SEBI proposes to ease HVDLEs from equity linked CG norms

Several proposals on the way to ease compliance

-Pammy Jaiswal, Partner & Sourish Kundu, Executive (corplaw@vinodkothari.com)

Introduction:-

The applicability of CG norms (on a COREX basis) was extended to HVDLEs i.e. entities having an outstanding value of listed non-convertible debt securities of Rs. 500 Crore and above, by SEBI vide its notification dated 7th September, 2021. Following the extension thread for mandatory applicability of Corporate Governance (CG) norms under SEBI Listing Regulations (LODR) on High-Value Debt Listed Entities (HVDLEs) from FY 23-24 to FY 24-25 and again postponing it from 1st April, 2025, SEBI released another Consultation Paper (CP) on 31st October, 2024 containing several proposals to ease the compliance burden of HVDLEs. A similar CP was issued earlier on 8th October, 2024 to review the CG norms primarily focusing on related party transactions (RPTs) [Our analysis on the same can be read here].

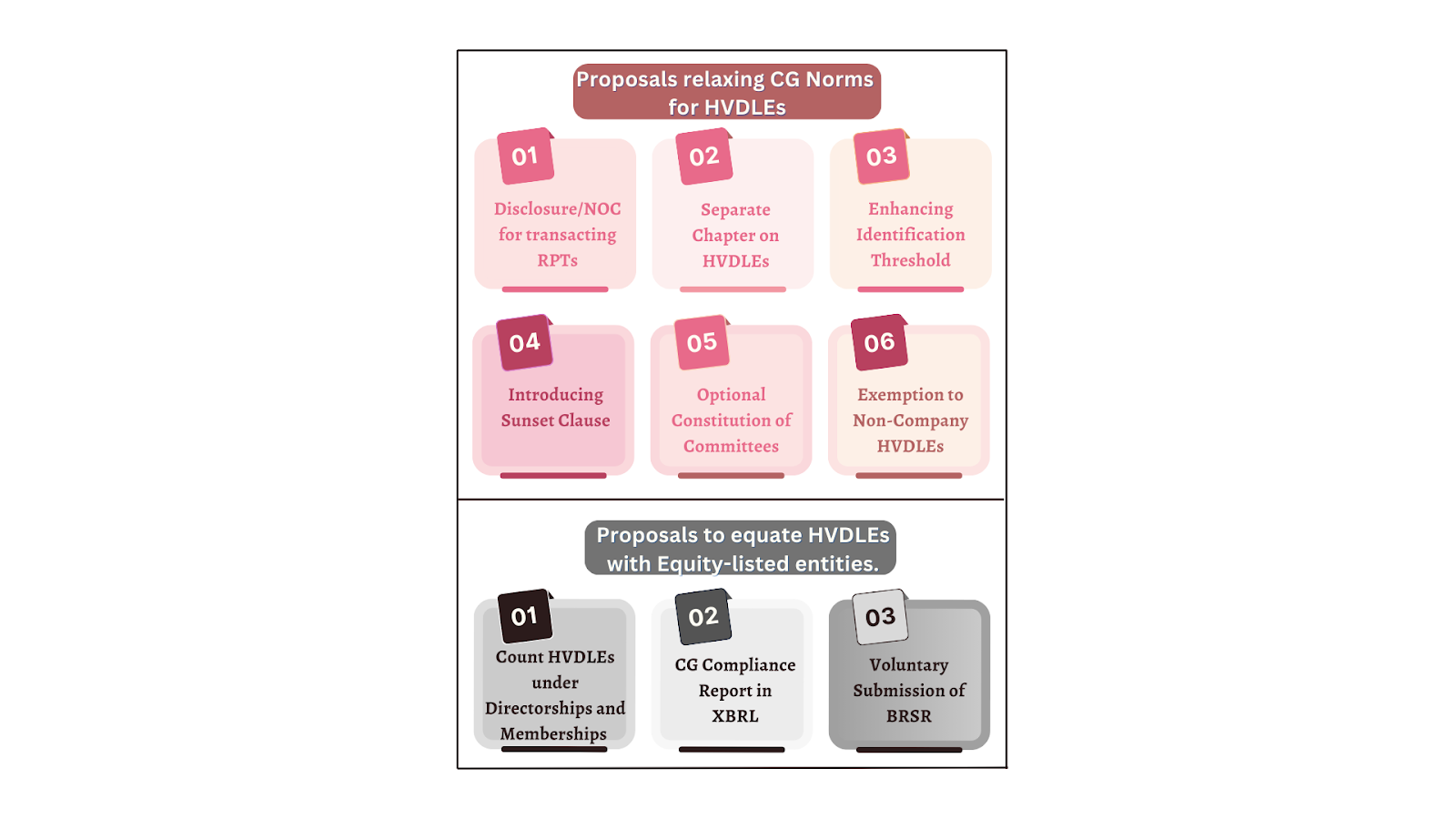

While the intent behind the CG norms being made applicable was to protect debenture holders and assimilate corporate governance amongst such issuer entities, the complexities associated with its implementation hindered the ease of doing business and increased the compliance burden manifold. The current CP delves into the comments received on the previous proposal as well as the issues that HVDLEs have been facing in practically implementing the CG norms (i.e. Regulations 16 to 27 of LODR, 2015). While it discusses the much needed and critical areas (CG chapter, mandatory committees, RPTs, etc.) where HVDLEs can be considered to be relieved and not be kept on the same pedestal as that of the equity listed entities, however, for some provisions (included for max no. of directorship, committee membership, XBRL filings, etc.), HVDLEs have been proposed to be roped in at par with entities with their specified securities listed. While each of the proposals have been discussed in detail below, a snapshot of the same can be seen in the diagram below:

Proposals relaxing CG Norms for HVDLEs

- Providing In-Principle Declaration or obtaining No-Objection Certificate (NOC) from NCD holders in connection with RPTs:

One of the most crucial concerns for HVDLEs was the impossibility of compliance when it came to securing approvals for RPTs. The same was highlighted by SEBI in its earlier CP dated 8th February, 2023 wherein it was mentioned that 104 out of 138 HVDLEs as of 31st March, 2022, comprised of shareholders with more than 90% of them being related parties (RPs).

