RBI’s Pillar 3 Proposes Disclosure of Liquidity Risks and Measures

Move from Narrative Disclosures to Structured Transparency

– Payal Agarwal, Partner | payal@vinodkothari.com

The draft Capital Adequacy Amendment Directions of RBI propose changes to the existing Directions in relation to the Pillar 3 disclosure requirements (Market Discipline). The amendments are proposed to be made towards better alignment of the regulatory disclosure framework with the Basel norms. In addition to the new disclosure requirements with respect to Liquidity Risks and Macro-prudential Supervisory measures, the Draft proposes a move from narrative disclosures to a more structured, comprehensive transparency.

Proposed to be effective from: quarter ended 30th September, 2026

Highlights of the proposal

- Banks to have formal disclosure policy for Pillar 3 data

- Key elements of the policy to be described in the year-end Pillar 3 report or cross- referenced to another location where they are available

- Formal attestation by one or more WTDs in writing that Pillar 3 disclosures have been prepared in accordance with the board-agreed internal control processes

- Safeguarding proprietary and confidential information:

- Disclosure not required for proprietary or confidential information that may reveal the position of a bank or contravene its legal obligations

- More general information about the subject matter including the fact that specific items of information have not been disclosed and the reasons thereof.

- Guiding principles of Pillar 3 disclosures specified

- Disclosures to be clear, comprehensive, meaningful, consistent and comparable

- Disclosure of data points for previous period not required in case of first-time reporting of a metric

- For permitted transitions, the transitional data shall be reported unless the bank is compliant with fully loaded requirements

- For regulatory disclosures on the website, archive period proposed to increase to 10 years, against existing 3 years’ requirement

Disclosure on Liquidity Risk Management measures

The proposed format, amongst others, incorporates a new field for liquidity related disclosures. This includes, qualitative and quantitative disclosures on liquidity risk management aspects, alongside disclosure of Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR):

| Qualitative disclosures: LRM governance Funding strategy including policies on diversification and tenor Liquidity risk mitigation techniquesExplanation of stress testingOutline of contingency funding plans | Quantitative disclosures: Measurement tools for structural liquidity and cash flow projections Concentration limits on collateral pools and sources of fundingLiquidity exposures and funding needs and entity and branch level including limitations on transferability of liquidityBalance sheet and off-balance sheet items broken down into maturity buckets and the resultant liquidity gaps |

Contents of disclosure (Annex III)

|

Proposed Format |

Existing Format |

New Disclosures |

Frequency of Disclosure |

|---|---|---|---|

|

1. Overview of risk management, key prudential metrics, and RWA |

|||

|

Template KM1: Key metrics (at consolidated group level) |

New addition in the form of summary table, cross-linked to respective detailed tables |

|

Quarterly |

|

Table OVA: Bank risk management approach |

General qualitative disclosure requirement under Risk Exposure and Assessment |

More granular information such as risk governance structure, qualitative information on stress testing etc. |

Annual |

|

Template OV1: Overview of RWA |

No specific equivalent |

RWAs and minimum capital requirements broken down for various risk categories: credit, CCR, market, operational etc. |

Quarterly |

|

2. Linkages between financial statements and regulatory exposures |

|||

|

Table LIA: Explanations of differences between accounting and regulatory exposure amounts |

New table, some information overlap with Table DF-1: Scope of application |

Qualitative explanations on the differences observed between accounting carrying value and amounts considered for regulatory purposes |

Annual |

|

Table LIB: Outline of the differences in the scope of consolidation (entity by entity) |

Corresponds to Table DF-1: Scope of application |

– |

Annual |

|

Template LI1: Differences between accounting and regulatory scopes of consolidation and mapping of financial statement categories with regulatory risk categories |

No specific table; however, overlaps with Table DF-12: Composition of capital – reconciliation requirements |

Breakdown of each component of balance sheet by risk framework — credit risk, CCR, securitisation, market risk, or not subject to capital requirements/ capital deduction |

Annual |

|

Template LI2: Main sources of differences between regulatory exposure amounts and carrying values in financial statements |

No specific table; source of material differences between its total balance sheet assets (net of on-balance sheet derivative and SFT assets) as reported in its financial statements and its on-balance sheet exposures to be disclosed and detailed in line 1 of the common disclosure template. |

Detailed template covers sources of differences, viz., valuation differences, netting differences, provisions, and prudential filters — by risk category column. |

Annual |

|

Template PV1 – Prudent valuation adjustments (PVAs) |

– Only a single line-item within regulatory capital composition table |

Break down PVAs by type (CVA loss, closeout cost, early termination, model risk, operational risk, funding costs, administrative costs, other) and by instrument category (equity, rates, FX, credit) and book (trading / banking). |

Annual |

|

3 Composition of Capital |

|||

|

Table CCA – Main features of regulatory capital instruments |

Table DF-13: Main features of regulatory capital instruments |

– |

Ongoing, at least on a semi-annual basis |

|

Template CC1 – Composition of regulatory capital |

Table DF-11: Composition of capital |

– |

Semi-annual |

|

Template CC2: Reconciliation of regulatory capital to balance sheet |

Table DF-12: Composition of capital – reconciliation requirements |

Higher granularity provided under each line-item |

Semi-annual |

|

4 Remuneration |

|||

|

Table REMA – Remuneration policy |

Qualitative disclosures under Table DF-15: Disclosure requirements for remuneration |

Annual |

|

|

Template REM1 – Remuneration awarded during financial year |

Quantitative disclosures under Table DF-15: Disclosure requirements for remuneration |

