Existing companies may apply within 6 months of 1st July; new companies may avoid registration on satisfying Type 1 and asset size conditions

The RBI’s relief to exempt pure investment companies from exemption from regulation, is now in final shape. We have earlier commented on the draft Amendment Directions. The final amendments in Directions, notified on 29th April, 2026, accept some of the public feedback. However, the condition that the NBFC seeking exemption should not have any debt on the liability, nor any debt on the asset side, even if from/to group entities, remains.

The exemption window opens on 1st July, based on asset size, no customer interface, no public funds and some other conditions (discussed below). The window remains till 31st Dec., 2026; however, even in future, it will be open for NBFCs to opt to exit from registration.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-04-29 18:53:102026-04-29 19:04:48Option to exit: Type 1 NBFCs get continuing deregistration option

Additionally, upfront fair valuation may also deplete retained earnings

The new ECL framework marks a major regulatory shift for India’s banking sector; it has been long overdue, and therefore, there was no case that the RBI could have deferred it further; pleadings to defer the implementation were rejected by the regulator. It comes coupled with regulatory floors for provisions, which would cause a major increase in provisioning requirements over the earlier requirements. Our assessment, on a very conservative basis, is that the first hit to Bank P/Ls will be at least Rs 60000 crores in the aggregate.

This is in addition to fair valuation requirement on upfront adoption, as on 1st April, 2027. While a vaguely worded part in para 19 was inserted on suggestions of the stakeholders, if interest rates have moved up since the date of the original loan, there will be almost a sure case of upfront valuation loss, which will eat up retained earnings.

RBI had come up with a draft framework on ECL pursuant to the Statement on Developmental and Regulatory Policies, wherein it indicated its intention to replace the extant framework based on incurred loss with an ECL approach. The final regulations were notified on 26th April and are applicable w.e.f 1.04.2027 i.e., for FY 27-28. The manner of implementation will be that all loans as on 1st April 2027 will be fair valued, and all new loans/financial instruments originated or acquired on or after 1st April 2027 will be subject to ECL provisions. See the highlights of the final regulations here.

A major impact that the directions will have on the Banking sector is the need to maintain increased provisioning pursuant to a shift from an incurred loss framework to the ECL framework. Under the earlier framework, banks made provisions only after a loss has incurred, i.e., when loans actually turn non-performing. The newECL model, however, requires banks to anticipate potential credit losses and set aside provisions for such anticipated losses.

Banks presently classify an asset as SMA1 when it hits 30 DPD, and SMA2 when it turns 60. Both these, however, are standard assets, which currently call for 0.4% provision. Under ECL norms, both these will be treated as Stage 2 assets, which calls for a lifetime probability of loss, with a regulatory floor of 5%. Thus, the differential provision here becomes 4.6%.

Once an asset turns NPA, the present regulatory requirement is a 15% provision; the ECL framework puts these assets under Stage 3, where the regulatory minimum provision, depending on the collateral and ageing, may range from 25% to 100%. Our Table below gives a more granular comparison.

Type of asset

Asset classification

Existing requirement

New requirement w.e.f 1.04.2027

Difference

Farm Credit, Loan to Small and Micro Enterprises

SMA 0

0.25%

0.25%

–

SMA 1

0.25%

5%

4.75%

SMA 2

0.25%

5%

4.75%

NPA

15%

25%-100% based on Vintage

10%-85% based on Vintage

Commercial real estate loans

SMA 0

1%

Construction Phase -1.25%

Operational Phase – 1%

Construction Phase -0.25%

Operational Phase – Nil

SMA 1

1%

Construction Phase -1.8125%

Operational Phase – 1.5625%

Construction Phase -0.8125%

Operational Phase – 0.5625%

SMA 2

1%

Construction Phase -1.8125%

Operational Phase – 1.5625%

Construction Phase -0.8125%

Operational Phase – 0.5625%

NPA

15%

25%-100% based on Vintage

10%-85% based on Vintage

Secured retail loans, Corporate Loan, Loan to Medium Enterprises

SMA 0

0.4%

0.4%

–

SMA 1

0.4%

5% (0.4% for loans against FD, NSC, LIC and KVP)

(2.5% for direct exposures to/guaranteed by State Governments)

4.6%

No change for loans against FD, NSC, LIC and KVP

SMA 2

0.4%

5%(0.4% for loans against FD, NSC, LIC and KVP)