The current proposal is set against a reference to a banking transaction wherein the lender reserves the right to allow the borrower to enter into any transaction that might be unfavorable to the lender such as entering into RPTs. Thus, HVDLEs being of the nature of a borrower and the debenture holders being the lenders, it is paramount to protect the latter’s interests by enforcing such provisions as may be necessary and safeguarding them through a debenture trustee.

In view of the same, the proposition has the following features:

- Either provide an upfront declaration in the offer document with respect to the amount of RPTs proposed to be entered over the tenure of the NCDs along with the percentage of the same when compared with the issue size or obtain an NOC from the debenture trustee, who in turn needs to obtain it from the debenture holders (the majority not being related to the issuer) for all the material RPTs as and when they are required to be transacted;

- VKCo Comments – Until the fine print of the regulations is rolled out, it is understood that only the broader limits of the estimated RPTs are required to be mentioned unless otherwise finer details are required which can become extremely difficult for these entities.Further, for the alternative requirement, there does not seem to be any incentive to first approach the debenture trustee and thereafter the trustee to approach the NCD holders, which can actually be done directly.

- monitoring of the issue proceeds by a credit rating agency; and

- declare the following in the offer document upfront and be maintained over the tenure of the NCDs:

- debt-equity ratio,

- debt service coverage ratio;

- interest service coverage ratio and;

- such other financial/ non-financial covenants

- VKCO Comments – Both the aforesaid proposals do not serve the exact purpose of maintaining controls over RPT. Also, these are also reflected in the financials to some extent.

- Introduction of a separate chapter for the governance of HVDLEs

LODR in its present form consists of 12 Chapters, each having its purpose and application. As far as the CG norms are concerned, HVDLEs are required to follow the provisions primarily centered around equity listed entities which, inter alia, relate to the composition of the Board of Directors, the constitution of various specialized committees, stipulations regarding RPTs and so on. Having said that, these provisions are not completely relatable to HVDLEs since the majority of these entities are purely debt listed without any other security being listed. Accordingly, it has been proposed to introduce a separate chapter on CG norms for HVDLEs distinct from the existing one for equity listed entities.