More granular details sought |

Annual |

|

Template REM2: Special payments |

Annual |

||

|

Template REM3: Deferred remuneration |

Annual |

||

|

5. Credit Risk |

|||

|

Table CRA – General qualitative information about credit risk |

Table DF-3: Credit risk: general disclosures for all banks |

Specific disclosure w.r.t. credit risk function, viz.,

|

Annual |

|

Template CR1: Credit quality of assets |

Semi-annual |

||

|

Template CR2: Changes in stock of non-performing loans and debt securities |

Semi-annual |

||

|

Table CRB: Additional disclosure related to the credit quality of assets |

|

Annual |

|

|

Table CRC: Qualitative disclosure related to credit risk mitigation techniques |

Table DF-5: Credit risk mitigation: disclosures for standardised approaches |

– |

Annual |

|

Template CR3: Credit risk mitigation techniques – overview |

– |

Semi-annual |

|

|

Table CRD: Qualitative disclosures on bank’s use of external credit ratings under the standardised approach for credit risk |

Table DF-4 – Credit risk: disclosures for portfolios subject to the standardised approach (qualitative) |

Annual |

|

|

Template CR4: Standardised approach – credit risk exposure and Credit Risk Mitigation (CRM) effects |

– |

On-balance sheet and off-balance sheet exposures for each asset class:

|

Semi-annual |

|

Template CR5: Standardised approach – exposures by asset classes and risk weights |

Table DF-4 – Credit risk: disclosures for portfolios subject to the standardised approach (quantitative) |

Risk weight buckets increased; existing format divides into 3 major risk buckets |

Semi-annual |

|

6. Counterparty credit risk |

|||

|

Table CCRA – Qualitative disclosure related to counterparty credit risk |

Table DF-10: General disclosure for exposures related to counterparty credit risk |

– |

Annual |

|

Template CCR1 – Analysis of counterparty credit risk (CCR) exposure by approach |

Structured in a tabulated form with more granular data requirements |

Semi-annual |

|

|

Template CCR3 – CCR exposures by regulatory portfolio and risk weights |

Semi-annual |

||

|

Template CCR4 – Composition of collateral for CCR exposures |

Semi-annual |

||

|

Template CCR5 – Credit derivatives exposures |

|||

|

Template CCR6 – Exposures to central counterparties |

|||

|

7. Securitisation |

|||

|

Table SECA – Qualitative disclosure requirements related to securitisation exposures |

Table DF-6: Securitisation exposures: disclosure for standardised approach |

List of:

|

Annual |

|

Template SEC1 – Securitisation exposures in the banking book |

Bifurcation based on:

|

Semi-annual |

|

|

Template SEC2 – Securitisation exposures in the trading book |

Semi-annual |

||

|

Template SEC3 – Securitisation exposures in the banking book and associated regulatory capital requirements – bank acting as originator |

– |

Semi-annual |

|

|

Template SEC4 – Securitisation exposures in the banking book and associated capital requirements – bank acting as investor |

– |

Semi-annual |

|

|

8. Market Risk |

|||

|

Table MRA – Qualitative disclosure requirements related to market risk |

Table DF-7: Market risk in trading book |

Elaboration of qualitative disclosures, viz.,

|

Annual |

|

Template MR1 – Market risk under the standardised approach |

Classification of positions:

|

Semi-annual |

|

|

9. Operational Risk |

|||

|

Table ORA: Disclosure related to operational risk and operational resilience |

Table DF-8: Operational risk |

Elaboration of qualitative disclosures |

|

|

10. Interest rate Risk |

|||

|

Table IRRA: Disclosure related to Interest Rate Risk |

Table DF-9: Interest rate risk in the banking book (IRRBB) |

Elaborated qualitative disclosures |

Annual for qualitative disclosure and semiannual for quantitative disclosure |

|

11. Macroprudential supervisory measures |

|||

|

Template GSIB1 – Disclosure of G-SIB indicators |

– |

12 indicators used in the assessment methodology of the G-SIB framework |

Annual |

|

Template CCyB1 – Geographical distribution of credit exposures used in the countercyclical capital buffer |

– |

Geographical breakdown of private sector credit exposures (values and RWAs) and Countercyclical capital buffer rate for computation of the bank-specific countercyclical capital buffer rate and amount |

Semi-annual |

|

12. Leverage Ratio |

|||

|

Template LR1 – Summary comparison of accounting assets vs leverage ratio exposure measure |

Table DF 17- Summary comparison of accounting assets vs. leverage ratio exposure measure |

– |

Quarterly |

|

Template LR2 – Leverage ratio common disclosure template |

Table DF-18: Leverage ratio common disclosure template |

– |

Quarterly |

|

13. Liquidity |

|||

|

Table LIQA – Liquidity risk management |

– |

See above |

Annual |

|

Template LIQ1 – Liquidity coverage ratio (LCR) |

– |

Unweighted and weighted values of

|

Quarterly |

|

Template LIQ2 – Net stable funding ratio (NSFR) |

– |

Unweighted value by residual maturity and weighted value of

|

Semi-annual |

Remote Device Locking: RBI proposes highly guarded path

Some proposals may be impractical

– Jeel Ranavat, Assistant Manager| finserv@vinodkothari.com

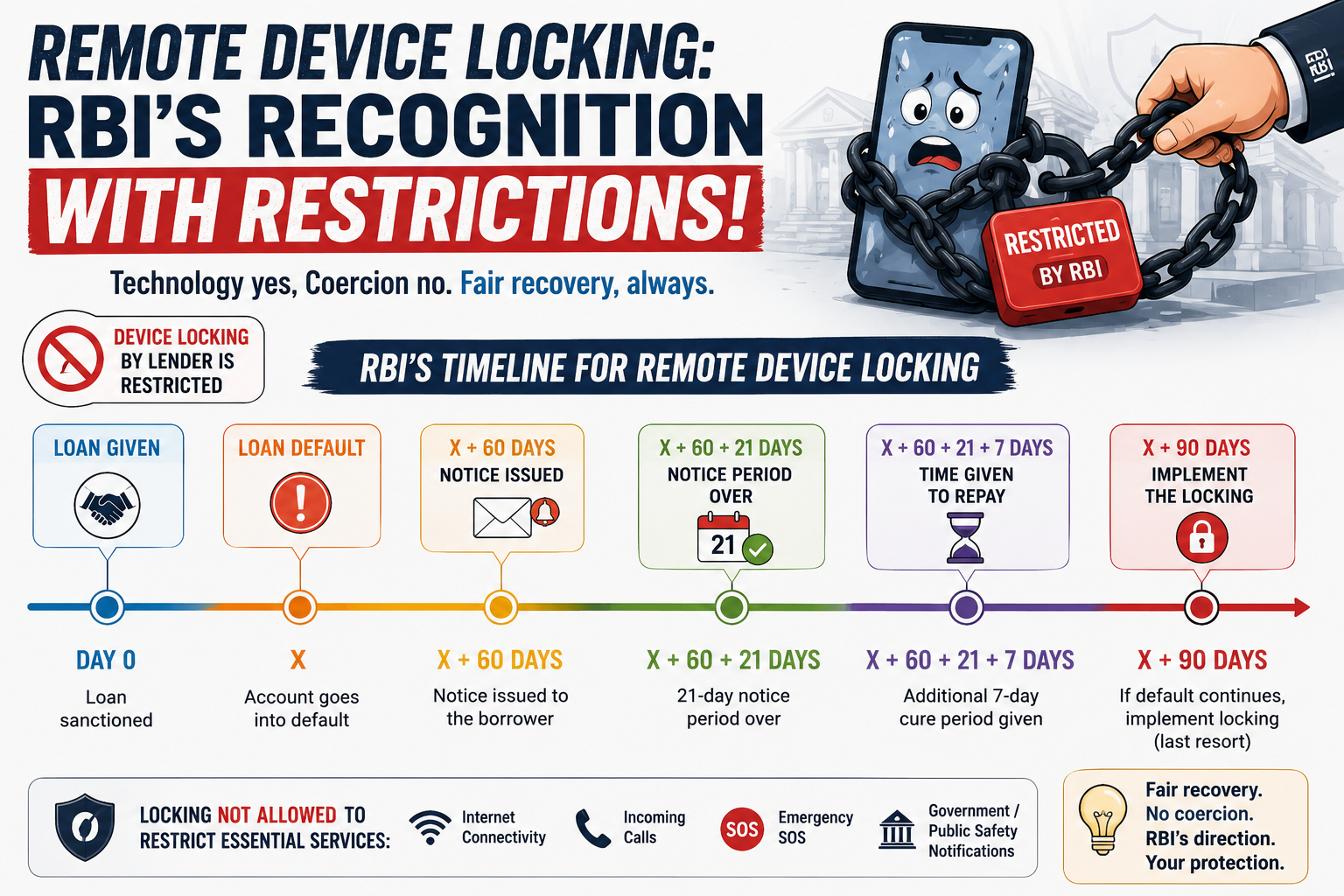

On May 21,2026, RBI issued revised draft RBI (Non-Banking Financial Companies – Responsible Business Conduct) Amendment Directions, 2026 that contains several paragraphs, not being there in the earlier Draft RBI (Non-Banking Financial Companies – Responsible Business Conduct) Second Amendment Directions, 2026 version, which permit a financier of devices to be able to remotely lock its partial functionality, on continued non-payment of dues. Among other safeguards, such as preserving the basic functionality (access to internet, incoming calls, emergency SOS features, and receipt of emergency Government or public-safety notifications), the RBI also imposes a minimum 90 days default to trigger the locking. In our view, given the short tenure of funding, the 90-day default threshold, clearly a legacy of long-term lending practices, is quite impractical in the context. We present the highlights and our critical appraisal of the RBI’s proposals.

Introduction

Remote device locking is fast becoming the new device in recovery practices. With the ability to remotely restrict access to a borrower’s device, lenders are increasingly viewing the technology as a powerful tool to control defaults and strengthen recoveries.

In the past supervisory observations, RBI raised concerns regarding “full device locking” mechanisms adopted by certain lenders/Lending Service Provider (LSPs), noting that such measures may be disproportionate, coercive, and restrict access to essential device functionalities. The concerns appear to stem from borrower protection and fair practices considerations, particularly where borrowers are denied access to basic device features unrelated to the financed asset or outstanding dues.

At the same time, the Digital Personal Data Protection Act, 2023 (DPDP Act) introduces an additional layer of regulatory scrutiny like device-level restrictions and monitoring inherently involve the processing and control of personal data, making borrower consent, lawful processing, proportionality, purpose limitation, and data minimisation central to any remote locking framework.

From a data protection perspective, excessive control over a borrower’s device may raise serious concerns around privacy, digital autonomy, and the broader obligation to safeguard the rights of data principals.

The RBI has issued Revised Draft – RBI (Non-Banking Financial Companies – Responsible Business Conduct) Amendment Directions, 2026 which provides deployment of technology-based mechanism for recovery of loan duesalso known as “Remote Device Locking”, and proposes to restrict the use of device-locking mechanisms as a recovery tool, except where the loan was specifically granted for financing the concerned mobile device.

