a “joining fee” plus a monthly subscription fee to have the right to use a vehicle from the company’s fleet of vehicles and to swap the vehicle for a different type of vehicle. Depending on the pricing tier, a customer may have unlimited swaps or may be limited to a certain number of swaps. A customer can initiate an exchange through the company’s mobile application, and the company will deliver the new vehicle and retrieve the vehicle currently in the customer’s possession. The company provides insurance coverage and access to roadside assistance and performs routine maintenance and repairs on the vehicles. See, House Bill, 537 (Northern California)[4] defining “vehicle subscription” for the purpose of applicability of alternative highway use tax.

Hence, one may define a subscription as follows:

A subscription contract is a contract where a subscriber avails a service, whether with or without a related asset, equipment or property, tangible or intangible, for a charge known as subscription fee, where the service provider agrees to provide, for a specified period, generally renewable at the option of the subscriber, a specific service. If an asset or equipment is put in the possession of the subscriber as a part of the service, the subscriber’s control over the same will be limited to the terms of the service, and generally, the service-provider shall have the ability to replace the same, whether for the purpose of a more effective service or otherwise.

The words lease, rent or hire mean the same thing – that is, transferring the right to use an asset. The act of ‘transferring’ right of use would mean that the lessee would have the exclusive right to use the asset and for that the asset as well as the control of the asset moves from the lessor to the lessee for the period of lease.

As one wonders, all of these would also happen in case of ‘subscription’ as discussed above; however, a fundamental difference is that, the customer’s intent in case of lease, is to have the ‘asset’ while in case of subscription, it is to have the ‘experience’ of the asset. Former is an ‘asset-oriented’ transaction, while the latter is a ‘service oriented’ transaction. Further, another important distinction lies in “commitment” to “an asset”. In a lease, the parties are committed to a particular asset identified at the beginning of the contract – replacements would only occur is the asset gets damaged or otherwise goes into an unusable state; however, inherent idea of ‘subscriptions’ is ‘choice’ and ‘flexibility’[5].

Hence, leases are different – differences are being tabulated below:

| Point of Comparison | Lease | Subscription |

| Subject matter of the contract | Transfer of right to use of an asset | Provision of a service |

| Description of parties | Lessor, lessee or renter | Service Provider, Subscriber |

| Consideration | Lease rentals or hire charges | Subscription fee |

| Typical period | Normally long enough to serve as an alternative mode of acquisition of an asset | Normally short and flexible, such it is an alternative to acquisition itself. It focuses on experience, rather than acquisition |

| Identification of the asset | Specifically identified | Generically identified – such as a car of a particular type or category or class. |

| Ownership of the asset | Throughout the term, remains with the lessor. EoT options may include an option to buy | A subscription contract moves completely from the domain of asset acquisition – asset acquisition becomes irrelevant for a subscriber, as the subscriber continues to avail the service on a continuing/recurring basis |

| Provision of asset-related services by the owner | Usually limited; however wet leases are also there | Usually, the bundle of service makes it a service contract. |

| Control over the asset | Remains with the lessee during the lease term | Remains with the owner/service provider. Subscriber’s control is limited to what is required for the enjoyment of the service |

| Vehicle registration | Normally, in the name of the lessee, with endorsement in the name of the lessor | Normally, in the name of the lessor, under a rental contract |

| Vehicle number plate | As in case of a private use vehicle, black colour in white background | Commercial use- hence, black colour on yellow background |

| GST applicability | A lease, being a transfer of right to use goods, is taxable at the same rate as applicable to the sale of the goods | A subscription service, not involving a transfer of right to use, being a service, is taxable at the residual rate, viz., 18% |

| Asset recognition by customer | Yes, as under the accounting standards | No |

Legal classification of a transaction is important as the same would impact the legal rights and obligations of the parties.

