Posts

Expected to bleed: ECL framework to cause ₹60,000 Cr. hole to Bank Profits

Dayita Kanodia and Chirag Agarwal | finserv@vinodkothari.com

The proposed ECL framework marks a major regulatory shift for India’s banking sector; it is long overdue, and therefore, there is no case that the RBI should have deferred it further. However, it comes coupled with regulatory floors for provisions, which would cause a major increase in provisioning requirements over the present requirements. Our assessment, on a very conservative basis, is that the first hit to Bank P/Ls will be at least Rs 60000 crores in the aggregate.

RBI came up with a draft framework on ECL pursuant to the Statement on Developmental and Regulatory Policies, wherein it indicated its intention to replace the extant framework based on incurred loss with an ECL approach. The highlights can be accessed here.

A major impact that the draft directions will have on the Banking sector is the need to maintain increased provisioning pursuant to a shift from an incurred loss framework to the ECL framework. Under the existing framework, banks make provisions only after a loss has been incurred, i.e., when loans actually turn non-performing. The proposed ECL model, however, requires banks to anticipate potential credit losses and set aside provisions for such anticipated losses.

Banks presently classify an asset as SMA1 when it hits 30 DPD, and SMA2 when it turns 60. Both these, however, are standard assets, which currently call for 0.4% provision. Under ECL norms, both these will be treated as Stage 2 assets, which calls for a lifetime probability of loss, with a regulatory floor of 5%. Thus, the differential provision here becomes 4.6%.

Once an asset turns NPA, the present regulatory requirement is a 15% provision; the ECL framework puts these assets under Stage 3, where the regulatory minimum provision, depending on the collateral and ageing, may range from 25% to 100%. Our Table below gives more granular comparison.

| Type of asset | Asset classification | Existing requirement | Proposed requirement | Difference |

| Farm Credit, Loan to Small and Micro Enterprises | SMA 0 | 0.25% | 0.25% | – |

| SMA 1 | 0.25% | 5% | 4.75% | |

| SMA 2 | 0.25% | 5% | 4.75% | |

| NPA | 15% | 25%-100% based on Vintage | 10%-85% based on Vintage | |

| Commercial real estate loans | SMA 0 | 1% | Construction Phase -1.25% Operational Phase – 1% | Construction Phase -0.25% Operational Phase – Nil |

| SMA 1 | 1% | Construction Phase -1.8125% Operational Phase – 1.5625% | Construction Phase -0.8125% Operational Phase – 0.5625% | |

| SMA 2 | 1% | Construction Phase -1.8125% Operational Phase – 1.5625% | Construction Phase -0.8125% Operational Phase – 0.5625% | |

| NPA | 15% | 25%-100% based on Vintage | 10%-85% based on Vintage | |

| Secured retail loans, Corporate Loan, Loan to Medium Enterprises | SMA 0 | 0.4% | 0.4% | – |

| SMA 1 | 0.4% | 5% | 4.6% | |

| SMA 2 | 0.4% | 5% | 4.6% | |

| NPA | 15% | 25%-100% based on Vintage | 10%-85% based on Vintage | |

| Home Loans | SMA 0 | 0.25% | 0.40% | 0.15% |

| SMA 1 | 0.25% | 1.5% | 1.25% | |

| SMA 2 | 0.25% | 1.5% | 1.25% | |

| NPA | 15% | 10%-100% based on Vintage | (-)5% – 85% based on Vintage | |

| LAP | SMA 0 | 0.4% | 0.4% | – |

| SMA 1 | 0.4% | 1.5% | 1.1% | |

| SMA 2 | 0.4% | 1.5% | 1.1% | |

| NPA | 15% | 10%-100% based on Vintage | (-)5% – 85% based on Vintage | |

| Unsecured Retail loan | SMA 0 | 0.4% | 1% | 0.6% |

| SMA 1 | 0.4% | 5% | 4.6% | |

| SMA 2 | 0.4% | 5% | 4.6% | |

| NPA | 25% | 25%-100% based on Vintage | 0%-75% based on Vintage |

The actual impact of such additional provisioning will be a hit of more than 3% to the profit of banks1. Based on the RBI Financial Stability Report of FY 24-252, the current level of SMA and NPA is estimated to be ₹3,78,000 crores (2%) and ₹4,28,000 crores (2.3%), respectively.

Accordingly, an additional provision of approximately₹ 18,000 crores (4.6% of SMA volume) and ₹ 42,000 crores (10% of NPA volume) will be required for SMA and NPA respectively, leading to a total impact of at least ₹60,000 crores. This estimate has been arrived at by considering the % of NPAs and SMA-1 & SMA-2 portfolios of banks. The actual impact may be higher, as lot of loans may be unsecured, and may have ageing exceeding 1 year, in which case the differential provision may be higher.

It may be noted that while the draft directions allow Banks to add back the excess ECL provisioning to the CET 1 capital, it does not neutralize the immediate profitability impact, as the additional provisions would still flow through the profit and loss account.

How do we expect banks to smoothen this hit that may affect the FY 27-28 P/L statements? We hold the view that it will be prudent for banks, who have system capabilities, to estimate their ECL differential, and create an additional provision in FY 25-26, or do technical write-offs.

Other Resources

- Expected credit losses on loans: Guide for NBFCs

- Impact of restructuring on ECL computation

- Tattva Session 3 – RBI Provisions and Expected Credit Loss (ECL): Understanding their Interplay

- The total Net profit of SCBs is ₹ 23.50 Lakh Crore for FY 24. (https://ddnews.gov.in/en/indian-scbs-post-record-net-profit-of-%E2%82%B923-50-lakh-crore-in-fy24-reduce-npas/ )

↩︎ - Based on our rough estimate of the data available here: https://www.rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=1300 ↩︎

ECL Framework for Banks: Key Highlights

Legal issues in factoring business in India

Originally by Nidhi Bothra (2011) | Updated by Simrat Singh | finserv@vinodkothari.com

Credit Factoring or simply factoring is an asset backed means of financing (tripartite agreement between the buyer, seller and the factor), whereby the account receivables are assigned to a third party called factor for a discount, releasing the tied-up capital and providing financial accommodation to the Company. The origin of factoring goes back to the 14th century in England. Earlier, factoring was confined to textile and garment industries, but later was spread across various industries and markets. Factoring has been defined as:

“Credit factoring may be defined as a continuing legal relationship between a financial institution (the “factor”) and a business concern (the “client”) selling goods or providing services to trade customers (the “customers”) whereby the factor purchases the client’s book debts either without or with recourse to the client, and in relation thereto controls the credit extended to customers and administers the sales ledger.”

UNIDROIT Convention on International Factoring, 1988 defines factoring as follows:

“Factoring contract” means a contract concluded between one party (the supplier) and another party (the factor) pursuant to which:

- the supplier may or will assign to the factor receivables arising from contracts of sale of goods made between the supplier and its customers (debtors) other than those for the sale of goods bought primarily for their personal, family or household use;

- the factor is to perform at least two of the following functions:

- finance for the supplier, including loans and advance payments;

- maintenance of accounts (ledgering) relating to the receivables;

- collection of receivables;

- protection against default in payment by debtors;

- notice of the assignment of the receivables is to be given to debtors.

US accounting standard ASC 860-10-05-14 defines ‘factoring arrangements’ as:

Factoring arrangements are a means of discounting accounts receivable on a nonrecourse, notification basis. Accounts receivable in their entirety are sold outright, usually to a transferee (the factor) that assumes the full risk of collection, without recourse to the transferor in the event of a loss. Debtors are directed to send payments to the transferee

Though Europe provides largest volumes globally, factoring in Asia as well has been growing rapidly in the last few years. Global factoring volumes reached EURO 3.66 Trillion in 2024 (up 3.6% from the previous year)1. In Asia-Pacific, India was the fastest-growing market in the region, up 120% to EUR 38.2 billion.2

The purport of factoring is to assign the account receivables to be able to:

- Instantly convert receivables into case, that enable the companies to have funds to finance the day to day operations of the company;

- Helps in efficient collection of the receivables and protection against bad debts;

- Outsourcing sales ledger administration and

- Availing credit protection for receivables.

Typically in a factoring transaction, a seller gets a prepayment limit from the factor, then enters into a transaction with the buyer and submits the invoice; notice to pay etc to the factor. The factor makes upfront payment to the seller, as a percentage of invoice value based on criteria, such as, quality of receivables, number and quality of the buyers and seller’s requirements (80% – 95% of invoice value) and maintains the sales ledger of the seller and collects payment from buyer. The balance payment is made to the seller, net of charges. The seller is not required to open an LC or a bank guarantee.