The regulatory message is increasingly clear that technology-driven recovery mechanisms cannot come at the cost of privacy, fairness, or access to essential digital services.

Pre-requisites for Remote Device Locking

Device-locking mechanisms as a recovery tool is not permitted. However, in case the loan was specifically granted for financing the concerned mobile device, such measures may be adopted by the lenders subject to certain conditions:

- Documentation and Communication:

- Clear and unambiguous disclosure which expressly authorises such restrictions in loan agreement.

- Further, trigger events for initiating recovery-related restrictions must be clearly defined and disclosed upfront to the borrower.

- Prior Notice: A structured notice and cure mechanism must be implemented prior to imposing any restriction.

- A minimum 21-day notice period should be provided once the account reaches 60 DPD, giving the borrower a chance to cure the default.

- Following expiry of 21 days notice an additional 7-day cure period is given to the borrower before any restrictive measure is imposed.

- DPD Status: Restrictions should be invoked only where the account remains in default beyond 90 DPD despite prior notices and cure opportunities, ensuring that such measures are used strictly as a last resort.

- Access Control: Under no circumstances should restrictions impair access to essential device functionalities, including internet connectivity, incoming calls, emergency SOS services, or government/public safety notifications.

Conclusion

Most device financing loans are short-tenure products, typically ranging from 3 to 12 months. If lenders are required to wait until 60 DPD, followed by a 21-day notice period, an additional 7-day cure window, and eventual restriction only after 90 DPD, this may significantly reduce the commercial effectiveness of remote device locking as a recovery tool.

In short-tenure device financing loans, recovery measures are most effective during the early stages of delinquency, when the borrower continues to actively rely on the device.

In practice, several lenders have historically adopted much earlier-stage device restrictions upon payment default. However, RBI appears to be consciously moving away from such practices due to concerns around coercive recovery measures, borrower protection, proportionality, and access to essential digital services.

Securitisation, Transfer and Distribution of Credit Risk- for Banks and NBFCs.

We are pleased to announce the launch of our e-book — Securitisation, Transfer and Distribution of Credit Risk- for Banks and NBFCs.

This book, spanning over 900+ pages, provides a comprehensive analysis of the evolving regulatory and transactional landscape relating to credit risk transfer in India, with detailed commentary on:

• RBI regulations on securitisation

• Transfer of Loan Exposures or so-called direct assignments

• Co-lending arrangements

• Loan syndication arrangements

• SEBI regulations governing the issue and listing of securitised debt instruments

Designed specifically for banks, NBFCs, market participants, legal professionals and compliance teams, the publication offers practical insights into the regulatory framework governing structured finance and credit distribution transactions.

The Commentary is based on RBI’s November, 2025 version of consolidated Directions.

The book was launched during the 14th Securitisation Summit, and the e-book is available exclusively through the Premium Section of our website.

Kindly note that access to the book will be for a period of one year from the date of purchase of the book.

Read an excerpt from the book here.

Click here to purchase now directly, or

Table of Contents

About the book ……………………………………………………………………………………………………………………………. 1

Preface to Second Edition …………………………………………………………………………………………………………… 22

Chapter 1: Understanding the Basics of Securitisation & Structured Finance ……………………………………. 24

Chapter 2: Securitisation in India: Tracing the developments in the market ………………………………………. 51

Chapter 3: Asset Classes and Structures in India ……………………………………………………………………………. 67

Chapter 4: Law of assignment and true sale of receivables ……………………………………………………………… 83

Chapter 5: Commentary on the Directions on Securitisation of Standard Assets ………………………………. 107

Chapter 6: Listing Regulations On Securitised Debt Instruments & Security Receipts ……………………… 458

Chapter 7: Commentary on the Directions on Transfer of Loan Exposures ……………………………………… 659

Chapter 8: Co-lending Arrangements …………………………………………………………………………………………. 844

Chapter 9: Loan syndication, Consortium Lending, Participation Certificates and Balance Transfers …. 917

Chapter 10: Taxation aspects of Securitisation, Transfer of Loan Exposures and Co-lending ……………. 939

ABOUT THE CONTRIBUTORS ……………………………………………………………………………………………… 960

SEBI proposes revival of open market buy-backs through stock exchange

– Abhishek Kumar Namdev, Assistant Manager | corplaw@vinodkothari.com

Introduction

Open-market buyback through stock exchanges, earlier discontinued by SEBI in a phased manner based on a 2023 amendment (see an article here), is proposed to be brought back in the buy-back regime. SEBI has released two consultation papers, on April 02, 2026 and May, 08, 2026 proposing to re-introduce open market buy-back of shares through stock exchanges.

Buyback through the SE route would usually be preferred for the ease of compliances and flexibility available with the listed entity. The process is rather simple and cost-effective, as compared to the lengthy process of tender offer or reverse book-building.

Reasons for phasing out this method in 2023?

Historically, buy-back through the stock exchange route was one of the recognized modes under the regulations, which was subsequently phased out pursuant to the 2023 amendments and discontinued w.e.f April 01, 2025. Reasons involved:

- Tax inequalities: Under the old taxation system companies were required to pay the buy-back tax under Section 115QA of the Income tax Act, 1961. Shareholders participating in the buy-back were not under any obligation to pay any tax on capital gains. This resulted in the shareholders availing a tax-free exit, while effectively, such tax burden was put on the remaining shareholders, through taxing the company that bought back the shares.