(2.5% for direct exposures to/guaranteed by State Governments)

4.6%

No change for loans against FD, NSC, LIC and KVP

NPA

15%

25%-100% based on Vintage

10%-100% for loans against FD, NSC, LIC and KVP and for direct exposures to/guaranteed by State Government)

10%-85% based on Vintage

Exposures under various schemes of Credit Guarantee Fund Trust for Micro andSmall Enterprises (CGTMSE), Credit Risk Guarantee Fund Trust for Low IncomeHousing (CRGFTLIH) and National Credit Guarantee Trustee Company Ltd (NCGTC)

SMA 0

0.4%

0.25%

0.15%

SMA 1

0.4%

0.25%

0.15%

SMA 2

0.4%

0.25%

0.15%

NPA

No provision for the guaranteed portion.

NPA provisioning as per extant guidelines for the portion outstanding in excess of the guarantee

(Only when the Governmentrepudiates its guarantee when invoked)

10%-100% based on vintage for secured and guaranteed portion

25%-100% based on vintage for unsecured and unguaranteed portion

(Only if the claims are not settled with ninety datesfrom the due date of the loan)

Home Loans

SMA 0

0.25%

0.25%

0.15%

SMA 1

0.25%

1.5%

1.25%

SMA 2

0.25%

1.5%

1.25%

NPA

15%

10%-100% based on Vintage

(-)5% – 85% based on Vintage

LAP

SMA 0

0.4%

0.4%

–

SMA 1

0.4%

1.5%

1.1%

SMA 2

0.4%

1.5%

1.1%

NPA

15%

10%-100% based on Vintage

(-)5% – 85% based on Vintage

Unsecured Retail loan

SMA 0

0.4%

1%

0.6%

SMA 1

0.4%

5%

4.6%

SMA 2

0.4%

5%

4.6%

NPA

25%

25%-100% based on Vintage

0%-75% based on Vintage

The actual impact of such additional provisioning will be a hit of more than 3% to the profit of banks. Based on the RBI Financial Stability Report of FY 24-25, the current level of SMA and NPA is estimated to be ₹3,78,000 crores (2%) and ₹4,28,000 crores (2.3%), respectively. Accordingly, an additional provision of approximately ₹ 18,000 crores (4.6% of SMA volume) and ₹ 42,000 crores (10% of NPA volume) will be required for SMA and NPA respectively, leading to a total impact of at least ₹60,000 crores. This estimate has been arrived at by considering the % of NPAs and SMA-1 & SMA-2 portfolios of banks. The actual impact may be higher, as lot of loans may be unsecured, and may have ageing exceeding 1 year, in which case the differential provision may be higher.

It may be noted that while the draft directions allow Banks to add back the excess ECL provisioning to the CET 1 capital, it does not neutralize the immediate profitability impact, as the additional provisions would still flow through the profit and loss account.

How do we expect banks to smoothen this hit that may affect the FY 27-28 P/L statements? We hold the view that it will be prudent for banks, who have system capabilities, to estimate their ECL differential, and create an additional provision in FY 25-26, or do technical write-offs.

Effective Interest Rate requirement applies to all loans effective 1st April, 2027

ECL does not come alone; it comes along with the Ind AS 109 companion – the requirement to compute effective interest rate (EIR) for all financial assets and financial instruments. How does EIR requirement differ from the existing rate of interest/internal rate of return approach? Because EIR has the impact of amortising loan acquisition costs or upfront fees. Currently, banks could have taken the upfront earnings such as processing or origination fees/costs directly to revenue – these will now have to part of the EIR computation. More than impacting the profit number, EIR creates a significant impact on loan management systems, as it results in dual computations – the accounting balances and the customer LMS balances are likely to be different.

Upfront recognition of fair value changes

Para 19 requires that on 1st April, 2027, that is, the date of first adoption, all financial assets and instruments will be fair valued, and the fair value changes (gains or losses) will be adjusted against retained earnings. This is consistent with the principles of first time adoption of Ind AS.

On stakeholder representation, the RBI added this part to Para 19:

Where facts and circumstances indicate that the transaction has been undertaken on terms such that the fair value of the financial asset is not materially different from its carrying cost, the same shall be presumed to be the best evidence of fair value.