The cost to the seller in factoring is the service fees, which is dependent on a) sales volume, b) number of customers, c) number of invoices and credit notes and d) degree of credit risk in the customer or the transaction.

Factoring and Bill Discounting

There is a very thin line of difference between factoring and bill discounting. Bill discounting unlike factoring is always with recourse to the client, whereas factoring may be with recourse or without. Generally there is no notice of assignment given to the customer in case of bill discounting and collections are done by the assignor , unlike factoring, where debt collection is done by the factor. Factoring can be called a financing and servicing function, whereas, bill discounting function is purely financial.

Types of Factoring

On the basis of geographical distribution

- Domestic Factoring

- Sales bill factoring

- Purchase bill factoring

- International Factoring – As international trade continues to increase, international factoring is being accepted as vital to the financial needs of the exporters and is getting the necessary support from the government, specifically in the developing countries to stimulate this mode of funding.

- Export factoring – It is seen as an alternative to letter of credit, as the importers insist on trading in open account terms. Export factoring eases the credit and collection troubles in case of international sales and accelerates cashflows and provides liquidity in the business.

On the basis of credit risk protection

- On recourse basis, wherein the factor can recover the amount from the seller, in case of non-payment of the amount to the factor. Thus, though the receivables have been assigned, the credit risk remains with the client.

- On non-recourse basis also called old line factoring, wherein the risk of non-payment of invoices is borne by the factor. However, the factor only bears credit risk in such transactions. In case non-payment is due to any other reason other than financial incapacity, such as disputes over quality of goods, breach of contract, set-offs or fraud , the factor does not assume liability and the risk remains with the client.

Other types:

- Advance factoring: In case of advance factoring, the factor provides financial accommodation and non-financial services. The factor keeps a margin while funding, which is called the client’s equity and is payable on actual collection.

- Maturity factoring: Here, the factor makes payment on a due date. This sort of funding is resorted to by clients who are in need of non-financial services offered by the factors.

- Supplier guarantee factoring: Also known as drop shipment factoring. This sort of factoring is common where the client acts as a mediator between the supplier and the customer.

Overview of factoring in India:

India’s factoring turnover in 2024 was around Euros 38,200 Million in total as compared to a total of Euros 3,894,631 million worldwide3 and the turnover over the last 7 years (2018-2024) has seen a tremendous growth; while that of Asia has risen 38% from 2018 to 2024 and is valued at Euros 3,894,631Million.

Fig 1: Factoring volumes in India: Source: FCI Annual Review 2025

Some of the challenges faced by the factoring companies in India are a) there was no specific law for assignment of debt, b) there was no recovery forum available to the factoring NBFCs such as DRT or under Sarfaesi Act, c) Lack of access to information on credit worthiness and d) assignment of debt involves heavy stamp duty cost.

UNCITRAL laws on assignment

Article 2 of the United Nations Convention on the Assignment of Receivables in International Trade defines ‘Assignment’ as –

“Assignment” means the transfer by agreement from one person (“assignor”) to another person (“assignee”) of all or part of or an undivided interest in the assignor’s contractual right to payment of a monetary sum (“receivable”) from a third person (“the debtor”). The creation of rights in receivables as security for indebtedness or other obligation is deemed to be a transfer;

The Factoring Regulation Act, 2011

In order to revive the business and render liquidity specifically to the small and medium enterprises, the Finance Minister, in the Parliament session held in March, 2011 had tabled a pilot bill to bring the factoring business in India under regulation. The Bill was passed as the Factoring Regulation Act, 2011

While the intent of the Act may be to stimulate the growth of factoring business in India, but a close look at the Act does not enumerate so. The Act is a regulation Act, but the need was for an Act to promote factoring and not so much to regulate. Some of the highlights of the Act are as mentioned below:

- The name makes it unclear whether the Act is for regulating assignment; factoring or both. Further it should have been a regulation of factor’s’ and nor factor, to be more appropriate.

- Section 2 (a) of the Act defines means transfer by agreement to a factor of an undivided interest, in whole or in part, in the receivables of an assignor due from a debtor…The definition talks about undivided interest to be assigned only and does not consider assignment of fractional interest within its ambit. This would mean that any assignment of fractional interest would not be covered under this definition. Further whether the assignment could be in terms of money, in terms of time or rate of interest is not clear from the definition.

- The definition of receivables, in Section 2(p) of the Act includes futures receivables as well, which is in line with international laws.

- Section 3(1) of the Act says –

No Factor shall commence or carry on the factoring business unless it obtains a certificate of registration from the Reserve Bank to commence or carry on the factoring business under this Act.

The definition should have said no ‘person’ shall commence or carry on the factoring business rather than using the term factor. A person shall only become a factor after obtaining a certificate of registration from the Reserve Bank as the section suggests. However the section already terms such a person as a ‘factor’, making the definition circular.

- Section 3(3) of the Act states every company carrying or commencing factoring business to be registered with RBI, and such companies would be classified as NBFCs and all the provisions applicable to NBFCs would be applicable here as well. Section 3(4) requires existing NBFCs to take a fresh certificate of registration, if they are principally engaged in the business of factoring. But the Act does not render clarity whether there would be a separate class of NBFCs carrying out factoring business.

- Section 7(3) states that in case the receivables are encumbered to any creditor, the assignee shall pay the consideration for such assignment to the creditor to whom the receivables have been encumbered. In case of fixed charge created over assets, the provisions of this section are well thought, however in case of floating charges, this would render several difficulties for the assignor. Most companies have fixed and floating charges created over their assets, the assets on which floating charge is created are regularly rotated in business and are only crystallized in case of default or non-payment. If the company was to assign such assets it would be practically impossible for the assignee to identify which receivables are currently subject to the floating charge, and to whom the consideration ought to be paid. This uncertainty could discourage assignments, create disputes between secured creditors and assignees, and undermine the commercial utility of receivables financing.

- Section 8 of the Act requires the notice of assignment to be given to the debtor, without which the assignee shall not be entitled to demand payment of the receivables from the debtor. However Section 7(2) of the Act, makes Section 8 redundant, as it states that on execution of agreement in writing for assignment of receivables, the assignee shall have ‘absolute right to recover such receivable and exercise all the rights and remedies of the assignor whether by way of damages or otherwise, or whether notice of assignment as provided in sub-section (1) of section 8 is given or not.’ This is not in line with the proviso to Section 130 (1) of the Transfer of Property Act, 1882 which mandates that the assignee will be able to recover or enforce the debt when the debtor is made party to the transfer or has received express notice of such an assignment.

- Section 8, 9 and 10 provide for the requirements of notice of assignment. The intent of Section 11 seems that even in case notice of assignment is not provided the debtor would not be absolved from his duties to make payment. However the section is worded as ‘till notice is served on the debtor, the rights and obligations in its contract with the assignor, shall remain unchanged, excepting the change of the party to whom the receivables are assigned which may become entitled to receive the payment of the receivable from the debtor;’ this means whether or not notice for assignment is provided the rights and obligations of the debtor towards the assignee would remain unaffected. If so was the intent of the Section, then there was no need for any notice of assignment to be given to the debtor, as by the virtue of this section read with section 7(2), the assignee would have all the right on receivables as that of the assignor.

- The UNCITRAL model law on assignment requires that notification of assignment of debt is to be given by either the assignor or the assignee, the assignee may not retain more than the value of its right in the receivable and notification of the assignment or a payment instruction is effective when received by the debtor. However, until the debtor receives notification of the assignment, the debtor is entitled to be discharged by paying in accordance with the original contract.

- Import factoring is not permitted as per Section 31(1) of the Act.

- Further recourse to the assignor is not permitted under the Act.

- The proposed law provides for compulsory registration of every transaction of assignment of receivable with the Central Registry to be set up under the Sarfaesi Act within a period of 30 days.

Factoring or financing transaction?

In Major’s Furniture Mart, Inc v. Castle Credit Corporation4, the question in consideration in the case was whether the transaction was a true sale or mere financing. Major’s was into retail sale of furniture and Castle into the business of financing such dealers as Major’s. Under an agreement, Major’s had sold its receivables to Castle, with full recourse against Major’s. The Court held the assignment of receivables by the furniture seller to the factoring company a case of financing and not assignment, as the factor had full recourse on the seller and the factor only paid a part of the total debt factored by him.