Since a subscription is a bundle of services, it may also have elements of lease. A subscription is essentially a package; hence, the use of an asset is also embodied in a subscription. Hence, to the extent a subscription entails a right of using an asset, there is a bailment contract in a subscription too. Hence, bailment is a common feature of both leases and subscription contracts. Therefore, the rights and obligations of the bailor and bailee as per law of contracts may be applicable in case of subscription too.

Thus, from a broader perspective, both a lease and a subscription are forms of bailment contracts only as the possession passes to the customer. Hence, general contractual rules as are applicable to bailment contracts would apply in both the cases. Besides, from a legal perspective, the following may be noted –

Note that due to the features as discussed above, in India, a subscription service may get covered under Rent a Cab Scheme, 1989. Thus, as under the Motor Vehicles Act and rules thereunder, the vehicle would be registered in the name of subscription provider and the number plate of the vehicle shall bear yellow alpha-numerals with black background registration mark. However, in case of leases, the vehicle would generally be registered in the name of the lessee, and shall bear black colour in white background.

For accounting purposes, does a subscription of an asset amount to a lease? If it does, the accounting standard on leases IFRS 16/ Ind AS 116 applies. The standard will require on-balance sheet treatment of the non-cancellable lease rentals in the books of the subscriber in most cases. Hence, the characterisation of the transaction as a “lease” for the purpose of the accounting standard becomes critical.

Ind AS 116 provides guidance on assessing whether a contract is a lease. A lease is defined in Para 9 as follows: “A contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration” Therefore, there has to be a conveyance of the right to use an asset, which implies an identified asset.

In order for the contract to be a contract of lease:

It is notable that accounting standards quite often deviate from the legal form of the contract – hence, even if the legal form of the contract is a subscription, the accounting standards may still treat the contract as a lease. For example, IndAS 116, para B14 provides for the supplier to have substantive rights of substitution, that further, such right to be economically beneficial to the supplier.

Hence, for the purposes of accounting standards:

Hence, a typical subscription contract, which enables the subscription provider to provide service to the customer by using different vehicles (which belong to the preferred class/category chosen by the customer), it may be contended that the customer’s right to use is not perfected in such contracts. Further, given that the customer can ‘swap’ vehicles during the subscription period, it can be said that a subscription contract does not have an ‘identified asset’, per se.

Notably, accounting standards emphasise on substance over form. Hence, a pure subscription contract may not fall under Ind AS 116 (for reasons as above).

The GST law has different rates for motor vehicles. There are broadly 4 classes:

The GST rate on the various subscription models prevalent in the market varies and depends on the nature of transaction between the dealer and the end user. In our view, the subscription-based model is close to a rental service, and therefore, the rate will be 18%. Alternatively, if it is taken as an independent service the rate of tax is still 18%. On the question whether such a subscription service may be regarded as a ‘composite supply’, the tax rate on the principal supply shall determine the tax rate on the conjugate services. However, since the principle supply is still a lease or rental and not a transfer of right to use akin to purchase of the asset, the rate would still stand as 18%.

It is not that subscription contracts per se are a technological innovation, but the idea of an asset being converted into a subscription service is quite new, relative to the idea of leasing or hiring. Hence, the first predicament for one trying to state the law of subscription vs. lease is that there is no authoritative definition of a subscription, as compared to a lease.

The discussion is an attempt to identify key differentiators between lease and subscription. Essentially, a subscription contract is ‘service’ based while a lease is ‘asset’ based. However, classification of a particular contract would depend on the substance of the transaction rather than the form. A contract may be a subscription by name, but may have predominantly lease-type features. However, merely because a contract has some lease-type features would not lead to its classification as lease. Hence, one will have to assess what is the predominant flavour of the contract and of course, intent of the parties to the transaction to determine whether the contract is a lease or a subscription.

[1] https://www.bcg.com/en-in/publications/2021/how-car-subscriptions-impact-auto-sales

[2] https://dictionary.thelaw.com/subscription/

[3] https://law.justia.com/codes/indiana/2019/title-9/article-32/chapter-11/section-9-32-11-20/

[4] https://dashboard.ncleg.gov/api/Services/BillSummary/2019/H537-SMSV-44(e4)-v-2

[5] See an article titled “Insurers are Teaming up with Car Subscriptions”, published in CBInsights (2018). Per Porsche North America CEO Klaus Zellmer, younger people “do not want to engage with a commitment for three years. They want to change their phones; they want to change their TV channels. It’s all about subscriptions.”

[6] https://www.cbic.gov.in/resources//htdocs-cbec/gst/Notification11-CGST.pd

Our other articles on leasing:

https://vinodkothari.com/leasing/

– Abhirup Ghosh (abhirup@vinodkothari.com)

Like all assets, leased assets also undergo impairment. IAS 36 is the relevant standard for impairment of assets, however, IFRS 9 deals with impairment of financial assets, as well as lease receivables.

Therefore, even though lease transactions are governed by IFRS 16, for impairment of leased assets, one has to refer either of aforesaid standards.

In this article, we will focus on the manner in which leased assets are impaired, especially the way expected credit losses (ECL) could be calculated for lease transactions.

The approach of impairment differs with the nature of lease. In case of an operating lease, the lessor recognizes the asset under Property, Plant and Equipment. Therefore, the lease asset capitalized in the books of the lessor has to undergo impairment testing under IAS 36. In addition to that, the lease receivables that fall under the purview of IFRS 9 also have to be tested for impairment. In case of operating leases, only those rentals which are overdue shall undergo impairment testing under IFRS 9.

In case of financial leases, the lessor recognizes only lease receivables in its books. Therefore, there is no question of assessing impairment on the fixed asset in such case; only ECL has to be provided on the lease rentals.

Unlike the erstwhile standards on leasing, IFRS 16 provides for recognition of Right of Use (ROU) Asset in the books of the lessee, and a corresponding lease liability.

The ROU asset will also have to undergo impairment testing under IAS 36.

The requirement to impair an asset under IAS 36 gets triggered only when any of the following indicators are noticed:

a.) External indicators:

b.) Internal indicators:

The standard looks at assets Cash Generating Units, in case of lease transactions, each asset on lease would be treated as CGU for the purpose of this standard.

The impairment loss is calculated based on the carrying value of the asset and the recoverable value.

Recoverable value is the higher of the following:

a.) Fair value of the asset, less cost of disposal

b.) Value in use

Fair value of the asset is arrived at based on the valuation of the asset using appropriate valuation methodologies. From the fair value, cost of disposal has to be reduced, which includes:

The value in use computed based on the present value of all the future cash flows from the asset, discounted at rate which truly reflects the time value of money and the risks specific to the asset. To compute value in use, a risk weighted cash flows approach must be adopted.

There are two ways in which this approach can be adopted – a) by adjusting the cashflows, b) by adjusting the discounting rate.

In the first one, the future cash expected cash flows must be assigned different probabilities of recovery which would corroborate with the risk associated with the asset, and then discount the cash flows at the agreed yield of the transaction.

Alternatively, the instead of assigning probabilities of recovery on the cash flows, the original expected cash flows may be considered, however, the discounting rate may be adjusted to corroborate with the risks associated with the assets.

If the recoverable value of the asset is lower than the carrying amount, then the difference has to be booked as an impairment loss and the carrying amount has to be brought down to that extent.

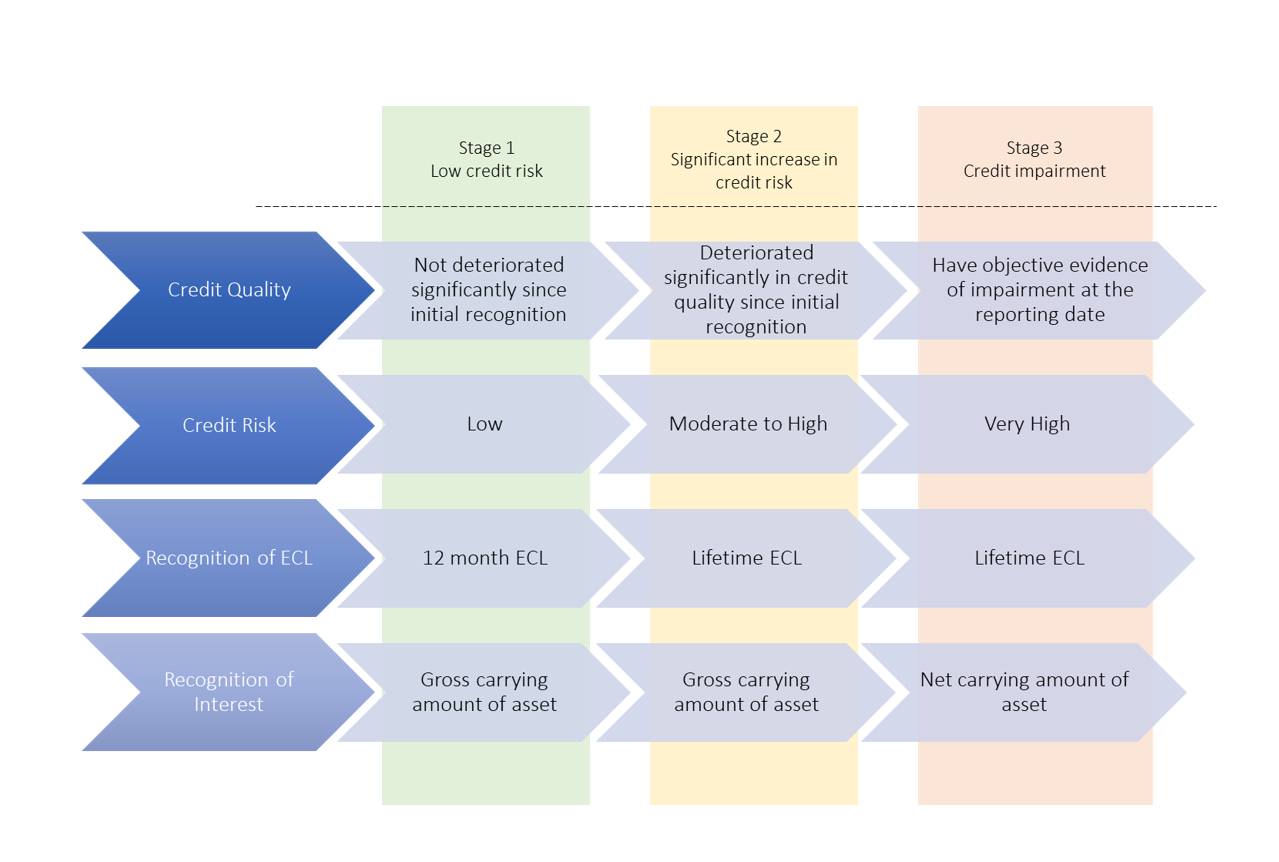

There are two approaches for computing ECL:

In the general approach, ECL is computed based on 12-months losses for instruments not showing significant increase in credit risk, and lifetime losses for instruments showing significant increase in credit risk.

In the simplified approach, ECL is computed based on lifetime losses on financial instruments, irrespective of whether it is showing significant increase in credit risk or not. This approach is mandatory for trade receivables not having a significant financing component. This approach is option for lease receivables and trade receivables having a significant financing component.

Therefore, for lease transactions, a reporting entity can opt for either of the two approaches.

Staging of financial instruments based on different risk categories is one of the key aspects of the general approach. There are three stages:

a) Stage 1 – A financial instrument is classified under Stage 1 at the inception of the transaction, unless the asset is credit impaired at the time of purchase. Subsequently, if the assets do not show significant increase in credit risk, they are classified under Stage 1.

b) Stage 2 – A financial instrument is classified under Stage 2, when it shows significant increase in credit risk. The credit risk on the reporting date is compared with the credit risk at the time of initial recognition.

c) Stage 3 – Lastly, if the financial asset shows objective evidence of impairment, the asset is credit impaired and classified as Stage 3.

For the purpose staging, the following considerations may be taken care of:

An entity can rebut this presumption if it has reasonable and supportable information that is available without undue cost or effort, that demonstrates that the credit risk has not increased significantly since initial recognition even though the contractual payments are more than 30 days past due. However, the Reserve Bank of India in its notification on Implementation of Indian Accounting Standards for NBFCs[1], has stated that in case, the reporting entity wishes to rebut the presumption, then clear justification must be documented, and such shall be placed before the Audit Committee of the Board. However, in any event the recognition of significant increase in credit risk should not be deferred beyond 60 days past due.

Further, when an entity determines that there have been significant increases in credit risk before contractual payments are more than 30 days past due, the rebuttable presumption does not apply.

Once the staging is complete the expected credit losses on the assets depending on their stage.

In case of Stage 1 assets, 12-months credit losses are provided. In case of Stage 2 and Stage 3 assets, lifetime credit losses are provided.

The difference between a Stage 2 and Stage 3 asset is that for the latter, the asset has to be impaired to the extent of the expected credit losses and the showed at net amount.

The graphic below summarises the general approach of ECL.

In the simplified approach, the concept of staging does not apply. There is no requirement of assessment of significant increase in credit risk. Lifetime credit losses have to be provided.

This is optional for lease transactions, however, if the reporting entity wishes to adopt this approach, it has to be implemented separately on operating and financial leases.

While computing ECL, operating lease and financial leases must be considered separately. While financial leases are financial transactions, hence, akin to loan transactions, operating leases are operating/ rental contracts. However, ECL, in the both cases, are done based on the future expected cash flows from the contract, that is the lease rentals.

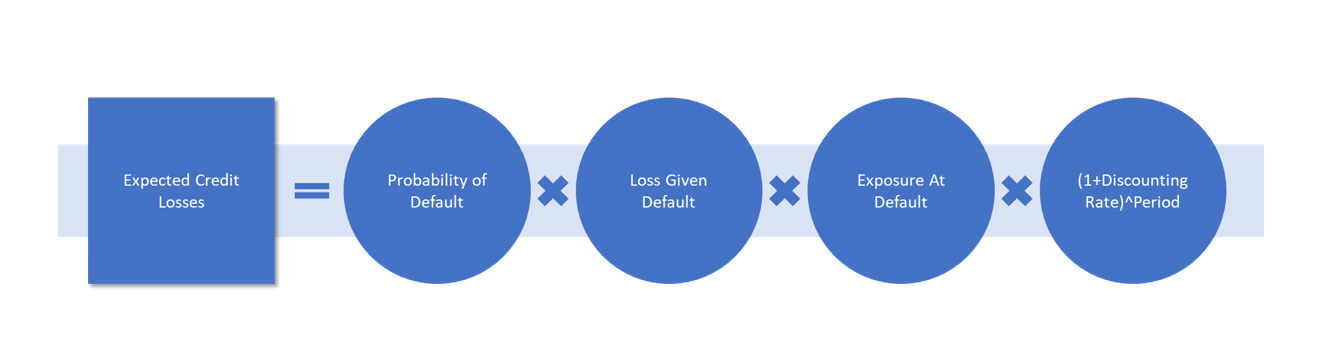

The most appropriate approach of computing ECL in case of lease transactions in the “Loss Rate Approach”. In this approach, the ECL is computed based on the Probability of Defaults and Loss Given Defaults. The PD and LGD rates are applied on the Exposure at Default, and subsequently, discounted at the effective interest rate or the yield of the transaction.

One of the most important components of computing ECL. For entities which follow Internal Risk Based Approach, this is usually an outcome of the IRB. However, where the reporting entity does not follow an IRB approach, a scorecard approach may be adopted for the same.

In a scorecard approach, various factors specific to the asset and the borrower are weighted to assess the credit risk and produce a PD level.