VKCO Comments: While this proposal is noteworthy, however, instead of rolling out a new chapter, there could have been certain modifications in the existing regulations by way of a proviso to align with the needs of an HVDLE. Further, one also needs to wait to see the fine print of the provisions once the same is issued.

- Increase in threshold for being identified as an HVDLE

Based on the data provided by NSDL as of 31st March, 2024, the number of pure debt listed entities with an outstanding of more than Rs. 500 crores is 166 (comprising of an aggregate outstanding of Rs. 13.54 lakh crores), of which 112 entities are those having an outstanding of more than Rs. 1,000 crores (comprising of an aggregate outstanding of Rs. 13.16 lakh crores).

Further, referring to SEBI’s circular dated 19th October, 2023 in which the threshold limit of outstanding long-term borrowing was enhanced from Rs.100 crore to Rs.1,000 Crore for the purpose of being identified as a Large Corporate called for introspection at the existing threshold of being identified as an HVDLE. Aligned with its objectives of tightening the regulatory regimes for debt listed entities and at the same time promoting ease of doing business in the corporate bond market, the proposal suggests doubling the limit from the present threshold of Rs. 500 crores to Rs. 1,000 crores.

VKCo Comments: The proposal to enhance the extant threshold is encouraging in terms of governing the maximum value of outstanding debt while at the same time achieving the same without bearing the burden of compliance by an increased number of purely debt listed entities. Subsequently, effective implementation of such a proposal aligns it with the identification criteria of Large Corporates.

- Introduction of “sunset provisions” for non-applicability of CG norms:

The extant Regulation 3(3) of SEBI (LODR), 2015 provides for the applicability of the CG norms even when the value of the outstanding debt securities falls below the specified threshold forever. The same is in contradiction with respect to the period of applicability as compared to its equity counterpart wherein Regulation 15(2)(a) provides that the norms will have to be complied till such time that the equity share capital or net-worth of the listed entity falls and remains below the specified threshold for a period of three consecutive financial years. Accordingly, for the purpose of aligning the non-applicability, a similar sunset provision for HVDLEs too has been proposed. The proposal outlines that the CG norms shall continue to remain in force for HVDLEs till such time the value of outstanding debt listed securities (reviewed on the cutoff day being 31st March of every financial year) reduces and remains below the defined limits for a period of three consecutive financial years and further ensuring compliance within a period of six months from the date of a subsequent increase in the value above the trigger. The proposition also provides for disclosing such compliances in the Corporate Governance compliance report to be submitted on and following the third quarter of the trigger.

VKCO Comments: The proposal is welcome since it clearly sets the HVDLEs free from the barrier of once an HVDLE so always an HVDLE. This proposal sets a clear nexus between the compliance and the size of the debt outstanding, for the protection of which in the very first place, the compliance triggered.

- Certain mandatory committees made optional

Regulations 19, 20 and 21 of LODR mandate the constitution of the Nomination and Remuneration Committee (NRC), Stakeholders Relationship Committee (SRC) and Risk Management Committee (RMC) respectively and provide for their composition, the number of meetings to be held, quorum, duties and responsibilities, among other things. The proposal recognises the difficulties of constituting multiple committees by HVDLEs and therefore, extends the option of either establishing such committees or ensuring delegation and discharge of their functions by the Audit Committee in the case of NRC and RMC and by the Board of Directors in case of SRC.

VKCo Comments: Given the close construct of debt listed entities, it is often observed that the constitution of such committees becomes more of a hardship than in smoothening compliance and discussing specific matters. Accordingly, it looks appropriate to redirect the functions of NRC and RMC to the Audit Committee and that of the SRC to the Board.

- Exemption to entities not being a Company

Several entities are not incorporated in the form of companies and therefore, are regulated by specific acts of the Parliament. The rationale behind this move lies in the fact that the administration of these entities is governed by such specific Acts subject to approval from the concerned Ministries. An exclusion on similar lines was granted to equity listed entities by way of Regulation 15(2)(b) which was later omitted w.e.f. 1s September, 2021 vide notification dated 5th May, 2021.