In another case of Endico Potatoes Inc. and others vs. CIT Group/Factoring Inc.5, in case of a factoring transaction, the court opined:

“Resolution of whether the “contemporaneous transfer,” as CIT describes Merberg’s assignment of accounts receivable to CIT and CIT’s loan advances to Merberg, constitutes a purchase for value or whether the exchange provides CIT with no more than a security interest, depends on the substance of the relationship between CIT and Merberg, and not simply the label attached to the transaction. In determining the substance of the transaction, the Court may look to a number of factors, including the right of the creditor to recover from the debtor any deficiency if the assets assigned are not sufficient to satisfy the debt, the effect on the creditor’s right to the assets assigned if the debtor were to pay the debt from independent funds, whether the debtor has a right to any funds recovered from the sale of assets above that necessary to satisfy the debt, and whether the assignment itself reduces the debt.

Major’s Furniture Mart, Inc. v. Castle Credit Corp.6, Levin v. City Trust Co.7, Hassett v. Sprague Electric Co.8, In re Evergreen Valley Resort, Inc.9. The root of all of these factors is the transfer of risk. Where the lender has purchased the accounts receivable, the borrower’s debt is extinguished and the lender’s risk with regard to the performance of the accounts is direct, that is, the lender and not the borrower bears the risk of non-performance by the account debtor. If the lender holds only a security interest, however, the lender’s risk is derivative or secondary, that is, the borrower remains liable for the debt and bears the risk of non-payment by the account debtor, while the lender only bears the risk that the account debtor’s non-payment will leave the borrower unable to satisfy the loan.

In CF Motor Freight v. Schwartz10, the court recharacterized what was labeled a factoring arrangement as a secured loan. The agreement expressly stated it was a “Factoring Agreement,” and each receivable was stamped as “sold and assigned.” The court even acknowledged that factoring typically involves the purchase of accounts receivable. Under the arrangement, the transferee advanced 86% of the invoice value upfront, with an additional 10% payable if and when collections were made. However, if a receivable was not collected within 60 days, the transferee could demand repayment from the transferor. Because of this recourse provision, the court concluded that the transferee had not truly assumed the risks associated with ownership and therefore treated the arrangement as a secured loan.

In Home Bond Co. v. McChesney11, the US Supreme Court held that certain contracts labeled as “purchases” of receivables were in fact loans secured by receivables, because the transferor retained the risk of non-payment (through repurchase obligations and collection duties), and the transferee’s “service charges” were essentially disguised interest. The ratio being that a transaction is a loan, not a sale, when the transferor bears the risks and costs of collection, even if the contract is formally styled as a sale. In Taylor v. Daynes12, the Utah Supreme Court stated that whether a sale has occurred depends not on labels or form but on whether the risks and benefits of ownership have been transferred to the transferee.

Another aspect considered by courts to determine whether it is a case of sale of receivables is alienability i.e. ability to transfer/resell for a profit. When an account is transferred, if the transferee has a right to alienate the acquired account, it is a case of sale and not financing. In Nickey Gregory Co. v. AgriCap, LLC, the court treated the transaction as a secured loan, partly because the transferee’s rights were closer to a lender’s, it did not have full indicia of ownership, including unrestricted alienability.

In a more recent case of Re: Qualia Clinical Service, Inc v. Inova Capital Funding, LLC; Inova Capital Funding, Inc, the bankruptcy court found that the invoice purchase agreement was clearly and unambiguously a financing arrangement. The court made that finding on the terms of the agreement itself. In particular, the court noted that the recourse provisions contained in section 7.02 of the agreement, which shift all collection risks to Qualia.

“….. “The question for the court then is whether the Nature of the recourse, and the true nature of the transaction, are such that the legal rights and economic consequences of the agreement bear a greater similarity to a financing transaction or to a sale.”

This agreement, which shifts all risk to Qualia, is a disguised loan rather than a true sale. Where the “seller” retains “virtually all of the risk of noncollection,” the transaction cannot properly be considered a true sale.

If the assignment alone did not reduce the obligation of the assignor towards the assignee and the assignee at any given point of time, directly demand the money from the assignor, there is no transfer of risk. If the primary risk of customer’s non-payment remained with the assignor, then it cannot qualify as a true sale.

Credit insurance and factoring:

Insurers are allowed to offer Trade Credit Insurance which provides protection to suppliers against the risk of non-payment for goods and services by buyers. Typically, it covers a portfolio of buyers and indemnifies the insured for an agreed percentage of the invoice value that remains unpaid. As per IRDAI (Trade Credit Insurance) Guidelines, 2021 (‘Guidelines’), the scope of cover may include commercial risks such as insolvency or protracted default of the buyer, as well as rejection of goods (either after delivery or before shipment, in cases where the goods were exclusively manufactured for the buyer). It may also extend to political risks, such as changes in law, war, or related disruptions; however, this protection is applicable only for buyers located outside India and in countries agreed upon under the policy.

The risks covered under the Guidelines are not exhaustive, and insurers may extend coverage to additional risks, provided these have a direct nexus with the delivery of goods or services. As per the Guidelines, Trade credit insurance policy may be issued to the following:

- Seller / Supplier of goods or services;

- Factoring company;

- Bank / Financial Institution, engaged in Trade Finance

As per the Guidelines, insurers are permitted to extend coverage for transactions involving factoring, reverse factoring on the TreDS platform (as clarified under the IRDAI circular dated 9 October 2023), and bill discounting. Lastly, insurance is available only in case of non-recourse factoring.

- FCI Annual Review 2025 ↩︎

- FCI Annual Review 2025 ↩︎

- Data from Factors Chain International http://www.factors-chain.com/?p=ich&uli=AMGATE_7101-2_1_TICH_L1403780046 ↩︎

- 602 F.2d 538; 1979 U.S. App. LEXIS 13808; 26 U.C.C. Rep ↩︎

- SECOND CIRCUIT Nos. 1751, 1961 Decided: October 2, 1995, ↩︎

- Supra ↩︎

- 482 F.2d 937, 940 (2d Cir. 1973) ↩︎

- 30 B.R. 642, 647-48 (Bankr. S.D.N.Y. 1983) ↩︎

- 23 B.R. 659, 660-61 (Bankr. D. Me. 1982) ↩︎

- 215 B.R. 947, 951 (Bankr. E.D. Pa. 1997) ↩︎

- 239 U.S. 568 (1916) ↩︎

- 118 Utah 61 (Utah 1950) ↩︎

See our other resources on Factoring:

- Transfer of Factoring receivables exempted from MHP

- PPT on Basics of Factoring

- India Factoring Report 2023

- Basics of Factoring in India

- Money advanced by factor in factoring – a loan or not?

- India Factoring Report 2013

- Export Factoring

- Fractured Factoring: Amendments may give a push to a potent trade finance solution

Budget, Bazaars and Bank Rate: Understanding inflation, GDP, Repo Rate etc.

Access the Youtube video at https://www.youtube.com/watch?v=EXH6Nt1fXdg

See our other resources on this topic:

Overview of RBI (Project Finance) Directions, 2025

Link to the YouTube video – https://www.youtube.com/watch?v=uCbe66Amk9w

Our article on the RBI (Project Finance) Directions, 2025

Balancing flexibility and discipline: Analysis of RBI’s Project Finance Directions, 2025

Aanchal Kaur Nagpal, Senior Manager and Simrat Singh, Senior Executive | finserv@vinodkothari.con

Updated as on 28th October, 2025

Project loans, used to finance large infrastructure and industrial ventures like highways, power plants and railways etc., are fundamentally different from regular business or personal loans. Unlike typical loans that are repaid from either the borrower’s existing operations and balance sheet (in case of the former) or the borrower’s own credit worthiness (in case of the latter), project loans are forward-looking: they primarily rely on cash flows of the project, generated only after the project becomes operational. Because of this, delays in project completion due to various factors such as land acquisition issues and regulatory delays which may be beyond the control of the developer are common. These may arise from. Such delays, though being routine and not necessarily indicating borrower’s stress, triggered adverse asset classifications under the existing rules.

When the RBI introduced its 2019 prudential framework to enable early recognition and time bound resolution of stressed assets, it excluded such project loans from its scope (see para 25). As a result, these continued to be governed by old norms, specifically para 4.2.5 of the 2015 IRCAP and later, para 3 of Annex III under the RBI SBR Directions. However, these norms did not reflect the unique risks faced by project finance especially during the construction phase.