In case of lease transactions, besides the borrower specific factors, the experience in the asset class also must be given sufficient weightage. For example, personal use assets like cars, two-wheelers etc. may be assigned to a lower risk weight, whereas, for assets such as construction equipments, farming equipments, etc. where repayment of rentals depend on the generation of cash flows from the asset, may be assigned a higher risk weight.

Once the credit risk is assessed, the PD level has to be produced through:

Usually, PD levels are representation of the performance of similar assets in the past, however, for ECL, a forward-looking approach has to be adopted, and accordingly the PD levels have to be calibrated to give a forward-looking effect.

Alternatively, a simpler approach may be adopted where the reporting entities may rely on internal benchmarking and external ratings to predict a PD level.

The loss given default signifies what proportion of the exposure, will actually be lost, should there be a default. The LGD rate is a function of the past trends of recovery of cash flows organically, and also the recovery from the underlying asset.

Therefore, LGD can be denoted as 1 – Recovery Rate.

For determining the LGD of a lease, the following may be considered:

The estimation of the aforementioned may be influenced by several factors, namely, the sector in which the asset is deployed, the geography, nature of asset etc.

Macroeconomic factors and the dependence of the aforesaid factors on the same must also be considered. For examples, situations like flood or drought would impact the recoverability of tractors. Similarly, situations like the pandemic COVID-19, would impact all of the aforesaid factors.

This reflects the exposure outstanding periodically for the entire tenure of the loan.

Usually, the effective interest rate of the transaction is used for discounting the cash flows and the credit losses.

This refers to the contractual tenure of the facility. While determining the period, the ability of the customer to cancel or prepay, or the lessor’s ability to call the facility must also be considered.

The utilization of each of the factors for computation of ECL has been illustrated with the following numerical example:

| Scheduled Cashflows | Amort Schedule | |||||

| Period | Cash flows | Interest | Principal | Closing POS | ||

| 0 | ₹ -1,00,000.00 | ₹ – | ₹ – | ₹ -1,00,000.00 | ||

| 1 | ₹ 25,000.00 | ₹ 7,930.83 | ₹ 17,069.17 | ₹ -82,930.83 | ||

| 2 | ₹ 25,000.00 | ₹ 6,577.10 | ₹ 18,422.90 | ₹ -64,507.93 | ||

| 3 | ₹ 25,000.00 | ₹ 5,116.01 | ₹ 19,883.99 | ₹ -44,623.94 | ||

| 4 | ₹ 25,000.00 | ₹ 3,539.05 | ₹ 21,460.95 | ₹ -23,162.98 | ||

| 5 | ₹ 25,000.00 | ₹ 1,837.02 | ₹ 23,162.98 | ₹ 0.00 | ||

| EIR | 8% | |||||

| Computation of ECL | ||||||

| Period | EAD | PD (Marginal) | PD (Cumulative) | LGD | EIR | Marginal ECL |

| 0 | ||||||

| 1 | ₹ 1,00,000.00 | 3% | 3% | 20% | 8% | ₹ 555.91 |

| 2 | ₹ 82,930.83 | 3% | 6% | 20% | 8% | ₹ 427.15 |

| 3 | ₹ 64,507.93 | 3% | 9% | 20% | 8% | ₹ 307.84 |

| 4 | ₹ 44,623.94 | 4% | 13% | 20% | 8% | ₹ 263.07 |

| 5 | ₹ 23,162.98 | 4% | 17% | 20% | 8% | ₹ 126.52 |

| 12 Month’s ECL | ₹ 555.91 | |||||

| Lifetime ECL | ₹ 1,680.49 | |||||

| EIR | Computed using IRR formula | |

| PD and LGD | Assumed numbers | |

| Marginal ECL | (PD*LGD*EAD)/(1+EIR)^Period | |

This article only tries to discuss one of the most commonly adopted approach for ECL computation. There could be several variations made to the aforementioned, or different approaches may be adopted. Ultimately, it is the management’s call to decide the approach which best suits the nature of the assets and the customers the entity is the dealing with.

[1] https://www.rbi.org.in/scripts/FS_Notification.aspx?Id=11818&fn=14&Mode=0