SEBI’s ease of doing business for trusts and amendment in ‘Fit and Proper person’ criteria

– Abhishek Namdev, Assistant Manager | corplaw@vinodkothari.com

– Abhishek Namdev, Assistant Manager | corplaw@vinodkothari.com

Manisha Ghosh, Senior Executive | finserv@vinodkothari.com

Investment limits under Voluntary retention route (Rs. 2,50,000 crore) for investment in corporate bonds and G-secs have been merged and made a part of the limit assigned for regular investments by FPIs under General Route (15%, 2% and 6% of outstanding stock of Corporate debt securities, State Government securities and Central Government respectively); as a result, FPIs that commit to keep funds for at least 3 years may escape the restrictions applicable in case of corporate bonds relating to minimum residual maturity requirement and issue-wise limits on single FPI (not exceeding 50% of any issue). This introduces significant scope for those FPIs that are sure of staying invested in India for a long term, avoiding opportunism while granting them significant operational flexibility.

The Indian market has witnessed a sharp and sustained decline in FPI investments over the past few years, reflecting a clear shift toward net outflows. The data reflects a structural decline in FPI investments over the period, transitioning from strong inflows in 2020 to persistent net withdrawals from 2022 onwards. The brief stabilization in 2024 appears temporary rather than a trend reversal, suggesting continued caution or reallocation by FPIs in recent financial years.

Team Finserv | finserv@vinodkothari.com

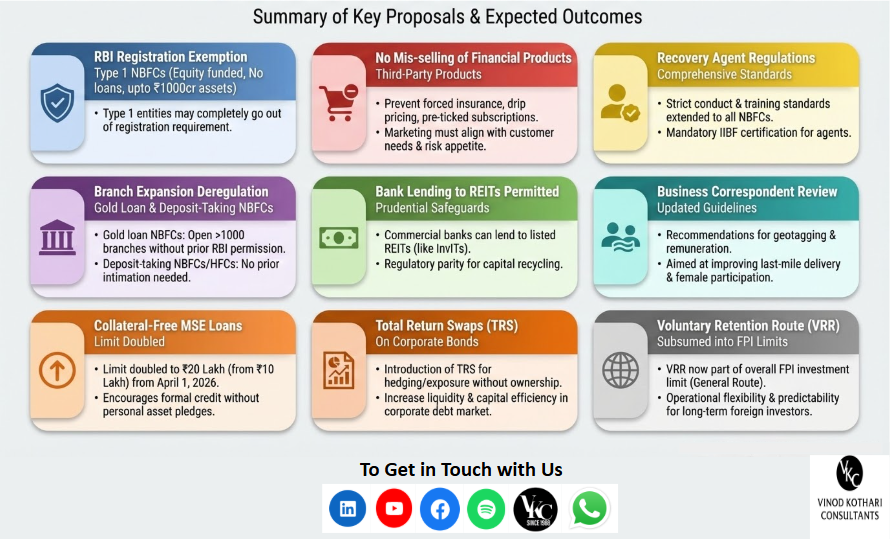

The Budget 2026 may not have brought any significant regulatory amendments or reliefs for the financial sector entities, however, the regulator has proposed a box full of surprises for the regulated entities. The Statement on Developmental and Regulatory Policies dated February 6, 2026 has proposed various significant changes. The measures span a wide spectrum, from exempting Type 1 NBFCs (with no public funds and no customer interface) from registration, to stricter norms on sale of third-party products, a harmonised recovery agent framework, permission for bank lending to REITs and an increase of collateral-free loan limits for MSMEs, among others. While the detailed guidelines for each of the proposals are yet to be issued, we provide a quick snapshot and implications of these proposals.

After several years of regulatory supervision over investment companies and small size NBFCs, the RBI has proposed to exempt NBFCs having no public funds and customer interface, with asset size not exceeding ₹1000 crore, from the requirement of registration. This will bring such NBFCs, which are commonly referred to as Type 1 NBFCs, outside the purview of RBI supervision, compliance and reporting requirements.

Earlier, access to public funds and customer interface were factors for applicability of several regulations, but not for complete exemption.

What is Customer Interface[1]

Para 6(4) of under the RBI (NBFCs – Registration, Exemptions and Framework for Scale Based Regulation) Directions, 2025 (“RBI Master Directions”) defines customer interface as “interaction between the NBFC and its customers while carrying on its business”

In essence, customer interface exists where an NBFC directly deals with customers in the course of its business, such as sourcing borrowers, communicating loan terms, collecting repayments, or addressing grievances. The concept focuses on direct dealing/direct public engagement between the NBFC and its customers in the conduct of its business.

Entities engaged in capital market transactions such as trading in shares, investments etc are not seen as having customer interface.

As to whether lending intragroup results in customer interface, the question is contentious – see our article here. .

Currently, NBFCs that do not have any customer interface are exempt from the fair lending practice norms, KYC norms, CIC reporting requirements are such other customer centric compliances.

What is “Public Funds”

Public funds is defined under RBI Master Directions as “includes funds raised either directly or indirectly through public deposits, inter-corporate deposits, bank finance and all funds received from outside sources such as funds raised by issue of Commercial Papers, debentures etc. but excludes funds raised by issue of instruments compulsorily convertible into equity shares within a period not exceeding five years from the date of issue.”

The expression public funds is much wider than public deposits; public deposits are only one part of it. Public funds broadly mean all funds raised by an NBFC from sources other than its own or self-funds. The definition is inclusive and covers multiple forms of debt funding, while also leaving room for other similar sources. Importantly, public funds are to be understood in contrast with self-funds, such as equity capital, which represent ownership and not fundraising. Funds raised from group entities are generally not regarded as public funds; however, if a group entity merely acts as a conduit for funds raised from the outside sources, such funds will still carry the character of public funds due to the direct and clear nexus with the public source.

The use of public funds is a key trigger for prudential regulation, as the RBI seeks to ensure safety and stability where public money is involved. In the absence of access to public funds, NBFCs are exempted from complying with prudential regulations, liquidity risk management framework and LCR norms.

Why Customer Interface and Public Funds Are Important

The RBI uses customer interface and public funds as risk filters to determine the extent of regulatory oversight required for an NBFC. Entities that neither deal with external customers nor raise public funds are considered to pose minimal consumer and systemic risk.

In line with this risk-based approach, the RBI has proposed to exempt NBFCs with no customer interface and no public funds, and with asset size not exceeding ₹1,000 crore, from the requirement of registration.

Banks and NBFCs routinely distribute third-party products alongside extending their core financial services. Such distribution is undertaken both through physical branches and through digital lending applications and platforms. It has, however, been frequently observed that certain banks and NBFCs take undue advantage of borrowers by using deceptive practices and dark patterns to sell third party products.

Dark patterns are tricky user interfaces “that benefit an online service by leading users into making decisions they might not otherwise make. Some dark patterns deceive users while others covertly manipulate or coerce them into choices that are not in their best interests[2]. Hence, there comes a need to regulate the same. The Central Consumer Protection Authority (“CCPA”), issued the Guidelines for Prevention and Regulation of Dark Patterns, 2023 to regulate such practices.

Digital lenders themselves may quite often be employing practices such as:

Accordingly, there is a felt need to ensure that third party products and services that are being sold at the bank counters or lending platforms are suitable to customer needs and are commensurate with the risk appetite of individual clients. It has therefore been decided to issue comprehensive instructions to REs on advertising, marketing and sales of financial products and services. The draft instructions in this regard shall be issued shortly for public consultation.

RBI has, from time to time, reminded lenders that they shall remain fully responsible for activities outsourced by them and, accordingly, are accountable for the conduct of their service providers, including recovery agents. In particular, the regulator has emphasised that lenders must ensure that neither they nor their agents engage in any form of intimidation or harassment, whether verbal or physical, during debt recovery.

While detailed guidelines governing the conduct of recovery agents are prescribed for HFCs, similar comprehensive guidelines are currently not specifically extended to NBFCs. RBI has now proposed that it will harmonise all the extant conduct-related instructions on engagement of recovery agents and other aspects related to the recovery of loans for all regulated entities.

An important requirement for recovery agents was with respect to the training of recovery agents. The recovery agents engaged by HFCs are required to undergo the training as prescribed by Indian Institute of Banking and Finance (IIBF) and obtain the certificate from the institute. If such training and certification requirements for recovery agents are extended to NBFCs, it will increase compliance and operational costs due to training expenses, certification fees, and time invested in upskilling agents. NBFCs may also need to strengthen their internal processes for onboarding, monitoring, and periodic re-certification of recovery agents. However, while this may raise short-term costs, it is likely to improve the quality of recoveries, reduce customer complaints and conduct risk, and strengthen long-term operational discipline.

As per the RBI Branch Authorisation Directions, NBFC-ICCs engaged in the business of lending against gold collateral are required to obtain prior approval of the RBI to open branches exceeding 1,000. Further, deposit-taking NBFCs and HFCs are required to inform the RBI and NHB, respectively, before opening any branch.

RBI has proposed to dispense with the requirement of prior approval or intimation for opening branches by such NBFCs. The change is likely to reduce hurdles in opening new branches for gold loan NBFCs, allowing them to expand more quickly and grow their operations.

| Type of NBFC | Erstwhile Requirement | Proposed Requirement |

| Deposit Taking NBFCs | Prior Intimation for the opening of branches | No need for prior intimation |

| HFCs | Prior Intimation to NHB before opening any branch | No need for prior intimation |

| NBFC-ICC (involved in gold lending) | Prior approval is required for branches exceeding 1000 | No need for prior approval |

The draft amendment directions have been issued here.

Banks were originally not permitted to lend to either InvITs or REITs, as these vehicles were created to refinance banks’ exposures in completed projects using market-based investor funds. While bank lending to InvITs was later allowed, subject to a prudential framework prescribed by the RBI. Banks must have a Board-approved policy governing InvIT exposures, covering appraisal, sanctioning, internal limits, and monitoring.

Prior to lending, banks are required to assess critical parameters including sufficiency of cash flows at the InvIT level, ensure that the combined leverage of the InvIT and its underlying SPVs remains within approved limits, and continuously monitor SPV performance, as the InvIT’s repayment capacity depends on these SPVs; banks must also consider the legal aspects of lending to trust structures, particularly enforcement of security. Lending is permitted only where none of the underlying SPVs with existing bank loans is facing financial difficulty, and any bank finance used by InvITs to acquire equity in other entities must comply with existing RBI restrictions.Lending to REITs, however, continued to be prohibited.

Regulatory Cap on Bank Investment in REITs/InvITs:

In view of the strong regulatory, disclosure, and governance framework applicable to listed REITs, it is now proposed to permit commercial banks to lend to REITs, subject to appropriate prudential safeguards. At the same time, the existing lending framework for InvITs will be harmonised with the safeguards proposed for REITs to ensure consistency and parity across both structures.

The proposal allows banks to lend to REITs within a well-defined risk framework, ensuring financial stability is not compromised. The proposal brings regulatory consistency between REITs and InvITs, creating a more uniform and predictable regime. At the same time, it enables efficient recycling of capital from completed real estate and infrastructure projects, supporting new lending without adding significant systemic risk.

A Business Correspondent (‘BC’) acts as an extension of a bank itself, to provide banking related services in areas which do not have access to such services. The intent of the BC model is financial inclusion, in order to connect everyone to the banking system. The scope includes among other things, creating awareness about savings and other products and education and advice on managing money and debt counselling, processing and submission of applications to banks, etc.

The activities to be undertaken by the BCs would be within the normal course of the bank’s banking business, but conducted through the BCs at places other than the bank premises/ATMs. Thus, the scope would not just be limited to marketing, sourcing and distribution of financial products, rather, it would be extended to provide banking services to the customers from the place of business of the BC.

Business Correspondents have been functioning as critical enablers of last mile access to financial services, particularly in respect of underserved, rural, and remote locations. Presently, BCs are regulated through RBI (Commercial Banks – Branch Authorisation) Directions, 2025. The Directions outline the eligibility criteria, due diligence requirements, oversight and monitoring, scope of activities, etc for engaging a Business Correspondent by banks.

RBI had set up a committee, consisting of officials from RBI , Department of Financial Service, Indian Banking Association and NABARD, to comprehensively examine their operations and make suitable recommendations for enhancing their efficiency. Discussions were held on action points of the previous meeting, Geotagging of BCs, Development of BC portal, Penalties imposed by banks on CBCs, Caution Money required from CBCs, BC Remuneration, participation of women in BC workforce etc.

Based on the Committee’s recommendations, the related regulatory guidelines are being reviewed, and the draft amendment directions will be issued shortly.

In 2010, following the RBI Working Group’s report (released March 6, 2010) on the Credit Guarantee Scheme (CGS) under CGTMSE, RBI mandated banks via circular in May 2010 to provide collateral-free business loans up to Rs. 10 lakh to Micro and Small Enterprises (MSEs).