To address these issues, the RBI released the Draft Project Finance Directions in May 2024, proposing a dedicated regulatory framework tailored to project loans. The Project Finance Directions (‘Directions’) have been issued on 19 June, 2025. This article explores the need for such a framework, the changes brought in the regulatory regime, and their impact on borrowers and lenders.

Project finance vs other kinds of finance

In corporate lending, credit decisions are primarily based on the borrower’s balance sheet strength, existing cash flows and overall financial health. where the lender primarily assumes credit risk

In contrast, in project finance, repayments as well as the primary security depend primarily on the successful implementation and projected cash flows of a specific project, rather than the borrower’s overall financial position. Accordingly, the lender takes two different risks:

- Project risk i.e. the risk that the project may face commencement delays due to factors like regulatory bottlenecks, land acquisition issues or construction delays and;

- Credit risk i.e. the risk of inadequacy of cashflows to make the scheduled contractual payouts.

Importantly, in project finance, delays in cashflows often happen due to non-credit factors linked to project execution, mainly project delays. As a result, automatic downgrading of classification due to any project delay may not only fail to provide a true risk profile of the loan but also cause increased provisioning burden on the lender.

Overview of the Directions

The Directions deal with the following broad aspects:

- Classification of projects and project finance;

- Prudential requirements for extending project loans including:

- Provisioning requirements;

- Conditions for sanction, disbursement and monitoring.

- Resolution and restructuring of project loans

- Either due to stress;

- Extension/ delays in DCCO.

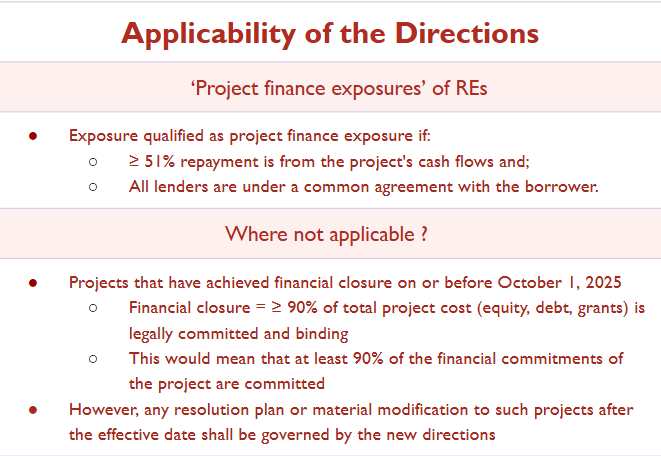

Applicability

Classification of ‘project’ and ‘project finance’

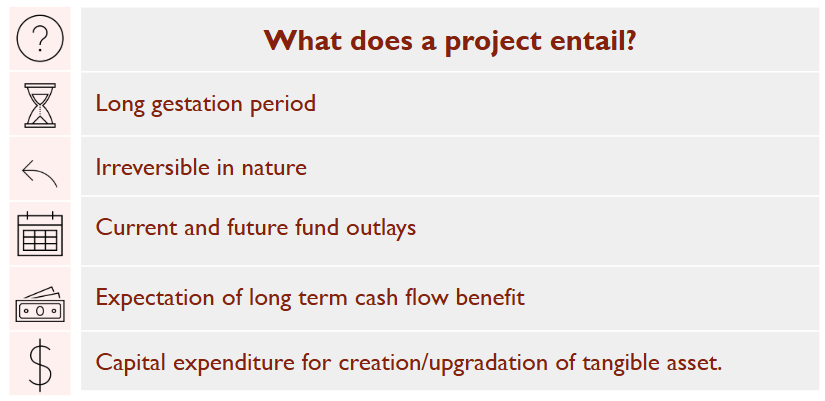

Under the Directions, a project is defined as to involve capital expenditure for the creation, expansion or upgradation of tangible assets or facilities, with the expectation of long-term cash flow benefits [see para 9(l)], with the following features:

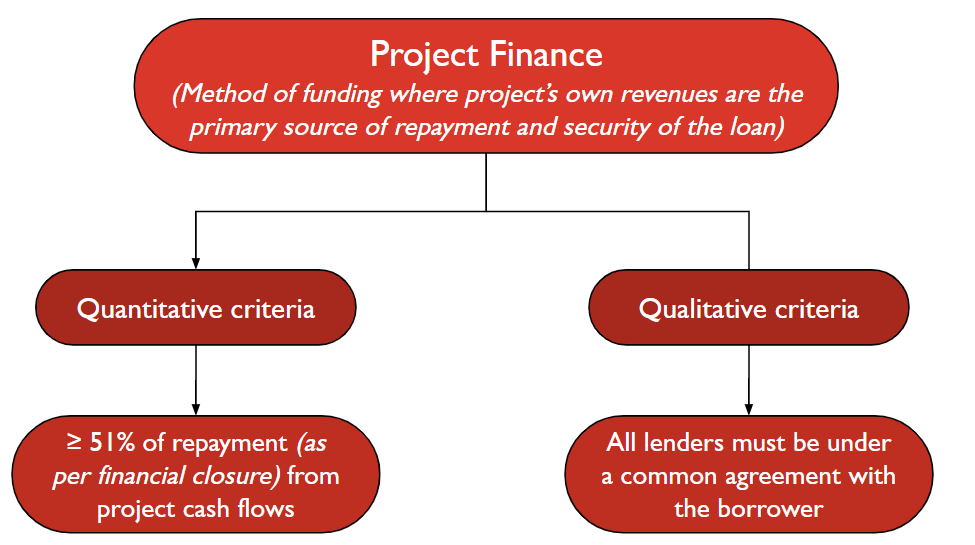

Project finance is a method of funding where the project’s cash flows/ revenue own revenues are the primary source of repayment as well as the and security for the loan [see para 9(m)].

- It can be:

- Greenfield (new project);

- Brownfield (existing project enhancement).

To qualify as project finance under the Directions:

Note: Loan terms can differ across lenders if agreed by all parties

The earlier definition of project finance under the SBR Directions was generic and vague, referring merely to a “project loan” as any term loan extended for setting up an economic venture. The Directions have provided more clarity on what would be considered as project finance and have linked it to the definition of project finance under the Basel Framework, while also providing a quantitative threshold of 51%.

Project finance envisages the lender’s exposure in a project, which is typically in the process of being set up. The repayment will be from the project cashflow i.e. the payout structure is connected with the commencement of commercial operations of the project. The lending is based on the projected cash flows of the project rather than the balance sheet of the developer. It is distinct from asset finance, where loans are backed by existing assets generating income. Further, project finance differs from a working capital loan/general corporate purpose loan where the latter is towards financing the working capital needs of the developer entity based on the overall health of the entity.

Would it mean that project loans cannot have any other collateral and must solely rely on the project as the security? The answer is negative since the threshold specified allows to have other/ additional collateral, say, personal guarantee of the developer etc., however, the primary security shall be the project cashflows.

Other important terminology

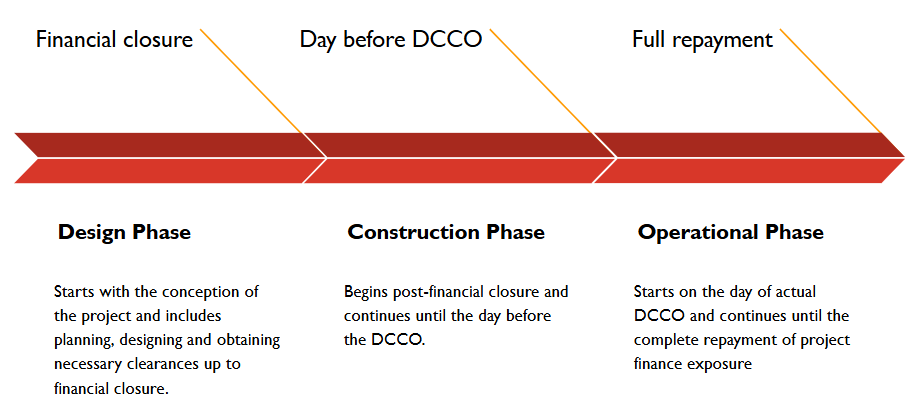

DCCO

The Date of Commencement of Commercial Operations (DCCO) is a key milestone in project finance, marking the transition from construction to operational phase when a project begins to generate revenue.The Directions recognises three forms of DCCO. [see Para 9(e) to (m)]