What does this imply? If the terms of the financial facility have remained the same, does it mean no fair valuation has to be done? Surely no, at least in our opinion. Any fair value change in fixed rate instruments happens for two reasons: change in credit spreads (rating changes, credit quality changes, etc), or change in rate of interest. If there is a facility extended, say at a rate of interest of 8%, whereas the prevailing rate of interest for a borrower of similar credit standing has moved up to 10%, will there be a fair value decrease? Surely yes.

There are lots of loans which were extended during Covid or periods of low interest rates, which are still continuing. In all such cases, fair value losses are imminent.

The meaning of the para above can only be that if the terms of the original facility are similar to what they would currently be, then the fair value will not have to be computed.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-04-28 11:28:182026-04-28 13:54:58A[U]n Expected Injury: ECL is here, likely to hurt bank profits and retained earnings in FY28

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-04-27 16:22:522026-06-12 16:12:57Virtual Certificate Course on Grooming of Chief Compliance Officers of NBFCs

Simrat Singh and Jeel Ranavat | Finserv@vinodkothari.com

The RBI has proposed an overhaul of the existing prepaid payment instruments (PPI) framework through its draft Master Direction, 2026. The changes aim to, inter-alia, simplify classification, tighten cash usage, restrict cross border payments etc. In this note, we discuss some of the key proposals of the draft master directions.

Simpler classification

Two overarching categories are proposed:

General Purpose PPI: Comprising Full-KYC PPI and Small PPI (single type, no further sub-types);

Special Purpose PPI: comprising Gift PPI, Transit PPI, PPI for Foreign Nationals/NRIs (UPI One World) and any other with prior RBI approval. PPI-MTS renamed into Transit PPI

Credit card loading restricted

With a view to curb ‘loan-loaded PPIs’, it is proposed that credit cards can now be used only for Special Purpose PPIs, while General Purpose PPIs are limited to bank account debit, cash or another PPI. This signals a clear intent to ring-fence credit-backed spending to specific use cases. See our resource around loan loaded PPIs here.

Statutory auditor certification for net worth compliance

The draft introduces a procedural clarification by requiring non-bank PPI applicants to submit a certificate from their statutory auditor confirming compliance with the minimum net worth criteria of ₹5 Crores. While the threshold itself remains unchanged, earlier a CA certificate was required; the draft now specifically mandates certification by the statutory auditor in a prescribed format..

Sharp cut in cash usage

Cash usage sees the biggest tightening. Cash loading for Full-KYC PPIs is reduced from ₹50,000 to ₹10,000 per month, pushing higher-value transactions towards bank-linked digital modes. The move appears designed to curb anonymity and improve traceability.

P2P transfers also curtailed

Peer-to-peer transfer (i.e. transfer to another person’s bank account or PPI) limits have been standardised. Instead of differentiated limits based on beneficiary registration, a flat cap of ₹25,000 per month is now proposed.

Monthly usage cap formalised

While earlier regulations relied on outstanding balance caps, the draft introduces an explicit ₹2 lakh monthly debit limit for Full-KYC PPIs. In substance, this aligns with the existing ceiling but adds clarity on usage.

Banks get faster go-live

Banks issuing PPIs will no longer require prior approval if they are already qualified to issue debit cards. A prior intimation to RBI will be sufficient, allowing faster product launches. This acknowledges that regulated banks already meet baseline prudential standards.

This significantly reduces time-to-market and reflects regulatory reliance on the existing prudential and compliance standards applicable to banks. The change is expected to enhance agility, support faster product innovation, and strengthen banks’ participation in the digital payments ecosystem.

Non-bank approvals streamlined

For non-bank issuers, the process is simplified with perpetual authorisation and removal of the explicit in-principle approval stage. The timeline for submission post-regulatory NOC is also relaxed to 45 days from the earlier requirement of 30 days. The draft is silent on the earlier requirement of submitting a System Audit Report (SAR) at the time of authorisation. However, an IS Audit report is proposed to be submitted annually by the issuer.

Core portion interest computation shifts to monthly basis

The draft revises the methodology for computing interest on the core portion by moving from a fortnightly to a monthly calculation framework. Instead of averaging 26 lowest fortnightly balances, issuers will now compute the average of 12 lowest monthly outstanding balances, with the minimum one-year operational requirement continuing. This change appears to be a pragmatic step towards operational simplification, reducing computational intensity while aligning the framework with more conventional monthly cycles. While the earlier explicit restriction on availing loans against such deposits is not reiterated, the fiduciary nature of PPI funds implies that pledging or leveraging customer balances would, in our view, remain impermissible.

Foreign wallet norms liberalised; A push for UPI One World

In contrast to tightening elsewhere, the framework for foreign users is expanded. The UPI One World wallet will now be available to all foreign nationals and NRIs, with a higher ₹5 lakh monthly usage limit.

This step is aimed at making UPI more accessible to international users, especially inbound travellers who often face challenges in using domestic payment systems. By enabling seamless, wallet-based access to UPI, the framework improves convenience and enhances the overall payment experience in India.

Cross-border usage removed

A key change is the blanket removal of cross-border transaction capability for PPIs. Earlier, AD-1 bank issued PPIs could be used for limited overseas transactions. The draft eliminates this entirely, narrowing the scope of PPIs.

Other notable changes

Closed system PPIs continue to remain outside regulation but marketplaces are explicitly excluded from claiming this status. The definition of “merchant” has been broadened, removing the requirement of contractual acceptance. Small PPIs will now expire after 24 months with mandatory balance transfer in case the same has not been converted into Full-KYC PPI, instead of merely restricting further credits.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-04-23 20:09:352026-04-23 20:13:22RBI’s Draft PPI Norms: Stricter Cash Rules, Simplified Categories, No Cross Border Payments and More

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-04-23 12:06:022026-04-27 17:08:03Workshop on Financial Sector Entities: RBI Related Party Lending Restrictions and Related Party Transactions under Listing Regulations /Companies Act

MCA, with the objective of simplifying the incorporation process and enhancing ease of doing business, has issued a public notice dated April 08, 2026, proposing amendments to the Companies (Incorporation) Rules 2014 (“Incorporation Rules”), and inviting public comments on the same. The proposed amendments, inter alia, aim to rationalise and merge multiple forms, reduce documentation requirements, introduce greater flexibility in incorporation and post-incorporation compliances, enable digital modes of communication, and streamline approval processes, thereby providing an overall boost to ease of doing business.

A comparative summary of the existing requirements and the changes proposed is provided below:

Particular

Existing provision/requirements

Changes proposed

Merging of Existing Forms for change of name, shifting of RO, Conversion and approvals

Multiple forms are required for different actions- For change of name and registered office INC-4 (Change in member/nominee by OPC) INC-22 (Change in RO within local jurisdiction)INC-23 (Shifting of RO from one State to another)INC-24 (For change of company’s name) For conversions / approvals / orders: INC-6 (Conversion of OPC)INC-12 (Section 8 licence application)INC-18 (Conversion of Section 8 company)INC-20 (Surrender/revocation of Section 8 licence)INC-27 (Conversion between public/private company)RD-1 (Application to Regional Director) INC-28 (Filing of Court/Tribunal orders)

To reduce multiplicity of filings and repetitive disclosures, the draft draft proposes consolidation of several incorporation-related forms into two simplified e-forms-“E-CHNG” – one single form for changes in registered office and name“E-CON”– one single form for conversions, approvals and orders)

Withdrawal of Reserved name

Rule 9A provides for filing of application before Registrar vide SPICE+ for reservation of name at the time of incorporation and RUN at the time of change of name

A proviso to Rule 9A is proposed to be inserted thereby providing flexibility for withdrawal of reserved names permitted before filing of main incorporation forms or name change application.

Conversion of Section 8 Company

Existing provisions do not allow conversion of a Section 8 company limited by guarantee to a Section 8 company limited by shares.

Rule 39 is proposed to be amended to allow conversion of section 8 company limited by guarantee to a Section 8 company limited by shares

Liability of Deceased Subscriber

Currently, there is no specific provision addressing liability where a subscriber dies before paying for shares at incorporation

New Rule 23B proposed to be inserted thereby providing clarity that in such cases (other than OPCs), the legal representative shall be liable to pay the unpaid amount. Upon payment, the legal representative will assume the rights of the subscriber as if originally subscribed.