A collateral-free business loan is an unsecured loan for business needs, requiring no pledge of assets like house, car, or property as mortgage until repayment backed by CGTMSE guarantee cover.

| MSEs are defined under the MSMED Act, 2006 and require mandatory Udyam Registration for eligibility, bank loans, priority sector benefits, and CGTMSE coverage—along with no blacklisting, viable project, and engagement in approved manufacturing/service/retail activities. Classifications: Micro enterprise (investment in plant/machinery ≤ Rs. 2.5 crore; turnover ≤ Rs. 10 crore); Small enterprise (investment ≤ Rs. 25 crore; turnover ≤ Rs. 100 crore); and Medium enterprise (investment ≤ Rs. 125 crore; turnover ≤ Rs. 500 crore). Banks must enforce this at branches, linking CGS/CGTMSE usage to staff evaluations for strict compliance. This remains the existing statutory requirement for MSE lending. |

RBI has decided to raise the collateral-free loan limit for MSEs from Rs. 10 lakh to Rs. 20 lakh, applicable to loans sanctioned or renewed on or after April 1, 2026, aiming to improve formal credit access, entrepreneurial activity, and last-mile delivery for collateral-scarce MSEs.

This policy shift represents a watershed moment for India’s grassroots economy, effectively doubling the financial runway for the nation’s most resilient entrepreneurs. By aligning with the PMMY ceiling, the policy ensures that a business’s potential rather than a proprietor’s personal property dictates its growth. This extra funding allows small businesses to move beyond daily expenses and finally invest in better machinery or technology to compete. Furthermore, it opens doors for women and young owners who may not own property to get formal bank support based purely on their performance. Ultimately, this change encourages more businesses to register officially, clearing the path for millions of small units to scale up and create more jobs without the fear of losing personal assets.

A Total Return Swap (TRS) is a derivative contract where a protection buyer exchanges the variable total return of an asset for a fixed return, shielding them from volatility. In this setup, the protection buyers swap the “total return” from the asset pool, with a return computed at a fixed spread on a base rate, say LIBOR. Protection sellers in a TRS guarantee a prefixed spread to protection buyers, who in turn, agree to pass on the actual collections and actual variations in prices on the credit asset to protection sellers. Essentially, the protection seller gains market exposure without a large upfront investment, while the protection buyer hedges their risk. Since protection sellers receive the total return from the asset, protection sellers also have the benefit of upside, if any, from the reference asset.

In India, the corporate bond market has historically lacked deep liquidity. To solve this, the Union Budget 2026 and the RBI have proposed introducing TRS specifically for corporate bonds and credit indices.

This development is a strategic shift toward “capital-efficient” investing. For business professionals, this means institutional investors can now gain exposure to corporate debt or hedge their existing bond portfolios without locking up massive amounts of capital on their balance sheets. By allowing the market to trade the “risk” and “returns” of bonds separately from the bonds themselves, the RBI aims to boost liquidity and make it easier for companies across various credit ratings to raise funds. Ultimately, this reform bridges a critical gap in India’s financial ecosystem, transforming the corporate bond market into a more active, transparent, and globally competitive space.

The draft amendment directions have been issued here.

Voluntary retention route for investment bonds and G-secs has been merged and made a part of the limit assigned for regular investments by FPIs; as a result, FPIs that commit to keep funds for at least 3 years may escape the minimum residual maturity requirement and the limits on investment in a bond issue by a single FPI. This introduces significant flexibility for those FPIs that are sure of staying invested in India for a long term, avoiding opportunism while granting them significant flexibility.

According to the Master Direction – Reserve Bank of India (Non-resident Investment in Debt Instruments) Directions, 2025, there are 5 channels of investments in debt instruments by non-resident investors. Under the VRR Route, FPIs are granted various operational exemptions, easing the investment process. VRR was introduced to encourage long term FPI investment in Indian debt markets by offering a dedicated investment channel with greater flexibility.

Given the strong utilisation of the VRR limits and to improve predictability and ease of doing business, the RBI has now decided to subsume VRR investments within the overall FPI investment limits under the General Route, while also providing additional operational flexibilities to FPIs investing through the VRR.

The detailed mechanism governing such limits has been notified here.

[1] Refer to our detailed write up on this topic- https://vinodkothari.com/2025/09/all-in-the-group-and-still-a a-customer/

– Neha Malu, Associate | finserv@vinodkothari.com

On 8th May, 2025, RBI notified amendments to the Master Direction – Reserve Bank of India (Non-resident Investment in Debt Instruments) Directions, 2025, governing investments by Foreign Portfolio Investors in corporate debt securities. The changes impact both the general investment route and the Voluntary Retention Route (VRR).

A. Removal of short-term investment limit:

In the case of general route, the earlier cap that restricted a FPI investment in corporate debt securities with residual maturity of up to one year to 30% of its total investment in such securities has been repealed.

However, under the general route, a separate provision, clause 4.4(i) continues to allow investment only in securities with original/residual maturity above one year. Therefore, while the 30% threshold is no longer relevant, FPIs under the general route still cannot invest in short-term corporate debt except debt securities provided in para 4.4(viii) which includes SRs and debt instruments issued by ARCs, debt instruments issued under CIRP, default bonds, PTCs and SDIs issued and listed as per SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008.

Under the VRR scheme, however, pursuant to para 5.4(v), the minimum residual maturity requirement does not apply. This means FPIs opting for the VRR can invest in corporate debt securities with shorter maturities, offering greater flexibility.

B. Withdrawal of concentration limits:

The previous restriction that capped FPI investment (including its related entities) in corporate debt securities to 15% (for long-term FPIs) and 10% (for other FPIs) of the prevailing investment limit has also been withdrawn.

The removal of these limits simplifies the regulatory framework and provides FPIs greater flexibility in structuring their debt portfolios. It may also help in improving the depth and liquidity of the corporate bond market, particularly in the short-end of the maturity spectrum.

| Our FPI resource centre is available at: https://vinodkothari.com/resources-on-fpi/ |

Prapti Kanakia | corplaw@vinodkothari.com

August 2, 2024 (original article dated October 31, 2023)

SEBI Circular, effective 1st November 2023, required FPIs to provide the details of their beneficial owners without applying any threshold in the shareholding or on layers of intermediate entities until all the natural persons are identified. An enabling provision to this effect had also been inserted as Reg. 22(6) in SEBI (Foreign Portfolio Investors) Regulations, 2019 effective from 10th August 2023. SEBI vide circular dated 27th July, 2023, had also mandated all non-individual FPIs to obtain Legal Entity Identifier (LEI) number by 23rd January 2024[1]. However, LEI could not address the requirement of additional disclosures as the LEI data stops at the parent entity level and does not provide the details of natural persons in control of the entity.

As to what could be the trigger for these regulatory changes may be anybody’s guess, but tacitly, the SEBI circular dated 24th August, 2023[2] (Circular) introducing some significant changes in beneficial ownership details by FPIs, made several admissions. It seemingly admitted that the disclosure of beneficial ownership by FPIs took advantage of technicalities by structuring the holding of natural persons to less than 10%. It also admitted that several FPIs had concentric investments in a single corporate group, making it apparent that these FPIs were used as conduits for investing in a single entity, and therefore, there may be affiliation between the FPIs and the controlling shareholders.

Briefly stated, the changed norms required FPIs, which have either (a) 50% or more of their Indian equity AUM in a single corporate group; or (b) hold along with investor group more than INR 25,000 Crore of equity AUM in Indian markets, to disclose their beneficial ownership, drilled down to the natural person level, irrespective of the percentage of holding, unless eligible for exemption.

These requirements, though effective from 1st November 2023, gave a time frame of 90 calendar days for existing FPIs to re-adjust their holdings. Meaning, FPIs had time till 29th January 2024 to realign their investment within the threshold prescribed in order to avoid providing the details of the beneficial owner as required under the Circular. Post 29th January 2024, FPIs whose investment continued to exceed the threshold as mentioned above were required to disclose the details of beneficial owners within 30 trading days ending on 12th March 2024, which if not provided led to cancellation of the FPI registration license and in the interim, blocking of account for further purchase of equity securities and restricted voting rights in investee companies.

The new norms differed from the erstwhile norms, where BO disclosure was required if a natural person’s beneficial holding exceeded the threshold as prescribed under PML (Maintenance of Records) Rules 2005, as indicated below:

Figure I – Threshold under PML (Maintenance of Records) Rules, 2005

The new norms required mandatory disclosure of BO, irrespective of the percentage of holding by the BO. No matter how many layers of entities covered the identity of the BO, FPIs had to identify the natural persons holding any ownership, economic interest, or exercising control, if the FPIs fall in either of the 2 categories discussed below, unless exempted.

If, instead of investing in a diverse pool of assets, an FPI has concentrated into a single corporate group, there are apparent concerns that the FPI is being used as a facade for making investments into a single entity. Thus, if on an AUM basis, more than 50% of the AUM of an FPI is in a “single corporate group”, the FPI has to provide the BO disclosure unless exempted (refer discussion below).

Intent: As per SEBI BM Agenda, the intent is to ensure there is no circumvention of minimum public shareholding norms or disclosures under SAST Regulations or investing funds routed through land border sharing countries and therefore, the need to obtain granular information around the ownership of, economic interest in, and control of FPIs with concentrated equity holdings in single companies or corporate groups.

Meaning of single corporate group: SEBI did not provide any clarity on single corporate group and left it to the stock exchanges/depositories. Rather than limiting to the existing law, BSE/NSE[3] identified a single corporate group more practically. Apart from entities having common control i.e. holding, subsidiary, associate, joint venture, and entities where promoters have major shareholding, entities which are mentioned on the website or in the annual report of the entity as a group company, have also been considered as a part of the group.

Basis this definition, BSE on its own identified the companies forming part of a single corporate group and asked the listed entities to confirm the name of the group as identified by BSE by sending communication in terms of Para 16 of the SEBI Circular that requires Stock exchanges/ Depositories to maintain a repository containing names of companies forming a part of each single corporate group and disseminate the same publicly on their websites[4].

FPIs with an AUM of more than INR 25,000 crore, either individually or along with their investor group[5], may pose a systematic risk in the Indian markets. It will be more concerning if such FPIs are tacitly controlled by unfriendly nations, and therefore, SEBI mandated BO disclosure from such FPIs too.

Intent: As per SEBI BM Agenda, the intent was to examine from the perspective of DPIIT Press Note 3 of April 17, 2020 (although not applicable to FPI investments), if the FPI route could potentially be misused to circumvent the stipulations of the same and disrupt the orderly functioning of Indian securities markets by their actions by having a substantial number of investors from countries that share land borders with India. It is likely that the FPI with a large Indian equity portfolio may itself be situated out of a non–land bordering country, the first level/ intermediate investors in such FPIs may be based out of land–bordering countries. This reiterated the need to obtain granular information around the ownership of, economic interest in, and control of such FPIs.

There might be cases where the FPI has taken exposure over an SCG only, however, may have investments globally as well and the percentage of Indian investments might be quite less when compared with its overall global investment. In such a scenario, there are fewer chances of FPIs being used as a conduit for avoiding compliance or hiding the identity of the BO. Therefore, the FPIs which are holding more than 50% of their Indian AUM in an SCG and such investments are less than 25% of their global AUM, are exempt from providing the BO disclosure.

SEBI vide circular[6] dated 20th March, 2024, further exempted SCG focused FPIs meeting the following conditions:

Intent: As per the Consultation Paper the intent is that if FPI has exposure in SCG with no identified promoter in the apex company, there is no risk of circumvention of minimum public shareholding provision and may be exempted from the disclosure requirement. Further, there is a possibility that even though the apex company itself has no identified promoter, the FPI might still hold a significant part of its portfolio in group companies that have an identified promoter and therefore if their holding in the group is not significant exemption can be granted.

Fig. II Exemption from disclosure requirement in case there is no promoter in SCG.

FPIs whose Indian AUM is more than INR 25,000 crore and their investments in India are less than 50% of their overall global investments are exempt from providing such disclosure since the probability of such FPIs being used as a facade to obtain control over Indian markets is quite less.

FPIs that have a wide investor base or are backed by the government or government related investors do not pose any risk to Indian markets or the probability is quite low, and therefore the following categories of FPIs are exempt from providing BO disclosure. Also, if the investors in FPI fall under the below mentioned categories, then identification of BO for such investors will not be required. In case the constituents of Large sized FPIs fall under below mentioned category, their holding will also not be aggregated with their investor group to calculate the limit of Rs. 25,000 Crore.

Figure III – List of exempted FPI[7]

The below figures provide a gist of the scenarios where FPIs are required to provide the disclosure

Figure IV – Flowchart depicting the scenarios that would warrant additional disclosures

The FPIs are put under the obligation to ensure compliance with the SEBI Circular, i.e. providing the BO disclosure and monitoring the concentration limit in a single corporate group and the equity investments in India. Additionally, DDPs are also required to monitor the same and intimate the FPIs wherever they breach the criteria and once the registration of FPI is invalidated as a result of non-disclosure, the Depository will intimate the investee listed company to freeze the voting rights of such FPIs to the extent of actual shareholding or shareholding corresponding to 50% of its equity AUM on the date its FPI registration is rendered invalid, whichever is lower (refer the example below).

To ensure that there is no regulatory arbitrage amongst DDPs, a standard operating procedure (SOP)[8] has been framed & followed by all the DDPs to independently validate the conformance of FPIs with the conditions and exemptions prescribed. The SOP is based on the application of the core principles of minimising Type II errors i.e. where legitimate FPIs and their investors face challenges of onerous regulatory requirements) without adding to Type I errors i.e., where FPIs that may be breaching regulations, circumvent the need to make disclosures that would bring such breaches to light, through the ‘trust – but verify’ route.

The FPIs whose registration is rendered invalid as a result of non-disclosure are restricted from casting their vote and it is the responsibility of investee listed company to ensure that the voting rights of such FPIs are freezed to the extent of actual shareholding or shareholding corresponding to 50% of equity AUM on the date its FPI registration is rendered invalid, whichever is lower. The said information will be provided by the depository to the investee listed entity/its RTA. The following example clarifies calculation of extent of shareholding to be freezed.

Eg. FPI XYZ has 60 shares of Company A and 40 shares of Company B as on May 13, 2024, and the FPI fails to make the additional disclosures, thereby rendering its FPI registration invalid from May 13, 2024. Thereafter, FPI’s voting rights shall be restricted to shareholding corresponding to 30 shares of Company A and 20 shares of Company B.

Suppose as on July 01, 2024, the FPI has liquidated some shares and holds 15 shares of Company A and 30 shares of Company B. As on this date, the FPI will be able to exercise voting rights corresponding to 15 shares of Company A but only 20 shares of Company B (maximum permissible voting rights in Company A).[9]

The listed entities were required to intimate the details of their corporate group to the stock exchanges and any change is to be intimated within 2 working days of the effective date of such change[10].

The non-compliant FPIs are also restricted from purchasing further equity shares, however, the responsibility is not upon the listed entity to not issue equity shares to such FPIs. The DDPs/Custodian will block the account of FPIs for further purchases and they cannot participate in any corporate action which increases the equity shareholding such as rights issue, FPOs, etc. However, credit as a result of any involuntary corporate actions such as bonus issue, scheme of arrangement, etc will be allowed.

SEBI had stated that there cannot be sustained capital formation without transparency and trust. The Circular is a move to foster trust and increase transparency in the Indian Capital markets. The Circular does not seem to be a hindrance to genuine FPIs, though operational challenges might be faced by the FPIs in identifying the BOs.

[1] 180 days from the date of issue of the SEBI Circular.

[2] The said circular was approved in the SEBI Board meeting dated 28th June, 2023

[3] Circular dated 30th November 2023

[4] NSE – https://www.nseindia.com/regulations/listing-compliance

BSE – https://www.bseindia.com/static/about/corporate_group_repository.aspx

[5] Investor group means FPIs which, directly or indirectly, have common ownership of more than 50% or common control.

[6] The said exemption was approved in the SEBI Board meeting dated March 15, 2024

[7] Exemption to University Funds fulfilling certain conditions granted vide SEBI Circular dated August 01, 2024

[8] https://av.sc.com/in/content/docs/in-sop-for-granular-reporting.pdf

[9] Calculation manner as provided in SOP

[10] BSE Circular dated 09th February, 2024

Shaifali Sharma | Vinod Kothari and Company

In March, 2019, the RBI with an objective to attract long-term and stable FPI investments into debt markets in India introduced a scheme called the ‘Voluntary Retention Route’ (VRR)[1]. Investments through this route are in addition to the FPI General Investment limits, provided FPIs voluntarily commit to retain a minimum of 75% of its allocated investments (called the Committed Portfolio Size or CPS) for a minimum period of 3 years (retention period).However, such 75% of CPS shall be invested within 3 months from the date of allotment of investment limits. Recognizing the disruption posed by the COVID-19 pandemic, RBI vide circular dated May 22, 2020[2], has granted additional 3-months relaxation to FPIs for making the required investments. The circular further addresses the questions as to which all FPIs are covered under this relaxation and how the retention period will be determined.

This article intends to discuss the features of the VRR scheme and the implications of RBI’s circular in brief.

RBI, to motivate long term investments in Indian debt markets, launched a new channel of investment for FPIs on March 01, 2019[3] (subsequently the scheme was amended on May 24, 2019[4]), free from the macro-prudential and other regulatory norms applicable to FPI investment in debt markets and providing operational flexibility to manage investments by FPIs. Under this route, FPIs voluntarily commit to retain a required minimum percentage of their investments for a period of at least 3 years.

The VRR scheme was further amended on January 23, 2020[5], widening its scope and provides certain relaxations to FPIs.

| Option 1

|

Continue investments for an additional identical retention period |

|

Option 2

|

Liquidate its portfolio and exit; or

|

| Shift its investments to the ‘General Investment Limit’, subject to availability of limit under the same; or

|

|

| Hold its investments until its date of maturity or until it is sold, whichever is earlier. |

Any FPI wishing to exit its investments, fully or partly, prior to the end of the retention period may do so by selling their investments to another FPI or FPIs.

As discussed above, once the allotment of the investment limit has been made, the successful allottees shall invest at least 75% of their CPS within 3 months from the date of allotment. While announcing various measures to ease the financial stress caused by the COVID-19 pandemic, RBI Governor acknowledged the fact that VRR scheme has evinced strong investor participation, with investments exceeding 90% of the limits allotted under the scheme.

Considering the difficulties in investing 75% of allotted limits, it has been decided that an additional 3 months will be allowed to FPIs to fulfill this requirement.

FPIs that have been allotted investment limits, between January 24, 2020 (the date of reopening of allotment of investment limits) and April 30, 2020 are eligible to claim the relaxation of additional 3 months.

The retention period of 3 years commence from the date of allotment of investment limit and not from date of investments by FPIs. However, post above relaxation granted, the retention period shall be determined as follows:

| FPIS

|

RETENTION PERIOD |

| *Unqualified FPIs | Retention period commence from the date of allotment of investment limit

|

| **Qualified FPIs opting relaxation

|

Retention period commence from the date that the FPI invests 75% of CPS |

| Qualified FPIs not opting relaxation

|

Retention period commence from the date of allotment of investment limit |

*Unqualified FPIs – whose investments limits are not allotted b/w 24.01.2020 and 30.04.2020

**Qualified FPIs to relaxation – whose investments limits not allotted b/w 24.01.2020 and 30.04.2020

Since no separate penal provisions are prescribed under the circular, in terms of VRR Scheme, any violation by FPIs shall be subjected to regulatory action as determined by SEBI. FPIs are permitted, with the approval of the custodian, to regularize minor violations immediately upon notice, and in any case, within 5 working days of the violation. Custodians shall report all non-minor violations as well as minor violations that have not been regularised to SEBI

The COVID-19 disruption has adversely impacted the Indian markets where investors are dealing with the market volatility. Given this, FPIs are pulling out their investments from the Indian markets (both equity and debt). Thus, relaxing investments rules of VRR Scheme during such financial distress, will help the foreign investors manage their investments appropriately.

You may also read our write ups on following topics:

Relaxations to FPIs ahead of Budget, 2020, click here

Recommendations to further liberalise FPI Regulations, click here

RBI removes cap on investment in corporate bonds by FPIs, click here

SEBI brings in liberalised framework for Foreign Portfolio Investors, click here

For more write ups, kindly visit our website at: https://vinodkothari.com/category/corporate-laws/

To access various web-lectures, webinars and other useful resources useful for the Corporate and Financial sector, visit and subscribe to our Youtube channel: https://www.youtube.com/channel/UCgzB-ZviIMcuA_1uv6jATbg

[1]https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11561&Mode=0

[2]https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11896&Mode=0

[3]https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11492&Mode=0

[4]https://www.rbi.org.in/Scripts/BS_CircularIndexDisplay.aspx?Id=11561

[5]https://rbidocs.rbi.org.in/rdocs/notification/PDFs/APDIR19FABE1903188142B9B669952C85D3DCEE.PDF

[6] https://rbidocs.rbi.org.in/rdocs/notification/PDFs/NT199035211F142484DEBA657412BFCB17999.PDF