CRE and its sub-category CRE-RH

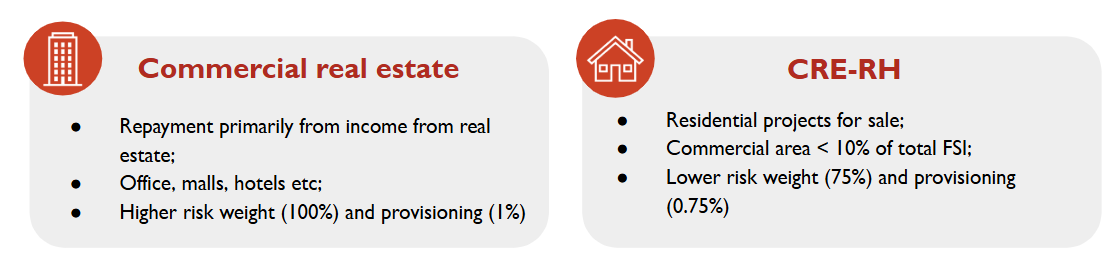

Defined in Directions on Classification of Exposures as Commercial Real Estate Exposures, CRE refers to loans or exposures where repayment primarily depends on income generated by the real estate asset itself. This typically includes office spaces, malls, warehouses, hotels and multi-family housing complexes that are leased or sold in the open market. Since CRE is a sub-head of project finance, it also follows similar characteritics of project finance i.e.both repayment of the loan and recovery in case of default are closely tied to the cash flows from the real estate asset such as rental income or sale proceeds. [see para 9(b)]. The definition is aligned with the definiton of income-producing real estate (IPRE) under Basel norms. Our article discussing CRE can be assessed here. https://vinodkothari.com/2023/04/commercial-real-estate-lending-risks-and-regulatory-focus/

Commercial Real Estate – Residential Housing (CRE-RH) [see para 9(c)]

Since residential housing projects generally pose lesser risk and volatility compared to commercial properties, the RBI created a distinct sub-category within CRE called CRE-RH vide notification dated June 21, 2013. CRE-RH includes loans given to builders or developers for residential housing projects meant for sale.To classify as CRE-RH, the project must be predominantly residential and commercial components like shops or schools should not exceed 10% of the total built-up area (FSI). If the commercial area crosses this 10% threshold, the entire project will be CRE. This distinction isn’t just semantic, it has regulatory benefits. Since CRE-RH are subject to lower risk due to various reasons such as diversified cash flows and lower dependency on a single occpnt, RBI has assigned lower capital risk weights i.e. 75% to CRE-RH compared to standard CRE 100% and lower provisioning provisioning requirements (0.75% vs. 1%).

Prudential requirements

Provisioning requirements

In the context of project finance, where risks vary across different phases of a project’s lifecycle, a one-size-fits-all provisioning approach throughout the project life may not be relevant. .

Under the SBR, provisioning norms made no distinction between the construction and operational phases of a project. A uniform provisioning rate was applied i.e. 0.75% for CRE-RH and 1% for CRE while other loans were provisioned at 0.4% irrespective of whether the project was just starting construction or had already begun generating revenue. This approach, while simple, failed to reflect the heightened risks associated during the construction phase , such as delays, cost overruns, or regulatory hurdles.

To address this gap, the Draft Directions, proposed a conservative approach calling for a 5% provision during the construction phase and 2.5% during the operational phase, with the operational rate reducible to 1% if following conditions were met:

- the project demonstrated positive net operating cash flows sufficient to service all current repayment obligations, and

- there was a minimum 20% reduction in long-term debt from the level outstanding at the time of achieving DCCO.

These draft norms were considered overly harsh, particularly for long-gestation infrastructure projects where cash flows stabilise gradually.

Taking stakeholder feedback into account, the Directions adopted a more balanced g structure as follows:

| Project type | Construction Phase | Operational phase – after commencement of repayment interest and principle |

| Commercial real estate (CRE) | 1.25% | 1% |

| CRE – Residential Housing | 1% | 0.75% |

| Other projects | 1% | 0.40% |

| DCCO deferred projects: | Additional provisioning to be maintained depending on the type of project:0.375% per quarter for infra projects0.5625% per quarter for non-infra projects | |

| NPA project finance accounts | As per extant instructions | |

| Provisionig for existing projects | Continued to be governed by extant norms;If resolution is done for any fresh credit event or change in terms occur after the effective date of these directions, then provisioning as per these Directions | |

RBI’s draft proposal for lower risk-weights for high quality infrastructure projects

The RBI has issued a draft amendment to the Scale Based Regulations, 2023 on 27th October, 2025, proposing a lower risk weight framework for ‘High-Quality Infrastructure Projects’. Once finalised, the provisions would be applicable from April 1, 2026, or from an earlier date when adopted by an NBFC in entirety. The intent of the amendment is to recognise and incentivise lending to stable, well-performing infrastructure projects by prescribing reduced risk weights for such exposures. Under the draft, “High-Quality Infrastructure Projects” are defined as infrastructure projects meeting all of the following conditions:

- The project has completed at least one year of satisfactory operations post achievement of the actual DCCO;

- The exposure is classified as ‘standard’ in the books of the lender;

- The obligor’s revenue depend on one main primary counterparty, which shall be the Central Government or a Public Sector Entity, and the contractual terms ensure certainty of payment, such as through availability-based1 or take-or-pay arrangements2;

- The contractual provisions offer strong creditor protection such as escrow of cash flows, legal first charge on project assets and other appropriate safeguards in case of early termination;

- The obligor has adequate internal or external funding arrangements to meet current and future working capital or other funding needs, as assessed by the lender;

- The obligor is restricted from undertaking actions detrimental to creditors, such as raising additional debt secured by the project’s cash flows or assets without lender’s consent.

Projects meeting all of the above criteria will qualify as high-quality infrastructure assets and will attract lower risk weights, as follows:

- 50%, where the obligor has repaid at least 10% of the sanctioned amount;

- 75%, where the obligor has repaid at least 5% but less than 10% of the sanctioned amount.

If a project subsequently fails to meet any of the qualifying conditions, it will cease to be treated as a high-quality asset and will instead attract the standard risk weight of 100% applicable to regular infrastructure exposures.

Conditions of project finance

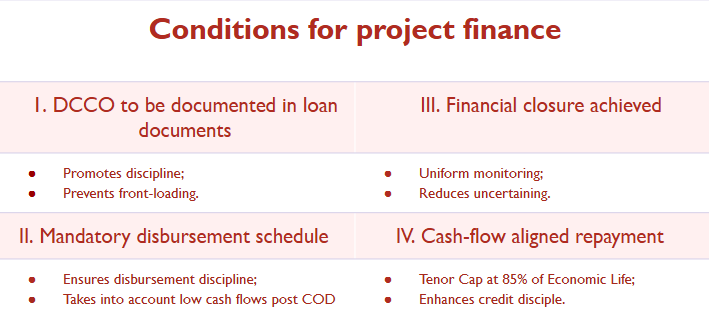

The onus is on the lender to ensure that the following conditions are met before extending any project finance. These conditions will ensure that the facility is structured prudently and is aligned with the implementation as well as cash flows of the project, thereby mitigating both credit as well as project risk. The requirements are more or less similar to the earlier Directions.

Repayment schedule during operational phase is designed to factor initial cash flows

- Repayment tenor, including the moratorium period, if any, shall not exceed 85% of the economic life of a project.

- This means there is a mandatory 15% tail period i.e. if the project has an economic life of 20 years and the loans are to be repaid in 17 years, the last 3 years are the tail period.Tail period gives comfort to the lender that in case of any default or delay in repayment by the time of maturity, there is still some period left to recover dues from the project cash flows after the scheduled loan maturity.

- Would this mean that a borrower cannot obtain a top-up loan after the expiry of 85% of the loan tenure?

- The requirement applies to loans with all kinds of tenures, either short or long.

One borrower, multiple lenders

- If a project is financed by more than one lender, RBI mandates that the DCCO, whether original, extended or actual, shall be the same across all lenders. This will ensure that:

- DCCO is uniform across all lenders

- Project progress as well as any delays are uniform across all lenders

- Uniform asset classification, preventing any lender from having a different provisioning status.

- To ensure balanced risk sharing, the Directions have put consortium lending limits (Para 15): Where projects are under-construction:

- Aggregate exposure of all lenders is ≤ ₹1,500 crore: each lender shall hold at least 10% of total exposure;

- For projects with exposure > ₹1,500 crore: each lender must hold at least 5% or ₹150 crore, whichever is higher.

