Introduction to FEMA (NDI) Rules, 2019 and recent amendments

For relevant questions discussed during the webinar, click here.

For relevant questions discussed during the webinar, click here.

-Munmi Phukon, Pammy Jaiswal and Richa Saraf (corplaw@vinodkothari.com)

ICRA has published a report on 23.04.2020[1], listing out some 328 entities[2] who have availed or sought a payment relief from the lending institutions or investors. The list also includes names of such entities that have received an in-principle approval from investors in their market instruments (like non-convertible debentures)- prior to the original due date- for shifting the original due date ahead, but where a formal approval from the investors was received either after the original due date or is still pending to be received.

Earlier, Securities and Exchange Board of India (SEBI) had, vide circular no. SEBI/ HO/ MIRSD/ CRADT/ CIR/ P/ 2020/53 dated 30.03.2020[3], addressed to the credit rating agencies (CRAs), granted certain relaxation from compliance with certain provisions of the circulars issued under SEBI (Credit Rating Agencies) Regulations, 1999 due to the COVID-19 pandemic. The circular stipulated that appropriate disclosures in this regard shall be made in the press release, seemingly, the report published by ICRA is a part of the disclosure requirement specified by SEBI.

In view of the COVID crisis, companies in large numbers are approaching investors or will be approaching investors for restructuring of the debentures, therefore, it becomes pertinent to discuss- how the restructuring is carried on? whether a meeting of debenture holders will be required to be convened? what will be the consequences if the restructuring is not done? and other related questions. Below we discuss the same.

In financial terms, “default” means failure to pay debts, whether principal or interest. Under ISDA Master Agreement[4], failure by the party to make, when due, any payment is listed as an event of default and one of the termination events. However, the ISDA Master Agreement provides that in case of a force majeure event, payments can be deferred. Most of the standard agreements, contain specific clauses pertaining to force majeure, where the party required to perform any contractual obligation is required to intimate the other party as soon as it becomes aware of happening of any force majeure event. While in some cases, due to impossibility of performance, the agreement itself is frustrated; in some other cases, the obligations are merely deferred till the event persists.

Our article “COVID- 19 and The Shut Down: The Impact of Force Majeure” can be accessed from the link: https://vinodkothari.com/2020/03/covid-19-and-the-shut-down-the-impact-of-force-majeure/

A debenture holder has several options available in case of default: (a) insolvency proceedings; (b) enforcement of security interest; (c) proceedings for recovery of debt due. Below we discuss the same:

– Right to call for meeting of debenture holders: Rule 18 (4) of the Companies (Share Capital and Debentures) Rules, 2014 stipulates that the meeting of all the debenture holders shall be convened by the debenture trustee on:

– Right to make an application before NCLT: Section 71(10) of the Companies Act, 2013 provides that on failure of the company to redeem the debentures on the date of their maturity or failure to pay interest on the debentures when it is due, an application may be filed by any or all of the debenture holders or debenture trustee, seeking redemption of the debentures forthwith on payment of principal and interest due thereon.

– Application under IBC: Section 5(7) of IBC defines a “financial creditor” to mean any person to whom a financial debt is owed and includes a person to whom such debt has been legally assigned or transferred to, and Section 5(8) of IBC defines “financial debt” as a debt along with interest, if any, which is disbursed against the consideration for the time value of money and includes any amount raised pursuant to any note purchase facility or the issue of bonds, notes, debentures, loan stock or any similar instrument. Thus, debenture holders are treated as financial creditors for the purpose of IBC and may exercise all the rights as available to a financial creditor.

As per Section 6 of IBC-“Where any corporate debtor commits a default, a financial creditor, an operational creditor or the corporate debtor itself may initiate corporate insolvency resolution process in respect of such corporate debtor in the manner as provided under this Chapter”. Accordingly, the debenture holders (whether secured or not) may apply for initiation of corporate insolvency resolution process against the company under Section 7 of IBC. In fact the Central Government has, vide notification no. S.O. 1091(E) dated 27th February, 2019, notified that such right may also be exercised by the debenture holder, through a debenture trustee.

– Right to enforce security interest: The right of foreclosure is a counter-part of right of redemption. Just like a company has a right of redeeming the security after payment of debt amount, a secured debenture holder has a right of foreclosure or sale in case of default in redemption. In the case of Baroda Rayon Corporation Limited vs. ICICI Limited[5] and in Canara Bank vs. Apple Finance Limited[6], Bombay High Court upheld the right of the debenture trustee to sell off the properties of the company for the benefit of the debenture holders.

Here, it is pertinent to understand how the debenture holders shall exercise the right of foreclosure. The law distinguishes between security interests based on the nature of the collateral. For instance, in case of security interests on immovable properties, Chapter IV of Transfer of Property Act, 1882 applies. Further, the security interest, in case of secured debentures, can be enforced in the following manner: (a) In case the debenture holder is a bank/ financial institution, as per the provisions of Securitisation and Reconstruction of Financial Assets and Enforcement of Securities Interest Act, 2002; and (b) In case the debenture holder is not a bank/ financial institution, as per the common law procedures.

– Other remedies: Any default in the terms of the debentures is a breach of contract, and the debenture holder may sue the company for breach of contract as per the provisions of Contract Act, 1872, and further seek for compensation as per the terms of the debenture, or in absence of specific term in the agreement, compensation may be claimed as per the provisions of Section 73 of the Contract Act, 1872.

In view of the COVID pandemic one of the issue that was arising was that the issuers of debt instruments who were not able to fulfil the obligations as per the terms of the debentures or redeem the same on the maturity date were running to courts for seeking interlocutory reliefs, seeking to restrain the debenture holders from exercising any rights against the defaulting issuer. In the case of Indiabulls Housing Finance Ltd. vs. SEBI[7], the petitioner prayed for an ad interim direction to restrain any coercive action against it, with respect to the repayment to be made by it to its non-convertible debenture holders. In the said case, granting the prayer, the Hon’ble Delhi High Court directed maintenance of status quo with respect to the repayments to be made by the petitioner to the NCD holders.

Further, there was a lack of clarity on how rating and valuation of a security would be revised in view of the default or the restructuring? Therefore, SEBI has issued the following circulars:

With respect to recognition of default, the circular stipulates that CRAs recognize default based on the guidance issued vide SEBI circular dated May 3, 2010[9] and November 1, 2016[10], however, based on its assessment, if the CRA is of the view that the delay in payment of interest/principle has arisen solely due to the lockdown conditions creating temporary operational challenges in servicing debt, including due to procedural delays in approval of moratorium on loans by the lending institutions, CRAs may not consider the same as a default event and/or recognize default.

In the context of COVID, the restructuring of debentures shall mean nothing but deferral of the date of redemption. The terms of the debentures, including the maturity date, etc is specified in the terms of issuance. The terms of issuance also provides how the variation in terms can be effectuated. Therefore, it is pertinent that to make any changes in terms of debentures, the relevant clauses in the issuance terms are considered.

In terms of Reg. 59 (2) of the SEBI LODR Regulations, 2015, any material modification to the structure of debentures in terms of coupon redemption etc. are required to approved by the Board of Directors and the debenture trustee (DT). Further, in terms of Reg. 59(1), prior approval of the stock exchange(s) shall also be required for such material modification which shall be given by the stock exchange(s) only after obtaining the approval of the Board and the DT.

In addition to the approval as aforesaid, in terms of Regulation 15(2)(b) of SEBI DT Regulations, DT is required to call a meeting of the debenture holders on happening of any event which in the opinion of the DT affects the interest of the holders. Similar provision is there in the Companies (Share Capital and Debenture) Rules, 2014 also [sub- rule (4) of Rule 18].

Unlike the requirements of obtaining shareholders’ consent by way of special/ ordinary resolution for various matters including variation of rights thereof, there is no explicit provision for obtaining of a consent of the debenture holders for restructuring of the debentures under the Companies Act, 2013 (‘CA 13’). However, the provisions of SS 2 being, mutatis mutandis, applicable to a meeting of debenture holders also, all the provisions w.r.t convening/ conducting of general meeting such as, sending of notice, explanatory statement etc. as applicable to general meetings shall apply to the meeting of debenture holders.

However, looking at the current crisis situation, where calling of a physical meeting is not possible, and issuers will be required to hold the meeting of the debenture holders, in case consent by e-mail is not possible due to the large number of debenture holders, through video conferencing mode. The modalities for participation (like voting, two-way communication, recording, etc.) and other compliances related of sending of notices etc. may be in the manner clarified by the MCA Circular dated 13.04.2020[13].

In a nutshell, the procedural requirements to be followed for restructuring of debentures shall be as provided hereunder.

| S. No

|

Relevant Provisions | Actionable/ Compliance | Remarks |

| 1. | Regulation 50 (3) of LODR Regulations | Prior intimation to the stock exchange (SE) for the meeting board of directors, at which the restructuring is proposed to be considered.

|

2 working days in before the board meeting.

(excl. date of intimation and date of meeting) |

| 2. | Sec. 173 of CA 13 | BM to be convened by the Company for proposed restructuring including the revised terms subject to approval of the stock exchanges and the debenture holders.

|

Through VC considering the COVID 19 Guidelines issued by the Govt. Our FAQs in this regard may be found at : https://www.google.com/url?q=https://vinodkothari.com/2020/03/board-meetings-during-shutdown/&sa=D&source=hangouts&ust=1587820272757000&usg=AFQjCNEictCwK_-LNnlH7oiB1GMmdRzO6w

|

| 3. | Regulation 59(2)(a) of LODR Regulations

|

Obtain approval of the DT | Before applying to SEs. |

| 4. | Regulation 59 of the Listing Regulations | Seek prior approval from the stock exchange

|

After taking the consent of the board of directors and DT.

|

| 5. | Regulation 15(2) of DT Regulations, 1993 | Separate meeting of debenture holders to be called for deferment in repayment due to liquidity crunch in the hour of crisis.

|

The meeting may be called by the company itself or through the DT.

Since the scope of SS 2 issued by ICSI includes meetings of debenture holders also, the company will have to observe the requirements of SS 2 in convening the meeting of debenture holders. However, considering the current crisis situation, such meeting may be convened through VC facility as clarified by MCA Circular dated 13th April, 2020. Our FAQs in this regard may be found at https://vinodkothari.com/2020/04/general-meetings-by-video-conferencing-recognising-the-inevitable/

|

| 6. | Regulation 51 (2) of the Listing Regulations | Intimation to the stock exchanges being an action that shall affect payment of interest or redemption of NCDs

|

ASAP but not later than 24 hours of Board decision. |

In usual circumstances, if any variation is carried out in the debenture terms, the parties enter into an addendum, amending the clauses contained in the debenture subscription agreement (and also, in the trust deed/ security documents, if required), however, given the current scenario and the lock down, it is not possible for parties to sign and execute the agreements. Since the restructuring already has the approval of the majority debenture holders, it is deemed that the resolution “overrides the terms of issuance”. Thus, in our view, the resolution passed by the debenture holders approving the restructuring should suffice, and modification in the agreements may not be required.

[1] https://www.icra.in/Rationale/ShowRationaleReport/?Id=94320

[2] The rating agency has stated that the list is not a comprehensive one, as information about some rated entities are not readily available as of now, and separate disclosures will be made w.r.t. such entities.

[3]https://www.sebi.gov.in/legal/circulars/mar-2020/relaxation-from-compliance-with-certain-provisions-of-the-circulars-issued-under-sebi-credit-rating-agencies-regulations-1999-due-to-the-covid-19-pandemic-and-moratorium-permitted-by-rbi-_46449.html

[4] https://www.sec.gov/Archives/edgar/data/1065696/000119312511118050/dex101.html

[5] 2002 (2) BomCR 608, (2002) 2 BOMLR 915, 2003 113 CompCas 466 Bom, 2002 (2) MhLj 322

[6] AIR 2008 Bom 16, (2007) 77 SCL 92 Bom

[7]https://images.assettype.com/barandbench/2020-04/6ec54849-0188-4fe3-a841-88c2861124d5/Indiabulls_vs_SEBI.pdf

[8]https://www.sebi.gov.in/legal/circulars/mar-2020/relaxation-from-compliance-with-certain-provisions-of-the-circulars-issued-under-sebi-credit-rating-agencies-regulations-1999-due-to-the-covid-19-pandemic-and-moratorium-permitted-by-rbi-_46449.html

[9] https://www.sebi.gov.in/legal/circulars/may-2010/guidelines-for-credit-rating-agencies_1467.html

[10]https://www.sebi.gov.in/legal/circulars/nov-2016/enhanced-standards-for-credit-rating-agencies-cras-_33585.html

[11]https://www.sebi.gov.in/legal/circulars/apr-2020/review-of-provisions-of-the-circular-dated-september-24-2019-issued-under-sebi-mutual-funds-regulations-1996-due-to-the-covid-19-pandemic-and-moratorium-permitted-by-rbi_46549.html

[12] https://www.sebi.gov.in/legal/circulars/sep-2019/valuation-of-money-market-and-debt-securities_44383.html

[13] http://www.mca.gov.in/Ministry/pdf/Circular17_13042020.pdf

Please click below for youtube presentation on the above topic:

Our other content related to COVID-19 disruption may be referred here: https://vinodkothari.com/covid-19-incorporated-responses/

Our other articles relating to restructuring on account of COVID-19 disruption may also be viewed here:

Our presentation can be viewed here – https://vinodkothari.com/2021/09/structuring-of-debt-instruments/

-SEBI’s Order in Yes Bank promoters indicates long arm of the provision

Munmi Phukon | Partner | Vinod Kothari & Company

While structuring of instruments like debentures, parties resort to various covenants in order to protect the interests of the investors and also to reflect the intent and purpose of the parties more specifically. One fairly commonplace practice with promoters of Indian listed companies to raise funds on the strength of their shareholding in their companies. It is often observed that, in structuring such transactions, companies find innovative ways of creating pseudo security interests on shares. Therefore, a careful analysis of the documentation entered into by the parties is required to conclude whether the covenants amount to creation of an encumbrance or not.

SEBI has recently dealt with such a case[1], in which SEBI throws some light on what could constitute an encumbrance for the purpose of SEBI (SAST) Regulations, 2011 (Regulations). SEBI considered the covenants mentioned in the debenture trust deed (DTD) executed by the promoter entities of the listed entity at the time of issuance of NCDs and held the promoters liable for non-disclosure of the encumbrance created on the shares held in the listed entity.

SAST Regulations are considered to be a social welfare legislation. The aim and intent of the Regulations is to protect the interest of the investors and ensuring market integrity. That is why, the Regulations recognise the importance of event based and periodic disclosures, specifically by the promoters of the entity, through Regulation 29 to 31 thereof. It has always been seen as a measure for ensuring better corporate governance which in turn enables the regulators and stock exchanges to monitor the transactions of the promoters.

Transactions involving promoters’ shares are considered crucial in order to ensure transparency as regards the ownership/ control of the target company as well as price discovery of the shares in an informed manner. The genesis of the requirements of such disclosures arose in the beginning of 2009 when SEBI made it mandatory by amending the provisions of the erstwhile Regulations.

Later, similar requirements were provided in the revamped SAST Regulations vide Regulation 31 which requires the promoters to disclose about the shares of the target company encumbered by them on a yearly basis to the stock exchange(s) where the shares of the target company are listed and also to the target company. The promoters have also been mandated, by virtue of an amendment made in the said Regulation, to give declaration to the audit committee of the target company and the stock exchange(s) on a yearly basis about not having any encumbrance.

Further, SEBI vide its Circular dated 7th August, 2019[2] read with its Press Release-PR No.16/2019[3] requires the promoters to disclose to the stock exchange(s) and the target company, the detailed reasons for encumbrance if the combined encumbrance by the promoter along with PACs with him equals or exceeds, a) 50% of their shareholding in the target company; or b) 20% of the total share capital of the target company and also any positive changes therein thereafter within two working days from the creation of such encumbrance.

Furthermore, Regulation 29 requiring disclosure of acquisition/ disposal of shares of the target company by an acquirer on meeting certain threshold, interestingly, also provides that shares taken by way of encumbrance shall be treated as an acquisition, and shares given upon release of encumbrance shall be treated as a disposal and shall also require disclosure. In this context, it is pertinent to note if the pledgee/creditor gets voting rights also or has the right to cause the shareholder to vote as per the instructions of the creditor, the transaction would well amount to acquisition of control and hence, triggering the Regulation 3 as well.

The term ‘encumbrance’ is defined under Regulation 28(3) of the SAST Re gulations. Further, there has been an amendment to the existing definition w.e.f 29th July, 2019 vide SEBI (Substantial Acquisition of Shares and Takeovers) (Second Amendment) Regulations, 2019[4]. Evidently, the text of the existing definition signifies that it is an inclusive explanation and not an exhaustive one keeping the same open to different interpretations.

gulations. Further, there has been an amendment to the existing definition w.e.f 29th July, 2019 vide SEBI (Substantial Acquisition of Shares and Takeovers) (Second Amendment) Regulations, 2019[4]. Evidently, the text of the existing definition signifies that it is an inclusive explanation and not an exhaustive one keeping the same open to different interpretations.

SEBI had tried to clarify the broad definition through its FAQs that, non- disposal undertaking (NDU) will be covered under the purview of ‘encumbrance’. The FAQs also clarified that NDUs may, inter alia, include the following:

“- not encumbering shares to another party without the prior approval of the party with whom the shares have been encumbered;

As mentioned above, the existing text of the definition has been expanded. As claimed by SEBI itself, the amendments have been made in the context of recent concerns w.r.t. promoter/ companies raising funds from Mutual Funds/ NBFCs through structured obligations, pledge of shares, non- disposal undertakings, corporate/ promoter guarantees and various other complex structures, which reads as below:

“(3) For the purposes of this Chapter, the term “encumbrance” shall include,

The Order of SEBI seems to be an attempt of making an interpretation of certain clauses of the debenture trust deeds (DTDs) entered into by the promoter entities in the context of the then definition of ‘encumbrance’ provided u/r 28(3). SEBI found the following clauses in the DTDs and construed the same as creation of encumbrance on the shares of the listed company:

SEBI contended that the covenants related to maintenance of asset cover/ borrowing cap at all times restrict the abilities of the borrowers/ promoters to dispose of the shares of the listed entity held by them. Therefore, the same should be considered as encumbrance for the purpose of Regulation 28(3). Further, the requirement of obtaining prior approval/ consent of the debenture holders before disposing of the shares tantamount to be a non- disposal undertaking as clarified vide the FAQs which include not encumbering shares to another party without prior approval of the party with whom the shares have been encumbered.

In two passages in Salmon on Jurisprudence, 12th Edition, at Page 241 under the sub-heading “Rights in re propria and rights in re aliena” the learned author has stated thus:

“Rights may be divided into two kinds, distinguished by the civilians as Jura in re propria[5] and jura in re aliena[6]. The latter may also be conveniently termed encumbrances, if we use that term in its widest permissible sense. A right in re aliena or encumbrance is one which limits or derogates from some more general right belonging to some other person in respect of the same subject -matter. All other are jura in re propria.”

At Page 242 the learned author has observed as follows:

“it is essential to an encumbrance that it should in the technical language of our law, run with, the right encumbered by it. In other words, the document and the servant rights are necessarily concurrent. By time it is meant that an encumbrance must follow the encumbered right into the hands of new owners, so that a change of ownership will not free the right from the burden imposed upon it. If this is not so — if the right is transferable free from the burden — there is no true encumbrance.”

Thus, the true test of an encumbrance is the concurrence of the right with property – that the right attaches to property and travels along with it. Salmon has discussed encumbrances elaborately and mentions 4 types of encumbrances: leases, servitudes, security interests, and trusts. A lease confers a right to use the property. Servitude is a right to the limited use of the property such as the right of way or easements. Security interests (including mortgages) are encumbrances vested in a creditor. A trust is the obligation attached to property to hold it for the benefit of another.

Madras High Court also in the matter of M. Ratanchand Chordia And Ors. vs Kasim Khaleeli[7] held as below:

“The word “Encumbrances” in regard to a person or an estate denotes a burden which ordinarily consists of debts, obligations and responsibilities. In the sphere of law it connotes a liability attached to the property arising out of a claim or lien subsisting in favour of a person who is not the owner of the property. Thus a mortgage, a charge and vendor’s lien are all instances of encumbrances. The essence of an encumbrance is that it must bear upon the property directly and in-directly and not remotely or circuitously. It is a right in re aliena circumscribing and subtracting from the general proprietary right of another person. An encumbered right, that is a right subject to a limitation, is called servient while the encumbrance itself is designated as dominant.”

The following important features of encumbrances arise from the discussion above:

Negative Lien is used in banking parlance for a borrower to undertake not to create any charge on his property without the consent of the lender.

A negative pledge covenant does not give the negative pledgee a security interest or, in general, any other right in the debtor’s property.

It was held in Knott[8] that Negative Pledgee’s remedies are purely contractual and that the covenant confers no right in the property.

The generally accepted view as mentioned before is that the negative pledge does not create a proprietary or security interest and is therefore not registrable. [Tracy Hobbs, The Negative Pledge: A Brief Guide, 8(7) J.I.B.L.269 (1993)]

A “springing lien” refers to lien granted in the future by a debtor (borrower or lessee) in favor of its creditors whereby the right conferred on the lender springs into a full-fledged lien or pledge either on the happening of certain events, or the discretion of the person holding the pledge.

Whether a so-called springing lien will amount to encumbrance or security interest will depend on intent of parties. If the debtor is free to deal with the subject matter before the trigger events that transform a springing lien into full-fledged lien have taken place, it cannot be said that the lien is an obligation attached to property. Therefore, it will not amount to encumbrance. However, if the lien comes attached with restrictions on sale, it will amount to encumbrance, because the combination of restriction on sale, and automatic attachment of a right on the asset that cannot be sold, in conjunction, will amount to a passable burden on property.

As discussed earlier, an encumbrance carries certain features along with it. A mere restraint on sale or negative covenant is not an encumbrance. Having said so, SEBI’s view in this context may not be in line with the jurisprudence of encumbrance.

However, it is seen that SEBI has been constantly endeavoring to expand the scope of the disclosure requirements, in the wake of various corporate governance failure recently witnessed by the country. SEBI, realizing the recent concerns w.r.t. promoters raising funds through structured obligations, pledge of shares, NDUs and various other complex structures and its impact on the corporate governance structures, had amended the meaning of encumbrance provided in Regulation 28(3). The said amendment has been made to include all such structures including any restriction on the free and marketable title to shares, by whatever name called, whether executed directly or indirectly or any covenant, transaction, condition or arrangement in the nature of encumbrance, by whatever name called, whether executed directly or indirectly.

Considering the amended definition of the term ‘encumbrance’, apparently, SEBI’s intent gets clearer that it wants to include all the possible arrangements/ structures which may carry a potential dilution in the promoter holding. The views held by SEBI are still open for a contest before the Securities Appellate Tribunal.

Read our related articles:

For more updates, please visit our website.

[1] https://www.sebi.gov.in/enforcement/orders/mar-2020/adjudication-order-in-respect-of-two-entities-in-the-matter-of-yes-bank-ltd-_46477.html

[2] https://www.sebi.gov.in/legal/circulars/aug-2019/disclosure-of-reasons-for-encumbrance-by-promoter-of-listed-companies_43837.html

[3] https://www.sebi.gov.in/media/press-releases/jun-2019/sebi-board-meeting_43417.html

[4] https://www.sebi.gov.in/legal/regulations/jul-2019/securities-and-exchange-board-of-india-substantial-acquisition-of-shares-and-takeovers-second-amendment-regulations-2019_43812.html

[5] Right over one’s own property

[6] Right over someone else’s property

[7] https://indiankanoon.org/doc/548843/

[8] Knott v. Shepherdstown Manufacturing Co. 5 S.E. 266 (W. Va. 1888)

– by Megha Saraf

Updated as on 24th April, 2020

While currently the world is suffering due to the pandemic COVID-19, our regulatory authorities have been continuously providing reliefs/ relaxations to all corporate houses from making various compliances required under the statutory laws. While some of the major relaxations such as conducting extraordinary general meeting of shareholders through VC, making contribution to PM-CARES Fund as a notified CSR expenditure or making compliances under Listing Regulations have already been notified, MCA has come up with yet another Circular[1] granting relaxation from holding AGMs to such companies that follows calendar year as their financial year.

Section 2(41) of the Companies Act, 2013 (“Act, 2013”) lays down the definition of “financial year” as, “in relation to any company or body corporate, means the period ending on the 31st day of March every year, and where it has been incorporated on or after the 1st day of January of a year, the period ending on the 31st day of March of the following year, in respect whereof financial statement of the company or body corporate is made up:

Provided that where a company or body corporate, which is a holding company or a subsidiary or associate company of a company incorporated outside India and is required to follow a different financial year for consolidation of its accounts outside India, the Central Government may, on an application made by that company or body corporate in such form and manner as may be prescribed, allow any period as its financial year, whether or not that period is a year:”

XX

There are corporate groups where the structure of shareholding is such, that the holding company is situated outside India and is having Indian subsidiaries. The provisions of law provide that where the relationship between the group is such, that it requires the Indian company to follow a different financial year for the purpose of consolidation of its accounts with the accounts of the company situated outside India, such Indian company can have a different financial year. However, such company needs to apply to the Tribunal for the same.

Section 96 of the Act, 2013 provides that a company is required to hold an AGM within 6 months from the date of closing of the financial year. However, a newly incorporated company can have its first AGM within 9 months of the closure of the financial year.

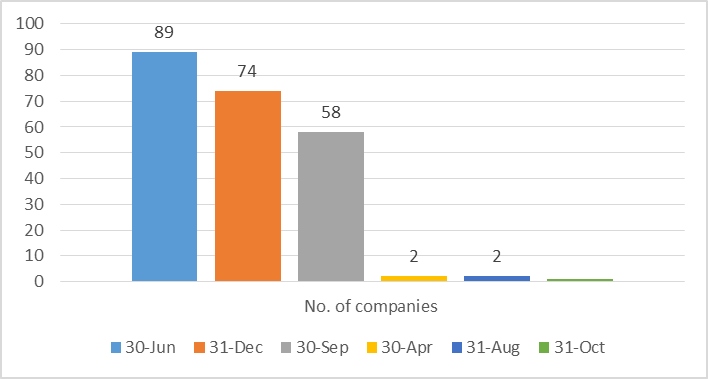

Source[2]: Business Standard: 226 firms to march to a new accounting year

Yes. As per the above graph, there are nearly 226 companies in India that follow a different financial year. Out of the 226 companies, 74 are such companies whose calendar year is the financial year i.e. January- December.

Currently, only companies that follows calendar year as financial year have been granted a 3-months relaxation from holding their AGMs i.e. such companies are allowed to hold their AGMs till 30th September, 2020 instead of June, 2020. Further, the due dates of all other related compliances such as filing of annual returns or financial statements which are required to be done within 60 days/ 30 days as applicable shall be construed accordingly.

Regulation 44(5) of the SEBI (LODR) Regulations, 2015 provides that where the listed entity is within top 100 listed entities based on market capitalization, they have to hold their AGM within 5 months from the closure of the financial year i.e. by August 31, 2020. However, considering the present situation and the need for social distancing, conducting AGMs within such time was becoming a challenge for large corporates. Keeping this in mind, SEBI has granted relief to such entities by extending the requirement by 1 month i.e. till September 30, 2020. However, there was no clarity on what if such entity is a listed entity and follows calendar year as their financial year and is among the top 100 listed entities.

SEBI has now also clarified the same vide its Circular[3] dated 23rd April, 2020 and the present timeline may be summarized as follows:

| Sl. No. | Type of company | Time line under the Companies Act, 2013 | Time line under the SEBI (LODR) Regulations, 2015 | Extended timeline |

| 1 | Listed company following Apr- Mar as F.Y. | Within 6 months from end of FY i.e. 30th September, 2020 | Does not provide | No extension |

| 2 | Listed company following Jan-Dec as F.Y. | Within 6 months from end of FY i.e. till 30th June, 2020 | Does not provide | Extended by 3 months i.e. till 30th September, 2020 |

| 3 | Listed company following Apr- Mar as F.Y. and amongst top 100 listed entities | General provision- Within 6 months from end of FY i.e. 30th September, 2020 | Within 5 months from end of FY i.e. till 31st August, 2020 | Extended by 1 month i.e. till 30th September, 2020 |

| 4 | Listed company following Jan- Dec as F.Y. and amongst top 100 listed entities | General provision- Within 6 months from end of FY i.e. 30th September, 2020 | Within 5 months from end of FY i.e. till 31st May, 2020 | Extended till 30th September, 2020 under both laws |

Therefore, all types of companies can conduct their AGMs till 30th September, 2020.

Our other articles on related subject may be found here.

[1] http://www.mca.gov.in/Ministry/pdf/Circular18_21042020.pdf

[2] https://www.business-standard.com/article/companies/226-firms-to-march-to-a-new-accounting-year-113100300666_1.html

[3] https://www.sebi.gov.in/legal/circulars/apr-2020/relaxation-in-relation-to-regulation-44-5-of-the-sebi-listing-obligations-and-disclosure-requirements-regulations-2015-lodr-on-holding-of-annual-general-meeting-agm-by-top-100-listed-entitie-_46552.html

Nidhi Ladha and Abhijit Nagee | corplaw@vinodkothari.com

Loading…

Loading…

Loading…

Loading…

Vinod Kothari and Payel Jain | corplaw@vinodkotari.com

Loading…

Vinod Kothari and Nidhi Ladha | corplaw@vinodkothari.com

Loading…