Shifting of Registered office

Proof of existence of registered office – Acceptable Documents

Currently, under Rule 25, limited set of documents are accepted as a proof of existence of RO-Ownership proof (registered title document in company’s name)Notarised lease/rent agreement with recent rent receipt (≤ 1 month)Owner’s authorisation/NOC with ownership proofUtility bill (telephone, gas, electricity, etc.) in owner’s name (≤ 2 months)

Rule 25 is proposed to be substituted so that-Clearly cover different scenarios – owned, leased/rented, co-working spaces, and SEZ unitsExpand list of acceptable documents such as title deed, property tax receipt, municipal records (khata), allotment/possession letters, payment receipts, and recent utility billsProvide clarity on requirement of authorisation letter in different cases

Shifting of Registered Office during pendency of inquiry investigation

Currently, shifting of registered office is not allowed if any inquiry, inspection or investigation has been initiated against the company or any prosecution is pending against the company under the Act.

Rule 30 (9) is proposed to be revised thereby allowing shifting of the registered office even during pending inquiry, inspection, or investigation, subject to Board undertaking. It also permits shifting in IBC cases where defaults occurred prior to the change in management.

Apart from the key changes discussed above, the draft rules also propose certain additional amendments, including:

For conversion of private limited company into OPC:

requirement of obtaining an affidavit from directors confirming that all the members of the company have given their consent for conversion, to be omitted. [Rule 7(4)(iii)]

Criminal liability specific to OPCs under Rule 7A is proposed to be omitted

Rule 8 that provides guidance for Names which resemble too closely with name of existing company is proposed to be simplified and rule 8A regarding trademark related objections is proposed to be substituted thereby providing more clarity thereto.

List of KYC docs and information required from subscribers at the time of incorporation, as provided in Rule 16, is proposed to be reduced;

Cap on number of directors for whom DIN can be applied at the time of incorporation is proposed to be increased from three to five.

Requirement of separate filing of DIR-12 for first directors is proposed to be omitted.

Copies of public notices to-

the Chief Secretary and Income Tax Department at the time of shifting of RO or conversion,

debenture-holders, creditors, Registrar, SEBI and concerned regulators under various sub-rules. may now be sent via speed post or e-mail, with the registeredpost requirement proposed to be removed

Physical verification of RO is proposed to be made more flexible through insertion of new Rule 25B, allowing the Registrar to conduct such verification via an authorised person, in the presence of two local witnesses, with assistance from local police if required

Overall, the proposed amendments are a positive step towards making the company incorporation process simpler, faster, and more practical. By reducing the number of forms, easing documentation requirements, and allowing more flexibility in procedures, the MCA aims to lower the compliance burden on companies, especially startups and small businesses.

The changes also bring better clarity in areas like registered office documents, liability of subscribers, and shifting of registered office, which will help avoid confusion and practical difficulties.

Currently, the amendments are in draft form only and comments have been invited from stakeholders on the same by 9th May, 2026. Practical difficulty, if any, in implementation, particularly while filing the revised or new e-forms, can be better assessed once the amendments are finalised and the corresponding e-forms are made available.

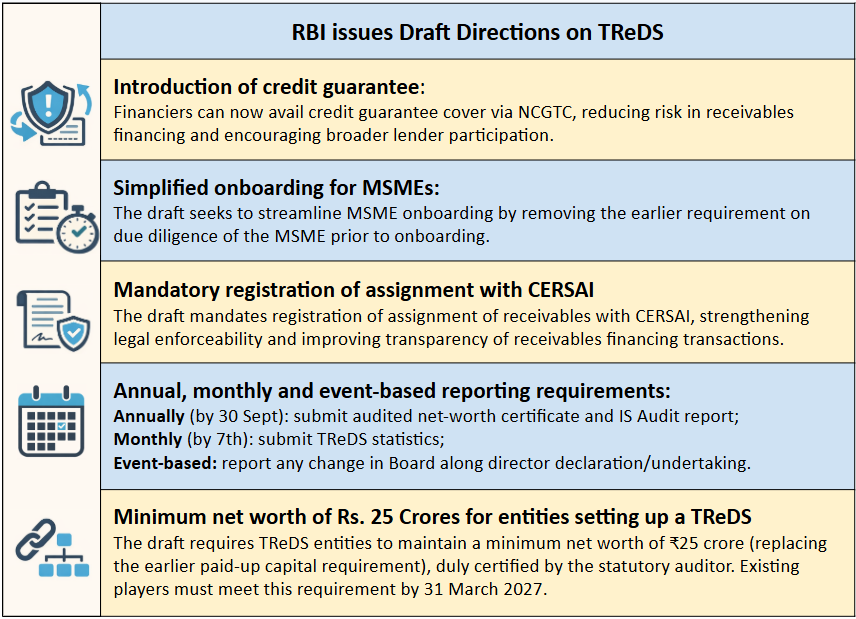

Financiers are now permitted to avail credit guarantee cover (via NCGTC) for exposures on TReDS. This is a significant step towards de-risking receivables financing and encouraging wider participation by lenders. Notably, RBI had already expanded the ecosystem in 2023 by permitting insurers as participants to provide credit insurance cover for such exposures.