These caps essentially require participating lenders to hold sufficient skin in the game and thereby promote responsible credit appraisal as well as avoid risk from being concentrated in a few lenders, especially where other lenders have negligible exposure and hence, less incentive to ensure monitoring.

- Inter-lender transfer

- These minimum exposure norms will not apply to operational phase projects;

- In design or construction phase, lenders are permitted buy/sell exposure only under syndication arrangements as per TLE, and within the exposure limits

- In operational phase, exposures can be freely transferred as per TLE norms.

This may be because construction and pre-operational stages are inherently more uncertain and riskier, and therefore, the regulator requires lenders who are willing to remain committed and not exit easily to avoid creating instability.

Project lifecycle – 3 different phases

A project has been divided into 3 phased viz Design, Construction and Operational.

Why does this classification matter?

The regulatory framework treats each phase differently for various risk, compliance and prudential reasons.

- Disbursement discipline (Para 21)

- Disbursal of funds must be linked to project completion milestones i.e. completion of phases.

- Lenders must also track progress in equity infusion and other financing sources as agreed at financial closure

- Asset classification (Para 22 & 29)

- In design and construction phases, loans can be classified as NPA based on recovery performance, as per IRACP norms.

- Once an account is classified as NPA, it can only be upgraded after demonstrating satisfactory performance during the operational phase

- Resolution trigger (Para 23)

- If any credit event (e.g., default) occurs with any lender during the construction phase, a collective resolution process is triggered

- Provisioning norms (Para 32)

- Provisioning rates are higher for projects under construction

- Once the project enters the operational phase, provisioning reduces, reflecting lower credit risk.

Mandatory requirements before sanctioning a project finance loan: (13)

- Achievement of financial closure and documentation of original DCCO;

- Project specific disbursement schedule vis a vis stage of completion is included in loan agreement

- Post DCCO repayment schedule designed to factor initial cash flows

Prudential conditions related to disbursement and monitoring:

Lender to ensure the following:

- Clearances are obtained by the lender:

- All requisite approvals/clearances for implementing/constructing the project are obtained before financial closure.(examples: environmental clearance, legal clearance, regulatory clearances, etc.)

- Approvals/clearances contingent upon achievement of certain milestones would be deemed to be applicable when such milestones are achieved.

- Availability of sufficient (prescribed) minimum land/right of way with the lender before disbursal of funds

- This would mean that lender must ensure that the builder executing the project has either:

- Ownership of the land (through purchase, lease etc.) or

- This would mean that lender must ensure that the builder executing the project has either:

- Legal rights to use/access the land i.e. Right of Way.

- For PPP projects, disbursal of funds to occur only after declaration of the appointed date.

- Except where non-fund based facilities are mandated by the concessioning authority as a pre-requisite for declaration of the appointed date itself;

- Disbursal to be proportionate

- To stages of completion of project, infusion of equity or other sources of finance and receipt of clearances

- Lender’s Independent Engineer/Architect to certify the stages

- Creation and maintenance of a project finance database (see para 37):

- Every lender to capture and maintain, on an ongoing basis, project specific information relating to:

- Debtor and project profile;

- Change in DCCO;

- Credit events other than deferment of DCCO;

- Specifications of project

- Any updation shall be made within 15 days from any change in information;

- Necessary systems to be placed within 3 months from the effective date ie by 1st January, 2026

- Every lender to capture and maintain, on an ongoing basis, project specific information relating to:

Resolution of Project Loans

Prudential norms for resolution

- Lender to monitor performance of project on on-going basis;

- Expected to initiate a resolution plan well in advance.

- Collective resolution to be initiated by the lenders in case credit event happens with any one lender

- In case of any credit event;

- Lender to report the same:

- to the Central Repository of Information on Large Credit and;

- to all other lenders, in case of consortium lending.

- Lender to take a review of debtor account within 30 days.

- Inter creditor agreement and decision to implement a resolution plan may be done during this period.

- Implement the resolution plan within 180 days from the end of the review period.

- Lender to report the same:

Resolution plans involving extension of DCCO

Paragraphs 26 to 28 provide a structured framework under which project loans may continue to be classified as ‘standard’ despite delays in project completion, provided specific conditions are met. The objective is to offer flexibility to lenders and borrowers in addressing genuine project delays or cost escalations, without triggering an immediate downgrade to NPA so long as the resolution is timely and prudently implemented.

- Permitted DCCO deferment

- The DCCO may be deferred, with a corresponding adjustment in the repayment schedule. However, such deferment is subject to the following maximum limits:

- Up to 3 years for infrastructure projects

- Up to 2 years for non-infrastructure projects (including commercial real estate)

- The DCCO may be deferred, with a corresponding adjustment in the repayment schedule. However, such deferment is subject to the following maximum limits:

- Cost overrun associated with the DCCO deferment:

- A cap of 10% of the original project cost, over and above Interest During Construction (IDC)

- The overrun must be financed through a Standby Credit Facility sanctioned at the time of financial closure

- Post-funding, key financial metrics such as the Debt-Equity ratio and credit rating must remain unchanged or show improvement in favour of the lender

- Deferment in DCCO associated with change in scope and size

- Rise in project cost (excluding cost overrun) is at least 25% or more of the original project outlay

- Reassessment of project viability by the lender before approving the revised scope and DCCO

- If the project has an existing credit rating, the new rating must not deteriorate by more than one notch; if unrated and aggregate lender exposure is ₹100 crore or more, the revised project must obtain an investment-grade rating

- This benefit of maintaining ‘Standard’ classification due to a change in scope can be availed only once during the project’s life

- Resolution plan (‘RP’) deemed successfully implemented only if:

- Necessary documentation completed within 180 days from the end of the Review Period and;

- Revised capital structure and financing terms are duly reflected in the books of both the lender and the borrower.

- Immediate downgrading to NPA if the resolution plan is not implemented within the timeline and conditions above

- Once NPA, account can be upgraded only after:

- Satisfactory performance post actual DCCO, in case of non-compliance with conditions of resolution plan;

- Successful implementation of resolution plan, in case of non-implementation of RP within the specified time.

- Once NPA, account can be upgraded only after:

See a detailed PPT on the Project Finance Directions here

See our video on Project Finance Directions here

- A contractual model where the project earns fixed payments from the counterparty based on the asset’s availability and performance, irrespective of actual usage or demand ↩︎

- A contract under which the buyer agrees to pay for a specified quantity of output (e.g., power, gas, water) whether or not it actually takes delivery, ensuring predictable cash flows for the project. ↩︎

Full Day Workshop On Leasing and Asset Backed Finance

SEBI Securitisation Regulations: Track Record, Risk retention and Investment size among several new requirements

– Dayita Kanodia (finserv@vinodkothari.com)

Requirements to apply to all listed issuances, from financial and non-financial issuers

Below are the major highlights of the SDI amendment regulations:

SEBI on May 5, 2025 has issued the SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) (Amendment) Regulations. 2025. It may be noted that the SDI Regulations, was first notified on 26th May, 2008, after public consultation on the proposed regulatory structure with respect to public offer and listing of SDIs, following the amendments made in the SCRA. The Regulations, originally referred to as the SEBI (Public Offer and Listing of Securitised Debt Instruments) Regulations, 2008, were subsequently renamed as SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008, w.e.f. 26th June, 2018.

In order to ensure that the regulatory framework remains in accordance with the recent developments in the securitisation market, a working group chaired by Mr. Vinod Kothari was formed to suggest changes to the 2008 SDI regulations. Based on the suggestions of the working group and deliberations of SEBI with RBI, the amendment has been issued. The amendment primarily aims to align the SEBI norms for Securitised Debt Instruments (SDIs) with that of the RBI SSA Directions which only applies in case of securitisations undertaken by RBI regulated entities.

It can be said that these amendments are not in conflict with the SSA Directions and therefore for financial sector entities while there may be some additional compliance requirements if the securitisation notes are listed, there are as such no pain points which discourages such entities to go for listing. Further, certain requirements such as MRR, MHP, minimum ticket size have only been mandated for public issue of SDIs and therefore are not applicable in case of privately placed SDIs.

This article discusses the major amendments in the SDI Framework.

Major Changes

Definition of debt

The amendment makes the following changes to the definition of debt:

- All financial assets now covered – In order to align the SDI Regulations with the RBI SSA Directions, the definition of ‘debt’ has been amended to cover all financial assets as permitted to be originated by an RBI regulated originator. Further, this is subject to the such classes of assets and receivables as are permissible under the RBI Directions. Note that the RBI SSA Directions does not provide a definition of ‘debt’ or ‘receivables’, however, provides a negative list of assets that cannot be securitised under Para 6(d) of the RBI SSA Directions.

- Equipment leasing receivables, rental receivables now covered under the definition of debt.

- Listed debt securities – The explicit mention of ‘listed’ debt securities may remove the ambiguity with regard to whether SDIs can be issued backed by underlying unlisted debt securities, and limits the same to only listed debt securities. The second proviso to the definition further clarifies that unlisted debt securities are not permitted as an underlying for the SDIs.

- Trade receivables (arising from bills or invoices duly accepted by the obligors) – As regards securitisation of trade receivables, acceptance of bills or invoices is a pre-condition for eligibility of the same as a debt under the SDI Regulations.

‘Acceptance’, in literal terms, would mean acknowledgement of the existence of receivables. Under the Negotiable Instruments Act, 1881, ‘acceptance’ is not defined, however, ‘acceptor’ is defined to mean the drawee of a bill having signed his assent upon the bill, and delivered the same, or given notice of such signing to the holder or to some person on his behalf.

Note that a bill or invoice may either be a hard copy or in digital form. In the context of digital bill, acceptance through signature is not possible; therefore, existence of no disputes indicating a non-acceptance, should be considered as a valid acceptance.

- Such Debt/ receivable including sustainable SDIs as may be notified by SEBI – In addition to the forms of debts covered under the SDI Regulations, powers have been reserved with SEBI to specify other forms or nature of debt/ receivable as may be covered under the aforesaid definition. Further, the clause explicitly refers to sustainable SDIs, for which a consultation had been initiated by SEBI in August 2024[1].

Conditions governing securitisation

SEBI has mandated the following conditions to be met for securitisation under the SDI Framework:

- No single obligor to constitute more than 25% of the asset pool – This condition has been mandated with a view to ensure appropriate diversification of the asset pool so that risk is not concentrated with only a few obligors. However, it may be noted here that the RBI regulations does not currently prescribe any such obligor concentration condition. Only in case of Simple, Transparent and Comparable securitisation transactions, there is a mandate requiring a maximum concentration of 2% of the pool for each obligor.

However, SEBI has retained the power to relax this condition. In our view, this may be relaxed by SEBI for RBI regulated entities considering that RBI does not prescribe for any such condition.

- All assets to be homogenous – This is yet another provision which is only required by RBI in case of STC transactions. However, even in the context of RBI regulations, what exactly constitutes a homogenous asset is mostly a subjective test. SEBI has defined homogenous to mean same or similar risk or return profile arising from the proposed underlying for a securitised debt instrument. This has made the test of homogeneity even more subjective. For the purpose of determining homogeneity, reference can be made to the homogeneity parameters laid out by RBI in case of Simple, Transparent and Comparable securitization transactions.

- SDIs will need to be fully paid up- The SDIs will need to be fully paid up, i.e., partly paid up SDIs cannot be securitised.

- Originators to have a track record of 3 financial years: Originators should be in the same business of originating the receivables being securitised for a period of at least three financial years. This restricts new entities from securitising their receivables. However, this condition in our view should only apply to business entities other than business entities, complying with this condition does not seem feasible.

- Obligors to have a track record of 3 financial years– The intent behind this seems to to reduce the risk associated with the transaction as the obligors having a track record in the same operations which resulted in the creation of receivables being securitized. However, this condition cannot be met in most types of future flow securitisation transactions such as toll road receivables and receivables from music royalties.

SEBI has made it clear that the last two conditions of maintenance of track record of 3 years for originators and obligors will not apply in case of transactions where the originators is an RBI regulated entity.

Amendments only applicable in case of public issue of SDIs

The following amendments will only be applicable if the SDIs are issued to the public. Here, it may be noted that the maximum number of investors in case of private placement of SDIs is limited to 50.

Minimum Ticket Size

The Erstwhile SDI Regulations did not provide for any minimum ticket size. However, with a view to align the SDI regulations with that of RBI’s SSA Direction, a minimum ticket size of Rs. 1 crore has been mandated in case of originators which are RBI regulated as well as of non-RBI regulated entities. It may however be noted that the minimum ticket size requirement has only been introduced in case of public offer of SDIs. Further, in cases with SDIs having listed securities as underlying, the minimum ticket size shall be the face value of such listed security.

Securitisation is generally perceived as a sophisticated and complex structure and therefore the regulators are not comfortable in making the same available to the retail investors. Accordingly, a minimum ticket size of Rs. 1 Crore has been mandated for public issue of SDIs. In case of privately placed SDIs, the issuer will therefore have the discretion to decide on the minimum ticket size. However, since the RBI also mandates a minimum ticket size of Rs. 1 Crore, financial sector entities will need to adhere to the same.

Here, it is also important to note that in case of public issue of SDIs with respect to originators not regulated by RBI, SEBI has made it clear that the minimum ticket size of Rs. 1 Crore should be seen both at initial subscription as well as at the time of subsequent transfers of SDIs. However, nothing has been said for subsequent transfers in cases where the originator is a RBI regulated entity. The RBI SSA Directions also requires such minimum ticket size of Rs. 1 Crore to be seen only at the time of initial subscription. This in many cases led to the securitisation notes being broken down into smaller amounts in the secondary market.

In the absence of anything mentioned for RBI regulated entities, it can be said that there is no change with respect to the ticket size for RBI regulated entities even in the case of publicly issued SDIs which should be seen only at the time of initial subscription.

It is worth mentioning that under the SSA Directions of RBI requires that in case of transactions carried out outside of the SSA Directions (the transactions undertaken by non-RBI regulated entities), the investors which are regulated by RBI have to maintain full capital charge. This therefore discourages Banks from investing in securitisation transactions which are carried out outside the ambit of the SSA Directions. Therefore, both retail investors as well RBI regulated entities will not be the investors which will hinder liquidity and overall growth of the SDI market.

Minimum Risk Retention

Aligning with RBI’s SSA Direction, a Minimum Risk Retention (MRR) requirement for public issue of SDIs has been mandated requiring retention by the originator of a minimum of

- 5% in case the residual maturity of the underlying loans is upto 24 months and

- 10% in case residual maturity is more than 24 months

Further, in case of RMBS transactions, the MRR has been kept at 5% irrespective of the original tenure.

SEBI has aligned the entire MRR conditions with that of the RBI SSA Directions, including the quantum and form of maintenance of MRR. Accordingly, for financial sector entities, there is no change with respect to MRR.

By introducing MRR in the SDI Regulations, non-financial sector entities will be held to similar standards of accountability, skin-in-the-game, reducing the risks associated with the originate-to-sell model and aligning their practices with those of financial sector originators. This will strengthen investor confidence across the board and mitigate risks of moral hazard or lax underwriting standards.

It may however be noted here that in case of non financial originators, there could be situations where retention is being maintained in some form (for example in leasing transactions, the residual value of the leased assets continues to be held by the originator) and therefore such originators will be required to hold MRR in addition to the retention maintained.

Minimum Holding Period

SEBI has aligned the MHP conditions as prescribed under the SSA directions for all RBI regulated entities. Accordingly, there is no additional compliance requirement for RBI regulated entities. For receivables other than loans, the MHP condition will be specified by SEBI.

Exercise of Clean up Call option by the originator

The provisions for the exercise of the clean up call option has been aligned with those prescribed under the SSA Directions. These provisions have been introduced under the chapter applicable in case of public offer of SDIs. However, the SDI Regulations always provided for the exercise of clean up call option and what has been now introduced in simply the manner in which such an option has to be exercised.

In case of private placement of SDIs, can the clean up call option be exercised at a threshold exceeding 10% ?

Although the provisions for the exercise of clean up call options has been made a part of chapter applicable in case of public offers, it should however be noted that these provisions are also a part of the RBI SSA Directions. Accordingly, financial sector originators are bound by such conditions even if they go for private placement of SDIs. Further, even in the case of the non-financial sector originator, clean up call is simply the clean up of the leftovers when they serve no economic purpose. Therefore, in our view, exercising clean up calls at a higher threshold should not arise.

Periodic Disclosures to be made

On December 16, SEBI issued a circular (‘Periodic Disclosure Circular’) mandating periodic disclosures in respect of Securitised Debt Instruments (SDIs).