- Inequitable shareholder participation: The price-time order matching system meant that only a few shareholders could end up selling their entire shareholding by participating in the buy back, while others despite willingness may be excluded, making the process chance-based rather than offering equitable participation.

- Artificial demand: In addition to the issues of participation inequality and tax inequalities, the lengthy time frame of buy-back via the stock market route also generated fears of price manipulation as well as price distortions since continuous purchase by the company would have an impact on the market prices over time.

Reverting back to the SE route: what changed?

The primary rationale for bringing back buybacks through SE route is on account of the tax inefficiencies being resolved pursuant to the Finance Act, 2026. The taxation of buy-back proceeds has been rationalised, putting the tax burden on those shareholders whose shares are being bought back.

Additionally, to ensure that there is no misuse of the buyback provisions by the promoters or promoter group members, the new taxation regime imposes additional tax-rates on buyback by such shareholders. See an article on the changes in relation to buy-back taxation.

On the other hand, open-market buyback through the SE route is also recognized for enabling efficient price discovery, improved liquidity, and flexible capital management for companies. Thus, the balance is in favour of enabling buybacks through the SE route again.

Is it a revert or a new framework?

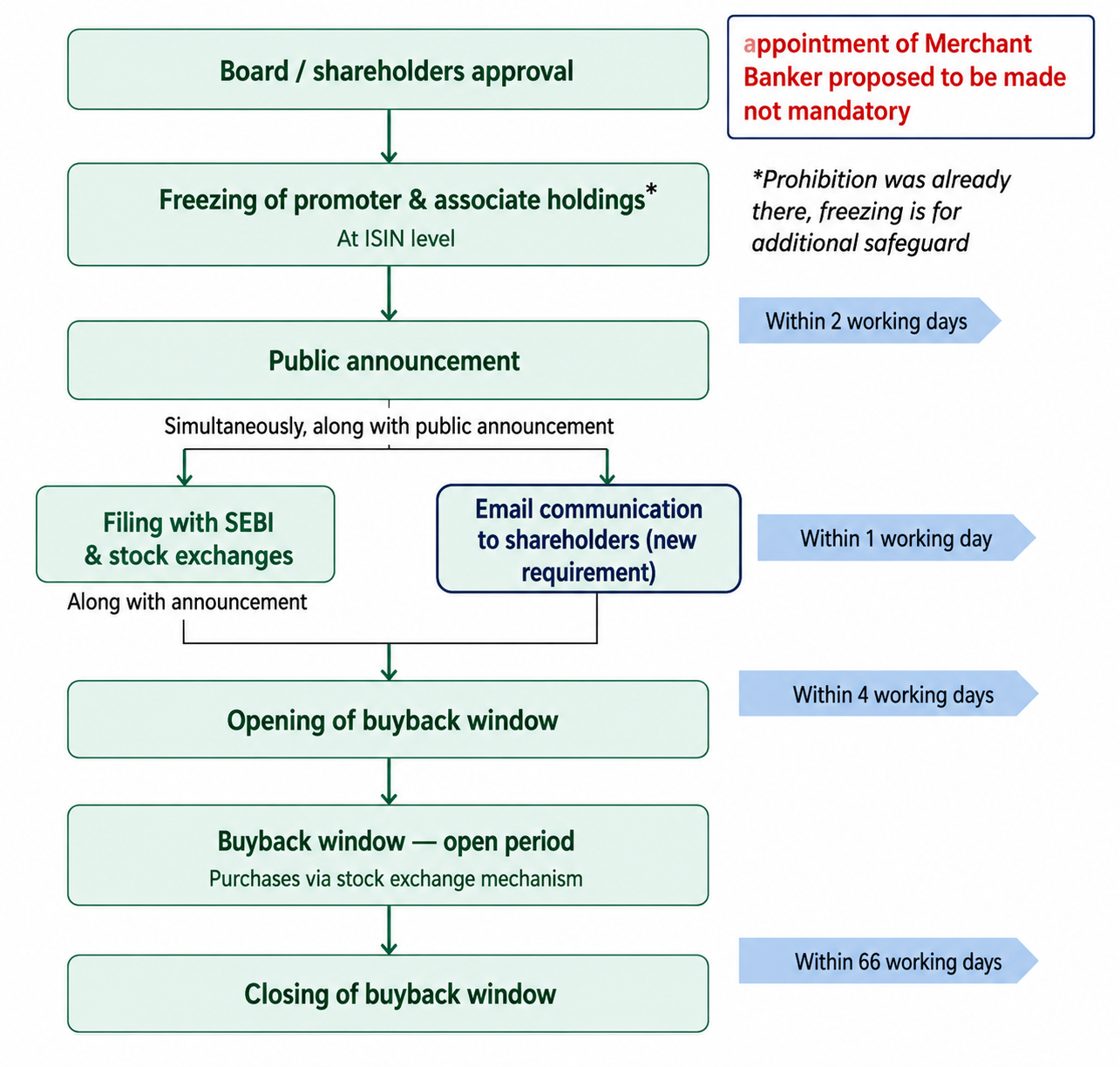

The proposal is neither a “revert”, nor a completely new framework. See figure below for proposed changes in the process of buyback through SE route:

The 8th May CP proposes certain modifications to the erstwhile provisions of the Buyback Regulations for ease of doing business and further strengthening the buyback framework, as tabulated below:

| Provision | Extant requirements | Proposed changes | Remarks |

| Public announcement (Reg. 16(iv)(b) | Newspaper publication within 2 working days of board/postal ballot resolution;also placed on the website of SE, merchant banker and company | Additional mandatory electronic intimation (including email communication) to shareholders as on the date of public announcement, within one working day from the date of such public announcement. | To ensure due information to shareholders in a timely manner. |

| Duration (Reg. 17(ii)) | 6 months – prior to 2023 amendment Reduced to 66 and thereafter 22 working days pursuant to 2023 amendments | 66 working days | To ensure timely execution while providing adequate flexibility to the issuers |

| Separate Trading Window (Explanation to reg. 16) | Through a separate trading window provided by the stock exchange. | To be done under the normal trading window | A separate trading window is not required in view of the uniformity in tax treatment. Accordingly, this is not required. |

| Disclosure of Company Identity in Buy-back Orders (Reg. 17) | The company’s identity as purchaser was required to be displayed on the electronic screen at the time of placing the order. | NA |

Proposals applicable to all forms of buyback

While the CP is primarily focussed on bringing back SE mechanism for buybacks, some proposals have been made for amendments in the existing regulations w.r.t. all forms of buyback:

| Provision | Extant requirements | Proposed changes | Remarks |

| Prohibition on trading by promoters and associates (Reg. 24(i)(e) | From buyback approval till offer closure – prohibition on promoters and their associates, including inter-se transfers | Promoters’ shareholding to remain frozen at an ISIN level during the buy-back period, Exception: for tendering shares in a tender offer buy-back | Freezing of PAN at an ISIN level provides an additional safeguard against use of buyback by promoters for market manipulation. Tendering of shares during tender offer is permitted, in view of the additional tax-rates imposed on promoters pursuant to the Finance Act. |

| Minimum public shareholding compliance | No explicit provisions | Buyback not to be announced in breach of MPS requirements | This is a clarificatory change; even though the Regulations did not explicitly mention about MPS requirements, the issuer is required to ensure compliance will all applicable laws at all times. |

| Interval between two Buy-Back offers (Reg. 4(vii)) | Lock-in of 1 year from expiry of the buy-back period | Reference to CA, 2013 instead of explicit provisions | The CLAB, 2026 proposes various amendments in relation to the buyback framework; this will ensure alignment between the SEBI Regulations and CA, 2013. See an article here. |

| Appointment of Merchant Banker (“MB”) | Mandatory | Functions of merchant banker to be re-distributed to LE, SEs and Secretarial auditor. | For reducing the procedural and compliance costs |

Our Remarks

Overall, the proposal reflects a shift from prohibition to reinstatement of an earlier permitted mechanism of buyback through the SE route, with additional safeguards to ensure there are no regulatory loopholes. With changes proposed in CA, 2013 under the Corporate Laws Amendment Bill, and a favourable tax regime pursuant to the Finance Act, 2026, this seems to be an opportune time to revisit and revise the buyback framework applicable to the listed entities.

The rebirth of buyback through SE mechanism is expected to provide companies with greater flexibility in structuring buy-backs, while also ensuring a more equitable framework for shareholder participation and taxation outcomes. The proposal, therefore, seeks to strike a balanced approach between market efficiency and fairness, addressing past issues without dispensing with the benefits of the mechanism.

FAQs on Type-I NBFC Registration Exemption

– Anita Baid, Dayita Kanodia & Chirag Agarwal | finserv@vinodkothari.com

Loading…

Loading…

Repossessed, Revalued, Regulated: RBI’s framework for treatment of repossessed property

-Anita Baid & Dayita Kanodia | finserv@vinodkothari.com

RBI, on May 5, 2026, came out with the draft directions on Specified Non-financial Assets (SNFA). These directions have been introduced with the intent of specifying the treatment of non-financial and non-banking assets, particularly immovable property, acquired by the lender in satisfaction of their claims on the borrower.

It is relevant to note that a common framework has been introduced for banks and NBFC, which is in contradiction to the recent consolidation approach adopted by the Department of Regulations. This could possibly also create confusion as to the treatment of non-banking assets relevant for banks, being referred to under the common framework, to be also made applicable on NBFC. In case of banks, the Banking Regulations Act prohibits banks from holding such non-banking assets (NBAs) beyond a period of 7 years, except for property acquired for own use.

Key Highlights of the Proposal:

Our comments on the key proposals have been provided below:

- SNFA would include those immovable assets which are acquired by a RE in satisfaction or part satisfaction of its claims on the borrower along with the non-banking assets as per Section 9 of the BR Act.

VKC comment: This would mean that movable property, like vehicles, equipment, is not being covered under the purview of these regulations. Further, the restriction on banks as provided under the BR Act to acquire any immovable assets other than assets put to its own use should not apply to NBFCs.

- The SNFA can only be acquired by the RE concerned when

- The RE’s exposure to a borrower is classified as non-performing, and

- Where other means of recovery have been explored and deemed unviable.

VKC comment: This could be practically challenging since in certain adverse situations (like fraud classification) the RE may not want to wait for the asset to turn into an NPA before repossession is done. However, practically, evaluation and classification as fraud would easily take 90 days.

Further, the fact that all other means of recovery has been explored and deemed unviable would be very subjective to establish.

- Acquisition will result in proportionate extinguishment of the exposure in lieu of which the SNFA is being acquired. Any part extinguishment of claims by the RE concerned would be deemed as restructuring

VKC comment: It is understood that any compromise settlement of the dues would be done as per the extant regulations for banks and NBFCs (as the case may be) and the amount outstanding post such settlement shall be considered to determine the remaining claims, if any.

- Upon acquisition, the SNFA shall be recorded in the balance sheet at the lower of-

- The NBV of the extinguished exposure or

- The distress sale value of the SNFA arrived at by at least two independent external valuers.

At each subsequent reporting date, the SNFA shall be carried on the balance sheet at the lower of the last available distress sale value, or the revised NBV (value of extinguished exposure, net of the notional provisions applicable had the exposure continued on the books of the RE).

VKC Comment: The accounting treatment of the SNFA should have been governed as per the provisions of the accounting standards (para 3.2.23 of Ind AS 109). There could be a possible conflict since the accounting standards require the asset to be recognised on fair value.

- Post-acquisition, the SNFA will be revalued at least once every two years on a distress sale basis. The reasons for failure to dispose of the asset earlier shall also be recorded. Valuation gains should be ignored and any diminution in value should be recognised in profit and loss statement immediately.

- Any accrued interest or charges with respect to the exposure shall not be recognised till the SNFA is actually disposed off and such interest or charges are received by the RE.

VKC Comment: This is consistent with the IRAC provisions which requires the RE to shift from accrual accounting to cash basis accounting upon the asset turning into an NPA.

- Any expense/income incurred for the SNFA should be recognised in the P/L account for the year in which the same is incurred/earned.

- Disposal of such SNFA shall be by way of a public auction following the SARFAESI procedures

VKC Comment: SARFAESI is applicable to NBFCs having an asset size of more than 100 crore and where the outstanding amount is a minimum of ₹20 L. Accordingly, in some cases, SARFAESI may not be applicable at all. In such cases, following SARFAESI procedures should ideally not be made mandatory.

- SNFA cannot be sold back to the borrower or its RPs (as defined under the IBC, 2016)

VKC Comments: Even under IBC, 29A bars the borrower and its connected persons from bidding on the repossessed assets (except for certain exemptions in case of MSME borrowers).

- In case of failure to dispose the SNFA within earlier of:

- 7 years from the date of acquisition or

- The carrying value becoming zero

the asset shall be deemed to have been employed for its own use by the RE and will be recorded as a fixed asset.

VKC Comments: It seems unclear if the RE concerned can put the assets to its own use immediately on the acquisition of such assets.

- Specific disclosure to be made as a part of the financial statements as per the format prescribed by RBI.

Also, read our article,

Repricing of ESOPs on account of market price crash

Abhishek Kumar Namdev, Assistant Manager | corplaw@vinodkothari.com

Background

The basic intent of any company to bring out an ESOP Scheme is to incentivize its employees. Such incentives are basically in the nature of appreciation in the prices of shares. To explain this by way of an illustration, the following may be considered:

Grant price/ Exercise Price at the time of grant – INR 200 per share

Vesting – 1 year from date of grant

Market price at the time of exercise = INR 280 per share

Incentive / gain – INR (280 – 200) = INR 80 per share

This simply means that the usual expectation of any company is that the profits will increase because of which the share prices will also shoot up. In such a scenario, if instead of an increase in the share prices, the same falls so sharply that it even falls below the exercise price, there is no motivation or reason for any employee to exercise their vested options as it has no relevance from being economically beneficial. Those employees holding “underwater options” find no incentive to exercise the same.

Therefore, the next logical question is: Can the exercise price be decreased? Such adjustment is generally termed as repricing of ESOPs. In this write up, we have discussed the legal permissibility of repricing the options and the different scenarios in which the same can be given effect to.

Does Indian law permit repricing?

The answer is yes, and it finds regulatory support under the SEBI (Share Based Employee Benefits and Sweat Equity) Regulations, 2021 (“SBEB Regulations”).

Regulation 7(5) of the SBEB Regulations states that the price of options that have not been exercised may be changed irrespective of whether they have been vested or unvested if the option is rendered unattractive due to a fall in the price of shares in the market. Having said that, such repricing should not be detrimental to the interest of employees and will be subject to shareholder approval.The trigger is specific, a fall in market price rendering the option unattractive.

Also, the conditions are clear, such repricing should not be prejudicial to the interest of employees, and secondly, shareholders must approve it by way of a special resolution. Given the scenario where the market price has fallen, the repricing will be done downward so as to make the options attractive again.

For pricing of the ESOPs, following provisions become particularly relevant:

Indian law prescribes specific guidelines for the determination and disclosure of the exercise price. The relevant provisions are discussed below.

- Determination of Pricing of ESOPs: The SBEB Regulations provide the responsibility for determining exercise price solely to the compensation committee (NRC), with the sole condition that the committee shall follow the relevant accounting policies. Moreover, Regulation 17 does not mandate any minimum floor or prescribe any formula for setting the exercise price.

However, SBEB Regulations do provide a benchmark for listed companies to follow while determining the exercise price. More specifically, regulation 2(1)(x) read with regulation 2(1)(hh)(i) indicate that for listed entities, the benchmark for the purpose of determining exercise price would be the latest closing price at a recognized stock exchange, where the higher trading volume in the shares of the Company is recorded, on the date prior to the date on which the compensation committee considers granting of ESOP.

What practices do listed entities typically adopt in structuring their ESOP schemes?

While most ESOP schemes provide that the exercise price shall be determined by the compensation committee at the time of grant, the manner in which such discretion is exercised varies across entities. In practice, a few broad approaches were observed which have been discussed below.

The most common approach, particularly among listed companies, is to set the exercise price at exactly the market price as defined under Regulation 2(1)(x), that is to say, the closing price on the exchange with higher trading volume on the day preceding the grant date, with no discount applied. An example of this approach is set out in one of a company’s grant disclosures.

The second approach is where the ESOPs are granted at a discount to market price, with the discount range varying widely. An example of such an approach is reflected in an ESOP scheme that permits pricing at a discount of up to 50% to the closing market price on the stock exchange with higher trading volume.

The third approach is setting the exercise price at face value. While uncommon among established listed companies, has been adopted by several new-age, recently-listed companies. This practice is largely a carry-forward of pre-IPO ESOP structures where options were originally granted before listing, at a time when face value was the only viable pricing anchor.

A Company, in its Scheme, fixed the exercise price at Rs. 1 per option, equal to the face value of its equity share. Similarly, another Company, across itsseveral Schemes, consistently grants options at an exercise price of Rs. 1 per share which is equal to face value even as the market price at the time of grant has ranged about Rs. 230 per share, making the spread between exercise price and market price substantial.

Another practice found is to obtain prior shareholder approval for granting options within a specified discount range, for instance at 20–25% on the last closing price before the day of grant and granting the authority to fix the actual discount to either the Board / Committee within the approved range.

- Section 62(1)(b) read with Rule 12 of the Companies (Share Capital and Debentures) Rules, 2014 requires every company to make certain disclosures in the explanatory statement annexed to the notice for passing the special resolution, including disclosure with respect to the exercise price or the formula for determining the same.

Why not just cancel and regrant?

Can some companies prefer the option of cancelling the existing options and issue fresh ones at the current market price? This looks cleaner apparently but technically two problems.

First, under Ind AS 102, cancellation during the vesting period other than on account of cancellation due to forfeiture for non fulfilment of vesting conditions, is treated as accelerated vesting. As a result, all unrecognised compensation cost gets recognised immediately, hitting the P&L upfront. Second, a fresh grant resets the vesting clock, meaning the minimum one-year vesting period under Regulation 18 of the SBEB Regulations starts afresh. Employees may end up waiting longer than they originally required.

Global scenarios

In US, listed companies are required to follow ‘The Nasdaq Stock Market LLC Rules’1, which requires every company to take the shareholders’ approval unless the original plan expressly permits repricing. The SEC treats exchange programmes where employees voluntarily swap underwater options for new ones as the company gives a tender offer, triggering Schedule to filing requirements. The market-accepted approach has evolved toward “value-for-value” exchanges, where employees receive fewer new options calibrated to the fair value of the surrendered ones, limiting dilution and accounting impact.

The Singapore Mainboard Rules mandate that the scheme itself provide for adjustments to the subscription or option price. Consequently, adjustments implemented strictly in accordance with the scheme may not necessitate separate shareholder approval. That being said, such adjustments are subject to an important safeguard, namely, that participants must be placed in a position economically equivalent to that of shareholders, thereby preventing any undue advantage. However, where the adjustment pertains to the option price, the manner in which such adjustments can ensure economic equivalence with shareholders remains a question.

The Toronto Stock Exchange (‘TSX’) through its Policy on Security Based Compensation requires a shareholder approval of any repricing of options if the participant is an Insider of the issuer, regardless of the terms of the plan. If a company’s option plan contains amendment provisions approved by shareholders that permit repricing of outstanding options held by non-insiders, then the TSX will not require shareholder approval for the repricing of such options.

The common principle across jurisdictions is shareholder primacy & full transparency.

Need for Shareholder’s approval for repricing

One of the major tasks before the Company is to approach the shareholders for repricing the options. However, the first question that comes to mind is can there be a situation where repricing can be done without the approval of the shareholders. Ordinarily, repricing requires the nod from the members, but such cases would be where the members fixed the grant price under the scheme. Where the authority to fix the grant price has been bestowed upon the NRC / Board, then any changes in the same should also be ideally decided by them. For example, the Scheme defines that the exercise price shall be at a discount of up to 25% or Rs. 20 (discount in terms of the percentage or absolute number) on the closing market price prior to the date of grant, in this case the NRC / Board should be having the power to determine the exercise price without have a recourse to shareholders as long as the fixation as well as repricing conditions align with the legislation as well as shareholders approval originally granted. Alternatively, the Scheme may provide that the exercise price shall be such price as may be determined by the NRC at the time of each grant, in accordance with the applicable provisions of the SBEB Regulations, 2021. Governance concern

The governance concern with repricing is straightforward. Shareholders who bought shares at the market price have no mechanism to reprice their investment when prices fall. Extending a repricing benefit to employees, particularly those in senior management, without strong justification may create an asymmetry that institutional investors and proxy advisors may become reluctant to accept. However, on the other hand, it is important to accept that it is these very employees that put in their efforts to push up the performance as well as share prices. It might also be imperative to note that where the market prices decline on account of external factors or global factors, repricing becomes all the more significant.

Among listed companies, there have been a few companies which sought shareholder’s approval for repricing There is no SEBI informal guidance on repricing, a gap that itself reflects how underexplored this area remains.

Conclusion

Where the shareholders have not accorded the power to the NRC /Board to reprice the ESOPs, it is legally required for the companies to take the approval route under the SBEB Regulations but comes with clear conditions, which include:

- NRC rationale on record;

- shareholder approval by special resolution;

- no dip below face value;

- accounting impact; and

- Corresponding disclosures where the exercise price was earlier disclosed.

See our other resources on ESOPs

- https://vinodkothari.com/2025/06/esops-for-founders-well-intended-relief-garbled-by-language/

- https://vinodkothari.com/2022/04/esops-as-part-of-managerial-remuneration/

- https://vinodkothari.com/2023/09/stock-options-entail-multi-stage-disclosure-to-stock-exchanges/

- Rule 5635(c) of the Nasdaq Stock Market LLC Rules ↩︎