🔹 Simplified onboarding for MSMEs:

In line with the Governor’s statement, the draft seeks to streamline MSME onboarding by removing the earlier requirement on due diligence of the MSME prior to onboarding.

🔹 Mandatory registration of assignment with CERSAI:

The draft mandates (earlier recommended) registration of assignment of receivables with CERSAI, strengthening legal enforceability and improving transparency of receivables financing transactions.

🔹Annual, monthly and event-based reporting requirements:

Annually (by 30 Sept): submit audited net-worth certificate and IS/Cyber Security Audit report. Monthly (by 7th): submit TReDS statistics. Event-based: report any change in Board along with director declaration/undertaking.

🔹Minimum net worth of Rs. 25 Crores for entities setting up a TReDS

The draft requires TReDS entities to maintain a minimum net worth of ₹25 crore (replacing the earlier paid-up capital requirement), duly certified by the statutory auditor. Existing players must meet this requirement by 31 March 2027.

RBI continues its drive of regulatory reforms for the banking sector, with the recent one being the amendment proposed in the governance directions applicable to commercial banks i.e. Draft Reserve Bank of India (Commercial Banks – Governance) Amendment Directions, 2026 (Draft Directions) relating to policy and non-policy matters placed before the Board for approval, review, information etc. proposed to be made applicable from September 1, 2026. As indicated in RBI’s Statement on Developmental and Regulatory Policies, RBI has undertaken comprehensive review and rationalization of all earlier instructions in an endeavor to enable Boards to utilize its time effectively, and to facilitate a more focused and qualitative engagement on strategy and risk governance.

While, the Draft Directions provide a compilation of matters to be placed before the Board and those that can be delegated to a specific committee or any committee of board/ management, it also provides the principles to be considered by the board while delegating the matters thereby ensuring the adequate oversight of the board on delegated matters. The amendment would primarily affect the manner in which information is placed before the board of banks, manner and extent of delegation of their powers to committees of board and/or management and reporting requirements for such matters.

The Draft Directions are applicable to both public sector banks and private sector banks.

In this piece, the authors analyse the proposed amendment, impact and indicate the likely actionables for Banks if the amendment is notified as is.

The Role of the Board

The Board of a Bank is expected to majorly focus on overseeing the risk profile of the Bank, monitoring the integrity of its business and control mechanisms, ensuring the expert management, and maximising the interests of its stakeholders. The Board always had the power to delegate certain items to management and board committees, in some cases by way of express provisions in RBI directions, guidelines. But at the same time, it must set and enforce clear lines of responsibility and accountability for itself as well as the senior management.

The Draft Directions draw a clear line between the matters to be dealt by the Board and the matters which can be delegated to committees with only material matters being placed before the Board. Further, a principle based approach is provided for the manner in which information is placed before the Board.

Principle Based Approach for matters to be placed before the Board

The objective of these principles is for the Board to consciously examine the areas where it devotes its valuable time and expertise. The principles require the Board to document express guidelines on the manner in which information is being placed before it.

The board is required to clearly articulate the matters reserved for its approval or to be brought to its notice for information or reporting, based on applicable laws and define the nature, level of detail and frequency of information required from the management. To optimize the time of the Board for real value addition, the chairperson of the Board shall have the primary responsibility of setting the agenda of the meeting.

The matters being placed before it or the Board committees, sub-committees or senior management must be reviewed periodically. This would enable the Board to examine and revoke delegation or further delegate responsibilities wherever required. The review must be detailed enough to include the timelines for circulation of agenda items, adequacy of information captured in the agenda, time allotted for important matters, etc.

The Powers of Delegation

The RBI (Commercial Banks – Governance) Directions, 2025 (existing Directions) provide for delegation of specific items viz. reviews dealing with various performance areas, monitoring of the exposures (both credit and investment) of the bank, review of the adequacy of the risk management process and upgradation thereof, internal control system, ensuring compliance with the statutory / regulatory framework, etc. to a Committee of Board. For ease of reference, the Draft Directions compile as well as draw a clear line between the matters to be dealt by the Board and the matters which can be delegated to committees with only material matters being placed before the Board.

This distinction would enable the Board to focus on its key areas of responsibility – risk and strategy governance and strengthens its powers of oversight over the risk management system, exposures to related entities and conformity with corporate governance standards[1].

Policy Matters

A list of policies which must be placed before the Board for its approval and which may be delegated for review are prescribed in Appendix-I of the Draft Directions. The Board is responsible for approving the policies at the time of framing and only periodical review is to be delegated to the committees. In case of any ‘material amendments’ (to be defined by the Board), the Board’s approval must be sought. Thus, the Board does not lose complete oversight.

Along with a major consolidating exercise, the Draft Directions also indicate policies where delegation is expressly allowed, even where the underlying directions/ guidelines did not expressly provide for the same. Accordingly, the amendments are enabling in nature in certain cases, as illustrated below:

Where the bank intends to function as a Professional Clearing Member in commodity derivatives, policy for-Specification of risk control measures and prudential norms for exposure limits for each trading member;Governing the bank’s exposure to trading members, ensuring consistency with the overall risk appetite and regulatory requirements.

Policy on- Courses / certifications required for specialised areas of operationsList of sensitive positions to be covered under mandatory leave requirements

Any Committee to which powers have been delegated by the Board.

Matters other than policy

Matters other than policies which must be placed before the Board for its approval, review or information are given in Appendix-II of Draft Directions. While several matters must be mandatorily taken up by the Board, the Board shall have the discretion to delegate certain matters even where the underlying directions/ guidelines did not expressly provide for the same. Accordingly, the amendments are enabling in nature in certain cases – for e.g. matters relating to risk assessment methodology for RBIA, Annual Audit Plan, analysis of incidents of operational risk failures & their impact to audit committee, matters relating to investment portfolio to risk management committee.

The Draft Directions also provide for discontinuation of about 6 matters at the discretion of the Board. In certain cases, such as ATM transactions including failed transactions and penalties paid, certain details are to be placed before the Board. The details must be forwarded to RBI along with the Board’s observations. The Draft Directions proposes that such review may be discontinued at the discretion of the Board. Accordingly, amendments would be required in the underlying laws as well. Similarly in case of matters relating to loans to stockbrokers and market makers where the provisions mandate half-yearly review of the aggregate portfolio, its quality and performance by the Board, the board will have to exercise its discretion depending on the extent of exposure.

Proposed Omissions

Certain provisions of the existing Directions proposed to be omitted are as follows:

Para

Provision deals with

VKC Remarks

14

The Board should focus on the 7 themes of: Business Strategy, Risk, Financial Reports and their integrity, Compliance, Customer Protection, Financial Inclusion, Human Resources

Instead of specifying the themes, the proposed amendment indicates that the ultimate responsibility for the bank’s performance, conduct and control rests with the Board and that it needs to ensure that sufficient time is dedicated to strategy and risk governance.

16

Review of action taken on points arising from earlier meetings till the satisfaction of the board

Broader discretion provided to Banks to decide internal processes and articulate matters requiring its approval or to be brought for reporting or noting of information.

17

Placing regulatory communication from RBI and the government along with supplementary information before the Board

18

Delegation expressly permitted for: Reviews dealing with various performance areas and only a summary on each of the reviews may be put up to the Board at periodic intervals; Monitoring of the exposures (both credit and investment) of the bank; Review of the adequacy of the risk management process and upgradation thereof; Internal control system; Ensuring compliance with the statutory / regulatory framework, etc.

A prescriptive list of permitted delegation has been specified by RBI, refer discussion below.

19

Procedural technicalities relating to placing a summary of key observations by directors at the next board meeting and confirmation by directors for their observations, dissents etc.

Broader discretion provided to Banks to decide internal processes.

Conclusion

The Draft Directions propose to optimise the time of the Board of Banks to focus on strategic and governance matters instead of operational matters. While this measure aims to boost the productivity of Banks and bring ease of doing business in the short term, once notified, several actionables would arise for Banks. Banks must examine their current decision making structure, at the level of the Board and delegation to committees, to understand how they would align it with the proposed amendments.

[1] Para 15 of the existing directions retained as para 11A of the Draft Directions.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-04-15 15:11:112026-04-15 15:19:42Delegation of powers by Board made prescriptive yet principle based