The disclosure requirements are effective from March 31, 2026 and are required to be made on a periodic basis within 30 days from the end of March and September each year.

The format for the disclosures has been aligned with the periodic disclosure requirements mandated by the RBI for securitisation transactions. Under the Periodic Disclosures Circular, formats have been prescribed for (i) securitisation of loans, listed SDIs, and credit facilities, and (ii) other types of exposures.

Major disclosure requirements include Maturity characteristics of the underlying assets, MHP and MRR details, rating, recovery initiatives for default cases, industry-wise and geography-wise breakups, etc.

Other Amendments

- Norms for liquidity facility aligned with that of RBI regulations

- All references to the Companies Act 1956 has been changed to Companies Act 2013

- Chapter on registration of trustees has been removed and reference has been made to SEBI (Debenture Trustees) Regulations, 1993

- Disclosure requirements for the originator and the SPDE have been prescribed; however the disclosure formats are yet to be issued by SEBI.

- Public offer of SDIs to remain open for a minimum period of 2 working days and upto a maximum of 10 working days.

Amendments proposed in the SEBI(LODR) Regulations

There are primarily two regulations which govern the listing of SDIs:

- SEBI SDI Regulations

- SEBI LODR Regulations

The following amendments have been proposed in the LODR regulations:

- SCORES registration to be taken at the trustee level

- Outstanding litigations, any material developments in relation to the originator or servicer or any other party to the transaction which could be prejudicial to the interests of the investors to be disclosed on an annual basis.

- Servicing related defaults to be disclosed on an annual basis.

[1] Read an article on the concept of sustainable SDIs at – https://vinodkothari.com/2024/09/sustainable-securitisation-the-next-in-filling-sustainable-finance-gap-in-india

Bond Credit Enhancement Framework: Competitive, rational, reasonable

-Vinod Kothari (vinod@vinodkothari.com)

The RBI’s proposed framework for partial credit enhancement for bonds has significant improvements over the last 2015 version

The RBI released the draft of a new comprehensive framework for non-fund based support, including guarantees, co-acceptances, as well as partial credit enhancement (PCE) for bonds. The PCE framework is proposed to be significantly revamped, over its earlier 2015 version.

Note that PCE for corporate bonds was mentioned in the FM’s Budget 20251, specifically indicating the setting up of a PCE facility under the National Bank for Financing of Infrastructural Development (NaBFID).

A quick snapshot of how PCE works and who all can benefit is illustrated below:

The highlights of the changes under the new PCE framework are:

What is PCE?

Partial Credit Enhancement (PCE) is a risk-mitigating financial tool where a third party provides limited financial backing to improve the creditworthiness of a debt instrument. Provision of wrap or credit support for bonds is quite a common practice globally.

PCE is a contingent liquidity facility – it allows the bond issuer to draw upon the PCE provider to service the bond. For example, if a coupon payment of a bond is due and the issuer has difficulty in servicing the same, the issuer may tap the PCE facility and do the servicing. The amount so tapped becomes the liability of the issuer to the PCE provider, of course, subordinated to the bondholders. In this sense, the PCE facility is a contingent line of credit.

A situation of inability may arise at the time of eventual redemption of the bonds too – at that stage as well, the issuer may draw upon the PCE facility.

Since the credit support is partial and not total, the maximum claim of the bond issuer against the PCE provider is limited to the extent of guarantee – if there is a 20% guarantee, only 20% of the bond size may be drawn by the issuer. If the facility is revolving in nature, this 20% may refer to the maximum amount tapped at any point of time.

Given that bond defaults are quite often triggered by timing and not the eventual failure of the bond issuer, a PCE facility provides a great avenue for avoiding default and consequential downgrade. PCE provides a liquidity window, allowing the issuer to arrange liquidity in the meantime.

Who can be the guarantee provider?

PCE under the earlier framework could have been given by banks. The ambit of guarantee providers has been expanded to include SCBs, AIFIs, NBFCs in Top, Upper and Middle Layers and HFCs. However, in case of NBFCs and HFCs, there are additional conditions as well as limit restrictions.

As may be known, entities such as NABFID have been tasked with promoting bond markets by giving credit support.

Who may be the bond issuers?

The PCE can be extended against bonds issued by corporates /special purpose vehicles (SPVs) for funding all types of projects and to bonds issued by Non-deposit taking NBFCs with asset size of ₹1,000 crore and above registered with RBI (including HFCs).

What are the key features of the bonds?

- REs may offer PCE only in respect of bonds whose pre-enhanced rating is “BBB minus” or better.

- REs shall not invest in corporate bonds which are credit enhanced by other REs. They may, however, provide other need based credit facilities (funded and/ or non-funded) to the corporate/ SPV.

- To be eligible for PCE, corporate bonds shall be rated by a minimum of two external credit rating agencies at all times.

- Further, additional conditions for providing PCE to bonds issued by NBFCs and HFCs:

- The tenor of the bond issued by NBFCs/ HFCs for which PCE is provided shall not be less than three years.

- The proceeds from the bonds backed by PCE from REs shall only be utilized for refinancing the existing debt of the NBFCs/ HFCs. Further, REs shall introduce appropriate mechanisms to monitor and ensure that the end-use condition is met.

What will be the form of PCE?

PCE shall be provided in the form of an irrevocable contingent line of credit (LOC) which will be drawn in case of shortfall in cash flows for servicing the bonds and thereby may improve the credit rating of the bond issue. The contingent facility may, at the discretion of the PCE providing RE, be made available as a revolving facility. Further, PCE cannot be provided by way of guarantee.

What is the difference between a guarantee and an LOC? If a guarantor is called upon to make payments for a beneficiary, the guarantor steps into the shoes of the creditor, and has the same claim against the beneficiary as the original creditor. For example, if a guarantor makes a payment for a bond issuer’s obligations, the guarantor will have the same rights as the bondholders (security, priority, etc). On the contrary, the LOC is simply a line of liquidity, and explicitly, the claims of the LOC provider are subordinated to the claims of the bondholders.

If the bond partly amortises, is the amount of the PCE proportionately reduced? This should not be so. In fact, the PCE facility continues till the amortisation of the bonds in full. It is quite natural to expect that the defaults by a bond issuer may be back-heavy. For example, if there is a 20% PCE, it may have to be used for making the last tranche of redemption of the bonds. Therefore, the liability of the PCE provider will come down only when the outstanding obligation of the bond issuer comes to less than the size of the PCE.

Any limits or restrictions on the quantum of PCE by a single RE?

The existing PCE framework restricts a single entity to providing only 20% of the total 50% PCE limit for a bond issuance. It is now proposed that the sub-limit of 20% be removed, enabling single entity to provide upto 50% PCE support.

Further, the exposure of an RE by way of PCEs to bonds issued by an NBFC/ HFC shall be restricted to one percent of capital funds of the RE, within the extant single/ group borrower exposure limits.

Who can invest in credit-enhanced bonds?

Under the existing framework, only the entities providing PCE were restricted from investing in the bonds they had credit-enhanced. However, the new Draft Directions expand this restriction by prohibiting all REs from investing in bonds that have been credit-enhanced through a PCE, regardless of whether they are the PCE provider. The draft regulations state that the same is with an intent to promote REs enabling wider investor participation.

This is, in fact, a major point that may need the attention of the regulator. A universal bar on all REs from investing in bonds which are wrapped by a PCE is neither desirable, nor optimal. Most bond placements are done by REs, and REs may have to warehouse the bonds. In addition, the treasuries of many REs make opportunistic investments in bonds.

Take, for instance, bonds credit enhanced by NABFID. The whole purpose of NABFID is to permit bonds to be issued by infrastructure sector entities, by which banks who may have extended funding will get an exit. But the treasuries of the very same banks may want to invest in the bonds, once the bonds have the backing of NABFID support. There is no reason why, for the sake of wider participation, investment by regulated entities should be barred. This is particularly at the present stage of India’s bond markets, where the markets are not liquid and mature enough to attract retail participation.

What is the impact on capital computation?

Under the Draft Directions the capital is required to be maintained by the REs providing PCE based on the PCE amount based on applicable risk weight to the pre-enhanced rating of the bond. Under the earlier framework, the capital was computed so as to be equal to the difference between the capital required on bond before credit enhancement and the capital required on bond after credit enhancement. That is, the existing framework ensures that the PCE does not result into a capital release on a system-wide basis. This was not a logical provision, and we at VKC have made this point on various occasions2.