Further, it is awaited as to how effective and permanent such an exemption would be, but SEBI’s working group has proposed for dispensation of entities like NABARD, SIDBI, NHB, EXIM Bank and such other entities fulfilling the criteria as laid out above and application of CG norms to the extent that it does not violate their respective regulatory framework formulated by the concerned authorities.

VKCo Comments: While SEBI refers to the introduction of similar exclusion for equity listed entities, however, it has also mentioned the subsequent amendment wherein the same was omitted. In any case, the instant proposal is a welcome change since it will help such entities to give preference to their principal statutes and not an ancillary one like LODR.

Proposals to equate certain CG Norms for HVDLEs to that of equity listed entities:

- Count HVDLEs under no. of directorships, and memberships of Committees:

The extant provisions of Regulation 17A of LODR and Section 165 of the Companies Act, 2013 limit the number of directorship positions that a person can hold, with appropriate sub-limits being set out with respect to public companies and equity listed companies. Similarly, Regulation 26 of the SEBI (LODR), 2015 places ceiling limits on the number of memberships and chairmanships that a person can hold in committees across all listed entities, with explicit exclusion for such positions held in HVDLEs.

The instant proposal is for including the directors in HVDLEs as well as committee membership and chairpersonship positions held in HVDLE just as equity listed entities are included.

The same has been proposed in view of the fact that directorship is a significant position in any company and therefore, multiple directorships beyond a reasonable limit are likely to inhibit the ability of a person to allocate appropriate time to play an effective role in delivering its responsibilities including the timely repayment of debt..

Further, the initial proposal for inclusion of HVDLEs in max no. of directorship allows a period of six months or till the next AGM to ensure compliance.

VKCO Comments: The rationale completely aligns with the proposal made and seems to be justified.

- Compulsory filing of CG Compliance Report in XBRL format:

Pursuant to Regulation 27(2), which mandates the submission of a quarterly report on complying with CG norms by listed entities, the format of the report has been supervised by Annexure 3 under Section II-B of the Master Circular for compliance with the provisions of SEBI (LODR), 2015 by listed entities in case of equity listed entities and Annexure VII-A under Chapter VII of the Master Circular for listing obligations and disclosure requirements for Non-convertible Securities, Securitized Debt Instruments and/or Commercial Paper in case of HVDLEs. The issue arises from the practice adopted by HVDLEs in the instant case, where filings made on the website of the stock exchange have been made in PDF format thereby affecting the readability and clause-wise compliance monitoring. Unlike the above-mentioned proposals which aim at bringing about relaxations for HVDLEs, this particular proposal tightens the regime by binding the XBRL format that is consistent with what is being filed by equity listed entities, for the report to be submitted on a quarterly basis.

VKCo Comments: This proposal is with an objective to align and standardize the filing of quarterly CG compliance report for bringing parity as in the case of equity listed entities.

- Voluntary submission of Business Responsibility and Sustainability Report (BRSR):

This proposal originates from SEBI’s endeavour to inculcate good CG practices in HVDLEs, to be at par with equity listed entities. It is supported by Regulation 34(2)(f) which requires the top 1,000 listed entities (based on market capitalization) to include a BRSR in their annual report. It is pertinent to note in this respect that publishing of BRSR by HVDLEs is voluntary and not a mandatory requirement unless such an HVDLE also satisfies the criteria of the above-stated regulation.

VKCo Comments: The inclusion of a voluntary provision in the legislation with respect to a comprehensive report like BRSR is not likely to be submitted given the huge details under the BRSR. However, an opportunity to submit BRSR can be a game changer for an HVDLE from the perspective of being able to raise funds based on its reporting standards in this regard.

Concluding Remarks:

The proposal under the CP provides hope for a breather when it comes to compliance with CG norms and at the same time introduces certain new requirements to maintain uniformity whether it is for the XBRL filing or inclusion of directorship and committee membership as well as chairmanship in an HVDLE for the max no. of such positions. It will also be interesting to see what is rolled out under the new chapter for HVDLEs as well as the fine print of provisions as far as RPT controls are concerned.

Refer to our related resources below: