Policy Updates from SEBI: June Meeting Highlights

– Abhishek Namdev, Assistant Manager and Srihari G.S., Executive | corplaw@vinodkothari.com

The 19th June board meeting of SEBI witnessed significant decisions for capital markets, including, inter-alia, simplification of the securities transmission framework, reintroduction of open market buy-back through stock exchanges, the GARUDA mechanism for faster processing of AIF placement memoranda, amendments to the SDI Regulations aligning with RBI’s securitisation framework, and changes to the framework governing municipal debt securities, etc. While the changes in the text of respective regulations are awaited, we present our brief understanding of the various approved amendments.

- Simplification of transmission of securities (see Consultation Paper here)

- Quick Transmission Processing (QTP) for small-value claims –

| In case of physical holdings | Up to Rs. 10,000 |

| In case of demat holdings | Up to Rs. 30,000 |

- Limits for simplified documentation doubled: Rs. 5L to Rs. 10L (physical), Rs. 15L to Rs. 30L (demat).

- Relaxations pertaining to documentation:

- Requirement of submission of PAN is removed.

- The Probate of Will has been done away with.

- Combined affidavit-cum-NOC is permitted.

- A copy of death certificate with QR Code has been introduced as an eligible document.

- Verification from overseas branches of Indian banks – for death certificates issued in foreign jurisdictions

- Rationale – Aimed at reducing cost and procedural hardship for claimants by providing PAN and probate relaxations and alignment with recent succession law amendments.

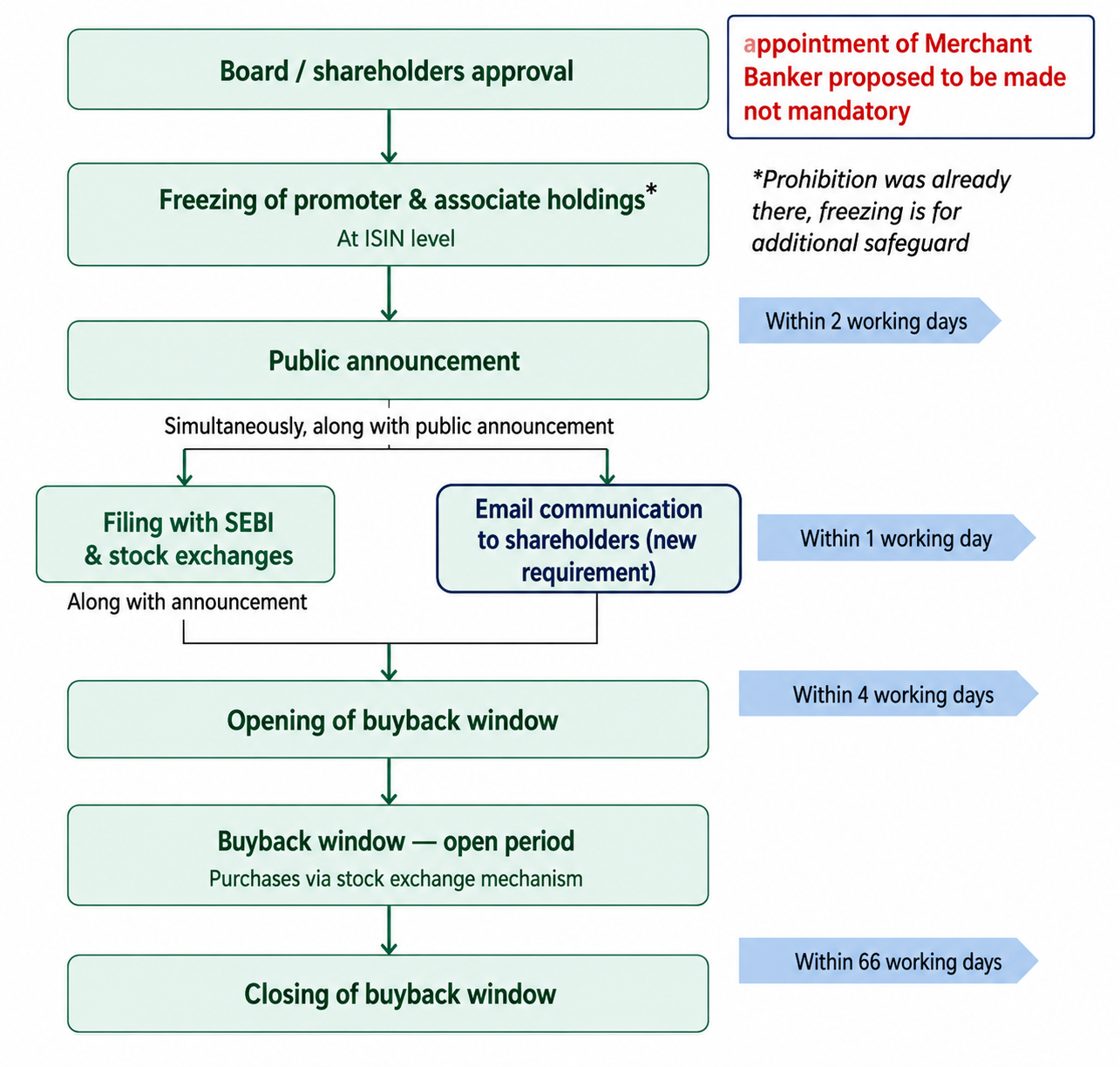

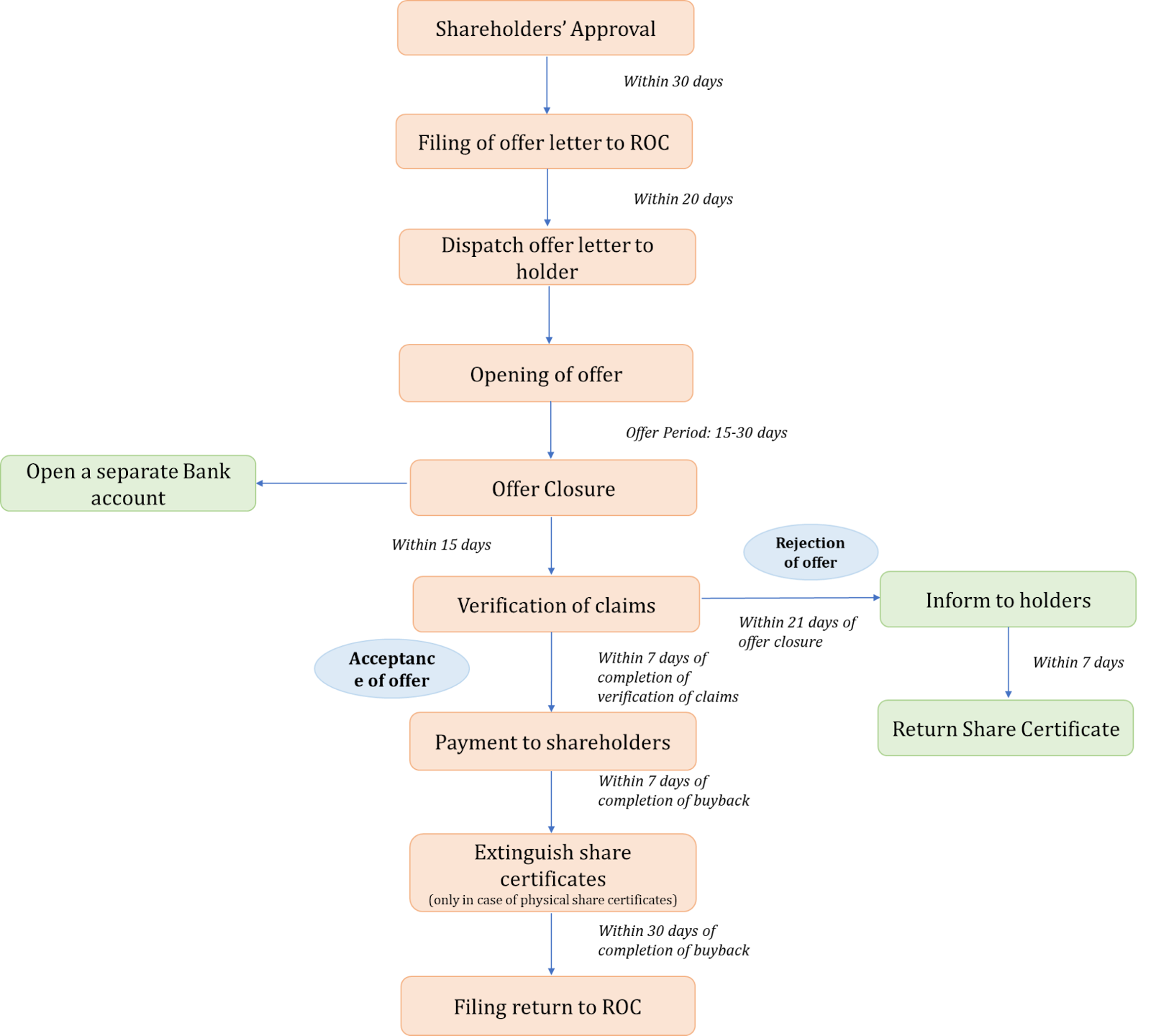

- Re-introduction of Open Market Buy back through Stock Exchanges and Review of the SEBI (Buy- back of Securities) Regulations, 2018 (see detailed write-up here.)

- Open market buy-back through SE route for buy-back to be effective from August 01, 2026

| Before Amendment | After Amendment |

| Tender offer route | Tender offer route |

| Open market route through reverse book building | Open market route through reverse book building |

| NA | Open market buy -back through stock exchange |

- Dissemination of information about buy-back to be made by way of electronic means in addition to Public announcement through newspaper advertisements.

- Buy-back through such route be completed within 66 working days from the opening of buy-back with at least 40% of funds earmarked shall be utilized during the first half of buy-back period.

- It will be treated as normal trading transaction(separate trading window is not required).

- Shares or securities under buy – backremain frozen at ISIN level during buy-back period for promoter(s) or his/their associates (except for tendering shares in buyback offer).

- Explicit clarification to comply with minimum public shareholding requirement post buyback

- Intervals between two buy-backs aligned as per Companies Act, 2013 (1 year as per proviso to section 68(2)(g)).

- Appointment of a merchant banker is made discretionary. Accordingly, its activities can be assigned to:

- Company,

- Compliance Officer,

- Statutory Auditor,

- Secretarial Auditor, and

- Stock Exchange

Rationale: The aforesaid amendment is driven by the revision in taxation framework, with the objective of offering an additional, flexible buy-back route, reducing procedural complexity, alignment with the Companies Act, 2013 and strengthening investor protection. Discretionary Merchant Banker appointment reduces cost, with duties reallocated to existing compliance/audit functionaries.

- Easing entry for AIFs: AIF Rollout Upon Document Acknowledgement (GARUDA) Mechanism for Processing of Placement Memorandum of AIFs filed with SEBI (see Consultation Paper here)

- Timeline for launch of new schemes with SEBI by AIFs has been reduced from 30 days to 10 working days for AIFs

- For large value funds, accredited investor (‘AI’) only schemes and Angel Funds, filing of PPM exempt in view of the sophisticated investor class involved.

- Aligning issue of Securitised Debt Instruments (SDIs) with RBI Directions on securitisation (see Consultation Paper here)

- Permitting single-asset securitisation transactions by RBI-regulated entities

- Omitting the condition of single-obligor concentration limit of 25% of the asset pool for RBI-regulated entities

- Shifting of disclosure and reporting obligations from originator to servicer to align with current marker practice.

- Trustees associated with the RBI-regulated originator to be limited to maximum of 1 representative

- In other cases, cannot constitute more than one-half of the Board of Trustees of the SPDE.

- Clarification that the prohibition on acquisition of debt/ receivables by SPDE is if:

- the originator is part of the same group as that of the trustee or the originator is under the same control as that of the trustee

- SEBI to appoint a new trustee while suspending/ cancelling the registration of an old trustee

- Existing provisions required winding up of schemes of SPDE upon suspension/ cancellation of trustee’s registration

- Rationale for amendment: To align provisions of SDI Regulations in relation to securitisation transactions originated by Regulated Entities (REs) of RBI with the RBI regulatory framework.

- Furthering development of municipal bond market: Amendments to SEBI (Issue and Listing of Municipal Debt Securities) Regulations, 2015 (‘ILMDS Regulations’) (see Consultation Paper here)

- Permitting municipalities to raise funds for re-financing of existing debt of specific project(s) subject to appropriate disclosures

- Disclosure requirements and operational aspects specified for raising of funds through a pooled finance vehicle. Clause (l) of Regulation 2(1) contains enabling provisions for raising of funds through such vehicle.

- Encourage retail participation through

- Permitting Electronic modes for making advertisements for public issues.

- Permitting offer incentives in the form of additional interest or a discount to the issue price to certain categories of investors, namely senior citizens, women, serving and retired defence personnel, widows and widowers of defence personnel, retail individual investors.

- Permitting face value/trading lot for Municipal debt securities issued on private placement basis at Rs. 1 lac or lower value of Rs. 10,000/- with fixed maturity and without any structured obligations

- Extension in timeline for post-issue listing compliances:

- submission of quarterly financial results within 60 days from end of FY (previously 45 days) Audit annual financial results within 90 days from end of FY (previously 60 days)

- Rationale: The amendments are intended to develop the municipal bond market and to encourage retail participation while maintaining appropriate investor protection safeguards.